246 Photos and videos

I started publishing on Substack one month ago:

snmart.substack.com

Since then, I’ve written deep dives on $AAOI, $AEHR, $VELO, $SNDK, $IBRX, $OUST, $PDFS and $LPK / $LPKF.

Several of them are already up 50% since publication. Others are still in accumulation mode.

I’m not trying to sell you “10x stock picks,” even if some of them may eventually get there.

What I’m really selling is filings work, earnings call analysis, annual reports, industry context, and precision.

And above all: Conviction.

Paid subscribers get access to the full deep dives: the thesis, numbers, valuation, catalysts, risks and the early signals I’m tracking before they become consensus.

Start with the free articles first. If my work adds value, I’d be grateful if you considered becoming a paid subscriber.

2

2

20

6,326

This shift is bullish for $LPKF / $LPK:

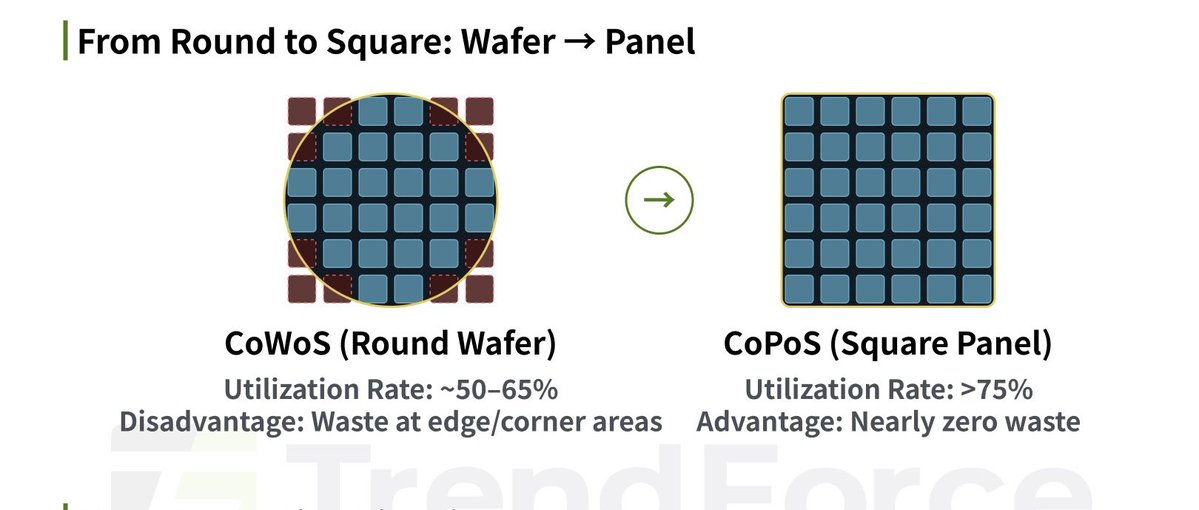

> Advanced packaging started on round silicon wafers. It's moving to square panels.

> The problem with round: CoWoS puts the GPU and HBM on a shared silicon interposer, processed on a 300mm wafer. As you can see below, round geometry wastes area. You can't tile rectangular packages into a circle without losing the edges, and it gets worse as AI packages get larger.

> A square panel reduces that penalty. Packages tile cleanly, and you get far more working area than a wafer allows.

> And here is where $LPKF is positioned: a glass panel is useless until you can put precise vertical connections through it.

> Through-glass vias. Glass is hard, brittle, unforgiving. Drilling clean, high-density vias at panel scale is a real engineering problem, not a solved one.

> Which is where $LPKF sits. Its LIDE process (Laser Induced Deep Etching) is built for exactly this: through-glass vias. It's at the structuring layer, the step that has to work before anyone can package on a panel.

A pick and shovel for the glass era.

