Which are the SMEs you are looking at Sekhar Bhai.

Have you looked at Emmforce Autotech Ltd by any chance.

This looks very interesting and away from limelight at this moment!

Discl: Biased and invested.

1

1

151

Jun 13

Then we have some fundamentally good stocks but not in momentum at all like nisus, afcom, tbi corn n emmforce. Anindita is also good but not crossing 1200 levels

3

254

Jun 13

Tac, afcom nisus emmforce....all have disappointed on price action front. Freshara n Prizor just saved the portfolio. Prizor is 5 times from my buying now. Sold some last week. Have faith in all 4 which disappointed. Reduce some qty in tac, afcom for other opportunity.

2

7

1,030

Jun 10

Map my India has started moving. We continue to believe this as 2x opportunity from our recom levels.

Sheela foam story has just started. Amazing turnaround by management.

Raymond life style is consolidation play . Stock cannot be neglected at 5x Ev / Ebidta.

Surya Roshni can be dark horse for the year.

Sudarshan Chem, Market share gained in pigment space from 3 pc to 15 pc.

HeG green can be 2x of current HEG market cap. Should not be missed. Core business should do very well.

Emmforce is an interesting play for mini portfolio. this can be really big. They won an order from largest auto company for 9 years supply.

Entering into Defence.

Emil : Multiple drivers and attractive valuation. Can this be next Fine organic?

Talk to our team for more details

Good Risk reward in infra names.

We are positive on Reliance, HDFC bank, TCS, Hul, Col pal , Infy, ITC , Icici pru, Shriram, Sbi , Ambuja Cem, Shree Cem

Abhishek Jain

Arihant Capital

17

43

288

29,678

Jun 8

CII Himachal Pradesh delegation, led by Chairman, Mr Sanjay Suri, Chairman, CII Himachal Pradesh, and Wholetime Director, Morepen Laboratories Limited India, and Mr Ashok Mehta (Emmforce-Emmbros), Vice Chairman, CII Himachal Pradesh, and Managing Director, EmmForce Autotech, called on key leaders of the Government of Himachal Pradesh including Shri Harshwardhan Chauhan, Hon’ble Minister for Industries, Labour & Employment; Shri Kamlesh Kumar Pant, Chief Secretary; Shri R D Nazeem, Additional Chief Secretary (Industries & Transport); Dr Yunus, Commissioner Industries, State Excise & Taxation; and Ms Deepika Khatri, Joint Director Industries.

The delegation deliberated on critical industry issues such as extension of the Industrial Policy, expediting pending approvals, ensuring competitive power tariffs, streamlining Fire and PCB NOCs, addressing transport union challenges, resolving HIMUDA-related concerns in Parwanoo, and strengthening power infrastructure across industrial areas.

The interaction reflects CII’s continued commitment to enabling a progressive, responsive, and industry-friendly ecosystem in Himachal Pradesh through constructive policy advocacy and collaboration.

#CII4NR #IndustryInteraction #CIIHimachalPradesh #IndustrialPolicy

1

184

Some of the interesting SME's -

Kalyani Cast tech

Sunlite Recycling

Neetu Yoshi

Emmforce

Cryogenic Ogs

May be, i will write in detail going forward.

1

2

494

Jun 1

Record Sales, Record Profit के बाद क्या?

