Jun 11

Montage Tech just sampled DDR5 RCD06 at 9200 MT/s — 15% faster than Gen5. AI server memory upgrade cycle is real and accelerating from HBM down to standard DRAM. The whole stack moves. #AlphaGBM #DDR5 #MemorySupercycle

25

Jun 9

GoldKey Technology 2025 Forensic Audit youtu.be/deww-iYzEiU?si=9soT… 来自 @YouTube #GoldKeyTechnology #MemorySuperCycle #FinancialForensics #HBM #EnterpriseSSD #CorporateGovernance #HDINResearch #TechInvesting

3

Jun 9

GoldKey's -$57M Cash Black Hole: Can an AI Memory Super-Cycle Save This ... youtu.be/RX-PXPyfJxs?si=n72j… 来自 @YouTube #GoldKeyTechnology #MemorySuperCycle #FinancialForensics #HBM #EnterpriseSSD #CorporateGovernance #HDINResearch #TechInvesting

3

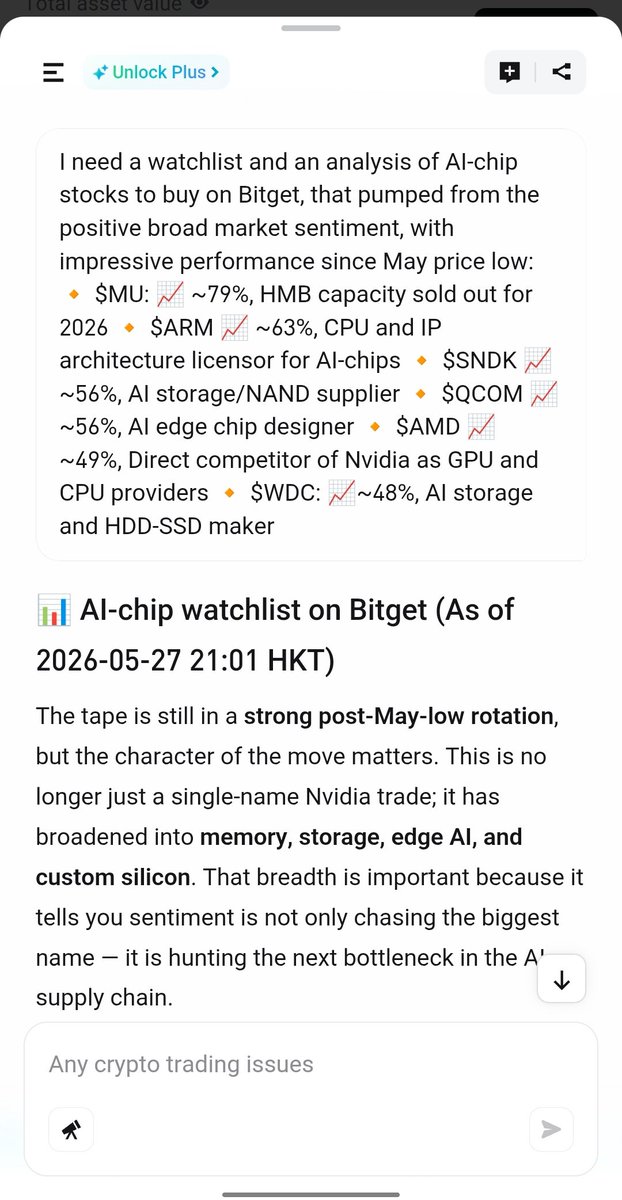

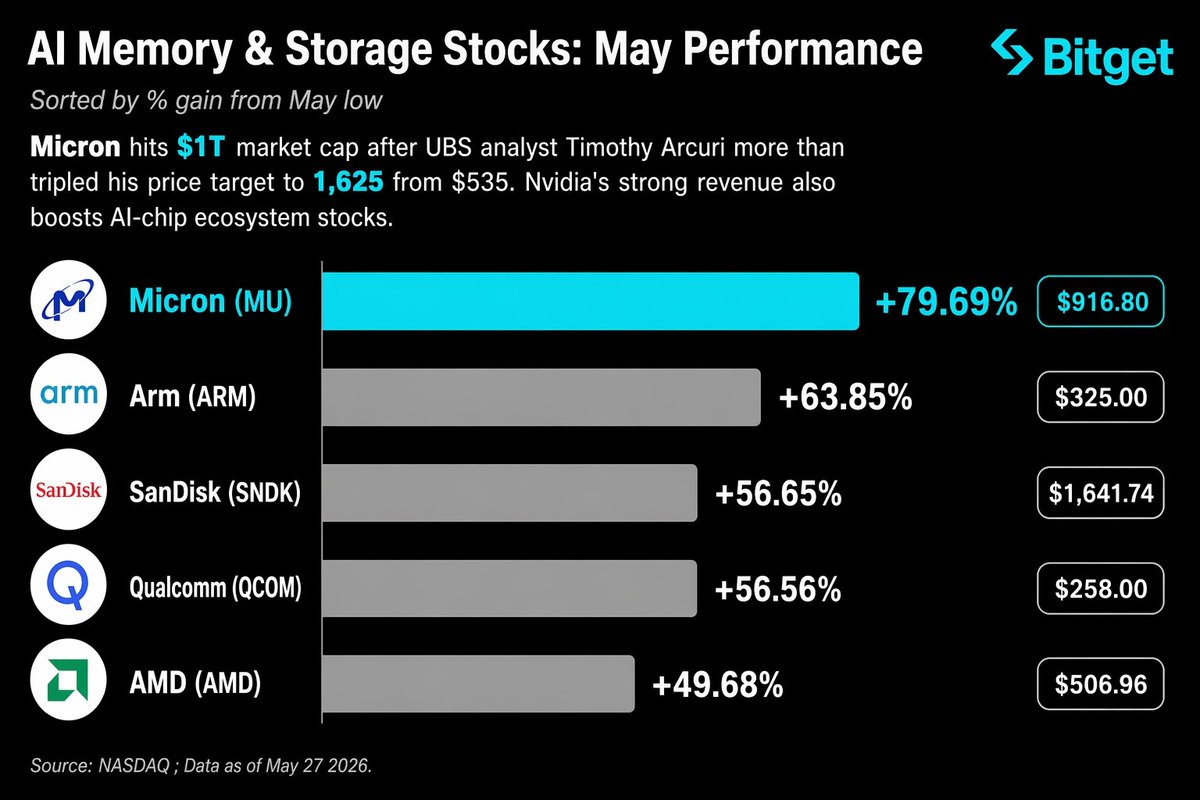

May 27

🚨 AI Memory & Storage Stocks Still Heating Up! 🔥📈

Micron ( $MU) is the poster child — HBM capacity sold out through all of 2026, and the broader AI-chip rotation is lifting the entire supply chain (memory, storage, edge, and architecture plays).

I just fed GetAgent the latest market data on Bitget and asked for a full watchlist analysis of AI-chip stocks that have been pumping hard since the May lows on strong fundamentals and AI bottleneck sentiment.

Here’s what GetAgent delivered (key takeaways):

Momentum leaders: $MU ( 18.53% today — most explosive), $SNDK ( 6.01%), $AMD

AI bottleneck plays: $SNDK, $MU, $WDC (storage & memory supercycle)

Best risk-reward balance: $QCOM (clean valuation edge AI), $WDC

