Jun 15

The EU is mobilizing €3 billion to cut dependency on single suppliers for critical raw materials by 50% by 2029. The RESourceEU Action Plan aims to bolster battery, rare earth & defence value chains. ⛓️

insights.policy-insider.ai/?…

#CRMA #SupplyChain

10

🇪🇺⚗️ Philippe Kehren, CEO of Solvay, just gave one of the clearest and most honest assessments of Europe's industrial position I've heard from a major CEO.

Worth your time. Every quote below is verbatim. 🧵

🎬 Watch the full interview 👇

🏭 On Solvay and supply chain resilience:

"We have more than 80% of our sales done regionally. It's very important to be close to the market, close to your customers."

"I think now it's over — we have to get back to shorter logistic chains and to get back to raw materials and energies that are available locally."

"When you are a leader in your market, you master your technologies, you master your processes and you can adjust very quickly. If overnight you cannot buy anymore a certain type of raw material from a certain location, you're able to change very quickly."

🌍 On whether Europe can compete:

"Yes — Europe has everything to be competitive and sustainable in the future. It has the best engineers, technicians, operators, assets. One of the most efficient chemical production units in the world are based in Europe."

And then the line that should make every European policymaker pause:

"A lot of the pain we suffer today has been self-inflicted."

🧲 On rare earths — and this is the part the critical minerals community needs to hear:

"Rare earth is a good example. We've outsourced completely the production of rare earth material for permanent magnets. Between 90 and 100% of those materials today come from China."

"The plant in La Rochelle is in fact unique outside of China. It's the only plant outside of China that is able to produce any type of rare earth material from any type of source. We've been doing that for more than 75 years — this plant started up in 1948."

"We know how to produce those materials. We can do it very quickly. But we need to have the value chain. We need to have buyers. We need to have contracts with volumes and prices. This is today what is missing in order to invest further."

That last sentence is the most important line in the entire interview.

Europe has the only plant outside Asia capable of processing every major rare earth element at industrial scale. It has been operating for 78 years. It inaugurated a new magnet-grade production line in April 2025.

And it still cannot get enough long-term offtake contracts from European OEMs and magnet manufacturers to justify the next investment round.

⚡ On energy — the other half of the industrial sovereignty equation:

"We need to have competitive energy in the long run by developing nuclear, by developing renewable energy, ways to store renewable energy, hydro... We decided not to produce gas in Europe — that's a fair choice. But you cannot say I don't develop nuclear neither. You need something."

"We see today that the countries that have decided to have nuclear production are more competitive and more sustainable."

For energy-intensive processes like rare earth solvent extraction — large heated mixer-settler circuits running 24/7 — this isn't abstract policy. It is the difference between a viable OPEX profile and a structural cost disadvantage versus Chinese producers who operate on subsidised industrial power.

🔧 On the CO2 transition and industrial competitiveness:

"If you pay at the same time those projects that are very expensive plus the CO2 quotas because you have a large deficit, you pay the energy transition twice."

"We need to support the industrials that are doing this by giving them the right level of incentives and CO2 quota so that they can indeed pay this transition and solve at the same time their competitiveness challenge."

"It's perfectly compatible to do the energy transition and at the same time be competitive and secure an industrial production in Europe."

💷 On floor prices for strategic materials — a specific, concrete policy proposal:

"One way to unlock this situation would be to set floor prices — to say we guarantee you a certain minimum level of price so that you can secure the return on your investment — and that in that way it would not penalise the customers neither. It's a nice way to diversify and de-risk something that can be strategic."

This is Solvay's direct ask to European policymakers. Not grants. Not subsidies. Price floors for strategic materials — the same mechanism used in the UK for offshore wind contracts (CfD), now proposed for rare earth oxides and critical chemical intermediates.

🔑 On what "economic security" actually means:

"Economic security is really about looking at the value chains. In the past we had this idea that you look at the final product and then you can produce all the rest of the pieces anywhere else. I think that's not completely true."

"It doesn't mean we will produce 100% locally of course, but we need to at least master all the elements of the value chain and master the processes of the different pieces. That's very important so that you can create optionalities and be in control."

"Be in control is really what is very important in the current circumstances."

🌍 The bigger picture Kehren is describing

Europe's industrial model is at an inflection point. High energy costs, dependence on Chinese critical materials, and competition from both Chinese state-backed industry and US subsidy-backed manufacturing (IRA, CHIPS Act) are simultaneously compressing the space for European companies to operate competitively.

Kehren's argument — and Solvay's position illustrates it precisely — is that the response cannot be either purely market-led or purely policy-driven. It requires:

✅ Policy frameworks that make long-term investment decisions credible (stable energy prices, joint procurement, offtake support)

✅ Industry commitment to building the full value chain — not just individual nodes

✅ OEM and downstream manufacturers actually signing the long-term supply agreements that anchor project finance

✅ Financial institutions moving at the speed the geopolitical situation demands

📍 The September 2026 milestone running in parallel:

While Kehren makes the case for policy support, Solvay is already moving. Industrial-scale Dy and Tb separation at La Rochelle is targeted for September 2026 — dysprosium and terbium, the two heavy rare earths under active Chinese export controls, at the only facility outside Asia capable of separating them at industrial throughput.

The policy argument and the commercial delivery are happening simultaneously. The question is whether European OEMs, magnet manufacturers, and policymakers move fast enough to match it.

