May 21

Esse blade tá tão forte em qualquer time q se por ele no time da firefly, ela provavelmente vai performar melhor que bucheron kkkkk. Com os novaflare da fugue da lingsha vindo juntos, nós FF mains nem nos preocupamos com qualquer metaswitch pq temos o protagonismo ao nosso favor

1

1

186

May 10

Over the course of my career, 4 conversations have played the biggest role in me going from a recruitment consultant in 2013 to raising $5.3M for @meetdexai last week.

→ 2015: A call that brought me from Next Ventures to Accenture

2 years in as a Senior Recruitment Consultant at Next Ventures, I was on a call with Accenture's internal recruiter about a candidate I was working on placing for them. As we were wrapping up, he asked: "Do you just want to come and do this here?"

I said yes, please, and started recruiting financial services and technology consultants for them a few weeks later. It was my first step into internal recruiting.

→ 2016: A chat that took me from Metaswitch Networks to Improbable

I met @TShipperlee in a coffee shop where we spoke about a role at Improbable. The company had about 50 people. a16z had just led their Series A and it was the hottest ticket in town.

I went in for an interview shortly after, and then spent the next 3 years helping scale it to a 650 person Series B Unicorn with offices across London, San Francisco and Washington DC.

→ 2022: A call that brought me from Sensat to Atomico

In 2022 I was sitting on an offer to lead talent for a T1 VC firm, I gave Dan, the OG of Venture Talent at Atomico a call to learn more about the role.

After a few conversations, Dan asked if I wanted to chat about a role with Atomico and I jumped at the chance. A few weeks later I joined the team, I spent the next two and half years supporting early stage teams all over Europe.

→ 2025: The call that started Dex

@kickso from Concept Ventures called me to make an offer to lead our Pre-Seed round. That call started everything Dex is today.

It was day 3 of our fundraise, and, by the end of that week we closed our $3.1M round from Concept Ventures and a16z speedrun.

--

The journey's been a bit bonkers, but I wouldn't expect anything less.

P.S. The next key conversation in your career might be closer than you think. Dex is ready when you are: meetdex.ai.