#sumitmehrotra #emmforce

Watch Complete Poscast 👇👇

youtu.be/EEfO_MzXUJ4?si=s73v…

2

37

4,327

May 28

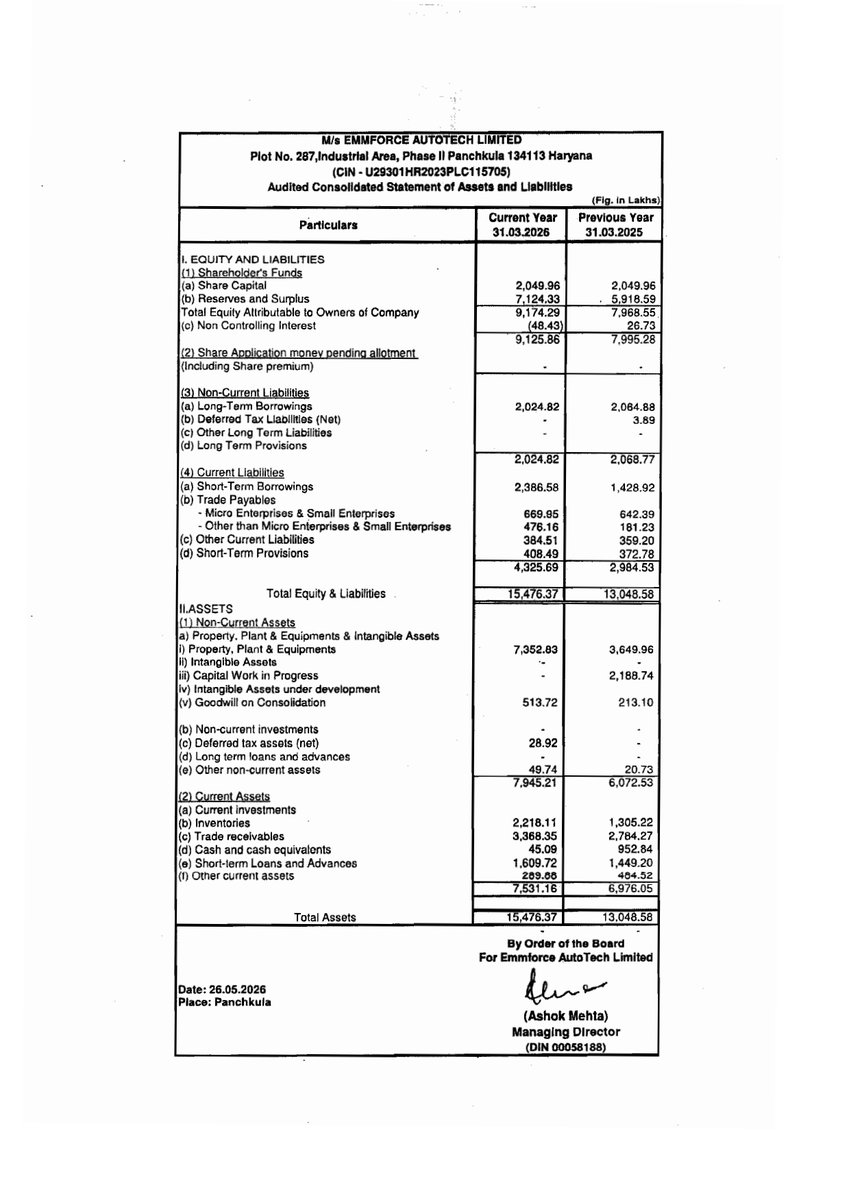

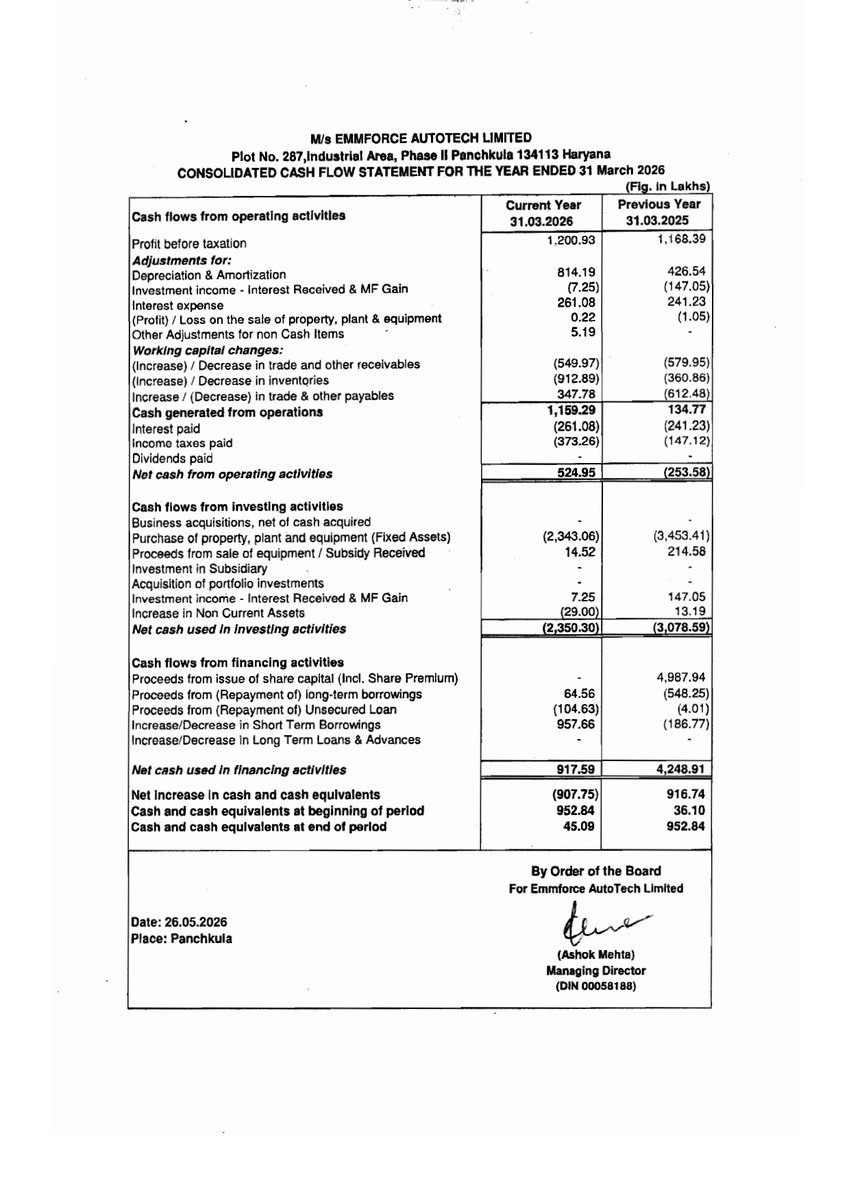

Emmforce Autotech Ltd Concall Summary for Q4FY26

MANAGEMENT COMMENTARY

• FY26 marked defining operational year

• Capacity expansion completed ahead strategically

• Manufacturing ecosystem strengthened significantly

• Backward integration focus accelerating steadily

• Execution phase now actively underway

OUTLOOK

• FY27 revenue target around ₹195 Cr

• FY28 revenue target near ₹240 Cr

• EBITDA margin guidance maintained 20-22%

• PAT margins guided near 10%

• Export order execution starting FY27

INDUSTRY

• China Plus One trend strengthening

• India gaining global supplier preference

• Freight costs increased moderately recently

• Currency depreciation supporting exports partially

• US inventory rationalization currently ongoing

COMPETITIVE POSITION

• Strong niche drivetrain positioning maintained

• Integrated manufacturing platform differentiating business

• Precision engineering capabilities driving stickiness

• Focus remains high-margin opportunities only

• Faster turnaround improving customer retention

RISKS

• Working capital cycle remains elevated

• Export transit cycles impacting liquidity

• Global slowdown risks remain monitorable

• Higher depreciation impacted recent PAT

• Manpower additions pressured short-term margins

GROWTH DRIVERS

• EMSPL subsidiary achieved turnaround quickly

• R&D investments maintained consistently

• Hydraulic gear pumps launched successfully

• OEM contribution expected rising steadily

• Agri business scaling aggressively now

PRODUCT MIX

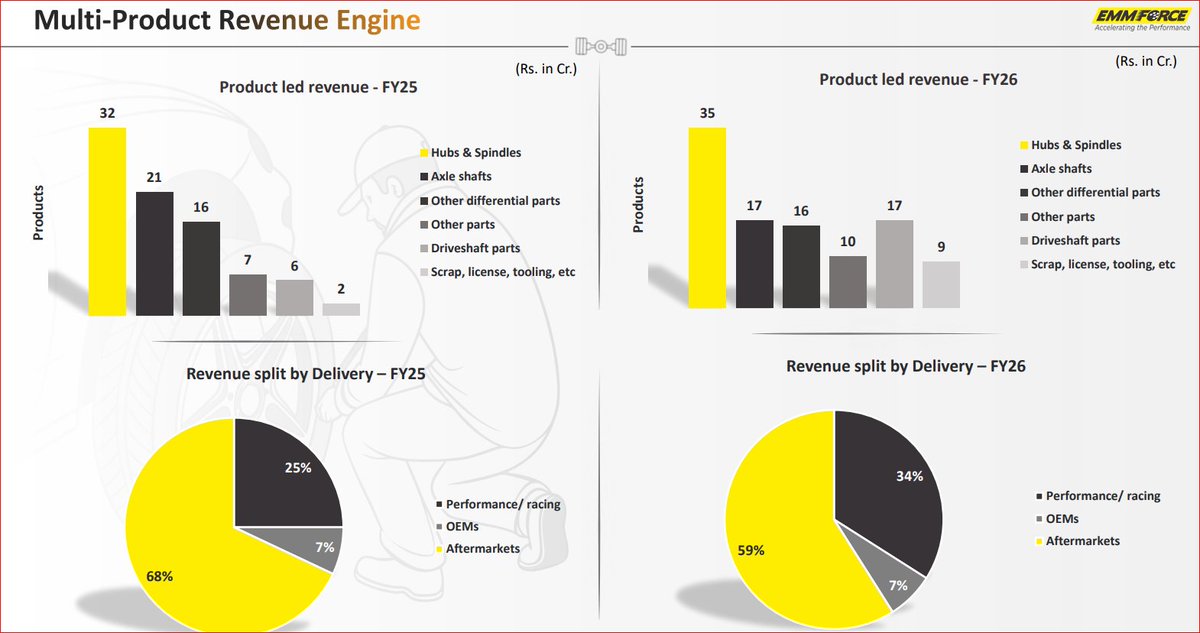

• Automotive remains dominant revenue segment

• Agri contribution increasing rapidly

• OEM mix targeted near 60%

• Drivetrain components remain core focus

• Existing capacity significantly underutilized currently

FINANCIALS

• FY26 revenue reached ₹113 Cr

• EBITDA stood near ₹23 Cr

• EBITDA margin maintained around 20%

• Net Debt/Equity remained comfortable 0.48x

• Asset turnover expected improving sharply

CONCLUSION

• Heavy investment cycle largely completed

