1. Netweb Technologies India Ltd🔖 (Pure-play HPC/AI servers, private cloud, data centre infra)

💡Specifications: High-performance computing, AI systems, storage, DC servers. Strong in NVIDIA/Blackwell deployments. #netwebtech

1

1

8

1,092

Jun 13

We are pleased to announce that @netwebtech has joined the #BFSITechConclave as the Exhibition Partner!

As one of India’s leading providers of high-performance computing (HPC), AI infrastructure, servers, storage, and data center solutions, #Netweb delivers powerful, scalable, and “Make in India” compliant technologies. These solutions help BFSI organizations accelerate AI adoption, strengthen data infrastructure, and drive digital transformation with high-performance systems tailored for the industry’s demanding needs.

We look forward to showcasing their cutting-edge HPC and AI solutions at the exhibition.

See you at the BFSI Technology Conclave!

Event Details: 19 & 20 June 2026 | Radisson Blu Plaza Resort & Convention Centre, Karjat

Register Now → t.ly/19bfsikX

@srikrp @NivedanPrakash @H_Y_DESAI @ravignair @Prabhasjha3110 @AparnaTawade

1

252

Jun 12

NETWEB TECH - 1 of the strongest chart / techq i can see in todays market

Retracining from .618 fib of last swing run with pin bar formation

good strong reversal candle with good volume

#netweb #netwebtech #datacentre #AI #chartsdontlie #nifty #nifty50

x.com/luvjain75/status/20643…

Jun 9

NETWEB TECH - update

- Showing recovery sign from retracemnt level of around .618 of current move

- stock formed a bullish harami pattern around these level

- GOOD 1 or 2 day follow up required to take stock new high

- Also stock also has taken support fro 50EMA

