Ensuring Twitter compliance of commission regulations.

Joined June 2017

- Tweets 44,356

- Following 528

- Followers 709

- Likes 217,563

3,510 Photos and videos

Jürgen, Europe's strongest Eurocrat retweeted

Egal was ihr macht, gebt ihm nicht die Infinity Steine

Sid Rosenberg encourages the Jewish community to be proud and not to "hide your yarmulkes."

4

1

22

1,314

Jürgen, Europe's strongest Eurocrat retweeted

Jun 1

Jun 1

Microsoft Bans Claude Code After AI Costs More Than The Humans It Replaced

36

1,255

18,371

568,615

Jürgen, Europe's strongest Eurocrat retweeted

120

669

11,005

359,874

Jürgen, Europe's strongest Eurocrat retweeted

In 2006, Germany killed a bear called Bruno the Problem Bear.

In 2026, Germany killed a whale called Timmy the Exploding Whale.

In 2046, we must kill something even bigger or face the wrath of the gods.

21

34

854

15,595

Jürgen, Europe's strongest Eurocrat retweeted

𝟲𝟬𝟬.𝟬𝟬𝟬€ kostet es, zwei Kinder großzuziehen (Direktkosten Verdienstausfall). Fast genau so viel bezieht ein kinderloser Mensch im Alter an Rente, Gesundheit und Pflege aus dem Umlagesystem.

Ein einseitiges Geschäft:

Eltern investieren, Kinderlose profitieren.

🧵

180

103

608

103,618

Jürgen, Europe's strongest Eurocrat retweeted

Excuse me, I think there’s been a mistake, I need to speak with the manager. I was supposed to be part of the in-group the law protects but does not bind, not the out-group it binds but does not protect.

May 23

Feeling robbed of my path to citizenship right now after grinding a PhD and contributing to foundational AI computing technologies for the United States for the past ~ 10 years.

Feels like robbing top and technologists like me of the opportunity to achieve the American Dream.

30

2,095

23,775

473,943

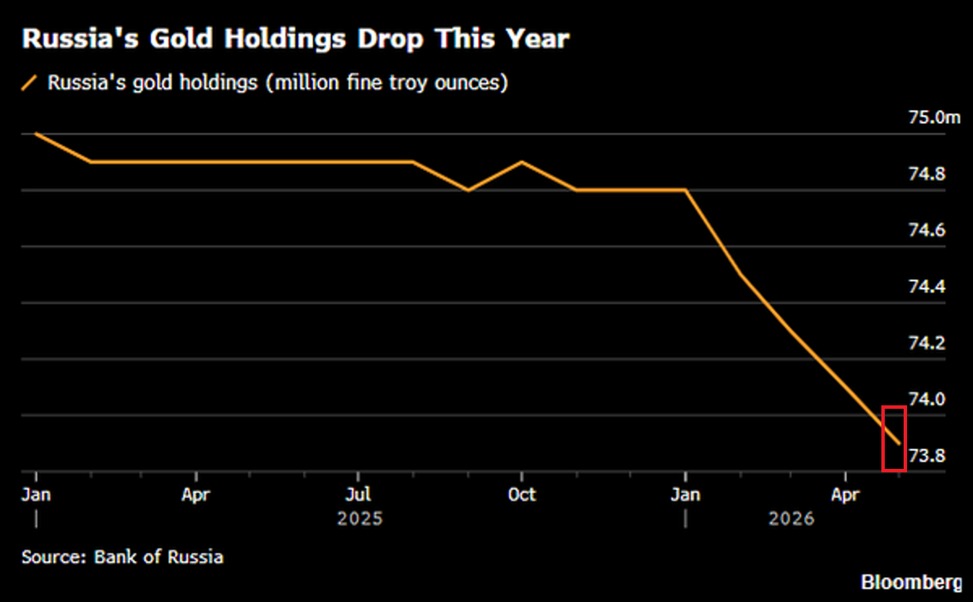

POV: You're the Russian central bank and have to issue bonds at 15% yearly interest in a foreign currency that is prone to deflation.

May 22

🇷🇺 Russland verkauft seine Goldreserven im Rekordtempo.

📉 –900.000 Unzen in nur 4 Monaten (2026)

💰 Erlös: ~4,3 Mrd. $ bei ø $4.800/Unze

📊 Niedrigster Stand seit Februar 2022 – dem Monat des Einmarsches

Und: Direkt nach Putins Besuch bei Xi hat sich der Goldpreis zwar nicht bewegt, aber Russland hat OFZ-Anleihen in chinesischen Yuan angekündigt – ein Zeichen dass Putin sich von Xi Finanzhilfe erhoffte, nicht bekommen hat und nun selbst Kapital aufnehmen muss.

