Pat retweeted

12m

The setup encoded information in a microwave cavity, where losing a photon flips parity. A coupled qubit then adds a replacement photon automatically, without active monitoring. The gain was modest over the longest-lived physical qubit, but enough to reach break-even.

1

1

456

Muktabh Mayank retweeted

12m

A qubit kept correcting itself as photons leaked away, stretching its lifetime to 196 microseconds and nudging passive error correction to a long-sought threshold. @PhysRevX phys.org/news/2026-06-passiv…

1

1

3

535

James Carter retweeted

$IONQ --- $IONQ just hit an epic milestone: it sold its first **6th-generation 256-algorithmic qubit (AQ)** quantum system. On the back of this win, management jacked up full-year 2026 revenue guidance to $225M–$245M, meaning over 100% organic growth this year. Total remaining performance obligations (RPO / contract backlog) has now skyrocketed to $370 million, giving the company near-perfect revenue visibility.

$IONQ also recently announced it’s moving forward with technology asset integration with SkyWater Technology to accelerate domestic semiconductor scale manufacturing of quantum chips. It was also selected for DARPA’s HARQ program, further cementing its leadership in the national secure compute space.

In its May Q1 2026 earnings, $IONQ posted $64.7 million in revenue, up a staggering 754.7% YoY. Its loss of -$0.34 per share was also narrower than the -$0.36 analyst consensus. This completely shattered the old market narrative that quantum computing "can never generate real commercial revenue."

1. The Ion Trap Pathway Is Delivering Commercial Reality

Superconducting quantum computing requires extreme near-absolute-zero cryogenic temperatures. Ion trap technology—using laser-suspended natural ions—delivers far smaller form factors, and could eventually run in standard data center environments. $IonQ has proven this pathway isn’t just technically viable—it’s far easier to commercialize and sell as turnkey enterprise systems.

2. The Ultimate Solution to the AI Compute Crunch

As LLM parameter counts scale into the trillions, traditional silicon-based GPUs will eventually hit hard physical and power limits. Quantum computing has native, unmatched advantages for optimization algorithms, drug discovery, advanced cryptography, and complex physics simulations. The macro narrative—"AI runs on energy, and energy optimization requires quantum computing"—is now driving premium capital rotating out of legacy AI plays straight into $IonQ.

2

11

72

5,408

Today in @NaturePhysics: after many years of electrons on helium (eHe) being proposed as an excellent qubit candidate, the team at EeroQ has now brought a peer reviewed eHe qubit state to life!

This now positions eHe as a powerful new entrant in the race to build a top-tier QC, with our team eventually using the spin state of the electron to build our qubits, then scaling rapidly to 10K qubits by using standard CMOS.

This accompanies the work we have already achieved on a scalable CMOS architecture with our Wonder Lake chip done at a commercial foundry, and I am so proud of our team (and all our supporters) for this terrific result on an eHe charge qubit and can't wait to share what is coming next to bring an eHe spin qubit QC to life!

1

2

75

#China #DeepSeek #AI #SpaceRace #AIRace #quantum #teleportation #qubit #PhotonicQuantumNetwork #Light #LiFi #data #SiliconValley

Nasdaq futures slumped and technology shares slid in Japan as surging popularity of a Chinese discount artificial intelligence model wobbled investors' faith in the profitability of AI and the sector's voracious demand for high-tech chips reut.rs/3EdHEIM