@SolvayGroup

#Solvay #PhilippeKehren #LaRochelle #RareEarths #REE #CriticalMinerals #EuropeanSovereignty #IndustrialSovereignty #CriticalRawMaterials #CRMA #RESourceEU #EuropeanCompetitiveness #EnergyPrices #Nuclear #EnergyTransition #CleanIndustrialDeal #NdFeB #PermanentMagnets #Neodymium #Praseodymium #Dysprosium #Terbium #MagnetGrade #REOSeparation #SolventExtraction #HeavyRareEarths #HREO #LREO #FloorPrices #StrategicAutonomy #CarbonNeutral #CO2 #ETS #EuropeanIndustry 🇪🇺🇫🇷🇧🇪⚗️🧲🔬💡🏭⚡🌍🔑🎬

2

1

8

477

Jun 12

De druk van China na Nexperia, de blokkade van de Straat van Hormuz door Iran en het buitenlandbeleid van de Verenigde Staten. Drie voorbeelden die volgens Peter de Jong zien dat we in een wereld van geo-economie leven.

Nederland en Europa zijn te afhankelijk geworden van kwetsbare ketens voor kritieke grondstoffen, schrijft Peter. ResourceEU en de Critical Raw Materials Act zijn stappen vooruit, maar blijven vooral defensief zolang de vraag naar nieuwe grondstoffen blijft groeien.

De vraag is daarom niet alleen hoe Europa meer kan mijnen, raffineren of recyclen. De vraag is hoe we minder afhankelijk worden door slimmer te ontwerpen, langer te gebruiken, beter te repareren en kritieke materialen hoogwaardiger in te zetten.

Circulariteit is daarmee een voorwaarde voor een weerbaar energiesysteem.

Lees hier de bijdrage: energiepodium.nl/item/een-we…

2

343

May 30

突發快點|歐盟對中國態度大轉彎?布魯塞爾醞釀新防線 中歐貿易戰陰影正在逼近

歐盟執委會5月29日罕見發出強烈訊號,直言目前歐中貿易與投資關係「不可持續」,並宣布將研究更強硬措施,保護歐洲產業免受中國商品大量湧入衝擊。這是近年來歐盟對中國最直接、最嚴厲的政策表態之一。

根據路透社披露,歐盟官員正在討論多項新工具,包括要求歐洲企業分散供應鏈、降低對中國依賴,以及建立新的貿易機制,限制中國在化工、金屬及綠色能源科技等領域進一步擴大市場影響力。相關方案預計最快今年第三季提出。

歐盟認為,中國在電動車、太陽能設備、電池及關鍵原材料領域的產能快速擴張,已對歐洲製造業形成巨大壓力。雖然歐盟去年已對中國電動車加徵關稅,但中國品牌在歐洲市場占有率仍持續上升。

值得注意的是,此舉與美國特朗普政府推動的「美國優先」產業政策形成某種呼應。歐盟近期也提出「購買歐洲貨」(Buy European)及RESourceEU計畫,希望建立自主供應鏈,減少對中國關鍵礦產及工業產品的依賴。

北京方面則迅速反擊。中國外交部批評歐盟選擇性引用貿易數據,並警告若歐盟推動新的技術主權及產業保護政策,中方將採取「強力反制措施」。

市場分析人士指出,如果歐盟最終跟隨美國加強對中國商品與投資限制,全球兩大消費市場與全球最大製造中心之間的摩擦恐將進一步升級。2026年下半年,中歐經貿關係可能成為全球經濟最大的風險變數之一。

資料來源:路透社

reuters.com/world/china/euro…

4

2

8

2,799

May 27

📄 The Batteries Regulation. The Industrial Accelerator Act. The RESourceEU Action Plan.

🇪🇺 Europe's policy framework for battery circularity is taking shape and the innovation ecosystem is responding.

Our new @EPOorg/@IEA report maps the full picture: epo.org/insight-battery-circ…

1

5

9

283

At the CCMI May Bureau, the ResourceEU Action Plan was adopted, calling for a strategic approach to #CriticalRawMaterials to build #preparedness and resilience 💪

Thanks to our rapporteurs, @Diamantouros and @Agata_Meysner 🤝

Read more ➡️link.europa.eu/BT3KmM

5

69

Sécuriser la demande, déjouer les pressions, éviter les pénuries…

Aujourd’hui lors de la réunion du G7 sur les métaux critiques, j’ai rappelé 3 priorités :

💎 Concentrer notre action sur une sélection commune de métaux critiques prioritaires - probablement les plus stratégiques, c’est à dire ceux indispensables à nos économies et pour lesquels nous dépendons collectivement (totalement ou presque) d’un seul fournisseur.

⛏️ Augmenter et diversifier nos sources d’approvisionnement, en partant des projets existants (l’UE soutient 60 projets d’extraction, de raffinage et de recyclage en cours dans le cadre de ReSourceEU 🇪🇺)

🧰 Se doter d’une boîte à outils efficace pour sécuriser la demande, et éviter que nos industries n’achètent que des matières premières critiques venues de Chine.

Merci à la présidence 🇫🇷 du @G7 et à @RolandLescure pour ces efforts en vue d’aboutir à des avancées concrètes. Nous sommes sur un bon chemin!

26

50

116

7,857

Apr 28

As an aside, the plant should benefit from the EU’s restrictions on rare earth waste exports, planned for later in '26.

(The ResourceEU plan aims to stop the bloc exporting valuable waste rich in rare earths, only to re-import finished magnets from third countries.)

