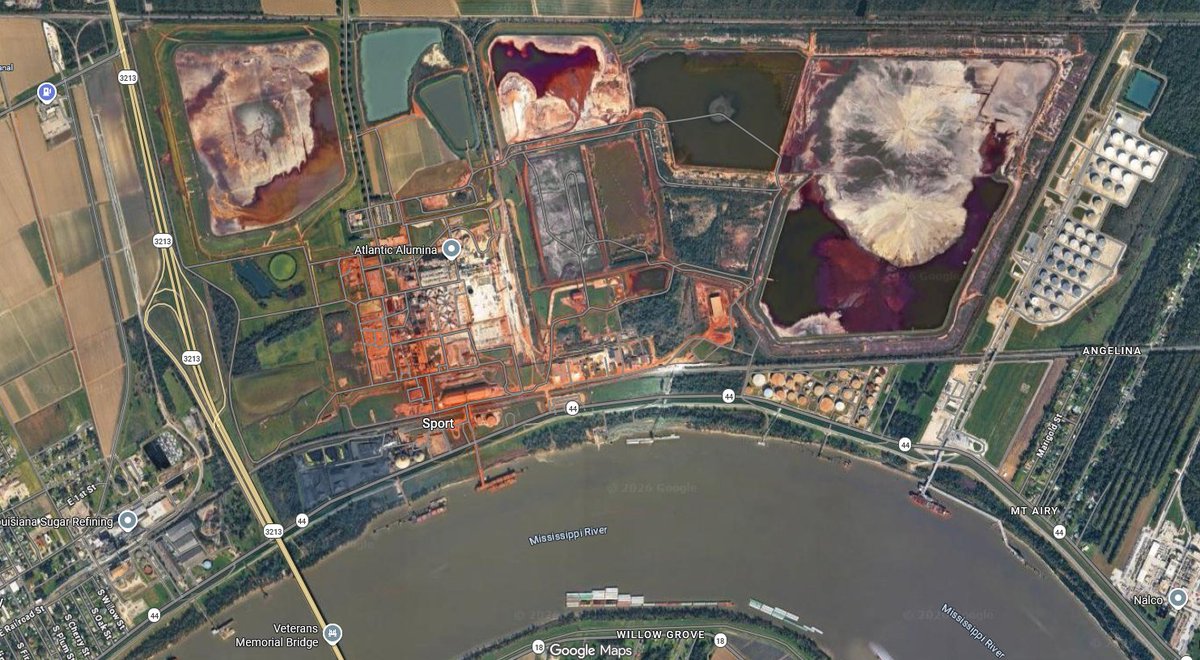

🇺🇸🏭 The US Department of Energy just awarded $67 million to turn a 30-million-tonne pile of industrial waste in Louisiana into a domestic rare earth and critical mineral supply chain.

The feedstock? Bauxite residue — "red mud" — from the last operating alumina refinery in the United States. And this one is unlike any other red mud deposit on earth. 🧵

🎬 Watch the ElementUSA video 👇

🎯 The Project — Straight to the Point

ElementUSA (formerly ElementUS Minerals LLC), in partnership with the Colorado School of Mines, has been awarded a $67 million DOE grant to design, construct, and operate a rare earth and critical mineral processing facility at St. John the Baptist Parish, Louisiana — targeting the legacy bauxite residue stockpiles at the Gramercy alumina refinery.

Total federal commitment across both agencies:

💰 $67M — U.S. Department of Energy (DOE), in partnership with Colorado School of Mines

💰 $29.9M — Department of Defense, Defense Production Act (DPA) Title III, specifically targeting gallium and scandium recovery for Pentagon supply chain needs

💰 $850M — Louisiana Economic Development investment decision to cement the facility in St. John Parish, projecting 200 direct and 550 indirect jobs

Also

⚗️📷 $66 million. U.S. Department of Energy. Phoenix Tailings. June 3, 2026. 🧲The @ENERGY

selected @PhoenixTailings for a $66 million grant — part of a $147.8 million program — to deploy next-generation rare earth separation and refining technology at commercial scale, partnered with MIT and the University of Minnesota.

Further Reading here👇

x.com/roblun1/status/2062571…

Back to ElementUSA Funding

This is not a single agency bet. Both the DOE and the DoD have independently assessed this project as strategically critical — through an energy security lens and a defense readiness lens simultaneously.

Groundbreaking for Phase 1 is expected to commence mid-2026.

🌋 Why This Feedstock Is Different

Red mud is one of the most abundant industrial waste streams on earth — global stockpiles exceed 4 billion tonnes. Most of it is essentially worthless for REE recovery, averaging 800 to 900 ppm total rare earth elements globally.

The Gramercy deposit is fundamentally different.

The Gramercy refinery has been processing Jamaican karstic bauxite since 1957. Jamaican karstic bauxites are globally unusual — they are naturally enriched in rare earth elements, yttrium, and scandium due to the lateritic weathering processes in tropical environments that formed them. When the Bayer process extracts alumina from this ore, the entire REE suite concentrates into the residue, roughly doubling its grade relative to the original ore.

The result: 30 million dry tonnes of surface-stockpiled material, expanding at approximately 1 million tonnes per year, characterised by:

🔬 Gramercy REE Basket — Key Elements:

⚗️ Total REE (TREE) — 3,000–4,000 ppm | ~4× global red mud average

🧲 Neodymium & Praseodymium (NdPr) — ~20× crustal average | Core NdFeB permanent magnet metals

🛡️ Dysprosium & Terbium (Dy/Tb) — ~20× crustal average | Critical HREE dopants for EV motors & defense

⚡ Yttrium (Y) — >20× crustal average | Major heavy rare earth phosphate fraction

🔩 Scandium (Sc) — 130–390 ppm | Exceeds global red mud avg of 45–150 ppm — highest value per kg in the basket

💡 Gallium (Ga) — Up to 200 ppm | Critical semiconductor input, severely limited in Western supply

🔋 Vanadium (V) — Up to 800 ppm | Grid-scale battery storage & high-strength steel alloying

🏗️ Iron matrix — ~50% of total mass | Extracted as commodity pig iron — funds the operation

More than 95% of the metals across the iron, rare earth, and critical mineral fractions are characterised as payable.

🧪 A Note on Grade — and Why the Basket Price Is the Real Number

3,000–4,000 ppm is objectively low grade compared to primary hard-rock REE deposits. Mountain Pass in California grades at approximately 89,932 ppm TREO (~9%), with NdPr concentrations exceeding 23,810 ppm (~2.4%).

But the Gramercy economics do not rest on absolute grade. They rest on three things:

1. The basket composition. Most conventional REE deposits are light-rare-earth dominated — rich in lanthanum and cerium, which have low commercial value and create persistent oversupply problems. The Gramercy basket is heavily weighted toward high-value heavy rare earths, yttrium, and scandium — the elements that matter most for magnets, defense systems, and aerospace.

2. Scandium as an economic multiplier. Scandium can represent up to 95% of the theoretical economic value of REEs in red mud. The 130–390 ppm Sc concentration at Gramercy means the site functions, from a unit economics perspective, as a high-grade scandium deposit that also produces a lucrative REE basket. Scandium prices have historically reached $3,000 per kilogram due to supply constraints from politically complex jurisdictions.

3. Zero mining cost. The material already exists as a surface-accessible, ultra-fine particulate slurry. There is no drilling, blasting, hauling, or primary comminution. The largest capital outlays of a conventional mine simply do not apply.

⚙️ The Flowsheet — Why Pyro First, Then Hydro

This is the engineering decision that makes the entire project viable.

Directly applying acid to raw red mud would be catastrophic. The Gramercy material is approximately 50% iron by mass. Direct leaching would consume enormous volumes of acid dissolving bulk iron rather than the target critical minerals, and create an iron-saturated pregnant leach solution from which extracting trace scandium, gallium, and HREEs would be chemically unmanageable.

ElementUSA's solution — developed with Enervoxa — is a two-phase integrated flowsheet:

Phase 1: Pyrometallurgical iron valorization 🔥

The dry bauxite residue is fed into a high-temperature smelting furnace using a continuous carbothermal reduction process. The ~50% iron fraction is chemically reduced and extracted as saleable commodity pig iron — converting the largest waste component into a continuous revenue stream that subsidises the baseline OPEX of the entire facility.

The residual slag, now thoroughly depleted of interfering iron, contains the concentrated aluminosilicates, calcium compounds, and the entire inventory of REEs, scandium, and gallium — at effectively double or triple their original concentration in the feed.

Phase 2: Hydrometallurgical separation ⚗️

The iron-depleted slag proceeds into aqueous leaching circuits. The flowsheet is engineered to first extract individual high-purity gallium and scandium streams — reflecting the DoD's specific strategic priorities — followed by precipitation of the remaining REEs as a mixed rare earth oxide (MREO) basket characterised by its heavy rare earth and yttrium weighting.

This MREO product targets downstream offtake in magnet, semiconductor, aerospace, and medical imaging applications.

🎓 The Academic Partnership: Colorado School of Mines

The $67M DOE award explicitly pairs ElementUSA with Colorado School of Mines — leveraging its renowned Waste-to-Value Center under the leadership of Dr. Elizabeth Holley.

This brings an interdisciplinary team covering technical validation, mineral characterisation, scale-up fluid dynamics, and flowsheet optimisation.

ElementUSA also operates the Critical Resource Accelerator — a 30,000-square-foot R&D hub in Cedar Park, Texas — staffed with hydrometallurgists and pyrometallurgists and equipped with full analytical laboratory and pilot-scale development capabilities ranging from 500mL to 20-litre bench reactors.

🌍 Zero-Waste Architecture

A core design objective of the ElementUSA flowsheet is zero solid waste closure.

By fractionating the red mud into pig iron, critical mineral products, REO basket, and a neutralised aluminosilicate residue, the facility is designed to eliminate the entire historical environmental liability of the Gramercy site.

The depleted aluminosilicate bulk — stripped of heavy metals and iron — is suitable for use as supplementary cementitious material, clinker substitute, or geopolymer concrete input.

The 3,300-acre Gramercy site currently accumulates 1 million additional tonnes of new residue per year. This facility is designed to process that incoming material while simultaneously treating the legacy stockpile — converting an ongoing environmental liability into a strategic supply chain asset.

🗺️ The Scale of the Commercial Ambition

Phase 2 targets a 1-million-tonne-per-year commercial throughput, backed by an estimated $1.1 billion capital expenditure — with construction commencement targeted as early as 2027.

The strategic objective: supply between 45% and 385% of current annual US demand for various critical elements from this single facility — positioning the US toward net-exporter status for specific defense-critical metals.

📋 What to Watch: The Scale-Up Journey

The Phase 1 demonstration groundbreaking is targeted for mid-2026 — and the Phase 2 commercial facility at 1 million tonnes per year has a construction commencement target of 2027.

That is an ambitious timeline by any measure in extractive metallurgy, and the engineering community knows it. Here is what the milestones actually mean and what to watch for:

⏱️ The timeline reality

Transitioning a complex pyro-hydrometallurgical flowsheet from bench-scale validation to mega-scale commercial operations has historically taken 5 to 10 years of iterative optimisation. Phase 1 groundbreaking in mid-2026 and Phase 2 construction starting in 2027 means both phases are effectively running in parallel'

Silica management at scale — Bauxite residue contains reactive silica that can polymerise in acid leach circuits, forming viscous gels that clog filtration and solvent extraction units.

HREE separation circuit performance — Separating dysprosium, terbium, and yttrium from a low-ppm pregnant leach solution at industrial throughput requires hundreds of sequential solvent extraction stages running with very precise fluid dynamics. The low tenor of HREEs in solution means large liquid volumes must be processed to yield commercial quantities — putting reagent management and phase separation under sustained pressure.

✅ What gives confidence

The dual federal mandate (DOE DoD), the Colorado School of Mines academic partnership, the 30,000 sq ft Critical Resource Accelerator R&D hub in Cedar Park Texas, and the $850M Louisiana Economic Development commitment all provide an unusually robust infrastructure for absorbing the engineering learning curve.

🔗 Connecting the Dots: The DOE's Emerging Secondary Feedstock Strategy

Regular readers will recall the recent post on Phoenix Tailings receiving a $66M DOE grant to build a demonstration facility in Oklahoma for high-purity rare earth metal production from industrial waste, partnering with MIT and the University of Minnesota.

ElementUSA now joins Phoenix Tailings in a clear DOE thesis: secondary feedstocks — industrial waste, tailings, legacy residues — are not a niche. They are a central pillar of the US domestic critical mineral supply chain strategy.

