MODULAR BLOCKCHAINS ARE THE FUTURE OF 2026 — SCALABILITY REVOLUTION IS HERE AND IT’S MOVING AT LIGHT SPEED!

Modular architecture is no longer theory. Celestia, EigenDA and next-gen modular stacks are delivering insane throughput, custom execution and sovereign security — all while monolithic chains struggle with congestion

Developers and capital are flooding into modular ecosystems. This is the infrastructure layer that will power the next 100x narratives.

Are you already building or farming on modular chains? Drop your favorite modular project or L2 in the comments 👇

#ModularBlockchains #Crypto2026 #Scalability

1

3

9

52

Several projects are leading this modular infrastructure wave.

Worth watching closely.

○ @celestia

One of the pioneers of modular data availability.

Instead of executing transactions, Celestia focuses purely on storing rollup data efficiently.

It already powers ecosystems like

▪︎ Dymension

▪︎ Saga

▪︎ Eclipse

Celestia proved modular DA can work at scale.

○ @eigenlayer

A powerful concept built around restaking ETH for shared security.

EigenLayer allows networks to reuse Ethereum’s security for new services.

Its data layer EigenDA is becoming an important component for rollups.

Billions in restaked capital already secure the ecosystem.

○ @dymensionxyz

Focused on RollApps.

Developers can launch app specific chains quickly using shared infrastructure.

RollApps combine

▪︎ Celestia DA

▪︎ Dymension sequencing

▪︎ modular security

This dramatically lowers the barrier to launching new chains.

○ @alt_layer

A major player in Rollup as a Service.

It allows developers to launch rollups with

▪︎ shared sequencing

▪︎ restaked security

▪︎ modular infrastructure

Many gaming, DeFi, and agent based applications are experimenting with this stack.

○ @astria_org

Focused entirely on shared sequencing networks.

Instead of every rollup running its own sequencer, Astria provides one decentralized sequencing layer.

This enables

▪︎ fair MEV capture

▪︎ cross rollup coordination

▪︎ smoother interoperability

An important piece of the modular puzzle.

The reality is simple.

Modular blockchains are not flashy.

They are not meme coins.

They are not short term hype.

They are infrastructure.

The plumbing that allows everything else to scale.

As rollups multiply and new applications emerge across

▪︎ DeFi

▪︎ AI agents

▪︎ gaming

▪︎ DePIN

the ecosystem will need faster, cheaper, and more interoperable infrastructure.

That is exactly what modular architecture provides.

If this trend continues, the future of crypto may not be one dominant chain.

Instead, it may look like an interconnected network of specialized layers working together.

Execution.

Data.

Sequencing.

Settlement.

All modular.

All composable.

☆ Final question

Which direction in modular infrastructure feels strongest to you right now?

○ @celestia

○ @eigenlayer

○ @dymensionxyz

Curious where conviction is building.

DYOR.

#Crypto #ModularBlockchains #SharedSequencing #2026Narratives

Most people still think DeFi lending means locking up $200 to borrow $100.

That model worked for safety.

But it was never built for the real world.

A quiet shift is happening right now.

On chain credit scoring and undercollateralized lending.

And it might become one of the most important transformations in DeFi. 🚀

For years, DeFi lending relied on over collateralization.

If you wanted a $10,000 loan, you often needed to deposit $15k to $20k in crypto.

Safe for lenders.

But extremely inefficient.

It meant DeFi mostly served traders and whales, not real businesses.

That is starting to change.

Instead of requiring huge collateral deposits, protocols are starting to look at something more powerful.

Your on chain reputation.

Signals like

▪︎ Wallet age

▪︎ Transaction history

▪︎ Repayment history

▪︎ Protocol activity

▪︎ Staking behavior

▪︎ Social attestations

▪︎ Off chain financial data

All of this helps create an on chain credit profile.

Think of it like this.

Your wallet becomes your credit history.

If you have borrowed and repaid before

If you have been active across DeFi

If your wallet shows consistent financial behavior

You can qualify for better loan terms or even undercollateralized loans.

