Joined June 2009

- Tweets 35,064

- Following 2,056

- Followers 1,088

- Likes 33,556

187 Photos and videos

Chris Coomber retweeted

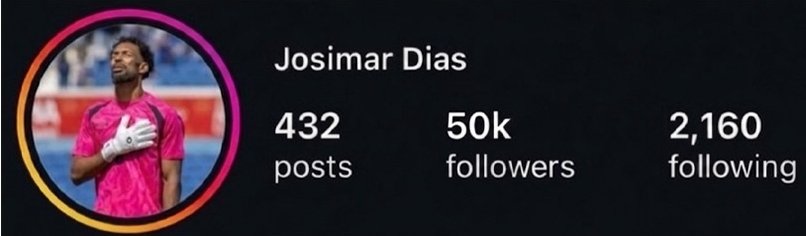

Cape Verde goalkeeper Josimar Vozinha had 50K Instagram followers before the match against Spain. After the game, he had 4.9 million followers, and now he has 9.6 million.

He said his mum couldn't travel to the US because of visa issues, and his grandparents, who raised him, couldn't be there because they had passed away.

8

54

639

18,896

Chris Coomber retweeted

Ten years ago today Farage unveiled his racist "Breaking Point" poster.

Within hours a far-right sympathiser murdered the MP Jo Cox.

Instead of apologising, Farage went on to verbally attack her husband.

Farage has always been scum.

Never Vote Reform.

163

2,352

6,388

58,770

Trump is World Class at unintended yet entirely predictable consequences, as well as horrific intended consequences. Clown.

Jun 15

The reflecting pool is now green, the color of all the money wasted on it. Painting the bottom has apparently heated the water and accelerated algae growth. Pure Genius.

people.com/reflecting-pool-g…

13

Chris Coomber retweeted

Jun 15

The reflecting pool is now green, the color of all the money wasted on it. Painting the bottom has apparently heated the water and accelerated algae growth. Pure Genius.

people.com/reflecting-pool-g…

309

1,190

7,136

200,695

Chris Coomber retweeted

Grow up. Homophobic innuendo isn’t going to get you out of this one.

Neither is pretending you’re a victim of antisemitism, which you conflate with opposing genocide.

You’re a government minister trying to get your political opponent arrested

I’m more disturbed that you spent the night thinking about me.

The antisemitism I’ve woken to from the extreme left over night is utterly unhinged, shameful and disturbing.