7

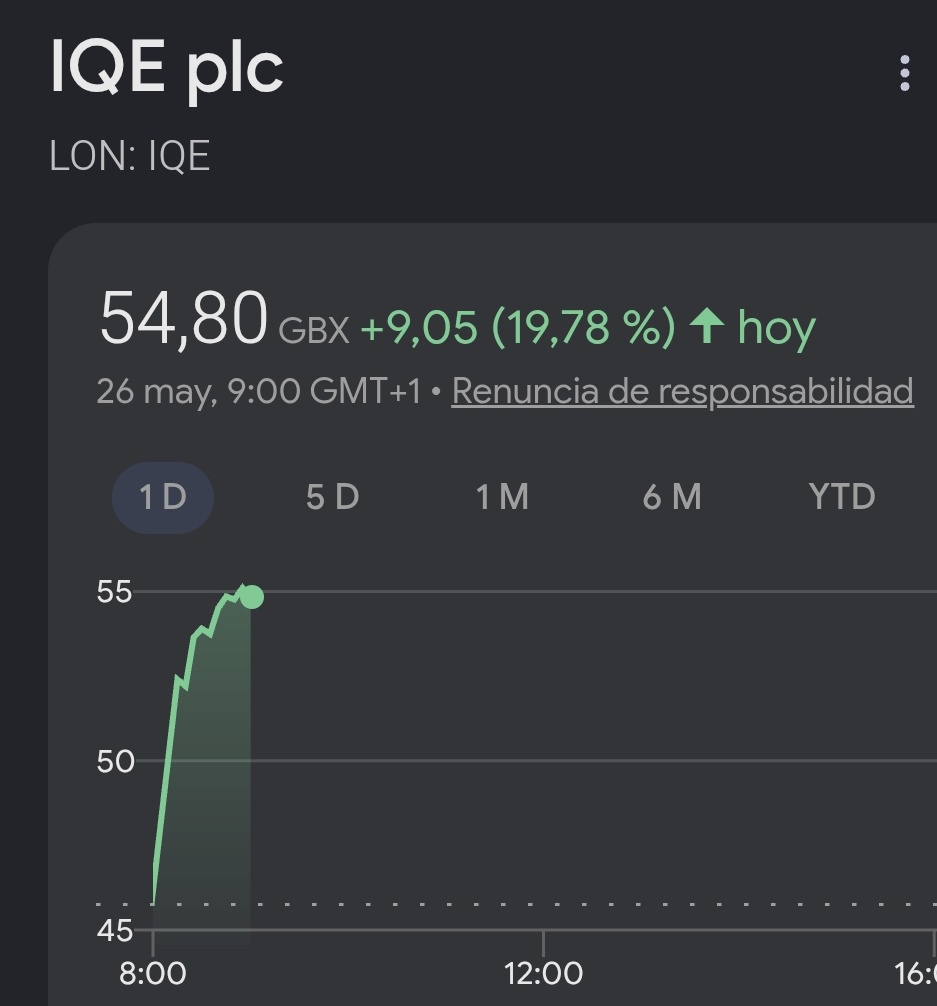

From a TA perspective, I also like $IQE here.

> After the huge move from the lows, the stock has been consolidating while still respecting the rising trendline.

> Price has tested that support area several times and, so far, buyers have stepped in.

> Volume has also cooled down during the consolidation, which makes the pullback look healthier.

> The 45p area looks like a key short term support zone, while a clean reclaim of 50 - 55p would make the setup much stronger.

For now, this still looks like healthy consolidation within an uptrend.

Im not the best person for TA, but I really like the $IQE setup here.

For proper technical analysis, follow @jrouldz and @mkfilko

I have increased my position in $IQE:

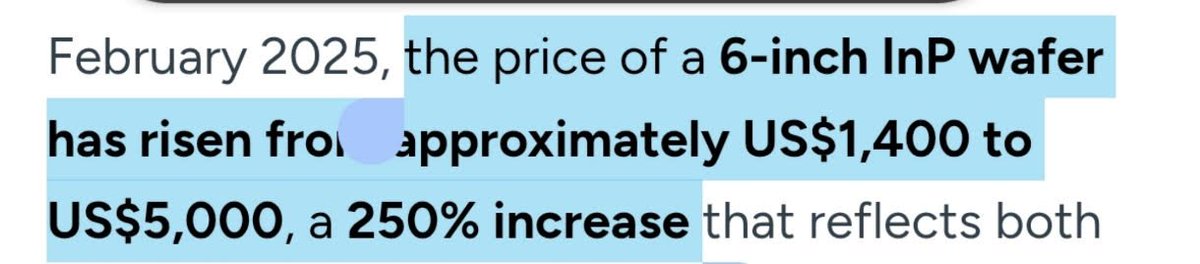

> The InP bottleneck just became a sovereignty problem. China controls InP exports through a licensing regime.

> A 6 inch InP wafer has gone from $1,400 to $5,000; a 250% jump.

> China produces 70% of the world's indium.

> $AXTI , the #2 InP substrate maker, makes most of its InP inside China and waits on Beijing export permits.

The West optical supply chain runs on InP substrate from two places: China ($AXTI ) and Japan (Sumitomo, JX).

Together $AXTI and Sumitomo are 80% of global supply.

> $COHR and $LITE do epitaxy in-house but buy their substrate externally.

> $COHR CEO literally flew to China with a US delegation to lobby on permit delays.

> Now look at $IQE. Through its Wafer Technology division in the UK, its one of the very few Western players that grows its own InP crystal and substrate.

Owning any Western substrate capacity starts being strategic.

If the West has to onshore its optical supply chain, $IQE is one of the few names already well positioned.

3

14

2,564

I have increased my position in $IQE:

> The InP bottleneck just became a sovereignty problem. China controls InP exports through a licensing regime.

> A 6 inch InP wafer has gone from $1,400 to $5,000; a 250% jump.

> China produces 70% of the world's indium.

> $AXTI , the #2 InP substrate maker, makes most of its InP inside China and waits on Beijing export permits.

The West optical supply chain runs on InP substrate from two places: China ($AXTI ) and Japan (Sumitomo, JX).

Together $AXTI and Sumitomo are 80% of global supply.

> $COHR and $LITE do epitaxy in-house but buy their substrate externally.

> $COHR CEO literally flew to China with a US delegation to lobby on permit delays.

> Now look at $IQE. Through its Wafer Technology division in the UK, its one of the very few Western players that grows its own InP crystal and substrate.