#netweb #chartsdontlie #netwebtech #datacentre #ai #AI

1

10

713

Jun 11

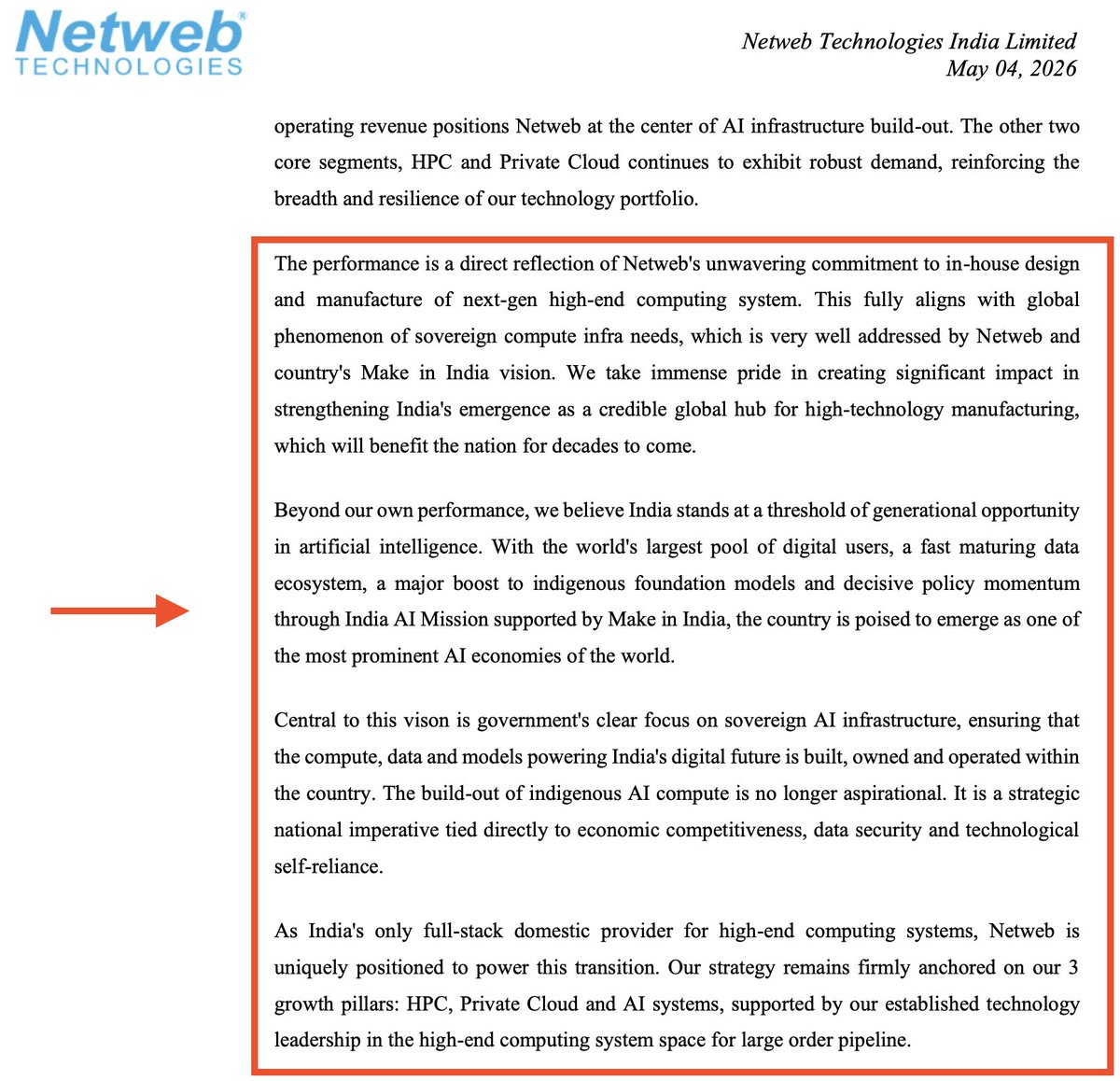

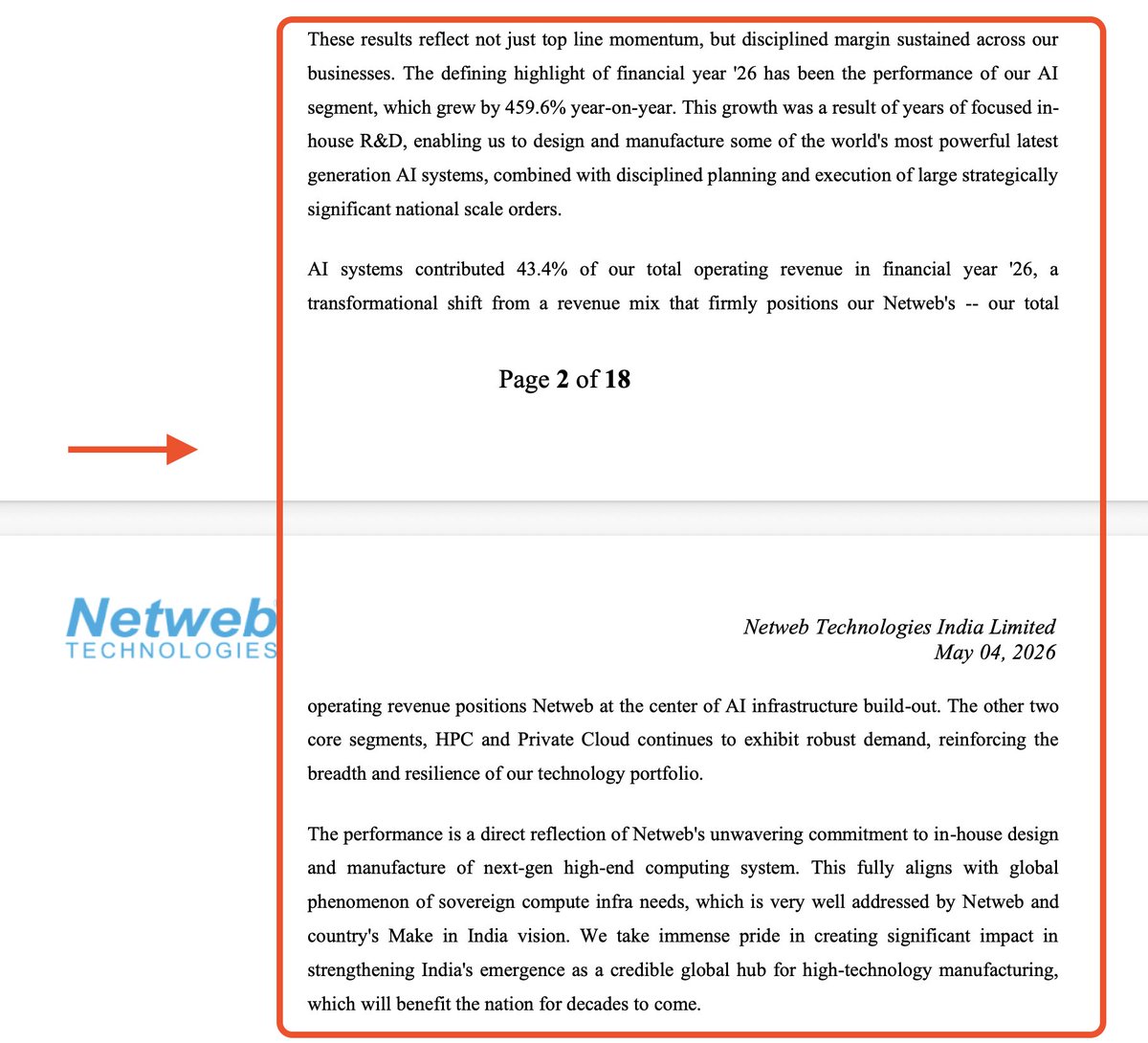

💻 $NETWEB — India's AI infrastructure company just reported its best year ever.

Revenue 90%. AI segment 460%. Net debt zero. ROCE 37.5%.

Then the promoters sold 4% of the company. And the stock fell ~15% in 2 weeks.

That combination deserves a very careful read.

🔍 What do they actually do?

Netweb Technologies is India's only Indian-origin OEM in High-End Computing. They design and manufacture supercomputers, HPC servers, AI infrastructure systems, and private cloud solutions — under the Tyrone brand.

Not just assembly. Genuine in-house R&D and design in Faridabad. Their systems run inside government data centres, ISRO, IITs, defence labs, and large enterprises. 600 supercomputing systems installed across India.

Think of them as the company building India's sovereign AI brain — the hardware layer that runs the models everyone talks about.

📊 FY26 numbers — standalone:

📈 Revenue: ₹1,149 Cr → ₹2,184 Cr ( 90% YoY) — landmark year

💰 PAT: ₹114 Cr → ₹206 Cr ( 80.9% YoY)

🏭 Adj. EBITDA: ₹290 Cr ( 82.4% YoY) | Margin: 13.3%

🤖 AI Systems segment: 459.6% YoY — now 43.4% of revenue (was 7% two years ago)

✅ ROCE: 37.5% | ROE: 32.9%

✅ Debt-free. Net cash: ₹83 Cr.

✅ CRISIL A (Stable) / A1 — rated limit raised to ₹2,420 Cr

📦 Order book: ₹2,100 Cr L1 pipeline ₹4,400 Cr

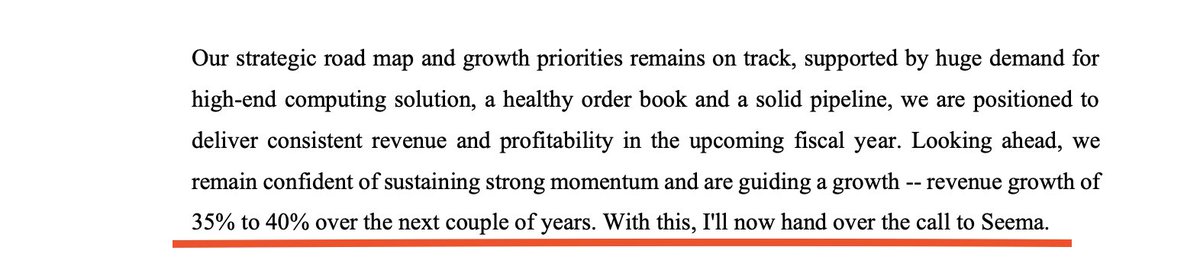

🚀 FY27 guidance: 35–40% revenue growth | 13–14% EBITDA margins

👥 131 new clients onboarded in FY26

The business is genuinely exceptional. These are not manufactured numbers.

📉 So why did it fall ~15% after record results?