171

775

6,715

193,491

Chris Coomber retweeted

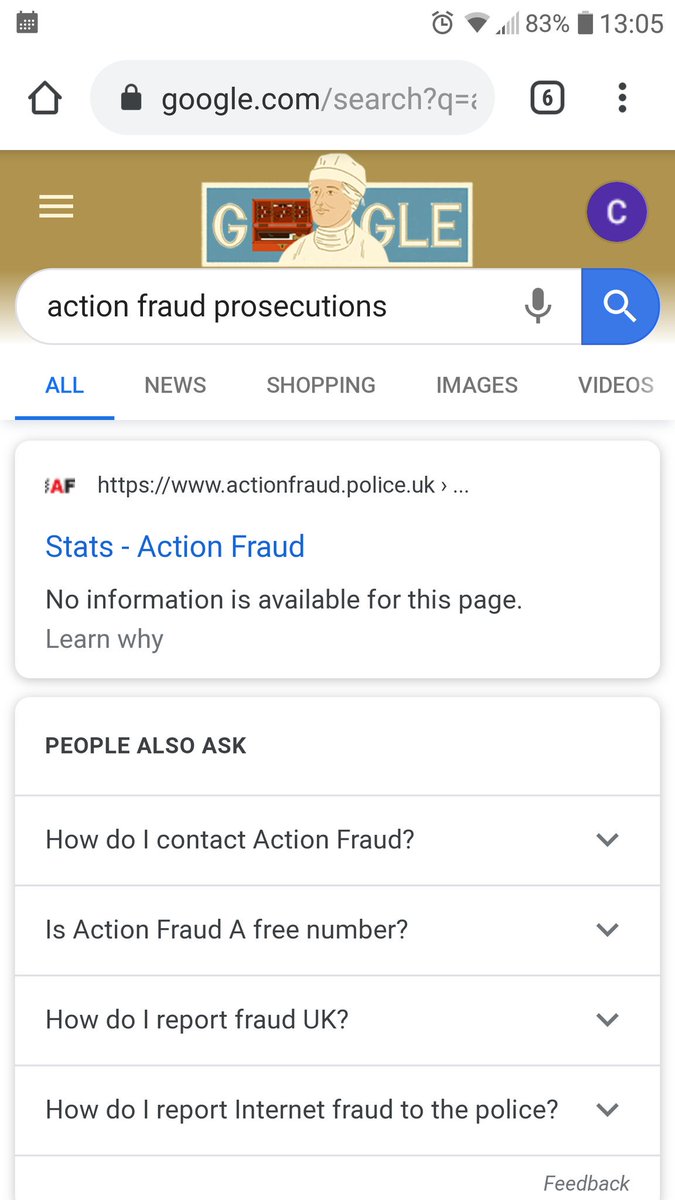

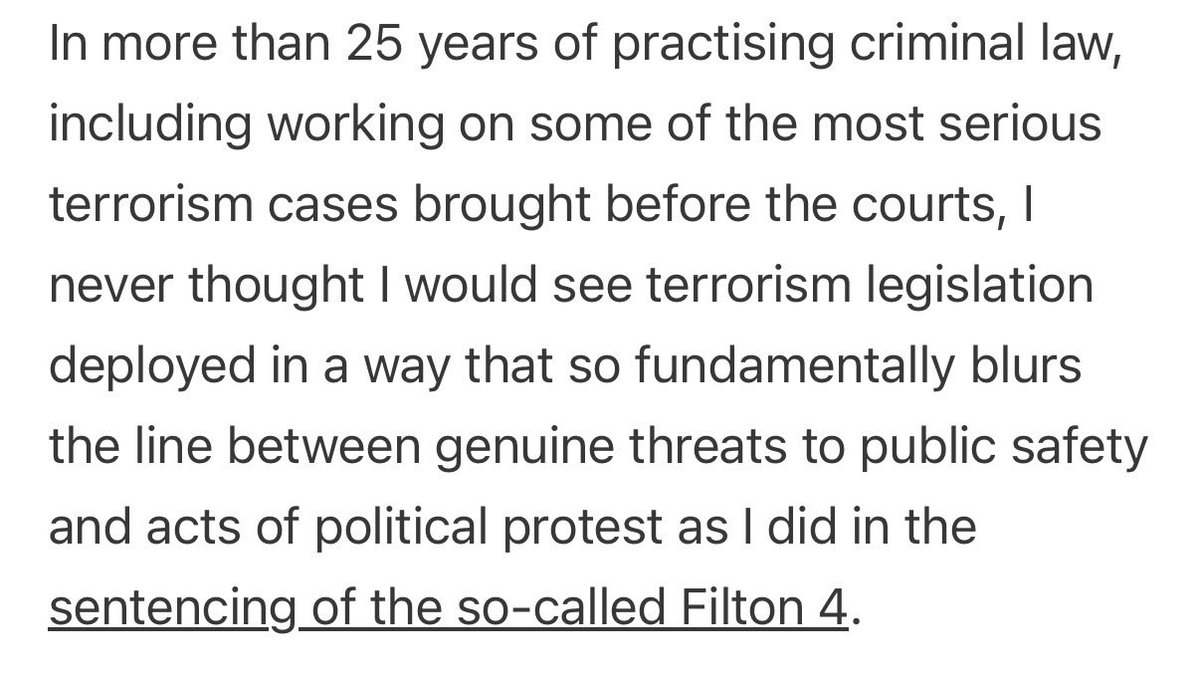

When the Filton trial didn’t get the verdict the state wanted, it bent the system to produce the desired results, aka corrupt official misconduct aftershock.media/the-great-b…

71

781

1,462

12,468

Chris Coomber retweeted

Jun 16

Benjamin Netanyahu can't attend United Nations sessions !!

TheMayor of New York Zohran Mamdani, has promised to get him arrested if he sets foot in the City

229

5,107

28,028

265,957

Chris Coomber retweeted

14h

Disabled children don't stop being disabled at 16, however, nearly a quarter of young people on child DLA failed the assessment for PIP

By @RachelCDailey_

thecanary.co/uk/2026/06/16/d…

6

162

235

3,541

Chris Coomber retweeted

You’ve got to admire the front of this man.

@MikeTappTweets tries to get the only Jewish party leader arrested because of his opposition to genocide.

Then he claims to be a victim of antisemitism when he’s called out on it.

These people are so nauseatingly awful!!

27

225

1,263

19,005

Chris Coomber retweeted

Y’all, not to be a huge nerd but for the reflecting pool you would need a minimum of about 8,000 liters of 12% hydrogen peroxide to reach the 50 parts per million concentration to kill algae…

Is this what happens when you have 0 scientists in your administration?

