Devyani-Sapphire Mega Merger: શેરહોલ્ડર્સ માટે મોટી તક કે મોટું જોખમ?

#DevyaniInternational #SapphireFoods #DevyaniSapphi #ReMerger #BusinessNews #MegaMerger @Ajay_1108

2

2

64

Andhra rajakeeya nayakulu Andhra prajala ninchi kaaka paininchi oodi paddara? Other states didn't lose their capitals . Once you create borders you only increase hate especially in this case . If you are sincere the only solution is remerger.

మన తెలంగాణకు అన్యాయం చేసింది ఆంధ్రా రాజకీయ నాయకులు. అంతేగానీ అక్కడి సామాన్య ప్రజలు కాదు.

తెలంగాణ ప్రజలు ఏనాడూ రాజకీయ రొచ్చులో పడి ఆంధ్రా అన్నదమ్ములను దూరం చేసుకోలేదు. స్నేహ సంబంధాలు తెంచుకోలేదు. భారతదేశంలో మనకంటే ముందు ఏర్పడిన ఛత్తీస్ఘడ్ , ఝార్ఖండ్ , ఉత్తరాఖండ్ ల విషయంలో ఈ స్థాయి ఉద్విగ్న పరిస్థితులు కలగలేదు. గమనించండి 🙏

రెండు తెలుగు రాష్ట్రాల మేలు కోరేవాడే నిజమైన దేశభక్తుడు.

94

Apr 27

Keeping it outside India is a greater challenge to India's NorthEast by use of terror proxies, threat to chicken neck, forceful conversion of Hindus, eviction causing demographic imbalances/refugee crisis, denial of access to sea, possibility of remerger with Pakistan etc.

2

1

33

Apr 27

D'un coté le move est compréhensible, et je dirais même que c'est sain : ça permet de tester les features at scale et la core team peut ensuite aller cherry-pick au pire, au mieux remerger.

2

5

2,080

They’re waiting for the central funds to come which is expected due to remerger of corp. only after that plan will be executed. Land is available at every layout for parks. At some places it is maintained well also 👍

2

16

Feb 19

nah im from ap and im happy with separate tg state as of now because we were getting too dominant with united ap ,look at current tg ,atleast they are coming up and occupying top posts ,they deserve it man ,in future remerger may happen but as of now nah lets focus on our states

2

111

13 Nov 2025

3/

Provocative Views on Lebanon and Syria: Echoes of Imperial Redrawing

Barrack's diplomatic rhetoric has extended beyond insults to provocative commentary on Lebanon's sovereignty and historical borders. In November 2025, he publicly described Lebanon as a "failed state" with a "paralyzed government," underscoring U.S. frustration and suggesting it is incapable of addressing security issues like disarming militias. He tied this assessment to the Sykes-Picot agreement, the 1916 Anglo-French pact that carved up the Ottoman Empire's territories, calling it a mistake that divided Syria and the region for imperial gain rather than peace, and vowing not to repeat it. Such statements have been interpreted as threats to Lebanon's independence, implying a potential remerger or reconfiguration with Syria to achieve regional stability, especially as Barrack positions Syria and Lebanon as "next pieces" for Levant peace under frameworks like the Abraham Accords.These views raise alarms about Barrack's intentions, particularly given his dual role as Ambassador to Turkey. Critics see his dismissal of Sykes-Picot borders and emphasis on unity as aligning with Turkish President Recep Tayyip Erdogan's neo-Ottoman ambitions, potentially aiming to rebuild influences reminiscent of the Ottoman Empire to curry favor with Ankara. By suggesting redrawn maps or integrated governance, Barrack appears to prioritize geopolitical realignments over sovereign integrity, fueling chaos and mistrust in an already volatile region.