Owning any Western substrate capacity starts being strategic.

If the West has to onshore its optical supply chain, $IQE is one of the few names already well positioned.

2

2

14

4,124

Nicolas retweeted

Jun 12

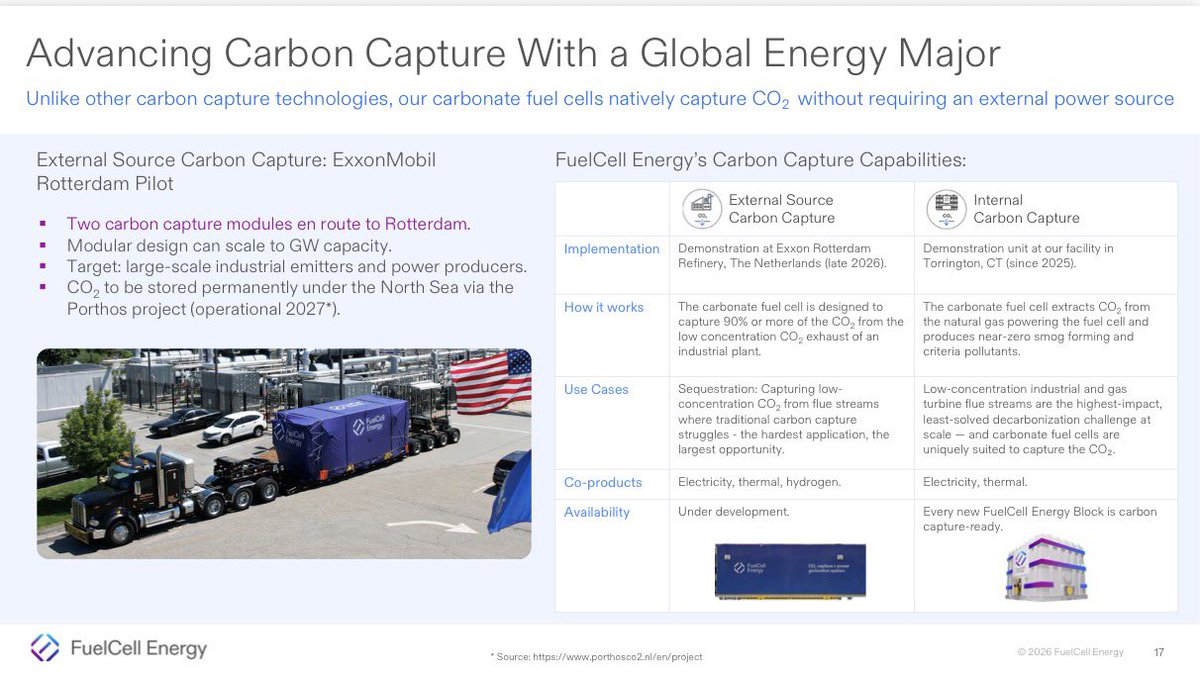

People have aped into pre-rev, basically pre-product names and ran them up to $10B , yet $FCEL has two commercially available products both with SAMs in the Hundreds of Billions working with:

1. Major data center players (T5, Inuverse, SDCL) and Hyperscalers with multiple late stage opportunities

2. $XOM for a carbon capture pilot that, if successful, unlocks a best-in-class, first of its kind market opportunity.

I find it to be such a gift that $FCEL trades at this market cap, and they have ~$500M in cash to support expansion to 500 MW and the path to profitability.

Jun 12

$FCEL Carbon Capture path with $XOM opens the door to a full stack of revenue streams

Here’s how $FCEL could see revenue:

Equipment Sales LTSAs (Standard)

- FCEL sells carbonate fuel cell modules directly to industrial customers (power plants, refineries, steel mills)

- Long-term service agreements layer in recurring revenue on top of hardware

XOM as Commercial Channel

- ExxonMobil identifies industrial customers globally, FCEL manufactures and services the hardware

- Revenue sharing structure TBD pending commercial framework negotiation

The IP Angle Not Understood

- Under the JDA (2019 2024 Amendment No. 5), $FCEL holds royalty-free, perpetual, worldwide licenses to jointly developed IP

- Covers Power AND Hydrogen applications, including CO₂ capture-integrated modules

- FCEL can commercialize independently, no Exxon approval required, zero royalties owed

The licenses survive the JDA term (currently through Dec 2026). FCEL keeps the technology runway regardless of how the XOM relationship evolves.

Module sales. Services. PPAs. Hydrogen. All on top of a royalty-free IP foundation.

The carbon capture thesis is much bigger than a fee per ton.

