⌚ Searching for the best fitness tracker? Compare the top wearables for tracking workouts, sleep, heart rate, and daily activity.

flexgearinsights.com/top-fit…

#FitnessTracker #WearableTech #HealthGoals #Smartwatch #FitTech

Jun 12

Busy schedule? No problem. 💼 GymNut AI generates personalized workouts that adapt to YOUR time and equipment. No guesswork, just results. 🚀

Get your custom plan for free! gymnutai.com

#GymNutAI #Fitness #BusyLife #AI #Workout #GymLife #AICoach #FitTech #FitnessApp

2

Jun 11

Day 5: Your trainer in your pocket! 📱 Form checks, meal swaps, or motivation: our AI Coach is here 24/7. Stop guessing and achieve your goals effortlessly! 📈

Try it FREE: gymnutai.com ✨

#GymNutAI #AICoach #FitnessGoals #Workout #GymLife #FitTech #Health #AI #iOSApp

2

Jun 9

🚨 New Feature Update! 🚨 You can now upload IMAGES for your custom exercises! 📸✨

Read the full blog post to learn more about this update!

🔗 cloudfit.tv/au/blog/custom-e…

#CloudFit #GymSoftware #FitnessTech #GymScreens #GymOwners #FitTech #ProductUpdate #CustomWorkouts

4

May 28

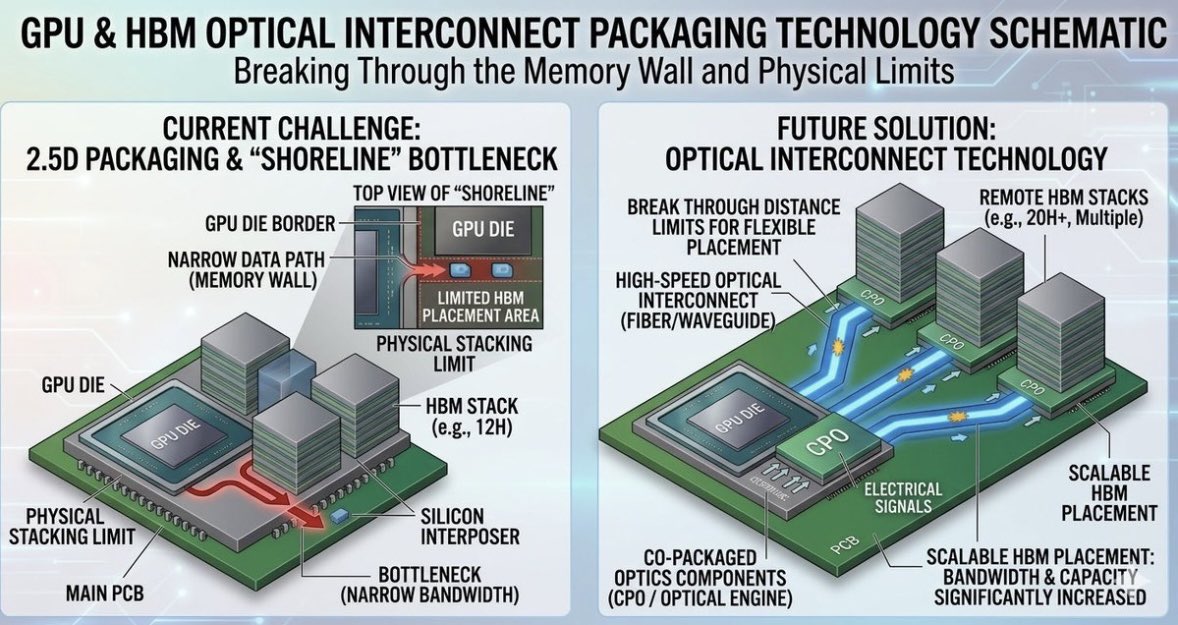

Co-Packaged Optics (CPO) : l’unique issue physique à l’expansion de l’IA

Les ingénieurs mémoire viennent d'admettre que la physique a fini par rattraper l'intelligence artificielle.

Le périmètre physique disponible autour des GPU Nvidia Blackwell, que l'on appelle le "shoreline", est désormais saturé et ne peut plus accueillir de modules de mémoire HBM supplémentaires.

