Jun 13

NYAD AD/DC showing divergence vs SPX. (Similarities)

If the NYAD breaks below it's own 200 day moving average before the SPX does, then it is the beginning of a correction or something significant

13

Jun 12

Not sure why so many stock market focused account expend so much energy on things that have zero impact on the stock market.

13

Germany technical recession ke kareeb, energy prices ke high hone se Europe ki badi economy slow ho rahi hai. #GermanyEconomy #RecessionAlert

11

Germany edges closer to a technical recession as rising energy costs stall Europe’s largest economy. #GermanyEconomy #RecessionAlert

4

Paper delivery is US. Decoupling is misleading. Tanker dark pools like $BWET are selling premium capacity: they capture arbitrage from physical prices higher than local US via manipulation of carry costs

35

Conde de Contar retweeted

Jun 10

No argument that the doom takes are overstated and the tape deserves respect.

Two issues with "the smart money isn't buying," though. It's circular, since you're reading positioning off price direction and every sell is someone else's buy. And the price you're reading is the paper market, which has decoupled from physical this whole episode, refiners paid $30-40 premiums to landed barrels while futures stayed subdued. So the futures tape isn't even a clean read on the molecules, let alone on who's informed.

The driver isn't mysterious either: the Hormuz war-premium is unwinding on reopening signals. Plausibly lower from here, but that's a headline-binary, not a verdict. Worth watching whether physical converges down with paper or stays bid.

Jun 10

I am reading so much doom and gloom about oil inventories running out in 10 days and this is generational buy opportunity.

To which my question is this . This most sophisticated funds, managers , traders with access to the most expensive data in the world are not buying the market . Why ???????

Because very clearly the data does not warrant it. There are a few possible reasons why oil keeps sinking ;

1. A deal is incoming that opens the straight

2. Demand destruction

3. Shipping is exiting straight dark

4. Oil supply ramping up to fill supply gap

All or some of the above may or may not be true . What is 100% true is the smartest most informed are not buying it . That is all that matters. Don’t overthink the why . And please don’t repost the doomed tweets because they clearly are bait and not factual .

Until the smart ones stop selling and start buying , it’s best to read between the lines rather then imposing your beliefs on market . It will turn out to be a lot cheaper

