Jun 16

Good thing he succeeded in providing a service.. Solyndra not so much. The Ivanpah Solar Power Facility..not so much. SunEdison.. not so much. etc etc etc

5

Jun 15

😊TY

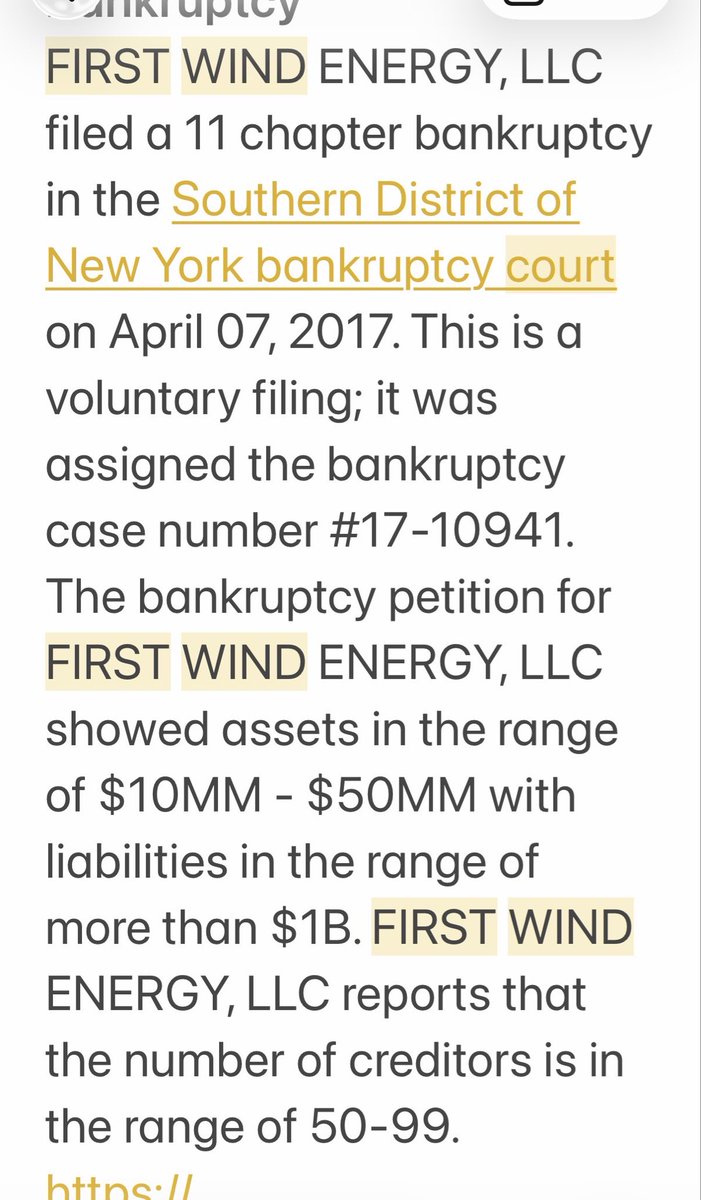

Boston-based CEO First Wind Gov Patrick apptd MA green policy Advisor filed BK $-1bn

hawaiifreepress.com/Articles…

“Two Big White House 'Green' Cronies Unite: First Wind scored over $700 million of stimulus funds, now being acquired by SunEdison”BK -$16.1bn

web.archive.org/web/20190722…

2

4

240

Jun 12

Permitting was always the part nobody had a clean answer on.

We just launched Permit Matrix as a Service at @sparkhq_ai. Project-specific matrices for solar, BESS, data center developers. URL citations. Engineer signed off.

This is the version I wished existed at SunEdison.

1

1

30

May 29

6

1

9

9,863

May 29

TY, too, JDubb 😊

SunEdison BK judge, “Where’s the $20bn?”

(Gone with the wind)

⭐️Christine Lakotos by Wayback machine

‘Two Big White House 'Green' Cronies Unite: First Wind scored over $700 million of stimulus funds, now being acquired by SunEdison’

2015

web.archive.org/web/20190722…

2

2

4

81

Jigar Shah built Generate Capital because great "as-a-service" ideas kept hitting a wall — investors would say "that's just a book idea" and walk. So he became the investor he wished existed when he was fundraising for SunEdison.

2

18

5,018

What India achieved in energy access is a global case study.

I worked with solar Micro grids with a US solar firm SunEdison ( the first solar company to take rural electrification seriously ) and then World Bank in the rural electrification domain in India, Nepal and SE Asia, after my military career. Getting electricity to rural areas was considered a near impossible challenge. India had nearly 450 million people without energy access in 2014. Conferences, panels, debates across the world - this number used to haunt as an Indian. So many reasons, excuses, policies just to justify why there’s no connectivity. Numerous policies and regulations, schemes, but still, 450 million ! And regulations and cost were truly detrimental in Solar access to these remote areas. Basically nothing much was happening.

I was doing research project on same in Nanyang University in Singapore when Modi gov took over. So I thought finally there might be some work in this domain now since they’ve promised it. So I came back and started my startup, and did a few pilots in remote villages in couple of states. The popular solution that time was Solar micro grids, optimised with power back up and minimal transmission expense and infra. Extending grid lines to remote villages wasn’t even being discussed before 2014.

