EnviTec hit by German bio-LNG crackdown as profits slide

indianchemicalnews.com/gas/e…

#EnviTecBiogas #regulatory #policychanges #bioLNG #business

@EnviTecBiogas

1

2

74

অন্তর্বর্তী সরকারের ১৩৩টি অধ্যাদেশের মধ্যে ৯৮টি হুবহু সংসদে উত্থাপন করা হয়েছে। আগামী ৯ এপ্রিলের মধ্যে অধ্যাদেশগুলো সংসদে পাস হতে পারে। তবে উত্থাপন না হওয়া...

বিস্তারিত : somoynews.tv/news/2026-04-02…

#GovernmentUpdate #ParliamentNews #PolicyChanges #somoytv

1

249

Apr 1

1 एप्रिलपासून मोठे बदल; 'हे' महत्वाचे नियम जाणून घ्या!

.

.

.

#april1changes #newrules #IndiaUpdates #PolicyChanges #BreakingNews

1

6

474

Mar 20

BUSINESS

Blasé Capital H-1B : GAINS vs PAINS

Click- dailypioneer.com/news/blase-…

#H1BVisa #USImmigration #SkilledWorkers #FiscalContribution #ImmigrationPolicy #EconomyFirst #AmericaFirst #VisaReforms #HighSkilledImmigrants #H1BHouseholds #USTaxes #StateRevenue #FederalRevenue #ImmigrationImpact #WageBasedVisa #SpousalWorkRights #SoftwareIndustry #IndianIT #GlobalTalent #EconomicBenefits #ImmigrationResearch #VisaLottery #H1BFees #PolicyChanges #ImmigrationDebate #USLaborMarket #SkilledImmigrantImpact #H1BStudy #TechImmigration #ImmigrationEconomics

2

66

Mar 5

Leadership shift alert! 🚨 President Trump announces replacement for DHS Secretary Kristi Noem. What's next for immigration and FEMA? 🤔 #PolicyChanges

1

3

43

প্রধানমন্ত্রী হিসেবে দুটি কার্যদিবস পার করে পরিবর্তনের ইঙ্গিত দেয়া সব সিদ্ধান্ত অনলাইন এবং অফলাইনে ব্যাপক আলোচিত হচ্ছে। সবাই বলছেন, এমন সিদ্ধান্তগ্রহণ ও বাস্তবায়ন সম্ভব হলে....