Empiler verticalement de nouvelles couches atteint des limites thermiques et mécaniques critiques, tandis qu'un élargissement latéral est géométriquement impossible sur l'interposeur actuel.

Pour briser ce mur de la mémoire, l'industrie s'apprête à opérer une rupture architecturale majeure en décrochant physiquement la HBM du GPU pour la déporter sur la carte ou au sein du rack.

Cette migration exige de remplacer les liaisons en cuivre par des interconnexions optiques ultra-rapides, miniaturisées au niveau du composant lui-même.

C'est l'acte de naissance massif du Co-Packaged Optics (CPO) à l'échelle du silicium, transformant une technologie de réseau en une nécessité d'architecture interne.

Les flux sous-jacents et les données de la chaîne d'approvisionnement confirment que le marché sous-estime la violence de cette transition industrielle.

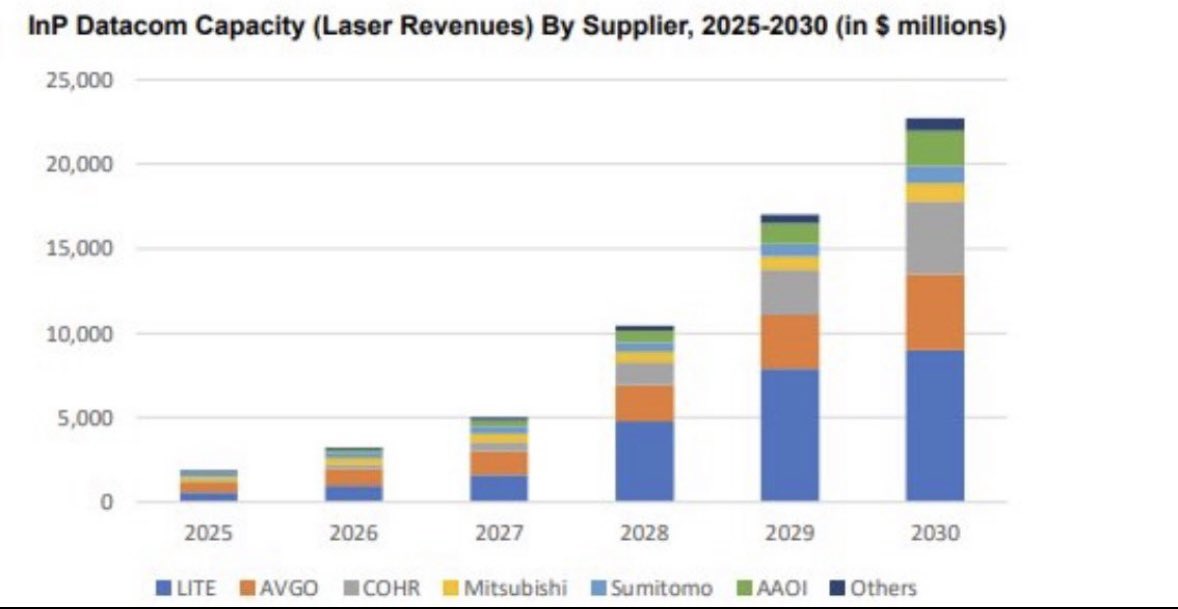

Selon les dernières modélisations de Rosenblatt, Nvidia a exigé de ses fournisseurs une multiplication par 20 des capacités de production de lasers au phosphure d'indium (InP) d'ici 2030.

Contrainte par la réalité des usines, la supply chain n'a pu s'engager que sur une hausse de 12x, garantissant un déficit structurel et un marché "short" pour le reste de la décennie.

Cette asymétrie se matérialise déjà dans les derniers résultats financiers de l'écosystème optique.

Chez Lumentum $LITE , les revenus des lasers à largeur de raie étroite progressent de 120% sur un an, tandis que Coherent $COHR double en urgence ses capacités de production de wafers face à des carnets de commandes pleins jusqu'en 2028.

Le marché actions commence à peine à pricer ce scénario, et la règle d'or de la bourse reste l'anticipation face à une phase de ramp-up industriel calée pour 2027.

