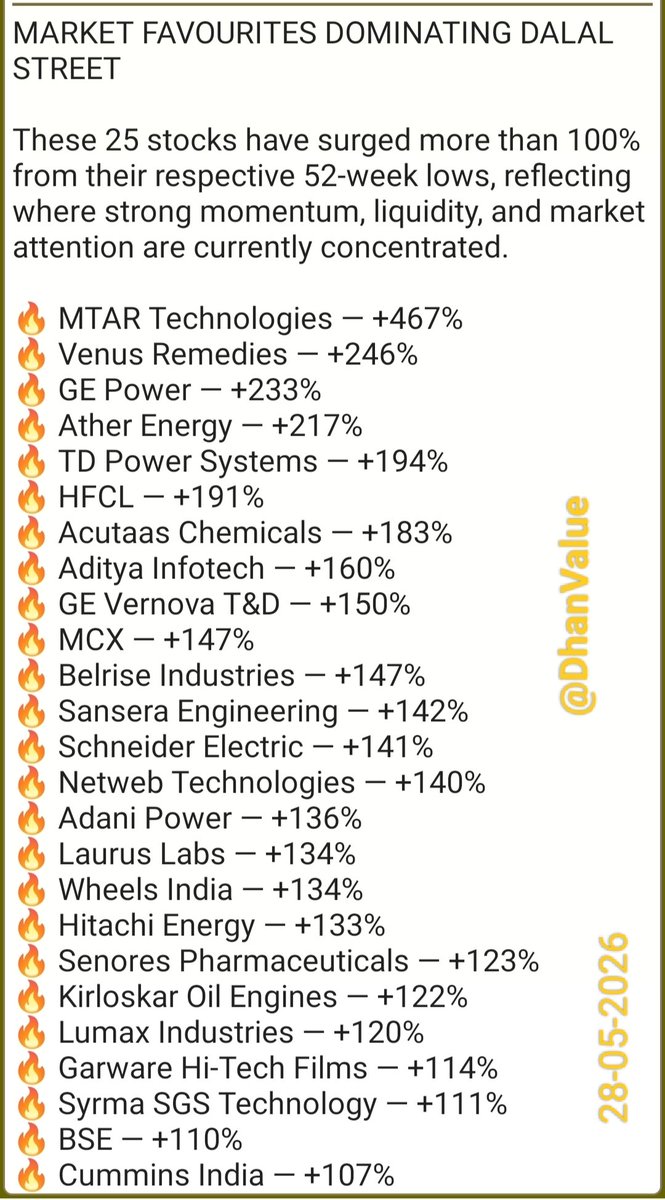

Netweb Technologies India Ltd Concall Summary for Q4FY26

CORE HIGHLIGHT

- Emerging leader in sovereign AI infrastructure

MANAGEMENT COMMENTARY

- FY26 described as landmark year

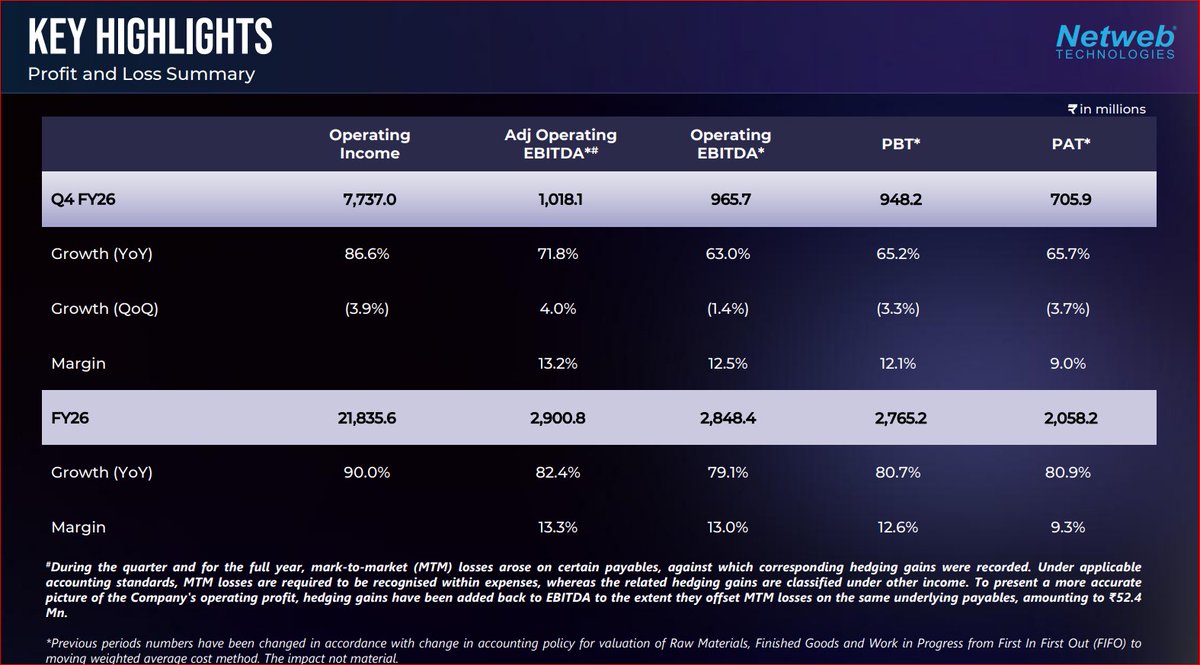

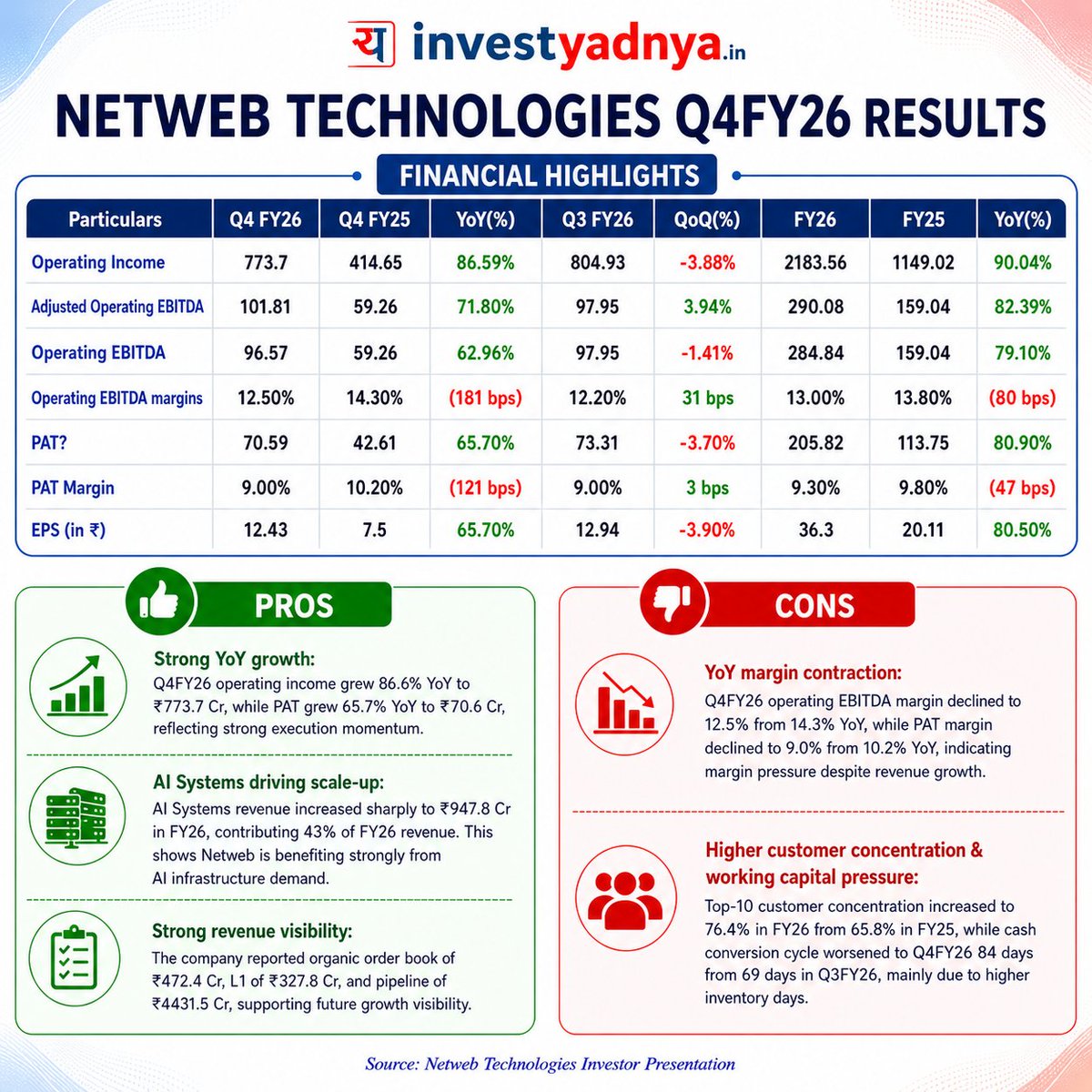

- Revenue growth reached 90% YoY

- AI segment growth remained exceptional

- Entered FY27 from strong position

- In-house R&D remained key priority

- “Make in India” strategy emphasized

- Sovereign AI infrastructure gaining importance

FUTURE OUTLOOK & GUIDANCE

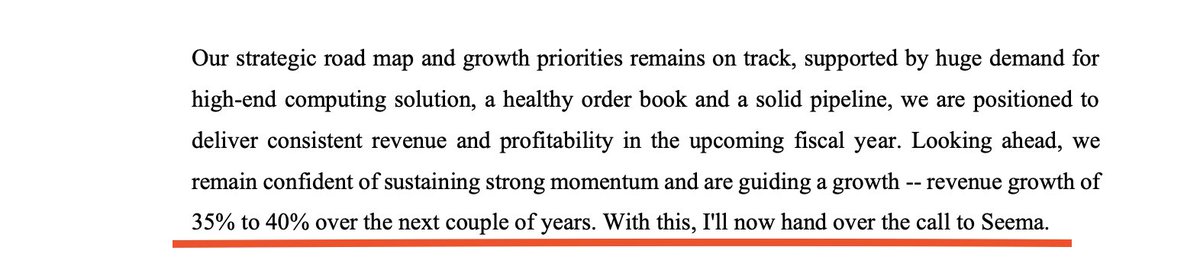

- Revenue growth guidance: 35–40%

- EBITDA margin guidance: 13–14%

- FY27 opening order book: ₹2,100 Cr

