Jun 9

CommBank is investing AU$140M in human-led service for complex customer moments. The same bank is also rolling out an AI-powered conversational banking assistant inside its mobile app.

Phil Hatton, Director of CRM Sales at @ServiceNow , captures the logic behind running both in parallel. "Whether it's complex, emotional or high stakes, that's where the human really has to be there and has to be properly equipped."

Nicole Willing has the full story.

➡️ Read more: eu1.hubs.ly/H0w1pl00

#CX #BankingCX #CustomerExperience #AIinCX #HumanSupport

1

103

One opportunity can completely change someone’s life.

I’m still searching for mine. 🙏

#Palestine #SaveGaza #HumanSupport #GazaCrisis #Peace

5

3

7

282

human support for genuine cases. This is not just an account, it’s someone’s digital life.”

#Instagram #Meta #AccountDisabled #BringBackAccounts #FixInstagram #HumanSupport #InstaSupport #MetaSupport #JusticeForUsers #StopAIAbuse

3

6

5,084

Apr 30

Customer service could be getting a major upgrade in California. A new proposal aims to cap hold times at just 5 minutes, pushing companies to prioritize real human support over endless automated loops. If passed, this could redefine how we experience customer care.

Read the full blog at - gemjournal.com/a-5-minute-ca…

#CustomerService #RightToHumanService #CaliforniaBill #ConsumerRights #TechPolicy #CustomerExperience #NoMoreWaiting #ServiceReform #HumanSupport #DigitalExperience

11

33

Apr 27

Ukihitaji usaidizi ata 3am tuko macho! 👀 This is what we mean when we promise to be your trusted financial partner 🫶🏾

#humansupport

#customerservice

#trendingreels

#corporatehumor

#fypX

1

13

42

Feb 27

After12 days without internet in Iran, and with the strictest censorship,I barely managed to get online to ask for help.

I’m in real need due to the current financial situation

If anyone can help even a little, I would truly appreciate it.