The reasons are straightforward:

✅ No greenfield mine permitting required

✅ Material is already liberated and surface-accessible

✅ Environmental remediation and critical mineral production become the same project

✅ Federal capital absorbs the technology development risk that private markets won't fund yet

🔗discoveryalert.com.au/rare-e…

📎 Sources:

🔗 DOE Award Announcement — Colorado School of Mines & ElementUSA $67M

minesnewsroom.com/news/color…

🔗 DoD Defense Production Act Title III Award — $29.9M Gallium & Scandium

war.gov/News/Releases/Releas…

🔗 Louisiana Economic Development — $850M Investment Decision

opportunitylouisiana.gov/new…

🔗 ElementUSA — Official Company Website

elementusaminerals.com

#ElementUSA #ColoradoSchoolOfMines #DOE #DepartmentOfEnergy #DefenseProductionAct #DPA #CriticalMinerals #RareEarths #REE #BauxiteResidue #RedMud #Gramercy #Louisiana #Scandium #Gallium #Vanadium #Dysprosium #Terbium #Neodymium #Praseodymium #Yttrium #NdFeB #PermanentMagnets #HeavyRareEarths #HREO #MREO #Hydrometallurgy #Pyrometallurgy #SolventExtraction 🇺🇸🏭⚗️🔥⚡🧪🌍🎓💰🔗♻️

⚗️🇺🇸🧲 $66 million. U.S. Department of Energy. Phoenix Tailings. June 3, 2026.

Washington just wrote one of its largest ever grants for rare earth separation to a company running technology that outcompetes China's legacy systems on every metric that matters. 🧵

What just happened

The @ENERGY selected @PhoenixTailings for a $66 million grant — part of a $147.8 million program — to deploy next-generation rare earth separation and refining technology at commercial scale, partnered with MIT and the University of Minnesota.

This is not a feasibility study. It is a commercial deployment grant for a company that already operates rare earth metallisation at commercial scale and is now scaling separation to match.

"The United States will win at rare earth processing with American innovation that outcompetes the hazardous legacy systems used overseas."

— Nicholas Myers, CEO, Phoenix Tailings

Why Phoenix Tailings is different ⚙️

Phoenix Tailings does not replicate Chinese solvent extraction. Their proprietary mixed halide electrochemical bath runs at roughly 700°C — versus the 1,050°C required by conventional MSE — cutting energy consumption by 35–45%, eliminating perfluorocarbon emissions (PFCs), and producing zero toxic chemical waste byproducts.

They process a diverse range of domestic feedstocks: monazite, bastnäsite, ionic clay concentrates, tailings — exactly the kind of mixed, variable feed that trips up conventional hydromet processes. That flexibility is what makes the DoE bet so strategic.

Their three core technology pillars backing this program:

🔬 Advanced chemistry — low-temperature, low-emissions separation chemistry

🏭 Industrial hardware — proprietary electrochemical reactors, not mixer-settlers

💻 Digital infrastructure — AI process control and real-time optimisation

x.com/roblun1/status/2056749…

globenewswire.com/news-relea…

@PhoenixTailings

#PhoenixTailings #DepartmentofEnergy #DoE #RareEarths #CriticalMinerals #REO #NdPr #Dysprosium #Terbium #MoltenSaltElectrolysis #Separation #Metallisation #AdvancedMagnetLab #NdFeB #DLA @wsenti @IONIC_RE @MomentumTP

1

1

16

1,894

🇪🇺⚗️ Philippe Kehren, CEO of Solvay, just gave one of the clearest and most honest assessments of Europe's industrial position I've heard from a major CEO.

Worth your time. Every quote below is verbatim. 🧵

🎬 Watch the full interview 👇

🏭 On Solvay and supply chain resilience:

"We have more than 80% of our sales done regionally. It's very important to be close to the market, close to your customers."

"I think now it's over — we have to get back to shorter logistic chains and to get back to raw materials and energies that are available locally."

"When you are a leader in your market, you master your technologies, you master your processes and you can adjust very quickly. If overnight you cannot buy anymore a certain type of raw material from a certain location, you're able to change very quickly."

🌍 On whether Europe can compete:

"Yes — Europe has everything to be competitive and sustainable in the future. It has the best engineers, technicians, operators, assets. One of the most efficient chemical production units in the world are based in Europe."

And then the line that should make every European policymaker pause:

"A lot of the pain we suffer today has been self-inflicted."

🧲 On rare earths — and this is the part the critical minerals community needs to hear:

"Rare earth is a good example. We've outsourced completely the production of rare earth material for permanent magnets. Between 90 and 100% of those materials today come from China."

"The plant in La Rochelle is in fact unique outside of China. It's the only plant outside of China that is able to produce any type of rare earth material from any type of source. We've been doing that for more than 75 years — this plant started up in 1948."

"We know how to produce those materials. We can do it very quickly. But we need to have the value chain. We need to have buyers. We need to have contracts with volumes and prices. This is today what is missing in order to invest further."

That last sentence is the most important line in the entire interview.

Europe has the only plant outside Asia capable of processing every major rare earth element at industrial scale. It has been operating for 78 years. It inaugurated a new magnet-grade production line in April 2025.

And it still cannot get enough long-term offtake contracts from European OEMs and magnet manufacturers to justify the next investment round.

⚡ On energy — the other half of the industrial sovereignty equation:

"We need to have competitive energy in the long run by developing nuclear, by developing renewable energy, ways to store renewable energy, hydro... We decided not to produce gas in Europe — that's a fair choice. But you cannot say I don't develop nuclear neither. You need something."

"We see today that the countries that have decided to have nuclear production are more competitive and more sustainable."

For energy-intensive processes like rare earth solvent extraction — large heated mixer-settler circuits running 24/7 — this isn't abstract policy. It is the difference between a viable OPEX profile and a structural cost disadvantage versus Chinese producers who operate on subsidised industrial power.

🔧 On the CO2 transition and industrial competitiveness:

"If you pay at the same time those projects that are very expensive plus the CO2 quotas because you have a large deficit, you pay the energy transition twice."

"We need to support the industrials that are doing this by giving them the right level of incentives and CO2 quota so that they can indeed pay this transition and solve at the same time their competitiveness challenge."

"It's perfectly compatible to do the energy transition and at the same time be competitive and secure an industrial production in Europe."

💷 On floor prices for strategic materials — a specific, concrete policy proposal:

"One way to unlock this situation would be to set floor prices — to say we guarantee you a certain minimum level of price so that you can secure the return on your investment — and that in that way it would not penalise the customers neither. It's a nice way to diversify and de-risk something that can be strategic."

This is Solvay's direct ask to European policymakers. Not grants. Not subsidies. Price floors for strategic materials — the same mechanism used in the UK for offshore wind contracts (CfD), now proposed for rare earth oxides and critical chemical intermediates.

🔑 On what "economic security" actually means:

"Economic security is really about looking at the value chains. In the past we had this idea that you look at the final product and then you can produce all the rest of the pieces anywhere else. I think that's not completely true."

"It doesn't mean we will produce 100% locally of course, but we need to at least master all the elements of the value chain and master the processes of the different pieces. That's very important so that you can create optionalities and be in control."

"Be in control is really what is very important in the current circumstances."

🌍 The bigger picture Kehren is describing

Europe's industrial model is at an inflection point. High energy costs, dependence on Chinese critical materials, and competition from both Chinese state-backed industry and US subsidy-backed manufacturing (IRA, CHIPS Act) are simultaneously compressing the space for European companies to operate competitively.

Kehren's argument — and Solvay's position illustrates it precisely — is that the response cannot be either purely market-led or purely policy-driven. It requires:

✅ Policy frameworks that make long-term investment decisions credible (stable energy prices, joint procurement, offtake support)

✅ Industry commitment to building the full value chain — not just individual nodes

✅ OEM and downstream manufacturers actually signing the long-term supply agreements that anchor project finance

✅ Financial institutions moving at the speed the geopolitical situation demands

📍 The September 2026 milestone running in parallel:

While Kehren makes the case for policy support, Solvay is already moving. Industrial-scale Dy and Tb separation at La Rochelle is targeted for September 2026 — dysprosium and terbium, the two heavy rare earths under active Chinese export controls, at the only facility outside Asia capable of separating them at industrial throughput.

The policy argument and the commercial delivery are happening simultaneously. The question is whether European OEMs, magnet manufacturers, and policymakers move fast enough to match it.

@SolvayGroup

#Solvay #PhilippeKehren #LaRochelle #RareEarths #REE #CriticalMinerals #EuropeanSovereignty #IndustrialSovereignty #CriticalRawMaterials #CRMA #RESourceEU #EuropeanCompetitiveness #EnergyPrices #Nuclear #EnergyTransition #CleanIndustrialDeal #NdFeB #PermanentMagnets #Neodymium #Praseodymium #Dysprosium #Terbium #MagnetGrade #REOSeparation #SolventExtraction #HeavyRareEarths #HREO #LREO #FloorPrices #StrategicAutonomy #CarbonNeutral #CO2 #ETS #EuropeanIndustry 🇪🇺🇫🇷🇧🇪⚗️🧲🔬💡🏭⚡🌍🔑🎬

2

8

471

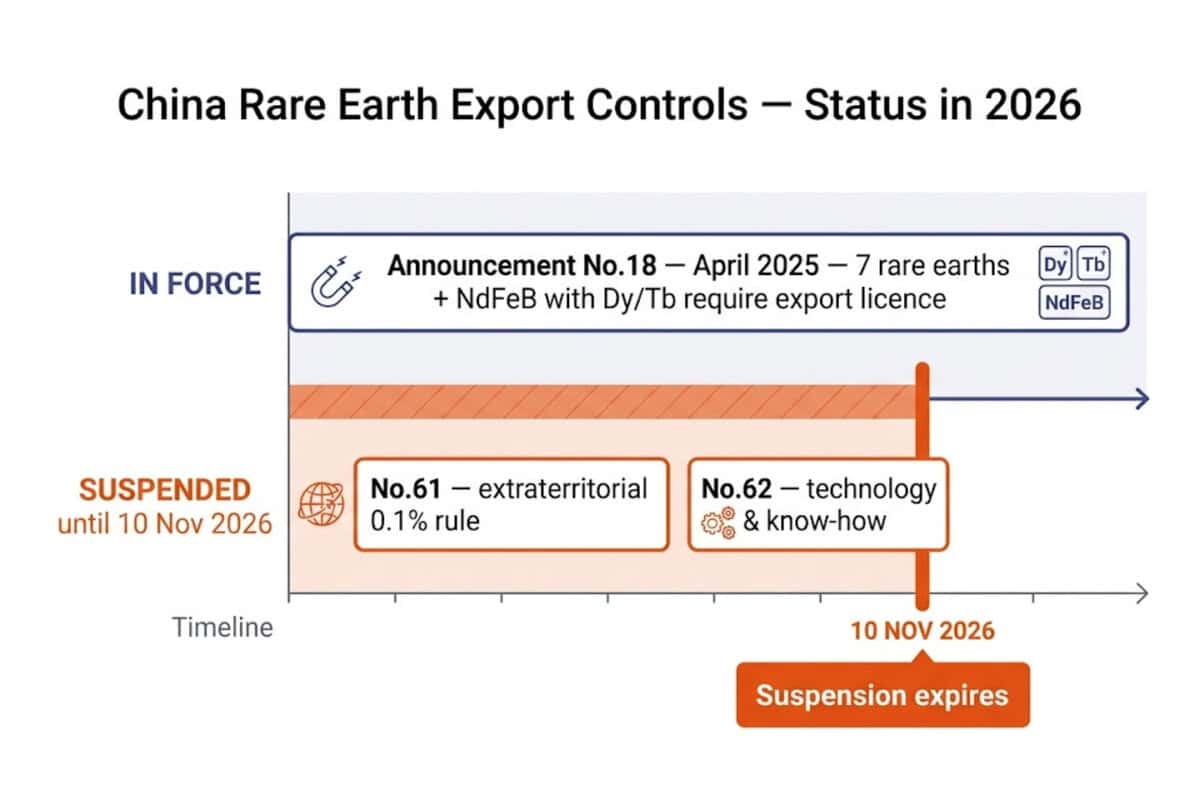

⚗️🇨🇳 China's rare earth strategy just went deeper than ore and magnets. It extended all the way into the chemistry cupboard.