Here's what the data tells you:

1️⃣ Revenue missed analyst estimates by 8% and EPS by 4.2% — when a stock is priced for perfection, even a great result disappoints

2️⃣ Promoters sold 4.02% of the company — holding dropped from 71% to 67%. No official reason given. In a stock that had run 3× in 12 months, promoter selling at the top raises questions

3️⃣ FY27 guidance of 35–40% is strong — but it's a deceleration from 90% in FY26. When the market prices in continuation of 90% growth, 35% feels like a disappointment

4️⃣ Valuation is not cheap by any measure:

→ P/E: ~85× on FY26 earnings

→ P/B: ~35× (Screener confirms stock trading at 34.9× book)

→ Market cap: ₹25,000 Cr on ₹206 Cr PAT

For context: the stock has risen ~10× from its IPO price of ₹500 in July 2023.

💬 For those asking: what do I do now?

Here's what the facts tell you — not advice, just the math:

→ At ~85× earnings, every quarter now has to be exceptional. One guidance miss and the valuation unwinds fast

→ The business case — India's sovereign AI infra, supercomputing, defence HPC — is real and multi-year. That doesn't change with a 15% pullback

→ The promoter selling at peak valuation is the single biggest flag. It doesn't mean the company is broken. But someone with the most information about the business decided now was a good time to sell

→ A 15% fall on a stock that ran 200% in 12 months is NOT a correction in valuation terms. It's still one of the most expensive stocks in Indian tech hardware

→ Chasing after a 15% pullback in a 85× P/E stock is a different risk profile than most people appreciate

The story is real. The price has already priced in the story — and then some.

India needs sovereign AI infrastructure. Netweb is uniquely positioned to build it. But what you pay for that positioning matters.

Not SEBI registered. Not advice. DYOR.

Join my telegram community for more such discussions: t.me/bang_on2026

#NETWEB #NetwebTech #ArtificialIntelligence #HPC #SuperComputing #SovereignAI #MakeInIndia #EquityResearch #ITHardware

1

4

472

Jun 11

Netweb માં શું રાખવી રોકાણની સ્ટ્રેટેજી?