#MutualAid #HumanSupport #Iran #USA

1

2

94

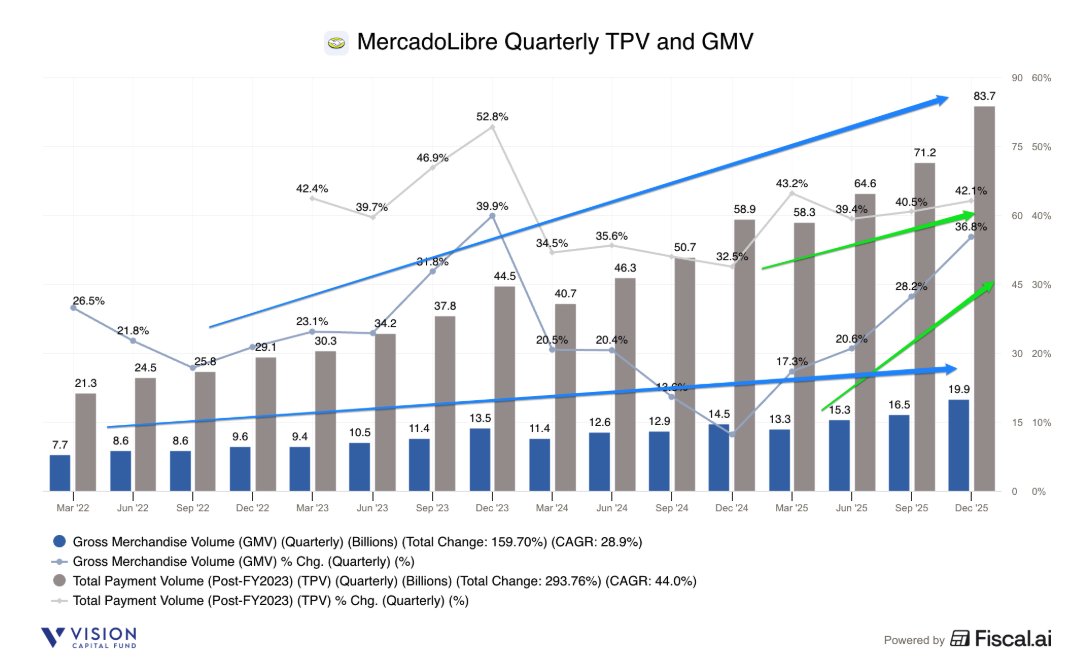

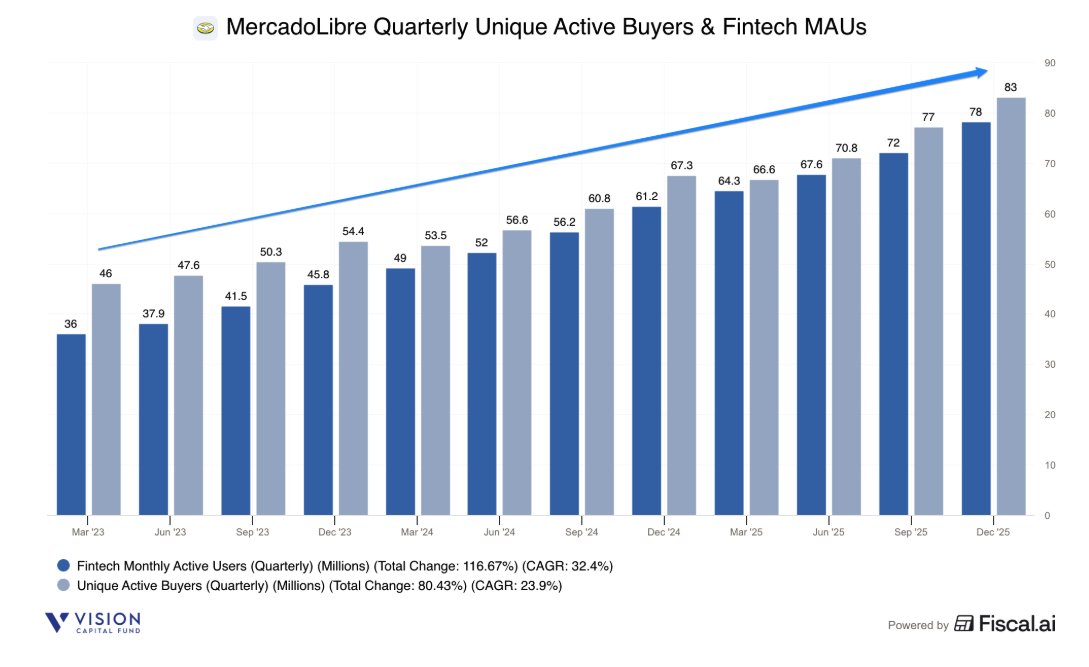

MercadoLibre $MELI 4Q25 Earnings

- Rev $8.8b 45% ↗️🟢

- GP $3.8b 38% ↗️🟢 margin 43.2% -217 bps ↘️🔴

- Adj EBITDA $1.1b 16% ↗️🟢 margin 12.9% -318 bps ↘️🔴

- EBIT $0.9b 8% ↗️🟡 margin 10.1% -338 bps ↘️🔴

- Net Inc $0.6b -13% ↘️🔴 margin 6.4% -416 bps ↘️🔴

- OCF $5.2b 78% ⤴️🟢 margin 59.5% 1121 bps ✅

- FCF $0.8b 36% ↗️🟢 margin 8.7% -53 bps ↘️🔴

FY25 Earnings

- Rev $28.9b 39% ↗️🟢

- Service Rev $25.3b 36% ↗️🟢

- Product Rev $3.6b 69% ↗️🟢

- GP $12.9b 34% ↗️🟢 margin 44.5% -159 bps ↘️🔴

- EBIT $3.2b 22% ↗️🟢 margin 11.1% -158 bps ↘️🔴

- Net Inc $2.8b 8% ↗️🟡 margin 9.8% -283 bps ↘️🔴

- OCF $12.1b 53% ↗️🟢 margin 41.9% 382 bps ✅

- FCF $1.5b 22% ↗️🟢 margin 5.1% -72 bps ↘️🔴

4Q25 Revenue by Segment

- Service Rev $7.5b 41% ↗️🟢

- Product Rev $1.2b 69% ↗️🟢

- Commerce Rev $5b 40% ↗️🟢

- Commerce Svc Rev $3.8b 32% ↗️🟢

- Commerce Pdt Rev $1.2b 71% ⤴️🟢

- Fintech Rev $3.8b 51% ↗️🟢

- Fintech Svc Rev $1.9b 33% ↗️🟢

- Fintech Credit Rev $1.9b 77% ⤴️🟢

4Q25 Revenue / Direct Contribution by Geography

- BR Rev $4.6b 48% ↗️🟢

- BR Commerce Rev $2.8b 42% ↗️🟢

- BR Fintech Rev $1.9b 59% ↗️🟢

- BR DC $517m -5% ↘️🔴 margin 11.1% -620 bps ↘️🔴

- MX Rev $2.1b 56% ↗️🟢

- MX Commerce Rev $1.4b 52% ↗️🟢

- MX Fintech Rev $730m 64% ↗️🟢

- MX DC $381m 56% ↗️🟢 margin 18.2% 6 bps ✅

- AR Rev $1.6b 23% ↗️🟢

- AR Commerce Rev $545m 11% ↗️🟡

- AR Fintech Rev $1.1b 30% ↗️🟢

- AR DC $600m -2% ↘️🔴 margin 37% -968 bps ↘️🔴

- Others Rev $414m 54% ↗️🟢

- Others Commerce Rev $295m 49% ↗️🟢

- Others Fintech Rev $119m 68% ↗️🟢