And most people building Western REE separation plants haven't fully priced in what that means. 🧵

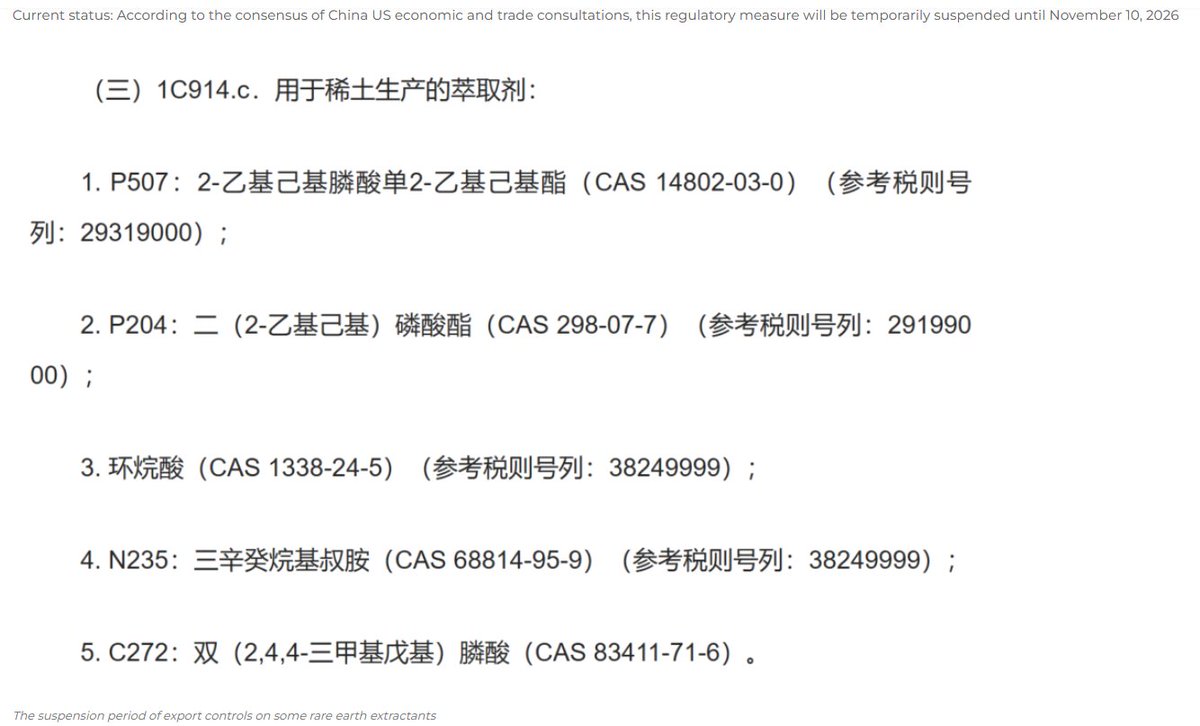

In November 2025, China's Ministry of Commerce formally implemented export controls on five key solvent extraction reagents — the organic chemicals that sit at the heart of virtually every rare earth separation plant on earth.

🧪 The Three Core Extractants — and What Each Does

The Chinese rare earth industry standardised around three primary organophosphorus extractants, each targeting a different part of the separation sequence:

⚗️P204 (D2EHPA / HDEHP)

Bis(2-ethylhexyl) phosphoric acid

Acidic extractant — strong affinity for heavier lanthanides and yttrium

Used for first-stage impurity removal and heavy REE separation (Sm, Eu, Gd, Y)

Also the benchmark extractant for removing iron and other impurities before the main REE circuit

⚗️P507 (EHEHPA)

2-Ethylhexyl phosphonic acid mono-2-ethylhexyl ester

Acidic extractant with higher separation coefficients than P204

Now the mainstream reagent for light rare earth separation — La, Ce, Pr, Nd

Preferred over P204 for NdPr separation because of better selectivity and lower saponification requirements

Critical for producing the magnet-grade NdPr oxide that LCM, Solvay, Carester, and every other Western metallization house needs

⚗️N235 (N1923)

Tri(octyl-decyl) tertiary amine

Alkaline/neutral extractant — operates in chloride systems

Used for light REE separation and associated element extraction in hydrochloric acid leach circuits

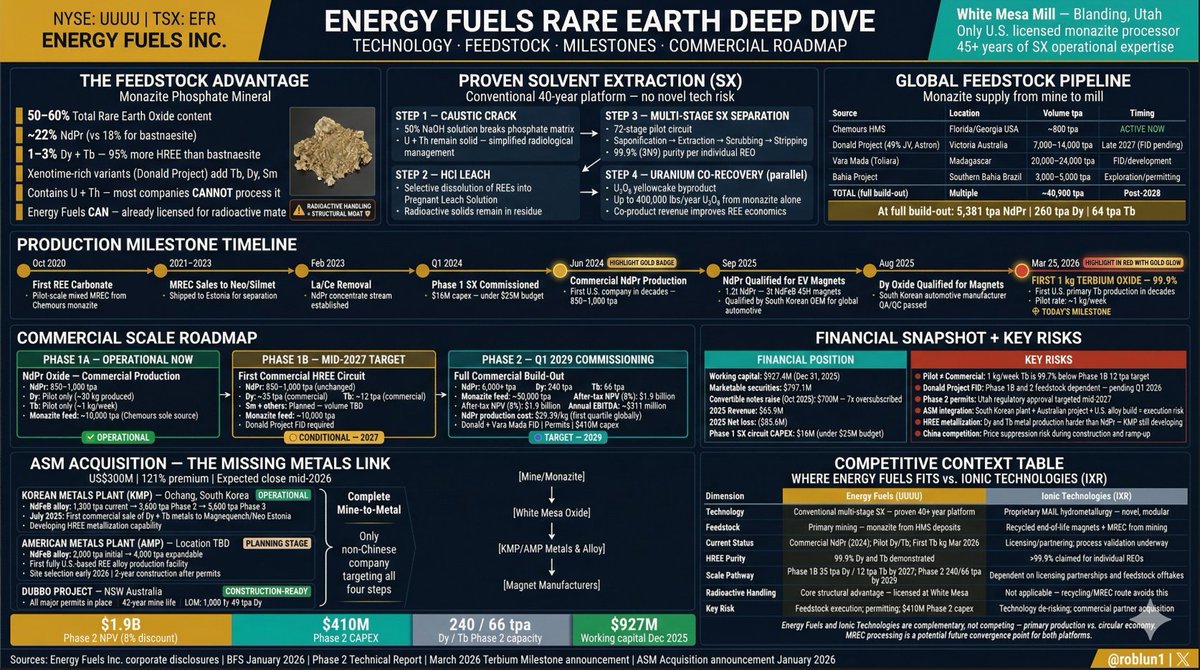

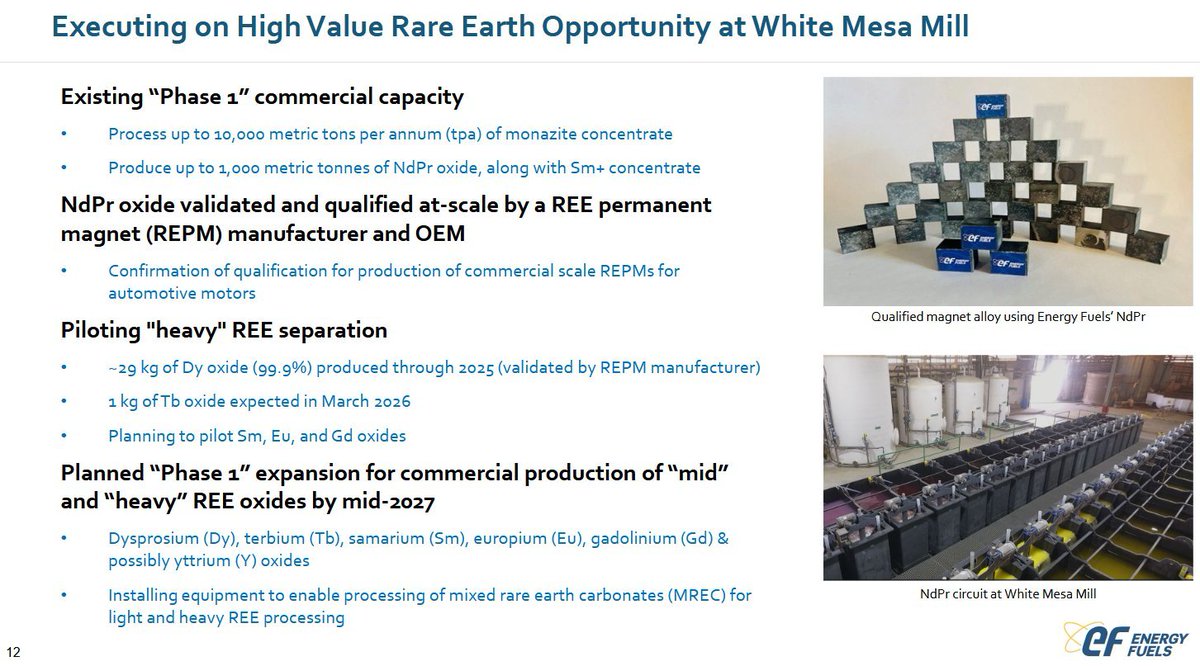

Together, these three chemicals underpin virtually every industrial REE separation plant operating outside China today — including Solvay's La Rochelle facility, Energy Fuels' White Mesa circuits, and the planned Carester/Caremag plant at Lacq, France.

These are not obscure laboratory reagents. P507 and P204 are the workhorse extractants of the global REE solvent extraction industry. They are used in virtually every commercial REE separation circuit operating today — including facilities in France, Estonia, the United States, and Japan.

⏸️ The current status: suspended — but not cancelled

Following the US-China economic and trade consultations, the controls have been temporarily suspended until November 10, 2026.

That is approximately five months from now.

The controls have not been lifted. They have been paused. They remain on the books under China's Export Control Law and the Regulations on Export Control of Dual Use Items — and they can be reactivated at any time, for any destination, based on end use, customer, or geopolitical circumstances.

For any Western REE separation project currently in development, that five-month window and the uncertainty beyond it are not background noise. They are a project risk that belongs on the critical path. ⚠️

🏭 Why this matters for Western separation plants

To understand the exposure, consider what a solvent extraction circuit actually needs:

A single commercial-scale REE separation plant — capable of processing thousands of tonnes of mixed rare earth concentrate per year — requires hundreds of tonnes of organic extractant just for the initial circuit fill before a single kilogram of separated REO is produced.

After that, ongoing solvent makeup is required continuously, because extractants degrade over time through radiolytic breakdown, chemical oxidation, and entrainment losses. The circuit never stops consuming them.

If export of P507, P204, and C272 from China requires a licence — and that licence is denied, delayed, or made conditional — a fully constructed, fully feedstocked REE separation plant simply cannot operate.

The concrete is poured. The mixer-settlers are installed. The leach circuits are running. And the plant sits idle because it cannot get its solvent inventory across the border. That is the specific vulnerability these controls create.

🌍 The broader strategic read

This is the most important point, and it goes beyond rare earths specifically.

⚗️C272 (Cyanex 272) is the benchmark extractant for cobalt/nickel separation by solvent extraction — used in battery recycling and lithium-ion battery precursor manufacturing globally. Its inclusion in these controls means the reach extends well beyond rare earth refining into the entire battery metals processing ecosystem.

What China has done is demonstrate that its leverage in the critical minerals value chain does not stop at:

❌ Controlling the ore deposits

❌ Controlling the separation and refining capacity

❌ Controlling the metal and alloy manufacturing

It now extends to controlling the process chemicals required to operate separation plants that Western countries are spending billions to build.

A rare earth project that has secured its mining licence, its offtake agreements, its government funding, and its construction contracts — but sources its extractants from China — carries a vulnerability that sits entirely outside its own control.

🔬 What the response looks like

There are credible paths forward, but none of them are instant:

1. Western extractant production

P507, P204, and C272 can be synthesised outside China. The chemistry is not secret — it is decades old. But commercial-scale Western production of these specific organophosphorus compounds has atrophied as Chinese supply became dominant on price. Restarting or scaling that production takes capital, time, and permitting.

2. Alternative extractant chemistries

This is where the technology landscape becomes directly relevant. Several next-generation separation approaches are specifically designed to eliminate dependence on Chinese organophosphorus extractants entirely:

A. 🫧Ionic liquid-based SX (e.g., MAIL-type systems) uses engineered amide ionic liquids instead of conventional organic diluents and phosphoric acid extractants — produced in Western laboratories

B. ⏳Continuous ion exchange / chromatography operates in entirely aqueous media with resin-based columns — no organic solvent phase at all

C. 📱Membrane-assisted SX uses immobilised extractant phases that dramatically reduce solvent inventory requirements

These are not just greener alternatives. In the current regulatory environment, extractant sovereignty is supply chain sovereignty.

3. Strategic inventory building

During the current suspension window, any Western operator relying on Chinese P507, P204, or C272 should be assessing whether they need to build forward inventory before November 2026 — and what their contingency is if the suspension is not extended.

⏰ The clock is running

The suspension expires November 10, 2026. That is not a distant horizon. For projects in active construction or commissioning, it is within the current project timeline.

The controls were implemented once. They were suspended under diplomatic pressure. The underlying regulatory framework — China's Export Control Law, dual-use classification, licence requirements — remains entirely intact.

⏰ November 10, 2026

The export control suspension expires in approximately five months.