2/2

16

571

#欧州委員会 は現在立法提案に向けて進めている #RESourceEU行動計画 において、2026年第2Qまでに希土類永久磁石のスクラップ及び廃棄物の輸出制限を提示し #アルミスクラップ に対するターゲット的措置を提示することを確認しました。

single-market-economy.ec.eur…

4

112

🇪🇺 The European Union has launched its critical minerals platform to boost supply chain resilience & cut reliance on dominant producers. 🌍⛏️

🛡️ Part of REsourceEU, it connects buyers & suppliers for key materials. 📅 Results due Sept.

tinyurl.com/2kwpj62r

1

4

300

Apr 15

I remain sceptical that Europe can speed up new mine approvals in a meaningful way.

Industry analysts share this view.

True, the EU is attempting a structural shift through the Critical Raw Materials Act (CRMA), which entered into force in May 2024.

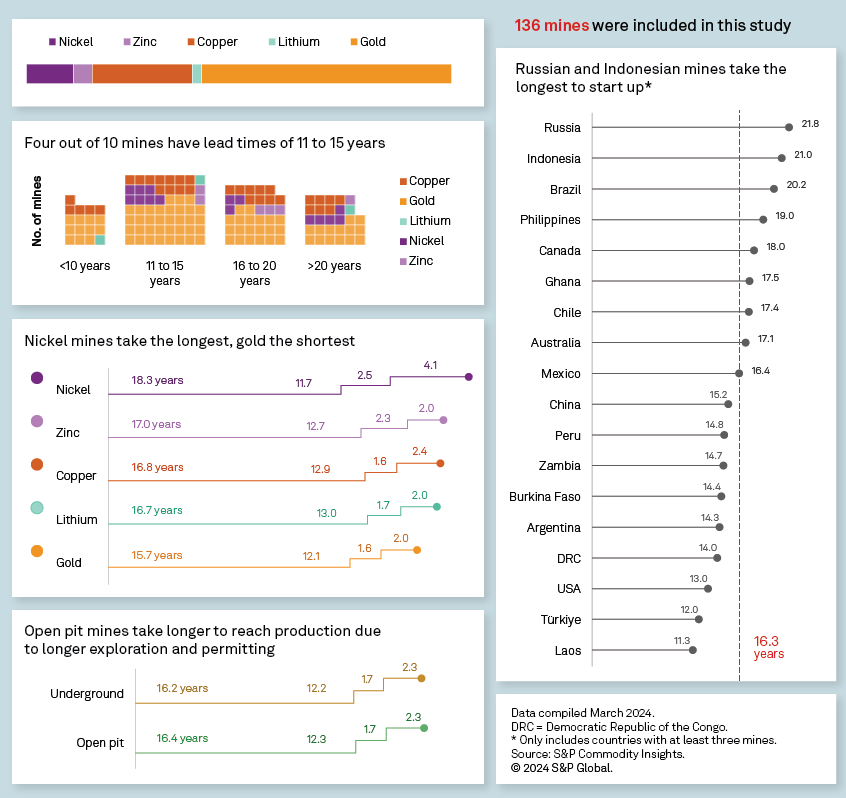

The CRMA aims to cut permitting times to a maximum of 27 months for extraction and 15 months for processing/recycling. The global average is 16 years, so this could be monumental if it works.

But there are deeper issues.

What has changed

- Strategic project designation: The EC adopted the first 47 strategic projects within the EU and 13 outside it in March 2025, representing over €22.5 billion in investments. These projects, including lithium in France and Germany, graphite in Sweden, receive "highest national significance" status for faster permitting.

- 2030 goals: The CRMA aims for 10% of EU critical raw materials consumption to be mined domestically by 2030. A sharp rise from the ~1% currently.

- Pipeline: Examples include the Keliber lithium project in Finland and Vulcan's Zero Carbon Lithium in Germany, with production slated for the late 2020s/early 2030s.

Why doubts remain

- Implementation gaps: While the EU sets rules, national and local authorities often hold the actual power, leading to potential analysis paralysis at the local level.

- Legitimacy challenge: Opposition remains strong. Local NIMBY sentiments can override EU-level approval.

- Financing: Projects need massive, high-risk capital. Accelerating permits doesn't guarantee funding or commercial viability.

- Quality: Europe's mineral resources are generally lower grade, making domestic mining less cost-effective. This may hinder development even with faster permits.

The next 12-24 months will be crucial. RESourceEU, an action plan unveiled in December 2025, aims to further amend the CRMA to further simplify permitting, highlighting that the 2024 framework is already being refined to tackle slow adoption.

In my view, these initiatives are useful and I hope there is progress. However, the Americas and Australia seem more attractive, with substantial upside in resource-rich regions like Brazil.

We shall see.