- Others DC $60m 50% ↗️🟢 margin 14% -38 bps ✅

4Q25 Biz Metrics

- GMV $19.9b 37% ↗️🟢

- GMV (BR) 35% ↗️🟢

- GMV (MX) 35% ↗️🟢

- GMV (AR) 42% ↗️🟢

- GMV (1P) $4b 80% ↗️🟢

- Items sold 752m 43% ↗️🟢

- Items sold per unique buyer 9.0 15% ↗️🟡

- Live listings 635m 42% ↗️🟢

- Unique Active Buyers 83.2m 24% ↗️🟢

- 0-1D Shipments 191m 29% ↗️🟢

- TPV $83.7b 42% ↗️🟢

- TPV Acquiring $55.7b 33% ↗️🟢

- TPV Acquiring OFF $34.9b 32% ↗️🟢

- TPV Acquiring ON $20.8b 34% ↗️🟢

- Monthly Active Sellers with Credit 33.8% 📶🟢

- TPN 4.5b 36% ↗️🟢

- Fintech MAU 77.9m 27% ↗️🟢

- Fintech AUM $18.8b 78% ↗️🟢

- Credit Portfolio $12.5bn 90% ↗️🟢

- CP (consumer) $4.5b 76% ⤴️🟢

- CP (credit card) $5.6b 114% ⤴️🟢

- CP (merchant) $2b 69% ↗️🟢

- CP (asset-backed) $0.4b 90% ⤴️🟢

- NIMAL 23.3% ⤴️🟢

- Past due 15-90D 7.6% ➡️🟢

- Past due >90D 16.8% ↘️🟢

- Provision >15D 103% ➡️🟢

- Provision >90D 150% ➡️🟢

- Advertising Rev 70% ↗️🟢

1 | Saw reacceleration in GMV and revenues from strategic investments to lower the free shipping threshold driving higher purchase frequency, new buyers, higher volumes, and higher, NPS at record levels

This acceleration is the result of our strategic investments to enhance the value proposition, most notably the decision to lower the free shipping threshold. More free shipping is driving higher purchase frequency and bringing new buyers into the ecosystem. This volume is translating directly into efficiency. Our logistics network absorbed the increase in volumes while driving productivity gains, proving our ability to scale effectively. Our value proposition is generating traction in Mexico, too, where GMV also grew 35%.