$ARM is pure narrative/IP play but lower fundamental visibility

Overall: the trade has broadened beyond just GPUs into real infrastructure bottlenecks — exactly why these names ran hard post-May.

My trading plan on Bitget👇:

I’m running a leveraged futures basket focused on the AI memory/storage rotation. Scaling into dips on the strongest momentum bottleneck names while keeping position size disciplined (max 2-3% risk per name).

Using Bitget’s USDT futures for clean exposure without spot holding. Target: ride the HBM/NAND supercycle through 2026 while trimming on strength. Stop-losses tight on any broad market reversal.

AI-chip stocks I’m MOST bullish on right now (post-GetAgent analysis):

1. $MU — Still the clear king. HBM sold out for 2026 insane momentum = highest upside left in the group.

2. $SNDK — Purest memory-supercycle play with clean balance sheet.

3. $WDC — Strong storage beneficiary with elite ROE and real operating leverage.

My updated Tier List for upside potential (AI Memory & Storage stocks only — using the official template):

🥇 S Tier → $MU (explosive momentum locked-in HBM demand)

🥈 A Tier → $SNDK (pure memory supercycle), $WDC (storage tailwind profitability)

🥉 B Tier → $QCOM (best valuation balance), $AMD (solid competitor narrative)

C Tier → $ARM (high story, lower visibility right now)

Which AI-chip stock are YOU most eyeing on Bitget right now? Drop it in the replies quick reason why! 👀 $MU $SNDK $WDC $QCOM $AMD $ARM