Every Western REE separation project currently operating or commissioning on P507 or P204 should have a clear answer to three questions:

Last Slide, shows DOAM-PPA —

⚗️🫧((dioctylamino)methyl)phenylphosphonic acid — a novel rare earth extractant synthesised by a research team at the Fujian Institute of Research on the Structure of Matter, Chinese Academy of Sciences.

It is in the same organophosphorus extractant family as P204, P507, and Cyanex 272 — the three Chinese-controlled extractants — but it is a next-generation molecule specifically engineered to outperform them, particularly for heavy rare earth (HREE) separation.

If the next generation of high-performance HREE extractants is also being developed inside Chinese state research institutes, what does Western extractant sovereignty actually look like long-term — and is ionic-liquid or aqueous-based separation chemistry the only credible path to genuine independence from Chinese process chemicals?

📦 What is your current extractant inventory and how long does it run your circuit?

🌍 Do you have a non-Chinese supply source qualified and contracted?

🔬 What is your longer-term chemistry strategy — and does it reduce or eliminate Chinese extractant dependency?

These are not theoretical questions. They are operational ones. ⚗️

🔗 metalleaching.com/rare-earth…

🔗 metalleaching.com/export-con…

#RareEarths #REE #CriticalMinerals #SolventExtraction #SX #P507 #P204 #D2EHPA #HDEHP #EHEHPA #N235 #C272 #Cyanex272 #REEExtractants #OrganophosphorusChemistry #LanthanideSeparation #CascadeExtraction #XuGuangxian #MixerSettlers #REESeparation #Hydrometallurgy #NdPr #Neodymium #Praseodymium #Dysprosium #Terbium #Yttrium #Samarium #MagnetGrade #REOPurity #ExportControls 🇨🇳⚗️🔬🧪⚠️🌍🏭⏰🔒🌱

1

2

13

619

🇺🇸⚗️ The U.S. Department of Energy has committed up to $19.3 million to advance a pilot-scale continuous ion exchange rare earth separation facility in Stillwater, Oklahoma.

It is a relatively modest number in the context of the billions flowing into the broader rare earth supply chain — but the technology it is funding sits at one of the most genuinely interesting and unresolved junctions in critical minerals processing today.

The award comes under DOE's Critical Material Innovation, Efficiency and Alternatives program (FOA 3105). Total project value is approximately US$50.5 million, with US$31.2 million in private co-funding alongside the federal contribution.

The specific target: build, demonstrate, and operate a pilot-scale continuous ion exchange (CIX) rare earth element production plant — a processing approach that offers some compelling theoretical advantages over conventional separation methods, but which has not yet been demonstrated at full commercial scale in the Western world.

That gap between pilot performance and commercial reality is worth understanding. 🧵

🔬 A brief note on why rare earth separation is so difficult

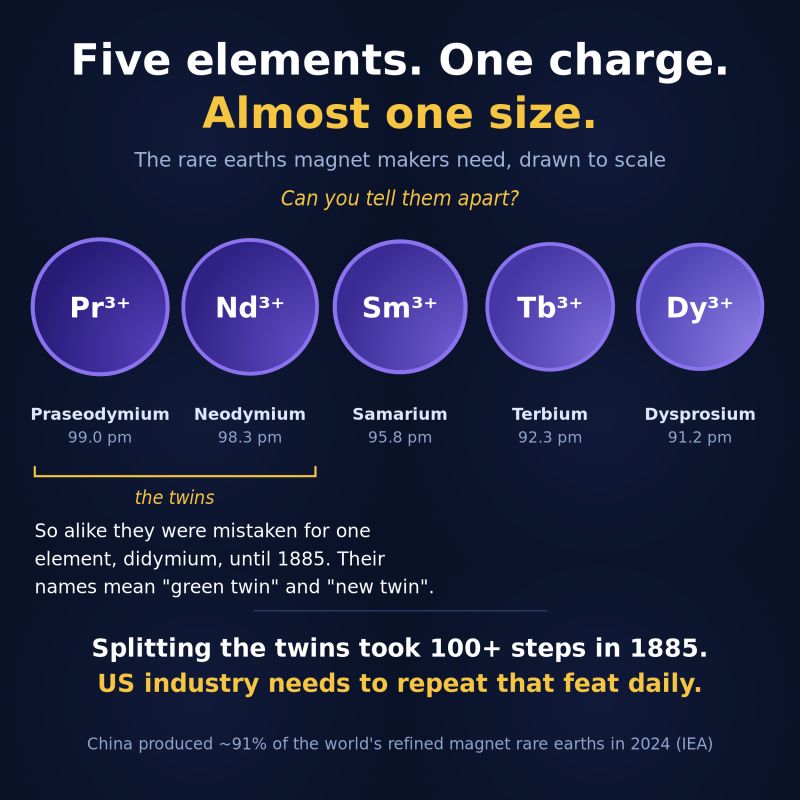

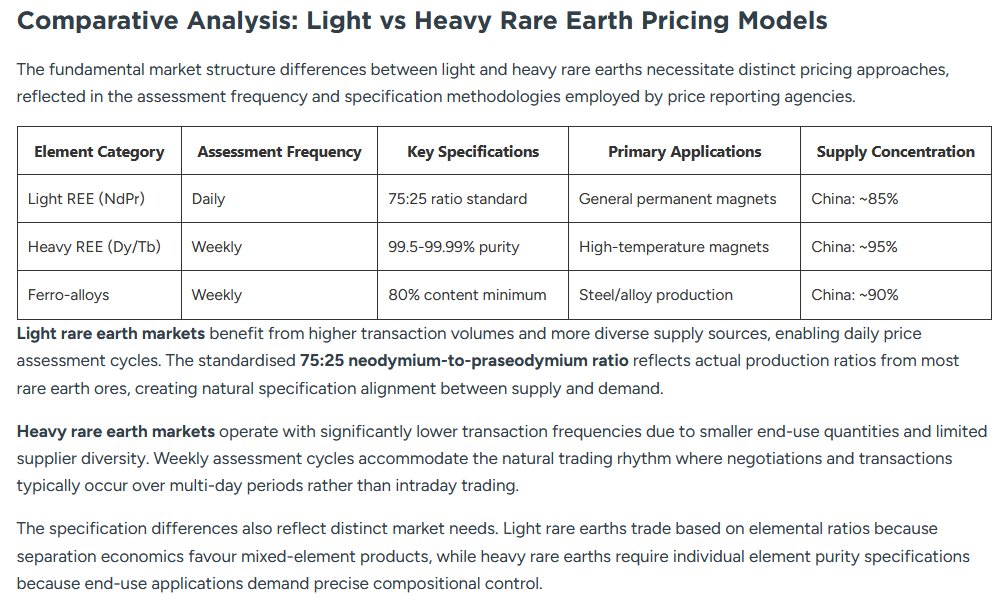

Once rare earth ore is leached, the resulting solution contains all 15 lanthanide elements dissolved together. Separating them into the individual high-purity oxides — neodymium, praseodymium, dysprosium, terbium — needed for magnet manufacturing is one of the more demanding challenges in extractive metallurgy.

The reason is straightforward: rare earth elements are almost chemically identical to each other. They carry the same 3 charge in solution.

Their ionic radii differ by fractions of a nanometre. The separation factors between adjacent lanthanides can be as low as 1.5 to 2.5 — meaning a single pass through any separation medium achieves almost no meaningful purification.

Industrial processes require hundreds or thousands of successive stages to reach the 99.5–99.999% purity levels that magnet and defense manufacturers require.

This is the fundamental challenge that every separation technology — conventional or novel — has to solve.

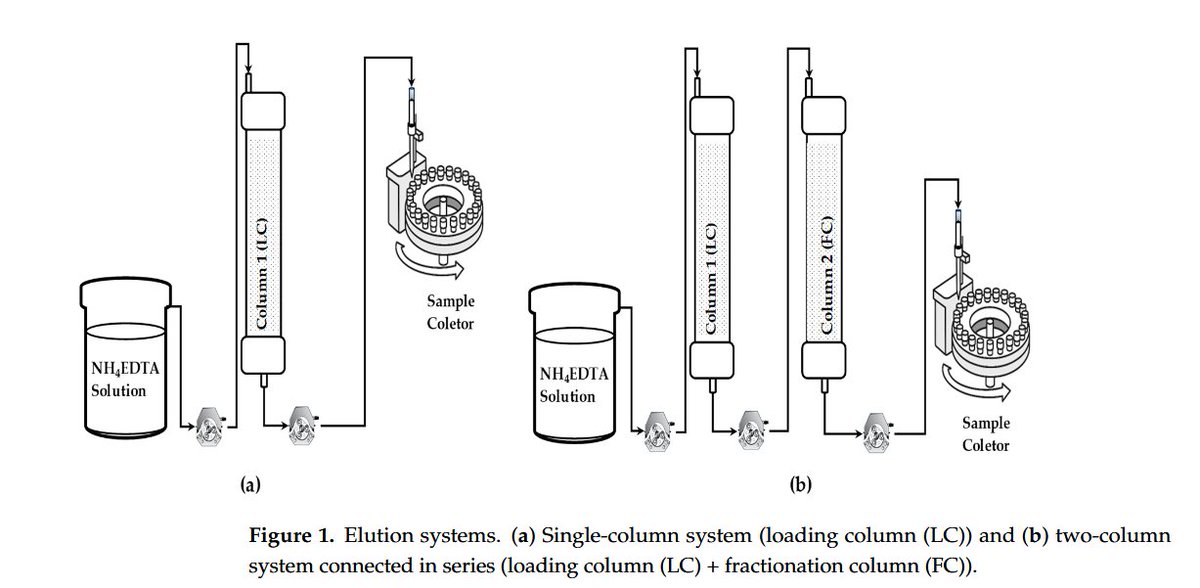

⚗️ What continuous ion exchange offers (Infographic)👇

Conventional solvent extraction (SX) — the current industrial standard globally — solves this problem using two immiscible liquid phases and large cascades of mixer-settler tanks.

It works reliably at scale, but it requires significant capital, a large physical footprint, long equilibrium times, and continuous circulation of organic solvents.

Continuous ion exchange takes a different approach:

The dissolved rare earth solution is pumped through solid resin-packed columns rather than liquid organic phases

Rare earth ions bind to functional groups on the resin and travel through at slightly different velocities, naturally segregating into distinct elution bands

The process operates in entirely aqueous chemistry — no flammable organic solvents, reduced environmental permitting complexity

A compact column array can theoretically replace much larger mixer-settler infrastructure

Pilot operations have demonstrated outputs reaching 99.99% to 99.999% purity

These are genuinely attractive characteristics, and they explain why both government agencies and private developers are investing in understanding the technology more deeply.

⚙️ The honest engineering picture at scale

Where it gets more complex is in the transition from pilot to industrial throughput — and this is where the rare earth chemistry itself creates challenges that are worth being clear-eyed about.

Those very small separation factors that make lanthanides hard to separate in the first place don't disappear at scale. As columns grow from laboratory diameter to the one-to-two-metre diameter needed for commercial throughput, maintaining uniform fluid flow becomes substantially more demanding. Poor flow distribution leads to channeling, dead zones, and degraded separation performance.

Resins also behave differently to liquid organic solvents over time. Solid resin beads can experience mechanical attrition, osmotic shock, and gradual degradation from exposure to strong acids. Trace impurities in real-world feedstocks — iron, aluminium, calcium, uranium, thorium — can progressively foul the resin's active sites, reducing capacity and requiring sophisticated pre-treatment upstream.

And while CIX eliminates organic solvents, it still requires significant volumes of aqueous eluents, careful gradient management, and energy-intensive recovery circuits to convert the separated REE solutions into solid, saleable oxides.

These are not reasons to dismiss the technology. They are the specific engineering questions that pilot programs like the Stillwater facility are designed to answer — at a scale where the answers become meaningful for commercial plant design.

🧪 Why rare earths are uniquely hard to separate

Every rare earth element in solution carries an identical 3 charge. The electrons that make one lanthanide subtly different from the next are buried deep inside the atom, shielded from the outside world, and contribute almost nothing to how each element behaves chemically. (See Image)👇

The only handle you have is the lanthanide contraction — a tiny, progressive decrease in atomic size across the series. The size difference between adjacent rare earths is measured in fractions of a nanometre. That is it. Fifteen elements, essentially the same charge, essentially the same chemistry.

Compare that to separating transition metals like iron, cobalt, or copper. These elements switch between multiple oxidation states easily — 2, 3, even 4 — and form complexes with very different electrical charges depending on the chemistry around them.

Ion exchange resins separate by electrostatic difference: grab one charge, let the other wash through. Separation factors for transition metals can reach 40 to over 300.

For adjacent rare earths? 1.5 to 2.5.