Pour exploiter ce narratif, mon sizing se concentre sur l'écosystème taïwanais et les leaders de niche technologique.

FOCI $3363 et Shunsin $6451 capturent la valeur immédiate sur le packaging optique avancé (CPO), tandis que Browave $3163 et Msscorps $6830 interviennent sur les composants de couplage et l'inspection des puces.

Fittech $6706 et $SIVE se positionnent sur les équipements de test laser et l'intégration, indispensables pour garantir les rendements de production.

En amont, $IQE sécurise l'épitaxie des wafers InP nécessaires aux fonderies, alors qu' $AAOI saisit la demande sur les modules de transmission de données.

Enfin, des acteurs comme $LPK, $FORM , $AEHR et Laytec (via $M7U) quadrillent la métrologie, le tri de puces et le test thermique critique pour ces architectures de haute précision.

L'optique n'est plus une simple option d'infrastructure pour interconnecter des serveurs, elle devient le système nerveux interne de chaque supercalculateur.

Le piège est en train de se refermer sur ceux qui ignorent la physique des flux.

Les comptes incontournables pour suivre ces entreprises et cette narrative sont : @Frenchie_ @aleabitoreddit @ParadisLabs @Ren_aramb

1

5

2,377

May 28

▪️ 𝐊𝐀𝐋𝐎𝐑𝐀𝐈

AI Coach is an AI-powered smart nutrition and calorie tracking app designed to help you build healthier eating habits effortlessly.

Simply take a photo of your meal and the app instantly analyzes calories, protein, carbohydrates, and fat values using advanced artificial intelligence.

AI Coach helps you monitor your daily nutrition, manage your calorie goals, and make smarter food decisions every day.

✨ Key Features:

📸 AI-powered food analysis from photos

🔥 Automatic calorie calculation

🥩 Protein, carbohydrate, and fat tracking

💧 Daily water intake tracker

📊 Weekly history and progress insights

🤖 Personalized AI nutrition recommendations

🌍 Multi-language support

⚡ Fast, modern, and premium user experience

AI Coach simplifies complex diet tracking and makes healthy living easier.

Whether your goal is weight loss, staying fit, or improving your nutrition, AI Coach is designed to support your journey every day.

#AICoach #NutritionAI #CalorieTracker #HealthApp #FitnessApp #ArtificialIntelligence #HealthyLifestyle #WeightLossJourney #AIApps #FoodTracking #BetaTesting #EarlyAccess #StartupApp #FitTech #SmartNutrition #MealTracker #HealthyEating #TechStartup #FitnessJourney #AI

2

57

May 25

Companies that pivoted from MicroLED to ride the current wave like Fittech and Ennostar are where I'm investing today personally. The idea being they benefit from sipho/CPO in the next 12mo and retain the microLED call option.

2

1

9

870

May 23

A few people asked me what my hypothetical AI infrastructure portfolio would look like over the next 6 to 12 months

Honestly, probably something like this:

$SIVE $SIVEF 14% - The cleanest AI photonics choke point I’ve found. Every major CPO architecture needs CW lasers, and Sivers is the sole Ayar supplier right now. Jabil basically said demand is uncapped. CHIPS Act exposure and a NASDAQ listing are nice bonuses on top

If they can execute this could be a wild ride

$AXTI 9% - InP substrates are one of those nobody talks about it but everybody needs it parts of the stack. Backlog already above $100M and they’re doubling capacity twice before 2028. Hyperscalers are clearly trying to lock supply early

$AAOI 9% - One of the few real American made 1.6T transceiver stories. They control their own InP lasers internally, 800G is ramping hard, and 1.6T qualification starts in Q3. The datacenter revenue target for 2027 is massive if they execute

$SOI 8% - Upstream pick and shovel for silicon photonics. Every silicon photonics chip starts with these wafers. Direct leverage to Tower’s contracted photonics ramp

$LPK $LPKF 6% - Probably one of the more overlooked names here. They dominate the laser processing side for glass substrates and already have most of the important customer qualifications. Production orders should start hitting later in 2026