• Execution-driven growth phase now starting

• Large export orders improving visibility

• Existing capacity supports future scaling

• Agri expansion remains major catalyst

#Q4results #sharemarket #stockmarket #EmmforceAutotech

1

4

419

72% topline growth guidance is really ambiguous, specially for automotive parts manufacturer like Emmforce. Hope they'll get there.

1

3

911

May 27

EMMFORCE AUTOTECH

FY27 GUIDANCE

REVENUE :190-195 Cr ( 75% )

PAT:18-19 Cr (100% )

1

11

692

May 27

#SME #Emmforce #EmmforceAutotech

Emmforce Autotech H2FY26 Earnings Call Highlights

👉 FY27 & Future Outlook

▫️Revenue guidance for FY27: Automotive business ~₹165 Cr Agri business ~₹30 Cr (total ~₹195 Cr).

💠For FY28, overall revenue targeted at ~₹240 Cr with Agri contributing ~₹50 Cr.

💠Management remains conservative in guidance despite visible growth drivers, expecting actuals to outperform.

▫️EBITDA margins targeted at 20-22% and PAT margins ~10% in FY27, supported by higher utilisation, backward integration benefits (EMSPL forging), and scale efficiencies.

💠Margins expected to improve further as new capacities and agri vertical scale; FY26 EBITDA margin held steady at ~20% despite front-loaded manpower and depreciation costs.

▫️Entering a new phase of scalable growth with newly commissioned capacities, enhanced in-house capabilities, and manufacturing backbone already in place.

💠Operating leverage will drive meaningful margin expansion as utilisation rises (auto currently 50-55%, agri 8-10%).

👉 Current Order Book / Projects and Future Pipeline

▫️Multi-year order book exceeding ₹500 Cr, providing medium-term visibility.

💠Key executed/visible orders include a large US export order (annualised revenue contribution ~₹60 Cr in FY27

💠Commercial production at full run rate from Dec 2025).

💠Another US export order expected to contribute ~₹10 Cr annually.

▫️Long-term drivetrain supply order with annual opportunity of ~₹10.5 Cr – PPAP samples submitted, commercial production expected from Q3 FY27.

💠Hydraulic Gear Pump (strategic core product) successfully launched in FY26 after 5-year R&D

💠Now integrated into portfolio with cross-selling opportunities across automotive, agri, and off-highway platforms.

