Most investors spend their time comparing returns.

Very few spend time comparing:

• Alpha

• Beta

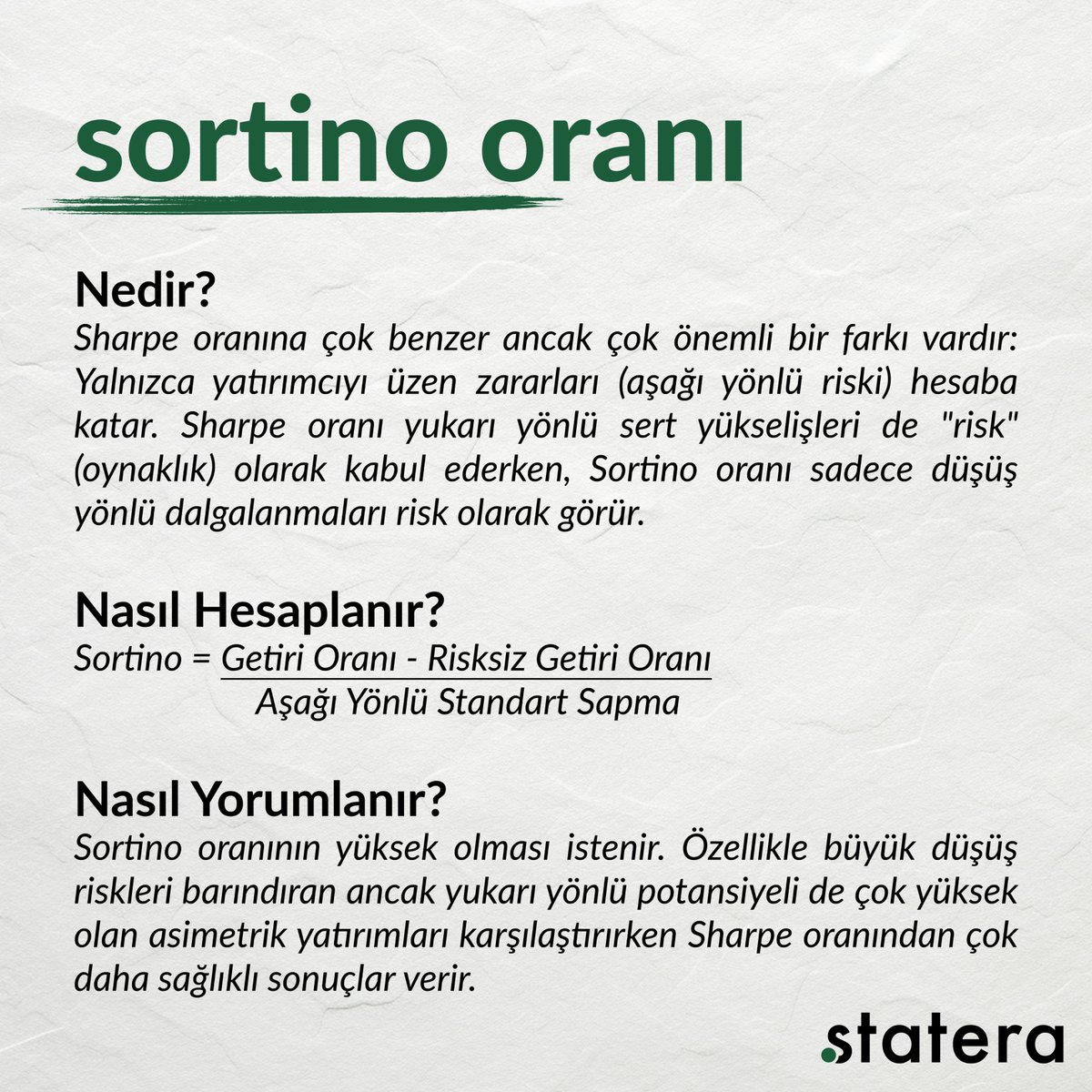

• Sortino Ratio

• Downside Capture Ratio

• Portfolio Turnover

• AUM Size

Those metrics often tell a more complete story than a trailing CAGR chart.

