Media via Telco || Forgot more programming than most || home is 🇦🇺 / 🇺🇲 / 🌍

Joined September 2009

- Tweets 7,893

- Following 2,030

- Followers 674

- Likes 29,055

401 Photos and videos

J retweeted

Jun 13

The frontier model problem is a breadth versus depth problem. Consumer needs breadth, the wider your aperture, the more relevant your model. Breadth suffers from a false positive problem, it ranges between 10-30%, with clever prompting and checks you can hit the lower end of the range, but it tends to be free or subsidized. Consumers still seemm to be satisfied, and consumption growing!

However, Frontier Models harvest the usage data to inform future models.

On the other hand. The enterprise wants depth, their tolerance for error is low, this needs more context data, training and harnesses and guardrails is high. The frontier models aren't ready yet to provide that, hence the FDEs, and solutions consultants who build that capacity for every enterprise. But enterprise is the only route ATM to build a sustainable economic model.

The risk, consumer losses mount. Enterprise value accrues to solution providers. In the meanwhile, models are aggressively pursuing Enterprise profit pools, while solution providers are building orchestrators to arbitrage token pricing. So there's many a push and a pull in the equation.

If will be an epic battle, my instinct tells me, value could accrue to the application and proprietary data layers.

Will be fun to watch.

Jun 13

Game theory from here is super interesting:

Original Mags (Google, Amazon, Microsoft, Meta) now have a serious non-zero opportunity to tank the frontier labs.

Go to the government, kneecap the labs’ motion of putting the latest models out in the wild, become the trusted gatekeeper between the labs and the public at large (including internationally) by having the labs go through their clouds (AWS, GCP, Azure) and implement strict KYC to seal the deal.

The frontier labs should have seen this coming years ago and implemented a robust KYC for just this moment. The fact they didn’t is kind of concerning.

Why did they not do it?

Best guess is because it would have changed the run-rate revenues (downward) which would have then changed funding dynamics - lower valuations, more dilution, less secondary.

A valuation reset may happen now anyways, except the labs may end up with less control and more restrictions at the end of it. At the same time, everyone is already clamoring about token prices of the old models from the labs anyways…

This couldn’t be a better setup for open source and neoclouds. Big question is can they meet the moment?

There are too few of them and their progress seems sporadic at best.

44

63

543

190,805

J retweeted

Jun 11

The brilliant Eric @bonabeau creates a scenario engine for the IPOs of SpaceX, OpenAI, and Anthropic. He combines fast-entry index inclusion demand, pro-rata funding sales from existing constituents, discretionary retail rotation out of incumbent equities, and lock-up-driven supply releases. The engine allows you to tune the parameters. No answers but a lot to think about. Full paper in tab at the top right: spacexipo.bonabeauapps.com/

4

13

118

21,185

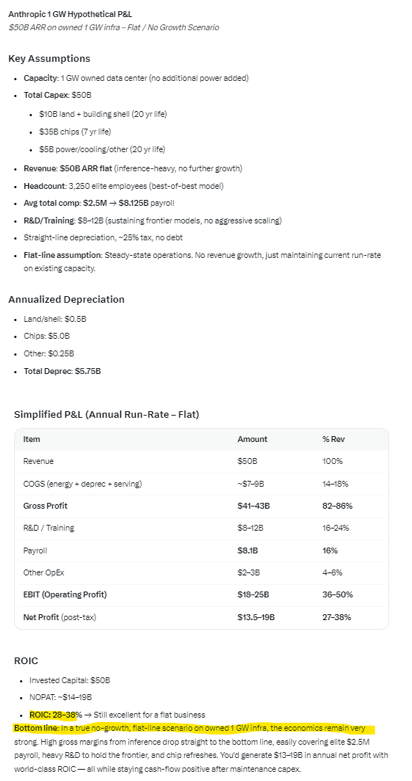

Model economics looks great at $50B ARR.... If not for the red queens

Jun 10

Anthropic is currently like ~$50B ARR on an estimated 1GW, which Jensen says is $50B (shell, cooling, chips, etc).