Russland liquidiert, was es jahrelang gehortet hat.

1

129

Congratulations to China for making the first step towards undoing the Treaty of Aigun.

26

Jürgen, Europe's strongest Eurocrat retweeted

May 23

Sevim Dağdelen (BSW) beim Betreten der russischen Botschaft im Mai 2025. Empfangen wird sie von einem GRU-Agenten und Kurator des Spionagenetzwerks in Deutschland.

🧵1/22

94

1,139

3,380

133,308

Jürgen, Europe's strongest Eurocrat retweeted

May 21

europeans after enabling their out of office auto reply until september

544

4,894

69,554

11,579,659

Der scheiß Clanker wird sich in Berlin niemals durchsetzen, weil er einen weder mit Chef oder Sir begrüßt, noch nen türkischen Kaffee anbietet noch nen Schwank von der Einschulung seiner Kinder erzählt.

May 20

🇨🇳 NEW: Chinese cities are rolling out AI-powered robot barber kiosks that scan customers in 3D and cut hair with millimeter precision for just 60 yen per session.

3

149

Jürgen, Europe's strongest Eurocrat retweeted

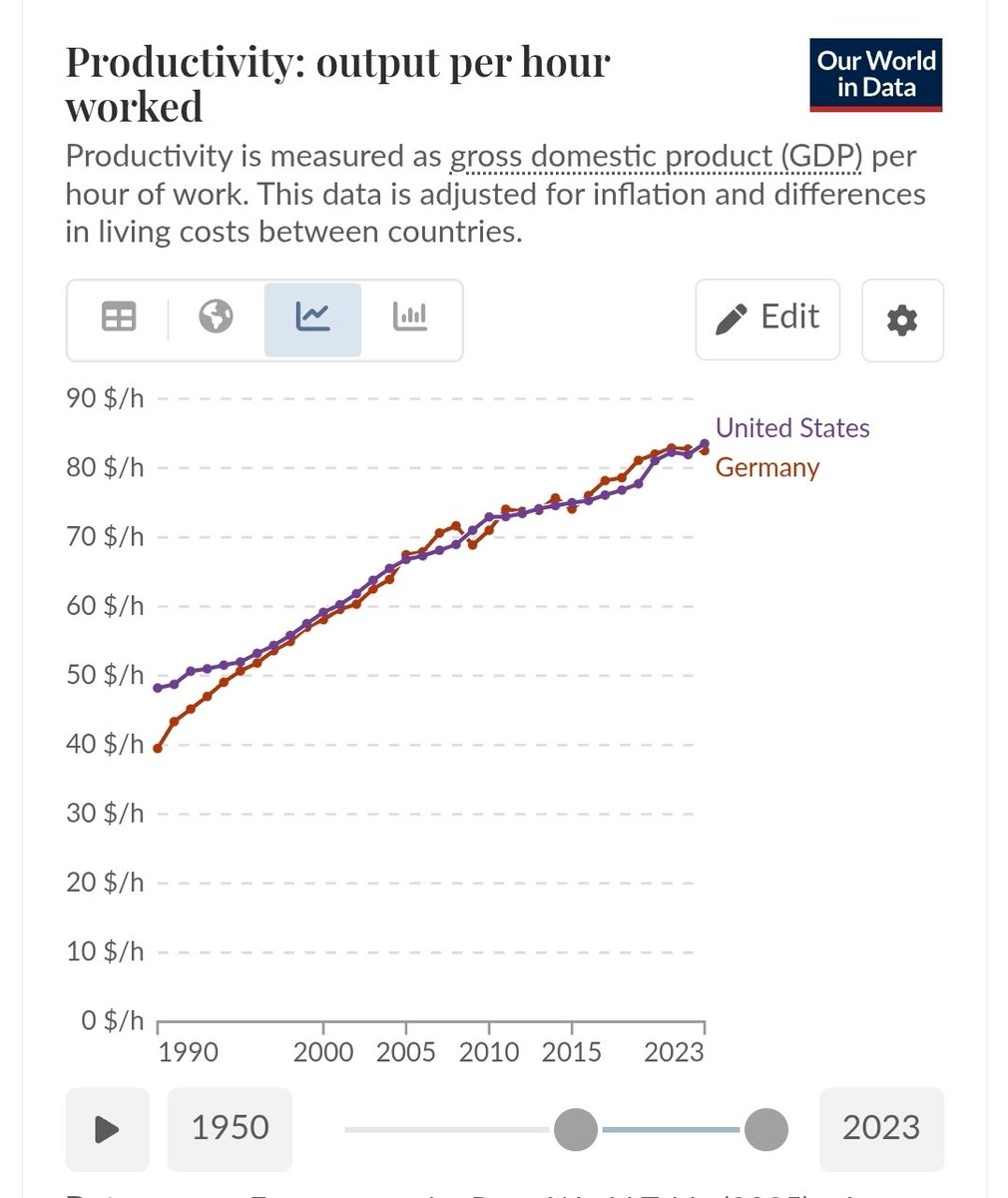

🇪🇺Is there a way to reverse the European decline?

I wanted to bring together a few considerations.

A) Is there a problem?

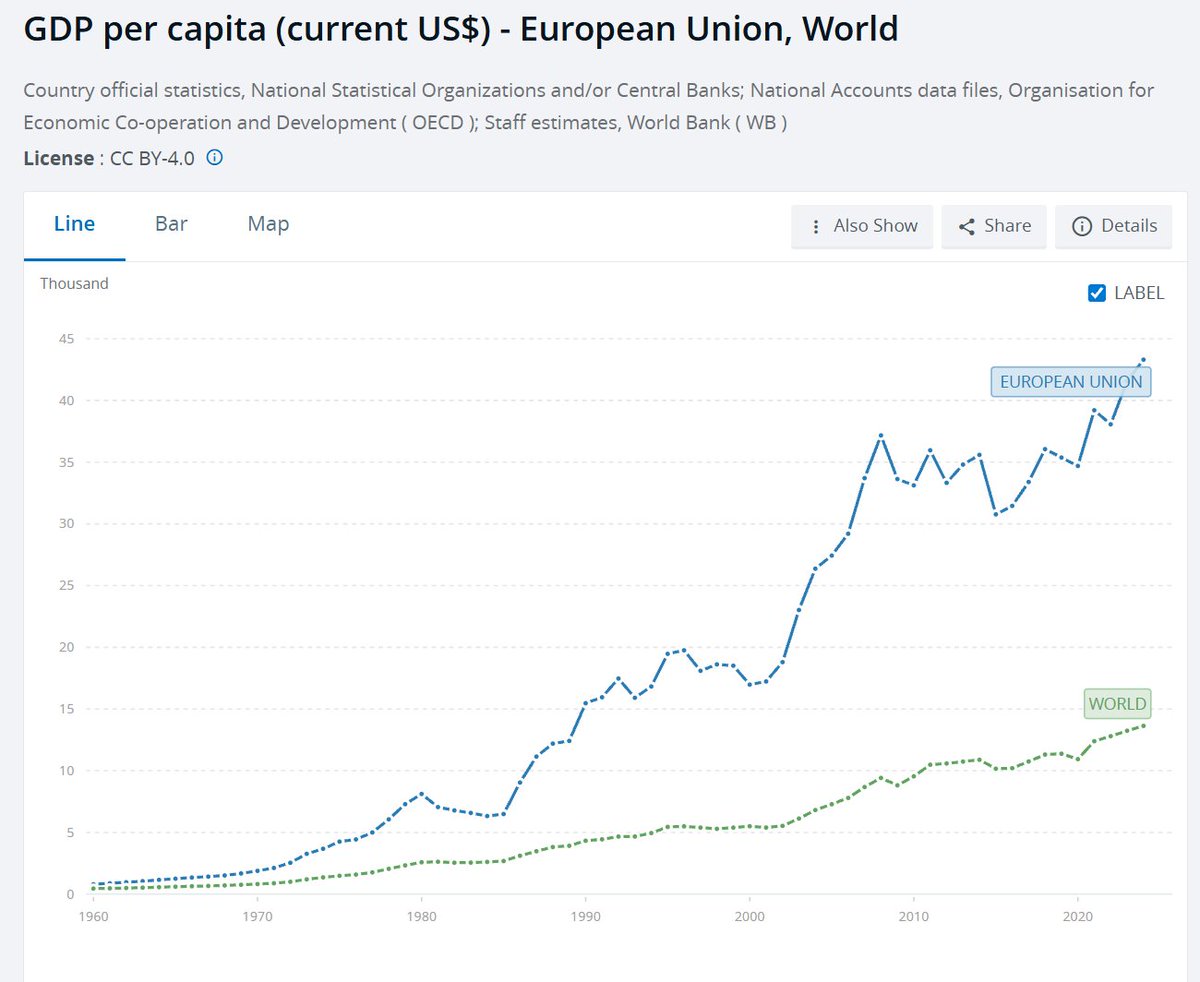

Relative decline compared to the US exists, but the catch-up of the rest of the world to Europe resembles Russia’s advances in Ukraine [Pic 1-2].