જાણો ખુશી મિસ્ત્રીની સલાહ @Khushimistry23

#netwebtech #investmentstrategy #returns

129

Jun 9

NETWEB TECH - update

- Showing recovery sign from retracemnt level of around .618 of current move

- stock formed a bullish harami pattern around these level

- GOOD 1 or 2 day follow up required to take stock new high

- Also stock also has taken support fro 50EMA

#netweb #chartsdontlie #netwebtech #datacentre #ai #AI

5

1,418

May 31

🚀 Netweb Technologies (CMP ₹4670) looks ready for a BIG move! 📈

Massive Cup & Handle breakout in play after a strong base formation. 🔥

If momentum sustains, this could be the start of the next bullish leg. 👀💰

#StocksToWatch #Breakout #NetwebTech

4

549

May 30

Netweb Technologies India Ltd Concall Summary for Q4FY26

CORE HIGHLIGHT

- Emerging leader in sovereign AI infrastructure

MANAGEMENT COMMENTARY

- FY26 described as landmark year

- Revenue growth reached 90% YoY

- AI segment growth remained exceptional

- Entered FY27 from strong position

- In-house R&D remained key priority

- “Make in India” strategy emphasized

- Sovereign AI infrastructure gaining importance

FUTURE OUTLOOK & GUIDANCE

- Revenue growth guidance: 35–40%

- EBITDA margin guidance: 13–14%

- FY27 opening order book: ₹2,100 Cr

- L1-inclusive order book: ₹2,400 Cr

- Strategic orders executed over quarters

- Total pipeline visibility: ₹6,500 Cr

INDUSTRY & MACRO TRENDS

- Sovereign AI becoming strategic necessity

- India AI Mission driving demand

- GPU infrastructure demand accelerating rapidly

- Global AI demand remains strong

- High-end compute demand expanding globally

- Data sovereignty gaining importance worldwide

COMPETITIVE POSITIONING

- India’s only fullstack domestic provider

- Focused on sovereign enterprise demand

- Not targeting hyperscaler segment currently

- Capability-driven technology positioning maintained

- Expertise in liquid-cooled architectures

- High-density GPU systems differentiation

RISKS & CONCERNS

- Inventory levels increased significantly

- Critical component sourcing remains challenge

- Forex MTM losses impacted earnings

- Strategic order spillovers delayed revenues

- Exports remain relatively small currently

- Global supply-chain pressure persists

GROWTH DRIVERS & STRATEGY

AI INFRASTRUCTURE

- AI contributes 43.4% revenues

- AI demand scaling aggressively

- National AI projects driving momentum

- Sovereign compute opportunity expanding rapidly

NEW FACILITY EXPANSION

- 15,000 sq.ft facility commissioned

- Facility supports liquid-cooled systems

- Advanced architectures manufacturing enhanced

R&D & TECHNOLOGY

- Strong in-house design capabilities

- Rapid adoption of Nvidia architectures

- Focus on risk-based architectures

- High-performance systems innovation continuing

LARGE-SCALE EXECUTION

- National-scale project execution validated

- Strategic orders enhancing credibility

- Complex deployments strengthening positioning

PRODUCT MIX & PORTFOLIO

- AI systems became largest segment

- HPC continues strong growth momentum

- Private cloud demand remains robust

- Focus shifting toward high-density racks

- Moving away from low-margin products

- 150kW rack capabilities being developed

FINANCIAL PERFORMANCE

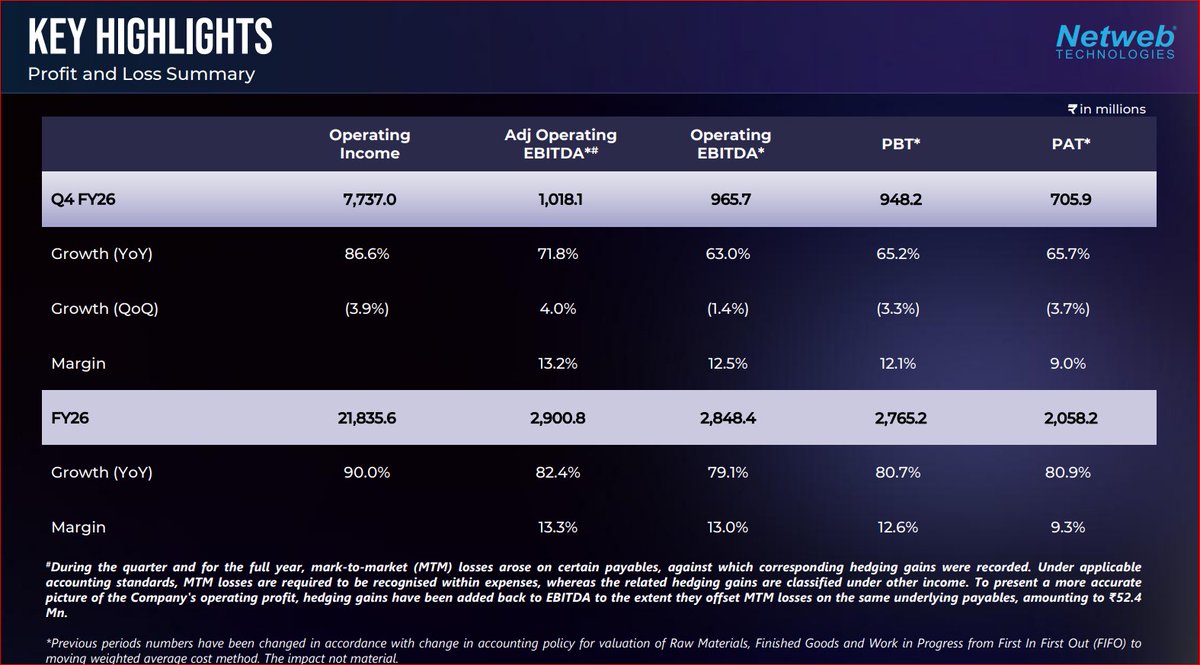

FY26

- Revenue: ₹21,836 Mn (↑90% YoY)

- PAT: ₹2,058 Mn (↑81% YoY)

- PAT Margin: 9.3%

- Strong profitability and growth achieved

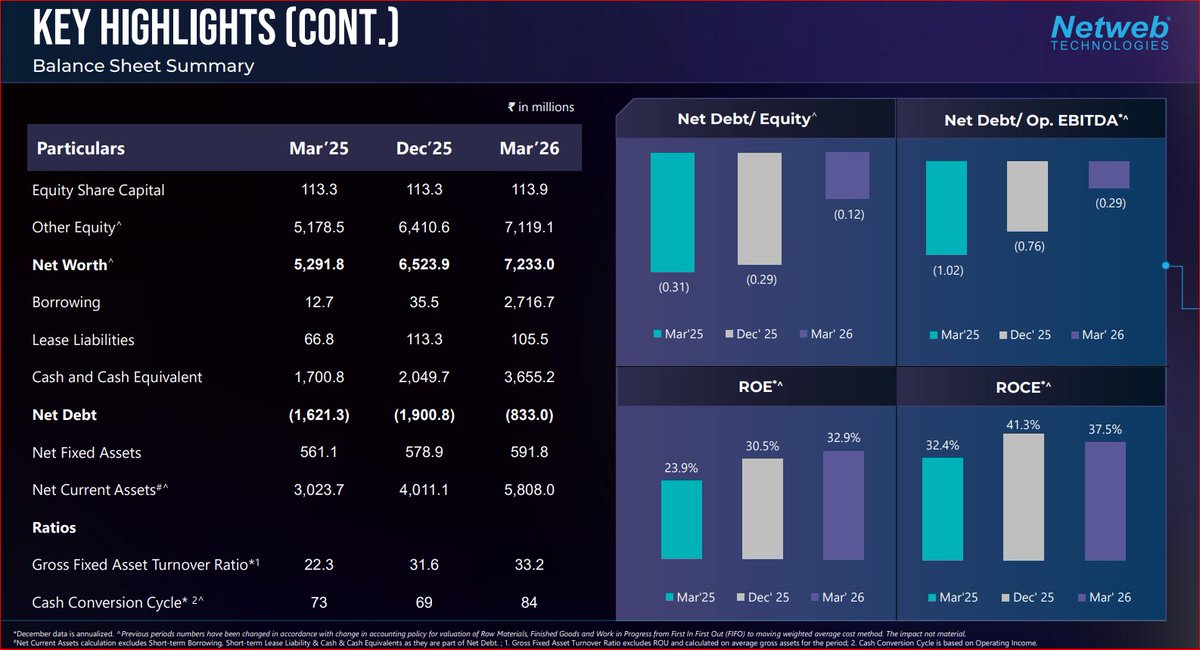

BALANCE SHEET & CASH FLOW

- Zero net debt company

- Net free cash: ₹833 Mn

- Operating cash flow: ₹1,715 Mn

- Strong liquidity position maintained

EFFICIENCY METRICS

- ROE stood at 32.9%

- ROCE stood at 37.5%

- Capital efficiency remained robust

KEY INSIGHT

- AI infrastructure becoming primary growth driver

OUTLOOK

- Strong order visibility supports growth

- AI demand outlook remains robust

- Sovereign AI spending likely accelerating

- Margin profile expected remaining stable

- Supply-chain availability remains monitorable

CONCLUSION

- FY26 marked transformational growth phase

- AI systems driving business transition

- Strong order book provides visibility

- Balance-sheet remains debt-free and strong

- Positioned strongly for India AI expansion

#Netweb #Netwebtechnologies #stockmarket

@gaze_observer @netwebtech

May 30

Netweb Conference Call Highlights | Q4 FY2026 🔥🔥🔥

The company is rapidly positioning itself as one of the strongest emerging players in India’s AI infrastructure and high-performance computing ecosystem.

One of the biggest highlights was the explosive growth in the AI systems business, which grew nearly 460% YoY in FY26 and now contributes more than 43% of the company’s total operating revenue. This clearly shows how rapidly the revenue mix is shifting towards AI-led infrastructure demand.

Management repeatedly highlighted that demand for sovereign AI infrastructure in India is becoming extremely strong, especially with the government’s increasing focus on AI compute capacity and large-scale GPU deployment across the country.

The company started FY27 with:

▪ ₹2,100 crore firm order book

▪ ₹2,400 crore order book including L1 orders

▪ ₹4,400 crore healthy pipeline

Out of this, nearly ₹1,600 crores comes from strategic orders, while the remaining business is organic in nature.

Management expects nearly 60% pipeline conversion over the next 18–24 months, which indicates strong medium-term visibility.

Another important point was that the company guided for 35–40% revenue growth in FY27 for the core business itself, excluding large strategic order execution. This suggests that the base business itself is growing aggressively.

Despite strong growth, management expects EBITDA margins to remain stable around 13–14% over the next few years.

One thing that stood out strongly was the company’s in-house capability stack.