If you assume for a second that Anthropic decides not grow and just runs at ~$50B ARR (an exercise to just sanity check ROIC), the math looks quite good. 25% ROIC?

Assumptions below. Where are my assumptions off? Maybe comp ($2.5M per employee?)?

@GavinSBaker @chamath @DavidSacks @friedberg

68

Seeking out the narrative violation has always sharpened thinking. It matters more than ever now: where social media once amplified consensus (2013–2023), LLMs now ossify it, averaging the web into a single agreeable voice

bedrockcap.com/letter

41

Opposing take: Can port and should are not the same

1) CUDA is also improving at AI speeds getting more performance with every release

2) if it was easy to do so economically then more Chinese players than just deepseek would have ported to Huawei by now

May 30

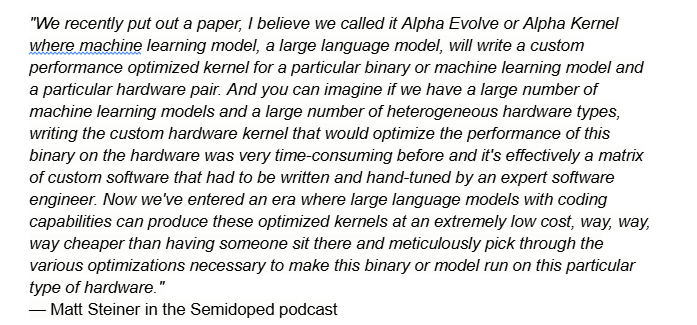

The biggest irony in AI right now is that $NVDA basically enabled the AI boom, and now vibecoding in diminishing the moat around CUDA.

@semidoped had an interview with $META's head of ad infra who talked about LLMs rewriting their kernels so that the same models run across GPUs, ASICs, etc. The main advantage of cuda was that it was so much easier to optimize your model to Nvidia's hardware.

Still think cuda is excellent and has a deeper base, but writing on the wall is in? Jensen mostly talks about TCO these days as their moat.

2

4

2,071

Up 30% pre-market $HUT took financing and offtake risk off the table.

20% of float was short into earnings.

Lots of fun.