This isn't a flaw in any particular technology. It is the physics of the lanthanide series. Every separation platform — SX, CIX, chromatography, ionic liquids — is working with the same vanishingly small chemical difference. The technologies vary in how efficiently they exploit it, and how reliably they maintain that performance at scale. 🔬

🏭 The dual-track approach

What is particularly instructive about this specific program is how it sits alongside a parallel conventional solvent extraction demonstration facility in Wheat Ridge, Colorado — five discrete SX circuits running continuously for 2,000–4,000 hours, generating the operational data required for a Definitive Feasibility Study on the Round Top, Texas deposit, with commercial production targeted for late 2028.

The two facilities serve different purposes. The Colorado SX facility generates the proven, bankable engineering data that project financiers and lenders require. The Oklahoma CIX pilot advances understanding of a next-generation separation approach, supported by government capital that absorbs the R&D overhead that private markets aren't yet positioned to fund.

Running both simultaneously is a pragmatic and well-considered way to advance the technology frontier without staking commercial timelines entirely on unproven processes.

🔭 Watch this space

🔭 Coming up

The rare earth separation landscape is genuinely diverse — and genuinely fascinating.

From conventional solvent extraction to continuous ion exchange, continuous chromatography, ionic-liquid systems, and a range of emerging alternatives, each technology brings its own chemistry, its own engineering profile, and its own set of trade-offs between purity, scale, cost, and environmental footprint.

Over the coming weeks I'll be taking a closer look at each of these separation technologies individually — what the underlying science actually is, how it behaves at scale, where it fits best in a commercial flowsheet, and what the honest engineering challenges are. ⚗️🔬

🔗 mining.com/usa-rare-earth-wi…

#USARareEarth #USAR #NASDAQ #DOE #DepartmentOfEnergy #FOA3105 #CriticalMinerals #RareEarths #REE #ContinuousIonExchange #CIX #CIC #SolventExtraction #REESeparation #RareEarthSeparation #Hydrometallurgy #NdFeB #PermanentMagnets #Neodymium #Dysprosium #Terbium #MagnetGrade #Stillwater #Oklahoma #RoundTop #WheatRidge #Colorado #MineToMagnet #CriticalMineralsStrategy 🇺🇸⚗️🔬🧪⚙️🧠💡🏭🌍

6

21

716

Jun 9

Every quality oil starts with a well-controlled extraction process. From seed preparation to final oil and meal streams, each stage plays an important role in improving oil recovery, process efficiency, and product quality.

With GOYUM Canola Oil Extraction Plants, the complete process is designed for reliable performance — from cleaning and conditioning of canola seeds to pressing, solvent extraction, desolventizing, and final handling.

We build complete canola oil extraction solutions designed for smooth operation, efficient recovery, and long-term industrial performance.

Check out the step-by-step breakdown in our slides to see how it works! 👇

Share your requirements — including your complete address, WhatsApp number, and email — and our team will provide a customized Techno-Commercial Quotation.

GOYUM SCREW PRESS

Websites: oilexpeller.com| goyumindia.com

Email: sales@oilmillmachinery.com

WhatsApp / Telegram : 919501765000

#CanolaOilExtraction #CanolaOilExtractionPlant #CanolaOilProcessing #CanolaProcessingPlant #OilExtractionProcess #SeedPreparation #SeedCleaning #Flaking #Cooking #Extrusion #OilPressing #OilExpeller #SolventExtraction #SolventExtractionPlant #OilDesolventizing #MealDesolventizing #CanolaMeal #EdibleOilIndustry #OilMillMachinery #OilProcessingPlant #TurnkeyProjects #IndustrialPlant #ProcessEngineering #MadeInIndia #ExportFromIndia #Goyum #GoyumIndia

18

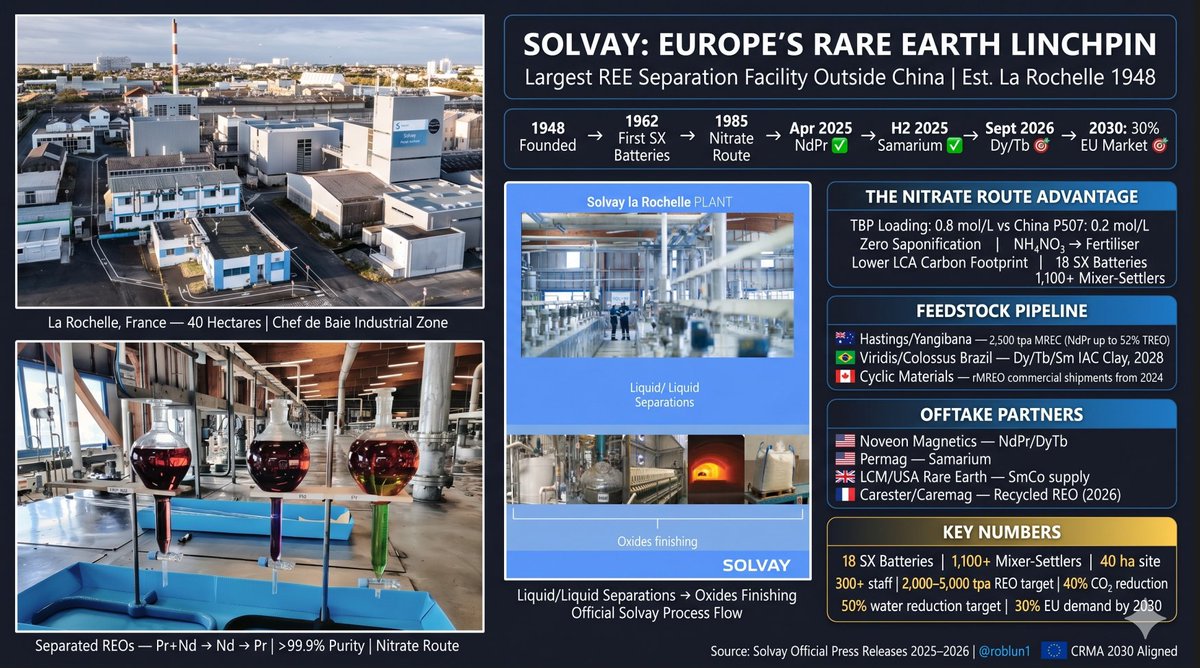

🧪🇫🇷⚗️ One plant. 75 years of chemistry. Europe's entire rare earth future.

The global race for permanent magnets is heating up, and Europe is aggressively securing its supply chain. At the very center of this shift is Solvay’s historic La Rochelle facility in France, the largest rare earth separation plant outside of China! 🇫🇷⚡

If you don't know Solvay's La Rochelle facility, you don't understand the Western rare earth supply chain. Thread. 🧵

📌 Infographic —

The numbers that define Europe's only serious REE refinery 📊

18 distinct solvent extraction batteries

1,100 individual mixer-settlers, running 24/7

40 hectares on the French Atlantic coast

300 specialist staff — 4,000 hours of training per year

One of 3 sites globally capable of processing ALL rare earths at industrial scale

This is not a pilot plant. This is not a demonstration facility. La Rochelle has been operating continuous liquid-liquid solvent extraction since 1962. When new Western players talk about building a "separation facility," this is what they're trying to replicate. It took Solvay 60 years to get here.

Why Solvay's chemistry is fundamentally different from China's 🔬

🧪 The Science of Separation.

While the Chinese industry relies heavily on the "Chloride Route" which consumes massive amounts of acid and alkaline neutralizers, Solvay champions the advanced "Nitrate Route".

Using highly efficient solvating extractants like TBP, Solvay's process drastically lowers operational costs, eliminates the need for constant chemical neutralization, and incredibly, turns its ammonium nitrate byproducts into commercial agricultural fertilizer! 🌱♻️

China separates REEs using the chloride route — hydrochloric acid P507 extractant. The problem: P507 releases protons that acidify the solution, so you have to continuously dump in NaOH or ammonia to neutralise it — generating massive toxic ammonium-nitrogen wastewater that has devastated communities around Chinese rare earth hubs.

Solvay uses the nitrate route — nitric acid Tributyl Phosphate (TBP):

✅ Zero saponification — TBP binds rare earth nitrates without releasing protons

✅ 0.8 mol/L loading capacity vs China's 0.2 mol/L with P507 — 4X more efficient

✅ NH₄NO₃ byproduct captured and sold as agricultural fertiliser — not toxic waste

✅ Lower carbon footprint (LCA-verified)

✅ Requires expensive stainless steel construction — that's the moat

The capital intensity of high-grade stainless steel throughout 1,100 tanks is why no one can just copy this. It is Solvay's economic and technical moat.

The 2025–2026 production ramp — what's commercial NOW ✅

April 8, 2025 — Official inauguration. NdPr oxide commercial production begins. First European facility producing magnet-grade Neodymium and Praseodymium at scale outside China.

H2 2025 — Solvay becomes Europe's first commercial producer of high-purity Samarium oxide — the foundational element for SmCo magnets used in aerospace, defense, radar, and sonar. Offtake locked with 🇬🇧 LCM (USA Rare Earth) and 🇺🇸 Permag in a 3–5 year closed-loop supply agreement.

September 2026 — Industrial-scale separation of Dysprosium and Terbium — the two heavy rare earths that make EV and wind turbine magnets resistant to demagnetisation at high temperatures. This is the critical target. Confirmed in the official Solvay–Viridis LOI press release, 1 June 2026.

2030 target: Supply 30% of total European demand for magnet-grade rare earths.

The feedstock pipeline is now transcontinental 🌍

🇦🇺 Hastings Technology Metals — Yangibana, Western Australia. Hard-rock ironstone deposit with world-leading NdPr:TREO ratio of up to 52% (Mountain Pass = 16%). MOU for 2,500 tpa MREC to La Rochelle, binding agreement being finalised. MREC route via Thailand hydromet plant.

🇧🇷 Viridis Mining — Colossus, Minas Gerais, Brazil. Ionic Adsorption Clay (IAC) deposit — 200Mt reserve, 9,400 tpa TREO at full scale, 40-year mine life. IAC naturally enriched in Dy, Tb, Sm, Gd — the heavy rare earths Solvay urgently needs. LOI signed June 1, 2026. Target MREC delivery 2028.

🇨🇦 Cyclic Materials — Kingston, Ontario. Magnet recycling rMREO confirmed chemically compatible with La Rochelle's nitrate-route SX circuits. Commercial shipments began late 2024. Transatlantic circular loop operational now.

🔄 Closing the Loop (Urban Mining & Recycling).

Because primary mining alone cannot meet future demand, Solvay is building a transatlantic circular economy:

🇨🇦 Cyclic Materials: Supplying recycled mixed rare earth oxides (rMREO) from dismantled North American electronics and motors directly to La Rochelle for purification.

🇫🇷 Carester & Caremag: Partnering locally to support a massive European hub in Lacq, France, dedicated to dismantling end-of-life magnets and feeding the recovered concentrates back into the advanced separation supply chain.

The offtake partners — who is buying this material? 🤝

🇺🇸 Noveon Magnetics — NdPr DyTb oxides. Binding supply agreement November 2025.

🇺🇸 Permag — Samarium oxide. Binding agreement November 2025.

🇬🇧 LCM (now USA Rare Earth) — Samarium metal and alloys. 3–5 year closed-loop deal.

CEO Philippe Kehren on the US/Europe split (Reuters, November 12, 2025): "We observe that US customers are ready to finalise commercial contracts today. This is not yet fully the case in Europe, but we are actively pursuing it."

The circular economy stack ♻️

🔄 Cyclic Materials (Canada) → rMREO → La Rochelle SX → Magnet-grade separated REOs

🔄 Carester/Caremag (Lacq, France — commissioning late 2026) → 2,000 tpa EOL magnets 5,000 tpa mined concentrates → feeds La Rochelle for final purification

🔄 REE-FLEX Project (2025–2028, EIT RawMaterials) → Carester KU Leuven SOLVOMET → next-gen modular SX optimised for mixed primary/recycled feedstocks

La Rochelle is not just a primary refinery. It is being engineered as the separation node for the entire European circular economy — from recycled London hard disk drives all the way to Brazilian clay.

The CRMA alignment — this is the backbone of EU strategy 🇪🇺

EU Critical Raw Materials Act 2030 mandates:

Extract ≥10% domestically

Process ≥40% domestically ← Solvay is the primary answer

Recycle ≥15% from secondary sources

No single country >65% of any processing stage

🎯 The 2030 Goal

La Rochelle, at 30% of European demand by 2030, is the single most important piece of industrial infrastructure in Europe's attempt to comply with its own legislation.

The bottom line

1. 🧪 Dy/Tb Separation — September 2026 Target

This is the most imminent milestone. Solvay has publicly committed to industrial-scale Dy/Tb separation lines commissioned by September 2026 — confirmed in the official Viridis LOI press release.