4

4

41

6,824

Nicolas retweeted

Jun 12

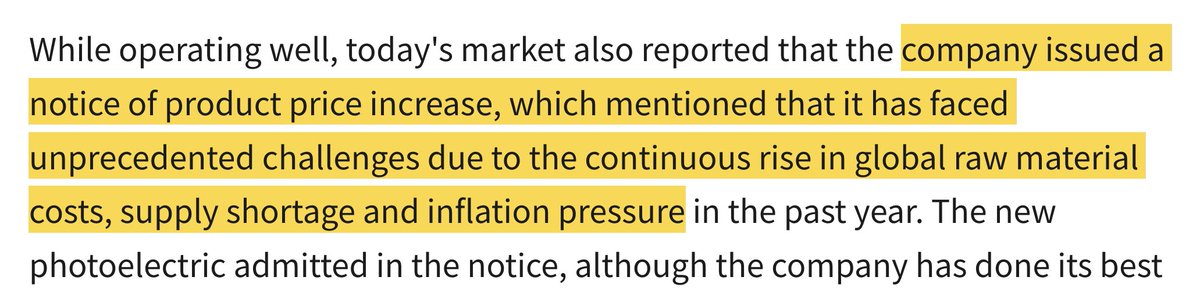

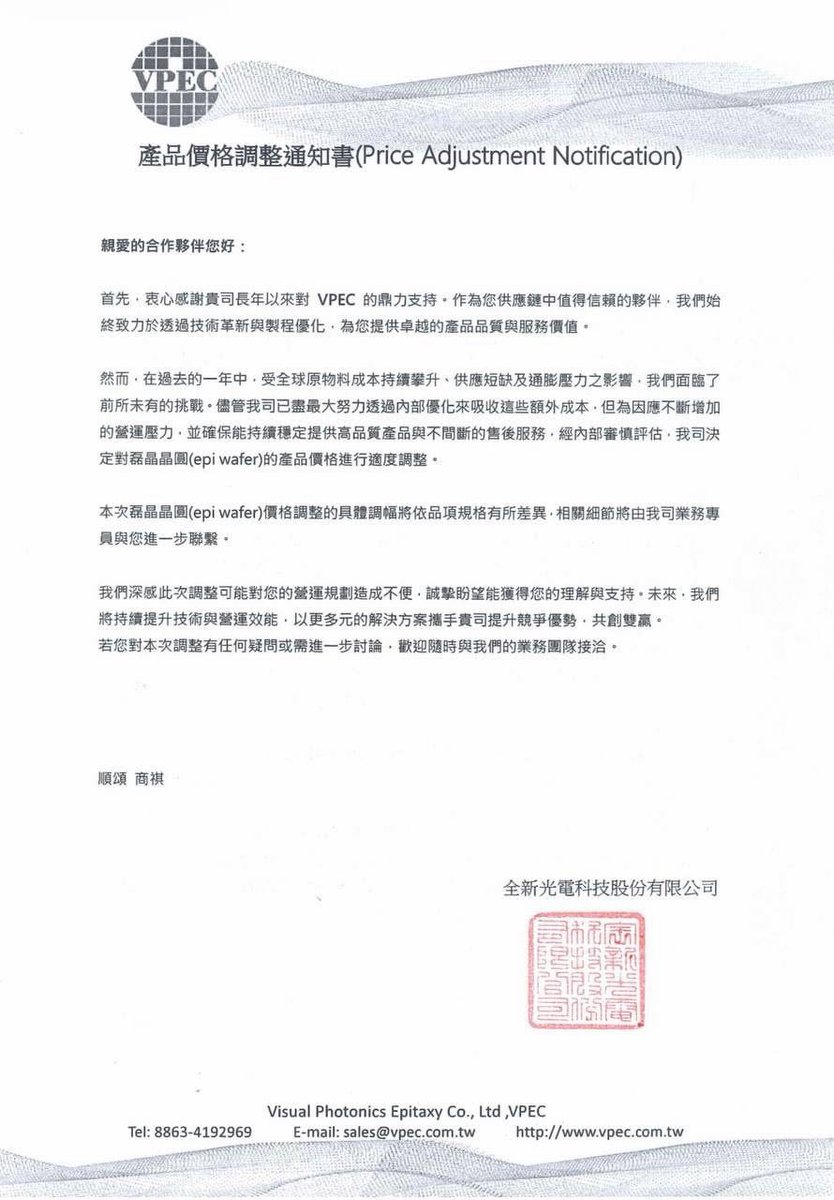

VPEC new price hikes on Epiwafers today.

Positive bottleneck read through on companies like $IQE and Landmark (3081) in terms of pricing power/demand for epiwafers.

This follows $MTSI investment into IQE to secure capacity, and shows how important some of these chokepoints are.

(disclosure: have positions in IQE)

VPEC全新光電

產品價格調整通知書 (Price Adjustment Notification)

親愛的合作夥伴您好:

首先,衷心感謝貴司長年以來對 VPEC 的鼎力支持。作為您供應鏈中值得信賴的夥伴,我們始終致力於透過技術革新與製程優化,為您提供卓越的產品品質與服務價值。

然而,在過去的一年中,受全球原物料成本持續攀升、供應短缺及通膨壓力之影響,我們面臨了前所未有的挑戰。儘管我司已盡最大努力透過內部優化來吸收這些額外成本,但為因應不斷增加的營運壓力,並確保能持續穩定提供高品質產品與不間斷的售後服務,經內部審慎評估,我司決定對磊晶晶圓的產品價格進行適度調整。

本次磊晶晶圓價格調整的具體調幅將依品項規格有所差異,相關細節將由我司業務專員與您進一步聯繫。

213

40

559

392,555

Nicolas retweeted

Jun 11

Thoughts/ clarifications on InP Substrates $AXTI ...