- L1-inclusive order book: ₹2,400 Cr

- Strategic orders executed over quarters

- Total pipeline visibility: ₹6,500 Cr

INDUSTRY & MACRO TRENDS

- Sovereign AI becoming strategic necessity

- India AI Mission driving demand

- GPU infrastructure demand accelerating rapidly

- Global AI demand remains strong

- High-end compute demand expanding globally

- Data sovereignty gaining importance worldwide

COMPETITIVE POSITIONING

- India’s only fullstack domestic provider

- Focused on sovereign enterprise demand

- Not targeting hyperscaler segment currently

- Capability-driven technology positioning maintained

- Expertise in liquid-cooled architectures

- High-density GPU systems differentiation

RISKS & CONCERNS

- Inventory levels increased significantly

- Critical component sourcing remains challenge

- Forex MTM losses impacted earnings

- Strategic order spillovers delayed revenues

- Exports remain relatively small currently

- Global supply-chain pressure persists

GROWTH DRIVERS & STRATEGY

AI INFRASTRUCTURE

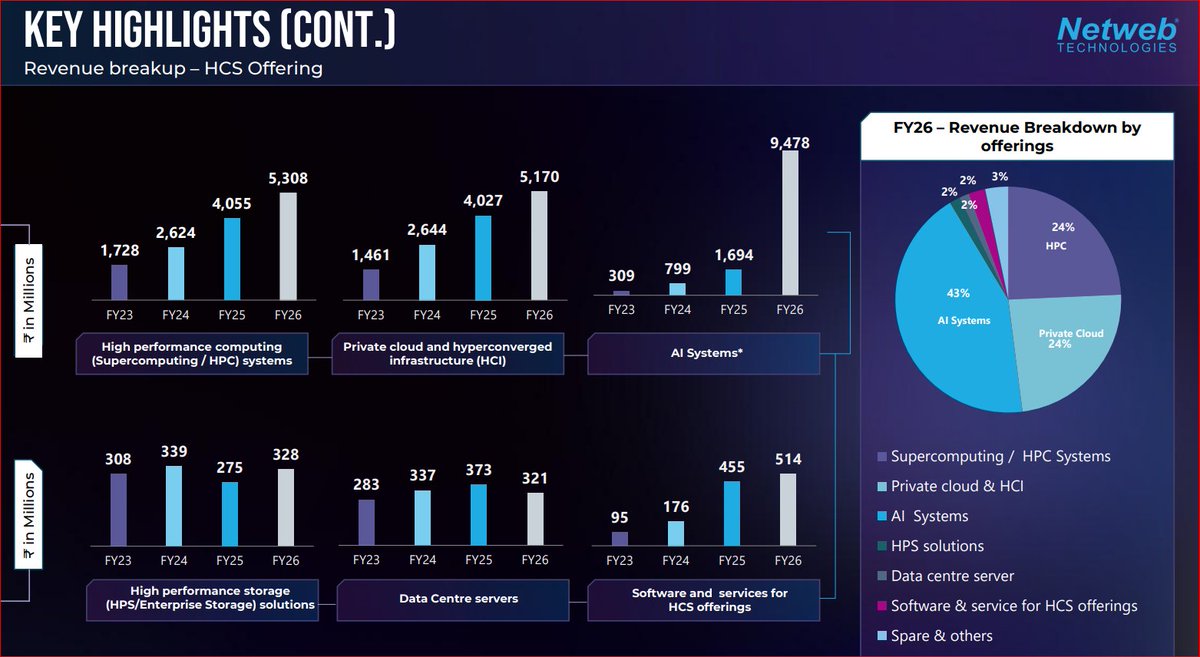

- AI contributes 43.4% revenues

- AI demand scaling aggressively

- National AI projects driving momentum

- Sovereign compute opportunity expanding rapidly

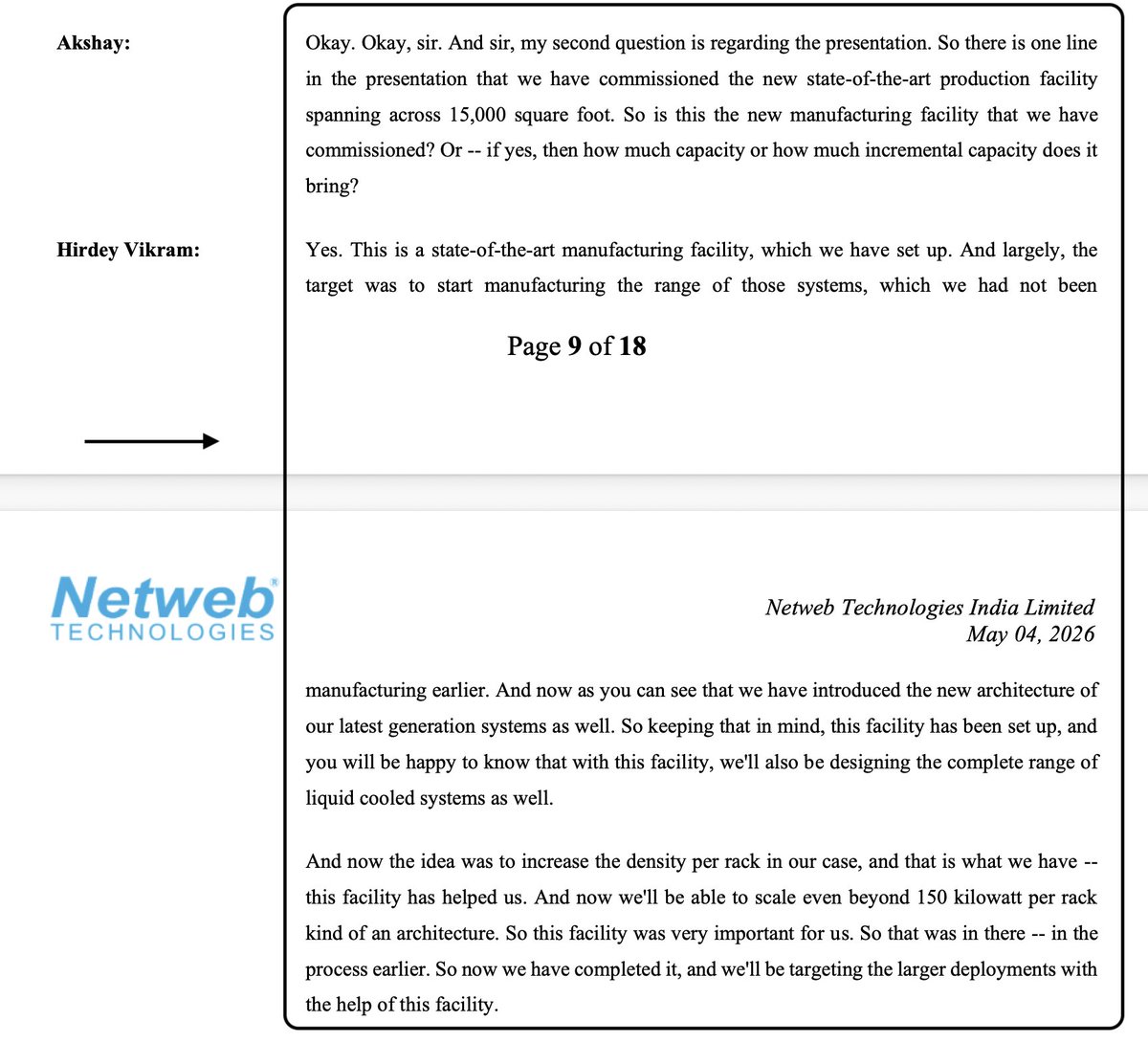

NEW FACILITY EXPANSION

- 15,000 sq.ft facility commissioned

- Facility supports liquid-cooled systems

- Advanced architectures manufacturing enhanced

R&D & TECHNOLOGY

- Strong in-house design capabilities

- Rapid adoption of Nvidia architectures

- Focus on risk-based architectures

- High-performance systems innovation continuing

LARGE-SCALE EXECUTION

- National-scale project execution validated

- Strategic orders enhancing credibility

- Complex deployments strengthening positioning

PRODUCT MIX & PORTFOLIO

- AI systems became largest segment

- HPC continues strong growth momentum

- Private cloud demand remains robust

- Focus shifting toward high-density racks

- Moving away from low-margin products

- 150kW rack capabilities being developed

FINANCIAL PERFORMANCE

FY26

- Revenue: ₹21,836 Mn (↑90% YoY)

- PAT: ₹2,058 Mn (↑81% YoY)