Watch for:

Official Solvay press release confirming Dy/Tb line commissioning (Q3 2026)

First commercial Dy/Tb oxide shipment to Noveon Magnetics or a defence customer

Any Q3 2026 earnings roadshow language confirming volumes — the May 2026 roadshow deck already flagged this milestone

⚠️ Risk: The line commissions but runs at minimal throughput — Solvay has been explicit that future scale-up is contingent on OEMs committing to "buy local." If European magnet makers don't sign offtake, the line runs but doesn't ramp.

2. 🇧🇷 Viridis/Colossus MREC — 2028 Target

This is the heavy REE feedstock answer — Dy, Tb, Sm, Gd from Brazilian ionic adsorption clay. Without Colossus, Solvay's Dy/Tb line has limited primary feedstock — it would rely almost entirely on recycled sources and whatever Hastings can supply (which is predominantly light REEs).

3. 🇦🇺 Hastings/Yangibana — "Few More Years" Is Right

Hastings has faced repeated construction delays and financing challenges at Yangibana. The MOU with Solvay for 2,500 tpa MREC was signed October 2022 — the binding offtake has still not been formalised.

⚠️ Risk: Hastings is a under significant financial pressure. Yangibana still required A$320M in additional financing to complete construction. The Thailand hydromet JV adds a second jurisdiction of execution risk. Realistically 2027–2028 for first MREC, if everything goes to plan.

4. ♻️ Magnet EOL Collection — The Structural Gap

This is the least-discussed but most structurally important constraint. Solvay's circular economy thesis — Cyclic Materials rMREO → La Rochelle SX → separated oxides — only scales if end-of-life EV motors and wind turbines are actually being collected and dismantled in volume.

While Solvay's La Rochelle facility has historically possessed the technical capability to separate all rare earths, the specific new industrial-scale separation circuits dedicated to heavy rare earths like Dysprosium (Dy) and Terbium (Tb) are currently in the final stages of deployment.

Solvay is officially targeting to commence the industrial-scale separation of Dy and Tb by September 2026. They are rolling out their massive capacity expansion in phases: they started with light rare earths like Neodymium (Nd) and Praseodymium (Pr) in April 2025, followed by Samarium (Sm) in the second half of 2025, making the dedicated heavy rare earth circuits the next major milestone.

Solvay is not a miner. It is not a recycler. It is the separation and purification bottleneck — the one step that cannot be skipped, cannot be rushed, and cannot be replicated in under a decade. The separation factor between adjacent lanthanides is so small that achieving >99.9% purity across 18 distinct SX batteries is an art form that has taken 75 years to master.

When Western governments say they want to "break China's rare earth dominance," Solvay's La Rochelle is the facility they are all implicitly relying on to make that possible. 🏭🇫🇷

Europe's green transition is officially getting its engine. 🚗💨🔋

📌 @roblun1

@SolvayGroup @Viridis_VMM @CyclicMaterials @LCM_Metals #Solvay #LaRochelle #RareEarths #CriticalMinerals #SolventExtraction #NitrateRoute #TBP #CYANEX572 #CircularEconomy #MagnetRecycling #Carester #Caremag #HastingsTechnologyMetals #LCM #Noveon #Permag #CRMA #CriticalRawMaterialsAct #EuropeanSovereignty #SupplyChain #EVs #Defense #GreenEnergy #EnergyTransition #France #ChineseExportControls #WesternSupplyChain #REEFLEX #EITRawMaterials #SmCo #IAC #MREC #SeparationTechnology #IndustrialChemistry 🧪⚗️🇫🇷🌍♻️🔋🧲💎🏭🇪🇺

2

2

11

928

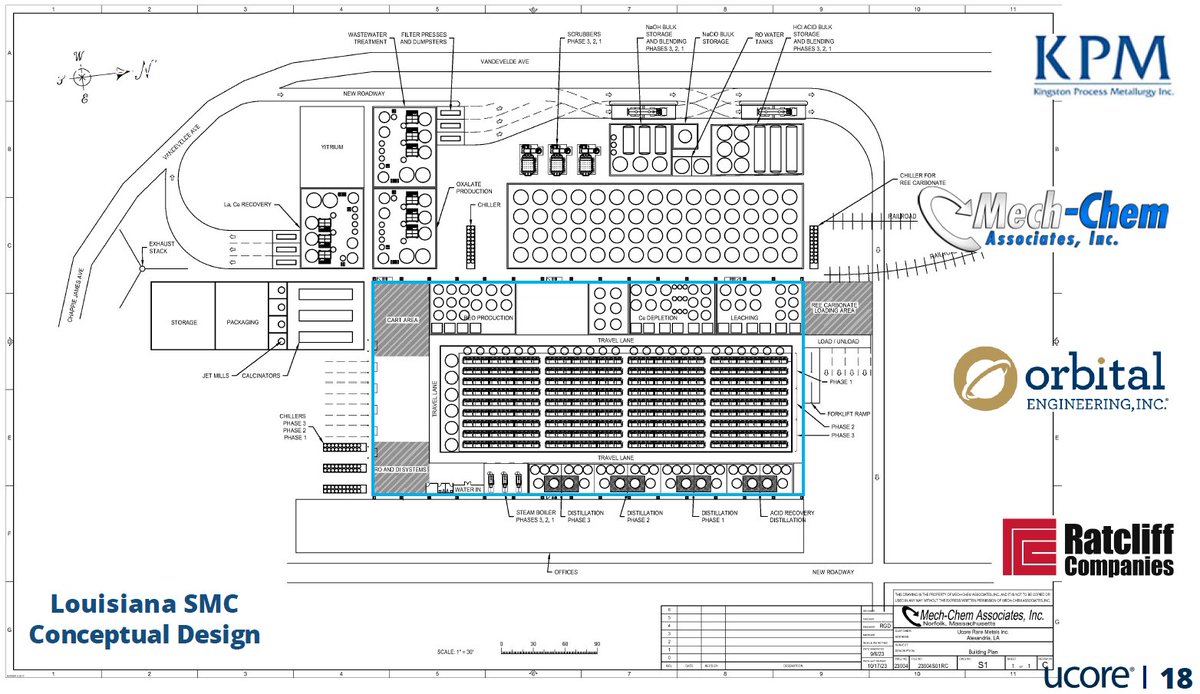

⚗️🧲🇺🇸 After 6,500 hours in a Kingston demo plant, Ucore just published the most detailed commercial engineering plan for a Western heavy rare earth separation facility ever released.

And the numbers are sharper, not smaller. 🧵

📐 [Attach images: RapidSX demo plant photo SMC floor plan schematic site layout with KPM/Orbital/Mech-Chem/Ratcliff logos]

🔬 RapidSX™ Technology Explained — Then vs Now

What the schematics show (your uploaded images):

The photo shows Ucore's Kingston, Ontario 52-stage RapidSX™ Commercial Demo Plant — rows of black-framed vertical columns filled with organic and aqueous solutions, valve manifolds and red actuators at every stage, all plumbed together in a long hall with yellow safety lanes on the floor. This is the physical embodiment of what is essentially a 52-stage continuous counter-current solvent extraction circuit, but executed in compact vertical columns rather than traditional mixer-settlers, making it roughly 10x smaller in footprint.

The floor plans show the full Louisiana SMC conceptual layout: REE carbonate loading area on the right, a dedicated leaching zone, Ce depletion circuit, REO production area, RO/DI water systems, steam boilers, three separate distillation trains (for acid recovery and concentration), oxalate production, yttrium recovery, jet mills/calcinators, storage and packaging — all feeding into the central RapidSX™ production hall. Phase 1 (the yellow highlighted rows) is the first RapidSX™ production lane; Phases 2 and 3 expand behind it using the same modular column architecture.

⚗️🧲🇺🇸 What RapidSX™ actually is

The flowchart maps the 52-stage process logic:

Feedstock (mixed REE chloride) enters at stage 1 → organic/aqueous mixing → phase separation (disengagement) at each stage → transfer to the next → through all 52 stages → final fractions recirculated → scrubbing, stripping, product precipitation → individual REE solution recovery → calcining → final REO powder. This runs as a fully automated, PLC-controlled, single-operator process with approximately 600 feedback sensors monitoring pH, interface levels, pressures and flow rates in real time.

The full site layout shows the engineering consortium behind the SMC: Mech-Chem Associates (process engineering), Kingston Process Metallurgy (KPM) (hydrometallurgical design), Orbital Engineering Inc. (CAPEX and capacity engineering, the lead on the May 2026 report), and Ratcliff Companies (construction).

What the May 27, 2026 Engineering Report actually changes ⚙️

What has changed — the optimisation:

1. The original Louisiana SMC plan called for four RapidSX™ production lines, each at ~3,000 tpa TREO, for a total of ~12,000 tpa. After 6,500 hours of Kingston demo trials, Orbital's engineering report has now optimised this to three production lines (~9,000 tpa) plus an initial 600 tpa standalone Machine A, for a total of ~9,600 tpa TREO.

2. Machine A itself has grown from 64 stages to ~118 stages, allowing it to directly produce NdPr, Pr, Nd, Sm, Gd, Tb and Dy from MREC/MREO feedstock without interim holding tanks — a critical redesign driven by direct feedback from North American defense contractors who need Western-sourced separated heavy REEs urgently.

3. Machine A capex: US$60M, partly funded by the DoW US$18.4M agreement; Production Line 1 adds another US$44M; oxide production and packaging US$31M — total Machine A Line 1 cumulative cost: US$135M, with Machine A commissioning targeted for H1 2027.

So the evolution is:

1. 52 stages (demo) →

2. 64 stages (earlier commercial design) →

3. ~118 stages (current Machine A design)

Each “stage” is a physical column step in the same machine. More stages = more resolution and flexibility, not multiple trips through the same 52‑stage loop.

⚗️♻️The Kingston demo plant runs 52 RapidSX stages. Ucore’s first commercial Machine A has now been redesigned to roughly 118 stages in a single pass, up from the original 64‑stage concept. That gives enough separation resolution to pull out NdPr, Nd, Pr, Sm, Gd, Tb and Dy from MREC/MREO feedstock in one continuous circuit, instead of running the feed through several shorter loops or intermediate holding tanks.

The platform, the plan, the clock ⏰

Ucore isn't just building a separator. The Louisiana SMC floor plans you're looking at show the full downstream: leaching, Ce depletion, yttrium recovery, acid distillation and recycling, oxalate precipitation, calcination, jet milling and packaging.

From MREC carbonate arriving at the loading dock to REO powder leaving in drums — the entire commercial flowsheet has been demonstrated at Kingston and is now being copy-pasted to Louisiana.

Machine A commissioning: H1 2027.

DoW funding committed: US$18.4M (Phase 2 project).

Canadian government conditional funding: C$36.3M (announced Oct 2025, pending finalization).

Defense contractors: actively qualifying Ucore's REO products.

The 2027 statutory defense sourcing deadline for non-Chinese rare earths isn't moving. Ucore's Machine A timeline is built around it.

investornews.com/member_news…

$UURAF $UCU 🇺🇸🇨🇦🧲

📌 @ucore

@ucore

#Ucore #UURAF #UCU #RapidSX #LouisianaSMC #RareEarths #HeavyRareEarths #Dysprosium #Terbium #NdPr #Samarium #Gadolinium #REO #SolventExtraction #HydroMet #CriticalMinerals #DefenseIndustrialBase #DoW #DoD #AlexandriaLouisiana #KingstonOntario #NorthAmerica #WesternSupplyChain #MineToMagnet #NdFeB #DefenceMagnets #SupplyChainResilience #ZeroChinaNexus #2027Deadline #OrbitalEngineering #MechChem #KPM #Onshoring #EVMagnets #WindTurbines #EnergyTransition 🔬⚗️🧲🇺🇸🇨🇦

1

8

621

🇦🇺⚗️ A $730M Australian rare earths project just became one of the most strategically important industrial operations on the planet.

@LynasRareEarths . Mount Weld, Western Australia. The world's largest rare earth producer outside China — and as of 2025, the world's only commercial producer of separated Dysprosium and Terbium outside China.

Here's why that matters more than almost anything happening in critical minerals right now 🧵👇

What Lynas Actually Is

Most people think of Lynas as a miner. That massively undersells it.

Lynas is a fully vertically integrated rare earth operation — mine to separated oxide — spanning two countries:

⛏️ Mount Weld, WA — the world's highest-grade rare earth deposit. Ore mined, crushed and concentrated on site

🚢 Concentrated ore shipped to Malaysia

🏭 LAMP, Gebeng, Malaysia — 100-hectare advanced materials plant. Cracking, leaching, solvent extraction, product finishing

📦 Separated, high-purity REOs shipped to customers in Asia, Europe and the USA

The $500M Mt Weld expansion targets 12,000 tpa NdPr feedstock capacity — the backbone of every EV motor and wind turbine generator being manufactured in the West.