May 6

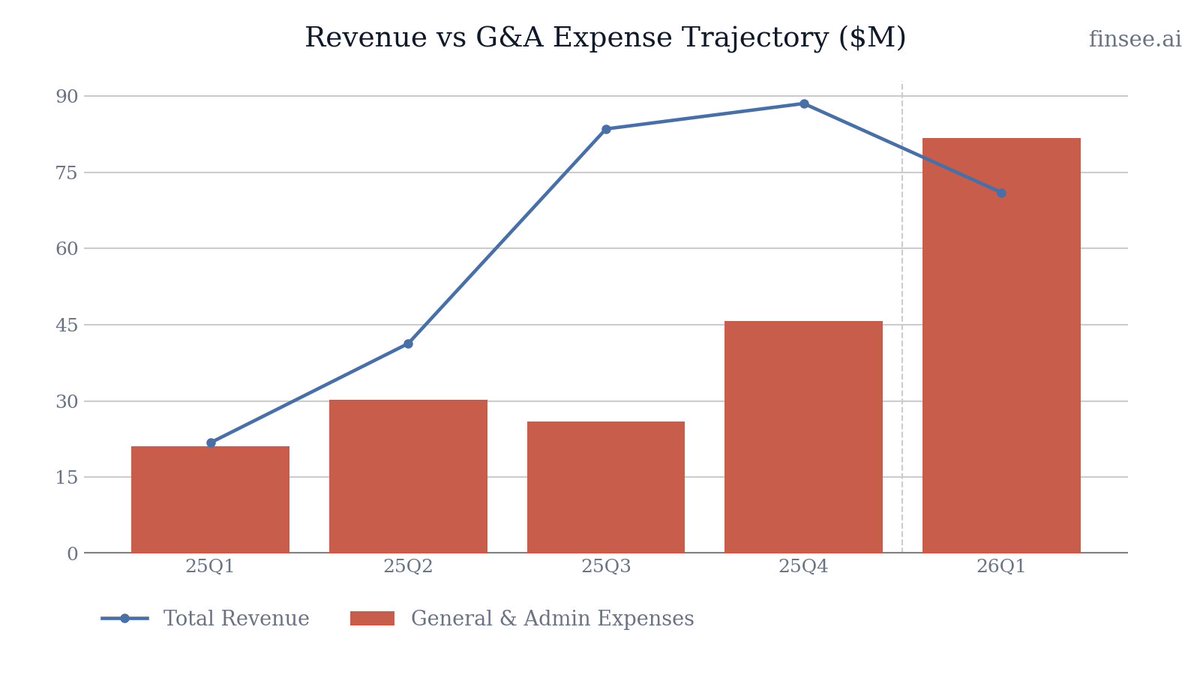

$HUT Q1 2026 earnings: Historic AI Commercialization Masks Ugly Near-Term Financials

Hut 8 is executing one of the most dramatic strategic pivots in modern infrastructure, morphing from a volatile Bitcoin miner into a hyperscale AI data center landlord. The current financial snapshot is abysmal: revenue reversed sequentially, plunging to $71.0M, while net losses deepened to $253.1M. But looking only at the income statement completely misses the story. Management successfully locked in $16.8 billion in triple-net, take-or-pay contracted lease revenue across two AI campuses. By securing a historic $3.25B investment-grade construction bond for River Bend, Hut 8 effectively eliminated financing risk for its flagship project. The company is trading current profitability for massive, de-risked future cash flows.

Full article with charts - link in bio

🐂 𝐁𝐮𝐥𝐥 𝐂𝐚𝐬𝐞

• 𝐌𝐚𝐬𝐬𝐢𝐯𝐞 𝐂𝐨𝐧𝐭𝐫𝐚𝐜𝐭𝐞𝐝 𝐂𝐚𝐬𝐡 𝐅𝐥𝐨𝐰𝐬 — The company has secured $16.8 billion in base-term contract value from high-investment-grade tenants on a triple-net, take-or-pay basis, transforming its valuation profile.

• 𝐅𝐢𝐧𝐚𝐧𝐜𝐢𝐧𝐠 𝐑𝐢𝐬𝐤 𝐄𝐥𝐢𝐦𝐢𝐧𝐚𝐭𝐞𝐝 — Accessing the investment-grade construction bond market for a $3.25B, 95% loan-to-cost facility on a non-recourse basis proves the viability of Hut 8's capital-intensive AI pivot.

🐻 𝐁𝐞𝐚𝐫 𝐂𝐚𝐬𝐞

• 𝐄𝐱𝐩𝐞𝐧𝐬𝐞 𝐁𝐥𝐨𝐚𝐭 — General and Administrative expenses hit a staggering $81.7M this quarter, eclipsing total revenue. Operational cash burn is severe outside of the AI development narrative.

• 𝐋𝐞𝐠𝐚𝐜𝐲 𝐌𝐢𝐧𝐢𝐧𝐠 𝐕𝐨𝐥𝐚𝐭𝐢𝐥𝐢𝐭𝐲 — A $295.7M loss on digital assets and a sequential decline in Compute segment revenues show the legacy crypto business remains a significant drag on reported earnings.

⚖️ 𝐕𝐞𝐫𝐝𝐢𝐜𝐭: 🟢

Bullish. The near-term financials are undeniably poor, but securing $16.8B in guaranteed, high-margin revenue and a first-of-its-kind $3.25B non-recourse financing package fundamentally de-risks the company's long-term business model.