Management repeatedly emphasized:

▪ In-house R&D

▪ In-house design capability

▪ In-house manufacturing

▪ Ability to adapt to custom AI architectures

This positions the company strongly within India’s “Make in India” AI and compute infrastructure theme.

The company also commissioned a new 15,000 sq. ft. state-of-the-art manufacturing facility, which enhances capabilities around:

▪ Liquid cooling systems

▪ High-density racks above 150 kW

▪ Next-generation AI infrastructure deployments

Management clarified that the company is capability-driven rather than capacity-driven, and current utilization levels remain around 65–70%, leaving room for scaling.

Another important point was around AI demand itself.

The company highlighted that both AI training and AI inference workloads are creating opportunities simultaneously, and rising inference demand is becoming an additive growth driver rather than replacing existing demand.

The Private Cloud and HPC businesses also continue to grow strongly, although their revenue contribution appears lower due to the exponential growth in the AI systems segment.

Interestingly, management also highlighted that India is currently more of a sovereign compute market rather than a hyperscaler-led market, though the company remains open to future opportunities involving players like Amazon or Microsoft if required.

Operationally, the company continues to maintain a very strong balance sheet position:

▪ Zero net debt company

▪ ₹833 million net free cash

▪ Healthy ROE of 32.9%

▪ ROCE of 37.5%

The increase in short-term borrowings during the quarter was clarified as temporary working capital funding for large strategic orders and governed by RBI/covenant-related requirements.

Another important detail was the promoter stake sale.

Management clarified that the 4% promoter stake sale was done only to improve stock liquidity, and no further dilution is planned for the next 12 months.

The company also expects:

▪ Stable cash conversion cycle within 80–110 days

▪ Routine FY27 capex of only ₹20–25 crores

▪ Strong domestic demand to remain the immediate priority before exports

Overall, management commentary strongly suggests that the company is positioning itself at the center of India’s rapidly expanding AI infrastructure ecosystem with strong order visibility, scalable in-house capabilities, and aggressive participation in sovereign AI deployment opportunities.

Disclaimer:

For educational and study purposes only.

Not a buy/sell recommendation.

3

8

750

May 29

#NetwebTech

Breakout stock 🪂

Current Price: 4670

Double top weekly chart at 4250-4300

Upswing : 5150/5400

Invalidation at : 4050

1. Double top weekly Breakout

2. Monthly Chart regain

3. ATH/Multi Period High

4. Volume Spurt

5. Rally Onn for long side.

#nifty #msci #trading

Jan 17

#Netweb

Current Level: 3347

Double Top Breakout with Box at 3350

Time consolidation breakout

Nov'25 top retested

Technical injection on Chart.

upside: 3860

Invalidation: 3050

#stocktobuy #stocktowatch #TradingView

1

6

66

4,902

May 29

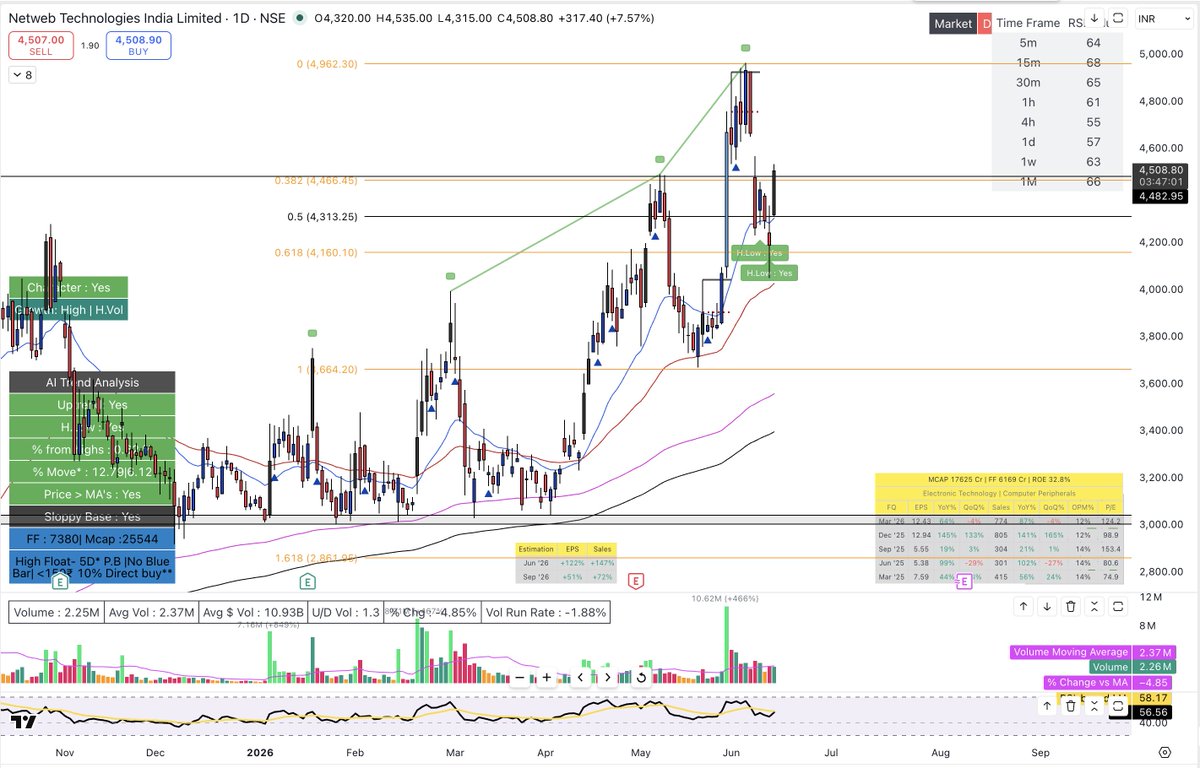

Everyone ignored #NETWEB when it was quietly consolidating around the ₹1,500–₹1,750 horizontal baseline early last year.

Now everyone is frantically chasing it at ₹4,571 after a violent vertical breakout to an intraday high of ₹4,680.

That’s how market psychology works.

The Catalyst: Exponentially accelerating domestic deployment of High-Performance Computing (HPC) infrastructure and AI-server architectures as enterprise and public sectors build out sovereign cloud networks.