Why SX is the Hard Part

Rare earth separation via Solvent Extraction (SX) is one of the most technically demanding processes in industrial chemistry. Here's why.

All 15 lanthanides share nearly identical atomic radii and the same 3 oxidation state. The only handle you have is lanthanide contraction — a minute, progressive decrease in ionic radius across the periodic table.

To exploit differences measured in picometres, Lynas runs liquid-liquid counter-current SX trains — immiscible organic and aqueous phases aggressively contacted and separated across hundreds of sequential mixer-settler stages.

The organic extractant selectively binds heavier REEs preferentially. The lighter ones stay aqueous. Then you strip, scrub, re-extract — repeatedly — incrementally building purity across the cascade. Because the separation factor between adjacent lanthanides (e.g. Nd vs Pr) is extremely low, a single contact stage achieves almost nothing. You need the entire cascading train to reach >99.9% purity.

That's what's running inside LAMP 24 hours a day, 365 days a year. And Lynas has been doing it at commercial scale longer than any Western operator alive.

The History-Making Milestone of 2025

🚨 This is the one that changed everything.

In May 2025, Lynas confirmed first production of Dysprosium Oxide from a newly commissioned Heavy Rare Earth separation circuit at Lynas Malaysia. Terbium followed in June 2025.

With those two products, Lynas became the world's only commercial producer of separated Heavy Rare Earth products outside China.

Read that again. Outside China, no other company on Earth was commercially producing separated Dy or Tb at this scale. Not in Europe. Not in the USA. Not anywhere.

The new HRE circuit was reconfigured from an existing SX train at ~$25M capex — extraordinary capital efficiency — and is designed with capacity to separate up to 1,500 tpa of SEGH (Samarium, Europium, Gadolinium, Holmium) per year, with Dy and Tb as the headline products.

Lynas' HRE product suite now spans 5 products: Dy, Tb, unseparated SEG, Holmium concentrate, and unseparated SEGH. A complete heavy rare earth offering. From one site. Outside China.

The Scale of What's Being Built

📊 Lynas production targets across the integrated operation:

🧲 NdPr — targeting 10,500 tpa (Lynas 2025 strategy) scaling toward 12,000 tpa with Mt Weld expansion

⚡ Dy Tb — new HRE circuit, 1,500 tpa SEGH separation capacity

🏭 Malaysia SX & PF — 10.5 ktpa capacity uplift underway, continuous flowsheet improvements

🌏 FY25 Revenue — A$556.5M, driven primarily by increased NdPr production and sales

For context on why Dy and Tb matter right now:

💰 Dysprosium oxide: $1,000 /kg outside China (Chinese export controls 2025)

💰 Terbium oxide: $4,500 /kg outside China

🚫 China imposed export controls on both in 2025 — and by 2027, Chinese REE content must be completely removed from US weapons systems

Lynas is now the only Western source of both. The strategic leverage is almost impossible to overstate.

The Kalgoorlie Piece

The $730M total investment picture includes the Kalgoorlie Rare Earths Processing Facility — a planned cracking and leaching plant in Western Australia that would move the most radioactivity-intensive processing steps onshore in Australia, reducing Lynas' regulatory exposure in Malaysia and further sovereignising the supply chain.

This is the strategic architecture of a company thinking decades ahead — not just optimising a plant, but reshoring the geopolitically sensitive front-end processing to a Five Eyes jurisdiction under the US-Australia Critical Minerals Framework.

Mount Weld → Kalgoorlie (crack & leach) → Malaysia (SX separation) → Global customers

Every node of that chain is outside China. Every product is traceable. Every oxide is verifiable Western origin. That's exactly what defence OEMs and EV manufacturers are being mandated to source.

The Big Picture

China controls ~85% of global rare earth refining. The Lynas operation is the single most important structural counter to that monopoly currently in production.

🇦🇺 World's largest REE producer outside China — operational for over a decade

⚡ World's only commercial separated Dy and Tb producer outside China — since May 2025

🧲 Scaling toward 12,000 tpa NdPr — enough for ~4M EV traction motors annually

🌏 Fully aligned with US-Australia Critical Minerals Framework

🔬 Continuous SX flowsheet improvements — the competitive moat deepens every quarter

Operating out of Western Australia.

$LYC 🇦🇺

#LynasRareEarths #RareEarths #CriticalMinerals #MountWeld #NdPr #Dysprosium #Terbium #SolventExtraction #AustralianMining #EnergyTransition #DefenceSupplyChain #WesternSupplyChain #EVs #Kalgoorlie #SovereignCapability #HeavyRareEarths #REE

2

4

16

1,031

⚗️🧲 PART TWO: SEG — The Most Strategically Important Product Nobody Has Heard Of

Following up on today's thread on Western CIF pricing and the separation bottleneck 👇

Most people talking about rare earths focus on NdPr amd DyTb. The real supply chain crisis is one step further down the periodic table.

Let me explain what SEG and SEGH actually is — and why it matters enormously.

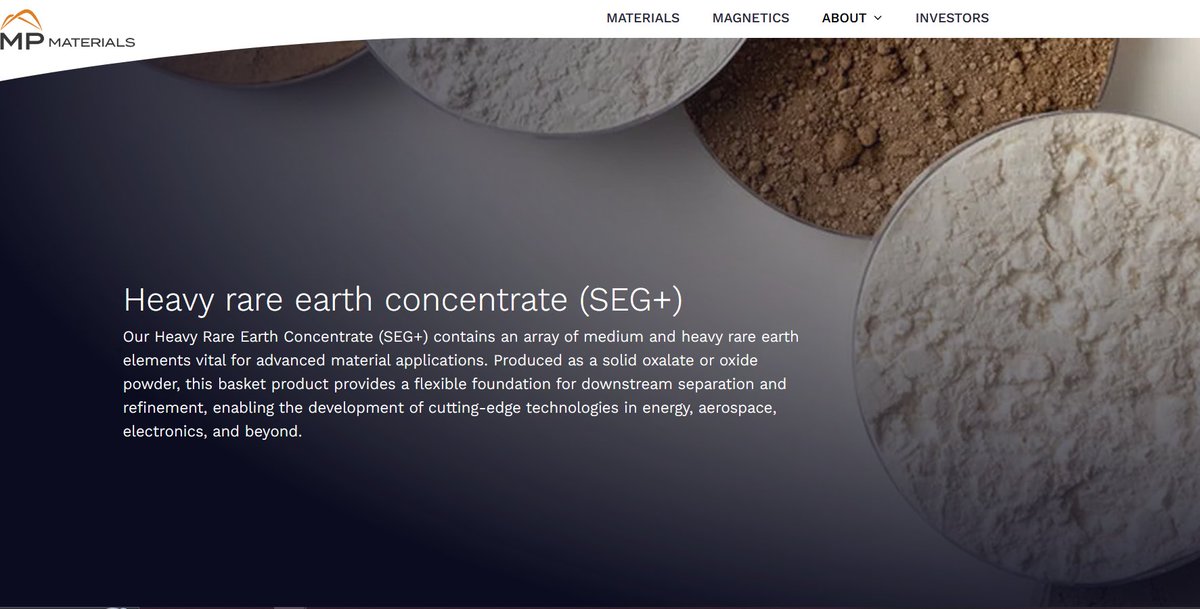

📦 WHAT IS SEG ?

SEG is MP Materials' Heavy Rare Earth Concentrate — produced at Mountain Pass, California:

Medium REEs in SEG :

🔵 Samarium (Sm) — SmCo high-performance defence magnets, cancer treatment, nuclear reactor control

🔵 Europium (Eu) — optical displays, phosphors, anti-counterfeiting (Euro banknotes)

🔵 Gadolinium (Gd) — MRI contrast agents, nuclear reactor shielding, neutron radiography

Heavy REEs in SEG :

🔴 Dysprosium (Dy) — NdFeB high-temperature magnet additive, EVs, wind turbines, defence

🔴 Terbium (Tb) — NdFeB magnet additive, naval sonar (Terfenol-D), fuel cells

🔴 Holmium, Erbium, Thulium, Ytterbium, Lutetium, Yttrium

The Dy Tb fraction = ~4% of total rare earth oxides in SEG — the two most critical, most China-controlled, most expensive elements in the entire basket

Form: solid oxalate or oxide powder (basket product)

Status: being continuously produced and stockpiled at Mountain Pass — not yet separated

Lynas's equivalent product is called SEGH (not SEG ):

Contains: Samarium, Europium, Gadolinium, Holmium, Dysprosium, Terbium

Also sold as a mixed compound to customers who further separate it

This is Lynas's current commercial product — the individually separated Dy and Tb oxides are a newer, small-volume production stream from their expanded HRE facility

🏭 THE CRITICAL DISTINCTION: BASKET PRODUCT vs SEPARATED OXIDES

MP Materials SEG :

→ Produced as solid oxalate or oxide powder

→ A basket product — all the above elements together, unseparated

→ Being continuously stockpiled at Mountain Pass

→ Heavy rare earth separation circuit commissioning Q2 2026

→ Until then: sold as feedstock for downstream third-party separation

Lynas SEGH (their equivalent):

→ Contains Sm, Eu, Gd, Ho, Dy, Tb as a mixed Heavy REE compound

→ Currently sold to customers who further process it into separated materials

→ Individually separated Dy and Tb oxides: new, small-volume, just scaling

→ Q3 FY2026: only ~8 tonnes Dy Tb combined from separated stream

Both products = feedstock that still needs further separation chemistry before it becomes a usable Dy₂O₃ or Tb₄O₇

🚨 THE HIDDEN QUESTION THAT CHANGES EVERYTHING

So if MP is stockpiling SEG and Lynas is selling SEGH as a mixed compound —

Who separates it into individual high-purity Dy₂O₃ and Tb₄O₇?

This is not a theoretical question.

Right now, today, in 2026 — outside China the answer is:

✅ Lynas — small volumes, Malaysia, scaling

❌ MP — not yet (H2 2026 target)

❌ Energy Fuels — NdPr only, no HRE separation yet

❌ Neo Performance Materials — downstream processor, not primary separator at scale, only in-house.

The separation chemistry IP for individual HRE oxides at >99.5% purity remains China's most tightly held advantage — and the West's most critical gap.

💡 WHERE IONIC TECHNOLOGIES SITS IN THIS PICTURE

Ionic Technologies' MAIL™ technology is specifically designed to separate individual REOs from mixed rare earth feedstocks — using patented multi-amide ionic liquid extraction rather than conventional solvent extraction.

The demonstrated results from recycled magnet feedstock:

🔬 Dy₂O₃ — 99.56% purity

🔬 Tb₄O₇ — 99.75% purity

🔬 Nd₂O₃ — 99.87% purity

The MAIL™ platform is feedstock agnostic — it can process recycled magnet scrap, MREC (Mixed Rare Earth Carbonate from mines), and critically, mixed SEG /SEGH concentrate.

In other words: the technology that Belfast uses to separate recycled magnet scrap into individual REOs is the same technology that could separate MP's stockpiled SEG or Lynas's SEGH into the high-purity individual Dy and Tb oxides that OEMs cannot currently source outside China.

💡 THE SEPARATION BOTTLENECK — PROVEN BY THE CYCLIC MATERIALS MODEL

Let me show you exactly why separation is the critical chokepoint — with a real example.

Cyclic Materials (Canada) is one of the best-funded rare earth recyclers in North America. It built its Hub100 plant in Kingston, Ontario using its proprietary REEPure™ technology — producing recycled Mixed Rare Earth Oxide (rMREO) from end-of-life magnets.

What did they do with that rMREO?

They shipped it to France.

To Solvay's La Rochelle plant — Europe's most experienced rare earth separator, operating since the 1970s — for further individual separation and purification into magnet-grade NdPr and Nd oxides.

➡️ Cyclic could recycle the magnets.

➡️ Cyclic could produce the mixed oxide.

➡️ But Cyclic could not separate it to individual high-purity oxides at specification grade.

➡️ They needed Solvay's 50 years of rare earth separation expertise to do that final step.

And this is with LREEs only — NdPr, which are the easier rare earths to separate.

🔬 THE FOUR WESTERN SEPARATION TECHNOLOGY ARCHETYPES

The West is now fielding four distinct technology approaches to solve the separation bottleneck. Understanding how they differ is critical for anyone assessing where the real value sits.