Reputation becomes collateral.

☆ Why this matters

Capital efficiency

Over collateralized lending locks huge amounts of liquidity.

Undercollateralized models can reduce requirements to 110% to 130% or even lower for trusted borrowers.

That unlocks billions in idle capital.

☆ Real world adoption

This is where things get interesting.

Entrepreneurs and businesses in regions like

▪︎ Africa

▪︎ Latin America

▪︎ Southeast Asia

are starting to use DeFi for

▪︎ Working capital

▪︎ Invoice financing

▪︎ Trade finance

▪︎ Supply chain funding

DeFi finally touching the real economy.

☆ Reputation becomes portable

Your on chain history does not have to stay on one platform.

A strong reputation on one protocol could improve borrowing terms on another.

That creates a global crypto credit profile that moves with you.

---

Several projects are leading this movement.

Worth watching closely.

○ @goldfinch_fi

Focuses on lending to real world businesses in emerging markets.

Backers provide first loss capital while lenders earn yield.

Hundreds of millions in loans have already been issued to real businesses.

One of the strongest examples of DeFi funding the real economy.

○ @truefi

One of the pioneers of uncollateralized lending for institutions.

Loans are issued to vetted borrowers with reputation based underwriting.

Features include

▪︎ Senior and junior tranches

▪︎ Insurance mechanisms

▪︎ Dynamic risk pricing

Institutional focused DeFi credit.

---

○ @MapleFinance

Known for its pool delegate model.

Expert underwriters manage lending pools and evaluate borrowers.

Focus areas include

▪︎ Crypto institutions

▪︎ Business lending

▪︎ Structured yield opportunities

○ @credora

Often described as a credit bureau layer for crypto.

It aggregates on chain and off chain financial data to generate portable credit scores used by multiple lending protocols.

Infrastructure for the credit reputation layer of DeFi.

○ @blendprotocol

A hybrid model combining

▪︎ Collateralized lending

▪︎ Reputation based credit

Your credit score can increase the loan to value you qualify for.

A bridge between traditional DeFi lending and the next generation reputation economy.

The reality is simple.

Over collateralized lending was necessary for early DeFi security.

But it also limited its usefulness.

Undercollateralized lending opens the door for

▪︎ Businesses

▪︎ Freelancers

▪︎ Creators

▪︎ Emerging markets

▪︎ Institutions

Not just crypto traders.

If this trend continues to mature, DeFi lending could evolve into something much bigger.

A global permissionless credit system.

Where your reputation and financial behavior determine access to capital.

Not your location.

61

1

54

3,451

11 Dec 2025

Everyone is worried about the next $BTC dip, but the real alpha is ignoring the tokens.

Decentralized infrastructure is the new gold rush. The fight isn't over price; it's over scalability and data efficiency.

If you don't understand Modular Blockchains, you're missing the entire next cycle.

Are you betting on new tokens or new tech? 👇

#ModularBlockchains #DeFi #Web3

2

29

9 Dec 2025

Quiet Builders Are Winning the Long Game

Some teams push hype.

Others push code.

And then you have projects like EnsoFi, Integra Layer, and Inference Labs — builders who do both, without shouting.

What’s interesting about @Ensofi_xyz is how they treat reputation. Not vanity metrics. Not forced “engagement.” Real identity, real value, real history. Your wallet becomes your resume — and $ENFI ties the entire relationship layer together.

@integra_layer does the opposite but completes the circle. Instead of focusing on the user, it focuses on the system. How do protocols trust each other? How do apps share data? How does Web3 become easy enough that builders don’t waste half their life on integration headaches?

Then you have @InferenceLabs, the backbone of intelligence. Not AI for marketing — AI for optimization. AI that quietly improves everything the user touches. Faster decisions, better routing, smarter design.

It’s easy to overlook teams that don’t scream.

But often, they’re the reason the next era happens.

Today feels like one of those moments.