Our top line grew by 45% YoY. As I mentioned earlier, our NPS is at record levels, and that's because of the investments that we have been doing. You mentioned CBT, 1P, the lowering of free shipping threshold, expanding more free shipping, increasing fulfillment capacity.

2 | Third time lowering free shipping thresholds, continue to see positive results that is driving them to continue to double down

This is the third time that we have lowered the threshold, and the results we're seeing now are

no different from the results we've seen in the past. Growth has accelerated, frequency has accelerated, we are at record conversion rates, record retention rates for new and existing buyers. We are having more new buyers. Our NPS in Brazil is at its peak. We have more sellers, more live listings per sellers. We are expanding market share and reaching our record levels. Yes, indeed, we are pleased and this is very much aligned to what we were planning for.

3 | Cost improvement in shipping costs will come from more volumes, higher utilisation, lower idle capacity

In terms of shipping costs, I would say we are pleased with the performance that we are having. The cost improvements come from several parts of the equation. On the one hand, of course, more volume is diluting, you know, more cost. We are taking advantage of idle capacity through our slow shipping network, meaning that we are able to ship items whenever we see a space in the value chain. Of course, we continue working on technology and productivity in order to make our operation even more efficient and more sustainable. We don't see a reason for this not to change or not to continue, right? We are positive. I think the team has done a tremendous job, but we still think we have more things to do.

4 | Stronger investments in shipping and credit card are resulting in 500-600bps margin compression and lower profitability near-term

The margin compression reflects our decision to invest in the areas of the business with the greatest long-term growth opportunity, especially shipping and credit card expansion.

You know, we've been talking about the investments that we are doing. We've talked a lot about the results of those investments, but we wanted to give a sense of what those investments were in terms of margin compression. What we did here is we basically, we look at the main areas of investment, like you said, the lowering of the shipping threshold that we did last year in Brazil. The credit card, we're investing in Brazil, Mexico, and now Argentina. OneB, which is continues its path to profitability, but still not profitable on its own. The same thing with CBT, which we are expanding now to the China and the U.S. corridor. We also added the smaller countries where we continue to invest as we reach scale in those countries. When we put all that together, we wanted to give you a sense of the pressure that that generated on our margins, and that gives

you a range of between 5 and 6 points. That's the intention of putting it on the letter. In terms of the trajectory, I think it's in line with what we have been talking about this in the past.

5 | Confident of underlying unit economics of CBT, OneB, credit cards, etc that they are profitable at scale, hence wiling to invest.

CBT is a business that, you know, when it's locally fulfilled, is profitable. International fulfillment needs to continue scaling and is moving in the right direction, but it will continue to scale and it will put some pressure on margins because of that. When you look at our OneB, I think we talked a lot about OneB, it continues to be profitable on a variable basis level, and before allocating central cost, direct, indirect cost, is profitable. The scale will play in our favor in terms of continuing to improve profitability. I think the credit card, Osvaldo will talk about this, I'm sure, in some of the questions, but the credit card continues to improve its profitability, in particular in Brazil, where we're seeing already a significant part of the portfolio, the older cohorts being profitable. I think a lot of moving parts, right? The individual businesses are moving in the right direction. You have a shift issue because some of these are growing at a faster pace. The bottom line is that we're very confident that the investments that we're making on our platform are addressing long-term, you know, the long-term opportunities that we see ahead of us, and we're also improving user experience in our platform.