4

7

23

2,239

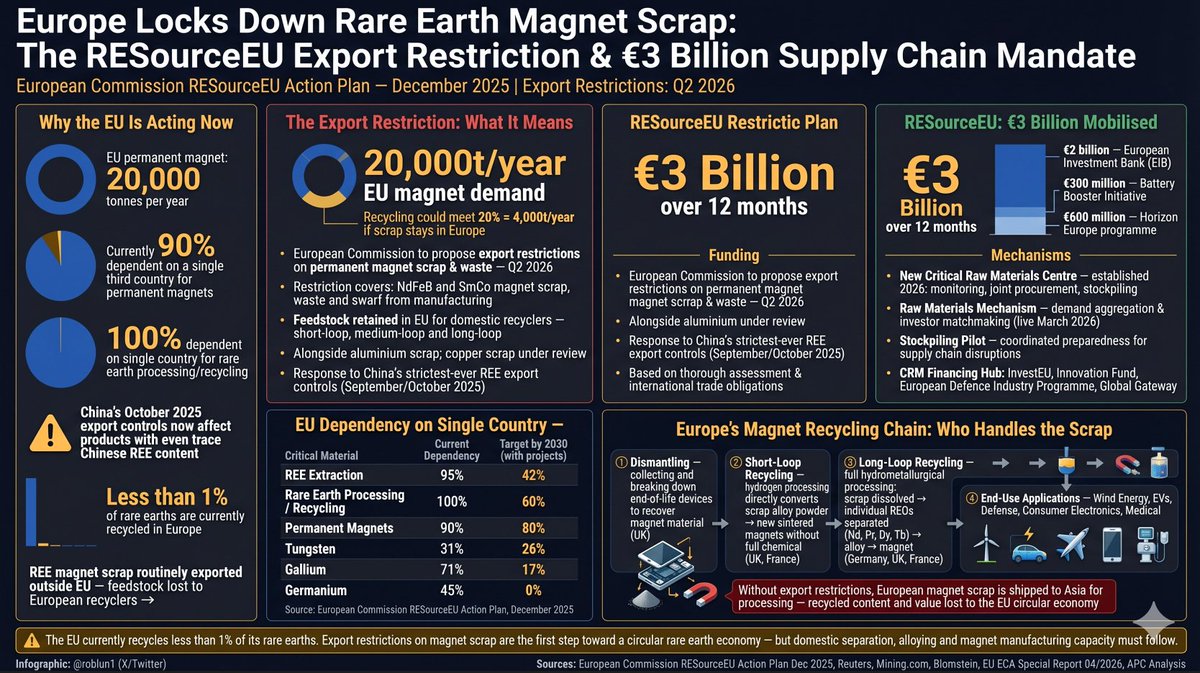

🚨 Europe is about to lock the door on rare earth magnet scrap exports — and it changes everything for EU magnet recyclers.

The European Commission's RESourceEU Action Plan, announced December 3, 2025, confirmed that export restrictions on rare earth permanent magnet scrap and waste will be proposed by Q2 2026.

The logic is simple but long overdue: Europe generates thousands of tonnes of end-of-life NdFeB magnet scrap every year from EVs, wind turbines, industrial motors and consumer electronics — and instead of recycling it domestically, most of that feedstock leaves the EU, gets processed in Asia, and the separated rare earth oxides are sold back to Europe at a premium.

The restriction closes that loop. Scrap that stays in Europe becomes feedstock for European short-loop and long-loop recyclers — and with €3 billion mobilised by the Commission over the next 12 months, the infrastructure to process it is being built right now.

To promote recycling within the EU, the bloc is expected to impose export restrictions on rare earth permanent magnet scrap in early 2026.

This measure is a key component of the EU's REsourceEU package. The recycling potential for rare earth permanent magnets is substantial, projected to meet 20% of the EU's current demand for 20,000 mt of permanent magnet materials. As a critical material for EVs, national defense, and renewable energy, the importance of permanent magnets is self-evident.

EU to curb exports of recyclable battery, rare earth waste to cut China reliance⏬

reuters.com/world/china/eu-i…

📊 The numbers behind the mandate:

🧲 EU permanent magnet demand: 20,000t/year

♻️ Recycling potential if scrap stays in EU: ~4,000t/year (20% of demand)

🔴 Current recycling rate of rare earths in Europe: <1%

🇨🇳 EU dependency on single country for REE processing: 100%

🎯 RESourceEU target by 2030: reduce that to 60%

The gap between where Europe is and where it needs to be is vast. The export restriction is the first structural lever to close it.

🗺️ Europe's magnet recycling chain is small but growing:

🔧 Dismantling — collecting EoL devices, recovering magnet material

⚡ Short-loop — hydrogen processing: scrap alloy → new sintered magnet (no separation needed)

🔬 Long-loop — full hydromet: dissolve → separate Nd, Pr, Dy, Tb → alloy → magnet

Key players span UK, Germany & France across every stage of this chain — from scrap collection to pure oxide separation.

Without domestic feedstock guarantees, none of these recyclers can scale. The export restriction fixes the feedstock problem at source.

💰 How €3 billion is being deployed:

🏦 €2B — European Investment Bank

🔋 €300M — Battery Booster Initiative

🔬 €600M — Horizon Europe

New structures being stood up:

✅ Critical Raw Materials Centre — monitoring, joint procurement, stockpiling (2026)

✅ Raw Materials Mechanism — matchmaking buyers, investors, stockpile services (live March 2026)

✅ Stockpiling Pilot — supply chain disruption preparedness

✅ Chinese entities restricted from HorizonEU CRM Work Programme

🔑 The strategic logic in one paragraph:

China controls ~90% of global REE processing. In October 2025, Beijing tightened export controls to cover even trace Chinese-origin content in magnets. Europe's response via RESourceEU is not just funding — it is structural: keep the scrap, build the recyclers, reduce the dependency.

The target: cut rare earth processing dependency from 100% to 60% by 2030.

The tool: export restrictions €3B a domestic circular magnet economy.