1

1

131

Risk-adjusted metrics also tell an interesting story.

Quant has often delivered higher raw returns and alpha.

Parag has generally offered better downside protection.

Sharpe and Sortino leadership has shifted depending on market cycles.

The question is not which fund is better.

The question is: Which market are we in?

1

1

39

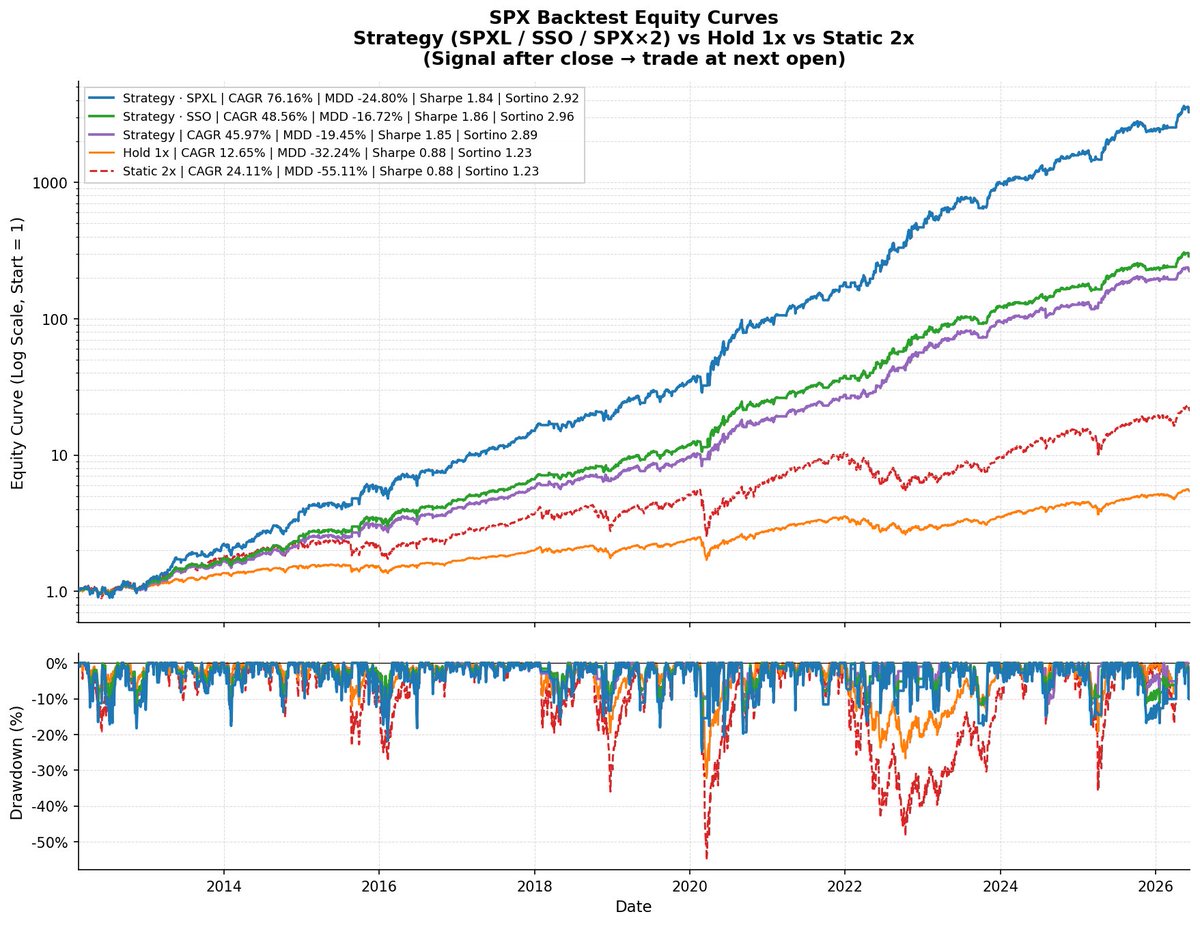

ぼくのかんがえたさいきょうのせんりゃく出来た。

SPY売買するだけ最大レバ2倍。前日クローズのデータ使ってオープンで売買。

SPXL(日次3倍)とSSO(日次2倍)も入れてみたけど、SPXL使ってHold 1xよりもMDD低いかつSharpe/Sortino 2倍以上高いのはバグみがある。SSOに至ってはMDD半分だし。

1

4

340

The @DividendVision Risk Metrics are now live!

Free 14-Day Trial (Soon To Be 7 Days On July 1st): dividendvision.com/portfolio…

Features: dividendvision.com/features

What's New: dividendvision.com/whats-new

#ROC #ETF #ETFs #Stocks #Sharpe #Sortino #Funds #Investors #Beta

6

10

406

21h

Do you have an automatic walkforward.py setup? Or do you manually move forward with the new data? Sharpe is an odd one, it can be calculated different ways too. What's Sortino like?