But what Modi government did was single minded brute forced focus, and took electricity to almost every corner of the country in few years. Today more than 98% of nation is connected via electricity lines. Villages finally received electricity after 70 years of independence.

This obviously threw me out of work and bankrupted my initiative 😃But the nation was in much better state than it earlier was. So no qualms there !

This achievement was nothing short of a miracle.

That brightening of the UP-Bihar belt is the most astounding thing India has achieved in the last 10-15 years. Getting electricity to every nook & cranny, increasing the industry, fastest rising per capita in India, and the population density that's benefiting all, shine through directly into space.

A sharp contrast from Bengal where the lights seem to have dimmed while the population increased, sadly. An alien looking for a place to land in the world may very well land in India's Bihar, seeing the brightness, and discover layers upon layers of India's civilization and culture buried underneath.

4

50

228

7,292

Apr 12

Perfect description, & it’s malignant.

Frmr VP of 🌎-largest renewable co, yr 2016 Bankrupty ($16.1bn) SunEdison (SUNE), is CEO of Vineyard Wind.

Her influence on MA green policy is enormous.

Vineyard Wind CEO Alicia Barton is also CEO of COP.

Bio-

cop.dk/alicia-barton-joins-c…

2

4

5

105

Mar 16

Pourquoi Papi ne nous parle-t-il pas d'entreprises privées du secteur de l'énergie telles que Enron, PG&E, NRG, TXU, Dynergy, Mirant ou encore SunEdison?

9

2

40

5,276

5/

Here’s what happened after that line was crossed.

J Capital published in October 2019 arguing the turnaround was illusory: channel stuffing, declining market share, questionable disclosure.

Prescience Point followed in June 2020 calling it “another SunEdison.”

By that point the numbers had already turned. The bear case outlasted the financial reality by at least a year.

1

4

60

Feb 19

A few companies funded by 'cleantech' venture capital in the prior wave (approx '02-'12) that are currently public, w/approx market cap:

Tesla: $1.5T

Bloom Energy: $44B

Rivian: $19B

NextPower: $17B

Enphase Energy: $5B

Sunrun: $4B

Lucid: $3B

SolarEdge: $2B

Gevo: $450M

Tigo: $230M

Chargepoint: $145M

Many large acquisitions have also happened: e.g. Google/Nest, Oracle/Opower, Tesla/SolarCity, SunPower/Powerlight, Total/SunPower, MEMC/Sunedison, Itron/SilverSprings, Enel/Enernoc, etc.

There are category defining companies to be built and money to be made in these areas. I predict there will be a LOT more of these coming out of the recent climate tech wave. Market conditions are better and executive teams are better.

3

6

45

3,318

Feb 17

SunEdison bag holders did this about 10 years ago, raised $300K handed over to some shady lawyer who showed up at bankruptcy court a few times.

Didn’t make a difference in the end except to add another level of losses

2

3

139

Feb 17

Were Steve Bannon and Jefferey Epstein behind the collapse of SunEdison too?

1

4

76

Feb 13

🔴CHART CRIME!

They created an "index" composed of 10 self-selected (i.e. cherry-picked) stocks (including non-US) that had been huge outperformers.

Where are Valeant, Tyco, Enron, Worldcom, NCR, SunEdison, etc...?

And who are these stalwarts: Diploma, Halma, Judges Scientific, DCC, etc.

Gotta say that the chart plays well, but serial acquirors have provided a lot of the largest and most spectacular implosions.