KEY TECHNICAL LEVELS:

• Support Zone 1: ₹4,154 (Hourly 20 & 50 EMA Cluster / Immediate Reversion Cushion)

• Support Zone 2: ₹3,672–₹3,781 (Daily 20 EMA Layer / Structural Breakout Base)

• Current Value Zone: ₹4,571

• Resistance Zone 1: ₹4,680–₹4,700 (Intraday High / Psychological Round Number)

• Resistance Zone 2: ₹5,000 (Macro Blue-Sky Expansion Zone)

• Trend Reversal Level: Sustained daily close below the major historical consolidation line of ₹3,250 completely invalidates the immediate vertical momentum bias.

The interesting part?

Price action has staged a clean, thunderous breakout above the prominent multi-month horizontal accumulation ceiling near ₹4,250 on the weekly chart. At a current price breaching ₹4,500, the stock is trading at extremely premium structural valuation multiples, effectively pricing in perfect execution for the next several quarters. While it commands a massive strategic moat as India’s premier native OEM for specialized AI-server nodes under the local manufacturing subsidies (PLI scheme), any minor delay in global GPU allocation constraints could trigger violent mean-reversion pullbacks.

Meanwhile:

• The massive breakout on the weekly chart has effectively wiped out any remaining overhead structural supply.

• Volume is expanding exponentially on the Daily and Hourly charts to support this vertical lift, while short-term EMAs have fanned out into a parallel bullish alignment.

• RSI is cruising at a deeply overbought 89.7 on the Hourly chart and 71.4 on the Daily chart. While this signals massive institutional buying dominance rather than exhaustion, a brief intra-day cooling off to allow the averages to catch up is technically expected.

MY PLAYBOOK:

• Riding the core positional equity with zero urge to disrupt a monster trend phase prematurely.

• Treating any sharp, short-term check-backs or pullbacks toward the ₹3,950–₹4,150 zone as high-probability structural areas to scale back into momentum exposure.

• Clean hourly acceptance and strong volume confirmation above the ₹4,680 peak unlocks a swift path toward the major psychological milestone at ₹5,000 .

Big moves rarely begin when sentiment feels comfortable.

They begin when nobody wants to buy and they extend when everyone wishes they did.

DYOR.

Not a recommendation.

#NETWEB #NetwebTech #StockMarketIndia #TechnicalAnalysis #PriceAction #AIServers #HPC

3

665

NETWEB TECHNOLOGIES INDIA Ltd stock is taking strong support at yellow zone.

Good results can trigger rally. PE ratio is above 100 but higher EPS on good results can bring down the PE ratio.

#netwebtechnologies #netweb

t.me/uremo24 || t.me/FNRA_daily

3

30

2,767

May 29

May 26

Stock Name - #Netwebtech 📊

CMP - 3849 📈

Keep in Track now 👁️ , Expecting a Spike from here or accumulate it in every dip for Short term .

#Ai #datacenter

1

6

597

May 28

Netweb Technologies India Ltd Concall Summary for Q4FY26

CORE HIGHLIGHT

- Emerging leader in sovereign AI infrastructure

MANAGEMENT COMMENTARY

- FY26 described as landmark year

- Revenue growth reached 90% YoY

- AI segment growth remained exceptional

- Entered FY27 from strong position

- In-house R&D remained key priority

- “Make in India” strategy emphasized

- Sovereign AI infrastructure gaining importance

FUTURE OUTLOOK & GUIDANCE

- Revenue growth guidance: 35–40%

- EBITDA margin guidance: 13–14%

- FY27 opening order book: ₹2,100 Cr

- L1-inclusive order book: ₹2,400 Cr

- Strategic orders executed over quarters

- Total pipeline visibility: ₹6,500 Cr

INDUSTRY & MACRO TRENDS

- Sovereign AI becoming strategic necessity

- India AI Mission driving demand

- GPU infrastructure demand accelerating rapidly

- Global AI demand remains strong

- High-end compute demand expanding globally

- Data sovereignty gaining importance worldwide

COMPETITIVE POSITIONING

- India’s only fullstack domestic provider

- Focused on sovereign enterprise demand

- Not targeting hyperscaler segment currently

- Capability-driven technology positioning maintained

- Expertise in liquid-cooled architectures

- High-density GPU systems differentiation

RISKS & CONCERNS

- Inventory levels increased significantly

- Critical component sourcing remains challenge

- Forex MTM losses impacted earnings

- Strategic order spillovers delayed revenues

- Exports remain relatively small currently

- Global supply-chain pressure persists

GROWTH DRIVERS & STRATEGY

AI INFRASTRUCTURE

- AI contributes 43.4% revenues

- AI demand scaling aggressively

- National AI projects driving momentum

- Sovereign compute opportunity expanding rapidly

NEW FACILITY EXPANSION

- 15,000 sq.ft facility commissioned

- Facility supports liquid-cooled systems

- Advanced architectures manufacturing enhanced

R&D & TECHNOLOGY

- Strong in-house design capabilities

- Rapid adoption of Nvidia architectures

- Focus on risk-based architectures

- High-performance systems innovation continuing

LARGE-SCALE EXECUTION

- National-scale project execution validated

- Strategic orders enhancing credibility

- Complex deployments strengthening positioning

PRODUCT MIX & PORTFOLIO

- AI systems became largest segment

- HPC continues strong growth momentum

- Private cloud demand remains robust

- Focus shifting toward high-density racks

- Moving away from low-margin products

- 150kW rack capabilities being developed

FINANCIAL PERFORMANCE

FY26

- Revenue: ₹21,836 Mn (↑90% YoY)

- PAT: ₹2,058 Mn (↑81% YoY)