> $AXT has been getting permits to ship to U.S. companies based outside of the U.S. Think of $COHR Sweden facility as an example.

> $COHR has ~5 substrate suppliers. Not limited to $AXT , although of course they want as much visibility as possible and the more the better. And Axt is a major player that is a major gate.

> $LITE has locked up major supply for a while with Sumitomo. But again, still want as much visibility and multi source as possible.

> $LITE $COHR $AAOI $NOK Do not make substrates. They source those from companies like Axt and then do their own epitaxy, or directly from an epi house like $IQE

> When companies say 'InP production / capacity' it is not the same as 'InP Substrates'. When Cohr etc. say they are expanding InP production, they are not saying they are making the actual substrates. They are expanding their ability to manufacture InP-based optical chips and devices, especially lasers, photodiodes, modulators, and related optoelectronic components

I'll do a full writeup later

13

9

180

27,674

Last post I compared $IQE to the layer below it in the chain ($AXTI, the substrate). Today, the layer above. And the name some of you keep asking about: $SIVE.

Substrate → epi → device → module. $IQE grows the epi. $SIVE builds laser devices. Sequential layers of the same AI optical chain.

The numbers:

$SIVE: ~$2.3B market cap on ~$30M trailing revenue. ~85x sales. EBITDA negative. $IQE: ~$650M market cap on ~$123M trailing revenue. ~5x sales. EBITDA positive. $IQE generates 4x the revenue at a quarter of the market cap.

Per dollar of revenue, the market pays roughly 15-16x more for $SIVE. 🤨

Credit where due. $SIVE owns the hottest narrative in the chain:

> Pure play light source for CPO.

> The layer everyone wants exposure to.

> Opportunity pipeline up 77% YTD to $799M (debatable)

> GlobalFoundries reference design partnership. > Management targeting 25 to 30% CAGR from 2027. > Fresh capital raised, Nasdaq New York dual listing in motion.

> $SIVE has one clean story. $IQE is five vectors the market struggles to model.

I rode that story from 10-15 SEK. It paid for a large part of my $IQE position. So this is not a bear post.

But my honest view on $SIVE today:

At ~85x sales, the price carries years of flawless execution before fundamentals catch up. Q1 revenue came in below estimates. Management says delayed, not lost. The H2 prints have to prove that.

Now moving to $IQE:

> Guiding 20% revenue growth in 2026 to at least £117M, with strong order book visibility into H2.

> Already EBITDA positive, guiding high single to low double digit £M EBITDA this year. This is a margin recovery story. ✅

> Photonics is the growth engine. Up 15% in FY25 even while wireless dragged, driven by AI optical and defence demand. InP for AI interconnects is what carries growth beyond 2026. ✅

> £81M recap closed, all bank debt cleared, MACOM equity and board seats behind it. ✅

> Trades at ~4x FY26 guided sales. Its closest East Asian epi peer, LandMark Optoelectronics, trades at ~70x forward. A 15x gap for the same layer of the same chain. ✅

$SIVE is priced for perfection it has not delivered yet. $IQE is priced for skepticism it no longer deserves, and this is what I’m challenging.

The same chain, with the same AI optical demand. But two opposite setups.

I sold all my $SIVE and rotated into $IQE. If $SIVE answers its questions and the price resets, I will look at re entry. Until then I own the layer the market has not repriced yet.

Do you think the gap closes from the $SIVE side or the $IQE side? I think from the $IQE side.

As always, just my 2c. I am ultra long $IQE. Thanks for reading! 🐵

- Leki the investing monkey

$AXTI vs $IQE: Some Food for Thought

$AXTI just printed an all time high near $143 in May. It trades north of 50x sales and is still losing money. 12.7% gross margin. Negative net margin.

$IQE trades at roughly 6x sales. It is EBITDA positive. It grows more revenue than $AXTI.

Both sit in the same supply chain. One layer apart. So why the 10x multiple gap?

Let's walk through it.

> $AXTI makes the substrate. The raw InP and GaAs wafer. The blank canvas.

> $IQE grows the epitaxy on top of that substrate. The active laser structure. The part that actually does the work.

> Substrate then epi then device then module. $AXTI is upstream of $IQE. They are not competitors. They are sequential.

In fact $IQE is a customer of the substrate layer. You cannot grow epi without a substrate underneath it.

So why does the market pay 50x sales for the upstream layer and 6x for the layer that adds more value on top?

Here is the answer, and frankly, some of the gap is real.

> $AXTI sits in a duopoly. $AXTI plus Sumitomo plus JX control 80 to 90% of the InP substrate market. That is a cleaner monopoly story than the epi layer where more players compete.

> $AXTI is a pure AI optical play. Over 90% of the business is optical substrate for data centre. One clean narrative. $IQE is five vectors stacked together. Photonics. Wireless. Defence. GaN power. MicroLED. Harder to model. The 40% wireless drop in FY25 masked the 15% photonics growth.