▫️Agri segment gaining traction:

💠TAFE approvals secured for rotavator blades and parts – commercial sales started, initial share of business ~₹15 lakh/month (potential to grow significantly to 70-80% share)

💠TAFE’s annual blade requirement supports ~₹4 Cr for Emmforce).

💠Distributor network activated in key states (Maharashtra, Karnataka, Madhya Pradesh).

💠Active discussions with additional large OEMs for blades and rotavator contract manufacturing.

👉 Other Notable Points

▫️FY26 performance: Performance remained in line with earlier guidance despite tariff-related headwinds and front-loaded investments.

▫️High export orientation (~94% revenue from overseas markets) with deep-rooted customer relationships (~95% retention).

💠Base business saw temporary softness in FY26 due to customer inventory rationalisation amid tariffs, but US customer visits confirmed demand and order momentum returning to full throttle.

💠Large US order contributed only ~₹5.5-6 Cr in FY26 (mainly March).

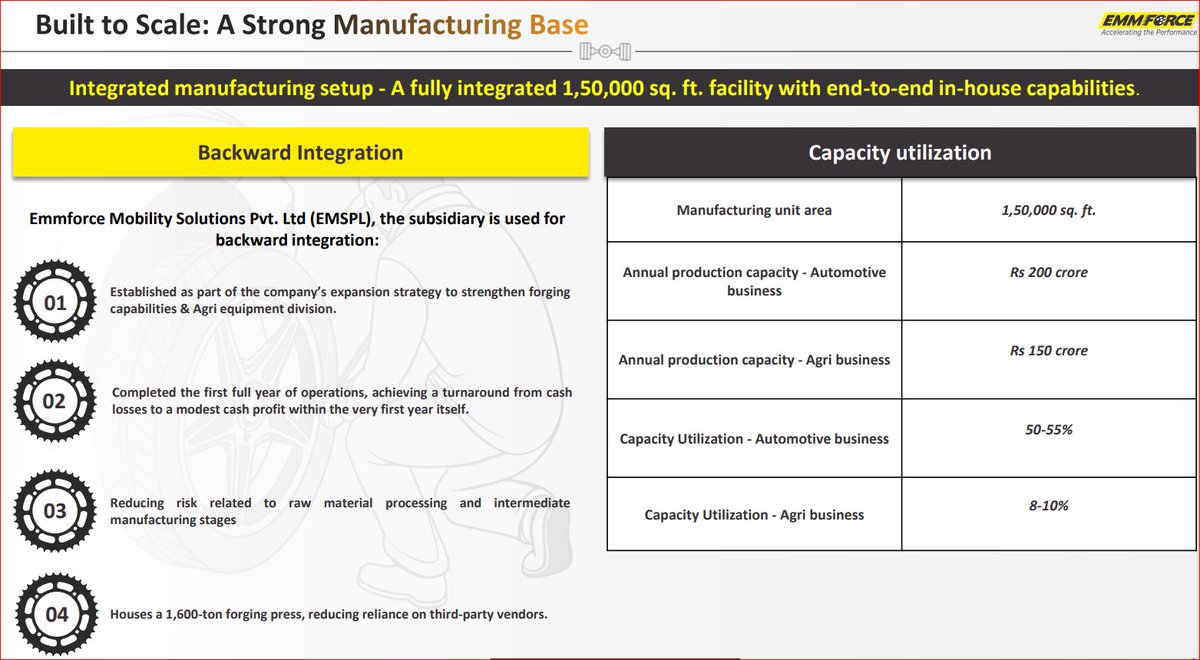

▫️Manufacturing moat: 1.5 lakh sq. ft. vertically integrated facility in Baddi with end-to-end capabilities (design, forging, machining, heat treatment, assembly, testing).

💠Subsidiary (forging agri equipment) completed first full year and turned to modest cash profit.

💠Houses 1,600-ton forging press, reducing vendor dependence. Annual capacity ₹350 Cr (Auto ₹200 Cr Agri ₹150 Cr).

▫️Balance sheet comfortable with net debt-to-equity of 0.48x.

💠Working capital elevated due to new US OEM ramp-up but well-supported by bank limits and export credit facilities (no major funding concerns).

▫️Strategic transition:

💠Moving beyond niche drivetrain components to solution-oriented OEM partner across automotive, agri, and industrial applications.

💠Focus remains on execution, capacity utilisation, OEM mix increase (targeting ~40% OEM in auto), and agri scale-up while maintaining financial discipline.

Mar 26

👉Mainboard stocks often get all the attention but some of the most compelling businesses are hiding in plain sight — on the SME Platform.

👉Smaller. Less covered, though noisy at times. Yet occasionally, genuinely exceptional.

———

👉Introducing SME Gems — a new independent series on Hidden Champions of the SME Platform :

💠 OBSC Perfection

💠 Aimtron Electronics

💠 Yash Highvoltage

💠 CFF Fluid Control

💠 DSM Fresh Foods

💠 L.T. Elevator

💠 Monolithisch India

💠 GSM Foils

👉Across Different Sectors. One common place.

🔗 smeresearch.github.io/SMEGem…

👉Stay tuned for more insights

———

⚠️ For educational purposes only. Not investment advice. Please DYODD.