Wider Scandals: A Pattern of Privilege and Influence Trading

Barrack's trajectory is marked by opportunistic climbs. Of Lebanese descent, he grew Colony Capital into an international giant, aiding personalities like Michael Jackson via Neverland Ranch acquisition during controversy. His Trump affiliations—inaugural fundraising and Middle East counsel—solidified his influence, but questionably. The UAE affair claimed he channeled Emirati sway into the administration, a charge dismissed but lingering . Critically, Barrack symbolizes the elite's ethical void: shielded by riches, he maneuvers through controversies with regrets and shifts, avoiding genuine accountability. His Lebanon remarks, combined with Epstein associations, support for al-Sharaa, and border rhetoric expose a hypocrisy—degrading others while dodging introspection .

Final Thoughts:

Emblem of Institutional Decay Tom Barrack is no outlier; he is the grotesque face of a corrupt system where power devours decency and shields the guilty. His vile "animalistic" slur against Lebanese reporters, broadcast far and wide by international outlets, reeks of unbridled cultural supremacy and imperial disdain. The damning Epstein revelations, unearthed by relentless U.S. media scrutiny through congressional probes, expose his ties to a monstrous pedophile network, shattering any pretense of moral authority. His shameless endorsement of al-Sharaa, whitewashing brutal atrocities against Alawites, Christians, and Druze, brands him as an enabler of genocide in pursuit of cynical alliances. Worst of all, his reckless threats to dissolve Lebanon's borders—dismissing it as a failed relic of Sykes-Picot and scheming Ottoman revivals to appease Erdogan—betray a dangerous zeal for redrawing maps at the expense of sovereign nations and human lives.

Enough is enough: Barrack must be stripped of his positions immediately, declared persona non grata in Lebanon, and held accountable for his beastly conduct. No more tolerance for such predatory emissaries—America's credibility demands their swift and total excision, or the rot will consume us all, dooming global trust and diplomacy to irreparable ruin.

2

19

367

6 Nov 2025

Agriculture minister Tummala Nageswara Rao has urged Andhra Pradesh Chief Minister N. Chandrababu Naidu to consider the remerger of five villages adjoining Bhadrachalam town with Telangana, in line with the long-standing demand of the local people and their historical association with the region.

#TummalaNageswaraRao #Bhadrachalam

deccanchronicle.com/southern…

1

1

149

6 Aug 2025

TOBACCO VANGUARD est. 1977

Not for all and sundry

NO TO MERGER

By M. Reuven

It has become fashionable once again to speak of marriage. The analysts, ever eager to tidy the market into symmetrical pairs, are speculating aloud that Altria should join hands with Japan Tobacco, or perhaps with Imperial Brands, and some even raise the prospect of a reverse merger with Philip Morris International. The logic is familiar. Consolidation, we are told, breeds efficiency. Scale assures competitiveness. Global reach makes one future-proof. So the argument runs, with the tone of inevitability.

Yet in the matter of tobacco, and particularly in the case of Altria, such reasoning demands closer scrutiny. The impulse to merge does not arise from necessity but from fashion. It is less a function of strategic analysis than of speculative restlessness. It proceeds not from capital discipline, but from a kind of insecurity dressed in the language of global ambition. Tobacco Vanguard remains unconvinced.

Altria should not seek merger. Not with Japan Tobacco. Not with Imperial Brands. Not with Philip Morris. Not at these valuations, and not within this cycle. The firm should continue to stand alone, precisely as it is: a fortress of American cash flow, a bastion of enduring pricing power, and a sovereign enterprise within a sector that is already bloated with leverage and fixated on reinvention.

The case begins with the United States. The domestic tobacco market remains the most profitable nicotine territory in the world. While volumes continue to decline, they do so within a predictable and well-managed range. The structure of the market, underpinned by long-standing legal settlements and regulated by the Food and Drug Administration, provides a degree of insulation that is unmatched elsewhere. Barriers to entry are high, illicit competition is negligible, and the loyalty of the consumer base remains substantial. Marlboro, Altria’s flagship, still commands nearly half the U.S. cigarette market. With every price rise, volume falls slightly, and yet operating margins expand. It is an equation of decline managed through discipline, not desperation.

