Good point. The BTC-equity correlation has definitely weakened compared to previous cycles. If the Fed signals a more accommodative path tomorrow, it could reinforce the narrative that Bitcoin is evolving into a distinct macro asset rather than simply a high-beta risk trade. The dot plot will likely be more important than the rate decision itself.

12

Going into the Fed's first meeting under Warsh, the cross-asset picture is quiet. Kresmion's regime model reads 0.22, squarely Neutral, high conviction, 48 days old.

10-year at 4.48%, high-yield spread 266bps, conditions accommodative. Calm before the dot-plot. $TLT

20

South Africans everywhere are tired of the problem of illegal immigration. All parts of South Africa are demonstrating that enough is enough. South Africa bent backwards, was accommodative, gave rights and did what no other African has ever done. Feel abused and community torn.

10

This USA world cup its pits shem 🤦🏾♂️🤦🏾♂️🤦🏾♂️🤦🏾♂️Americans are not accommodative shem

🚨 BREAKING: Iran player Mohammed Mohebi has been deported back to Iran after his gun celebration vs New Zealand

18

Published 1 day ago.

Invesco 2026 Mid-Year Investment Outlook.

Japan’s economy is expected to have an economic boost in the second half of 2026 and 2027.📈

Despite underlying inflation, the Bank of Japan is likely to MAINTAIN A GRADUAL PACE of monetary tightening.💯

Translation:

Japan is not under pressure.🔻

There will not be an emergency meeting.🔻

A landmark fiscal package introduced by Japan’s prime minister, coupled with pressure to maintain a steady, accommodative fiscal policy, will stabilize the Japanese economy.✅

This is documented.📝👇

.25% hike by the BOJ and no significant reaction from the market.✅

Accurate prediction.

No moved goal posts.

Meanwhile, the retail consensus was that aggressive and rapid rate hikes would lead to a significant crash.

This is not another example of “kicking the can down the road.”💯

That is just another recycled phrase when a prediction is missed.🎯

If there was an emergency in Japan, it wouldn’t be delayed.

An emergency is a situation that demands immediate action because delay risks irreversible harm.🔒

Japan is not experiencing panic because oil prices have decreased and the Iran war has become less severe compared to earlier this year.☝️