#SMEGems #SMEPlatform #HiddenChampions #SME

2

2

21

4,425

May 27

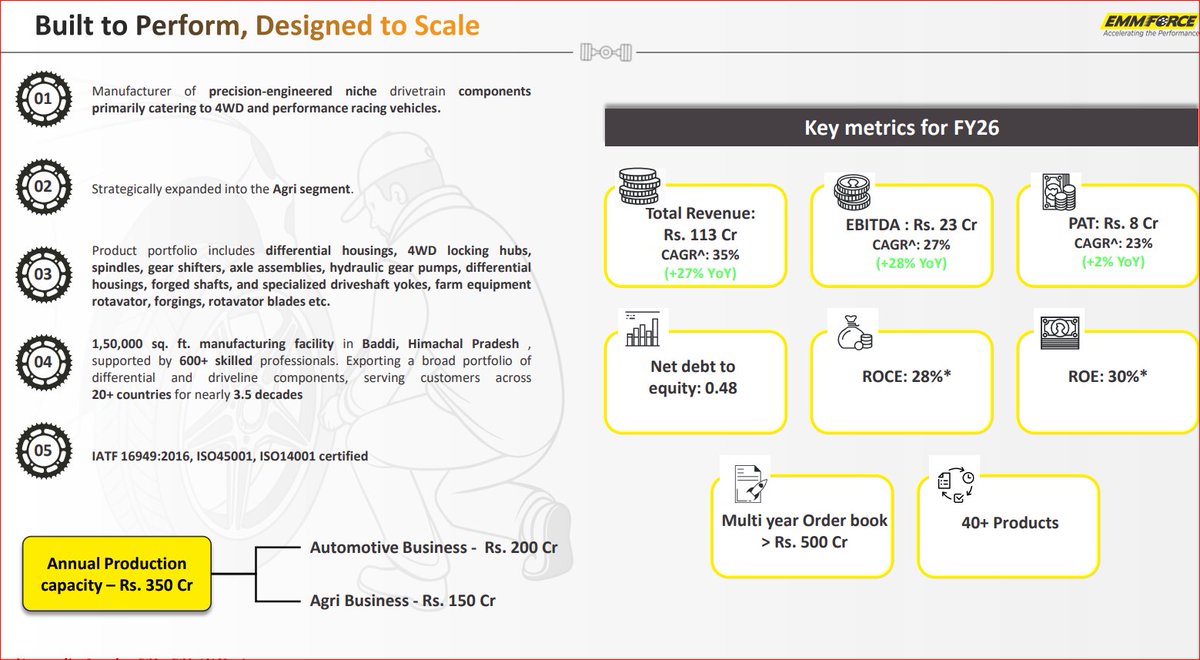

𝗘𝗺𝗺𝗳𝗼𝗿𝗰𝗲 𝗔𝘂𝘁𝗼𝘁𝗲𝗰𝗵 𝗟𝘁𝗱: 𝗙𝗬26 𝗜𝗻𝘃𝗲𝘀𝘁𝗼𝗿 𝗣𝗿𝗲𝘀𝗲𝗻𝘁𝗮𝘁𝗶𝗼𝗻 𝗛𝗶𝗴𝗵𝗹𝗶𝗴𝗵𝘁𝘀 🚀:

Emmforce Autotech Ltd, a specialist in precision-engineered niche drivetrain components, has outlined its strategic roadmap and financial projections for FY26, showcasing a strong growth trajectory.

𝗞𝗲𝘆 𝗙𝗶𝗻𝗮𝗻𝗰𝗶𝗮𝗹 𝗣𝗿𝗼𝗷𝗲𝗰𝘁𝗶𝗼𝗻𝘀 𝗳𝗼𝗿 𝗙𝗬26:

- 𝗧𝗼𝘁𝗮𝗹 𝗥𝗲𝘃𝗲𝗻𝘂𝗲: ₹113 Cr, with a projected 5-year CAGR of 35% & 27% YoY growth.

- 𝗘𝗕𝗜𝗧𝗗𝗔: ₹23 Cr, reflecting a 27% CAGR.

- 𝗣𝗔𝗧: ₹8 Cr, with a 23% CAGR.

- 𝗙𝗶𝗻𝗮𝗻𝗰𝗶𝗮𝗹 𝗛𝗲𝗮𝗹𝘁𝗵:

▸ Net Debt to Equity: 0.48

▸ ROCE: 28% (average of last 5 years from FY22 to FY26)

▸ ROE: 30% (average of last 5 years from FY22 to FY26)

𝗦𝘁𝗿𝗮𝘁𝗲𝗴𝗶𝗰 𝗚𝗿𝗼𝘄𝘁𝗵 𝗗𝗿𝗶𝘃𝗲𝗿𝘀:

- 𝗢𝗿𝗱𝗲𝗿 𝗕𝗼𝗼𝗸: A robust multi-year order book exceeding ₹500 Cr provides significant revenue visibility. 🌟

- 𝗔𝗴𝗿𝗶 𝗦𝗲𝗴𝗺𝗲𝗻𝘁 𝗘𝘅𝗽𝗮𝗻𝘀𝗶𝗼𝗻: Strategic diversification into the Agri segment, with a near-term capacity of ₹150 Cr and long-term annual potential of ₹250 Cr.

- 𝗚𝗹𝗼𝗯𝗮𝗹 𝗥𝗲𝗮𝗰𝗵: Continued export focus, serving customers across 20 countries with a strong emphasis on customer retention (~95%). 🌍

- 𝗣𝗿𝗼𝗱𝘂𝗰𝘁 𝗣𝗼𝗿𝘁𝗳𝗼𝗹𝗶𝗼: Diverse offerings including differential housings, 4WD locking hubs, spindles, gear shifters, axle assemblies, hydraulic gear pumps, and rotavator components.

- 𝗠𝗮𝗻𝘂𝗳𝗮𝗰𝘁𝘂𝗿𝗶𝗻𝗴 𝗣𝗿𝗼𝘄𝗲𝘀𝘀: A 1,50,000 sq. ft. integrated manufacturing facility in Baddi, Himachal Pradesh, with annual production capacity of ₹350 Cr (₹200 Cr Automotive, ₹150 Cr Agri).