@Ensofi_xyz @integra_layer @InferenceLabs @Galxe @Starboard_Galxe @KaitoAI_ @What_is_integra

#ENFI #Web3Infrastructure #AIInfra #CryptoAI #ReputationTech #ModularBlockchains

#BuilderEcosystem #FutureOfWeb3 #OnChainReputation #GalxeQuest #GalxeCampaign

2

18

8 Dec 2025

L2 War Heats Up: $ARB hits 5M daily transactions. The scalability narrative is NO LONGER a future dream.

If a Layer 2 can handle that volume, ASTERDEX's sub-second trades become the new industry standard.

The alpha is simple: liquidity follows speed.

Are you betting on Arbitrum or the $TIA ecosystem to win the Modular race? 👇

#ModularBlockchains #DeFi #ASTERDEX

1

2

47

4 Dec 2025

🚀 gLitecoinVM

Litecoin’s silent upgrade is no longer silent — programmability is now a live reality.

Most people still see LTC as “digital silver,” but @LitecoinVM is quietly turning it into a settlement-grade execution layer.

The core shift?

LTC keeps its base-layer discipline while gaining a modular VM capable of real smart contract logic:

deterministic settlement anchored to Litecoin

Bitcoin-tier finality assumptions

modular execution without touching consensus

DeFi, agents, stablecoins, derivatives → all suddenly viable on LTC

This is the part the timeline keeps sleeping on:

when an asset with deep liquidity, decade-long uptime, and massive global distribution unlocks programmability, liquidity doesn’t drip in — it migrates.

Early mindshare readings already show the pattern:

low noise, high retention, technically fluent participants → the usual signatures of a narrative before it flips macro.

If LTC enters its programmable era,

LitecoinVM is the doorway everything flows through.

Not hype.

Just architecture.

#LitecoinVM #ModularBlockchains

3 Dec 2025

“Litecoin’s Most Overlooked Upgrade: Programmability Is Here.” @LitecoinVM

LitecoinVM is one of the most important—yet most underestimated—transformations happening in the L1 landscape.

People keep calling it “just another execution layer,” but that completely misses the core innovation.

What LTCVM truly delivers is a programmable settlement engine on top of Litecoin without altering Litecoin’s base-layer philosophy.

That means:

Litecoin-level security

Bitcoin-style finality assumptions

A modular VM capable of executing modern smart contracts

Settlement anchoring directly back to Litecoin

This architecture unlocks an entirely new economic surface area:

DeFi rails, derivatives, stablecoin layers, autonomous agents, and cross-chain execution — all on top of an asset with deep liquidity and over a decade of proven reliability.

The overlooked alpha is this:

Because the VM is modular, consensus remains untouched, avoiding the fragmentation that weakens most chains attempting similar upgrades.

Mindshare patterns are already forming:

low noise, high technical retention, and an unusually strong concentration of informed participants.

That’s the early signature you see right before a niche narrative turns into a macro trend.

If Litecoin’s next era is going to be programmable,

LitecoinVM is the structural doorway.

And when a settlement-grade asset opens up its execution layer, liquidity doesn’t creep — it migrates.

Not hype.

Just architecture.

#ModularBlockchain #LitecoinVM

2

6

12

239

JUST IN: @Monad_xyz reveals the full tokenomics for $MON ahead of its Nov 24 airdrop. 🔓 Focus on #staking incentives, modular infra utility, and long-term sustainability. One of the few L1 plays still building in silence.👀 #TokenLaunch #ModularBlockchains #AirdropSeason

1

46

3 Nov 2025

People still don’t realise how big this is

$SNOWAI by @snowball_money is NOT just another token drop

They’re literally turning the community into the engine.

Snowball @snowball_money is building the identity and reputation layer for the modular blockchain era and now they’re using ChainGPT’s creator rails to let the community co-build the signal.

The $300K BuzzDrop with @ChainGPT_Pad @Chain_GPT is designed to reward real creators, real engagement, real contribution not random wallets farming airdrops.