#AIPump #BitgetFutures #AIStocks #MemorySupercycle

3

2

4

133

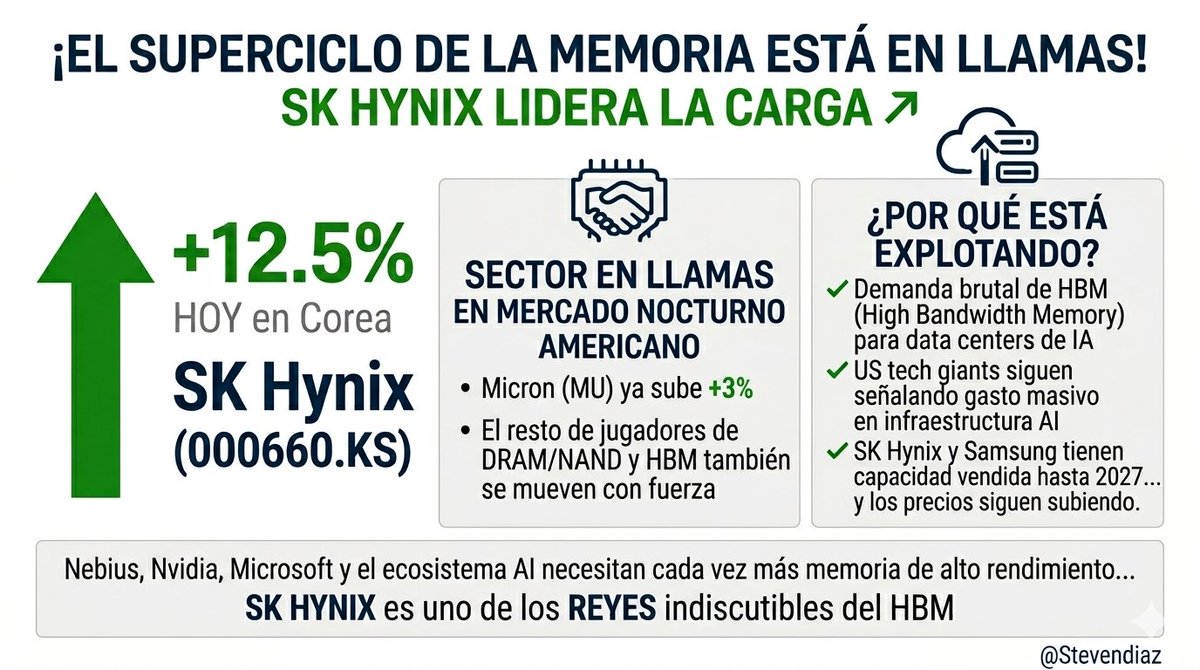

May 4

🚀 ¡EL SUPERCICLO DE LA MEMORIA ESTÁ EN LLAMAS! SK Hynix lidera la carga

SK Hynix (000660.KS) sube 12.5% HOY en Corea🔥🔥🔥🔥

Esto está arrastrando al alza a todo el sector de memorias en el mercado nocturno americano:

• Micron (MU) ya sube 3% en mercado nocturno.

• El resto de jugadores de DRAM/NAND y HBM también se mueven con fuerza.

¿Por qué está explotando?

✅ Demanda brutal de HBM (High Bandwidth Memory) para data centers de IA

✅ US tech giants siguen señalando gasto masivo en infraestructura AI

✅ SK Hynix y Samsung tienen capacidad vendida hasta 2027… y los precios siguen subiendo

✅ El “memory supercycle” está lejos de terminar.

Nebius, Nvidia, Microsoft y el resto del ecosistema AI necesitan cada vez más memoria de alto rendimiento… y SK Hynix es uno de los reyes indiscutibles del HBM.

¿Estás posicionado en memorias ($MU, $SNDK, SK Hynix ADR cuando cotice en USA, o el sector en general?