6 | While Argentina has the highest profitability, most of the margin compression came from higher fulfiment center costs and bad debt provisions for credit cards

Argentina continues to be the highest profitability market in terms of spread, in terms of margins. We did see some compression, mostly coming from fulfillment. As you know, we opened a couple of new fulfillment centers recently, so that generated some year-on-year compression on costs. Also provisions for bad debt because of the credit card. We launched the credit card in the middle of last year, so we're seeing some compression because of that. As you know, the credit card requires investments upfront, and there is some year-on-year increase on funding costs. It's true what you said. Sequentially, QoQ, the funding cost of our credit portfolio was lower in Q4 relative to Q3, but it still was higher relative to a year ago. Those are the main reasons for the compression that we saw in this quarter

7 | Margin pressure coming from deliberate decisions to pursue investments that are paying off with higher growth and gaining market share, not trying to optimise short-term margins, remain confident of long-term margin trajectory

You know, most of the margin pressure comes from deliberate decisions that we're making in terms of pursuing investments that are generating tremendous growth and improving user experience. As you mentioned, in Brazil in particular, we have been growing our GMV and gaining market share, mainly because of these investments.

We feel very comfortable with these investments and the current margin levels because we are seeing the results in terms of growth, market share gains, and improvements in user experience and engagement. As I said in the past, our main focus is on capturing the large opportunities in front of us in commerce, fintech, and advertising. We will not hesitate to invest in order to capture those opportunities as we have done in the past, even if that puts some short-term margin pressure. We're not trying to optimize short-term margin. We manage the business from a long-term perspective. We believe these investments are creating foundation for future growth. We remain confident in our long-term margin trajectory. Again, we are confident in the investments that we're doing in credit card and commerce, and we are seeing already the results.

8 | Ramped up sales & marketing spent on the higher end of then usual range largely on social media and affiliate marketing, seeing strong results

Specifically this quarter, if you see sequentially, we increased our spending by 60bps and YoY by 1.4bps on marketing. For the most part, is a result of expansion of our social channels. As we mentioned in the past, we are scaling our affiliate program with very positive results. In Brazil, for instance, the number of affiliates almost doubled in Q4 relative to Q3, and YoY we have 6x the number of affiliates that are selling and promoting products to MercadoLibre, Inc.. We see as a very, very positive and very... It's a channel that should help us drive growth in the future, we are investing in that particular channel. That explains most of the increase in investments and marketing. The rest of the lines remain the same. There might be some seasonality in Q4, but for the most part, is the affiliate program. Just to put it in perspective, if you look at the past several years, the range of investments in sales and marketing is between 11% and 12%. We are on the upper range of that level, but it's within those lines that we have been investing over the past several years.

9 | Leveraging on AI in advertising, acquiring salesforce, and for Mercado Page customers, 20% of GMV advised by AI seller assistant

Across our ecosystem, we are seeing clear evidence that our investments in artificial intelligence are accelerating revenue. In advertising, AI is powering our bidding algorithms, and automated campaign tools are generating better returns for sellers. This improved performance is driving higher adoption and capturing a larger share of advertisers' wallet, propelling the business to grow 67%. AI is also transforming the effectiveness of our acquiring sales force. In Brazil, these tools helped identify high-value merchants faster, resulting in higher TPV per merchant and shortened payback periods. This contributed to acquiring TPV, growing 25% in Brazil and 50% in Mexico. Our Mercado Pago AI assistant is solving 87% of interactions without the need of humansupport. Millions of users already adopt this conversational tool to manage their credit card, make transfers, and understand their credit offerings…I think it's worth highlighting the fact that we have a seller assistant today running in our platform. 20% of our GMV is somehow advised by our assistant.

10 | Think agentic commerce is early, know that it can help buyers improve the product discovery process, prefer that MELI is one providing that agentic experience instead as they have the 1P data to do it best, focusing on that

Let me start with the idea of agentic commerce and how that will play out for us and potentially disintermediating, which is something that I've been asked over and over. I think it's still a bit early in the game, but we don't think that solving one part of the value chain will actually change the rules of the game. Meaning that we still think that the key is to provide the best end-to-end experience for our customer.