3

1

4

841

May 5

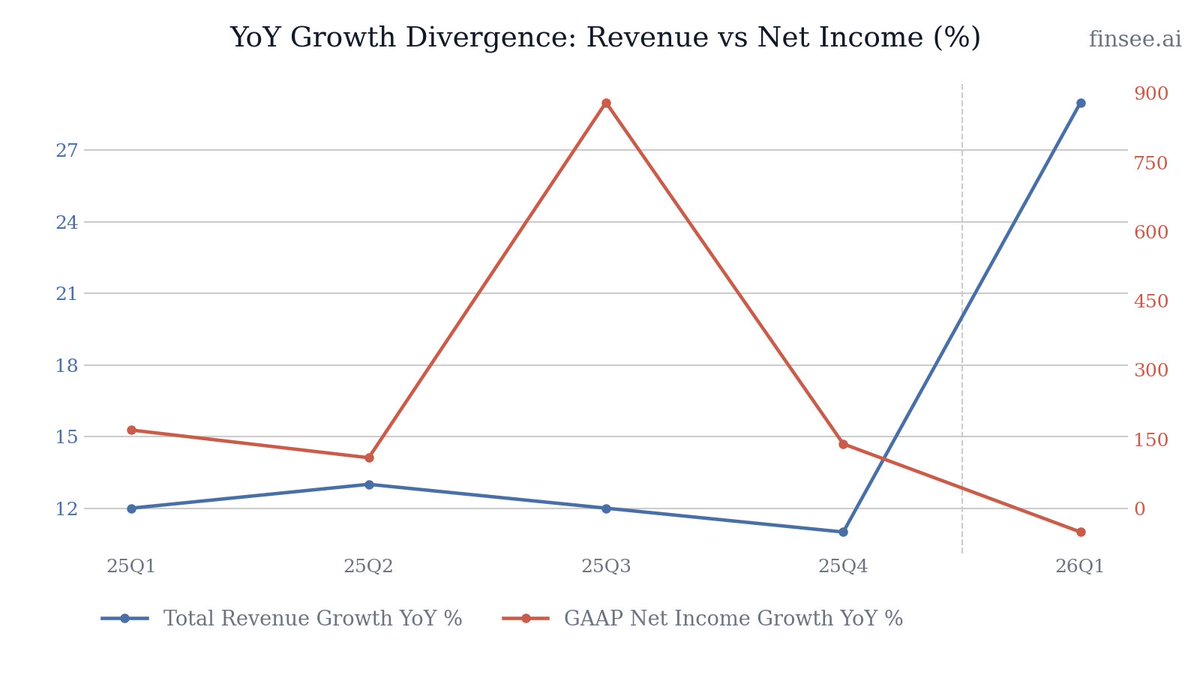

$CXDO Q1 2026 earnings: M&A Re-Accelerates Top Line, But Organic Cracks Emerge

Crexendo's Q1 2026 results are a tale of two realities. On the surface, total revenue growth dramatically accelerated to 29% YoY ($20.7M) driven by the recent acquisition of ESI. However, beneath the M&A headline, GAAP Net Income reversed course, falling 51% to $0.6M due to deal costs and amortization. More alarmingly, the company's core organic growth engine—the Software Solutions segment—is rapidly decelerating. While Non-GAAP metrics show a stable, cash-generating business, investors must ask whether the ESI acquisition is masking an organic slowdown.

Full article with charts - link in bio

🐂 𝐁𝐮𝐥𝐥 𝐂𝐚𝐬𝐞

• 𝐌&𝐀 𝐒𝐭𝐫𝐚𝐭𝐞𝐠𝐲 𝐃𝐞𝐥𝐢𝐯𝐞𝐫𝐢𝐧𝐠 𝐈𝐦𝐦𝐞𝐝𝐢𝐚𝐭𝐞 𝐒𝐜𝐚𝐥𝐞 — The ESI acquisition added significant top-line volume with just one month of contribution in Q1. This pushes Crexendo much closer to its stated $100M annual revenue trajectory.

• 𝐔𝐧𝐝𝐞𝐫𝐥𝐲𝐢𝐧𝐠 𝐂𝐚𝐬𝐡 𝐅𝐥𝐨𝐰 𝐑𝐞𝐦𝐚𝐢𝐧𝐬 𝐑𝐞𝐬𝐢𝐥𝐢𝐞𝐧𝐭 — Despite GAAP margin compression, Adjusted EBITDA grew from $2.7M to $3.2M, and operating cash flow improved to $2.0M. The core business continues to fund its own operations efficiently.

🐻 𝐁𝐞𝐚𝐫 𝐂𝐚𝐬𝐞

• 𝐒𝐨𝐟𝐭𝐰𝐚𝐫𝐞 𝐄𝐧𝐠𝐢𝐧𝐞 𝐢𝐬 𝐒𝐭𝐚𝐥𝐥𝐢𝐧𝐠 — Software Solutions revenue grew just 12% YoY to $7.7M, a severe deceleration from the 33% growth seen a year ago. It also declined sequentially from Q4 2025's $8.3M.

• 𝐈𝐧𝐭𝐞𝐠𝐫𝐚𝐭𝐢𝐨𝐧 𝐖𝐞𝐢𝐠𝐡𝐭𝐬 𝐨𝐧 𝐁𝐨𝐭𝐭𝐨𝐦 𝐋𝐢𝐧𝐞 — Operating expenses surged 36% YoY, heavily outpacing revenue growth. Acquisition-related expenses and elevated amortization have effectively halved GAAP profitability.

⚖️ 𝐕𝐞𝐫𝐝𝐢𝐜𝐭: ⚪

Neutral. The inorganic revenue jump from ESI is impressive, but the sequential decline and YoY deceleration in the high-margin Software Solutions segment is a flashing yellow light for organic growth.

𝐊𝐞𝐲 𝐓𝐡𝐞𝐦𝐞𝐬

🟢 𝐄𝐒𝐈 𝐀𝐜𝐪𝐮𝐢𝐬𝐢𝐭𝐢𝐨𝐧 𝐑𝐞𝐯𝐞𝐫𝐬𝐢𝐧𝐠 𝐓𝐨𝐩-𝐋𝐢𝐧𝐞 𝐒𝐭𝐚𝐠𝐧𝐚𝐭𝐢𝐨𝐧 [NEW]

The $34.7M acquisition of ESI (closed March 1) successfully shifted Crexendo out of its ~12% revenue growth rut. With only one month of ESI included in Q1, Service Revenue accelerated 29% YoY ($10.6M) and Product Revenue surged 141% YoY ($2.4M). As full quarters of ESI roll in, top-line growth should remain highly elevated.

🔴 𝐃𝐚𝐭𝐚 𝐂𝐨𝐧𝐭𝐫𝐚𝐝𝐢𝐜𝐭𝐬 '𝐒𝐭𝐫𝐚𝐭𝐞𝐠𝐢𝐜 𝐌𝐨𝐚𝐭' 𝐍𝐚𝐫𝐫𝐚𝐭𝐢𝐯𝐞 [NEW]

Management has repeatedly called the Software Solutions segment their 'strategic moat' and primary growth engine. The Q1 data directly contradicts this optimistic narrative. Software growth has been decelerating for four straight quarters, crashing to 12% YoY in Q1 2026. More concerning: it declined sequentially from $8.3M in 25Q4 to $7.7M in 26Q1. The organic growth story is losing steam.