Yo llevo $MU $STX $WDC

#SKHynix #HBM #MemorySupercycle #AI #Semiconductores #MU #InversionAI

1

16

1,222

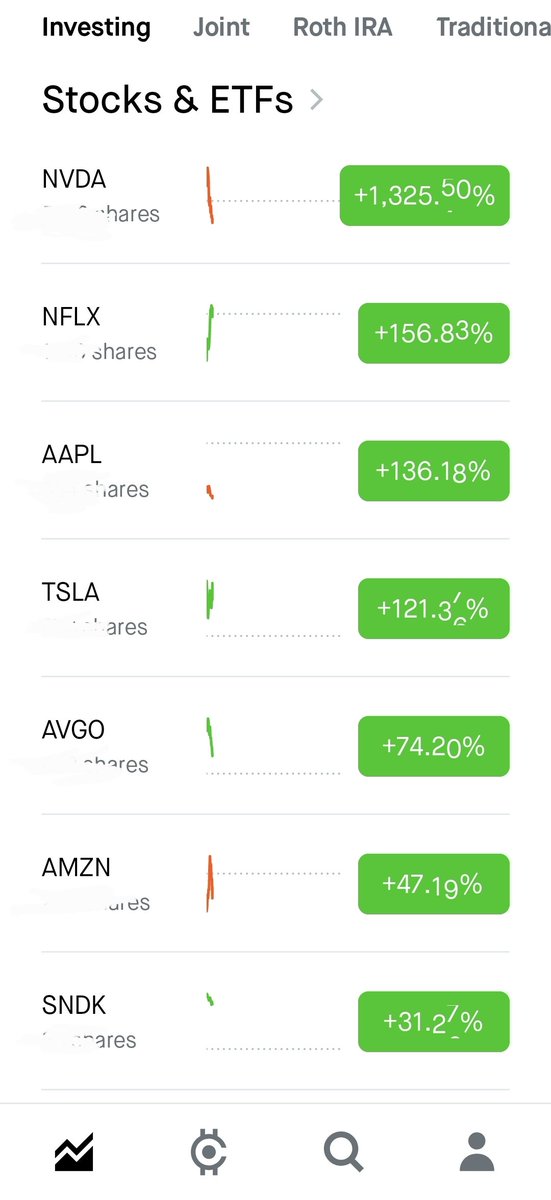

Apr 13

I've been heavily invested in fabless design companies like NVIDIA for years — and it's paid off big time as $NVDA 1,325%.

But recently, I'm diversifying more into memory & storage (DRAM, NAND, HBM) because AI demand is creating a structural supercycle — the old boom-bust cyclicality has significantly weakened.

Hyperscalers are locking in long-term supply, HBM is eating up capacity, and shortages are expected to persist into 2027–2028.

Recent performance:

$SNDK (Sandisk): 24.66% past week — AI data center storage exploding

Roundhill Memory ETF $DRAM: 19.95% past 2 wks since listing.

This is just a portion of my portfolio. Still bullish on fabless (design software moat) but adding memory exposure to capture the full AI infrastructure stack.

Past performance ≠ future results. Not investment advice.

What’s your take?

Fabless vs Memory — how are you positioning for the rest of 2026 and beyond?