1

3

1

92

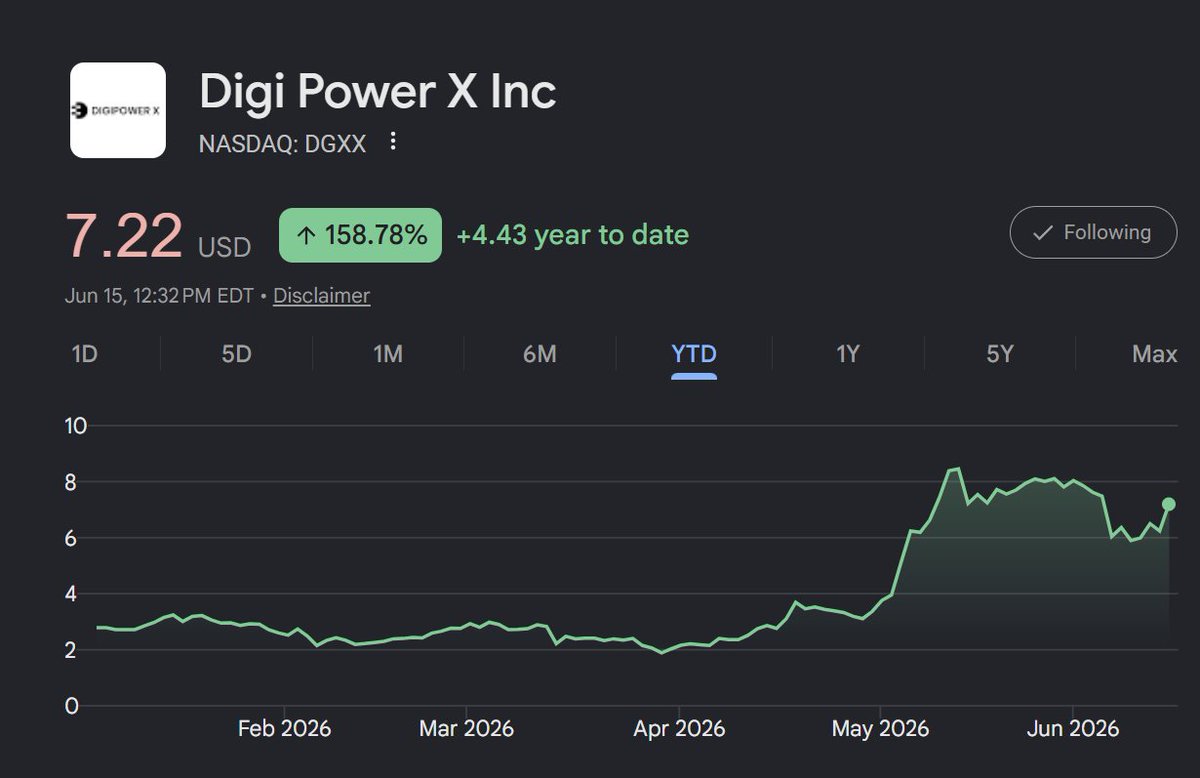

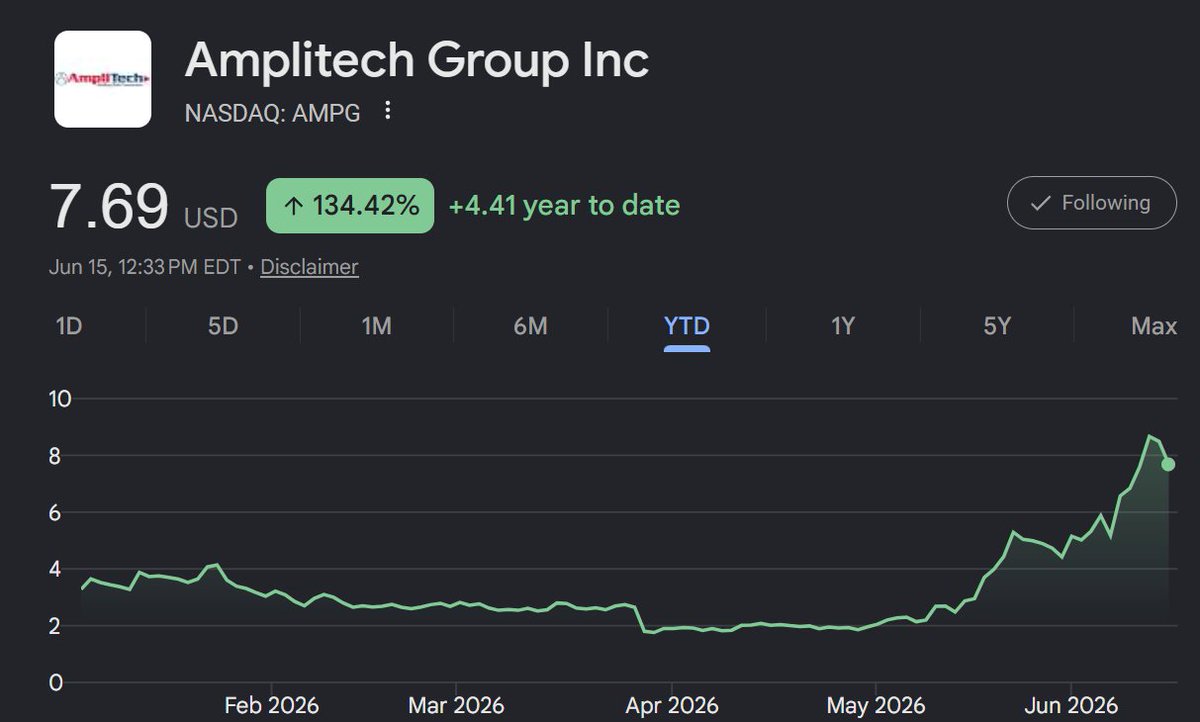

Why do I compare $AMPG ($0.2B) to $KEEL ($3.5B), $DGXX ($0.6B) and $NBIS ($66B)?

Fair question.

And the answer is bigger than people think, because AMPG isn't just in the same trend as these.

It's actually more diversified than any of them.

Let me explain properly.

Start with what they share.

They're all plays on the same thing: the physical infrastructure of the AI era.

Not the models, not the apps.

The actual hardware and buildout AI runs on.

That's the layer that quietly captures the money while everyone argues about chatbots.

$NBIS, $KEEL and $DGXX are neoclouds.

They sell AI compute out of data centers.

You need somewhere to run all this AI, so they build and rent the GPU infrastructure.

Picks and shovels for the cloud side.

Here's how I think about $AMPG: same idea, but on the tower instead of the data center.

That's what AI-RAN means.

The cell tower stops being a dumb relay and becomes an intelligent edge node, computing AI right where the data is created, in real time, because some decisions can't wait for a round-trip to a distant data center.

And the tower can't do any of it without a radio.

AMPG makes the only American 64T64R Massive MIMO radio that open AI-RAN runs on.

If a neocloud is the physical layer of cloud AI, AMPG is the physical layer of edge AI.

Honest framing: today a neocloud sells recurring compute and AMPG sells radio hardware, so the analogy is about where this is heading, the tower as the next edge data center, not a claim it's already an identical business. Same megatrend, earlier in its arc.