3

1

4

2,250

Jun 10

Physical premiums have been collapsing for past 3 weeks. Spreads also narrowing

1

890

Pio Chun retweeted

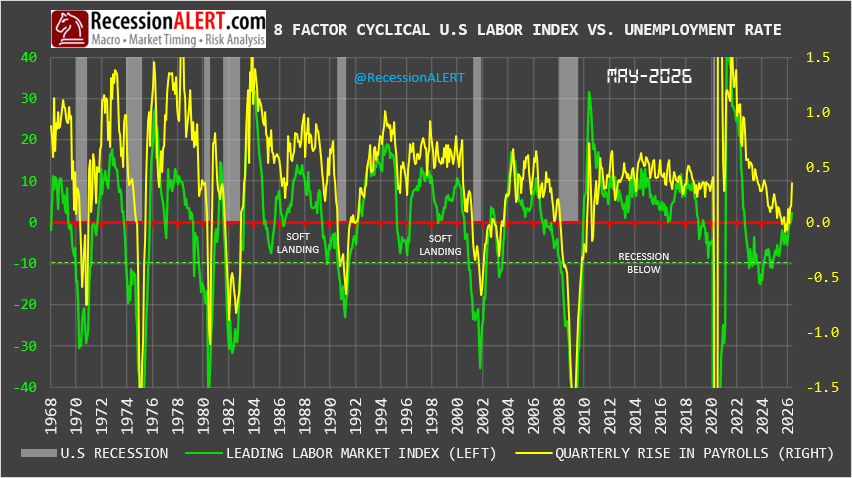

Recoveries don't announce themselves on the front page — they start in the plumbing, and the plumbing here is factory hours. The 8-factor cyclical labor index bottomed at -8.18 in May 2025 — an excursion that, in every prior modern cycle (1970-2020), sat inside a recession bar. This one did not. Instead it has climbed from December's -5.50 to 2.19 across five accelerating months, implied recession probability has collapsed from the mid-60s to 0.00%, and headline unemployment is pinned at 4.3%. Factories find a floor, hours extend before headcount, overtime absorbs the next marginal shift, openings rise, hiring follows — and the index captures that sequence eight months ahead of coincident payrolls, corroborated by ISM Manufacturing 54.0, JOLTS openings 7.6M, and May NFP 172k. Just 3 of 8 components have turned positive yet — the lead is narrow — but a soft landing confirmed at the leading edge is a different rate path, a different risk regime, and a different bill for anyone still positioned for the recession that never came.

2

5

16

1,683

Jun 9

The overlapping graphs are, as usual, opaque,

but the accompanying text is clear, boding well

for the future of the economy; 'laissez-faire' for

sure, literally, 'let them all work'.

27

ZANDI'S $5 GAS BOMB: RECESSION IN WEEKS UNLESS THE STRAIT OF HORMUZ IS REOPENED IMMEDIATELY

Mark Zandi, Moody’s Analytics Chief Economist, just dropped a bombshell assessment of where the economy stands right now. He says the next few days or weeks will decide everything as oil inventories dwindle and prices threaten to surge past the tipping point. With gas already near four dollars and fifty cents the margin for error has all but vanished and the most vulnerable households are running out of room.

THE WINDOW IS CLOSING FAST

➡️ Zandi says a resolution would be nice today but realistically it must come in the next few days

➡️ If it goes on much longer inventories will keep drawing down and the strategic petroleum reserve will start to fade.

➡️ Without the strait opening or more production soon oil prices are going to jump again.

➡️ That jump to five dollars a gallon would be enough to push the tenuous economy straight into recession.

THE DANGER MATH FROM SIMULATIONS

➡️ Zandi's models show it takes about one hundred twenty five dollars a barrel sustained for two or three months to reliably trigger a recession.

➡️ Today oil is closer to ninety or ninety five dollars but we are uncomfortably close to the line.

➡️ Five dollars at the pump lines up with that one twenty five a barrel threshold if the arithmetic holds.

THE CONSUMER FALLOUT

➡️ The thing Zandi worries about most is lower middle income households already under a lot of pressure.

➡️ Real disposable income after inflation and taxes is actually falling on a year over year basis right now.

➡️ If gas goes over five dollars and real incomes keep declining consumers are going to pack it in and stop spending.

THE NO RESCUE SCENARIO

➡️ Zandi does not see fiscal policymakers getting it together quickly enough to help.

➡️ The Federal Reserve will not come to the rescue either because inflation expectations are rising.

➡️ The Fed would rather get inflation under control even if it means a recession now to avoid a worse one later.

➡️ Zandi says "take our lumps up front" is the approach because there is really no good choice here.

➡️ Even a new Fed chair would not change the outcome as the committee stays focused on inflation over growth.

THE BOTTOM LINE

Mark Zandi's message is unmistakable: the economy is perched on the edge with almost no time left and absolutely no policy cavalry on the way if oil prices break higher.

The warning could not be any clearer or more urgent.

#ZandiWarning #OilPrices #RecessionAlert #FedPolicy #GasAtFive #ConsumerCrisis #NoRescueComing

9

15

89

10,209

May 27

2

208

Today 05/06/2026 ,AI is still useless in 99% of my daily tasks .

Worst , it is full of errors

I didn't trust it anymore

5

542

Apr 28

It's not a savings account it's a $25B credit card.

Yes, that would worry me very much, especially since the wayward brother would be borrowing even more money from you.

"Don't worry bro, this time it's going to make a ton of money, I swear! I won't lose it all this time!"

2

21