🟢 𝐀𝐈 𝐑𝐞𝐜𝐞𝐩𝐭𝐢𝐨𝐧𝐢𝐬𝐭 (𝐂𝐀𝐈𝐑𝐎) 𝐋𝐚𝐮𝐧𝐜𝐡 [NEW]

Crexendo released its AI Receptionist/Orchestrator (CAIRO) this quarter. This represents a tangible transition from legacy unified communications into AI-driven automation. Management previously stated this technology could increase Average Revenue Per Account (ARPA) by 40-50% for adopting SMBs. Early market response was flagged as highly positive.

🔴 𝐆𝐀𝐀𝐏 𝐌𝐚𝐫𝐠𝐢𝐧 𝐂𝐨𝐥𝐥𝐚𝐩𝐬𝐞 [NEW]

Reversing its trend of expanding profitability, operating expenses jumped 36% to $20.3M, outpacing the 29% revenue growth. Income from operations fell more than 60% YoY to $0.44M. While management notes non-GAAP metrics look better when excluding $0.8M in acquisition costs and $1.1M in amortization, the cash costs of integrating ESI are real and pressuring margins.

⚪ 𝐎𝐩𝐞𝐫𝐚𝐭𝐢𝐧𝐠 𝐂𝐚𝐬𝐡 𝐅𝐥𝐨𝐰 𝐒𝐭𝐚𝐛𝐢𝐥𝐢𝐭𝐲

Despite the GAAP noise, cash provided by operations reached $2.0M, an acceleration from $1.2M a year ago. This proves the underlying business remains highly cash-generative, which is vital given the balance sheet leverage used for the ESI acquisition.

🔴 𝐌𝐚𝐜𝐫𝐨 𝐄𝐧𝐯𝐢𝐫𝐨𝐧𝐦𝐞𝐧𝐭 𝐏𝐫𝐞𝐬𝐬𝐮𝐫𝐞𝐬 [NEW]

Management explicitly cautioned that they 'remain disciplined given the broader macro environment.' With software spending tightening universally, Crexendo faces the dual challenge of integrating a major acquisition while navigating a cautious SMB customer base reluctant to sign new telecom contracts.

𝐎𝐭𝐡𝐞𝐫 𝐊𝐏𝐈𝐬

𝐂𝐚𝐬𝐡 𝐚𝐧𝐝 𝐂𝐚𝐬𝐡 𝐄𝐪𝐮𝐢𝐯𝐚𝐥𝐞𝐧𝐭𝐬: $7.2 million

Reversing heavily from $31.4 million at the end of 2025. This 77% drop is the direct result of the $26.2 million net cash outlay for the ESI acquisition. While operating cash flows are positive, the financial cushion is substantially thinner.

𝐏𝐫𝐨𝐝𝐮𝐜𝐭 𝐑𝐞𝐯𝐞𝐧𝐮𝐞: $2.4 million

Accelerating dramatically by 141% YoY. This violently reverses a multi-quarter trend of shrinking hardware sales (down 25% YoY in 25Q3). This spike is almost entirely attributable to acquiring ESI's existing hardware-heavy customer base.

𝐆𝐮𝐢𝐝𝐚𝐧𝐜𝐞

𝐋𝐨𝐧𝐠-𝐭𝐞𝐫𝐦 𝐀𝐧𝐧𝐮𝐚𝐥 𝐑𝐞𝐯𝐞𝐧𝐮𝐞: $100 million trajectory

Management stated they are clearly on a trajectory toward $100M in annual revenue. With Q1 coming in at $20.7M (an $82.8M annualized run-rate), the company needs roughly 20% further growth to hit this milestone. Given that Q1 only contained one month of ESI, hitting a $25M quarterly run rate by 2026 year-end seems structurally plausible if organic growth doesn't stall completely.

𝐊𝐞𝐲 𝐐𝐮𝐞𝐬𝐭𝐢𝐨𝐧𝐬

𝐒𝐨𝐟𝐭𝐰𝐚𝐫𝐞 𝐒𝐨𝐥𝐮𝐭𝐢𝐨𝐧𝐬 𝐃𝐞𝐜𝐞𝐥𝐞𝐫𝐚𝐭𝐢𝐨𝐧

Software Solutions revenue fell sequentially from $8.3M to $7.7M, and YoY growth decelerated to 12%. How much of this is macro-driven versus a slowdown in legacy Metaswitch/BroadSoft conversions?