- PAT Margin: 9.3%

- Strong profitability and growth achieved

BALANCE SHEET & CASH FLOW

- Zero net debt company

- Net free cash: ₹833 Mn

- Operating cash flow: ₹1,715 Mn

- Strong liquidity position maintained

EFFICIENCY METRICS

- ROE stood at 32.9%

- ROCE stood at 37.5%

- Capital efficiency remained robust

KEY INSIGHT

- AI infrastructure becoming primary growth driver

OUTLOOK

- Strong order visibility supports growth

- AI demand outlook remains robust

- Sovereign AI spending likely accelerating

- Margin profile expected remaining stable

- Supply-chain availability remains monitorable

CONCLUSION

- FY26 marked transformational growth phase

- AI systems driving business transition

- Strong order book provides visibility

- Balance-sheet remains debt-free and strong

- Positioned strongly for India AI expansion

#Netweb #Netwebtechnologies #stockmarket

@FI_InvestIndia @gaze_observer @dmuthuk @aakankshalovely @netwebtech

May 28

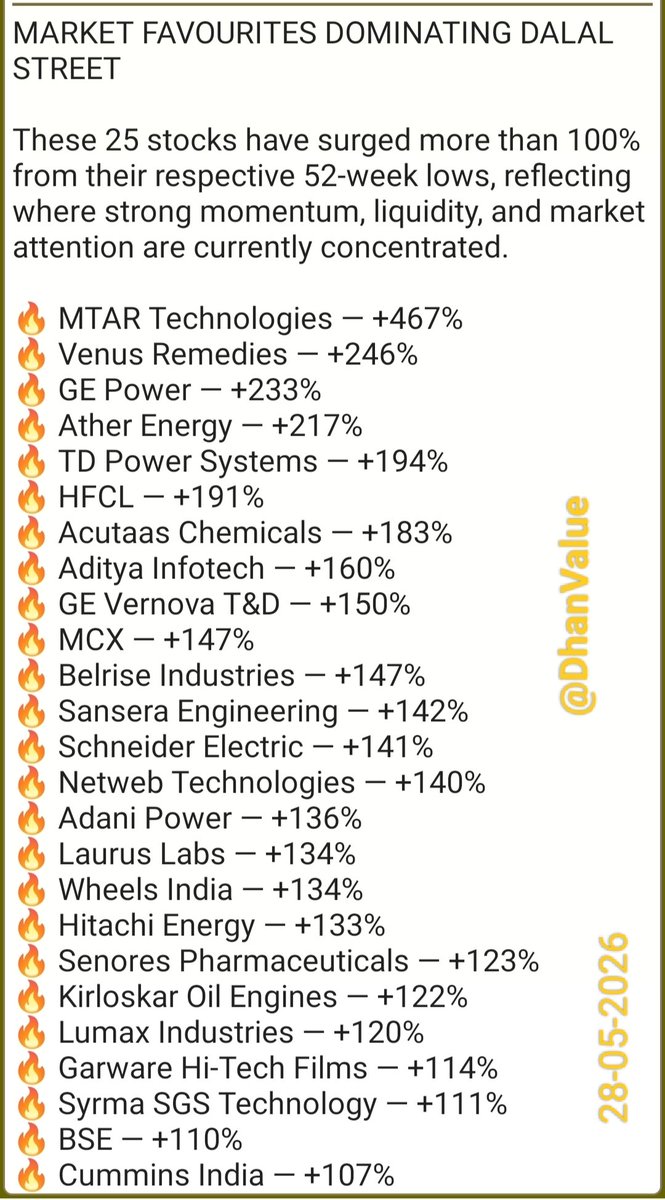

MARKET FAVOURITES DOMINATING DALAL STREET

These 25 stocks have surged more than 100% from their respective 52-week lows, reflecting where strong momentum, liquidity, and market attention are currently concentrated.

The market always rewards where sentiments, earnings visibility, liquidity, and participation align strongly.

28-05-2026

Disclaimer: For information purposes only.

1

6

1,111

May 27

Driving the next wave of India’s digital transformation ☁️⚡

The 10th Smart Datacenters & Cloud Infrastructure Summit 2026 brings together industry leaders, innovators, and policymakers to discuss the future of data centres, AI, cloud, and digital infrastructure-powering growth, resilience, and a stronger digital economy.

📍 Hyderabad

📅 28 May 2026

Register now: assocham.org/event-detail.ph…

For more details, please contact: varun.aggarwal@assocham.com

#SmartDatacentersSummit #CloudInfrastructure #DigitalTransformation #AI

@GoI_MeitY @TelanganaCMO @TGRising2047 @OffDSB @ASSOCHAMSG @TheSridharReddy @sttgdcindia @AdaniOnline @Unomindacom @AxisBank @CommScope @DeltaElectIndia @netwebtech @TyroneSystems @Siemon @sifydotcom @Pi_DATACENTERS @yottainfra @PwC_IN @JSALawIndia @bharath_cloud @PDRVideo @morphingm @uravulabs @VMARCwires @TheOfficialSBI @RESecurity @var_agg24

3

112

May 26

Stock Name - #Netwebtech 📊

CMP - 3849 📈

Keep in Track now 👁️ , Expecting a Spike from here or accumulate it in every dip for Short term .

#Ai #datacenter

2

12

2,473

May 21

My Top 04 Best Stocks for next few days 📊

Track for 15%-20% Upside Potential in Swing Basis for Next few Days 🚀

Save it for Later 🔖

1. #Netwebtech

2

5

49

13,644

May 12

#NETWEB Wave (5) seems to be done here.

Caution is warranted.

It may start the consolidation/correction phase soon.

THIS IS NOT A BUY/SELL/HOLD RECOMMENDATION. PLEASE DO YOUR OWN DUE DILIGENCE BEFORE MAKING A DECISION.

#NetwebTechnologies #Netwebtech

Apr 21

#NETWEB Consider wave (5) to be almost done here. Now all up to the upcoming earnings. Caution is warranted here.

Only if the earnings are great, an extension of wave (5) is possible.

THIS IS NOT A BUY/SELL/HOLD RECOMMENDATION. PLEASE DO YOUR OWN DUE DILIGENCE BEFORE MAKING A DECISION.