I would say that the part where we're putting most of our efforts is in developing our own agentic experience inside MercadoLibre. We think, and we are convinced that we have the first-party data to create the best search, best recommendation, best discovery engine, on which we can personalize, and, you know, lay over the agentic experience that the new technology drives.

We also know that there's a technology today that can dramatically improve the product discovery process. For that reason, we are putting all of our efforts and deploying lots of engineers in building our own agents and our own shopping assistant within MercadoLibre, Inc.

11 | Agentic commerce will accelerate shift of offline retail to online where MELI will benefit, and MELI will still be the go-to place for shopping online in LATAM

And by the way, if you believe that there is a world of agentic commerce, that could mean that, you know, retail will move even faster from the offline to the online world. All this to say that I do think that we are well-positioned to actually capturing ads revenues in the future, because we still think that MercadoLibre will be the go-to place for demand to do shopping online. On top of that, there's an issue on what happens with all the agentic commerce that will occur outside of MercadoLibre, because for sure, we will not have 100% market share. We think that that also represents an incremental opportunity for Meli, right?

12 | Agentic commerce also represents an additional digital revenue opportunity because MELI has a unique set of data, customer knowledge, and attribution capabilities

Today, we are providing with our tech stack, advertising services to third parties. We do that with Google Ad Manager, we do that with Disney, we do that with Roku, with HBO Max. The reason behind that is that we have a unique set of data, customer knowledge, attribution capabilities that we think are very hard to match. Eventually, what I'm trying to convey is that on the one hand, we are confident on MercadoLibre's own ability to capture traffic through its own agentic experience, and on top of that, we do think that advertising represent an additional revenue opportunity in a world in which there is agentic commerce.

By the way, the agentic world can also imply a faster shift of advertising dollars moving from traditional offline channels into digital advertising, which generates the opportunity to be even bigger. We remain positive, we remain focused. The only thing that we know for sure is that we need to put our developers to work to have the best tech stack for advertising and the best agentic experience inside MercadoLibre.

13 | Advertising remains in the early days with lots of potential

Penetration of ads with revenue as a % of GMV is still small compared to its potential. Very happy with the results so far, but even more encouraged with the potential looking ahead.

14 | While NPLs increases due to faster credit book growth, NIMs improved, which means risk was priced appropriately, confident of credit book, models and collection

Nonetheless, the increase in NPL was mostly related to the consumer and merchant books. Having said that, I think that more important than NPLs are NIMs, and those improved, meaning we are more profitable than we were a quarter before. What we did was, we increased the number of people and the riskier number of people we gave credit to, but we priced that risk accordingly, and therefore, we ended up having a significant, a larger spread than we did on the prior quarter….We feel very, very comfortable about the quality and the health of our portfolio, and that's the reason why you see our credit book growing at 90%, because we are confident on our models and our collection.

➡️ Key takeaways for MercadoLibre 4

MELI continues to grow as LATAM’s dominant e-commerce and fintech platform with a long growth runway with still low penetration. As expected, the market will not like MELI lowering free shipping costs in Brazil and the nearer term negative impact on profitability, we think it is highly strategic longer term to drive strong user engagement, activity, retention to allow it to compete effectively against Shopee in the low-to-mid priced segment, and results are clearly showing in the growth reacceleration. Excited to have Ariel Szarfsztej, the new CEO leading MELI going forward.

1

4

52

4,985

Feb 11

I used to dislike hitting the Support button on any platform.

Usually, it meant a long date with a chatbot that never understood my question

We’ve all been there, Please wait for a human.

You watch your phone battery die and whatever plans you had crumble while stuck in a support queue.

By the time it’s your turn, you've got other things to do and zero charge left.

I switched to @BitunixOfficial because they actually respect my time. When I need help, I’m not waiting for my turn in a digital lobby for hours.