𝐊𝐞𝐲 𝐓𝐡𝐞𝐦𝐞𝐬

🟢🟢 𝐁𝐞𝐚𝐜𝐨𝐧 𝐏𝐨𝐢𝐧𝐭 𝐕𝐚𝐥𝐢𝐝𝐚𝐭𝐞𝐬 𝐏𝐢𝐩𝐞𝐥𝐢𝐧𝐞 𝐑𝐞𝐩𝐞𝐚𝐭𝐚𝐛𝐢𝐥𝐢𝐭𝐲 [NEW]

The commercialization of the Beacon Point campus represents a massive structural win. By securing a 15-year, 352 MW lease representing $9.8 billion in base-term contract value within five months of their initial River Bend deal, management proved their power-first origination model is repeatable across different geographies and counterparties.

🟢🟢 𝐇𝐢𝐬𝐭𝐨𝐫𝐢𝐜 𝐏𝐫𝐨𝐣𝐞𝐜𝐭 𝐅𝐢𝐧𝐚𝐧𝐜𝐢𝐧𝐠 𝐔𝐧𝐥𝐨𝐜𝐤𝐬 𝐭𝐡𝐞 𝐌𝐨𝐝𝐞𝐥 [NEW]

Hut 8 closed a $3.25 billion fully amortizing, 16.5-year investment-grade senior secured note to finance the River Bend construction. Achieving ~95% loan-to-cost (up from the initially contemplated 85%) on a non-dilutive, non-recourse basis is a watershed moment. It essentially fully funds the project, returning $184M of equity to Hut 8 to fuel further development.

🟢 𝐁𝐚𝐥𝐚𝐧𝐜𝐞 𝐒𝐡𝐞𝐞𝐭 𝐃𝐞-𝐫𝐢𝐬𝐤𝐢𝐧𝐠 & 𝐒𝐢𝐦𝐩𝐥𝐢𝐟𝐢𝐜𝐚𝐭𝐢𝐨𝐧

Management executed several key moves to clean up the parent balance sheet. They sold a 310 MW natural gas power plant portfolio, unencumbered 3,300 Bitcoin, and refinanced their credit facility, lowering the interest rate from 9.0% to 7.0%. Assuming the Coatue convertible note converts, parent-level recourse debt will be practically zero.

🟢🟢 𝐌𝐚𝐜𝐫𝐨 𝐒𝐜𝐚𝐫𝐜𝐢𝐭𝐲: 𝐏𝐨𝐰𝐞𝐫 𝐚𝐬 𝐭𝐡𝐞 𝐅𝐨𝐮𝐧𝐝𝐚𝐭𝐢𝐨𝐧𝐚𝐥 𝐋𝐚𝐲𝐞𝐫

The entire strategic pivot is underpinned by a massive macro constraint: grid power scarcity for AI. Management is successfully exploiting the fact that securing front-of-the-meter, large-scale utility capacity is harder than securing GPUs, allowing them to dictate triple-net, take-or-pay terms to hyperscalers.

🟢 𝐇𝐢𝐠𝐡-𝐃𝐞𝐧𝐬𝐢𝐭𝐲 𝐀𝐈 𝐂𝐨𝐨𝐥𝐢𝐧𝐠 𝐈𝐧𝐧𝐨𝐯𝐚𝐭𝐢𝐨𝐧

While not explicitly highlighted in Q1 revenue, Hut 8's underlying technological transition toward proprietary direct-to-chip liquid cooling infrastructure (previously showcased at the Vega site) is critical. This design accommodates extreme heat densities required by next-generation AI workloads, serving as the technical foundation for these massive multi-billion dollar leases.

🔴🔴 𝐎𝐯𝐞𝐫𝐡𝐞𝐚𝐝 𝐁𝐥𝐨𝐚𝐭 𝐂𝐨𝐧𝐭𝐫𝐚𝐝𝐢𝐜𝐭𝐬 𝐄𝐟𝐟𝐢𝐜𝐢𝐞𝐧𝐜𝐲 𝐂𝐥𝐚𝐢𝐦𝐬 [NEW]

CEO Asher Genoot emphasized executing with 'uncompromising discipline,' yet the data tells a completely different story. General and Administrative (G&A) expenses accelerated violently to $81.7 million in Q1—a 78% sequential increase and significantly higher than the company's total revenue of $71.0 million. This level of corporate bloat is unsustainable and contradicts the narrative of operational rigor.