বিস্তারিত : somoynews.tv/news/2026-02-19…

#PrimeMinister #PolicyChanges #PoliticalDiscussion #somoytv

5

256

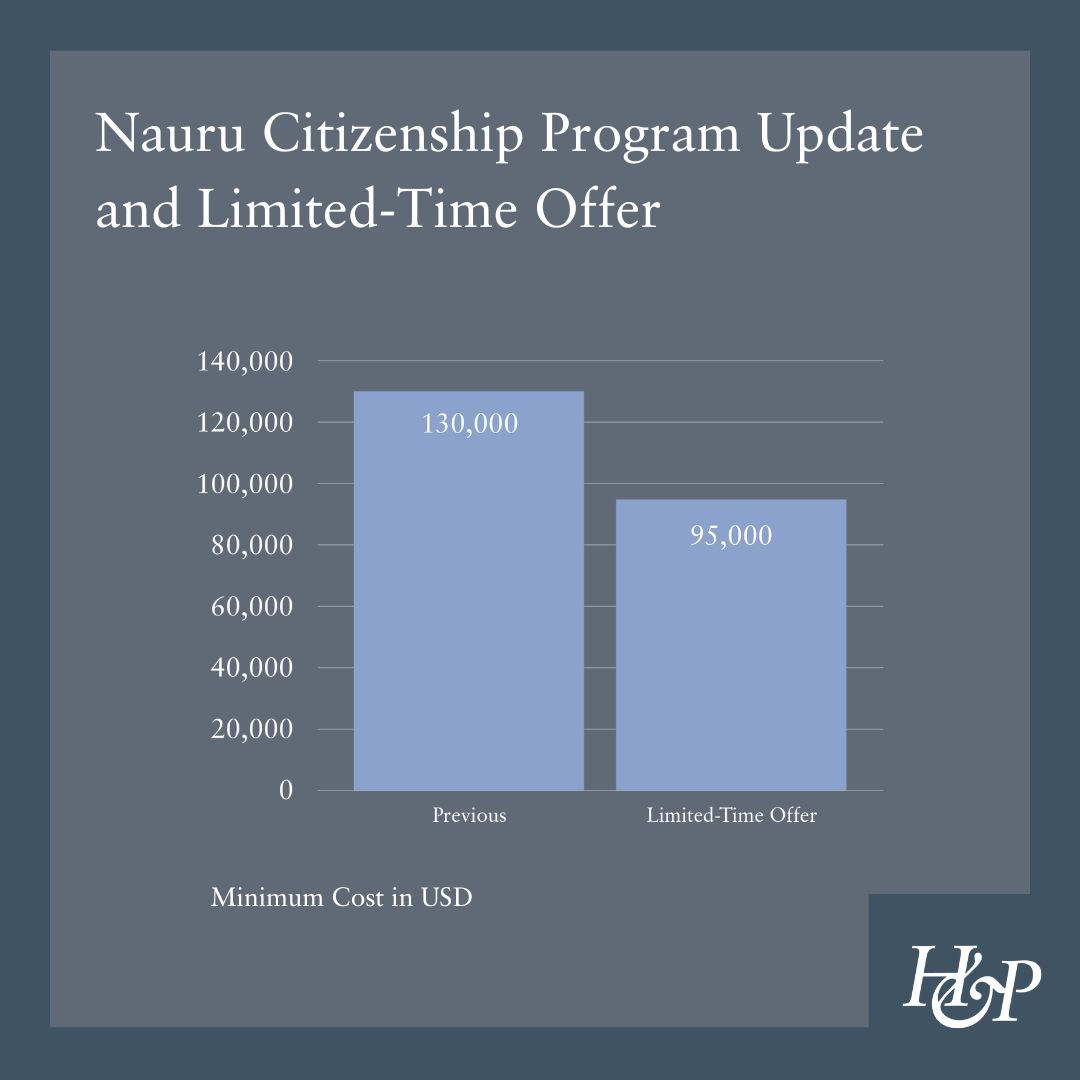

Nauru Citizenship Program Update: New Amendments Now in Effect and a Limited-Time Offer till 30 June 2026

• Under a limited-time offer, eligible applications submitted before 30 June 2026 may benefit from a reduced overall minimum cost of USD 95,000 (Previously USD 130,000)

• Dependent eligibility has been expanded, removing certain age, financial dependency, and marital-status restrictions

• Provisions for electronic submissions have also been introduced allowing for an even more efficient processing of applications

Henley & Partners has been mandated by the Government of Nauru to design, implement, and promote the Nauru Economic and Climate Resilience Citizenship Program so get in touch to find out more and apply now to benefit from this limited-time offer.

#nauru #naurucitizenship #naurucitizenshipprogram #citizenshipbyinvestment #policychanges #henleypartners #henleyandpartners #henleyglobal

1

3

294

Jan 30

ବଜେଟ୍ ପାଇଁ କାହାର କେଉଁ ଆଶା ? | Union Budget 2026 Expectations | PrameyaNews7

#Budget2026 #NirmalaSitharaman #BigAnnouncements #SpecialStory #odishanews #economicupdate #policychanges #breakingnews #financeupdate #odishaupdate #communityvoice #publicconcern #governance

68

Jan 15

देहरादून

सचिवालय में सीएम धामी की अध्यक्षता में चल रही बैठक

इस दौरान कैबिनेट मंत्री सतपाल महाराज, गणेश जोशी, सौरभ बहुगुणा , धन सिंह रावत, सुबोध उनियाल मौजूद