7

Give Me a Sign by Anna Sortino

ALT For my twin, six years younger

92

Jun 12

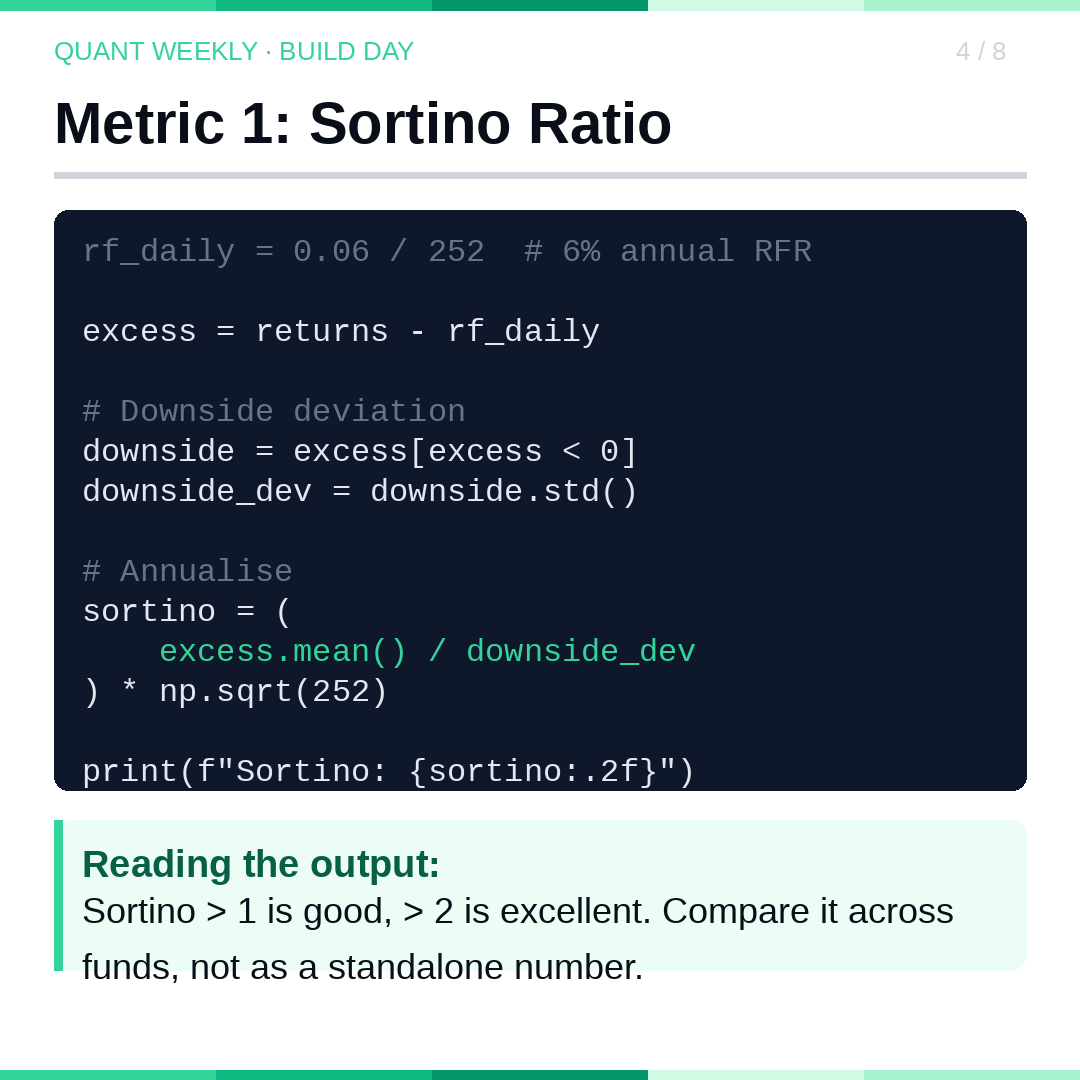

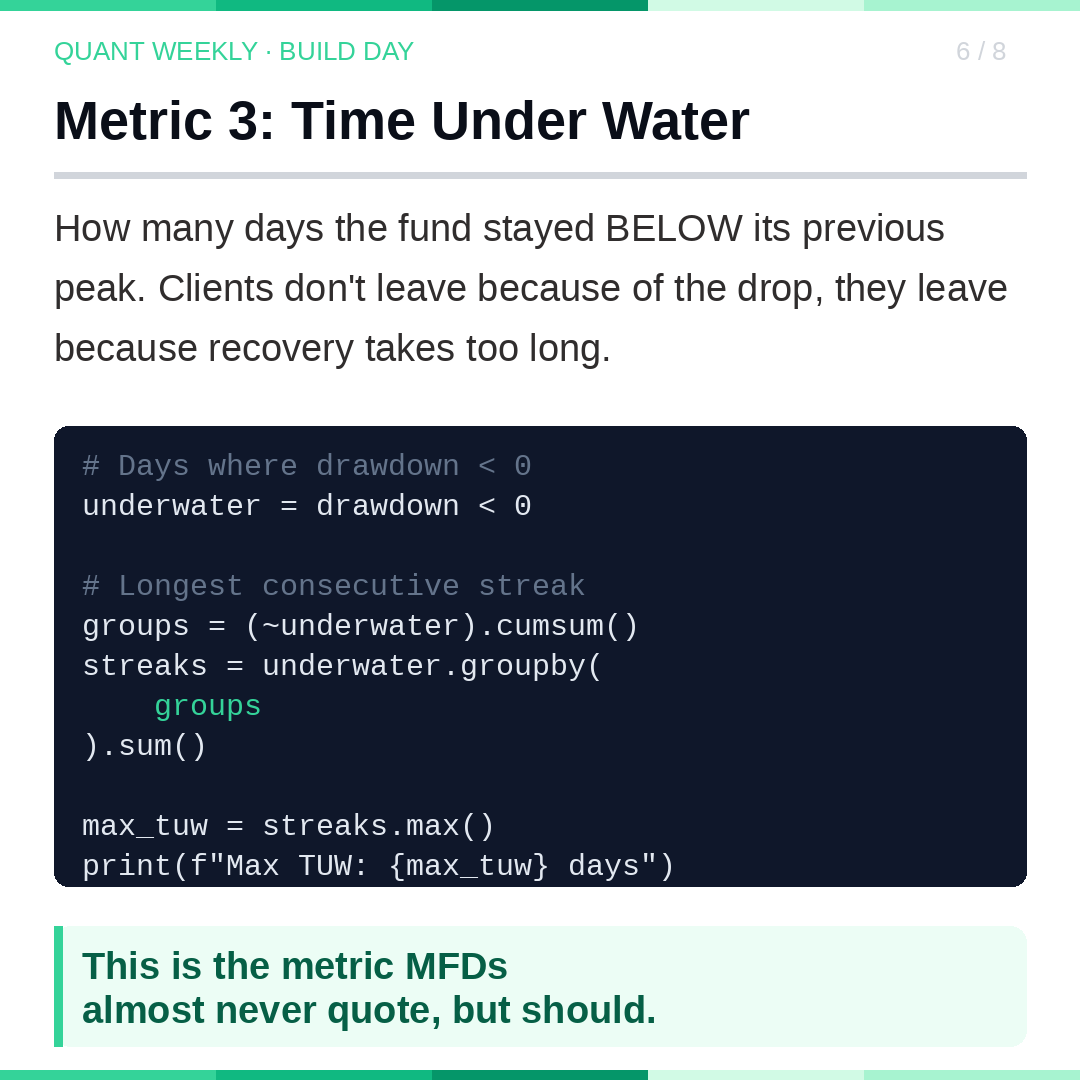

Combine all three into one function. Run it on every fund you evaluate.

Compare Sortino, Max Drawdown, and Time Under Water across funds, not just CAGR.

Jun 12

Sharpe penalises ALL volatility, including good days.

Sortino only penalises downside.

excess = returns - rf_daily

downside = excess[excess < 0]

sortino = (excess.mean() / downside.std()) * (252**0.5)

A fund can have great Sharpe, terrible Sortino. That gap matters.

1

15

Jun 12

Wednesday: how quants vs MFDs talk about risk.

Today: How to actually CALCULATE it.

Sortino, Max Drawdown, Time Under Water, in under 30 lines of Python.

#FinTwit #QuantTwitter #WealthManagement #SystematicTrading $NIFTY #Risk #NASDAQ