- 𝗥&𝗗 𝗙𝗼𝗰𝘂𝘀: Consistent allocation of ~2% of annual revenue to R&D, driving innovation in new products like Hydraulic Gear Pumps and process improvements.

𝗥𝗲𝗰𝗲𝗻𝘁 𝗪𝗶𝗻𝘀 & 𝗙𝘂𝘁𝘂𝗿𝗲 𝗢𝘂𝘁𝗹𝗼𝗼𝗸:

- Secured a ₹470 Cr U.S. export order, already in commercial production, expected to generate ~₹60 Cr annual revenue in FY27. 💰

- New long-term drivetrain supply order worth ₹10.50 Cr annually, with commercial production expected in Q3 FY27.

- TAFE approval for rotavator blades, with commercial sales commenced in Jan 2026.

- 𝗦𝘁𝗿𝗮𝘁𝗲𝗴𝗶𝗰 𝗜𝗻𝘁𝗲𝗻𝘁𝗶𝗼𝗻𝘀: Plans to migrate to the mainboard within a year & potential acquisition of Emmbros Automotives Pvt. Ltd. (related party).

The company's strategy focuses on scaling the Agri division, expanding to Tier-1 OEMs in the US, Europe, and Asia, and simplifying the group structure, aiming for significant growth and value creation.

📊 EMMFORCE AUTOTECH LTD | 🏷️ Investor Presentation

🌐 Details: wegro.app/L5qSXJ

⚡️Instant stock alerts on WhatsApp - Try FREE 👉 wegro.app/go

1

2

164

May 27

Emmforce no. are on expected lines, they told us in the March beginning the numbers would be 115cr.. and landed 112 cr. Let's hear today what they say about fy27.. last time they guided 200 cr

2

169

May 26

SME Investors Interactions

27/05/2026 14:00

K2INFRA - Investor Meet

27/05/2026 16:00

TECHD - Analyst Meet

27/05/2026 11:00

APS - Earnings Call

27/05/2026 14:00

EMMFORCE - Earnings Call

27/05/2026 15:00

MADHUSUDAN - Earnings Call

27/05/2026 15:00

TIPCO - Earnings Call

27/05/2026 16:00

DCCL - Earnings Call

27/05/2026 16:00

ANONDITA - Earnings Call

27/05/2026 16:00

CURRENT - Earnings Call

27/05/2026 16:00

ASARFI - Earnings Call

27/05/2026 16:00

KONSTELEC - Earnings Call

27/05/2026 16:00

NISUS - Earnings Call

27/05/2026 16:30

FINBUD - Earnings Call

27/05/2026 17:00

ARHAM - Earnings Call

27/05/2026 15:00

SHREEREF - Conference

28/05/2026 11:00

SATTVAENGG - Investor Meet

28/05/2026 10:00

ANLON - Earnings Call

28/05/2026 11:30

NEWJAISA - Earnings Call

28/05/2026 16:00

ADMACH - Earnings Call

28/05/2026 16:00

PCL - Earnings Call

29/05/2026 10:00

ZAPPFRESH - Investor Meet

29/05/2026 11:00

SAHASRA - Investor Meet

29/05/2026 15:00

SAHASRA - Investor Meet

29/05/2026 16:00

RIKHAV - Investor Meet

29/05/2026 17:30

GLEN - Investor Meet

29/05/2026 11:30

GGBL - Analyst Meet

29/05/2026 12:45

SSEGL - Earnings Call

29/05/2026 14:00

ZELIO - Earnings Call

29/05/2026 14:00

TEJASCARGO - Earnings Call

29/05/2026 15:00

MCON - Earnings Call

29/05/2026 15:30

TCL - Earnings Call

29/05/2026 16:00

SKP - Earnings Call

29/05/2026 16:00

SKM - Earnings Call

29/05/2026 16:00

VINYAS - Earnings Call

29/05/2026 17:00

BEWLTD - Earnings Call

30/05/2026 15:00

ENVIRO - Earnings Call

30/05/2026 16:30

TECHERA - Earnings Call

01/06/2026 11:00

DIGILOGIC - Investor Meet

01/06/2026 16:00

SELLOWRAP - Investor Meet

01/06/2026 10:30

VOEPL - Earnings Call

01/06/2026 12:00

INFLAME - Earnings Call

01/06/2026 12:00

SACHEEROME - Earnings Call

01/06/2026 13:00

CHANDAN - Earnings Call

01/06/2026 14:00

SHUBHSHREE - Earnings Call

01/06/2026 14:00

CNINFOTECH - Earnings Call

01/06/2026 15:00

RAPPID - Earnings Call

02/06/2026 12:30

BASILIC - Earnings Call

02/06/2026 14:30

SUPREMEPWR - Earnings Call

02/06/2026 15:30

MEGATHERM - Earnings Call

03/06/2026 12:00

VGINFOTECH - Investor Meet

03/06/2026 16:00

METAINFO - Earnings Call

04/06/2026 16:00

KHAZANCHI - Earnings Call

05/06/2026 11:00

DENTALKART - Earnings Call

05/06/2026 12:00

NISMGMT - Earnings Call

05/06/2026 14:00

DELTIC - Earnings Call

6

1,815

May 26

Nilesh's AI is best! It does its work of posting SME results at breakneck speed! @nileshkurhade 👍

But most results, are flat or negative and disappointing. Arrowhead, Crop life, Supreme Facility, Mayasheel, Aritas Vinyl, Identical NO Brains, Systematic, Energy Mission, GEM ENviro, E Factor, Swasth Foodtech (LOSS), Kahan, Emmforce, Shoora, Vivaa etc