But here's where AMPG actually pulls ahead of a pure neocloud play.

It isn't a one-trick bet.

While the neoclouds live or die on a single thesis, AMPG has multiple real legs underneath it.

✅ Zero debt.

✅ $20M cash.

✅ $200M market cap.

✅ 48% gross margins.

➟ Leg 1, the revenue engine that exists right now:

Telus. AMPG's radio is already deployed at a Tier-1 carrier, and on the last call the COO said they "continue to receive orders against that LOI" and projected Q2 "definitely much higher than Q1.".

That's real, recurring, shipping revenue.

A lot of these pure AI-infra names are still pre-revenue or burning cash.

AMPG is selling product today at 48% gross margins.

➟ Leg 2, space.

AMPG makes the low-noise amplifiers that are the "ears" of satellites.

It shipped prototypes to a "Fortune 50 satellite systems provider" building a LEO constellation, and the only Fortune 50 doing that is Amazon with Kuiper, which then showed up on AMPG's customer wall.

(Honest framing: the wall confirms Amazon as a customer, the LEO link is my deduction, not a disclosed deal.) With SpaceX now public, the whole space sector just got validated, and AMPG is the picks-and-shovels under it.

➟ Leg 3, quantum.

AMPG makes the cryogenic amplifiers superconducting quantum computers need for qubit readout, with proof-of-concept units shipped to names like IBM and Google.

Optionality, not revenue yet, but real and patented and American.

➟ Leg 4, defense.

Lockheed, Northrop, L3Harris, Boeing, NASA on the customer wall. Relationships that take years of qualification to earn.