> $AXTI is on Nasdaq. US institutional coverage. There is even a 2x leveraged ETF on it now. $IQE is on LSE. Thinner coverage Structural discount and lower liquidity.

> $AXTI has a record $100m InP backlog and turns profitable next quarter. Clean visibility.

That explains a lot of the gap. But not all of it. Here is what $IQE has that $AXTI does not.

> Western defence moat. $IQE is Western domiciled. ITAR and export controls make it a qualified supplier for Western military radar, satcom, missile seekers. $AXTI manufactures in China. That same geography is a liability in Western defence. The export control sword cuts the opposite way for each of them.

> Proprietary process IP. $IQE has its own NanoImprint Lithography that patterns laser gratings at wafer scale, production qualified since 2018. That is value add beyond a raw wafer. A substrate is closer to a commodity sold on scarcity.

> Multi vector diversification. The same breadth the market dislikes is also a hedge. $AXTI lives and dies on one end market. $IQE has five.

> It already makes money at the EBITDA line. $AXTI does not yet.

The takeaway and my thoughts:

I am not saying $IQE should trade at $AXTI multiples. The duopoly, the Nasdaq listing, the clean single story and the backlog visibility may justify a real premium for $AXTI.

But a 10x sales gap between two adjacent layers of the same chain, where the cheaper one makes money, has Western defence regulatory protection, holds its own process IP, and grows more revenue, is worth sitting with. $IQE also trades at a fraction of its closest East Asian peer (LandMark Optoelectronics) - a whopping 12x forward sales gap.

What do you think, do you think $IQE is undervalued here? I certainly do.

Just my 2c. I am long $IQE.

- Leki 🐵

20

24

179

55,363

A lot of people seem to be linking the $WOLF selloff to the recent SemiAnalysis CPO headlines.

I'm not sure the connection is that straightforward.

> CPO is an optical story: co-packaged optics, lasers, photonics. $WOLF doesn't make any of that. If CPO adoption gets pushed out, that's primarily an optical timing debate.

> The same applies to most of the 800V discussion. The near-term debate is largely about in-rack power architecture, a layer much closer to $NVTS and Infineon than to $WOLF .

> The $WOLF AI angle, if it works, sits one layer up: grid-to-rack power, medium-voltage conversion, solid-state transformers and high-voltage SiC.

That's where $WOLF is positioning its 3.3kV modules and 10kV SiC MOSFETs.

So unless I'm missing something (please let me know), the recent CPO headlines don't seem to invalidate the actual AI power thesis behind $WOLF.

1

10

1,288

Please let me know if im missing something here @jasonschips @BULLOFBRITAIN @ParadisLabs @KawzInvests @citrini