#AI #Semiconductors #Investing #NVIDIA #MemorySupercycle

1

1

6

1,774

Feb 11

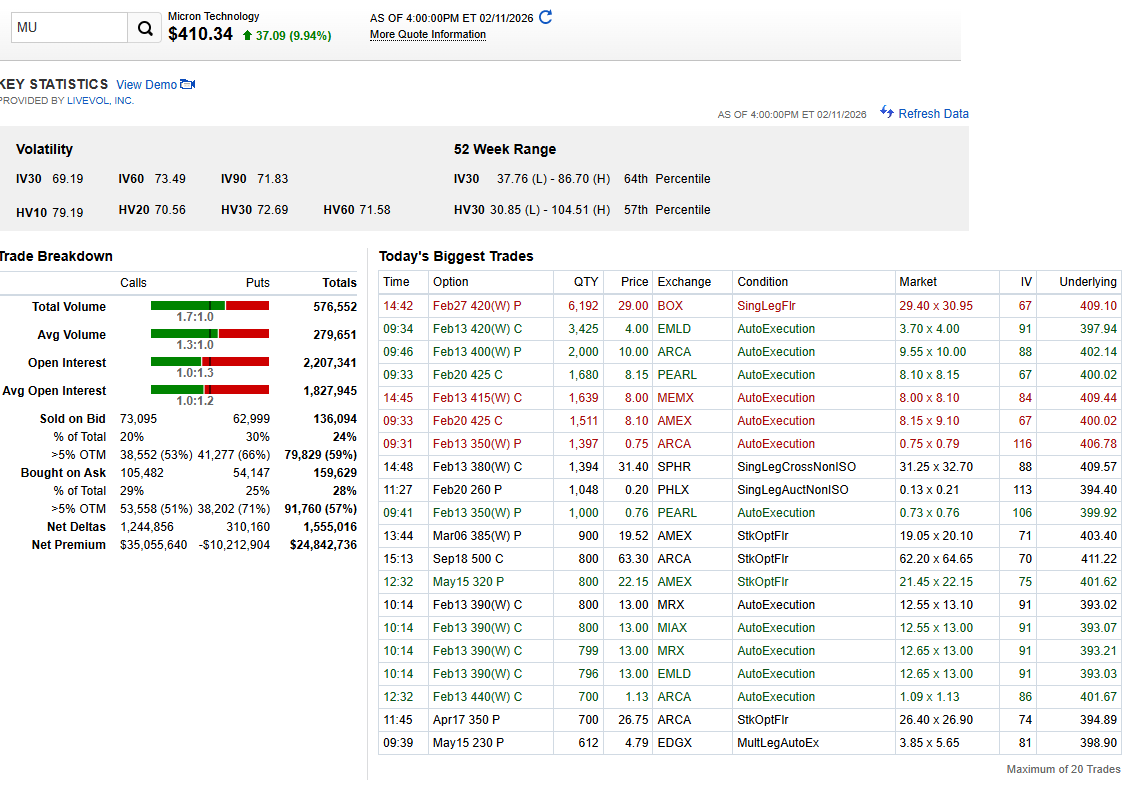

$MU Tale of the Tape Today...

Here are the $MU stats from today’s close (02/11/2026 @ 4:00pm ET)

$MU (2/11 close) $410.34 9.94% 🔥

Vol: IV still elevated — IV30 69 (≈64th pct), IV60 73, IV90 72. HV sitting ~71–73 range.

Options tape: Big day — 576k contracts traded (vs 280k avg). 2.21M OI (above avg).

Volume skew = Calls > Puts (1.7:1) = upside chase

But OI skew = Puts > Calls (1.0:1.3) = hedges still on

Flow / $: Net delta 1.56M and net premium $24.8M (calls doing the lifting).

Notable prints: Feb27 420P x 6,192 @ $29 heavy weekly strikes around 400–420 a Sep 500C block.

Take: MU ripped, traders chased calls, but the street is still structurally hedged with put-heavy OI → room for more upside if those hedges unwind.

#$MU #OptionsFlow #IV #Semis #MemorySupercycle

@smartertrader @aleabitoreddit @jukan05

5

630

Feb 9

2.9 美股日记 - Memory Supercycle 结束了吗?

一、宏观盘前指引

2/9 美股盘前处在典型“数据真空期”的震荡窗口:10Y 美债收益率约 4.22% 仍在区间内磨顶,黄金在 $5,020 高位震荡偏强,BTC 回到 $68k 更像是去杠杆后的均值回归而非“数字黄金”叙事重建。真正的方向被压缩到本周:受此前政府部分停摆影响,1 月 NFP 与 CPI 被历史性挤压至周三/周五集中发布,短线盘前波动更多是为两次宏观冲击预留仓位与波动预算,今日关注点在美联储官员表态对“缩表节奏与实际利率路径”的边际指引。

盘前异动主要围绕两条线:其一,AI 硬件反弹与估值修正并存(NVDA 上周五大涨后盘前小幅回吐、MU 因 HBM4 预期调整走弱),反映市场对“AI 军备竞赛等于确定性利润”的定价仍在摇摆;其二,监管重塑减肥药赛道(HIMS 受 FDA 强硬表态冲击、资金回流至 NVO 等合规头部)。

风格上,“Great Rotation”特征延续:资金从拥挤的 Mag7 抽离,推升道指史无前例突破 50,000 点,估值中枢向具备“物理护城河”的实体价值股(如 DOW、FDX、WMT)迁移。投资者的审美从“谁在造 AI”转向“谁在用 AI 赚钱”,高盛(GS)与卡特彼勒(CAT)等老牌巨头通过 AI 优化效率、重塑利润率上限,正将原本的“估值封顶资产”转化为“可成长资产”。这不仅是 AI 逻辑向实体的沉降,更是对“代码贬值”时代下实体资产价值的一次集体重新定价。

二、美股观察

1、赛道背景 - Memory Supercycle 讨论

SemiAnalysis(newsletter.semianalysis.com/…)用周期经济学而非单纯“AI 需求叙事”解释本轮存储行情,其核心在于:内存供给是一种高度“惯性化”的供给体系,而需求却呈现非线性跳变。

本轮与 1993(Windows PC)、2010(智能机 云)、2017–18(服务器 NAND)等周期的相似之处在于:单位系统内存含量出现“阶跃式提升”;但不同之处在于,AI 加速卡将 DRAM / HBM 的“每系统内存强度”推入非线性区间,同时供给端又遭遇 DRAM 缩放墙 HBM 封装/测试/认证瓶颈的多重锁死。结果是:供需缺口不是像历史周期那样快速收敛,而是在更长时间内维持紧平衡甚至恶化。

所以长期的供需缺口形成了储存赛道的“超级周期”,但需要注意的是,超级周期并不等于价格线性上行,期间价格仍然存在多次深度回撤。

2、核心博弈:未来 2-3 年的收入是否已被“Price In”