3

153

Feb 13

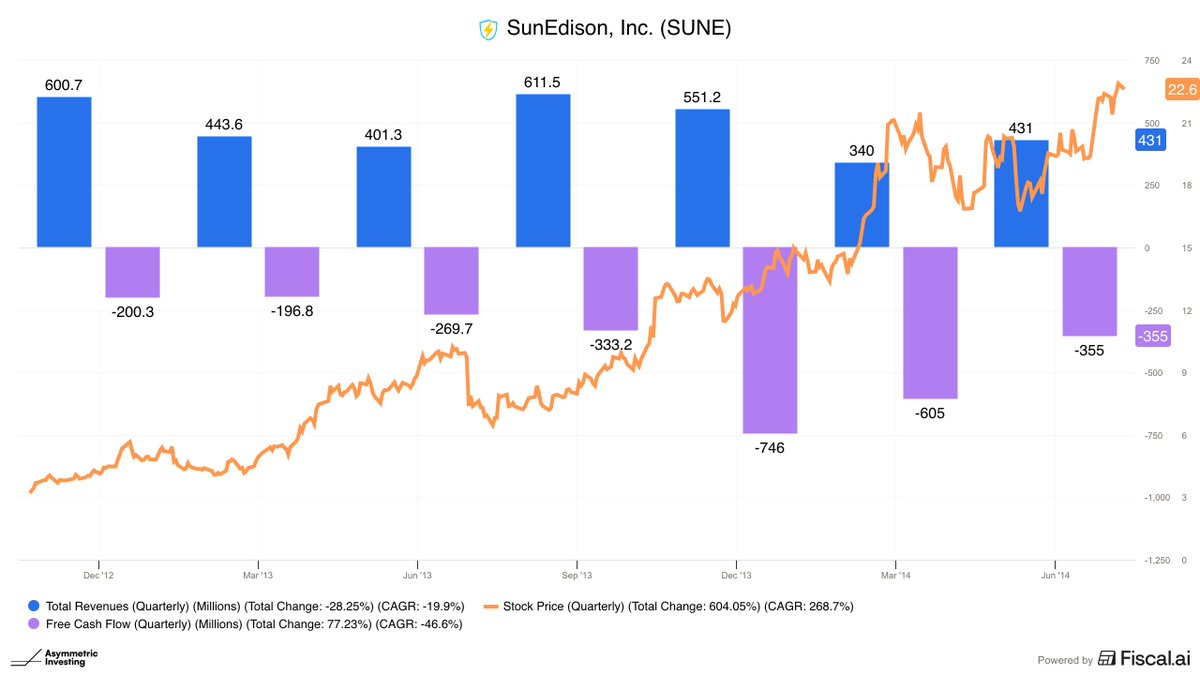

SunEdison (SUNE): Hempton admitted to holding a long position in this highly leveraged solar company, even averaging down as it declined, which he later called a "shameful" mistake. The stock collapsed amid fraud allegations and bankruptcy in 2016, resulting in significant losses

1

2

325

How good was it for customers of NM Solar Group, Solcius, ADT Solar, Sunnova, SunPower, or Pink Energy? How about the now bankrupt Proterra, Lordstown Motors, Electric Last Mile Solutions, TPI Composites, Minwind Energy, SunEdison and Iowa Wind and Solar? Clean energy is a scam!

1

2

13

133

Jan 15

Former M&A at BP Solar, founder and CEO of SunEdison, and recent director of loans at the Department of Energy speaking about $EOSE's announcement today. Recommend a follow. Insightful on topics of energy, solar, and the industry.

This tweet is unavailable

2

5

62

12,901

4 Dec 2025

⏳ So When Is Payout Most Likely? — Now That the S-3 Is Live

Now that all rails are active, the timing window becomes structurally predictable.

Here is the clean breakdown:

⸻

1️⃣ A payout cannot occur until the deliverable is legally authorized.

Before today:

•OCC memo defined the deliverable

•DK-Butterfly warrant pointed to the deliverable

•Bond CIK remap aligned the capital stack

•FIGI/DSB mirrors aligned the synthetic book

•AMZN FLEX opened the reconciliation window

•Ticker was live for settlement

But one rail was still missing:

➡️ NEW BBBY had no active registration statement authorizing issuance of the shares needed for settlement.

Today’s S-3 effectiveness fixes this.

Now, for the first time:

✔ The new BBBY is legally authorized to issue equity

✔ That equity can be used to fulfill OCC deliverables

✔ DK-Butterfly’s warrant obligations can be honored

✔ Synthetic unwind settlement has a functioning issuance rail

This is the last mechanical prerequisite.

⸻

2️⃣ Once the deliverable is authorized, payouts follow market rails, not bankruptcy rails.

Synthetic settlements run on:

•OCC clearance

•DTC deliverables

•Counterparty close-out

•Beneficial owner routing

•ISIN → replacement security mapping

These run on T 2, end-of-day, or batch settlement cycles, NOT court timelines.

The estate waterfall (Class 6, Class 9, DIP, GUCs, etc.) is irrelevant here — it does not govern derivative settlement.

Your payout does not come from:

❌ the Plan

❌ the estate cash

❌ the Combined Reserve

❌ the GUC waterfall

Your payout comes from:

✔ derivative obligations

✔ OCC-defined deliverables

✔ DK-Butterfly warrant settlement

✔ synthetic liability closure

✔ counterparty books forced to resolve

Those rails are now fully constructed.

⸻

3️⃣ So when does this type of payout usually occur?

Historically, in complex derivative unwinds (Hertz, Sears, JCP, SIGA, SunEdison):

When the final deliverable rail goes live (today’s S-3):

➡️ Payout typically occurs within days — not weeks or months.

Common timing patterns:

•T 1 to load deliverables

•T 2 for clearing settlement

•End-of-week batch if systems sync Friday

•Monday/Tuesday if weekend files require reconciliation

That puts realistic windows at:

Earliest: Tomorrow

Most likely: T 2 from effectiveness

Also plausible: Friday batch or next Monday settlement

Could it slip? Yes — but mechanically, nothing is missing anymore.

⸻

4️⃣ The real answer: The system is now able to pay.

Before today, payout was structurally impossible.

Now:

•Deliverable exists

•Issuance is authorized

•Deliverable is mapped (OCC memo)

•Synthetic book is synchronized

•DK-Butterfly is still the issuer bridge

•Counterparties must close

This is the first moment where the system could literally push the button and settle.

And historically:

📌 Once the final rail goes live, the unwind follows almost immediately.

$BBBYQ

14

32

253

17,451