$COHR 4% - Fully vertically integrated from substrate to optical device. NVIDIA taking a $2B stake changed the perception completely. 6inch InP progress is ahead of schedule and CPO revenue should start showing up in H2 2026

$TSEM 4% - Open foundry exposure to basically every CPO architecture. $1.3B of contracted photonics revenue for 2027 and most capacity already reserved through 2028 tells you demand is very real

$GLW 4% - The actual fiber layer underneath AI infrastructure. NVIDIA warrant deal, hyperscaler LTAs, and a $10B photonics roadmap by 2030. Not flashy, but critical

Fittech (TPE: 6706) 4% - Smaller Taiwan ecosystem play tied directly into the photonics buildout. Exposure to FOCI and Browave ramps without needing to own the obvious names.

$PENG 4% - One of the more interesting enterprise AI infrastructure names. Exposure to sovereign AI, neoclouds, and enterprise AI factories. Their MemoryAI CXL positioning looks unique right now and NVIDIA has openly recommended them

KRX:000660 SK Hynix 3% - Best HBM company in the world in my opinion. Margins are insane, DRAM pricing is exploding, and they’re basically sitting at the center of the memory bottleneck

KRX:402340 SK Square 2% - Simpler thesis here: discounted exposure to SK Hynix through the holding company structure

FOCI (TWO:3363) 3% - Sole FAU supplier for TSMC COUPE Gen 1 and Gen 2. Mass production starts H2 2026 and even Jabil hinted demand could exceed supply.

NCI (TWO:4092) 3% - Hidden materials choke point. Near monopoly on 7N red phosphorus which feeds directly into InP production. Tiny valuation compared to the scale of demand coming

Nextronics 8147 3% - Goldman confirmed their CPO connectors are already inside NVIDIA’s supply chain. Still very underfollowed for how important the positioning is.

Win Semi 3105 3% - Key manufacturing partner for scaling Sivers’ CW laser production. Mid 2026 qualification could remove a major bottleneck

Shunsin 6451 3% - Foxconn’s CPO packaging arm. Already shipping AI racks directly to NVIDIA and there are rumours Broadcom orders are coming too

$AIXA 2% - Pure-play equipment leverage to InP laser demand. If optical scaling keeps accelerating, they sell the picks and shovels needed to expand production

HB Tech 078150 2% - Optical inspection exposure to the glass substrate story. Supplier into SKC Absolics and benefits if AMD qualification gets finalised

SKC 011790 2% - Glass core substrate exposure. AMD qualification is reportedly in final testing and Phase 2 investment plans are getting serious.

MSSCORPS 6830 2% - One of the weirdest but most interesting names here. They handle optical loss detection for silicon photonics and effectively sit inside the CPO yield process.

$ALRIB 1% - MBE equipment angle for quantum dot lasers and silicon photonics. Small position but big upside if the ROSIE Tier 1 order lands.

$IQE 1% - InP epi wafer supplier with strategic review and possible M&A optionality. Feels like the market still isn’t paying attention

$NBIS 1% - Pure neocloud exposure. Inference demand sounds completely parabolic right now and pricing power has shown up almost overnight.

$LITE 1% - Obvious beneficiary of NVIDIA’s multi-year optical agreements. Could quietly become one of the biggest winners if CW laser demand keeps surprising higher

$NOK 1% - AI RAN and optical transport exposure. The NVIDIA partnership is real and telecom AI infrastructure feels underappreciated

$AEHR 1% - Owns a very niche but important layer: wafer-level burn-in for PICs. Exposure to both photonics and power semis

$VIAV 1% - Optical testing and validation. Every serious 1.6T deployment eventually runs through VIAVI gear somewhere in the process

I know it looks crowded with a lot of positions, but I’m trying to be realistic about how I’d actually invest

It’s easy to say just go all in on one name but for most people that’s way too binary and mentally exhausting

So instead I’d spread exposure across the parts of the stack I think matter most ie photonics, optical networking, substrates, packaging, memory, testing, foundries, AI factories etc

Basically the companies helping build the physical backbone AI actually runs on

Not financial advice obviously. Just how I’m personally thinking about the space right now

What would you add ?