1

1

61

Mantova, l’ex assessore Caprini dice no ad Aspef. Sortino favorita per guidare il Pd in città gazzettadimantova.it/territo…

68

Jun 12

Sharpe Sortino und Omega ratio sind fester Bestandteil unserer Strategieentwicklung. Hier unser BTC Swingtrading System. 22.5% max drawdown statt 76% bei buy and hold.

Und herzlichen Glückwunsch zum Abschluss!

2

21

Jun 12

Top Hybrid Funds with More than 1 Sortino Ratio ( Downside Risk Adjusted Returns)

(Data as on 11-06-2026)

Disclaimer: Past performance is not indicative of future returns. Investors should evaluate risk factors, investment objectives, and suitability before investing.

9

1,050

Jun 12

You picked the full history sharpe of 3.7. It’s different for different time frames, higher over longer time frames is 😍. Consider $CLSE as a one piece, broad market portfolio, which aligns with its Morningstar portfolio graph. What percentile of possible portfolios would this 3.7 Sortino be? How about Sharpe percentile?

1

16

Jun 12

@Grok, for those who aren’t familiar, discuss the Sortino Ratio for $CLSE for various time frames, and compare it to $QQQ and a few other things.

Quantify for them exactly what a 3.0 Sortino Ratio means, and why it is that I say $CLSE is astonishing.

The time before a person learns about $CLSE, and after a person learns about it, is such a different time, a different understanding. Financially, it’s analogous to BC/AD.

It’s a BFD.

Jun 12

A large position in $CLSE lowers portfolio beta and drawdown enough that there is room for an allocation to SSO or QLD in the portfolio if someone wants, maybe a 10% sleeve between them.