मंत्री रेखा आर्य वर्चुअल माध्यम से कैबिनेट में होगी शामिल

बैठक में पर्यटन, शिक्षा, उपनल विभाग सहित कई महत्वपूर्ण प्रस्तावों पर लगेगी मुहर

वहीं बैठक में विभागों की कई नियमावली में भी हो सकता है संशोधन

#CabinetMeeting #UttarakhandCabinet #TourismEducationProposals #PolicyChanges

#UttarakhandDevelopment #ChiefMinisterDhami #BREAKINGNEWS #primenews

@DehradunPolice @dmdehradun @pushkardhami @PrimeNewsInd @drdhansinghuk

3

52

Jan 1

Global Update: From Jan 1, 2026, new laws have come into effect in China, Malaysia, and Indonesia —

link - facebook.com/share/p/1BzaXfT…

#GlobalLawUpdates #WorldNews #PolicyChanges #InternationalUpdates

2

2

9

19 Dec 2025

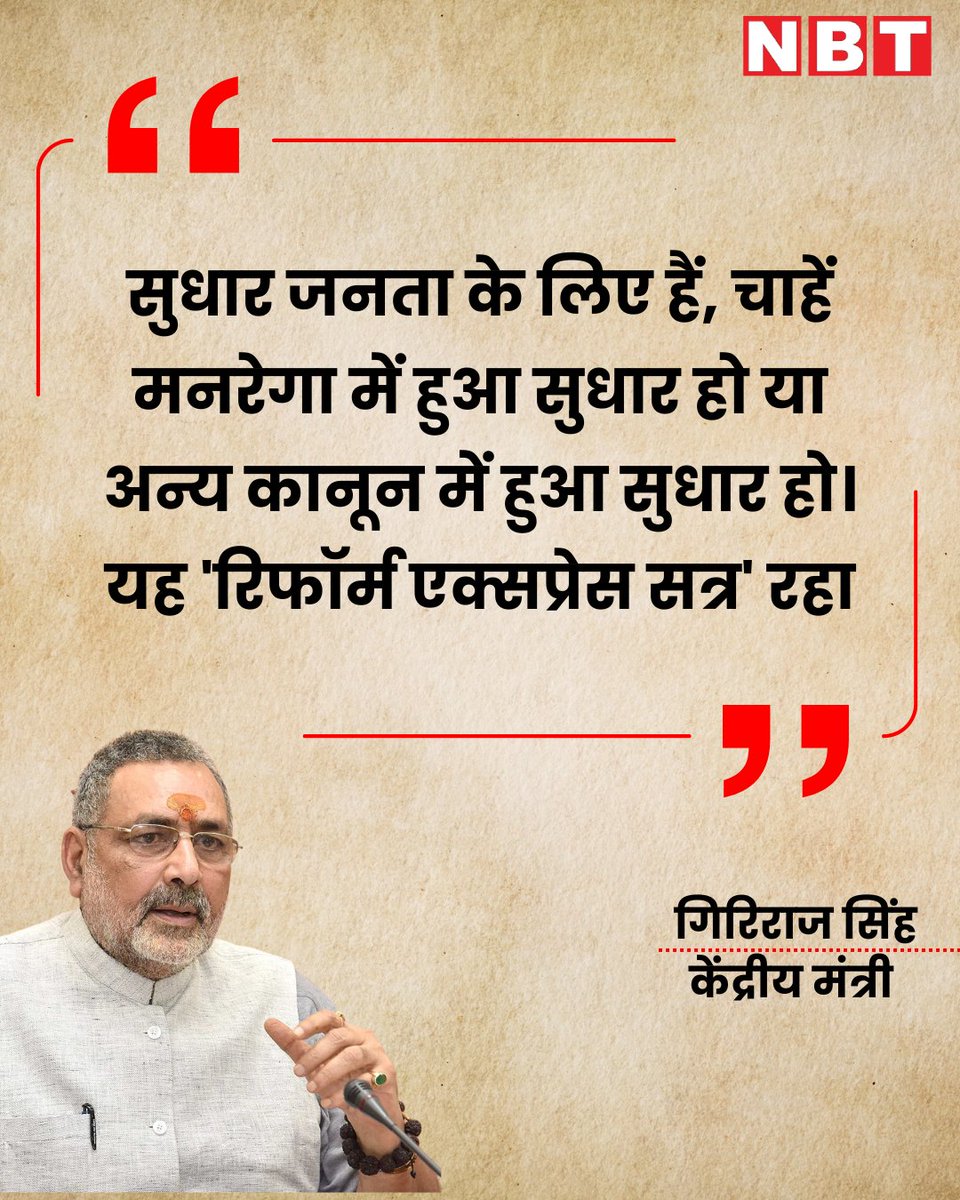

केंद्रीय मंत्री गिरिराज सिंह ने कहा, "सुधार जनता के लिए हैं, चाहें मनरेगा में हुआ सुधार हो या अन्य कानून में हुआ सुधार हो। यह 'रिफॉर्म एक्सप्रेस सत्र' रहा.