There is no international market offering a better structural profile than this. No regulatory system as stable. No consumer base as commercially responsive. No company better positioned to extract margin within it than Altria. The U.S. remains, in financial terms, the jewel of global tobacco. And Altria remains its most accomplished custodian.

The pressure to consolidate arises not from weakness but from a kind of institutional self-doubt. The argument for merger with Imperial Brands is largely cosmetic. Imperial brings with it a patchwork of European franchises, a compromised vapour portfolio, and exposure to regulatory climates that are more punitive than profitable. While the purchase price may appear attractive on paper, the quality of the business remains in question, even as its turnaround under Stefan Bomhard begins to bear considerable fruit. What strategic value it might provide could be acquired more efficiently in parts. Imperial, and its shareholders, are better left alone.

Japan Tobacco is often cited as a more compatible candidate. Yet it, too, brings complications of a different kind. The company remains partially state-owned and is entangled in a domestic political structure that does not lend itself to shareholder primacy. The Japanese Ministry of Finance holds a legally mandated stake in the firm, and any merger would, by necessity, involve high-level political negotiation. Altria’s private enterprise culture and shareholder-first ethos are unlikely to be easily reconciled with the bureaucratic temperament of a former state monopoly.

As for Philip Morris International, the argument is circular. The original demerger was deliberate. The attempted remerger in 2019 was wisely abandoned. PMI’s interest lies in accessing the U.S. market, not in sharing governance. Its strategic instinct is proprietary, not collaborative. The termination of the IQOS licensing arrangement illustrates the limits of their compatibility.

Tobacco Vanguard holds to the discipline of monetary realism. We remain sceptical of the abstractions that now dominate corporate vocabulary. Words such as “synergy”, “transformation”, and “harmonisation” conceal more than they reveal. They are ornaments of persuasion, not tools of analysis. The proper subject of consideration is cash. Altria pays its dividend. It generates consistent earnings per share through price control, operational efficiency, and judicious buybacks. It does not issue equity casually. It does not embark upon empire-building for its own sake. It retains strategic stakes in firms such as Anheuser-Busch and has exited others when conditions change. Its record of capital allocation is a model of restraint.

A large-scale merger would overturn this order. It would demand leverage, integration, compromise, and distraction. It would impose a burden of execution on a firm that has thrived by concentration, not by expansion. It would risk the dividend trajectory and endanger the internal clarity that has allowed Altria to prosper while others chase fashion.

To argue that Altria lacks access to new product platforms is mistaken. The company holds a majority interest in on!, it owns NJOY outright, and it has a structured joint venture with Japan Tobacco for the commercialisation of heated tobacco. If another product proves commercially or strategically necessary, it can be licensed, acquired, or developed internally. There is no strategic vacuum that requires a merger. There is only impatience, dressed up as necessity.

Altria should resist the call to consolidate. The logic of scale is not in itself a virtue. It becomes a liability when it obscures risk, burdens balance sheets, and disrupts focus. The true risk is not being smaller than PMI or BAT. The risk is mistaking bigness for value, and complexity for advantage.

To remain as it is, to continue extracting margin from the U.S. market, to sustain the dividend without interruption, and to invest with caution and clarity, this is not failure. It is strategy of the highest order.

The call to merge reflects a speculative modernism. It rests on the presumption that change is always improvement, that survival requires reinvention, and that capital should be restless. Tobacco Vanguard holds a different view. We defend clarity. We favour restraint. We believe in profit before posture.

Altria should remain what it is. It should convert American nicotine into shareholder capital with precision, with discipline, and without apology.

It should do so alone.

#Altria #MO #JapanTobacco #ImperialBrands #TobaccoInvesting #DividendDiscipline #MonetaryRealism #MergersAndAcquisitions #TobaccoVanguard $MO

2

8

236

15 Jul 2025

I think the split has become too wide for any reconciliation and remerger with India. We just have too balance our relationship with Chinese and Americans so they don't coddle these inbreds too much. 10 more years to widen the gap, also we need scorch earth policy inside. Come out of pajeetry and mine every place where any mineral deposits are there in India.