𝐎𝐫𝐠𝐚𝐧𝐢𝐜 𝐯𝐬. 𝐈𝐧𝐨𝐫𝐠𝐚𝐧𝐢𝐜 𝐆𝐫𝐨𝐰𝐭𝐡

Total revenue grew 29% YoY. If we strip out the exactly one month of contribution from ESI, what was the organic revenue growth rate for the quarter?

𝐄𝐒𝐈 𝐈𝐧𝐭𝐞𝐠𝐫𝐚𝐭𝐢𝐨𝐧 𝐂𝐨𝐬𝐭𝐬

Operating expenses grew 36% this quarter. Should we expect integration and acquisition-related expenses to remain elevated through the remainder of 2026, or was Q1 the peak?

𝐂𝐀𝐈𝐑𝐎 𝐌𝐨𝐧𝐞𝐭𝐢𝐳𝐚𝐭𝐢𝐨𝐧

With the CAIRO AI Receptionist now released, what specific attach rates are you targeting within your existing customer base by year-end?

2

4

1,091

7 Sep 2025

It’s football night (not) in America for GBFC legends @jon_dv, @officialjoef and @Kyriball. Photo credit to GBFC super fan, our Alianza* ally, @jamescox198

*Formerly Metaswitch, a Microsoft company

1

3

256

27 Aug 2025

2013

1. 🇺🇸 id8 Group R2 Studios

2. 🇺🇸 Pando Networks

3. 🇺🇸 MetricsHub

4. 🇨🇭 Netbreeze

5. 🇨🇦 InRelease

6. 🇫🇮 Nokia mobile phones unit

7. 🇦🇹 HLW Software

8. 🇺🇸 Apiphany

2014

1.🇺🇸 Parature

2. 🇳🇿 GreenButton

3. 🇫🇷 Capptain

4. 🇫🇷 SyntaxTree

4. 🇮🇳 InMage

5. 🇨🇦 Inception Mobile Inc.

6. 🇸🇪 Mojang Studios

7.. 🇮🇱 Aorato

8.. 🇺🇸 Acompli

9. 🇩🇪 HockeyApp

2015

1. 🇮🇱 Equivio

2. 🇺🇸 Revolution Analytics

3. 🇺🇸 Sunrise Atelier, Inc.

4. 🇮🇱 N-trig

5. 🇺🇸 LiveLoop

6. 🇨🇦 Datazen Software, Inc.

7. 🇩🇪 6 Wunderkinder GmbH

8. 🇺🇸 BlueStripe Software

9. 🇺🇸 FieldOne Systems LLC

10. 🇮🇱 Adallom

11. 🇺🇸 Incent Games, LLC

12. 🇺🇸 VoloMetrix, Inc.

13. 🇺🇸 Double Labs, Inc.

14. 🇨🇦 Adxstudio Inc.

15. 🇮🇪 Havok

16. 🇺🇸 Mobile Data Labs, Inc.

17. 🇮🇱 Secure Islands Technologies Ltd.

18. 🇺🇸 Metanautix

19. 🇺🇸 Talko, Inc.