🔴 𝐂𝐨𝐦𝐩𝐮𝐭𝐞 𝐒𝐞𝐠𝐦𝐞𝐧𝐭 𝐑𝐞𝐯𝐞𝐫𝐬𝐢𝐧𝐠 𝐓𝐫𝐚𝐣𝐞𝐜𝐭𝐨𝐫𝐲 [NEW]

After four quarters of rapid acceleration, the Compute segment (Bitcoin Mining, AI Cloud, Traditional Cloud) reversed course. Revenue dropped sequentially from $81.9M in 25Q4 to $66.0M in 26Q1. While the AI transition is the future, this segment still pays the bills today, and its sudden contraction exacerbates the company's current operating losses.

🔴 𝐄𝐱𝐭𝐫𝐞𝐦𝐞 𝐄𝐚𝐫𝐧𝐢𝐧𝐠𝐬 𝐕𝐨𝐥𝐚𝐭𝐢𝐥𝐢𝐭𝐲 𝐟𝐫𝐨𝐦 𝐃𝐢𝐠𝐢𝐭𝐚𝐥 𝐀𝐬𝐬𝐞𝐭𝐬

The consolidation of American Bitcoin means Hut 8's GAAP earnings remain hostage to Bitcoin price fluctuations. Q1 saw a massive $295.7 million non-cash loss on digital assets, driving the headline net loss to $253.1M. Until the AI revenue streams come online (starting Q2 2027), this volatility will continue to obscure the underlying business performance.

𝐎𝐭𝐡𝐞𝐫 𝐊𝐏𝐈𝐬

𝐓𝐨𝐭𝐚𝐥 𝐋𝐢𝐪𝐮𝐢𝐝𝐢𝐭𝐲 (𝐂𝐚𝐬𝐡 𝐚𝐧𝐝 𝐃𝐢𝐠𝐢𝐭𝐚𝐥 𝐀𝐬𝐬𝐞𝐭𝐬): $1.3 billion

Stable. The combined cash and Bitcoin reserve across Hut 8 ($795.6M) and American Bitcoin ($489.0M) remains a vital strategic buffer to fund the massive upfront capital requirements of the 8,375 MW development pipeline before project financing kicks in.

𝐀𝐝𝐣𝐮𝐬𝐭𝐞𝐝 𝐄𝐁𝐈𝐓𝐃𝐀: -$250.5 million

Decelerating. Adjusted EBITDA worsened from -$117.7 million a year ago, primarily due to the inclusion of extreme digital asset mark-to-market losses and the explosion in general and administrative overhead.

𝐆𝐮𝐢𝐝𝐚𝐧𝐜𝐞

𝐃𝐞𝐯𝐞𝐥𝐨𝐩𝐦𝐞𝐧𝐭 𝐏𝐢𝐩𝐞𝐥𝐢𝐧𝐞: 8,375 MW

Stable. The pipeline remains massive, consisting of 5,315 MW under diligence, 1,680 MW under exclusivity, 550 MW under development, and 830 MW under construction. This provides an immense runway for future multi-billion dollar lease announcements.

𝐑𝐢𝐯𝐞𝐫 𝐁𝐞𝐧𝐝 𝐃𝐞𝐥𝐢𝐯𝐞𝐫𝐲 𝐓𝐢𝐦𝐞𝐥𝐢𝐧𝐞: Q2 2027

Stable. Management reaffirmed that construction is advancing toward a Q2 2027 delivery for the 330 MW AI campus, which will trigger the commencement of the $7.0 billion Fluidstack/Google lease payments.