1

3

204

14 Jun 2025

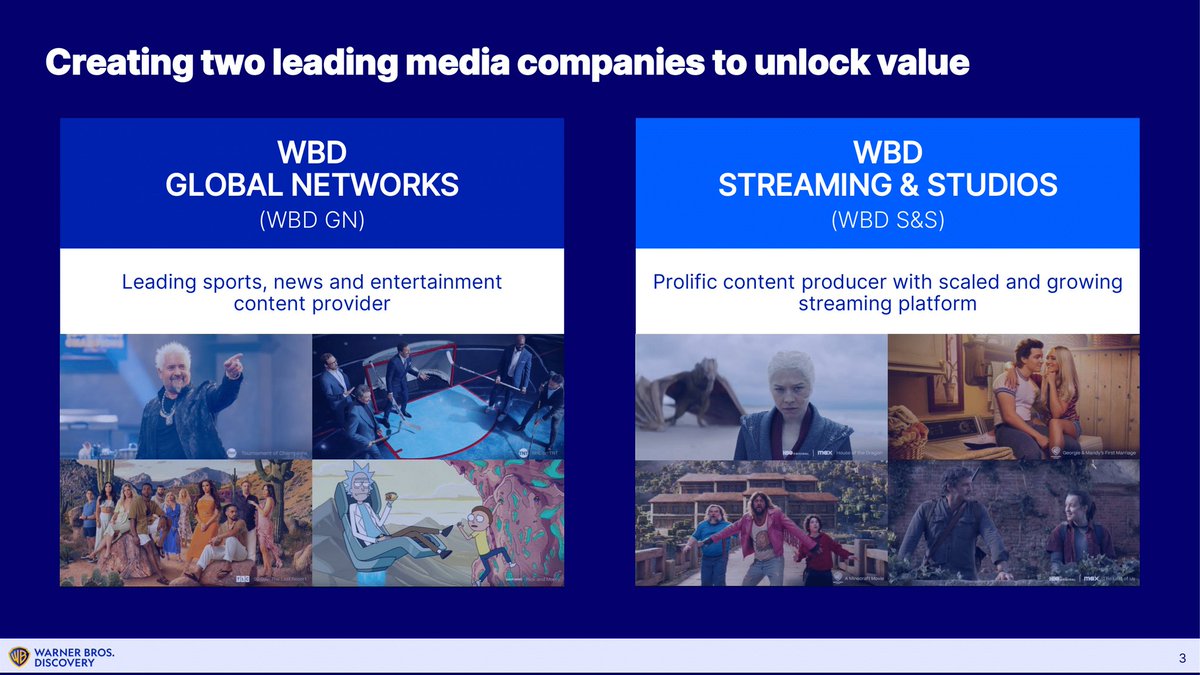

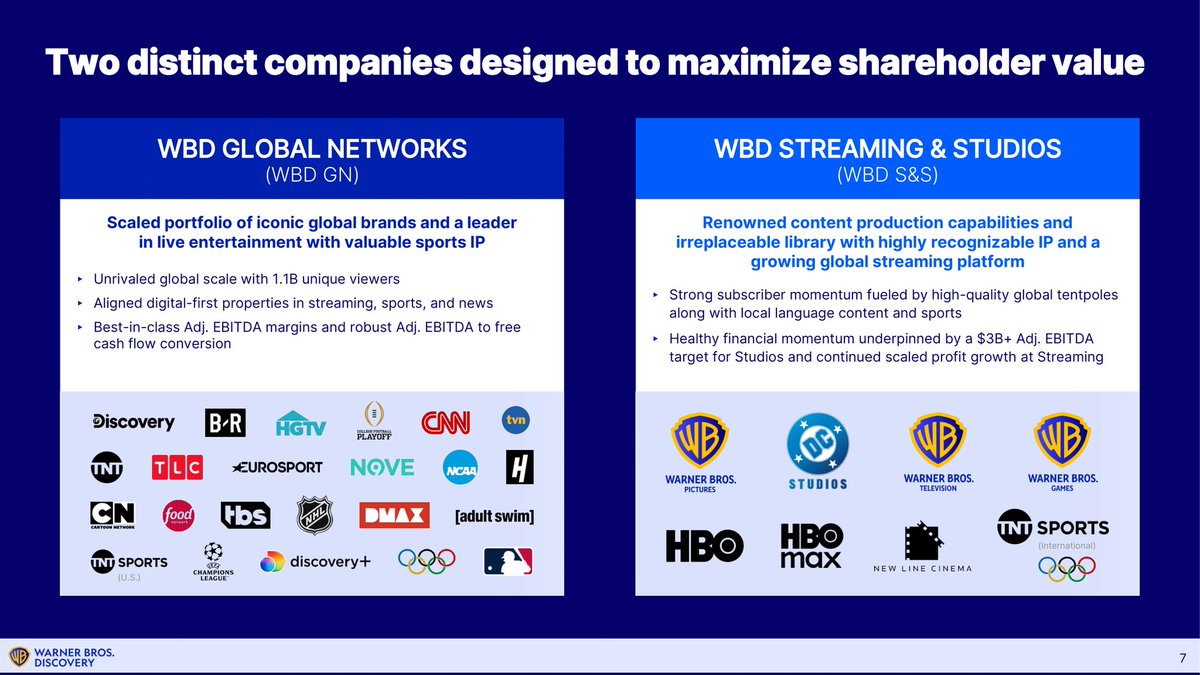

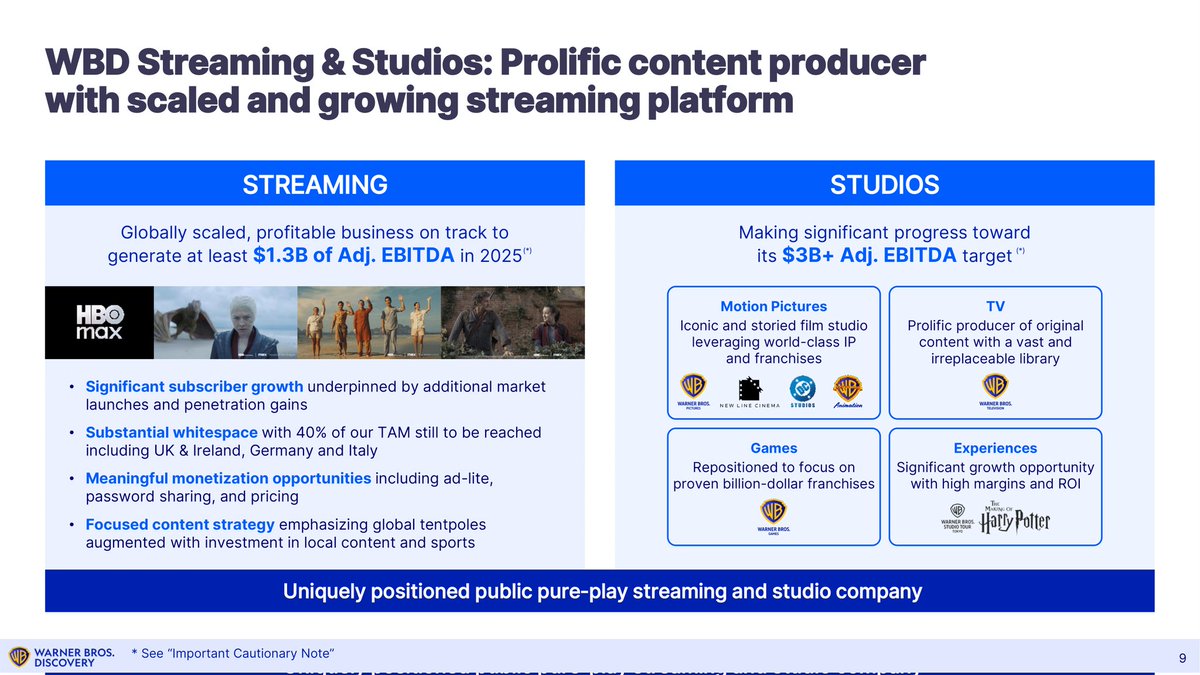

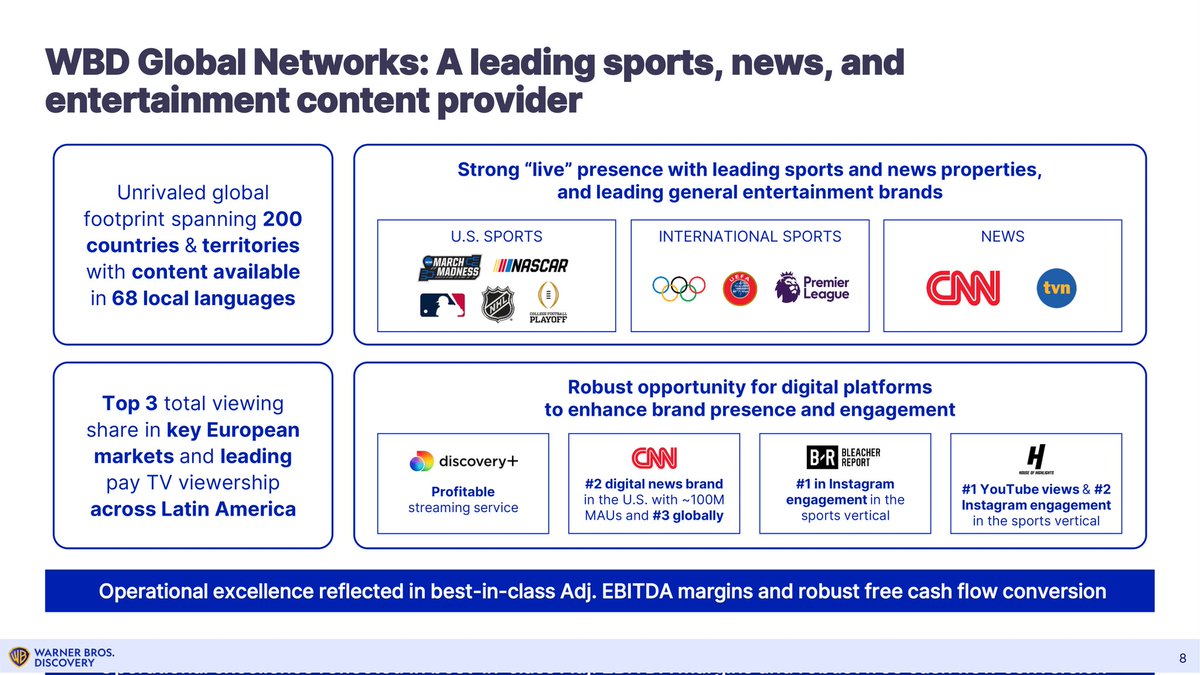

Analysis of the Warner Bros. Discovery Split and how it could operate: WBD Global Networks (GN) and WBD Streaming & Studios (S&S):

The split was announced on Monday this week but I have now had time to digest what all of these could possibly mean.

1. The company split allows the Streaming and Studios to offload debt, which means it will be easier for this company to get future financing for large motion picture and television projects and no longer have the obligation of servicing existing debt.

2. The debt is then offloaded to the Global Networks side, this side has a mixture of poor and average performing assets but with some diamonds in the rough, and some networks can do better and survive if their schedules were more concentrated.

3. Because of the obligation of taking up the debt and for having a 20% stake in WBD Streaming & Studios, it's certain that WBD Global Networks will be granted a licensing agreement to use IP and programming from the Streaming & Studios side, it is already said that 25% of what is on Max at present is on the networks. However, this would mean the S&S side would not earn any money from this, so not everything that's new will go to the GN side, as evident by the 25% statistic and new content being licensed to other streamers including Prime Video, and Hulu. This has been the new norm as of late.