#NetwebTechnologies #Netwebtech

1

1

4

1,082

May 6

Netweb Technologies India Ltd Concall Summary for Q4FY26

CORE HIGHLIGHT

- Emerging leader in sovereign AI infrastructure

MANAGEMENT COMMENTARY

- FY26 described as landmark year

- Revenue growth reached 90% YoY

- AI segment growth remained exceptional

- Entered FY27 from strong position

- In-house R&D remained key priority

- “Make in India” strategy emphasized

- Sovereign AI infrastructure gaining importance

FUTURE OUTLOOK & GUIDANCE

- Revenue growth guidance: 35–40%

- EBITDA margin guidance: 13–14%

- FY27 opening order book: ₹2,100 Cr

- L1-inclusive order book: ₹2,400 Cr

- Strategic orders executed over quarters

- Total pipeline visibility: ₹6,500 Cr

INDUSTRY & MACRO TRENDS

- Sovereign AI becoming strategic necessity

- India AI Mission driving demand

- GPU infrastructure demand accelerating rapidly

- Global AI demand remains strong

- High-end compute demand expanding globally

- Data sovereignty gaining importance worldwide

COMPETITIVE POSITIONING

- India’s only fullstack domestic provider

- Focused on sovereign enterprise demand

- Not targeting hyperscaler segment currently

- Capability-driven technology positioning maintained

- Expertise in liquid-cooled architectures

- High-density GPU systems differentiation

RISKS & CONCERNS

- Inventory levels increased significantly

- Critical component sourcing remains challenge

- Forex MTM losses impacted earnings

- Strategic order spillovers delayed revenues

- Exports remain relatively small currently

- Global supply-chain pressure persists

GROWTH DRIVERS & STRATEGY

AI INFRASTRUCTURE

- AI contributes 43.4% revenues

- AI demand scaling aggressively

- National AI projects driving momentum

- Sovereign compute opportunity expanding rapidly

NEW FACILITY EXPANSION

- 15,000 sq.ft facility commissioned

- Facility supports liquid-cooled systems

- Advanced architectures manufacturing enhanced

R&D & TECHNOLOGY

- Strong in-house design capabilities

- Rapid adoption of Nvidia architectures

- Focus on risk-based architectures

- High-performance systems innovation continuing

LARGE-SCALE EXECUTION

- National-scale project execution validated

- Strategic orders enhancing credibility

- Complex deployments strengthening positioning

PRODUCT MIX & PORTFOLIO

- AI systems became largest segment

- HPC continues strong growth momentum

- Private cloud demand remains robust

- Focus shifting toward high-density racks

- Moving away from low-margin products

- 150kW rack capabilities being developed

FINANCIAL PERFORMANCE

FY26

- Revenue: ₹21,836 Mn (↑90% YoY)

- PAT: ₹2,058 Mn (↑81% YoY)

- PAT Margin: 9.3%

- Strong profitability and growth achieved

BALANCE SHEET & CASH FLOW

- Zero net debt company

- Net free cash: ₹833 Mn

- Operating cash flow: ₹1,715 Mn

- Strong liquidity position maintained

EFFICIENCY METRICS

- ROE stood at 32.9%

- ROCE stood at 37.5%

- Capital efficiency remained robust

KEY INSIGHT

- AI infrastructure becoming primary growth driver

OUTLOOK

- Strong order visibility supports growth

- AI demand outlook remains robust

- Sovereign AI spending likely accelerating

- Margin profile expected remaining stable

- Supply-chain availability remains monitorable

CONCLUSION

- FY26 marked transformational growth phase

- AI systems driving business transition

- Strong order book provides visibility

- Balance-sheet remains debt-free and strong

- Positioned strongly for India AI expansion

#Netweb #Netwebtechnologies #stockmarket @FI_InvestIndia @gaze_observer @dmuthuk @aakankshalovely @netwebtech

1

2

4

1,991

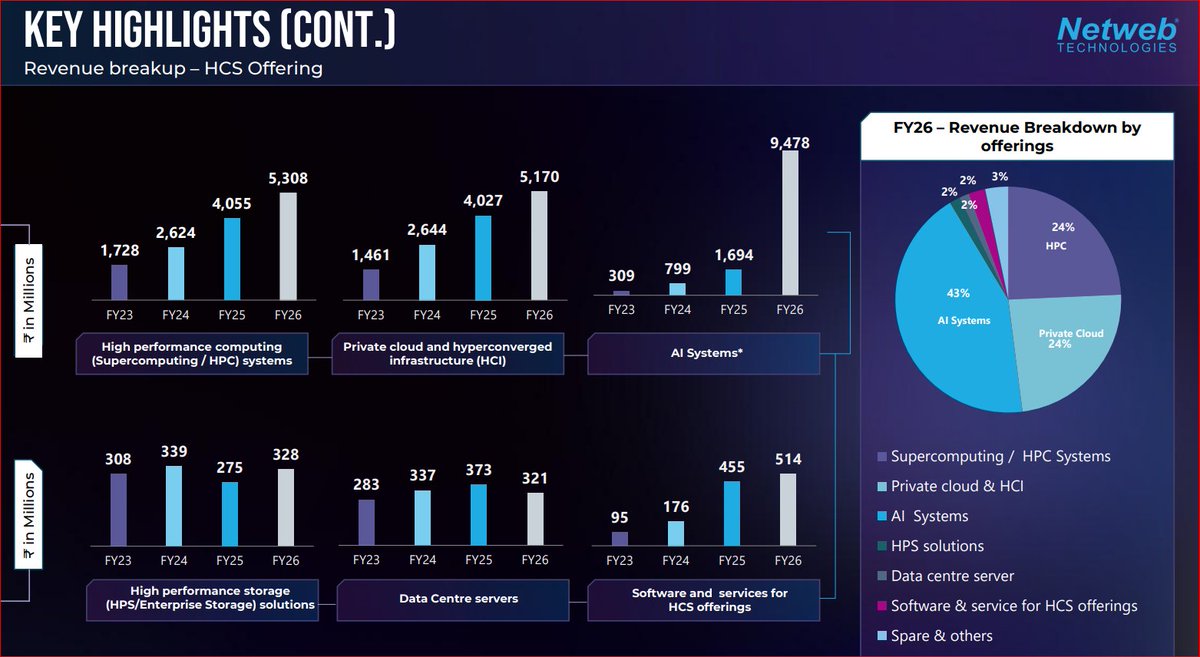

#NetwebTech

Most Powerful Growth Trigger from their latest presentation 👇🏻

AI Systems grew 460% YoY, marking an exceptional surge in demand.

This segment now contributes 43% of total revenue, indicating a sharp shift in business mix.

Such growth is not incremental; it reflects the early phase of a new category being built.

The demand is driven by generative AI, GPU based computing and large scale model training infrastructure.

If this trajectory sustains, Netweb can emerge as a key proxy for India’s AI infrastructure buildout.

2

7

49

2,728

May 4

Corporate Radar | Netweb Technologies

Q4 नतीजों में कहां से आया दबाव?

Nvidia के साथ पार्टनरशिप, कंपनी को कितना फायदा?

कैसी है कंपनी की मौजूदा ऑर्डरबुक?

देखिए Netweb Technologies के CMD संजय लोढ़ा की ज़ी बिज़नेस से खास बातचीत

#CorporateRadar #NetwebTechnologies #SanjayLodha #Nvidia #Q4Results @netwebtech @poojat_0211

1

3

1,261