That window is open now. 🪟

Critical Raw Materials for Energy Transition, Special Report 04/2026 PDF ⏬

eca.europa.eu/ECAPublication…

RESourceEU Action Plan⏬

single-market-economy.ec.eur…

#RareEarths #CriticalMinerals #RESourceEU #MagnetRecycling #CircularEconomy #NdFeB #EUGreenDeal #CriticalRawMaterials #SupplyChainResilience #EuropeanCommission #MagnetScrap #RareEarthRecycling #EVSupplyChain #WindEnergy #DefenseSupplyChain #CRMA

5

23

2,134

The platform connects buyers to suppliers and is part of the bloc’s RESourceEU strategy, announced in December to develop its supply chains for rare earths and other strategic minerals needed for the energy transition and defence applications.

1

3

1,006

📢 Open until 14 April 2026! Call for evidence: Support on the Revision of the Water Framework Directive #WFD

The @EU_Commission is gathering feedback to support a targeted revision of the #WFD under the #RESourceEU Action Plan on Critical Raw Materials.

Feedback is expected from:

🔹 Businesses in the critical raw materials value chain

🔹 Civil society organisations

🔹 Water management companies

🔹 National & regional authorities

🌊 For the #MSP community, this is one to watch: coastal and transitional waters fall under the #WFD

👇 More info down below & here! maritime-spatial-planning.ec…

Mar 17

EU water legislation must work effectively 💧🔎

Today, we launched a call for evidence to support a targeted revision of the EU Water Framework Directive

We call stakeholders & businesses to participate, particularly those affecting EU water bodies

>>> link.europa.eu/BdD3RM

1

2

92

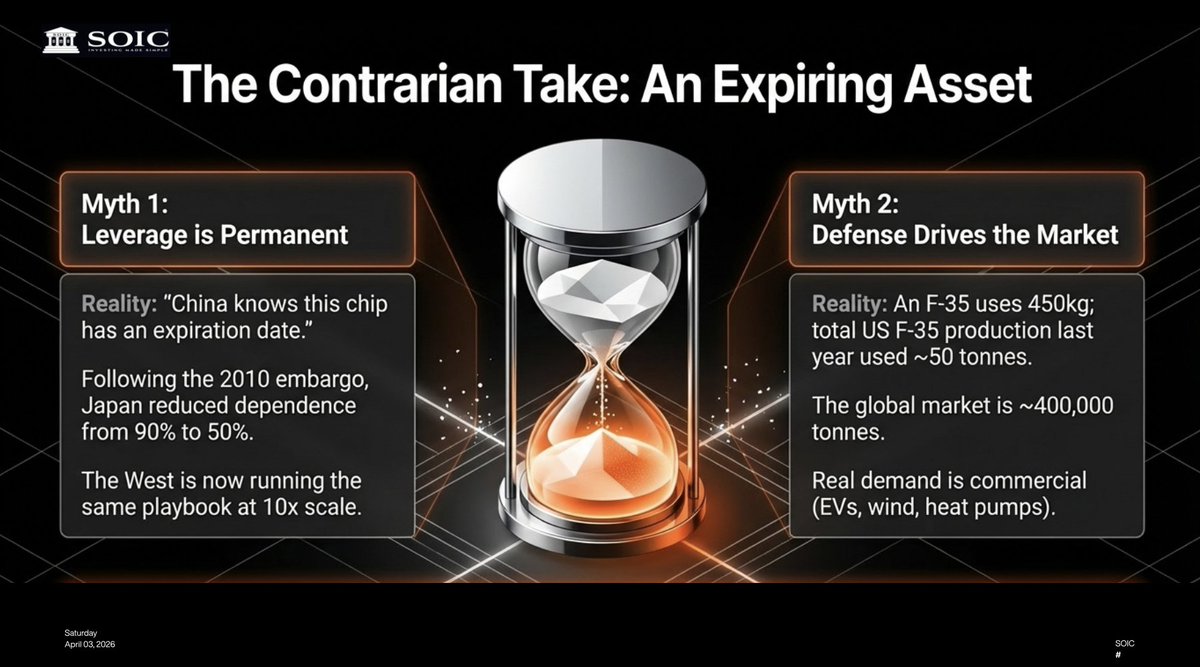

The Contrarian Take: China's Card Has an Expiration Date

Most coverage frames China's rare earth dominance as permanent and insurmountable. But there is another lens at which one can look at this -

China knows that this rare-earths chip has an expiration date, so they may as well play it now while it still has value.

The reasoning is sound. After the 2010 rare earth crisis (when China cut exports to Japan over a territorial dispute), Japan systematically reduced its dependence from ~90% to ~50%, and heading toward 50% this year. Japan invested in Lynas (Australia's largest non-China producer), built stockpiles, developed recycling technology, and diversified sources.

The same playbook is now being adopted globally, but at 10× the scale and urgency. The US DoD is directly investing equity in producers. The EU launched RESourceEU for joint purchasing and stockpiling. Norway discovered Europe's largest rare earth deposit. Australia's Iluka is building integrated processing. India just dropped an RFP for 6,000 MTPA of magnet capacity.

China's rare earth leverage is a wasting asset. The longer they wait to play it, the less leverage they'll have. April 2025 was Beijing's window of maximum impact — and even then, the partial suspension in November showed that China couldn't sustain maximum pressure without self-harm.

1

3

1,016

Mar 31

The EU has now produced:

— A Green Deal

— A Green Deal Industrial Plan

— A Net-Zero Industry Act

— A Critical Raw Materials Act

— A Clean Industrial Deal

— A Competitiveness Compass

— A RESourceEU Action Plan

— A RePowerEU framework

The Commission has published so many strategic documents that one could be forgiven for thinking Brussels mistakes mapmaking for travel.