2016

1. 🇦🇺 Event Zero

2. 🇫🇮 Teacher Gaming LLC

3. 🇬🇧 SwiftKey

4. 🇨🇦 Groove

5. 🇺🇸 Xamarin

6. 🇮🇹 Solair

7. 🇺🇸 Wand Labs

8. 🇺🇸 Beam

9. 🇺🇸 Genee

10. 🇺🇸 LinkedIn

2017

1. 🇨🇦 Maluuba

2. 🇸🇪 Simplygon

3. 🇺🇸 Deis

4. 🇺🇸 Intentional Software

5. 🇮🇱 Hexadite

6. 🇮🇱 Cloudyn

7. 🇺🇸 Cycle Computing

8. 🇺🇸 AltspaceVR

9. 🇺🇸 SWNG

2018

1. 🇺🇸 Avere Systems

2. 🇺🇸 Playfab

3. 🇺🇸 Semantic Machines

4. 🇬🇧 Ninja Theory

5. 🇺🇸 Undead Labs

6. 🇨🇦 Compulsion Games

7. 🇬🇧 Playground Games

8. 🇺🇸 Flipgrid

9. 🇺🇸 Bonsai

10. 🇺🇸 Lobe

11. 🇺🇸 Glint

12. 🇺🇸 GitHub

13. 🇺🇸 inXile Entertainment

14. 🇺🇸 Obsidian Entertainment

15. 🇺🇸 XOXCO

16. 🇺🇸 FSLogix

17. 🇺🇸 Spectrum

2019

1. 🇺🇸 Citus Data

2. 🇺🇸 DataSense

3. 🇺🇸 Express Logic

4. 🇬🇧 Dependabot

5. 🇺🇸 Drawbridge

6. 🇺🇸 Double Fine Productions

7. 🇺🇸 Pull Panda

8. 🇺🇸 BlueTalon

9. 🇺🇸 PromoteIQ

10. 🇺🇸 jClarity

11. 🇺🇸 Movere

12. 🇺🇸 Semmle

13. 🇨🇦 Mover

2020

1. 🇺🇸 npm

2. 🇺🇸 Affirmed Networks

3. 🇬🇧 Metaswitch Networks

4. 🇬🇧 Softomotive

5. 🇺🇸 ADRM Software

6. 🇺🇸 CyberX

7. 🇺🇸 Orions Systems

8. 🇺🇸 ZeniMax Media

9. 🇺🇸 Smash. gg

2021

1. 🇺🇸 The Marsden Group

2. 🇺🇸 Nuance Communications

3. 🇩🇪 Kinvolk

4. 🇺🇸 ReFirm Labs

5. 🇺🇸 AT&T Technology Network Cloud

6. 🇺🇸 RiskIQ

7. 🇺🇸 CloudKnox

8. 🇺🇸 Suplari

9. 🇺🇸 Peer5

10. 🇦🇺 Clipchamp

11. 🇺🇸 TakeLessons

12. 🇺🇸 Ally. io

13. 🇺🇸 Clear Software

14. 🇨🇦 Two Hat

15. 🇺🇸 Xandr

2022

1. 🇺🇸 Activision Blizzard

2. 🇮🇱 Oribi

3. 🇳🇱 Minit

4. 🇺🇸 Miburo

5. 🇬🇧 Lumenisity

2023

1. 🇺🇸 Fungible

2. 🇭🇺 Nemesys Games

2024

1. 🇺🇸 Inflection AI

Source: Microsoft, Wikipedia

4

10

856

15 Jul 2025

2013

1. 🇺🇸 id8 Group R2 Studios

2. 🇺🇸 Pando Networks

3. 🇺🇸 MetricsHub

4. 🇨🇭 Netbreeze

5. 🇨🇦 InRelease

6. 🇫🇮 Nokia mobile phones unit

7. 🇦🇹 HLW Software

8. 🇺🇸 Apiphany

2014

1.🇺🇸 Parature

2. 🇳🇿 GreenButton

3. 🇫🇷 Capptain

4. 🇫🇷 SyntaxTree

4. 🇮🇳 InMage

5. 🇨🇦 Inception Mobile Inc.

6. 🇸🇪 Mojang Studios

7.. 🇮🇱 Aorato

8.. 🇺🇸 Acompli

9. 🇩🇪 HockeyApp

2015

1. 🇮🇱 Equivio

2. 🇺🇸 Revolution Analytics

3. 🇺🇸 Sunrise Atelier, Inc.

4. 🇮🇱 N-trig

5. 🇺🇸 LiveLoop

6. 🇨🇦 Datazen Software, Inc.

7. 🇩🇪 6 Wunderkinder GmbH

8. 🇺🇸 BlueStripe Software

9. 🇺🇸 FieldOne Systems LLC

10. 🇮🇱 Adallom

11. 🇺🇸 Incent Games, LLC

12. 🇺🇸 VoloMetrix, Inc.

13. 🇺🇸 Double Labs, Inc.

14. 🇨🇦 Adxstudio Inc.

15. 🇮🇪 Havok

16. 🇺🇸 Mobile Data Labs, Inc.

17. 🇮🇱 Secure Islands Technologies Ltd.

18. 🇺🇸 Metanautix

19. 🇺🇸 Talko, Inc.