So put it together.

AMPG is in the exact same AI-infrastructure megatrend everyone loves the neoclouds for, except it also has real shipping revenue, a Tier-1 carrier ramping, space exposure, quantum optionality, and a defense business, all at a sub-$1B cap, debt-free, with 48% margins.

That's the part that breaks the lazy argument.

When someone says AMPG "already ran 135%" while cheering NBIS or DGXX up 160-190%, they're judging it by the chart, not the thesis.

And on the thesis, AMPG isn't behind these names.

It's the same trade, with more legs, earlier, and cheaper.

They picked the data center.

I'm adding the tower.

And the tower happens to also touch space, quantum and defense.

Not financial advice. I'm long $AMPG. DYOR. 📡

I like $NBIS. 190% .

I like $KEEL. 120% .

I like $DGXX. 160% .

But seeing people bullish on those and saying $AMPG (135%) already ran a lot, makes me think: are you OK?

They're all the same, in a growing industry, and AMPG its a truly rare of its kind, positioned for AI RAN.

I mean, everyone here knows I love all the stocks of the list, maybe NBIS a bit less, ok, give you that.

But these arguments don't make sense.

3

2

45

2,099

53m

This Chicago startup is chasing the quantum holy grail: a better qubit chicagobusiness.com/technolo… #QuantumComputing

4

Customer value and real adoption will decide quantum's impact more than qubit counts.

This Chicago startup is chasing the quantum holy grail: a better qubit chicagobusiness.com/technolo…

712

tbh the qubit count is just marketing until it beats classical on real invoices.

6

Momentum is building as Dynex prepares to welcome investors, family offices, and technology leaders to its upcoming Investor Luncheon in Toronto.

The luncheon is designed as a focused, high-level exchange on Dynex’s next stage of growth, its Canadian market strategy, and the commercial pathway for quantum-driven computing as it moves from breakthrough technology toward market deployment.

Tomorrow, @DynexQaaS and ThreeD Capital Inc. (@ThreeDCap) will host an exclusive investor evening in Toronto, bringing together investors, family offices, and technology leaders for a focused discussion on Dynex’s Canadian market strategy, technology roadmap, and investment opportunity.

At the center of the discussion will be Dynex’s proprietary Quantum-as-a-Service (QaaS) technology, its cloud-based, qubit-agnostic platform architecture, and the company’s development of end-to-end quantum-driven solutions for real-world enterprise applications.

Daniela Herrmann, CEO & Co-Founder of Dynex, will share Dynex’s growth strategy, technology roadmap, enterprise use cases, and capital markets vision with selected investors and strategic stakeholders.

Limited availability remains. We look forward to continuing the conversation in Toronto.

📍 Hy's Steakhouse & Cocktail Bar – 365 Bay St., Toronto, ON M5H 2V1, Canada

📅 Tuesday, June 16, 2026 | 12:00 PM - 2:00 PM EDT

👥 Investors, family offices, and technology leaders

RSVP and latest event details: luma.com/p44fjy91

1

2

3

41

This latest round of hyped fault-tolerant “news” — which should be taken with a grain of salt — dovetails perfectly with $IONQ Chad Sakac’s recent blog post, “Quantum Industry: We’re ALL in a ‘Put-Up or Shut-Up Moment.’”

Of course IonQ’s competitors are now trying to sing the same tune. They can’t afford to look like they’re lagging — yet even with their latest revisions and announcements, they remain well behind.

But more importantly, have any of these companies directly answered the three critical “put-up or shut-up” questions Chad Sakac posed? Absolutely not.

Chad Sakac frames three questions every quantum company should answer:

• How do you scale this?

• How do you mass manufacture this?

• What are the economics of this?

He argues these are massively under-asked, with too much focus on academic QEC progress and not enough on whether systems can actually be built, shipped, and deployed at scale.