1

10

363

📰 Monitoring regulacyjny PKEE 23–29.03.2026

W Brukseli dużo się dzieje - i to na kilku poziomach jednocześnie. Z jednej strony szybkie działania osłonowe i presja cenowa, z drugiej coraz więcej znaków zapytania przy kluczowych elementach polityki klimatycznej UE. W najnowszym wydaniu monitoringu zanalazły się takie kwestie, jak:

⚡ Presja na zmiany w ETS i rola systemu w reakcji na kryzys energetyczny

Komisja Europejska analizuje zmiany w systemie ETS – w tym zawieszenie mechanizmu automatycznego unieważniania nadwyżek uprawnień w rezerwie stabilizacyjnej, co ma zwiększyć elastyczność systemu w obliczu rosnącej zmienności cen CO₂. Propozycje, które mają zostać przedstawione przed Wielkanocą, są odpowiedzią na naciski części państw Unii, związane z wysokimi cenami energii w kontekście obecnych napięć geopolitycznych. Szerszy kontekst stanowi rosnąca presja cenowa mimo stabilnych dostaw energii, co – jak wskazał Komisarz ds. Energii, Dan Jørgensen, podczas debaty plenarnej Parlamentu Europejskiego – ponownie uwidacznia strukturalną zależność Unii Europejskiej od paliw kopalnych. W odpowiedzi UE rozważa dostosowania w ETS, ale i działania krótkoterminowe – np. większą elastyczność pomocy publicznej czy instrumenty osłonowe dla odbiorców. Równolegle trwa spór instytucjonalny dotyczący podstawy prawnej tych działań, w tym – możliwości wykorzystania art. 122 TFUE, odzwierciedlając napięcie między oczekiwaniami szybkiej reakcji a zachowaniem równowagi instytucjonalnej.

🌱 Niemcy sygnalizują potrzebę większej elastyczności w celach klimatycznych Unii

Niemiecka Minister Gospodarki i Energii, Katherina Reiche, wezwała do większej elastyczności w realizacji celu neutralności klimatycznej UE do 2050 r. wskazując, że dopuszczalne powinno być niewielkie odchylenie od poziomu zerowych emisji. W jej ocenie zbyt rygorystyczne podejście do celów klimatycznych może negatywnie wpływać na konkurencyjność przemysłu, zwłaszcza energochłonnego. Minister wskazała ponadto na potrzebę większego wykorzystania krajowych zasobów energetycznych i rewizji części polityk wspierających odnawialne źródła energii w kontekście kosztów i bezpieczeństwa dostaw. Jednocześnie Kanclerz Niemiec – Friedrich Merz – zadeklarował, że jeśli kryzys energetyczny będzie się utrzymywał, nie wyklucza wydłużenia funkcjonowania istniejących elektrowni węglowych. Wypowiedzi te wpisują się w szerszą debatę w Unii Europejskiej o równowadze między transformacją energetyczną a utrzymaniem wzrostu gospodarczego.

🏛️ Wstępne porozumienie w sprawie ETS2 w Parlamencie Europejskim

Europosłowie z głównych centrowych grup politycznych osiągnęli wstępne porozumienie dotyczące zmian w rezerwie stabilizacyjnej systemu ETS2, obejmującego sektor budynków i transportu, zasadniczo popierając propozycję Komisji Europejskiej. Kluczową modyfikacją jest przywrócenie klauzuli wygaszającej, przewidującej stopniowe unieważnianie niewykorzystanych uprawnień w rezerwie po 2031 r., by ograniczyć nadpodaż w dłuższym okresie. W części niewiążącej dokumentu posłowie apelują o wzmocnienie mechanizmu ograniczającego ceny uprawnień – w tym jego wydłużenie poza 2029 r., dostosowanie do bardziej aktualnego poziomu cen i szybszą reakcję w przypadku przekroczenia progu. Wskazano również na możliwość rozważenia czasowych wyłączeń dla budynków mieszkalnych w określonych warunkach. Głosowanie w komisji Środowiska PE (ENVI) planowane jest na połowę kwietnia br.

🏭 Debata w komisji ITRE o polityce przemysłowej i kosztach energii

Podczas dialogu strukturalnego w komisji ITRE PE 24 marca br., wiceprzewodniczący wykonawczy Komisji Europejskiej – Stéphane Séjourné – wskazał, że rosnące koszty energii, napięcia geopolityczne i presja konkurencyjna wymagają przyspieszenia działań na rzecz wzmocnienia bazy przemysłowej UE. Przedstawiony przez KE Industrial Accelerator Act ma łączyć cele dekarbonizacji, konkurencyjności i bezpieczeństwa, m.in. przez rozwój produkcji w Unii, prostsze procedury inwestycyjne oraz wzmocnienie zasad dotyczących inwestycji zagranicznych. Istotnym elementem dyskusji była także rola ETS, który według KE powinien w większym stopniu wspierać inwestycje w modernizację i dekarbonizację przemysłu. Europosłowie zwracali uwagę na wysokie ceny energii jako kluczowe wyzwanie dla przemysłu i na konieczność szybkiego wsparcia sektorów energochłonnych, przy zachowaniu równowagi między otwartością handlową a wzmacnianiem produkcji w UE.

