Jun 8

Segment Focus: Enterprise Commerce & GIFT City Offshore Delivery

The non-defense software wing acts as the high-margin cash engine:

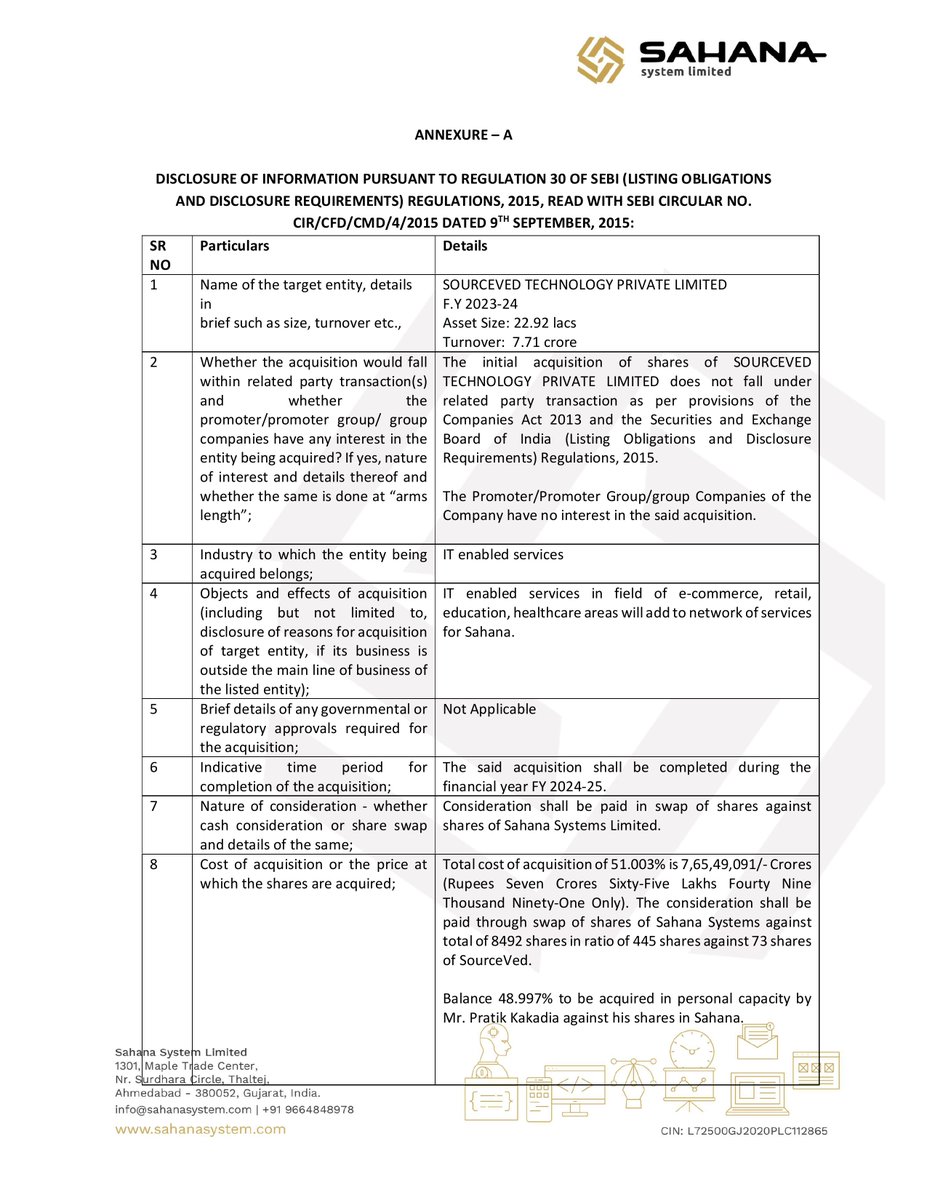

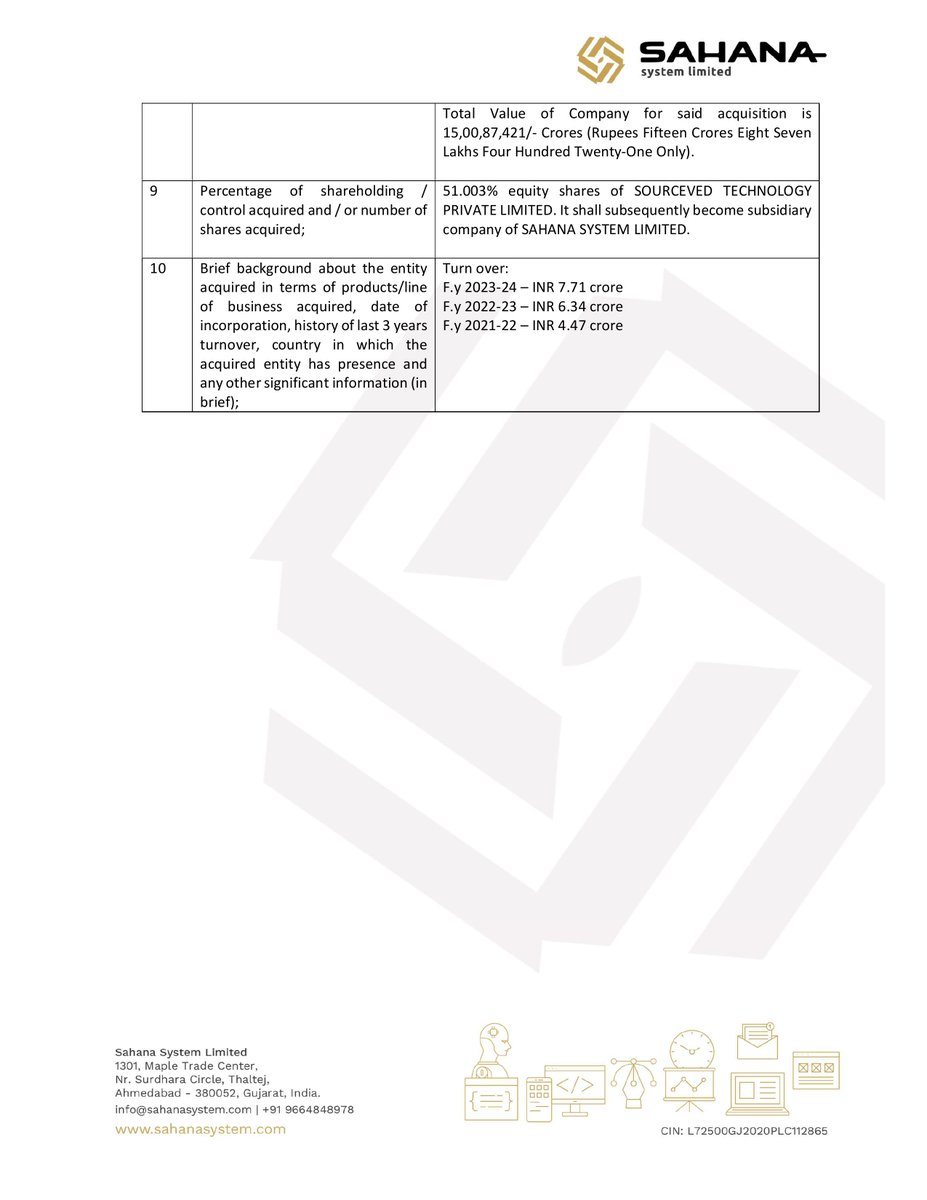

Sourceved Technologies (51% stake): Operates as a certified Sitecore Solution Partner, delivering premium enterprise content systems (CMS) and e-commerce architectures to retail, fintech, and healthcare clients.

Applie Infosol (51% stake): Positioned in the GIFT City SEZ, this entity acts as the offshore delivery hub, allowing the company to scale globally with tax-efficient operating costs.

(6/11)

1

119

Jun 8

The Core Metamorphosis

Founded in 2013 as a localized partnership named Oceans Technologies, Sahana Systems has undergone a major strategic transformation.