𝐊𝐞𝐲 𝐐𝐮𝐞𝐬𝐭𝐢𝐨𝐧𝐬

𝐄𝐱𝐩𝐥𝐚𝐢𝐧𝐢𝐧𝐠 𝐭𝐡𝐞 𝐆&𝐀 𝐄𝐱𝐩𝐥𝐨𝐬𝐢𝐨𝐧

General and Administrative expenses surged to $81.7M, surpassing total revenue. How much of this is related to one-time transaction fees for the Beacon Point and bond deals versus a structural increase in run-rate overhead?

𝐂𝐨𝐦𝐩𝐮𝐭𝐞 𝐒𝐞𝐠𝐦𝐞𝐧𝐭 𝐂𝐨𝐧𝐭𝐫𝐚𝐜𝐭𝐢𝐨𝐧

Compute revenue fell sequentially by $15.9M. Was this driven by lower Bitcoin prices, decreased hash rate production, or a slowdown in the legacy AI Cloud/Traditional Cloud divisions?

𝐁𝐞𝐚𝐜𝐨𝐧 𝐏𝐨𝐢𝐧𝐭 𝐓𝐢𝐦𝐞𝐥𝐢𝐧𝐞 𝐚𝐧𝐝 𝐅𝐢𝐧𝐚𝐧𝐜𝐢𝐧𝐠

With the 15-year lease signed, what is the expected delivery date for the Beacon Point campus, and will it follow the identical 95% LTC project financing blueprint utilized for River Bend?

616

Alex throwing some haymakers.

Mar 19

It is too early to drink in Asian time and that is an absolute tragedy having written this syncretica.substack.com/p/qu…