🔌 Europejski Pakiet Sieciowy - wspólne wystąpienie organizacji

Stowarzyszenia EURELECTRIC, DSO Entity, E.DSO, EDEC i GEODE pozytywnie oceniają Europejski Pakiet Sieciowy z grudnia 2025 r., podkreślając jego znaczenie dla planowania, wydawania pozwoleń i przyłączeń do sieci. Organizacje doceniają m.in. propozycje przyspieszenia procedur administracyjnych, rewizję TEN-E i podejście obejmujące inwestycje wyprzedzające. Jednocześnie krytykują m.in. niedostateczne uwzględnienie planowania oddolnego, brak dedykowanego finansowania dla operatorów systemów dystrybucyjnych oraz trudności we wdrożeniu części proponowanych rozwiązań.

🇪🇺🇬🇧 Negocjacje Unii Europejskiej z Wielką Brytanią w sprawie rynku energii elektrycznej

Kraje Unii upoważniły Komisję Europejską do rozpoczęcia negocjacji w sprawie ponownego włączenia Wielkiej Brytanii do rynku energii elektrycznej UE, co stanowi element szerszego resetu relacji po Brexicie. Mandat negocjacyjny obejmuje też rozmowy o wkładzie finansowym Brytyjczyków do funduszy spójności, jako warunku dostępu do jednolitego rynku. Oczekuje się, że reintegracja rynków energii zaowocuje niższymi cenami energii, większą stabilnością systemów elektroenergetycznych i przyspieszeniem inwestycji w OZE, przede wszystkim w regionie Morza Północnego. Jednocześnie negocjacje mogą być trudne ze względu na wrażliwość polityczną kwestii wkładu finansowego po stronie brytyjskiej.

📉 Spadek importu energii do Unii Europejskiej przy zmianie struktury dostaw

Jak wynika z danych Eurostatu, w 2025 r. UE odnotowała dalszy spadek importu energii – tak pod względem wartości, jak i wolumenu – co wpisuje się w trend obserwowany od 2022 r. Wartość importu wyniosła 336,7 mld euro, a wolumen 723,3 mln ton, przy czym szczególnie wyraźny był spadek w segmencie produktów ropopochodnych. Istotnie wzrósł przy tym import LNG – zarówno wartościowo, jak i ilościowo – podczas gdy wolumen importowanego gazu rurociągowego zmniejszył się. Struktura dostaw pozostaje skoncentrowana, z dominującą rolą USA w imporcie LNG i produktów ropopochodnych oraz Norwegii w dostawach gazu rurociągowego, co pokazuje utrzymującą się – mimo ogólnego spadku importu – zależność Unii od ograniczonej liczby partnerów zewnętrznych.

🔋 Postęp prac nad rewizją Critical Raw Materials Act (CRMA)

Prace nad rewizją CRMA wchodzą w kolejną fazę wraz z publikacją projektu raportu, przygotowanego przez sprawozdawcę Mohammeda Chahima z S&D. Proponowane zmiany, będące elementem planu RESourceEU, koncentrują się na zwiększeniu bezpieczeństwa dostaw surowców krytycznych i ograniczeniu zależności od importu, zwłaszcza z Chin. Projekt przewiduje uproszczenie procedur dla projektów strategicznych, zwiększenie celów recyklingu i rozwój rynku surowców wtórnych, przy rozszerzeniu zasad dotyczących odzysku materiałów. Wzmocniona ma zostać również rola KE w monitorowaniu ryzyk w łańcuchach dostaw i nadzorze nad działaniami firm. Inicjatywa ma na celu poprawę warunków inwestycyjnych i zwiększenie przewidywalności regulacyjnej. Głosowanie w komisji ITRE planowane jest na czerwiec, a głosowanie plenarne – na lipiec br.

🔌 Debata o Pakiecie Sieciowym i barierach dla inwestycji infrastrukturalnych

24 marca br. odbyła się debata poświęcona Europejskiemu Pakietowi Sieciowemu, zorganizowana przez ZPP w Europejskim Komitecie Ekonomiczno-Społecznym w Brukseli. Dyskusja, z udziałem m.in. europosłanki Andrei Wechsler i przedstawiciela KE, koncentrowała się na barierach dla inwestycji – w szczególności w zakresie procedur wydawania pozwoleń i przyłączeń do sieci, które spowalniają rozwój infrastruktury. Uczestniczący w spotkaniu, jako jeden z panelistów, @Ryszard_Pawlik – Kierownik Biura #PKEE w Brukseli – podkreślał z kolei konieczność odpowiedniego uwzględnienia w Pakiecie roli i wyzwań, stojących w UE przed operatorami systemów dystrybucyjnych.

1

6

1,030

Mar 30

📰 PKEE Regulatory Monitoring 23–29.03.2026

A lot is happening in Brussels - and on multiple fronts at once. On the one hand, rapid short-term response measures and rising price pressure; on the other, increasing uncertainty around key elements of EU climate policy. In this week’s edition, we cover:

⚡ Pressure to adjust the ETS and its role in responding to the energy crisis

The European Commission is assessing changes to the ETS, including the suspension of the automatic cancellation of surplus allowances in the Market Stability Reserve, in order to increase system flexibility amid growing carbon price volatility. The proposals, expected before Easter, respond to pressure from several member states facing high energy prices in the context of current geopolitical tensions. The broader context is rising price pressure despite stable physical energy supply, which – as Energy Commissioner Dan Jørgensen highlighted during the European Parliament plenary debate – once again exposes the EU’s structural dependence on fossil fuels. In response, the EU is considering both ETS adjustments and short-term measures such as more flexible state aid and consumer protection tools. At the same time, an institutional debate is ongoing over the legal basis for such actions, including the potential use of Article 122 of the Treaty, reflecting tensions between the need for rapid response and maintaining institutional balance.