5

22

166

7,984

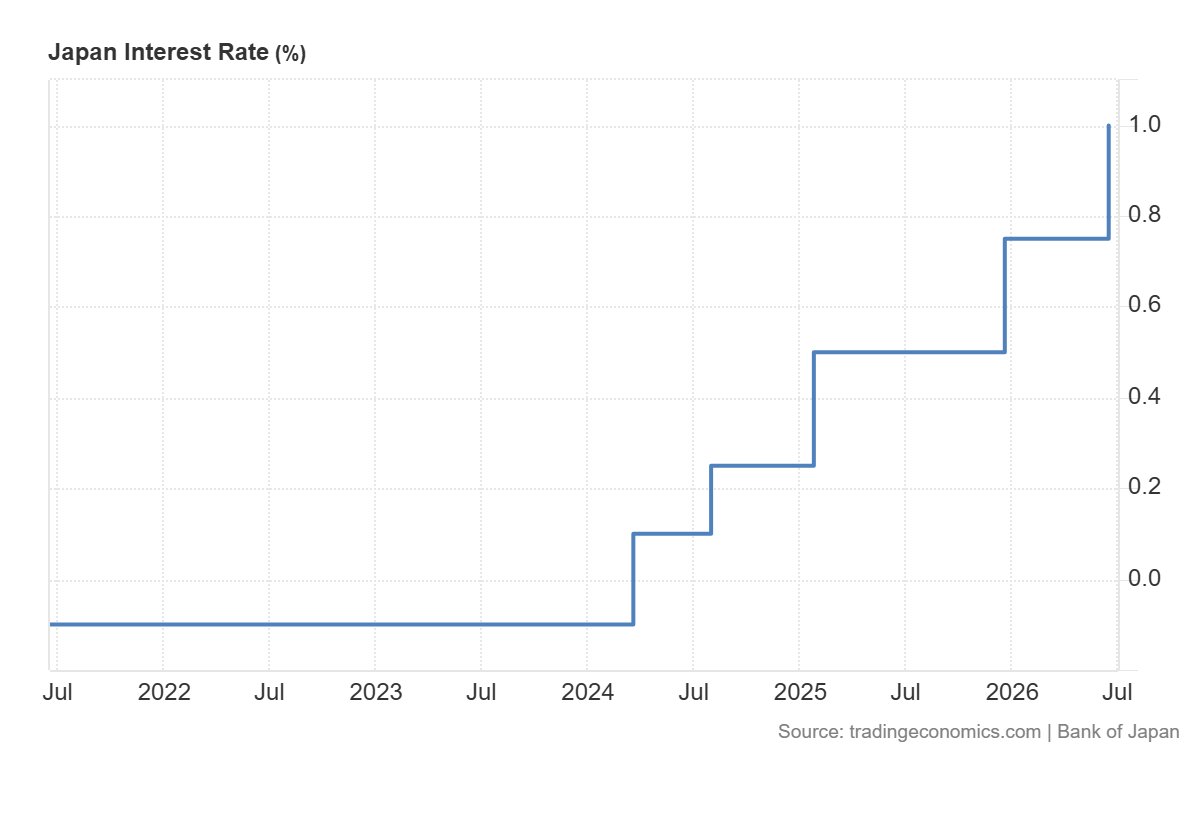

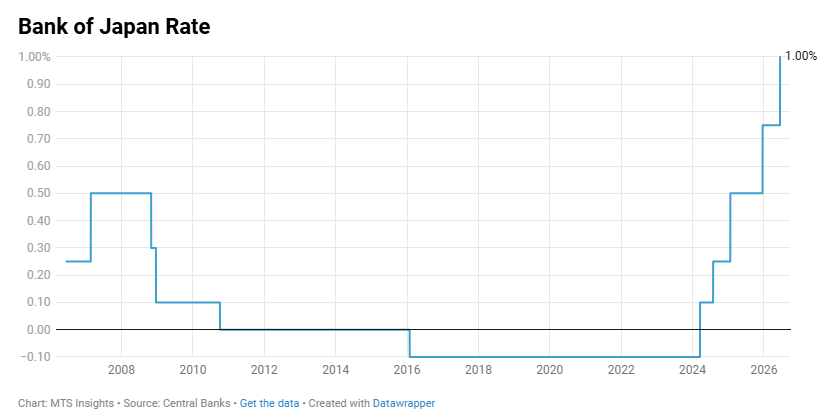

📊 The Bank of Japan raised its key short-term interest rate by 25 basis points to 1.0% in a 7-1 vote during its June meeting, aligning with market expectations and marking the highest borrowing costs since September 1995. The policy tightening specifically targets secondary inflationary pressures stemming from external energy shocks linked to the ongoing Middle East conflict.

📈 While the board noted that underlying inflation could temporarily accelerate above the 2% target due to these rising energy inputs, financial conditions are projected to remain structurally accommodative to support baseline economic activity. Notably, this meeting represents the central bank's first rate hike since December and proceeded without the governor in attendance, while board member Asada Toichiro dissented due to perceived downside risks to production and employment.

❓ Considering the BoJ's commitment to incremental tightening as warranted by financial developments, how do you expect this 1.0% regime to impact carry trade dynamics and global liquidity flows in the medium term?

#Macroeconomics #BankofJapan #MonetaryPolicy #DataAnalytics

1

41

US Construction Collapses — and the Market Listens

US housing starts fell well below expectations in May: 1.177 million annualized units versus 1.430 million expected, a 15.4% drop for the month. The bulk of the decline comes from the multifamily segment, which collapsed from 529,000 to 284,000 units — nearly halved. Single-family construction held up better, with only a slight decline. Building permits remained nearly stable, suggesting that builders’ intentions are still present even as actual activity slows markedly. Completions also fell 8.1% for the month and 14.2% year-over-year.