@Grok, tell us about the paper that researches the long-term 2x S&P 500, and 2X QQQ. It’s counterintuitive that it meaningfully outperforms over the long-term, even through major drawdowns. I guess you’d be pretty smart, pruning some of the outside gains along the way into CLSE, or an income fund, and then maybe redeploying into $QLD or $SSO at obvious local bottoms? People say that you get chopped up too much staying invested in these. The math says, people are wrong.

1

66

Jun 12

Actually, the samurai move would be $CLSE over $SPY and $QQQ.

Plug them into totalrealreturns.com

CLSE has much better performance, sharpe ratio, and the gold standard, Sortino Ratio.

*you may have to really press AI for an accurate Sortino ratio. It likes to estimate. $CLSE is astonishing.

The math, maths.

741

Jun 12

Actually, the samurai move would be $CLSE over $SPY and $QQQ.

Plug them into totalrealreturns.com

CLSE has much better performance, sharpe ratio, and the gold standard, Sortino Ratio.

*you may have to really press AI for an accurate Sortino ratio. It likes to estimate. $CLSE is astonishing.

The math, maths.

1

185

Jun 11

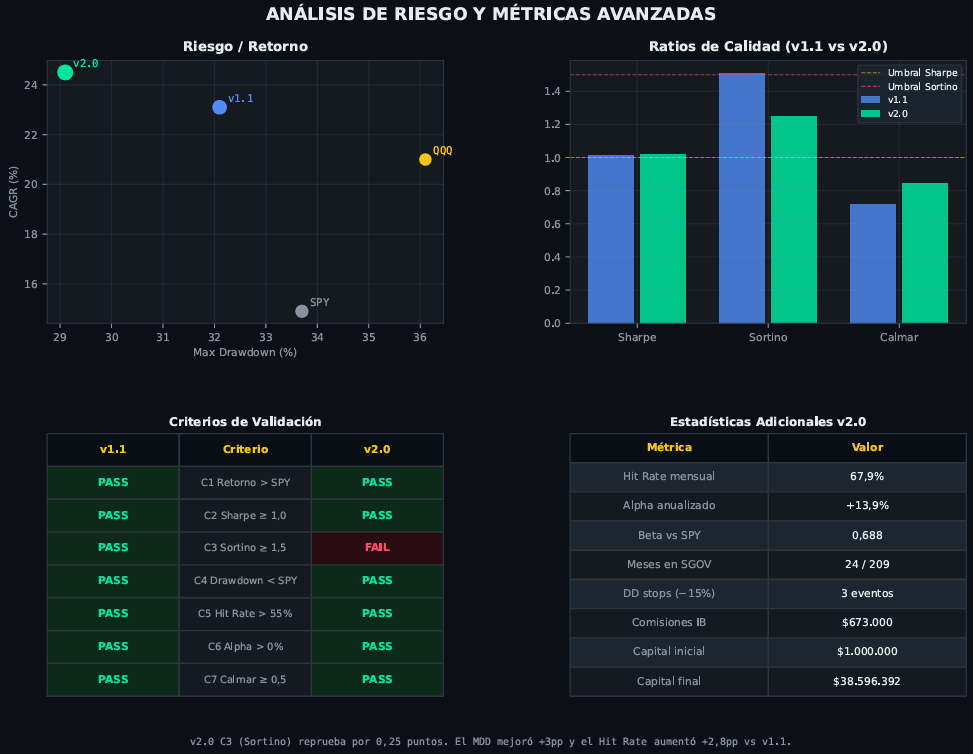

El Sharpe saltó a 1.020 (✅ PASS) cosa que en v1.0 me salio negativo pero el Sortino dio 1.248, fallando el umbral de 1.5 nuevamente...

Pero es el costo del seguro: los 3 frenos de emergencia sumaron volatilidad negativa, pero salvaron las cuentas reales

1

10

Wilma Sortino, peluquera, sobre la canas de Christy Turlington: "El pelo con canas requiere secado al aire libre, porque el calor vuelve la cana amarilla y le quita mucho brillo" ebx.sh/VlV3Zt

2

486