🌱 Germany signals the need for greater flexibility in EU climate targets

Germany’s Minister for Economic Affairs and Energy, Katherina Reiche, has called for greater flexibility in achieving the EU’s 2050 climate neutrality target, suggesting that a limited deviation from full net-zero emissions should be acceptable. She argued that overly rigid climate targets may negatively affect industrial competitiveness, particularly for energy-intensive sectors. The minister also pointed to the need for increased use of domestic energy resources and a review of certain renewable support policies in light of costs and security of supply. At the same time, German Chancellor Friedrich Merz indicated that, should the energy crisis persist, extending the operation of existing coal-fired power plants cannot be ruled out. These statements feed into a broader EU debate on balancing the energy transition with economic growth.

🏛️ Preliminary agreement on ETS2 in the European Parliament

MEPs from the main centrist political groups have reached a preliminary agreement on changes to the Market Stability Reserve under ETS2, covering buildings and transport, largely supporting the European Commission’s proposal. The key modification is the reinstatement of a sunset clause, providing for the gradual cancellation of unused allowances in the reserve after 2031 to limit long-term oversupply. In the non-binding part of the text, MEPs call for strengthening the price containment mechanism, including extending it beyond 2029, aligning it with more recent price levels and ensuring a faster response when thresholds are exceeded. They also point to the possibility of temporary exemptions for residential buildings under certain conditions. A vote in the Parliament’s Environment Committee (ENVI) is scheduled for mid-April.

🏭 ITRE committee debate on industrial policy and energy costs

During the structured dialogue in the European Parliament’s ITRE committee on 24 March, Commission Executive Vice-President Stéphane Séjourné stressed that rising energy costs, geopolitical tensions and competitive pressure require accelerated action to strengthen the EU’s industrial base. The proposed Industrial Accelerator Act aims to combine decarbonisation, competitiveness and security, including through boosting EU-based production, simplifying investment procedures and strengthening rules on foreign investment. The role of the ETS was also highlighted, with the Commission indicating it should better support investment in industrial modernisation and decarbonisation. MEPs pointed to high energy prices as a key challenge for industry and called for faster support to energy-intensive sectors, while maintaining a balance between openness and strengthening EU production.

🔌 European Grids package – joint industry position

Industry associations including EURELECTRIC, DSO Entity, E.DSO, EDEC and GEODE welcomed the European Grids package presented in December 2025, highlighting its importance for planning, permitting and grid connections. They positively assessed proposals to accelerate administrative procedures, revise TEN-E rules and support anticipatory investments. At the same time, they raised concerns about insufficient recognition of bottom-up planning, the lack of dedicated funding for distribution system operators and challenges related to the implementation of certain measures.

🇪🇺🇬🇧 EU-UK negotiations on electricity market integration

EU member states have authorised the European Commission to open negotiations on reintegrating the United Kingdom into the EU’s electricity market, as part of a broader post-Brexit reset. The mandate also includes discussions on a UK financial contribution to EU cohesion funds as a condition for access to the single market. Market reintegration is expected to contribute to lower electricity prices, greater system stability and increased renewable investment, particularly in the North Sea region. However, negotiations may prove complex due to the political sensitivity of financial contributions on the UK side.

📉 Decline in EU energy imports with shifting supply structure

According to Eurostat data, the EU recorded a further decline in energy imports in 2025, both in value and volume, continuing a trend observed since 2022. Total import value reached €336.7 billion and volume 723.3 million tonnes, with a particularly notable decrease in petroleum products. At the same time, LNG imports increased significantly in both value and volume, while pipeline gas imports declined in volume terms. The supply structure remains concentrated, with the United States dominating LNG and petroleum product imports and Norway remaining the main supplier of pipeline gas, indicating continued dependence on a limited number of external partners despite the overall decline in imports.

🔋 Progress on the revision of the Critical Raw Materials Act (CRMA)

Work on the CRMA revision is advancing with the publication of a draft report prepared by rapporteur Mohammed Chahim (S&D). The proposed changes, part of the RESourceEU plan, focus on strengthening supply security for critical raw materials and reducing reliance on imports, particularly from China. The draft includes simplified procedures for strategic projects, higher recycling targets and the development of secondary raw materials markets, alongside expanded recyclability rules. It also strengthens the Commission’s role in monitoring supply chain risks and overseeing company actions. The initiative aims to improve investment conditions and regulatory predictability. A vote in the ITRE committee is planned for June, followed by a plenary vote in July.

🔌 Debate on the Grids package and infrastructure investment barriers

On 24 March, a debate on the European Grids package was held at the European Economic and Social Committee in Brussels, organised by ZPP. The discussion, with participation from MEP Andrea Wechsler and a representative of the European Commission, focused on barriers to investment, particularly permitting procedures and grid connections that continue to delay infrastructure development. Ryszard Pawlik, Head of the Brussels Office of PKEE and one of the panelists, highlighted the need to properly reflect the role and challenges of distribution system operators within the package.

3

2,003

We thank #youth representative, Gurgen Petrosyan for his contribution at yesterday's CCMI study group on accelerating #RESourceEU🇪🇺

🗣️ Your voices count!

#YouthInvolvement #EUYouth

Find out➡️link.europa.eu/BT3KmM

5

147

The RESourceEU study group held a conclusive meeting to prepare the upcoming CCMI opinion on the acceleration of the #criticalrawmaterials strategy at a vital time for EU industrial #preparedness and #competitiveness💎🪨

Thanks to rapporteurs @Diamantouros and @Agata_Meysner

2

5

127