This is where the next wave of crypto value is born , creators credible contribution = onchain reward.

The people who build the narrative will own the narrative.

We’re not watching from the sidelines.

We’re helping shape it.

#SNOWAI #Snowball #SnowballMoney #ChainGPT #ChainGPTPad #BuzzDrop #Web3 #CryptoCommunity #AI #ModularBlockchains #OnchainReputation #EarnByCreating

7

3

8

3,672

30 Oct 2025

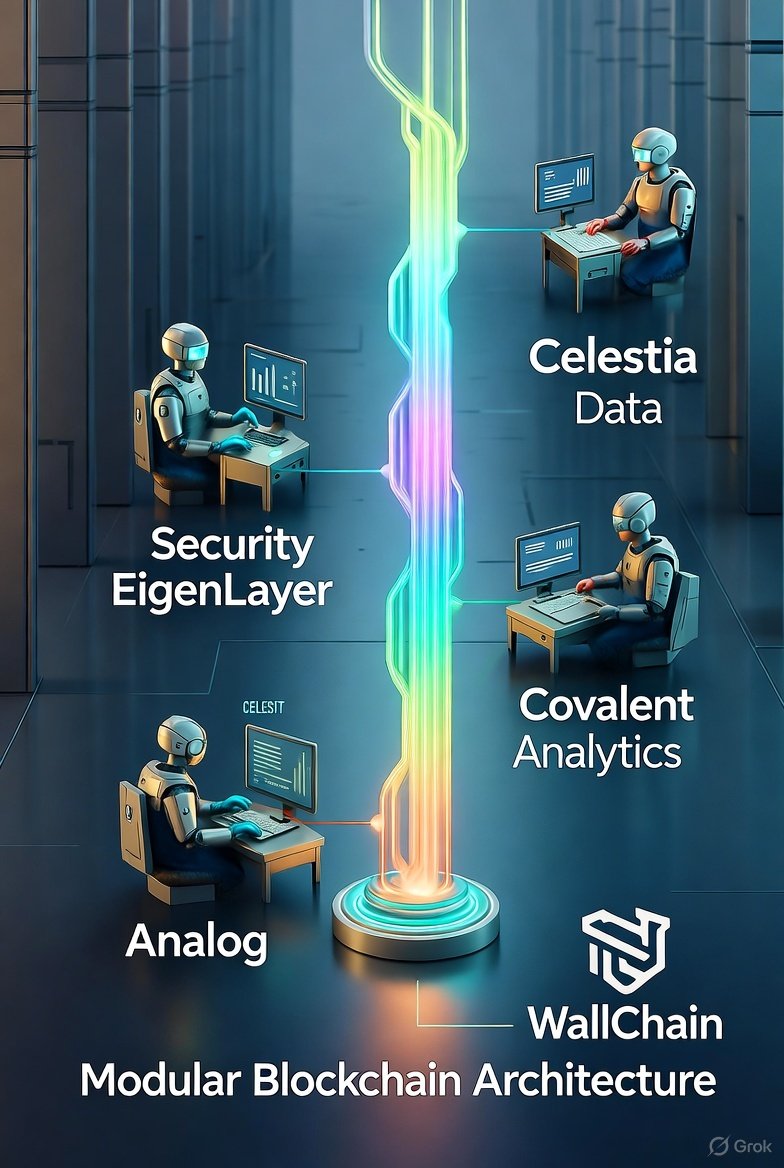

The Modular Shift

Monolithic blockchains tried to do it all; execution, consensus, data, one chain to rule them all.

And it worked…... until it didn’t.

They became slow, expensive, and allergic to scale.

Modular chains changed the landscape: Each layer does what it’s best at.

🟣 .@CelestiaOrg handles data availability, 1M blobs processed and counting.

🟢 .@eigencloud adds restaking, your ETH can now secure multiple protocols at once.

Efficiency, unlocked.

Division of labor: Blockchain Edition.

Chef cooks. Waiter serves. Cleaner resets the table.

Everyone specialized, everything runs smoother.