401

Nicolas retweeted

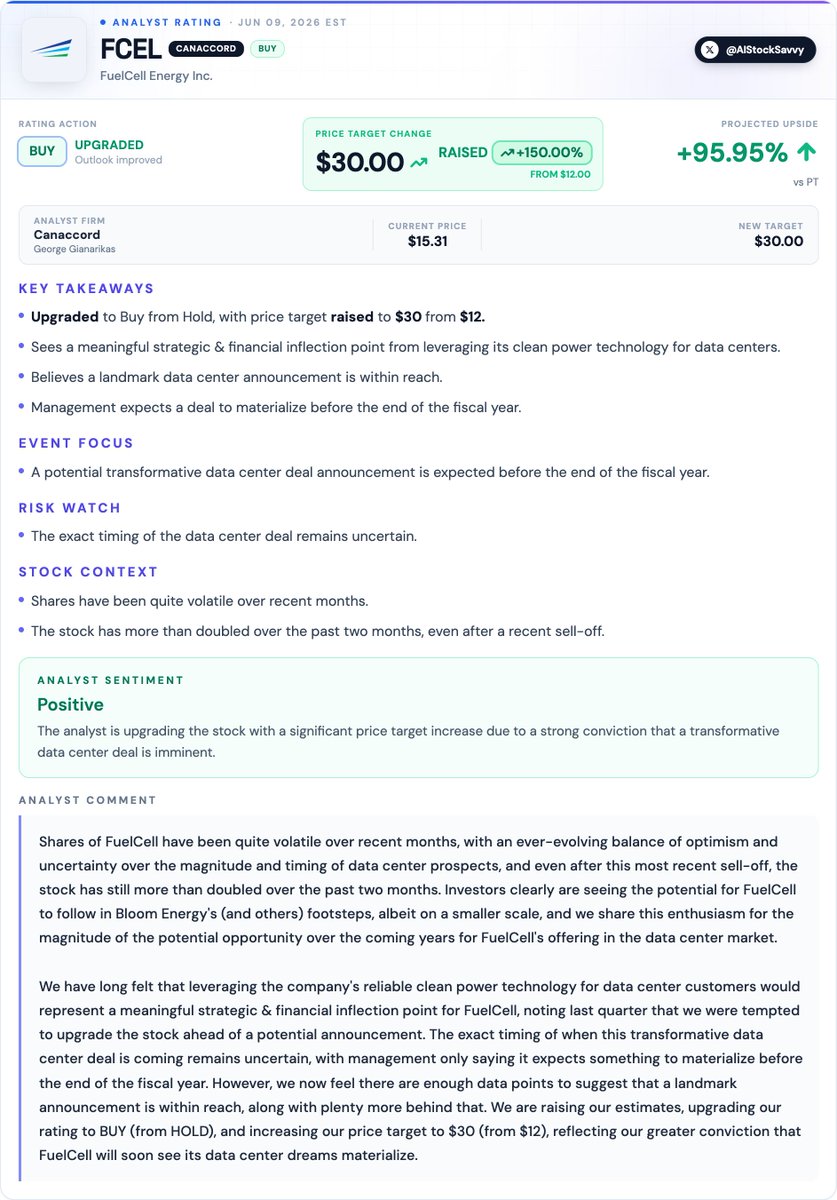

Jun 9

$FCEL PT upgrade to $30 by Canaccord this morning on the strong belief that "a landmark announcement is within reach" and the data center dream will materialize.

For those that follow me, we know it is coming.

Jun 9

$FCEL | Canaccord 𝐮𝐩𝐠𝐫𝐚𝐝𝐞𝐬 𝐅𝐮𝐞𝐥𝐂𝐞𝐥𝐥 𝐄𝐧𝐞𝐫𝐠𝐲 to 𝐁𝐮𝐲, 𝐦𝐨𝐫𝐞 𝐭𝐡𝐚𝐧 𝐝𝐨𝐮𝐛𝐥𝐞𝐬 𝐏𝐓 𝐭𝐨 $𝟑𝟎

Analyst sees a landmark data center announcement within reach, representing a meaningful strategic and financial inflection point for the company.

7

8

73

13,059

$WOLF Wolfspeed’s Solid 2026 Gets A GE Partnership Boost – CEO Says ‘High-Voltage Silicon Carbide Is Finally Production-Ready

“High-voltage silicon carbide is finally production-ready exactly as the market confronts a power-delivery crunch legacy silicon cannot solve,” said Robert Feurle, CEO at Wolfspeed.

5

4

26

2,628

$LPKF / $LPK Annual General Meeting was last week:

> CEO expected the x4 move only once $LPKF could announce "we've received orders to produce systems used in the production of high-performance chips." He's confident it comes THIS YEAR.

- AGM summary:

> They are in concrete negotiations with several customers for follow-on orders for machines intended for the planned ramp-up into volume production.

> $LPKF is expanding the LIDE opportunity: is moving beyond glass structuring into singulation and bonding for multilayer glass stacks. That increases the potential TAM.

> CPO solutions in 2029/2030

- The roadmap:

> LIDE ramp-up: 2027

> High-volume: 2029

The technology question is increasingly de-risked.

$LPKF looks like one of the most credible winners in glass structuring.

Full breakdown of the thesis below.

3

6

44

10,386

Nicolas retweeted

My highest conviction thesis this decade.

The investment research industry for retail investors (FinX, Substack etc.) is going to 10x fast.

And it's regardless of what the market ultimately does this decade.

Currently the market for institutional sell side research is estimated at ~$13.7B globally.

Now look at the mix from retail in the market itself.

Retail was 10% of US equity volume in 2010. 15% before COVID. In 2025 it's averaging 20-25% and it spiked north of 35% in April, an all time high per JPMorgan.

So if a third of all the capital hitting the market is retail and that market keeps growing?

That $13.7B research machine spends $0 advising 1/3 of the investor base aside from PTs they pull out without sharing ANY of their modelling.

Goldman isn't using their teams of Harvard grads to share the 2030 photonics TAM with retail.

So where does retail get its information? Right now, I see it as an insanely underserved market.

The status quo for retail is mostly slop articles generated by the big websites like Motley Fool and Yahoo farming SEO traffic giving 0 alpha.

The good stuff?

- There's a couple of Substacks probably doing 8 figures. Maybe a few dozen doing 7 figs at most.

- On FinX, there's a handful of maybe 20 influential X accounts (call it a few M followers combined) sharing actually high quality equity research.

This is peanuts. If 70% of the global capital right now is serviced by a $13B annual industry.

And FinX/Substack is only generating low hundreds of millions?

How can it not 10x here shortly as retail grows in influence and power?

Hence, I am all in.

40

36

460

64,260

" $IQE has no moat, $LITE and $COHR make their epi in-house "

People who say this are wrong:

> One: $LITE is an $IQE customer

In December 2025 $IQE announced a multi-year extension of its longstanding epiwafer supply agreement with $LITE for sensing.

So one of the two companies used to argue $IQE has no moat is literally buying epiwafers from $IQE.

$LITE makes its own epi for high-volume datacom InP. It buys from IQE for other products like sensing and VCSELs.

• $IQE is the neutral merchant supplier even the integrated players turn to.

> Two: $COHR doesn't even grow its own InP substrate. It buys the crystal externally and does epitaxy on top.

• $IQE makes its own InP substrate at Wafer Technology. So in the scarcest layer of the chain, $IQE is more vertically integrated than $COHR, not less.

So, What is the $IQE moat?

It's being the only global pure-play epitaxy supplier for everyone else, with 35 years of process know-how that can't be replicated and qualification lock-in measured in years.