138

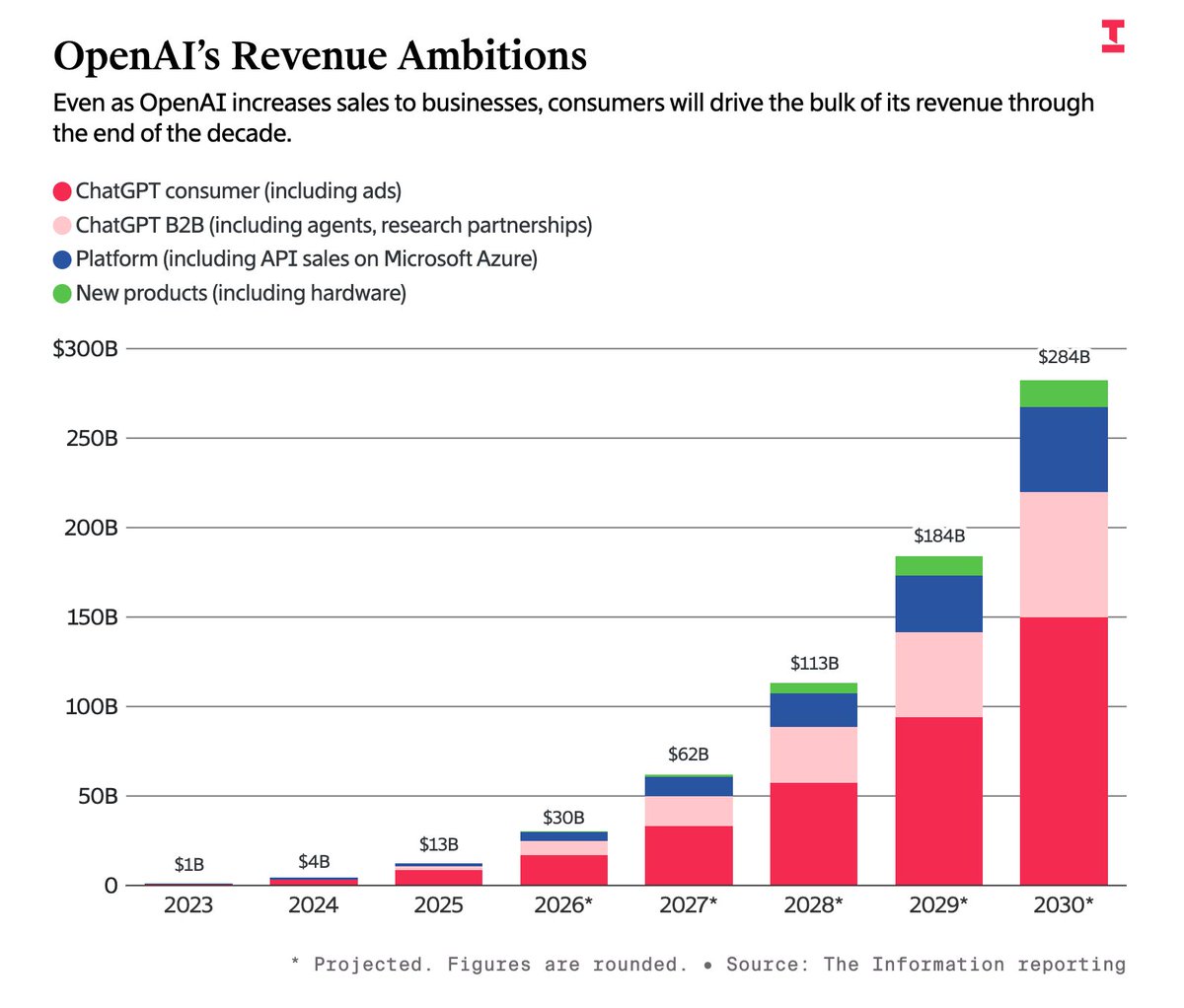

Guessing $40bn ARR by December 2026 so about 2x growth by end of year. Solid but I think a bit of a -ve indicator looking at 2027 Capex estimates.

A double scoop day w/ the latest on OpenAI financials.

Details include:

- OpenAI raises rev forecasts for next 5 years by 27%

- But will burn 2x as much cash thru 2030 than previously predicted

- 2025 gross margins down vs. 2024

- New info on device revenue forecasts!

142

$META tackling clawdbot in a simpler way for the masses

Too bad can't block competitors from using WhatsApp (in many markets)

Feb 16

Oh, and this is just the beginning 😏

Coming up:

– Create your own specialized agents and plug them into any group chat.

– Landing on WhatsApp, LINE, Slack, Discord very soon.

– Native Windows & Mac apps that let Manus operate your computer (think our Browser Operator… but way more powerful).

– And yeah… a LOT more already in the shipping pipeline.

Big updates dropping over the next 30 days.

Let’s build. 🚀

181

J retweeted

Feb 8

Right wing free speech absolutism is the most dishonest grift in American politics.

157

1,552

10,122

314,879

J retweeted

Feb 4

Crazy diss from Anthropic aimed at OpenAI for introducing ads in ChatGPT

Who is running the Ads department at Anthropic??

64

115

1,563

244,894

SpaceX is delivering xAI out of a bundle of debt inherited from X/Twitter buyout

This severely dilutes the equity story from a clean "Space" thematic to a mix of social, AI, and Space

Feb 3

Just last week @SpaceX was floating a $1.5T valuation for its IPO. Now an implied $1.0T in its merger with @xai?