The gap between the actual figure and the estimate is the signal: -15.4% when the market expected -8.5% is a significant negative surprise. The relative resilience of single-family permits indicates that single-family home builders are not giving up — but multifamily developers are slamming the brakes hard. This segment is more sensitive to high financing rates and restrictive credit conditions. It is a leading indicator of the real transmission of monetary tightening into the economy: high rates are now concretely biting into construction activity.

The immediate reaction is clear: the Nasdaq flips into negative territory in pre-market, the S&P edges modestly lower, and bond yields dip slightly — the 10-year loses 2.7 basis points to 4.441%. This move reflects classic reasoning: weak economic data reduce the probability of further rate hikes and reinforce expectations of a more accommodative Fed down the line. For the real estate and construction sectors, the pressure is direct. For bonds, it provides modest technical support. Tomorrow’s FOMC will absorb these figures into its assessment — they do not force a pivot, but they add weight to the caution camp.

Investors are reading these data through two simultaneous and contradictory lenses. The first: the economy is slowing, which validates the idea that the Fed has tightened enough and can consider cuts. The second: a collapse in construction signals real fragility in demand and credit, which is not good news in itself. The drop in yields suggests that the first lens is currently dominating — buying bonds because you are selling growth. But this reading can reverse quickly if other data confirm a deeper-than-expected slowdown.

Source: US Census Bureau.

21

Then you should have developed your region to be accommodative for all just as other region made theirs for you. Show me one LG in your region occupied by Yoruba, Hausa or Fulani ?

Shameless

1

3

197

I don't know man, I'm seeing too many eager to short it. Thing is if macro is accommodative, SPCX can probably keep going up despite "unreasonable" valuation, like TSLA did. Maybe it won't but I also wouldn't bet against it. Anyhow, no edge for me on SPCX so I won't touch it.

1

15

Japan is a developed, low-inflation economy exiting a long era of near-zero/negative rates and deflationary pressures. A 1% rate remains highly accommodative by global standards and reflects cautious tightening to support growth while addressing emerging risks.

1

16

How could people shift to a demand side issue already? OPEC has been accommodative, the strait is ready to be opened, venezuela oil is added, the US is exporting more than ever before, and alternative routes outside of the strait are being established. This is all supply side

3

506

📝Forward Guidance

•BOJ signals further rate hikes ahead, conditional on economic/price developments

•Will closely monitor Middle East situation’s impact on growth and inflation

•Financial conditions to remain accommodative even after this hike

1

20

Despite the rate hike, financial conditions remain accommodative, with negative real interest rates and favorable financing conditions for businesses. The BOJ signaled it expects to continue adjusting the degree of monetary accommodation over time, suggesting the path of least resistance remains toward further gradual rate increases if economic and inflation trends evolve as expected.

91

🇯🇵 The Bank of Japan raised its policy rate by 25 bps to 1.0%, continuing its gradual normalization cycle as inflation risks build and financial conditions remain highly accommodative.

1

2

136

🔴 ⚠️ BREAKING: BOJ RATE DECISION ACTUAL 1% (FORECAST 1%, PREVIOUS 0.75%) $MACRO

BoJ: will keep raising policy rate amid economic activity, prices, financial conditions developments

BOJ to halt bond taper from April 2027, maintain monthly JGB purchases near 2 trillion yen

BoJ: New guideline for money market operations effective from June 17

BOJ: will assess probability of achieving baseline outlook and associated risks in evaluating timing and speed of policy shift

BoJ: No change in plan to cut monthly JGB purchases by 200 billion yen each quarter through January-March 2027

BoJ's Asada on the Middle East situation: downside risks to output and jobs outweigh upside risks to prices, bank should act

BoJ: to maintain monthly JGB purchases near 2 trillion yen from April 2027

BOJ: accommodative financial conditions expected to persist after policy rate adjustment, continuing to strongly support economic activity

BOJ board members Takata and Tamura oppose outlook description on prices

OJ: bond tapering decision approved by 7-1 vote

BOJ: Japan’s economy has moderately rebounded, though some vulnerabilities remain

BoJ: will end interim evaluation of bond taper strategy

BOJ: risk of major economic slowdown appears to have eased from earlier

BoJ board member Takata: Rate of increase in CPI, including core inflation, has generally reached price stability target