(1)看涨逻辑

目前的定价模型大多基于“商品逻辑”,尚未计入“战略溢价”与“事后结算权利”。最新的合同异动表明,存储厂已开始签署包含“价格追偿条款”的订单,这意味着即便产能已售罄至 2027 年,其 ASP(平均售价)仍具备向上弹性。若 2027 年 HBM4 带来的“定制化价值”推高毛利率至 65% 以上(目前市场普遍预期为 50-55%),且政府补贴(如日本政府对美光的 $3.3B 资助)显著降低了 Capex 压力,那么美光等巨头的自由现金流(FCF)增速将远超目前的折现模型定价。

更重要的是,当前售罄主要集中在 HBM3E,而 2026–2027 年将进入 HBM4 与 GPU 深度堆叠的定制阶段,内存将不再是简单的“bit 出货”,而是高度定制化的系统级组件,毛利率与议价能力有可能脱离传统 memory 周期框架。

(2)看跌逻辑

当利润在短期内爆发时,P/E 看起来极低,但 P/S 往往已接近或突破历史极值,这意味着市场已经用“峰值收入”在折现未来。如果未来两年更多是履约交付而非超预期涨价,股价反而可能因“确定性兑现”而进入估值收缩阶段。

此外,历史 memory supercycle 几乎无一例外都伴随着重复下单的行为:客户在恐慌中锁量,导致需求被提前透支;一旦供给边际改善,库存压力会迅速反噬价格预期。换言之,即便基本面没有立刻恶化,股价也可能大幅下修。

3、策略思考

(1)Timing:什么时候布局更优?

超级周期中的最佳入场点,往往不是在“景气最强、订单最满”的时候,而是在价格/股价因宏观或情绪因素出现与基本面脱钩的回撤阶段。典型触发包括:宏观去杠杆导致高 beta 资产被无差别抛售、市场因“供给即将释放”的早期信号过度反应等。

(2)标的选择

寻找存储上游垄断的节点,例如掌握 HBM 测试、先进封装、关键材料或认证节奏的公司等。

三、Memory Supercycle 储备标的备选 - Pure Storage

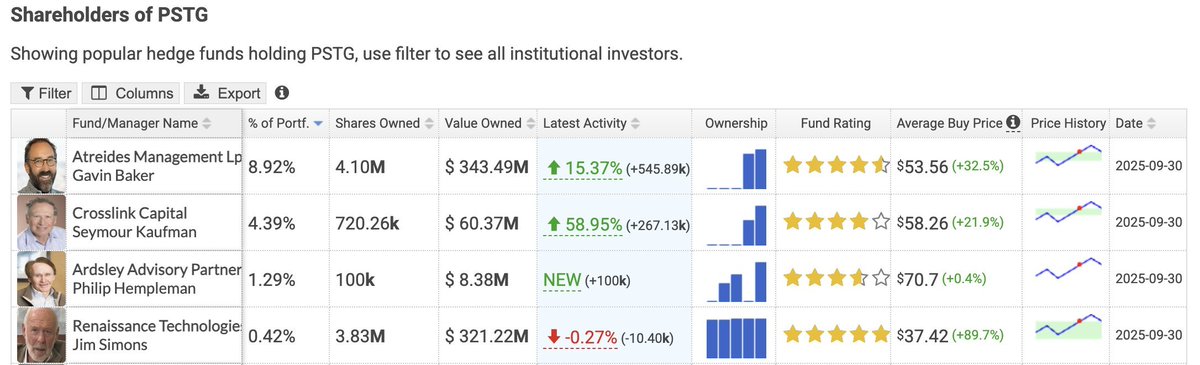

Pure Storage 是一家专注于全闪存(All-Flash)数据存储的基础设施公司,其核心竞争力在于 DirectFlash 架构:绕过传统 SSD 控制器,直接管理 NAND,从而显著降低延迟、提升吞吐,并在单位性能下大幅降低功耗。当前数据中心的核心瓶颈已从“算力不足”转向“电力与散热受限”,Pure 旨在解决这一痛点。根据公开讨论与其最新 13F 披露,知名科技投资人 Gavin Baker 已买入 PSTG。