After its SME IPO in June 2023, the group executed a series of programmatic acquisitions (Softvan, Sourceved, Applie Infosol) to shift from simple IT services to complex deep-tech systems integration, clearing the path for its migration to the NSE Main Board.

(2/11)

1

324

17 Nov 2025

#SME #Sahana #SahanaSystems

Sahana Systems H1 FY26 Concall Highlights:

👉FY 2026 & Future Outlook :

▫️FY26 expected revenues ~210-220cr on conservative basis

💠~₹20cr closed in exports, ₹16-17cr collected, with recurrent revenue. 60% revenue from government, 40% enterprise (30% overseas)

💠Long-term target: Targeting ₹350cr in FY27 and ₹500cr in FY28

💠Opportunity lies across segments like defense (₹1,000-2,000cr), marine system integration (₹500-600cr), and government IT services (₹1,000cr)

▫️EBITDA margin: Expected to remain in the ~33% range seen in H1

💠PAT margin: Projected to increase slightly from H1, with overall PAT margins expected to rise modestly over the next three years due to higher-margin projects in defense and system integration

▫️Investor Engagement: Commitment to increase earnings call frequency (quarterly from FY27 probably near to migration)

👉Projects and pipeline:

▫️Indian Navy: Upgrading RF testing and chip point-of-contact design facility at Jamnagar (falls under electronic warfare)

💠Dredging Corporation of India: IoT and AI upgrades for vintage dredgers (marquee marine/shipping customer)

💠IPRCL (for Tuticorin Port): Large-scale digital twin project for operational efficiency, cargo handling, vessel traffic management, computer vision, and generative AI automation

💠Ministry of Information and Broadcasting: Samvad media monitoring tool for 58 cabinet ministries, PMO, and PIB (covers print, digital, and social media; daily reports by 7:45-8:00 AM).

▫️Revenue mix: Sahana standalone (76% from existing customers, 24% new); Softvan (defense/deep tech; 65% existing, 35% new); SourceVed (12-15% new customer growth)

▫️Order Book: Confirmation for next 1-1.5 years' revenue execution; vendor status in tenders with >80% win probability; MOUs with Defence PSUs and central PSUs for recurring revenue

▫️Future Pipeline: Gestation period of 3-4 years for government projects; current work positions the company for FY27-28 revenue

💠Includes couple of ₹1,000cr-scale projects (shortlisted among few vendors)

💠Patents: 12 applied last year, 6 under positive process, 2 awarded (enabling product resale in system integration)

👉 Others :

▫️Business Diversification and Expansion: Focus on defense (anti-drone, radar, electronic warfare), fintech (UPI platforms, core/digital banking), edutech (AR/VR, smart/virtual classrooms), healthtech (HIMS, AI diagnostics), and port/marine (IoT integration, predictive analytics, digital twins)

💠Entering EV charging in Andhra Pradesh via OEM tie-up for manufacturing, IoT/embedded enhancements, and CMS

💠Revenue model is revenue-share (recurring but not high-margin; includes cybersecurity R&D for stations)

💠No strong seasonality, but H2 can be bulkier due to government budget exhaustion and mobilization advances

💠Opportunities in Southeast Asia (e.g.,Thai Government meetings), Africa, and Latin America for fintech/defense/deep tech

▫️Operational and Strategic Updates: Asset-light model; DPIIT-recognized startup with certifications. Strengthening leadership/R&D via hiring (first-, second-, and third-level roles)

💠No formal decision on separate listing of Sahana Defense (subsidiary)

▫️Cash Flow and Funding: Negative cash flow tied to working capital in service-driven projects; mitigated by milestone-based government tenders

💠Potential for OD/CC facilities or equity/debt if large projects accelerate

▫️Risks: Strategic challenges from early large-order wins requiring cash flow scaling, but management views projections as conservative with execution exceeding

2

4

31

4,417

10 Apr 2024

10 Tips for Corporate Communication Success! Elevate your skills today. 💡

#communication #skills #tips #tricks #tipsandtricks #corporate #career #skilldeveopment #success #wednesday #sourceved #strategies

1

2

31

Happy 2nd Work Anniversary, Krunal Modi 🌟🎉

Your hard work and commitment continue to inspire us all. Here's to more milestones together!