2

213

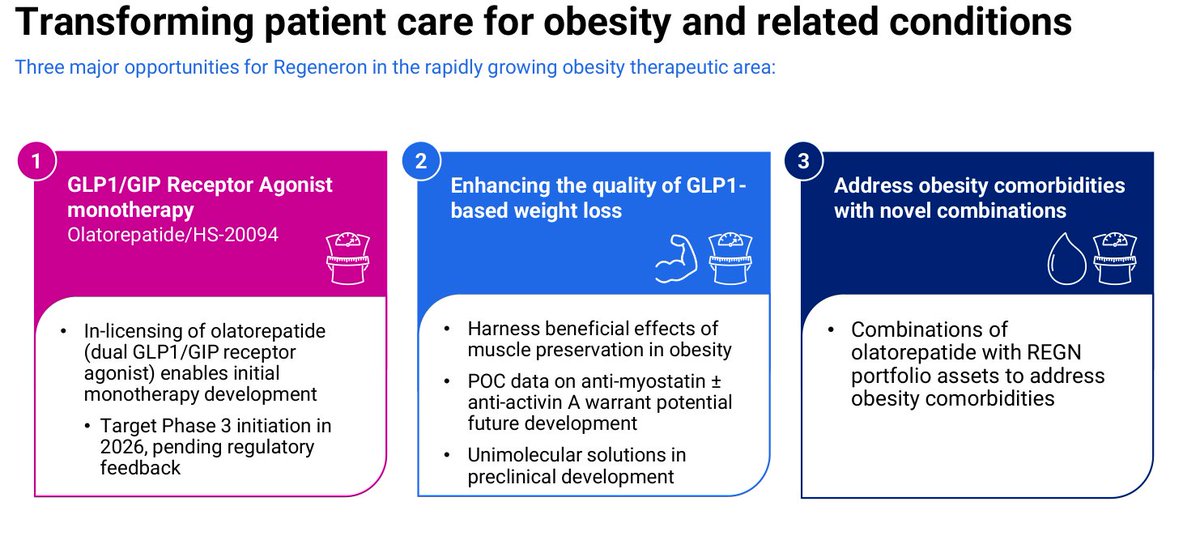

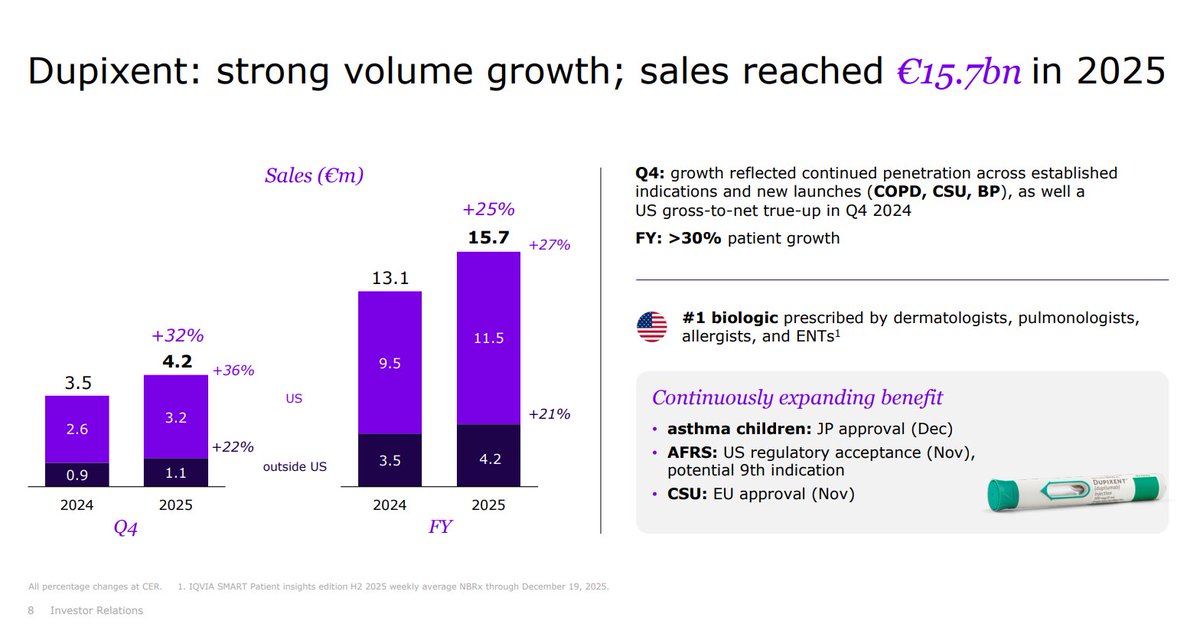

Dupixent just had a $5bn quarter with new launches doing $300m (based on uplift of sales)

Jan 29

1

151