The broader shift is that quantum is moving beyond the lab phase into commercial reality, which requires proving:

• Scalable architectures beyond a handful of systems

• A credible path to manufacturing at tens, hundreds, and eventually thousands of units

• An economic model that works at deployment scale

From an investment perspective, he argues these questions map directly onto how companies like IonQ are positioning themselves. In that framing:

• Electronic qubit control (Oxford Ionics) targets scalability

• System design aims at manufacturable, shippable architectures

• Simplified platforms improve unit economics at scale

The takeaway is that quantum companies should be viewed less like science projects and more like future industrial manufacturers. Physics defines what’s possible; engineering, manufacturing, and economics determine who wins.

medium.com/@sakacc/quantum-i…

2h

$IONQ $IBM The race to Fault Tolerance is heating up. Three companies (all with different modalities) are now projecting to deliver a fault tolerant machine before 2030:

1. IonQ: Projecting Fault Tolerant Trapped-Ion System (Unnamed) with 800 Logical Qubit by 2027.

2. QuEra: Projecting Fault Tolerant Neutral Atom System (Libra) with 100s of logical qubits by 2028.

3. IBM: Projecting Fault Superconducting Machine (Starling) with 200 Logical Qubits by 2029.

2

3

19

2,003

1h

Momentum is building as Dynex prepares to welcome investors, family offices, and technology leaders to its upcoming Investor Luncheon in Toronto.

The luncheon is designed as a focused, high-level exchange on Dynex’s next stage of growth, its Canadian market strategy, and the commercial pathway for quantum-driven computing as it moves from breakthrough technology toward market deployment.

Tomorrow, Dynex and ThreeD Capital Inc. (@ThreeDCap) will host an exclusive investor evening in Toronto, bringing together investors, family offices, and technology leaders for a focused discussion on Dynex’s Canadian market strategy, technology roadmap, and investment opportunity.

At the center of the discussion will be Dynex’s proprietary Quantum-as-a-Service (QaaS) technology, its cloud-based, qubit-agnostic platform architecture, and the company’s development of end-to-end quantum-driven solutions for real-world enterprise applications.

Daniela Herrmann, CEO & Co-Founder of Dynex, will share Dynex’s growth strategy, technology roadmap, enterprise use cases, and capital markets vision with selected investors and strategic stakeholders.

Limited availability remains. We look forward to continuing the conversation in Toronto.

📍 Hy's Steakhouse & Cocktail Bar – 365 Bay St., Toronto, ON M5H 2V1, Canada

📅 Tuesday, June 16, 2026 | 12:00 PM - 2:00 PM EDT

👥 Investors, family offices, and technology leaders

RSVP and latest event details: luma.com/p44fjy91

1

4

13

153

$QTUM Daily quantum paper digest 5/10: "Renormalization Group Flow" is more impressive, achieving end-to-end accuracy with efficient resource scaling and simplified measurement, while "Two-Qubit Hamiltonian" lacks rob...

6

Alice & Bob shifted from chipmaker to full quantum systems. Their new Helium system encodes a logical qubit using just 18 cat-qubits, up to 200x fewer hardware resources than standard approaches. Goal: fault-tolerant QC by 2030.

#QuantumComputing #QuantumTech

Source in comments

1

5

Quantum retweeted

🚀 Last week, we launched the Helium Quantum System (which is the world's first cat-qubit quantum computing platform open to research partners🤝)

The quantum industry loves milestones. 🎯

Growing qubit counts. Bigger roadmaps. Bolder promises.

Helium is something different. At its core, it's a place to explore one of the biggest challenges in quantum computing: quantum error correction. 🐈

The reality is that fault-tolerant quantum computing won't be the result of a single breakthrough. It will be an incremental journey, paved by user experimentation, careful engineering, and a deeper understanding of how to protect quantum information at scale. 🔬

That's why, instead of making predictions, we'd rather build the tools, run the experiments, and work alongside researchers to figure out what actually works.

That's the idea behind Helium! ⚡

If you'd like to learn more about the platform, the vision behind it, and why we built it, we've shared the story in a short blog post.

Read here 👉 alice-bob.com/blog/this-is-n…

#QuantumComputing #QuantumErrorCorrection #CatQubits #FaultTolerantQuantumComputing #Research #HPC #DeepTech

1

7

245