They're literally dumping hydrogen peroxide into the reflecting pool this morning... 😳

2,128

12,467

129,793

5,586,907

Chris Coomber retweeted

Jun 15

After a lifelong career in "justice," all these people have ended up doing is the government's dirty political work to cover up for a genocide.

I feel like I've just watched two court cases which were nothing more than pre-decided political theatre.

80

1,250

3,165

18,727

Chris Coomber retweeted

Jun 15

"Sorry, you can't play in the World Cup because Mark was crap at geography at school."

Jun 14

Shouldn't one of the requirements for a country to qualify to play in the World Cup that it be a country that people have heard of?

159

14,624

181,885

2,447,497

Chris Coomber retweeted

Jun 15

From a leading British lawyer, for Zeteo UK today:

zeteonews.co.uk/p/filton-4-p…

168

1,177

2,555

56,434

Chris Coomber retweeted

Jun 15

Blaming asylum seekers for homelessness? What about the 720,000 empty homes in England, and the 1,627,450 second homes in England alone.

Blaming asylum seekers for expensive food shops? What about the £3,100,000,000 profit Tesco made last year?

Blaming asylum seekers for expensive energy bills? What about the £438,000,000,000 made by just 20 energy companies in profit?

Blaming immigrants for not getting an NHS appointment? What about the 260,000 migrant workers keeping the NHS going? And what about the 25% real term cut in NHS funding, think that could do it?

Blaming people on welfare for a lack of money to fund the NHS? What about the £36,000,000,000 tax gap due to avoidance and evasion by the elite?

It's time to realise it's not immigrants, asylum seekers or people on welfare causing you any harm, it's capitalism and the mega rich hoarding all the wealth.

1,107

1,602

3,757

88,490

Chris Coomber retweeted

Jun 15

An insane stat

Jun 15

The average terror suspect arrested in England and Wales is now a white woman in her 50s as a result of the Palestine Action ban

2,800 arrests were made for supporting the group in 6 months -surpassing number of terror suspects detained in previous decade

inews.co.uk/news/politics/uk…

164

1,671

10,708

279,983

Chris Coomber retweeted

Jun 15

The Lady Chief Justice went to private school and Cambridge University but apparently has zero knowledge of history.

Jun 15

The Lady Chief Justice said proscription of Palestine Action “struck a fair balance” and that PA is not a peaceful civil disobedience group like the Suffragettes

271

1,357

5,236

117,446

Chris Coomber retweeted

Jun 13

This is part of my explanation in my report how I survived & then started taking my ex 'friends' at the banks on to protect maligned SME's...

My introduction to the weaponisation of insolvency came in 2008/09 when I became a victim of lending fraud at Barclays Bank through two small property development companies that I co-owned. Ironically, I had previously worked for Barclays as a financial adviser.

The relationship manager, whom I will call Mr K, repeatedly assured me in early 2007 that funding applications for the purchase and development of two properties had been submitted, approved and were "good to go". In reality, no applications had been made to Barclays' credit team. While funding was provided for the property purchases, the promised development finance never materialised, leaving me servicing loans on two empty buildings and under growing financial pressure as we headed towards the financial crisis in 2008.

When I challenged Barclays, the issue quickly ceased to be about the bank's conduct and became a question of survival. Senior staff attended my office and made it clear they were prepared to place my companies into administration, as they had already done with other affected customers. I replied that I was not an idiot and no court would believe I had knowingly purchased more than 10,000 square feet of property simply to leave it undeveloped and informed them that I intended to sue the bank.

The local Barclays Director then put his head in his hands and said: "Steve, you would win. We have companies going bust all over Hull — it's such a mess we've had to put a whole team on it."

I later learned that Mr K had been using his lending authority to approve transactions without properly disclosing their purpose to the credit team to meet his sales targets. According to the manager who later inherited his portfolio, Barclays' response was not to compensate affected customers but to make Mr K reconstruct the credit files retrospectively, presenting lending as though it had been properly approved before quietly moving him on.

That experience taught me a lesson I would encounter repeatedly over the years. Once serious allegations are raised against a large financial institution, the dispute can quickly shift from the conduct of the bank to the survival of the customer. It was my first real glimpse of how insolvency and the threat of insolvency can be used to contain complaints, manage reputational risk and place victims under immense pressure to settle.

The deception caused me substantial financial loss, delays and pressure that I would not otherwise have faced. Barclays having admitted Mr K’s dishonesty to me, eventually agreed to support the two small developments in 2009, when no other lenders would have done so. Most of Mr K’s other victims however, had already lost their businesses and livelihoods.