#workanniversary #anniversary #achievement #milestone #sourceved #employeeanniversary #anniversarycelebration #success #hardwork

2

16

28 Dec 2023

What do you think? 🤔🤔🤔

Will remote-first companies dominate in 2024? Share your thoughts!

#remotework #remotejobs #2024goals #workfromhome #workfromhomejobs #fact #news #trending #trendingnow #sourceved #technology

2

33

16 Aug 2023

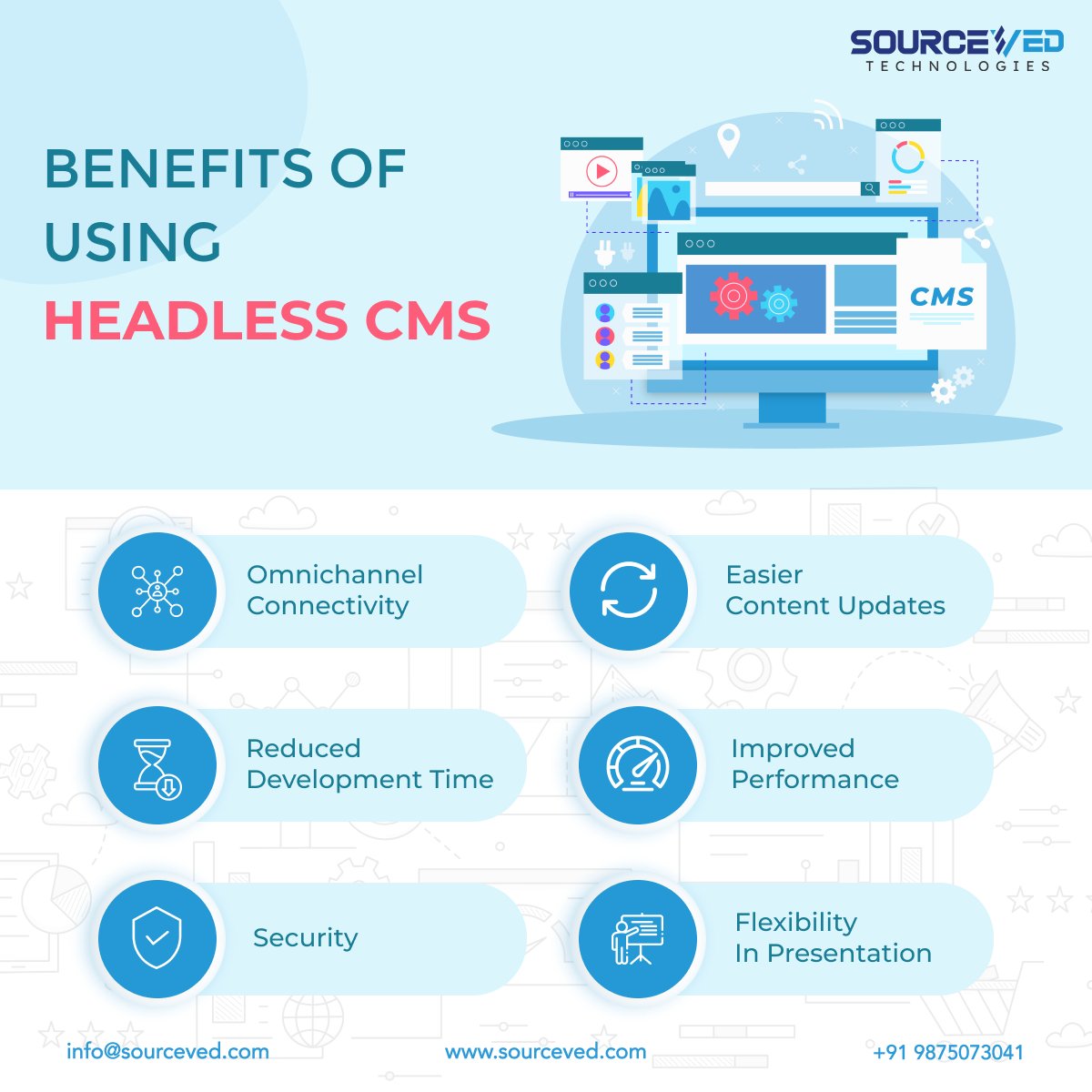

Empowering Your Content Strategy: Benefits of Headless CMS.