- PAT Margin: 9.3%

- Strong profitability and growth achieved

BALANCE SHEET & CASH FLOW

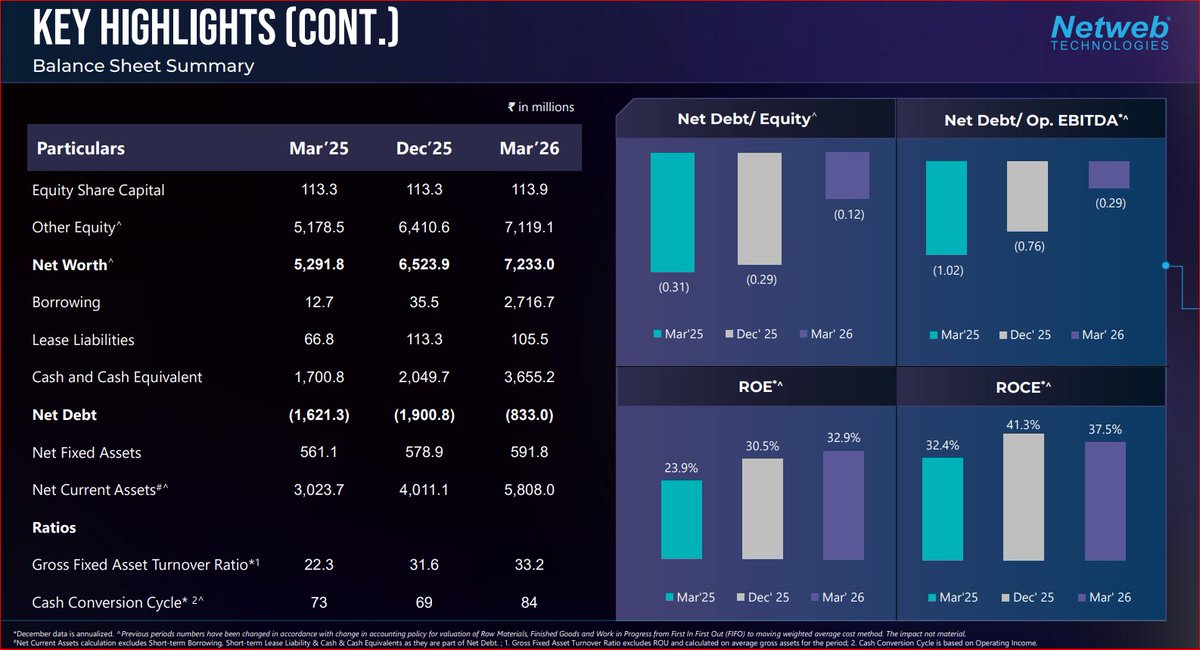

- Zero net debt company

- Net free cash: ₹833 Mn

- Operating cash flow: ₹1,715 Mn

- Strong liquidity position maintained

EFFICIENCY METRICS

- ROE stood at 32.9%

- ROCE stood at 37.5%

- Capital efficiency remained robust

KEY INSIGHT

- AI infrastructure becoming primary growth driver

OUTLOOK

- Strong order visibility supports growth

- AI demand outlook remains robust

- Sovereign AI spending likely accelerating

- Margin profile expected remaining stable

- Supply-chain availability remains monitorable

CONCLUSION

- FY26 marked transformational growth phase

- AI systems driving business transition

- Strong order book provides visibility

- Balance-sheet remains debt-free and strong

- Positioned strongly for India AI expansion

#Netweb #Netwebtechnologies #stockmarket

@gaze_observer @netwebtech

Netweb Conference Call Highlights | Q4 FY2026 🔥🔥🔥

The company is rapidly positioning itself as one of the strongest emerging players in India’s AI infrastructure and high-performance computing ecosystem.

One of the biggest highlights was the explosive growth in the AI systems business, which grew nearly 460% YoY in FY26 and now contributes more than 43% of the company’s total operating revenue. This clearly shows how rapidly the revenue mix is shifting towards AI-led infrastructure demand.

Management repeatedly highlighted that demand for sovereign AI infrastructure in India is becoming extremely strong, especially with the government’s increasing focus on AI compute capacity and large-scale GPU deployment across the country.

The company started FY27 with:

▪ ₹2,100 crore firm order book

▪ ₹2,400 crore order book including L1 orders

▪ ₹4,400 crore healthy pipeline

Out of this, nearly ₹1,600 crores comes from strategic orders, while the remaining business is organic in nature.

Management expects nearly 60% pipeline conversion over the next 18–24 months, which indicates strong medium-term visibility.

Another important point was that the company guided for 35–40% revenue growth in FY27 for the core business itself, excluding large strategic order execution. This suggests that the base business itself is growing aggressively.

Despite strong growth, management expects EBITDA margins to remain stable around 13–14% over the next few years.

One thing that stood out strongly was the company’s in-house capability stack.