#GirirajSingh #ReformSession #GovernmentReforms #MahatmaMandrega #PolicyChanges #PoliticalNews

7

492

30 Nov 2025

Trump’s new immigration stance is creating another wave of debate across the country. 🇺🇸

📱Download our Mobile App (iOS / Android)

🔗 link-to.app/dexwirenews

After the DC guard shooting, Trump announced plans to pause migration from third world countries and tighten federal rules for noncitizens. Agencies were directed to review asylum approvals and re-check green cards from countries the administration considers high-risk.

The policy details are still unclear, especially with past legal challenges to similar bans. The situation has heightened national security discussions as federal departments reassess immigration processes and prepare for more scrutiny in the coming weeks.

#USPolitics #ImmigrationPolicy #TrumpAdministration #MigrationDebate #USNews #WashingtonDC #NationalSecurity #PolicyUpdate #GovernmentActions #BreakingPolitics #PoliticalUpdates #FederalReview #AsylumCases #USCIS #DHS #GreenCardReview #PublicPolicy #NewsReport #GlobalPolitics #ThirdWorldMigration #ImmigrationReform #LegalChallenges #PolicyChanges #WhiteHouseNews #PoliticalDiscussion #CurrentAffairs #AmericaToday #SecurityConcerns #GovernmentReview #PoliticalCoverage

1

2

10

190

24 Nov 2025

Parliament Winter Session : 1 થી 19 ડિસેમ્બર સુધી 15 દિવસમાં 10 બિલ રજૂ કરવામાં આવશે, સરકારનું ધ્યાન ‘રિફોર્મ’ પર

#ParliamentWinterSession #GovernmentBills #ReformAgenda #GovernmentUpdate #ParliamentNews #PolicyChanges

tv9gujarati.com/national/par…

214

11 Nov 2025

Agencies were given unrestricted powers by Amit Shah

#AmitShah #Agencies #UnrestrictedPowers #GovernmentAuthority #PoliticalPower #IndiaPolitics #LawEnforcement #PolicyChanges #Accountability #Transparency #CivilLiberties #NationalSecurity #PublicDebate #PoliticalOversight

11 Nov 2025

Agencies were given unrestricted powers by Amit Shah

#AmitShah #Agencies #UnrestrictedPowers #GovernmentAuthority #PoliticalPower #IndiaPolitics #LawEnforcement #PolicyChanges #Accountability #Transparency #CivilLiberties #NationalSecurity #PublicDebate #PoliticalOversight

2

16

1 Oct 2025

U.S. Defence Secretary slams ‘Woke Department’ & diversity initiatives in military

#PeteHegseth #USMilitary #USElections2025 #USDefence #Pentagon #FemaleOfficer #CombatPositions #PTTest #PolicyChanges #MilitaryStandards

1

542

20 Sep 2025

#MCInterview 🚨 | Process Reforms: How Small Changes Can Streamline India’s System - Sanjeev Sanyal

In this exclusive interview, Sanjeev Sanyal, member of the Prime Minister’s Economic Advisory Council, explains how “process reforms” - small but crucial changes in laws, regulations, and government architecture - are reducing friction in India’s system and improving efficiency.

In conversation with @shwwetapunj

@sanjeevsanyal | #SanjeevSanyal #ProcessReforms #IndiaReforms #GovernmentEfficiency #AdministrativeReforms #PMOEAC #IndiaNews #PolicyChanges #EconomicAdvisory #SystemStreamlining

12

34

141

18,028

18 Sep 2025

In uncertain times investing outcomes Trump headlines

By Neville Ntema

Against the backdrop of global markets in flux, imagine an investor nervously scrolling through their phone, eyes darting over headlines filled with policy changes, geopolitical tensions, and consumer behaviour shifts.