I am digging into $POWI and $HLIT this weekend

19

31

318

28,498

May 16

美股光通信产业链深度研报:前瞻布局1.6T&CPO光子超级周期

在全球光子产业超级周期行情下,提前布局1.6T高速光互联 CPO共封装光学赛道,是当下最具确定性的投资主线,本人对此逻辑高度坚定。

基于产业高景气判断,我全面布局整条光通信全产业链,同时额外加码一处核心产能瓶颈标的,核心标的投资逻辑如下:

1. $SIVE Sivers Semiconductors

公司激光业务深度绑定**JBL Jabil、MRVL Marvell、Ayar Labs、O-Net**等头部客户,业绩随下游需求高速释放。

英伟达NVDA、谷歌GOOGL持续大力推动光子架构落地,1.6T与CPO产业落地进度,远超机构保守盈利预测。

行业唯一利空为供应链多元化分流,但捷普JBL独家优先合作足以印证其硬核实力。对比**MTSI Mouser、LITE Lumentum、COHR Coherent、Furukawa**等同业,全球高端激光厂商市值普遍突破百亿级别,而这家手握芯片产能壁垒的企业,当前总市值不足10亿美金,估值严重低估。

2. $6451 Shunsin Electronics

作为富士康旗下光芯片测试、封装、组装专属代工平台,公司市值相较$LWLG Lightwave Logic低15亿美金,估值存在明显错配。

背靠富士康庞大光子产业订单,经营风险充分释放。台积电旗下光学板块VisEra估值约50亿美金,第三代产品2028年下半年才实现放量;而富士康体系内的Shunsin明年即可开启产能大规模爬坡。

深度受益英伟达$NVDA在台CPO产业链刚需,公司明确扩产 行业需求爆发双重利好,前瞻市盈率处于低位,业绩弹性充足。

3. Win Semi 稳懋半导体

全球DFB激光芯片核心晶圆代工厂,承接SIVE激光产能扩产订单,同时切入**AVGO Broadcom、SpaceX**等高端前沿供应链。

梳理全产业链脉络可见,Win Semi几乎覆盖所有前沿光电核心赛道,其产业核心价值尚未被市场充分定价,具备极强预期差。

4. $MRVL Marvell Technology

对标迷你版AVGO博通,产业卡位价值突出。目前已与谷歌GOOGL达成深度技术合作,成长逻辑可延续至2028年之后。

核心强催化来自微软$MSFT Maia算力芯片量产,2026年下半年正式开启放量,2027-2029年维持指数级增长。此前收购Celestial补齐核心技术短板,战略布局极具前瞻性,股价回调阶段为优质布局窗口。

5. $HPS Hammond Power Solutions

变压器、电力开关设备属于算力基建偏传统配套品类,市场关注度较低。

当前行业产能缺口长达2-5年,企业在手订单同比增幅超100%,行业供需格局极度紧张。

自确立投资逻辑以来,该股涨幅仅20%以上,充足高确定性在手订单大幅降低投资风险。后续顺利落地产品提价,将直接带动公司毛利率上行。叠加去年完成厂区扩建,正式迈入高增速复利成长通道。

全赛道优质备选标的(附美股代码)

NBIS、JBL、RPI、TSEM、LITE、ARM、SOI、AXTI、IQE、ALRIB、Fittech、PCL

组合配置思路

主力持仓聚焦1.6T CPO光通信核心产业链标的,搭配与AI产业链低相关性细分标的做杠铃式均衡配置,平滑账户波动,长期把握光子超级周期产业红利。

3

10

44

13,734

May 12

🔥 CPO 真正的机会,可能不在最热门的大票,而在这些“隐藏供应链”

现在越来越多人开始讨论:

CPO(共封装光学)。

因为 AI 数据中心已经进入一个新阶段:

真正限制系统扩张的,越来越不是 GPU。

而是:

数据怎么传。

未来超大 AI 集群里。

几千颗 GPU 会同时交换海量数据。

如果网络带宽跟不上。

再强的 GPU 也会被堵死。

这也是为什么:

CPO 开始被视为下一代 AI 网络架构的重要方向。

因为它本质上是在解决:

功耗

延迟

带宽密度

信号完整性

这些 AI 数据中心越来越致命的问题。

比较关注的一批 CPO 相关公司:

$SIVE

Foci (3363)

$TSEM

Browave (3163)

PCL (4977)

$AXTI

Msscorps (6830)

$IQE

Shunsin (6451)

Furukawa Electric (5801)

$MTSI

Nextronics (8417)

$LITE

$COHR

FitTech (6706)

$GFS

$ASX

LandMark (3081)

$SOI

有意思的是:

这里面很多公司,市场平时根本不会重点关注。

但如果 CPO 真正开始大规模落地。

这些公司可能会慢慢进入 AI 核心供应链。

因为未来真正受益的,不只是光模块。

而是:

硅光

PIC

激光器

先进封装

玻璃基板

InP 衬底

SOI 晶圆

Foundry

高速测试

整个生态。

特别值得注意的是:

CPO 会重构整个产业链利润分配。

过去:

传统光模块厂商是核心。

但未来:

价值可能开始往:

芯片设计

先进封装

Foundry

材料

这些层转移。

这也是为什么:

$TSEM

$GFS

$ASX

这些 Foundry 开始越来越重要。

因为未来 PIC、硅光、CPO。

都需要更复杂的制造工艺。

另外一个被市场低估的方向是:

材料层。

$AXTI

$IQE

$SOI

这些其实都卡在:

上游核心衬底。

未来 AI 光互联真正全面爆发后。

最容易缺的。

很多时候不是终端产品。

而是:

没人能替代的底层材料。

而:

$LITE

$COHR

$MTSI

则属于 AI 光通信升级里的核心玩家。

未来 AI 网络越复杂。

高速光连接需求就越恐怖。

真正值得注意的是:

AI 的下一阶段,已经越来越不像“软件革命”。

而更像:

一场全球级基础设施升级。

而 CPO,很可能会成为其中最关键的一层。

因为未来 AI 拼的。

不只是算力。

而是:

谁的数据流最快。

4

5

1,181

Solid CPO basket. The mix of substrate (AXTI, $IQE, $SOI), laser/integrator ( SIVE, LITE, $COHR), foundry ( TSEM, GFS),andpackaging(GFS), and packaging ( GFS),andpackaging(ASX, Shunsin) covers every layer of the stack, which is the right way to play it given nobody knows yet which architecture or supplier wins at scale.

The Taiwan small caps are the ones I haven't done enough work on. Browave, Msscorps, Shunsin, Nextronics, LandMark, FitTech - all under-covered by English-language analysts. Curious which of those you think are most asymmetric from current levels.

Long $LITE, $TSEM in my book - the integrated and foundry layer picks.

Up 17% in 14 sessions, 12 points ahead of SPY. @STMPortfolio for daily marks.

3

1

12

3,268

May 12

Random CPO related names I like:

- $SIVE

- Foci (3363)

- $TSEM

- Browave (3163)

- PCL (4977)

- $AXTI

- Msscorps (6830)

- $IQE

- Shunsin (6451)

- Furukawa Electric (5801)

- $MTSI

- Nextronics (8417)

- $LITE

- $COHR

- FitTech (6706)

- $GFS

- $ASX

- LandMark (3081)

- $SOI

Disclosure: I own most, not all though.

124

165

1,881

304,976

Day 0. No app. No users. No clue if this works.

I'm building an AI workout planner — and I'm documenting everything from the start.

The wins. The dead ends. The 2am debugging sessions.

Follow along 👇

#buildinpublic #indiedev #fittech

1

3

67

if you have to choose Fittech or Shusin to add some shares today, who would it be?

4

2

57

May 5

I’m in Unimicron, Fittech, Foci, Microelectronics, Win Semi, Nanya and now Shunsin.

1

5

588

May 5

Fittech limit up 4 times in 5 days and new 52wk high 3 days in a row. April revenue may not show a jump, but May should if this ramp is actually taking place

Apr 26

Quick Fittech (6706.TW) update and correction/clarification thread. First I'm not sure who created it, but saw this.... unique explainer on the company in the cmoney forums👇

1

12

6,594