It’s a real human, right when I need them, before my screen even dims.

Live Chat: 24/7 instant pulse

Email: support@bitunix.com for high-context details.

Help Center: support.bitunix.com for the DIY moments.

The tech is elite, but a support team that doesn't make me wait for my turn is the real flex. 🤝

#UserExperience #Bitunix #HumanSupport

21

1

28

1,385

22 Dec 2025

📞 When IT goes wrong, people want people.

61% of UK employees say poor IT support affects how well they can do their job.

TG Systems = real humans, fast fixes, no jargon.

🌐 tg-systems.co.uk | 📧 info@tg-systems.com

#ITSupport #HumanSupport #SMEs #BusinessIT

2

48

13 Nov 2025

💬 Real people. Real support.

Just a team ready to listen and help when you need it.

Need a hand? 👉 shorturl.at/xAz6p

#RockWallet #HumanSupport

3

9

302

31 Jul 2025

What really makes Virtual Assistants stand out?

It’s not just about managing calendars or replying to emails.

Great VAs bring a special kind of energy—calm under pressure, sharp with details, and always thinking two steps ahead.

Here’s what makes us different:

✨ We adapt fast. New tools? New workflows? We pick them up quickly.

✨ We stay organized so you don’t have to stress the small stuff.

✨ We listen between the lines—catching what’s not said, not just what’s written.

✨ We anticipate needs. You don’t always have to ask—we’re already on it.

✨ We protect your time and reputation like it’s our own.

Being a VA isn’t just a job. It’s showing up as a trusted partner behind the scenes—keeping things running, clients happy, and your headspace clear.

Because when you grow, we grow too.

#VirtualAssistant #HumanSupport #RemoteWork #WorkWithHeart #ProductivityPartner #TrustMatters #Smartwork #RemoteJobs #Hiring #VA #Mod #CM #Web3 #CommunityManagement #OpenToWork #Defi #Crypto #Discord #NFTCommunity

1

8

210

Because when you're dealing with your financial future 💸📈, you deserve more than a bot response. 💬❤️

#HumanSupport #Bitcoin #Blockchain #Crypto #h2crypto 💼🔐

*Not investment advice

1

3

29

25 Jun 2025

Our clients' customers get more than replies — they get real support 🙋♀️💬.

No bots. No brush-offs. Just care, clarity, and commitment 🤝✅.

That’s the Chirpish way 🐦💼.

#CXMatters #ChirpishSupport #CustomerExperience #HumanSupport #EcommerceHelp

3

34

14 May 2025

What do our clients' customers experience? Real conversations, fast help, and service that feels human. 💬❤️

At Chirpish, we turn every interaction into a relationship-builder. 🚀

#CustomerExperience #Chirpish #HumanSupport

2

276

28 Jan 2025

Sick and tired of no human help? That's where we are different...

We pride ourselves on our support services: a happiness rating of 99%, a first-time response rate of less than 1 hour, and an average resolution time of 6 hours. #support #customersupport #humansupport

1

142

23 Jan 2025

👋 When you reach out to Upstream, you’re talking to real people - not AI chatbots.

Get you the support you deserve.

Because great service isn’t automated - it’s personal. ❤️

#HumanSupport #CustomerFirst #Upstream

1

134

23 Dec 2024

5

160

2 Nov 2024

Get blazing fast #WebHosting, fair pricing, and 24/7 #HumanSupport with @VeeroTech. Start hosting at just $0.99!

VeeroTech.net

#webhosting #cpanel #whmcs #Webdesign #webdev #99CentsHosting

3

77

18 Dec 2023

@X won't me into my acct b/c I have a new phone & new email etc. b/c all my devices & svcs are comprimised

I can't get @Discord, @Google, @twitch, @nintendo, @X, @facebook, @instagram to help.

I PAY for premium svcs, but receive ZERO HUMANSUPPORT #PokemonUNITE #NintendoSwitch

1

1

133