4. As WBD Global Networks is already lumbered with debt and weak assets, they can take advantage of a dividend payment from the S&S business.

5. The High Quality productions, including theatrical and HBO, will remain at the Streaming and Studios side, apart from the dividends from the 20% stake GN won't take advantage of this.

6. It is likely that when the debt is managed and gradually reduced, GN will merge back into S&S in years to come, some channels and brands would close down, but it is highly likely that the main channel brands will remain. At the moment the S&S side has identified HBO channels that will be closed down, although there are less channels in this business they're preparing for the formal split, by nature this business will be focusing on streaming. There are precious assets such as news and sports, due to the nature of this form of media, they're always going to be live and linear

7. The very nature of broadcasting is changing, with cable and satellite dying, and IP distribution becoming a much cheaper and accessible form of distribution, this can be in the form of FAST channels or pay channels on vMVPDs (Multichannel Video Programming Distributors) such as Hulu, YouTube TV, or Sling. The advancement in technology is a necessity and a lifeline for linear broadcasting, as it has a lot of financial overheads and requires the use of very specialist equipment and services such as satellite uplinking.

In Conclusion:

Apart from some channel closures, there won't be much changes, due to the different obligations of both sides to help each other out, they effectively reciprocate and work together as if it's one company, with the eventual end goal of a remerger, which is self-evident by the use of some of the same brands by both split companies. Viacom and CBS went through a similar process in 2006 but later remerged. In fact, WBD has already been rehearsing the split since December 2024 and was likely doing preparation work even before then, a full formal split will happen sometime in the middle of next year (2026).

6

20

70

4,135

ASST/BTC has been up nearly 900% since announcement of it becoming a BTC treasury company and remerger with @StriveFunds.

8 May 2025

1/ @StriveFunds just launched the first publicly traded asset manager #Bitcoin treasury company.

But this isn’t a passive allocation—Strive is using Bitcoin to rewire how capital is raised, deployed, and measured.

Let's break it down: 🧵👇

4

598

4 Feb 2025

How they handled ECMAScript Modules was an absolute shitshow. People got so fucking burnt out dealing with the bullshit and the team kept pushing back refusing to accept the pleading for years, Bun comes out and goes "We can just support both in the same system" and now you don't have to throw the baby out with the bath water and now only because Node is losing mindshare from Bun do they actually care to start listening to people.

We're just witnessing IO.js fracturing all over again, but this time instead of the team fracturing and forcing their hand in hopes of a remerger, it's a VC baked company who has no interest in merging into main.

18

560

16 Jan 2025

I watched this interview. It was refreshing to see Jammu and Kashmir CM Omar Abdullah speak so vividly about various topics.

(Except when asked about PoK remerger with India)

16 Jan 2025

Coming tonight to a screen near you. Yeh toh sirf trailer hain 😄

1

5

9

5,798

8 Jan 2025

Wait in 5-6 yrs same ppl will ask for remerger. Hubli has popln of almost 1M which will be focused for Centre Govt schemes in future.

1

3

72

11 Dec 2024

They had to abandon Joy Bangla, as I believe,vthey will soon rejoin Pakistan and share their slogan "Pakistan Zindabad".

Pakistan is starving. After the remerger of the two countries, whatever is left in Bangladesh will be sucked dry by West Pakistan, just as they were doing before 1971.

Only then can they share the nuclear arsenal of Pakistan. India must intervene if any such remerger attempt is anticipated.

2

18

6,730

4 Dec 2024

@RahulGandhi Sir no voice in loksabha from the Congress party about stop privatisation,revival of Vizag Steel and remerger in SAIL. Vizag steel foundation stone laid by your grandmother smt Indira Gandhi.visakha ikku aandhrula hakku.save Vizag steel

3

68