① SOLVAY (Belgium/France) — Conventional Solvent Extraction, Incumbent

🏭 La Rochelle, France — operating since the 1970s

→ Uses multi-stage mixer-settler solvent extraction (the same fundamental chemistry China uses)

→ Currently processing Cyclic Materials' rMREO feedstock for individual REO separation

→ Strength: 50 years of process knowledge, validated with OEMs

→ Limitation: capital-intensive, large physical footprint, complex permitting, decades to replicate

② ReElement Technologies (USA) — LAD Chromatography Resin

🏭 Marion, Indiana — Noblesville refinery expanded 141% (2025)

→ Uses Ligand-Assisted Displacement (LAD) chromatography — adapted from pharmaceutical sector

→ Claims 100x more efficient than conventional mixer-settler configurations

→ 80% lower waste profile vs conventional SX — critical for US permitting

→ Validated: Gd, Ga, Ge, Tb and Y to 99.999% purity (five nines)

→ Capacity target: 10,000 tpa via $200M TEP equity facility (Jan 2026)

→ Status: scaling Marion; HREEs including Dy and Tb at 99.5% in commercial production

→ Strength: modular, column-based, smaller footprint, defence-validated

→ Limitation: unproven at full industrial scale for HREE basket separation

③ Ucore Rare Metals (Canada/USA) — RapidSX™ Column Solvent Extraction

🏭 Kingston, Ontario (52-Stage Demo Plant) → Alexandria, Louisiana (Strategic Metals Complex)

→ Uses column-based SX — same chemistry as conventional but 3–4x faster throughput

→ No powered mixing tanks — gravity-fed column contactors replace mixer-settlers

→ 5,700 hours of HREE processing at demo plant

→ Demonstrated splits: LaCe, NdPr, SmEuGd, Sm, Gd, TbDy, Tb, Dy individually — all groups

→ $22.4M US Department of War Other Transaction Agreement — US DoD sponsored

→ Louisiana SMC: RapidSX™ Machine #1 installation mid-2026; HREE focus: Tb, Dy, Y

→ 25,000 samples proving RapidSX™ and conventional CSX yield virtually identical chemistry

→ Strength: proven heavy REE splits including individual Tb and Dy, DoD-validated, US sovereign

→ Limitation: not yet at commercial scale; Louisiana SMC still under construction

④ Ionic Technologies (UK) — MAIL™ Ionic Liquid Extraction

🏭 Belfast, Northern Ireland

→ Uses patented multi-amide ionic liquid (MAIL™) — fundamentally different chemistry to SX

→ Not conventional solvent extraction — does not require the same reagent infrastructure China built

→ Feedstock agnostic: oxidised magnets, coatings, variable grade, MREC, recycled scrap

→ Demonstrated: Nd₂O₃ 99.87%, Dy₂O₃ 99.56%, Tb₄O₇ 99.75% — from recycled feedstock

→ Ford durability tested — recycled rotor passed comparable to virgin material

→ 61% lower CO₂ vs primary mine supply chain

→ £23M UK Government backed (CirculaREEconomy £11M £12M capital grant OIP)

→ Strength: only Western technology demonstrated separating both recycled Dy AND Tb to spec; fully integrated — no Solvay needed; UK sovereign

🔮 THE ADAMAS FORECAST CONTEXT

Adamas Intelligence forecasts:

🔴 By early 2030s: China becomes a net importer of Dy and Tb

🔴 Pricing power transfers to Western CIF price levels

🔴 Rotterdam Tb ask price already: >$4,500/kg vs China EXW ~$936/kg

🔴 CIF North America Dy: forecast 8.3x Chinese price by 2027 (Benchmark Mineral Intelligence)

The stockpile being built at Mountain Pass right now will one day need to be separated into individual HRE oxides at Western facilities.

The pricing premium that separation commands is already visible in Rotterdam and CIF benchmarks.

The separation IP and demonstrated capability to deliver specification-grade Dy and Tb is held by a very short list of organisations outside China.

The value in this supply chain is not in the mine.

It is not even in the concentrate.

It is in the separation step.

📌 Sources: MP Materials SEG product page | Lynas Products page | Adamas Intelligence | Benchmark Mineral Intelligence | Ionic RE ASX | Fastmarkets CIP March 2026

🔗 mpmaterials.com/product/seg/

🔗 lynasrareearths.com/products…

#SEGplus #SEGH #RareEarths #HeavyRareEarths #Dysprosium #Terbium #Samarium #Gadolinium #MPMaterials #Lynas #IonicRareEarths #IonicTechnologies #MAIL #IXR #CriticalMinerals #WesternCIF #Separation #SolventExtraction #NdFeB #Magnets #SupplyChain #China #ExportControls #AdamasIntelligence #MountainPass #Belfast #PriceDiscovery #EnergyTransition #Defence

1

3

14

1,739

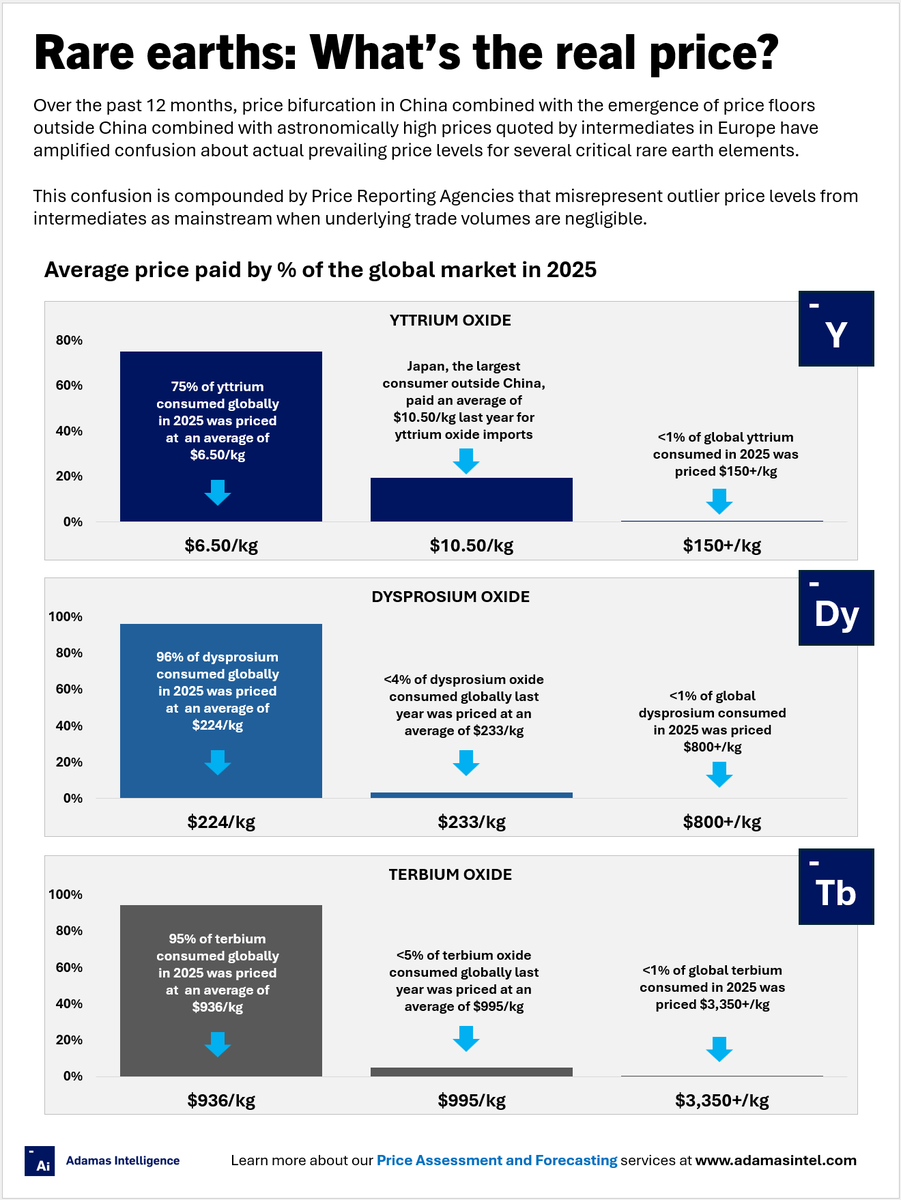

🚀 Adamas launches Western CIF price forecasts.

Part One

Very interesting, we also have Fastmarkets also launched rare earth price assessments in March 2026 — confirming the market urgency for non-Chinese price discovery.

discoveryalert.com.au/critic…

With multiple new Western refiners of NdPr and SEG products entering the market, interest is growing in reliable price forecasts for these oxides produced in – and delivered to – North America and Europe.

As Lynas Rare Earths, MP Materials, Neo Performance Materials, Energy Fuels and others ramp up separation capacity, key questions emerge: How will these materials be priced, and how will those prices evolve amid shifting regional and global supply-demand dynamics?

Today, virtually no separated and refined Dy, Tb, Sm, Gd, Y or Lu oxides are produced or traded outside China. With little-to-no transaction data available, traditional price discovery is nearly impossible.

To bridge this gap, Adamas has developed detailed production cost models for each of these oxides and analyzed end-users’ willingness to pay. This enables Adamas to forecast – Adamas's view – how Western CIF prices are likely to evolve in response to changing market fundamentals.

📋 DEEP RESEARCH BRIEF

The SEG Problem: Where Western Separation Actually Stands (May 2026)

Lynas (ASX: LYC) is currently the only commercial producer of separated Heavy Rare Earth oxides outside China. Here's what they have achieved:

✅ Separated Dysprosium oxide — first production May 2025

✅ Separated Terbium oxide — first production June 2025

✅ Separated Samarium oxide — first production March 2026, ahead of schedule

🔄 Expanded HRE facility under construction at Lynas Malaysia — full suite (Sm, Gd, Dy, Tb, Y, Lu) within 2 years

⚠️ BUT: Scale is still very small. Lynas produced only 8 tonnes of Dy and Tb combined in Q3 FY2026 — vs China's prior ~11 tonne/month of Terbium alone before export controls.

MP Materials (NYSE: MP) is behind Lynas on HRE separation:

🔄 Heavy rare earth separation circuit at Mountain Pass commissioning imminent as of Q1 2026

🔄 Expected commercial production mid-2026

📦 MP is currently stockpiling SEG concentrate — selling it as a basket product (oxalate/oxide powder) for downstream third-party separation

🚨 Until HRE separation is online, high-performance NdFeB magnets requiring Dy/Tb still cannot be made from domestic MP supply alone

The SEG Pricing Question ?

"Is the pricing model now about selling SEG as a feedstock for further refining?"

Yes — and this is the crux of the Adamas CIF pricing challenge. Because:

1. MP is selling SEG as a mixed concentrate — not separated oxides

2. The buyers of SEG are companies with the IP to separate it further — a very short list outside China

3. Lynas's separated Dy and Tb volumes are tiny relative to market need

4. Virtually no separated Gd, Y, Sm, Lu are traded outside China today — Adamas confirms this [Adamas article]

NdPr prices have surged 41% in 2026, but HRE oxides have no reliable Western price benchmark yet — hence why Adamas is launching its Western CIF price forecasting.

✅ There are emerging Western/European prices — and they are extraordinary compared to Chinese domestic prices. Here's the full picture:

1. 🏷️ Rotterdam "Ask Prices" — The European Security Premium Reality

The Rotterdam spot market has been the de facto European price discovery point for secured, non-Chinese Dy and Tb — and the numbers are staggering: See Image

But here's the critical context Adamas Intelligence revealed: less than 1% of global Dy and Tb volume is actually transacting at those Rotterdam prices. The vast majority is still priced at Chinese levels — because Western buyers have almost no alternative supply to purchase from. The Rotterdam price is an ask price with almost no sellers — which is exactly why Adamas calls existing European price assessments a "fallacy" and is building proper cost-based CIF forecasts.

2. 📊 Fastmarkets CIF Global Benchmarks — March 2026

Fastmarkets launched three new global CIF price assessments on 19 March 2026, becoming the first major PRA to formally price ex-China HREs:

MB-DY-0005 — Dysprosium oxide 99.5%, CIP global, $/kg

MB-DY-0006 — Ferro-Dysprosium 80%, CIP global, $/kg

MB-TB-0004 — Terbium oxide 99.99%, CIP global, $/kg

These are real transacted/assessed benchmarks — separate from the Rotterdam ask prices — and represent the first systematic ex-China price infrastructure.

discoveryalert.com.au/critic…

3. 📈 Benchmark Mineral Intelligence — The 8x Premium Forecast

Benchmark Mineral Intelligence data shows the price gap is widening, not closing:

In 2025: CIF North America Dy was 4.4x higher than EXW China

By 2027 forecast: CIF North America Dy projected at 8.3x higher than Chinese prices

European Tb prices showed a similar divergence pattern

🚨 The Yttrium Case Study — How Fast This Can Move

Yttrium oxide outside China has gone from ~10x Chinese domestic price last autumn → 115x by March 2026 → 150x by 30 April 2026:

CIF North America Yttrium oxide: $1,575/kg (30 April 2026)

China domestic average 2026: ~$10/kg

A 150x bifurcation — driven entirely by export controls and access security premiums

🔑 The Adamas "Fallacy" Argument — Why This Matters