2016

1. 🇦🇺 Event Zero

2. 🇫🇮 Teacher Gaming LLC

3. 🇬🇧 SwiftKey

4. 🇨🇦 Groove

5. 🇺🇸 Xamarin

6. 🇮🇹 Solair

7. 🇺🇸 Wand Labs

8. 🇺🇸 Beam

9. 🇺🇸 Genee

10. 🇺🇸 LinkedIn

2017

1. 🇨🇦 Maluuba

2. 🇸🇪 Simplygon

3. 🇺🇸 Deis

4. 🇺🇸 Intentional Software

5. 🇮🇱 Hexadite

6. 🇮🇱 Cloudyn

7. 🇺🇸 Cycle Computing

8. 🇺🇸 AltspaceVR

9. 🇺🇸 SWNG

2018

1. 🇺🇸 Avere Systems

2. 🇺🇸 Playfab

3. 🇺🇸 Semantic Machines

4. 🇬🇧 Ninja Theory

5. 🇺🇸 Undead Labs

6. 🇨🇦 Compulsion Games

7. 🇬🇧 Playground Games

8. 🇺🇸 Flipgrid

9. 🇺🇸 Bonsai

10. 🇺🇸 Lobe

11. 🇺🇸 Glint

12. 🇺🇸 GitHub

13. 🇺🇸 inXile Entertainment

14. 🇺🇸 Obsidian Entertainment

15. 🇺🇸 XOXCO

16. 🇺🇸 FSLogix

17. 🇺🇸 Spectrum

2019

1. 🇺🇸 Citus Data

2. 🇺🇸 DataSense

3. 🇺🇸 Express Logic

4. 🇬🇧 Dependabot

5. 🇺🇸 Drawbridge

6. 🇺🇸 Double Fine Productions

7. 🇺🇸 Pull Panda

8. 🇺🇸 BlueTalon

9. 🇺🇸 PromoteIQ

10. 🇺🇸 jClarity

11. 🇺🇸 Movere

12. 🇺🇸 Semmle

13. 🇨🇦 Mover

2020

1. 🇺🇸 npm

2. 🇺🇸 Affirmed Networks

3. 🇬🇧 Metaswitch Networks

4. 🇬🇧 Softomotive

5. 🇺🇸 ADRM Software

6. 🇺🇸 CyberX

7. 🇺🇸 Orions Systems

8. 🇺🇸 ZeniMax Media

9. 🇺🇸 Smash. gg

2021

1. 🇺🇸 The Marsden Group

2. 🇺🇸 Nuance Communications

3. 🇩🇪 Kinvolk

4. 🇺🇸 ReFirm Labs

5. 🇺🇸 AT&T Technology Network Cloud

6. 🇺🇸 RiskIQ

7. 🇺🇸 CloudKnox

8. 🇺🇸 Suplari

9. 🇺🇸 Peer5

10. 🇦🇺 Clipchamp

11. 🇺🇸 TakeLessons

12. 🇺🇸 Ally. io

13. 🇺🇸 Clear Software

14. 🇨🇦 Two Hat

15. 🇺🇸 Xandr

2022

1. 🇺🇸 Activision Blizzard

2. 🇮🇱 Oribi

3. 🇳🇱 Minit

4. 🇺🇸 Miburo

5. 🇬🇧 Lumenisity

2023

1. 🇺🇸 Fungible

2. 🇭🇺 Nemesys Games

2024

1. 🇺🇸 Inflection AI

Source: Microsoft, Wikipedia

2

7

576

3/3

Our work to provide these sessions to the community is only possible thanks to the funding provided by The National League Trust and our donors including Alianza, formerly Metaswitch and Pellings Architects.

2

5

1,969

2 Jul 2025

There are 2 reasoning for this.