The consequences were for me were still severe. My losses ran well into six figures, larger developments had to be abandoned or restructured, and the prolonged stress ultimately caused me to collapse and undergo extensive medical investigations. While I eventually recovered, albeit with some long term effects, the episode demonstrated how financial misconduct can inflict damage far beyond the balance sheet.

Not all the victims were so fortunate. One, whom I shall refer to as David M, was a well-known local businessman. After his companies were pushed into administration following the same unauthorised lending and false promises of funding by Mr K, Barclays and its appointed administrators then pursued his personal assets under a personal guarantee.

As the pressure on David increased, I assisted him informally, despite the obvious risks of doing so while I still banked and held mortgages with Barclays. Because he was a prominent figure in the local business community, his continuing complaints were causing the bank reputational difficulties.

In June 2010, my solicitor telephoned to warn me about a conversation that had taken place at a solicitors' lunch. A well-known local solicitor had stated that the administrators, in his own words, acting on Barclays' instructions, had placed “£60,000 on his desk” and told him to “take out” David M. He had joked that he “didn’t know whether to take his penthouse in Marbella first or his Bentley.”

Still having contacts within Barclays, I emailed a member of the Board and made it clear that public exposure of what had happened would reflect badly on the bank. Within weeks, David and I were in a meeting in Leeds with senior Barclays executives, including the Regional Director, who had just returned from discussions with the Board and had been instructed to "get a deal done."

Barclays were represented by their lead General Counsel for the UK and Europe, Mr C, together with their solicitors. David and I attended alone. Three hours later, a substantial settlement had been agreed and a Non-Disclosure Agreement signed.

What began as a dispute involving one dishonest bank manager gradually revealed a much wider pattern. When victims of bank misconduct fight back — particularly when they have evidence and are prepared to litigate or go public — the response often escalates. I had experienced the threat of administration myself and had also seen how insolvency processes could be used against other victims. More strikingly, I saw how determined institutions could be to prevent those practices from being exposed.

2

8

16

502

Chris Coomber retweeted

Jun 15

The suffragettes *blew up* Lloyd George’s house!

An indictment on how liberals remember history.

The Lady Chief Justice: Palestine Action was not a direct action civil disobedience protest group like the suffragettes, but used violence to destroy property

The suffragettes burned down country houses & train stations, bombed churches & sent letter bombs to politicians.

141

2,066

9,840

197,546

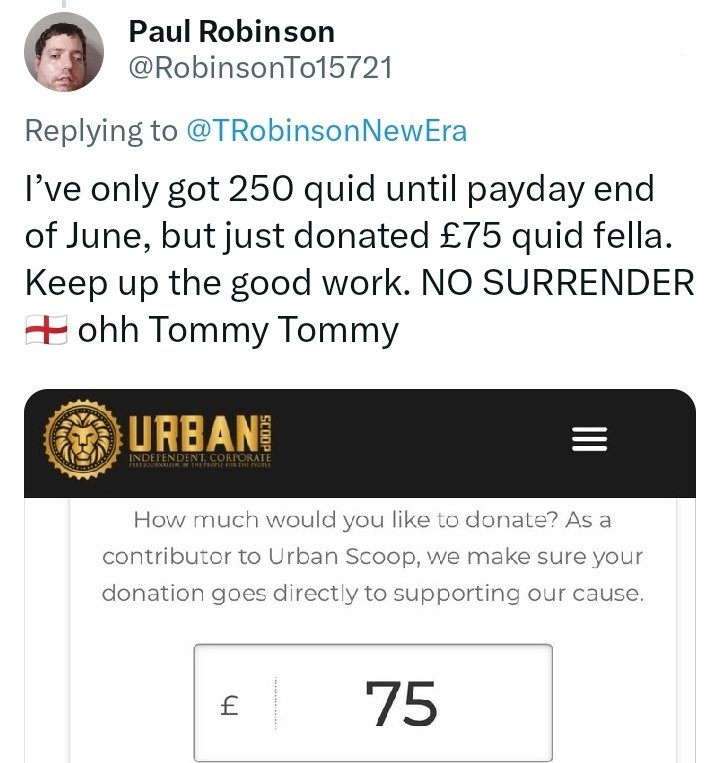

Chris Coomber retweeted

Jun 14

Tommy Robinson’s kids walking around in thousand quid CP Company coats & Breitlings on their wrists but here’s Paul forgoing food til payday in order to fund the little coke-rats next snortathon

That’s the thing with stupid. You can explain it but you can’t make it understand

96

691

2,633

94,583

Chris Coomber retweeted

Jun 13

Remember when they got mad about how Michelle Obama planting a vegetable garden would ruin the landscaping.

1,279

13,548

101,164

2,096,764