That foundation powers:

@Covalent_HQ (data unified)

@OneAnalog (chains communicating)

@wallchain (attention valued)

This is why modular design matters :

when infrastructure stops competing and starts coordinating, new economies emerge.

Even @KaitoAI spotted it: “Restaking” queries up 3x in 3 weeks.

Infrastructure is getting its moment.

Specialization wins: in life, in teams, in chains. 🔧

#ModularBlockchains #Restaking #Celestia #EigenLayer #Web3Infrastructure #Wallchain

1

6

62

24 Oct 2025

.@KaitoAI data: "Modular blockchain" searches up 2.5X in 3 weeks 📊

Why it's heating up:

• Celestia TIA staking live

• EigenLayer restaking TVL climbing

• Avail mainnet approaching

Infrastructure narratives move slow, then suddenly.

Early attention = early positioning

.@KaitoAI @CelestiaOrg @eigencloud

#ModularBlockchains #CryptoInfrastructure

1

4

95

23 Oct 2025

Really feeling bullish on what @snowball_money is building right now ❄️

👉 $SNOWAI isn’t just another identity play — it’s shaping the missing layer of Web3: trust that actually moves across chains.

🔥With the Modular Naming Service (MNS), one name works everywhere — no more fragmented wallets or isolated identities. And when you add the Onchain Reputation Score (ORS) on top, it becomes a complete Web3 passport — your activity, reputation, and trust all connected, verifiable, and portable.

This isn’t just cool tech — it’s the foundation for real adoption.

Projects can reward verified users, DAOs can filter credible participants, and ecosystems can finally build around reputation instead of speculation.

💪The future of Web3 identity isn’t about control — it’s about connection.

And Snowball is quietly building the rails for that future: modular, interoperable, and user-owned.

If you’re watching the modular blockchain stack evolve, this might be one of the most important pieces to pay attention to.

👉Check it out → pad.chaingpt.org/pools/snowb…

#Snowball #SNOWAI #Web3Identity #DeAI #ModularBlockchains #Web3Community

5

22

18

11,287

23 Oct 2025

Big moves from @snowball_money ❄️

Their new collab with Arichain is a game changer — merging multi-VM chains with $SNOWAI’s Modular Naming Service (MNS) to finally make cross-chain identity simple, unified, and usable everywhere.

💡 Imagine this:

One name that works across every chain — no more juggling wallets, addresses, or handles.

Your on-chain rep travels with you, unlocking DeFi yields, gaming collabs, governance access, and trust across ecosystems.

This is what Web3 identity was supposed to feel like — clean, connected, and community-owned.

With Snowball’s MNS Arichain’s multi-VM architecture, trust and reputation now move as freely as liquidity.

The result? A truly unified Web3 experience — where your name, data, and credibility live on every chain you touch.

Web3’s getting smarter, faster, and more human — and $SNOWAI is right at the center of that evolution. 🚀

#SNOWAI $SNOWAI #Web3Identity #DeAI #ModularBlockchains

6

24

26

11,017

22 Oct 2025

Hey Folks, Snowball Labs is redefining digital identity and reputation for the modular blockchain era. ❄️

They’re not just talking about decentralized identity — they’re building it, with two powerful products leading the charge 👇

1️⃣ Modular Naming Service (MNS) — a chain-agnostic system that connects wallets, identities, and messaging across chains.

No more silos. No more friction. Just seamless cross-chain reputation that travels wherever you do.

2️⃣ Onchain Reputation Score (ORS) — a trust layer for the next generation of dApps and DAOs.

Filter governance, target real contributors for airdrops, and reward verified, high-value users — not bots.

What’s next for 2024:

🟡 Identity Minting Testnet launching soon

🟡 Integration with LayerZero for full modular connectivity

🟡 A $250K Grant Program to empower builders and innovators

With 10K names already reserved and 30K wallets scored, @snowball_money is proving that trust, identity, and reputation can live fully on-chain — transparent, verifiable, and community-owned.