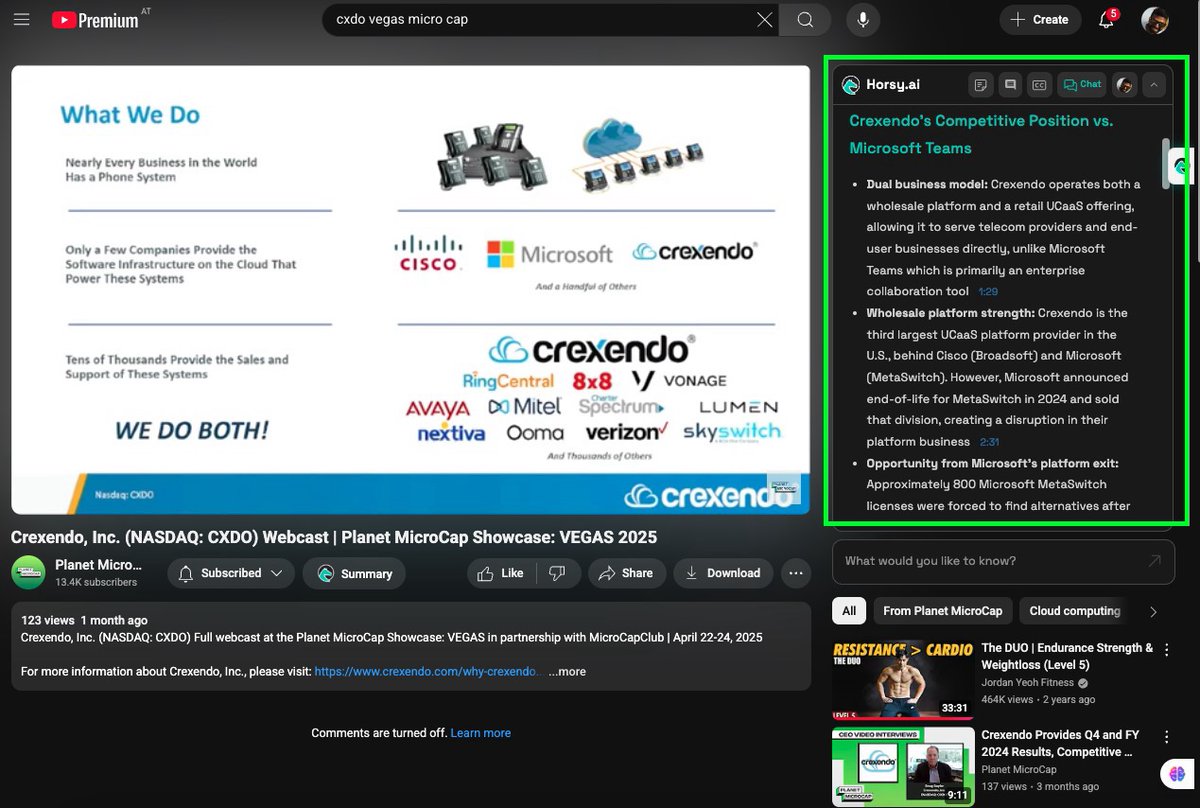

1. Crexendo focuses on SMBs and channel partners who want a customizable, branded communications solutions, something Microsoft doesn’t emphasize

In fact, Microsoft just shut down Metaswitch after acquiring them 4 years ago.

2. Crexendo decided to go after session based pricing instead of per seat. This drives cost down according to them to 1/3 pricing. Do check out also my tweet about Car sharing wars in Berlin and how km based pricing was odd one out, but won it eventually

These questions are well answered in the company's presentation in small cap vegas. chk it out. I use Horsy AI chrome extension to get to answers quicker.

youtube.com/watch?v=WF07uN3P…

1

2

53

5 Jun 2025

My thoughts on drafting for the metaswitch next patch:

Vs jax: Gnar, renek(if ur good on gim)Asol top, camille,(kayle if ur good)

Vs aatrox: conq fiora, K'sante, kennen renek,

Vs rammus/mundo: cam ambessa fio gwen and udyr

Vs fiora:dodge

2

2

658

11 Mar 2025

Honored for @Crexendo's @Netsapiens Platform to win @tmcnet's 2025 Product of the Year Award! We are focused on continuing to deliver value and innovation for all of our licensee community!

#CSP #ITSP #ILEC #MSP #SP #NTCA #MetaSwitch #Broadsoft #AI #UCaaS #Innovation $CXDO

10 Mar 2025

🚀 𝐁𝐑𝐄𝐀𝐊𝐈𝐍𝐆 𝐍𝐄𝐖𝐒: NetSapiens Platform Wins 2025 Product of the Year! 🏆🎉

Marking our Fifth Consecutive Win and 27th Industry Accolade!

Read the Full PR: bit.ly/43xVVdI

#TMC #AI #CloudCommunications #ProductOfTheYear #Crexendo #PoweredByNetSapiens

3

179

4 Mar 2025

$CXDO Crexendo reports Q4 EPS 6c, consensus 5c

Reports Q4 revenue $16.2M, consensus $15.64M. "Crexendo delivered another outstanding performance in the fourth quarter and full year of 2024, with double-digit revenue growth, GAAP profitability, and strong cash flow. These results are due to the continued efforts of our team, who continue to deliver strong efforts and results. I am extremely excited by our results across the board. We are seeing tremendous growth in our software solutions segment, which grew 30% year over year fueled by many opportunities being created by our two largest competitors in that sector, Cisco and Microsoft, not focusing on and enhancing that part of their business.

In fact, Microsoft recently announced the sale of its Metaswitch platform division, causing further instability and concern in the industry. This disruption plays to our strengths-a highly stable, adaptable platform backed by a long history of reliability. We believe this continued upheaval presents a significant opportunity for us. Additionally, we are seeing strong momentum in our telecom services sales, with continued growth driven by the integration of artificial intelligence applications designed to support small, mid-size, and enterprise-level customers," said Jeff Korn, Crexendo CEO.

2

317

4 Mar 2025

$CXDO reported very solid earnings.

Adj EPS $0.06 Beats $0.05 Estimate ✅

Sales $16.24M Beat $15.64M Estimate ✅

Biggest standout was the software segment has accelerated and is now growing over 30% YoY.