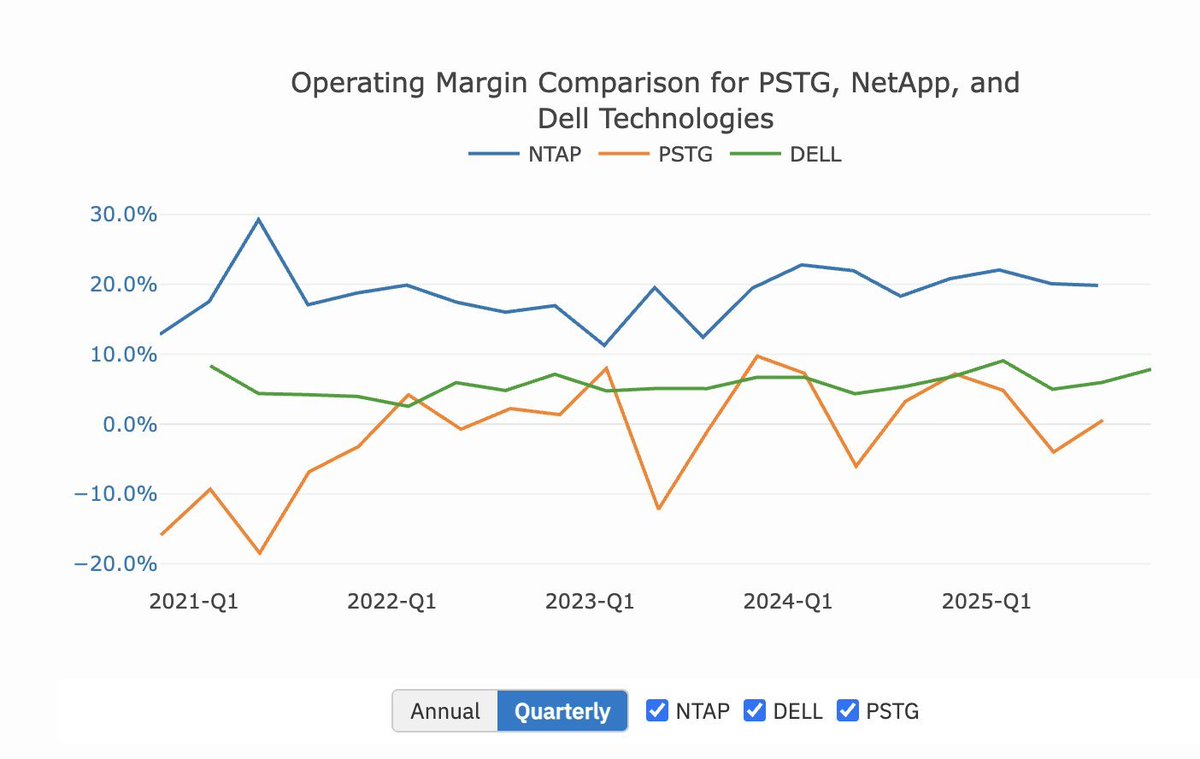

从数据上看,PSTG 正处在“主动牺牲短期利润、换取长期结构性位置”的阶段:FY25 收入约 32 亿美元、同比增长 ~12%,明显快于传统企业级存储行业;订阅 ARR 约 18% 增长、净留存率 117%,说明客户扩容与黏性仍然健康。毛利阶段性下滑并非竞争失速,而是公司在 E-family 产品线上主动吸收 NAND 成本、用价格与 TCO 优势替代机械硬盘,这是一次典型的“disk replacement land-grab”。更关键的是 hyperscaler 线索:Pure 已在 Meta 等超大规模客户中完成设计验证,未来采用软件授权 支持服务而非重资产卖硬件的模式,一旦进入 exabyte 级部署,其边际利润结构将明显优于传统存储厂商。

交易思考:目前 PTSG 并未进入 Memory Supercycle 的主线交易逻辑,但 Pure 有机会成为 AI 数据中心的低功耗数据层标准。鉴于目前 FCF 倍数较高,且 2 月 9 日正值宏观“数据压缩周”前的真空期,追高性价比极低;可等待科技股整体回撤期间建仓。

#MemorySupercycle #MU #SNDK #PSTG #Samsung #SKhynix

3

192

Feb 1

alright new format to track this

memorysupercycle[.]net

Jan 19

dram/ssd prices

(continued updates)

8

1

20

6,006

An excerpt from my upcoming Blog :

“Every modern AI system runs not just on GPUs, but on massive pools of high-bandwidth MEMORY . And that memory can only be made by three companies globally. 🎯

As AI data centers hoard #HBM, the entire memory supply chain is being reallocated. One gigabyte of HBM consumes roughly 4x the manufacturing capacity of regular DRAM, and AI is on track to absorb ~20% of global DRAM output by 2026‼️. Consumer demand hasn’t vanished, but capacity has. The result is a zero-sum game where AI customers paying 3–5x margins crowd out everything else, from laptops to smartphones to even GPU production itself.