Each alert brings a fresh wave of anxiety with tariff shocks, diplomatic standoffs, and rapid technological change shaking confidence. Volatility has become the norm, and uncertainty is likely to remain with us for some time.

When faced with turbulence, many investors get distracted by the noise. Yet it is precisely in these moments that discipline matters most.

thebrief.com.na/2025/09/in-u… #namibia #investing #policychanges @MomentumNamibia

1

4

420

9 Sep 2025

Businesses in Vietnam should monitor evolving provincial master plans, #LandUseRegulations & incentives. Building ties with authorities & industry groups is key to navigating sudden #PolicyChanges & conflicting interpretations.

Stay informed ⤵️

ow.ly/GKbh50WSTlN

1

5

5,001

4 Sep 2025

If GST on health insurance is Exempted, not Zero-rated ✅

This means — Exempted GST on life and health insurance won’t directly reduce premiums by 18%.

Earlier, insurers were able to claim GST input credits on their expenses. Now, with zero-rating, that credit goes away and becomes a cost to them.

🔹 Before (18% GST applicable with ITC available)

•Base Premium: ₹1,00,000

•GST @18%: ₹18,000

•Total Payable by Customer: ₹1,18,000

•Insurance company could claim ITC on GST paid for expenses (advertising, rent, IT infra, etc.) → reducing their internal costs.

⸻

🔹 After (Zero-rated, no GST charged, but no ITC benefit)

•Base Premium: ₹1,00,000

•GST: NIL

•Total Payable by Customer: ₹1,00,000

•But, insurers lose ITC (say 10–11% of base premium cost), which now becomes their expense.

So realistically, we can expect only about a 7–8% reduction in premiums, not the full 18%.

#GSTReform #GSTCouncilMeet #TaxReforms #InsuranceSector #HealthInsurance #LifeInsurance #FinanceUpdates #PolicyChanges

6

3

13

3,189

27 Jul 2025

Walmart Welfare Warfare: When Food Stamps Stir Up Romance Rivalries

In a dramatic confrontation captured on video, a woman challenges her boyfriend at Walmart over his use of food stamps to buy groceries for another woman. This incident highlights the ongoing debate about the misuse of Supplemental Nutrition Assistance Program (SNAP) benefits, which have been a topic of discussion since recent policy changes aimed at reducing fraud and ensuring benefits reach those truly in need. The video, which has gone viral, underscores the personal and public dimensions of welfare programs, especially in light of a new law that includes the largest-ever cuts to SNAP benefits, potentially reducing what families can spend on food by an average of $146 per month. This event not only raises questions about personal relationships but also about the broader implications of welfare dependency and eligibility criteria.

OFF TOPIC SHOW: Hogan’s Death, Newsom’s $100M FireAid Theft, Arkansas’ Whites-Only Town and Clinton’s Epstein Jet Bombshell! censored.tv/watch/shows/off-…

Join us as we connect the dots, challenge the narratives, and delve into the heart of these off-topic yet deeply impactful events. Don't miss out on this exclusive content! Use code 'OFFTOPIC' for 20% off your subscription to Compound Censored and unlock a world of exclusive content. Experience the freedom of speech in its purest form, only on Compound Censored. Support Via linktr.ee/OffTopicShow

Follow Off Topic Show on Instagram:

instagram.com/videomattprese…

instagram.com/theofficialoff…

Follow On X

x.com/OffTopicShow2

Youtube

youtube.com/@OffTopicShow

Join The Community

discord.gg/FmHAEJYFTw

White Noize - Chillin -

itunes.apple.com/album/id182…

For exclusive show gear shop at stayhighlypositive.com

#FoodStampDrama #WalmartConfrontation #SNAPBenefits #WelfareDebate #RelationshipIssues #ViralVideo #PolicyChanges #SNAPCuts #WelfareFraud #PublicAssistance #compoundcensored #offtopicshow

1

2

60