Management repeatedly emphasized:

▪ In-house R&D

▪ In-house design capability

▪ In-house manufacturing

▪ Ability to adapt to custom AI architectures

This positions the company strongly within India’s “Make in India” AI and compute infrastructure theme.

The company also commissioned a new 15,000 sq. ft. state-of-the-art manufacturing facility, which enhances capabilities around:

▪ Liquid cooling systems

▪ High-density racks above 150 kW

▪ Next-generation AI infrastructure deployments

Management clarified that the company is capability-driven rather than capacity-driven, and current utilization levels remain around 65–70%, leaving room for scaling.

Another important point was around AI demand itself.

The company highlighted that both AI training and AI inference workloads are creating opportunities simultaneously, and rising inference demand is becoming an additive growth driver rather than replacing existing demand.

The Private Cloud and HPC businesses also continue to grow strongly, although their revenue contribution appears lower due to the exponential growth in the AI systems segment.

Interestingly, management also highlighted that India is currently more of a sovereign compute market rather than a hyperscaler-led market, though the company remains open to future opportunities involving players like Amazon or Microsoft if required.

Operationally, the company continues to maintain a very strong balance sheet position:

▪ Zero net debt company

▪ ₹833 million net free cash

▪ Healthy ROE of 32.9%

▪ ROCE of 37.5%

The increase in short-term borrowings during the quarter was clarified as temporary working capital funding for large strategic orders and governed by RBI/covenant-related requirements.

Another important detail was the promoter stake sale.

Management clarified that the 4% promoter stake sale was done only to improve stock liquidity, and no further dilution is planned for the next 12 months.

The company also expects:

▪ Stable cash conversion cycle within 80–110 days

▪ Routine FY27 capex of only ₹20–25 crores

▪ Strong domestic demand to remain the immediate priority before exports

Overall, management commentary strongly suggests that the company is positioning itself at the center of India’s rapidly expanding AI infrastructure ecosystem with strong order visibility, scalable in-house capabilities, and aggressive participation in sovereign AI deployment opportunities.

Disclaimer:

For educational and study purposes only.

Not a buy/sell recommendation.