The company today is generating solid cash flow, and this will only accelerate once they finish up the cloud migration to Oracle.

"Crexendo delivered another outstanding performance in the fourth quarter and full year of 2024, with double-digit revenue growth, GAAP profitability, and strong cash flow. These results are due to the continued efforts of our team, who continue to deliver strong efforts and results. I am extremely excited by our results across the board. We are seeing tremendous growth in our software solutions segment, which grew 30% year over year fueled by many opportunities being created by our two largest competitors in that sector, Cisco and Microsoft, not focusing on and enhancing that part of their business. In fact, Microsoft recently announced the sale of its Metaswitch platform division, causing further instability and concern in the industry. This disruption plays to our strengths-a highly stable, adaptable platform backed by a long history of reliability. We believe this continued upheaval presents a significant opportunity for us. Additionally, we are seeing strong momentum in our telecom services sales, with continued growth driven by the integration of artificial intelligence applications designed to support small, mid-size, and enterprise-level customers," said Jeff Korn, Crexendo Chief Executive Officer.

Korn continued "We have substantial competitive advantages that we will continue to leverage to drive conversions to our platform and expand our market presence. Our relentless focus on innovation, customer service, and strategic growth is paying off, and I firmly believe the future has never been more exciting for Crexendo. We remain committed to investing in our technology, expanding our offerings, and delivering best-in-class solutions to our customers. I look forward to continued strong momentum as we build on our success in 2025 and beyond."

4 Mar 2025

$CXDO Crexendo Announces Record Fourth Quarter and Fiscal Year 2024 Results

stocktitan.net/news/CXDO/cre…

7

14

60

19,975

4 Mar 2025

#Microsoft has finalized its sale of #Metaswitch to #Alianza as it looks to streamline and refocus its telecoms portfolio. 🌐 🖥️

ccn.com/news/business/alianz…

538

4 Mar 2025

CEO and CPO chatting about the most interesting comms acquisition in 2025 at #MWC25. Alianza acquired Metaswitch Networks today. buff.ly/CJToVyU

3

412

18 Feb 2025

$CXDO also been a good one for me.

Steadily climbing up from my first buy in June.

Few big catalysts coming this year:

1) Oracle Cloud Migration - Save a few million a year from it

2) More $MSFT Metaswitch partners migrations

3) Aggressive international expansion ramping up

Likely won’t be a quick multi bagger, but happy it’s my #1 and view it as a safe bet to outperform the market.

7

8

31

5,011

14 Feb 2025

Metaswitch going end of life is causing many service providers to seek another platform that will be here for the long haul and offer good customer support and features.

$CXDO platform is ranked #1 across 248 G2 reviews for things like support, service, and quality, which is ultimately going to cause a lot of them to seek out a migration to their platform.

Metaswitch was sold to Alianza, and the promise is “AI powered cloud future”, which is really just saying “We are going to force you to migrate to us” because I highly doubt they will upgrade MetaSwitch with the acquisition.

Will be interesting to hear commentary the next earnings around the Metaswitch being sold, and how many service providers are still looking to migrate to the NetSapiens platform.

11 Feb 2025

The #Metaswitch EOL wasn’t just a disruption for Akabis—it was another twist in an exhausting cycle of migrations & uncertainty. After one major move, they faced yet another with MaX UC’s discontinuation.

Watch the full webinar: tinyurl.com/ffdevavb

#PoweredByNetSapiens

1

22

3,842

11 Feb 2025

The #Metaswitch EOL wasn’t just a disruption for Akabis—it was another twist in an exhausting cycle of migrations & uncertainty. After one major move, they faced yet another with MaX UC’s discontinuation.

Watch the full webinar: tinyurl.com/ffdevavb

#PoweredByNetSapiens

1

4

4,401

22 Jan 2025

Another great episode of Telco in 20 this week from @totogi CEO, @TelcoDR, who sat down with Alianza Founder & CEO, Brian Beutler, to discuss the company's game-changing Metaswitch acquisition. Tune in to learn more: tinyurl.com/54utt5at

2

2

256

20 Jan 2025

🚀 Looking To Navigate The Transition From #Metaswitch MaX UC to Another Platform? - Get This eBook! 🚀

🔗 bit.ly/4gcXdP4

#UCaaS #MSP #eBook #UC #PoweredByNetsapiens $CXDO

11 Dec 2024

🚀 Looking To Navigate The Transition From Metaswitch MaX UC to Another Platform? - Get This eBook! 🚀

🔗 [Download Now] bit.ly/4gcXdP4

#MetaswitchMigration #UCaaS #ServiceProviders #eBook #FutureProof #Crexendo #PoweredByNetsapiens

3

177