1

23

2,028

Nicolas retweeted

Jun 2

Given $ABCL doubling in 2 months, I feel this is relevant to share.

It’s natural to feel excited when a company you hold starts ripping. However, people sometimes also become emotionally driven by it. Nothing changes sentiment like price.

Remember: If one loves it at its 52 week highs, they should really love it if it drops sharply for no reason.

All of this is to say that I maintain my position of “I have no idea what the stock will do in the near term. But I’m relatively confident in where I believe it will be in 3-5 years from now”. The doubling in 2 months doesn’t make me any more confident in the company than I felt prior hand. And if it falls back, it won’t make me any less confident. Price has nothing to do with it.

People will often claim to be long term but then become an emotional wreck when the stock drops for no reason. It may be helpful to ask yourself “do I have enough conviction to where the stock can drop 50% for no reason and I’d still be as confident as ever?” If the answer is no, then why do you hold it?

The conversation about a potential short squeeze gets brought up as of late. Maybe. Idk much about how that stuff works. All I know is that, generally speaking, easy come easy go. So if it’s because of a squeeze, I wouldn’t get my heart set on anything in the near term. “Yeah but we have catalysts coming soon”. This is true. Maybe we just stay hot going into Q3. All I know is that if the stock cools off and falls back down, IDGAF.. I’m buying more.

So anyway, I think it’s always good to keep the long term in mind. Yes, f*** the short sellers. Feels great watching the stock rip and burning the shorts. But this is just a blip in the big picture. I stay mentally prepared for anything in the near term. I look forward to the ph 2 readouts, in which we will hopefully get some serious legs behind the stock.

I hope this perspective is helpful for some. As always.. Long and strong 💪

May 15

In growth stocks, I beleive it’s often helpful to try and understand what a company’s price could realistically look like in 3-5 years based on whichever figures you believe are most relevant. Whether that’s future rev, acceleration, earnings margin expansion, or something else.

This is as opposed to trying to determine what the fair price should be based on today or this year’s numbers.

Look 3-5 years out and compare it to today’s price. That’s how I would determine if a stock is a buy today or not. I don’t believe a complex DCF should be necessary for this. If it’s a buy, it should be obvious. And I wouldn’t bother unless it’s a screaming buy.

This is very difficult to do, which is one of the reasons why I pass up on pretty much every growth stock (except the ones I own, of course).

Sure, you might (likely you will) be down on your position after you initial entry, but the long-term view will help you navigate the price better in the near term. I’ve watched investors fumble the bag because they were focused too much on the near term and convinced themselves the stock was overvalued and would drop, only to watch the stock run away and never look back, with “valuation” catching up after the fact.

The opposite argument can be made about those who round tripped their gains because their company was all hype and no substance. The substance must be there.

I beleive this viewpoint is most applicable for generational companies growing fast. And you better be right that it’s “generational”… which is really hard. Nobody has all the answers.

Psychologically, it’s much easier to hold a company through “overvaluation” once it’s already a multibagger for you rather than entering the stock when it’s already ran up multi-fold and is considered “overvalued” on paper. Volatility is not for the weak… something to consider.

Opportunity cost should also be taken into consideration. Holding a stock that you’re already up 20x on and seeking for it to double again is way different than entering a stock that already went up 20x and seeking for it to 20x again.

This mindset is why I’m up 15x on PLTR. At one point, I was up 10x and the entire market is screaming it’s overvalued. I don’t care because I believe I’ll be up 100x one day… plenty of room to grow. Next thing I know I’m up 24x and the whole market is still screaming overvalued. Still don’t care because I believe the company is still on track to give me a 100x return on my initial investment one day. Today, the stock has fallen by nearly 35% and I’m back to being up ~16x, except the PE multiple has been slashed by like 70% YoY because the company is explosively growing. Still don’t care about price action because I believe I’m on track to be up 100x on my initial investment one day thanks to how company fundamentals are progressing.

So in summary, IMO, when holding a generational company with intact thesis, it’s sometimes best to accept the risk of “overvaluation” in the near term in exchange for being able to see it through to the end without letting go too early. This becomes much easier if you get in when theres a misperception in the market and it’s selling at a big discount, which is rare. Stocks go through periods of overvaluation and undervaluation, and it’s difficult to predict the near-term price or time when the tide will turn. With the generational companies… just hold. In the end, the stock will track fundamentals over the long run.

Hold elite companies for long periods of time. Track them closely. Ensure the thesis is intact. Be patient.

Investing is hard. It’s not recommended to pick individual stocks. Yet here we are. If one is going to do so, I believe this is a rational approach. I don’t claim it’s the only way or smartest. This is my way. I don’t know much in the big picture and am continually learning. Everyone’s situation is different. This is the viewpoint I’ve come to have over the 6 or so years I’ve been in the market.

Long and strong

22

19

146

19,990

It must be tough on days like these for someone with a large portfolio, but not quite at @Sandeman52 level, still having to show up at the office every morning.

You are in that weird middle ground where you have serious money ($1–2M), but not enough to comfortably retire yet.

Fortunately that's still not my problem 😂

1

200