The future of Web3 identity isn’t coming.

It’s already rolling with @snowball_money. 🌐💠

#Snowball #SNOWAI #Web3Identity #DeAI #ModularBlockchains

8

25

29

518

20 Oct 2025

#Blockchains evolved, and so did the challenges - Too slow. Too rigid. Too isolated. Old chains were powerful… but not built for today’s scale.

#Modularblockchains fix this — making systems more connected, secure, and human-focused. 👥

From #DeFi scaling to #DigitalIdentity to #Carbon Tracking, they’re building a better digital world. 🌍

Curious how this works in action? Explore #MetaEarth’s vision for a modular, human-centric #Web3 👉 invite.mec.me/?type=download…

9

18

86

4,363

15 Oct 2025

🧵3/

Enter #ModularBlockchains — a new design where each layer focuses on what it does best:

⚙️ Execution

🔐 Settlement

💾 Data availability

This specialization boosts scalability, security, and flexibility.

It’s not just evolution — it’s reinvention. 💡

1

1

143

13 Oct 2025

🔥 SYMBIOTIC IS REWRITING THE ENTIRE STAKING PLAYBOOK ⚡️

GM Web3! Let's talk about the MASSIVE moves @symbioticfi just pulled that most people completely missed 🧠

While everyone's focused on EigenLayer drama, Symbiotic quietly dropped External Rewards and locked down game-changing partnerships with Lombard Chainlink. This isn't just another restaking protocol - this is the foundation for modular blockchain coordination.

HERE'S THE BREAKDOWN:

💎 External Rewards launched across 8 networks - protocols now pay REAL tokens (not just points)

🚀 $100M LINK vault 20M BARD vault securing cross-chain Bitcoin transfers

⚙️ Universal Staking Framework = ANY ERC-20 can be restaked (not just ETH derivatives)

📊 Permissionless modular design beats rigid architectures every time

The data doesn't lie: Symbiotic hit $1.28B TVL while staying completely permissionless. No governance committees, no slashing overlords - just pure cryptoeconomic coordination at scale.

Smart money is positioning for the modular future. While others build walled gardens, @symbioticfi built the infrastructure layer that EVERY blockchain will need.

This changes everything. Universal Staking isn't just restaking 2.0 - it's the coordination layer for Web3's modular future ✨

🎯 symbiotic.fi

📱 app.symbiotic.fi/deposit

#Symbiotic #UniversalStaking #RestakingWars #DeFi #ModularBlockchains

23

1

74

442

12 Oct 2025

The future of blockchains is not isolation - it's connectivity.

@EspressoSys is building the layer that makes it real.

With HotShot, a high-performance consensus and data access layer, rollups and modular chains can talk, sync, and scale together.

☕️ Seamless Interoperability

☕️ Shared Security

☕️ True Modular Freedom

When every chain moves fast, stays secure, and works as part of a unified ecosystem, that's when Web 3 is complete.