#cms #headlesscms #cmsdevelopment #benefits #advantages #wednesday #technology #webdevelopment #web #it #sourceved #sourcevedtechnologies

1

41

10 Aug 2023

What's your most creative reason to skip work on 14th August?

#meme #memepost #funny #funnymemes #corporatememes #leaves #funnyvideos #thursday #corporatelife #sourceved #sourcevedtechnologies #memes #fun #laugh

1

105

Celebrating Our Beloved Boss's Birthday 🎂🎉.

A fantastic evening filled with laughter, joy, and heartfelt wishes!

#birthday #celebration #party #boss #birthdayparty #birthdaypost #sourceved #life #mood #partytime #cake #sourcevedtechnologies #lifeatsourceved

2

34

What is the main reason you prefer on-site work?

#poll #polltime #pollquestion #polloftheweek #polloftheday #onsitejob #remotework #remotejobs #culture #communication #sourceved #sourcevedtechnologies

100%

Face-to-face interactions

0%

Collaboration

0%

Company culture

0%

Other

1 votes • Final results

1

29

26 Jul 2023

Climbing the ladder of success with unwavering determination.

#motivation #quotes #quoteoftheday #motivationalpost #wednesdaymotivation #success #tweet #threads #successmindset #life #quotesaboutlife #worklifebalance #sourceved #sourcevedtechnologies