2

43

5,407

May 26

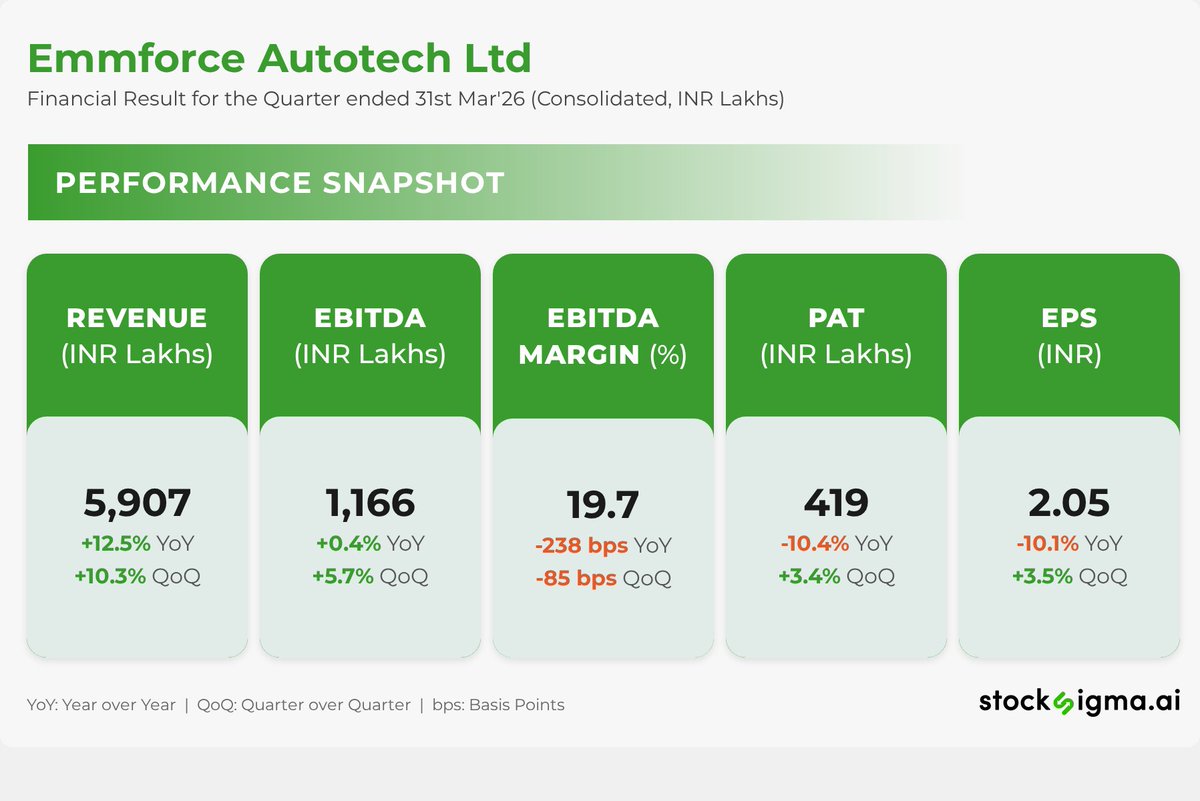

🫱EMMFORCE AUTOTECH FY26 ANNUAL RESULTS. H2FY26 RESULTS. Rs.120 was at 28.3p/e. Now 29.6x👎

MORE OR LESS FLAT H1 & H2. Unable to move EPS and hence valuation also remains FLAT. "Market expect better results, Emmforce!"

H2 FY26 Vs.H1 FY26

REV:Rs. 59Cr Rs. Vs Rs. 54Cr👍

PAT:Rs. 4.2Cr Vs Rs. 4Cr🫱

(May Compare with H2FY25 Rev=Rs. 51Cr & PAT=Rs. 5Cr )