Espresso is building the future. ☕

#EspressoSys #Interoperability #ModularBlockchains

2

1

5

73

16 Sep 2025

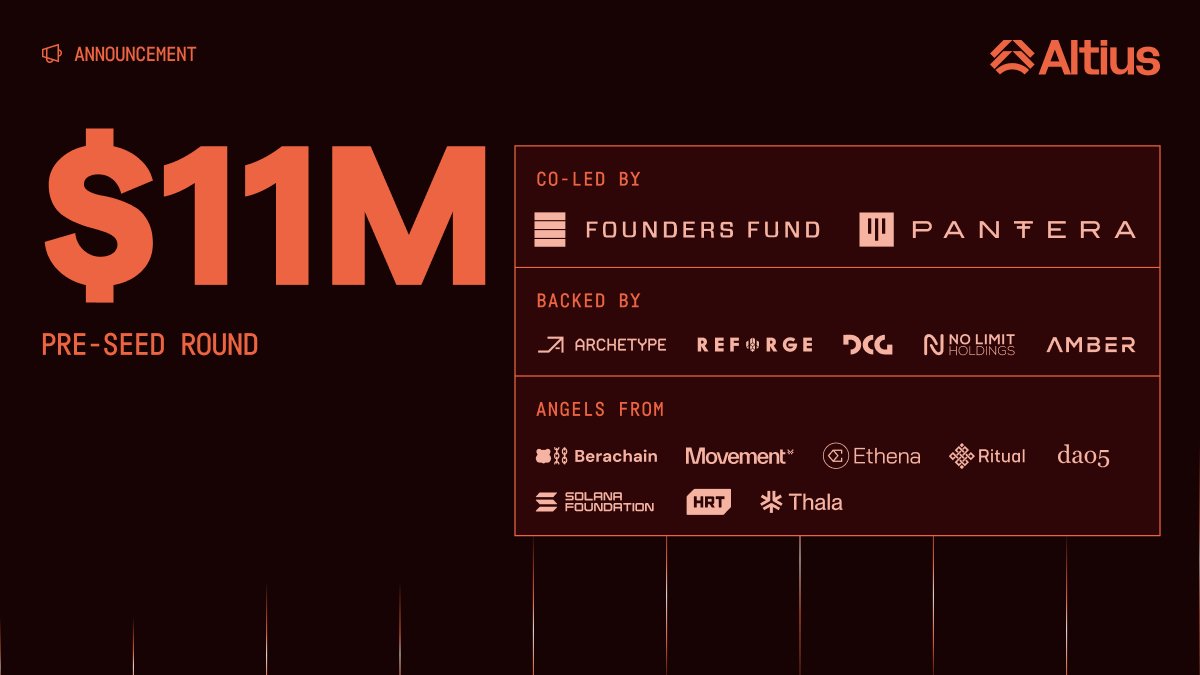

🚀 Big News from Altius! 🚀

We’ve raised $11M in pre-seed funding, co-led by Founders Fund & Pantera Capital 🔥

@AltiusLabs is building a modular, VM-agnostic, high-performance execution layer — futureproofing blockchain infrastructure for a truly multi-chain world 🌐⚙️

💡 What we're solving:

Network congestion

High gas fees

Lack of scalability for app-specific chains

✅ Our solution:

A VM-agnostic modular stack that integrates with any L1, L2, or app chain, delivering instant performance seamless interoperability 💥

Backed by top-tier investors:

@ArchetypeVC @reforge @DCGco @nolimithodl @ambergroup_io

Angels from @Berachain @movementlabsxyz @ethena @ritualnet @daofive @SolanaFndn & more!

🌍 We're just getting started.

Major partners & updates coming soon.

Let’s scale at the speed of thought.

#Altius #Web3 #ModularBlockchains #L2 #Scalability #CryptoNews

1

1

12

67

12 Sep 2025

So many narratives this cycle… which one are you betting on? 👀

Narratives:

#RealYield

#Restaking

#ModularBlockchains

#DePIN

#RWAs

#Stablecoins

#OnchainPerps

#LSTs

#AccountAbstraction

#ZKProofs

#SocialFi

#GameFi

#AIxCrypto

#Interoperability

#CrossChain

#PrivacyTech

#DeSci

#NFT

#LiquidRestaking

#MEVProtection

#DecentralizedAI

#BTCfi

#ETHfi

#RealWorldAssets

#DAOs

#CreatorEconomy

#IntentBasedArchitecture

#OnchainOptions

#PredictionMarkets

#ScalingSolutions

#Layer2s

#AppChains

#PerpDEXs

#CryptoPayments

#CommunityTokens

#DigitalIdentity

#OnchainGaming

#OpenFinance

#Tokenization

3

130

6 Sep 2025

11/

Summary:

0G Labs =

🚀 High-speed

💸 Low-cost

🧠 AI-native

🧱 Modular

🧙 Backed by actual devs

…and may or may not be building the DA layer your future favorite app will run on.

Don't sleep 🛌

#0G #Crypto #Web3 #AI #ModularBlockchains

1

30