Dollar/Yen little changed after Bank of Japan hikes rates as expected, last at 160.16

BOJ’s Tamura considering underlying CPI inflation already aligned with price stability target

BOJ: Japan’s economy has generally evolved in line with baseline scenario

BOJ: will act swiftly, including boosting JGB purchases and carrying out fixed-rate buy operations if long-term rates climb rapidly

2

6

143

"As for the future conduct of monetary policy, given that underlying CPI inflation has been approaching 2 percent and financial conditions have been accommodative, the Bank will continue to raise the policy interest rate and adjust the degree of monetary accommodation, in response to developments in economic activity and prices as well as financial conditions. In this regard, it will consider the timing and pace of adjustment, while closely monitoring the impact of the future course of the situation in the Middle East on Japan's economic activity and prices and examining the likelihood of realizing the baseline scenario of the outlook for economic activity and prices and the risks to the outlook." @Bank_of_Japan_e

1

5

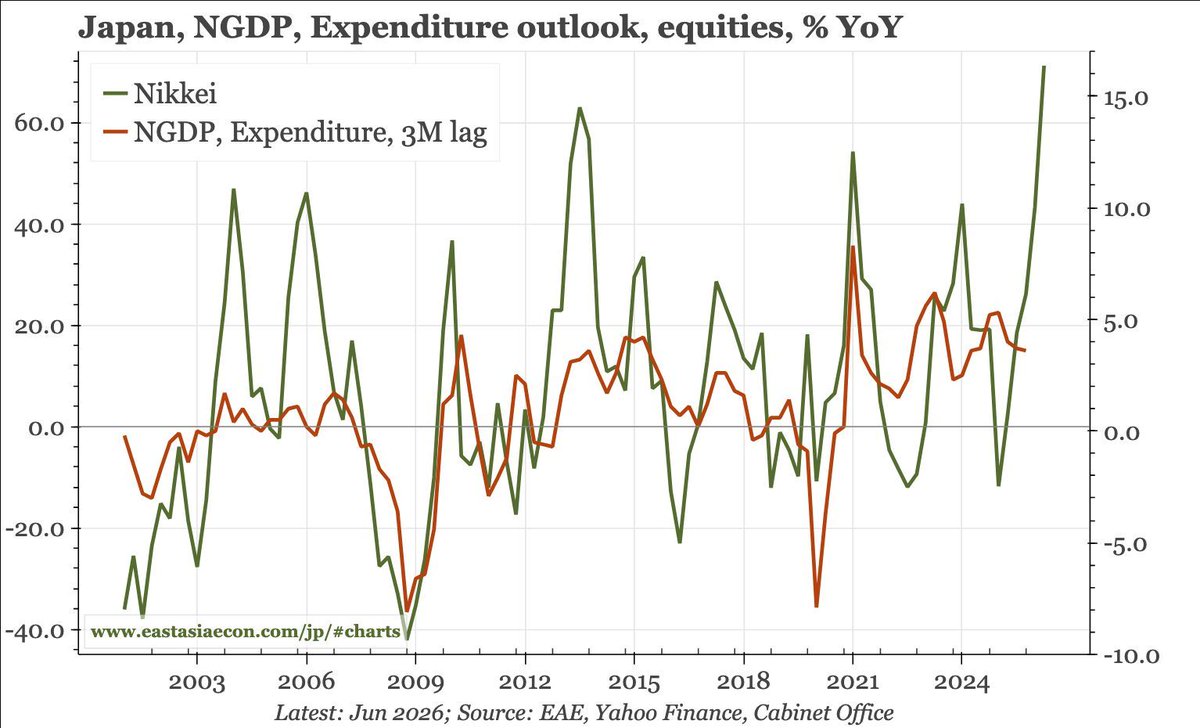

East Asia Today

Another round of bad economic data in China. The BOJ raised rates today, with little reaction in either equities or fx, suggesting with rates at 1% monetary policy still remains very accommodative. In Korea, rather than higher import prices, it is the rise in export prices that is more significant.

eastasiaecon.com/east-asia-t…

1

3

272