#SENisms #MemorySuperCycle

I release the Full Blog & my Official disclosure at 500✅🎯

5

812

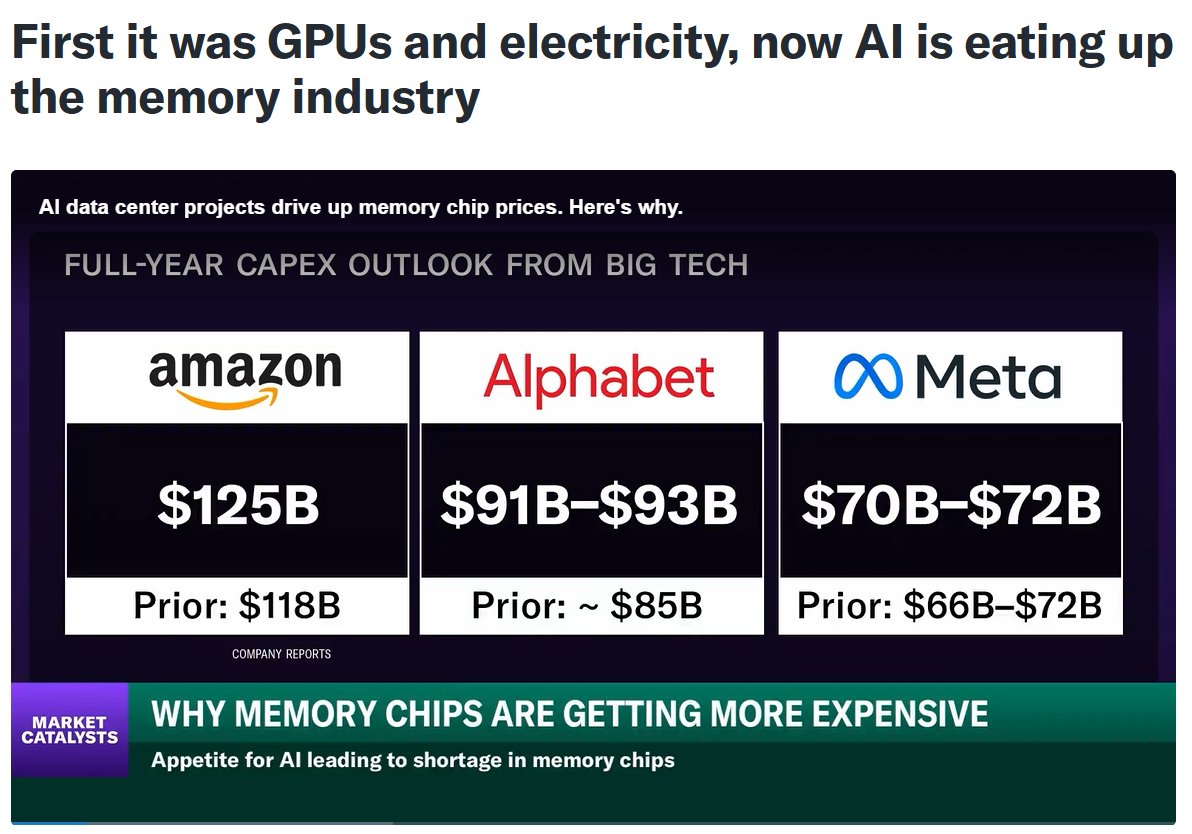

20 Nov 2025

AI just moved from eating GPUs & electricity

→ to devouring the entire memory stack.2025 Big Tech CapEx (latest guidance)

Amazon: $125B (prev ~$118B)

Alphabet: $91–93B (prev ~$85B)

Meta: $70–72B (prev $66–72B)

Hundreds of billions flowing straight into HBM3E, DDR5, CXL, packaging, and foundry lines.

Samsung & SK hynix are already sold out through 2026.

DRAM & NAND bit pricing is exploding.

Yet many memory-adjacent small- and mid-cap names (equipment, materials, packaging, IP) still trade at single-digit EV/EBITDA and <1× book.

The same thing that happened with NAND in 2016–18 and HBM in 2022–23 is happening again — only 10× larger this time.

Owner-mindset move:

While the market obsesses over $800B AI model cap tables, quietly accumulate the undervalued picks-and-shovels trading at 2022 prices.Memory cycle AI capex super-cycle = multi-year compounding setup for patient capital.

#GlobalSmallCapValue #MemorySuperCycle #FundamentalsOnly $nvda $meta $amzn $alphabet

3

69