FY26 Vs FY25

REV:Rs. 113Cr Vs Rs. 89Cr👍

PAT:Rs. 8.24Cr Vs Rs. 8Cr🫱

EMMFORCE AUTO SME IPO was in APRIL 2024 at Rs. 98 at 24p/e

May 26

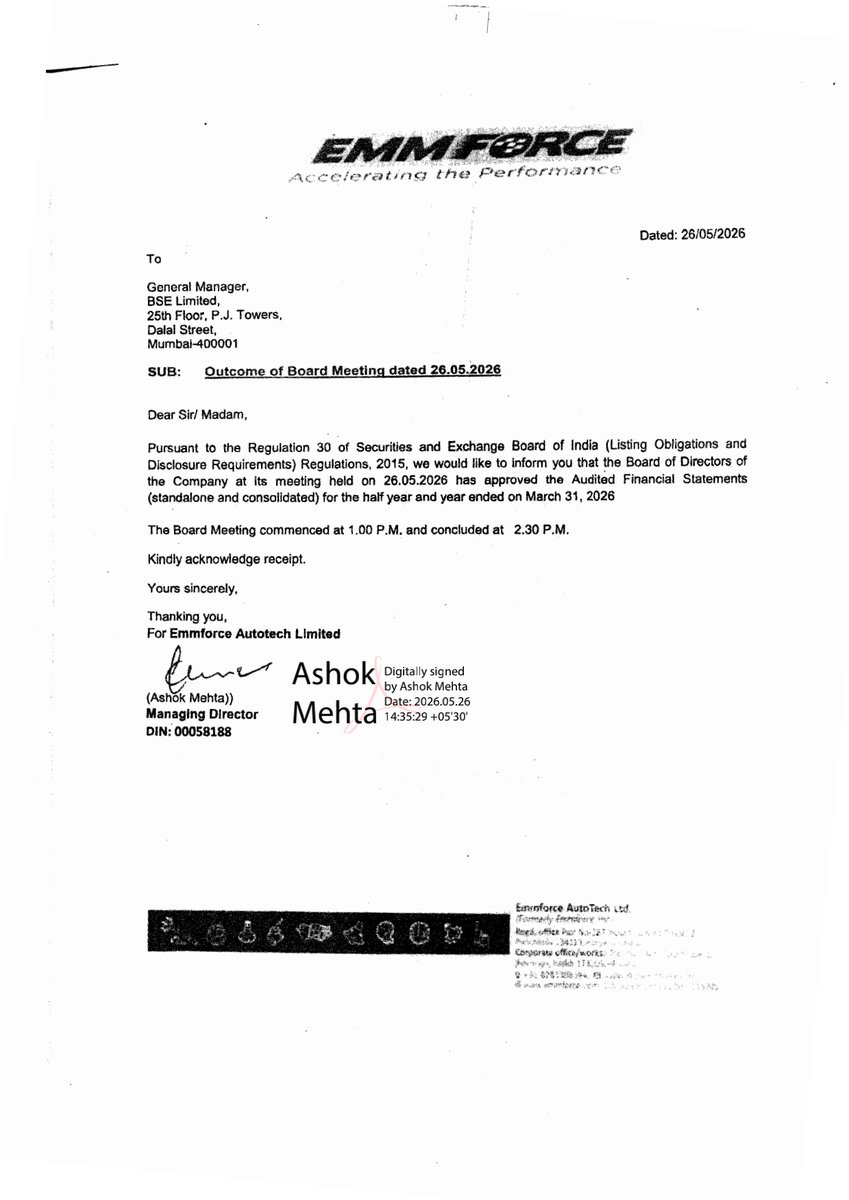

📌 Emmforce Autotech Ltd informed the exchange about its approval for the financial results for the period ended March 31, 2026. #SME #EMMFORCE 📄🧾

3

1

22

4,354

May 26

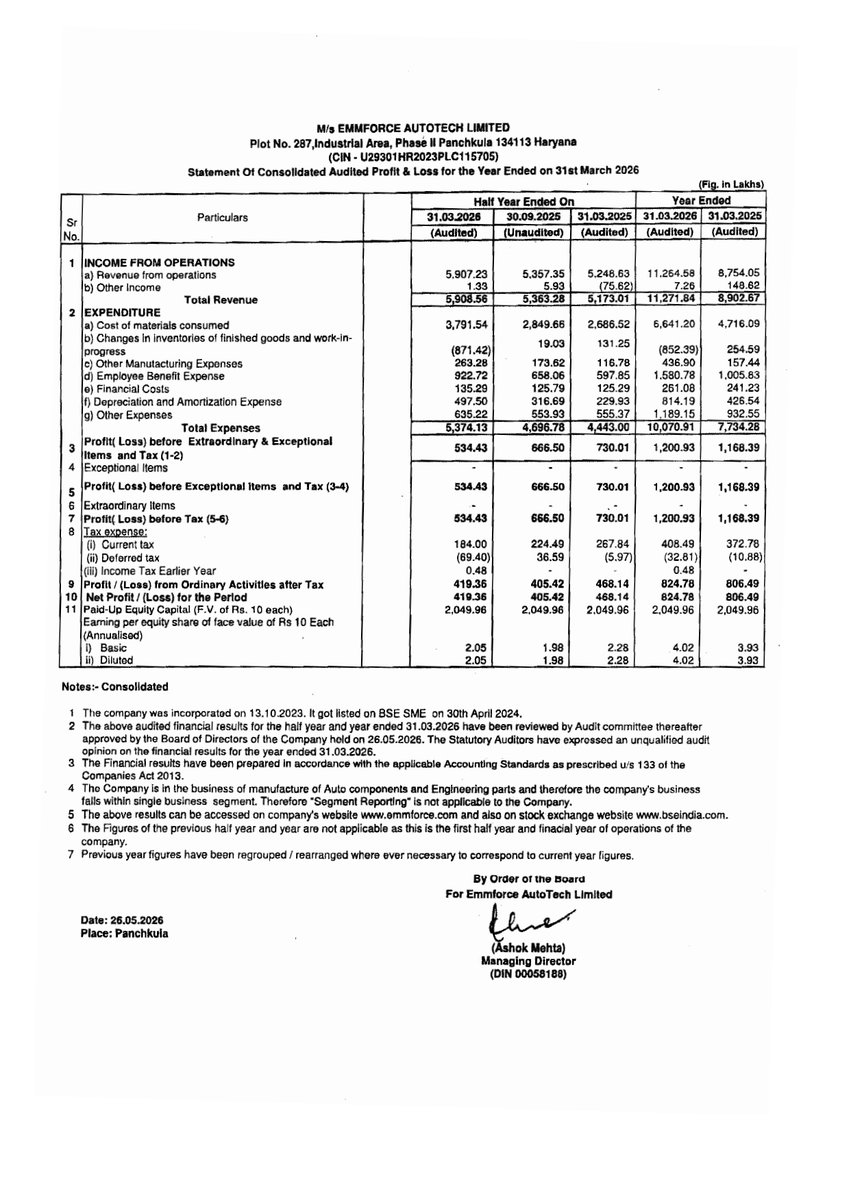

#EMMFORCE

Emmforce Autotech Ltd | Financial Result for the Quarter ended 31st Mar'26 (Consolidated, INR Lakhs) | Disc: AI generated, please verify

2

262

May 26

Result to watch out today in SME.

Nisus

Emmforce

Atmastco

Flysbs

Tipco

Systematic

Hi green

Dentalkart

16

3,008