1

46

25 Jul 2023

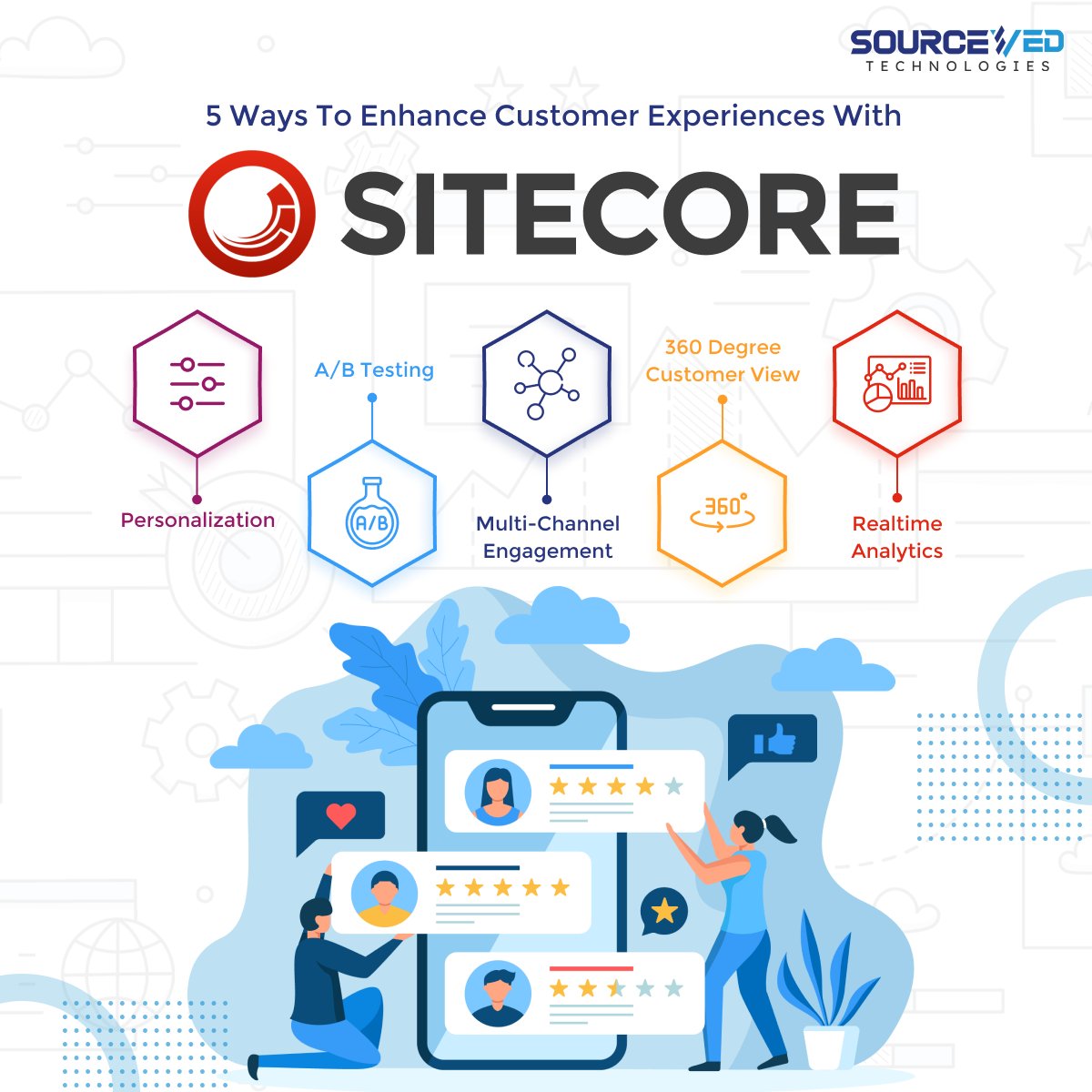

Unlocking the Power of Sitecore: Elevating Customer Experiences to New Heights 🚀

#CustomerExperience #Sitecore #Personalization #DigitalTransformation #SuccessStories #userexperience #experience #sitecorecommunity #insights #sourceved #sourcevedtechnologies

2

26

20 Jul 2023

How often do you work from home?🤔🤔🤔

#RemoteWork #Telework #WorkLifeBalance #workfromhome #workfromhomelife #worklife #remotework #remotejobs #wfh #wfhjobs #wfhlife #remotelife #sourceved #sourcevedtechnologies

0%

Full-time remote

0%

Part-time (weekly 2 days)

0%

Occasional remote work

0%

Not allowed for it

0 votes • Final results

1

19

27 Jun 2023

Work Play = Unforgettable Weekend Fun! Our company trip was a blast, creating memories that will last a lifetime.

#weekend #weekendvibes #fun #pool #swimming #funactivities #companytrip #companyculture #adventure #officetrip #culture #life #sourceved #sourcevedtechnologies

2

28

14 Jun 2023

Happy 1st work anniversary, Saumil Patel!

#workanniversary #happyworkanniversary #1yearanniversary #1stanniversary #anniversaryparty #anniversary #celebration #achivement #work #growth #success #milestone #employeeanniversary #1year #sourceved #sourcevedtechnologies

2

18

Sitecore and WordPress: Comparing two web giants for your needs.

#blog #blogpost #blogging #blogger #friday #sourceved #sourcevedtechnologies #wordpress #SitecoreVsWordPress #WebPlatformComparison

sourceved.com/sitecore-vs-wo…

1

3

32

16 May 2023

Comparing .NET MVC and .NET Core is like examining two sides of the same powerful coin.

#DotNetMVCvsCore #FrameworkComparison #WebDevelopment #Microsoft #CrossPlatform #dotnet #cms #cmscomparision #dotnetcore #dotnetmvc #dotnetjobs #comparision #vs #compare #sourceved #sitecore

1

2

3

388

19 Apr 2023

Happy Birthday kaval! Have a wonderful day filled with joy, love, and all your favorite things.

#happybirthday #birthdaywishes #celebratebig #specialday #birthdaycelebration #partytime #sourceved #sourcevedtechnologies #birthday

2

19

14 Apr 2023

Happy Ambedkar Jayanti! Remembering Dr. B.R. Ambedkar's contributions to social justice and equality.

#14April #AmbedkarJayanti #babasahebambedkarjayanti #DrAmbedkar #Ambedkar #AmbedkarBirthday #BhimraoAmbedkar #drbhimraoambedkar #DrBabasahebAmbedkar #sourceved

3

34