The main case can be made for developed Western European countries: structurally lower growth than the US, and lower growth than much of the rest of the world. European history in the new millennium is Italian stagnation, but also 150 million people quadrupling their GDP per capita.

B) Let’s set the bar:

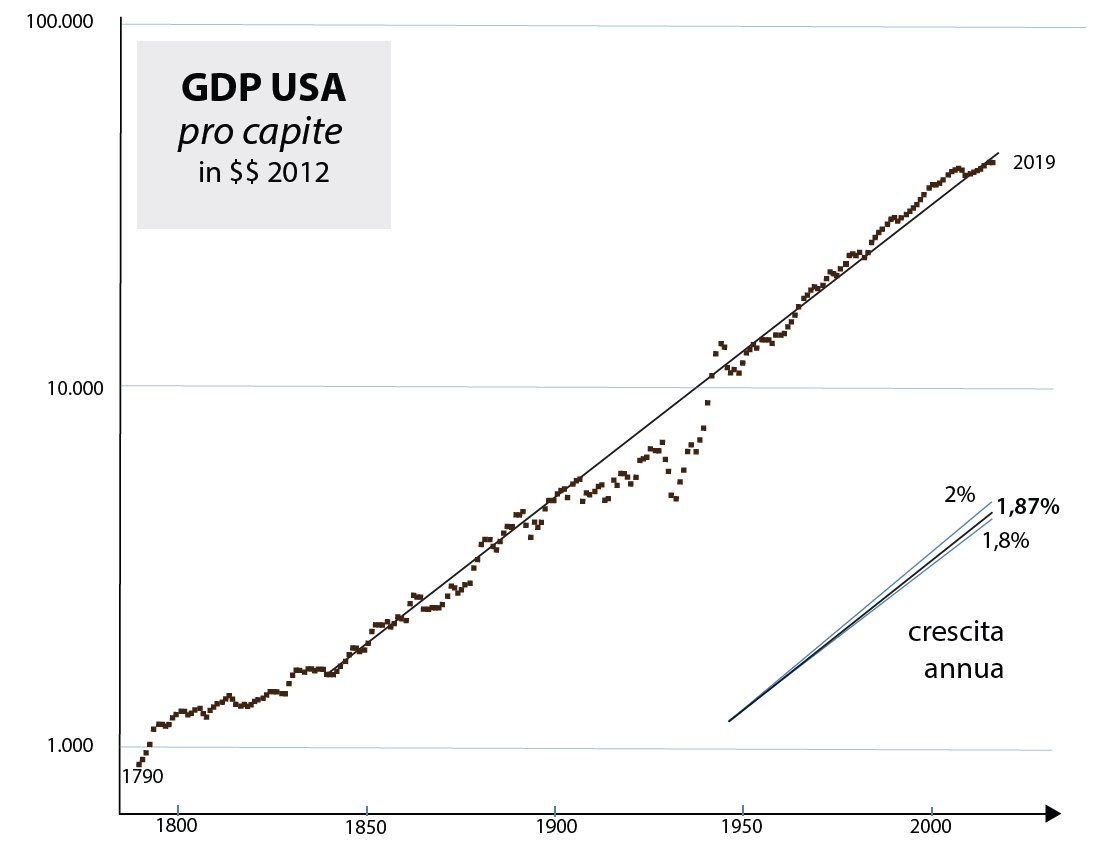

2% long-term real GDP per capita growth is more or less the upper limit a developed country can aspire to. The US has been hitting this benchmark with stunning consistency for roughly 200 years [Pic 3], and it is a good proxy for the pace of advancement of the technological frontier.

Looking nostalgically at France's or Italy’s 5% annual growth rates in the 1970s is foolish: Poland and Bulgaria are going through that development phase right now. Growth rates must always be compared to the level of development, otherwise comparisons are meaningless. From the perspective of long-term structural prospects, a Brazil growing at 1.9% is far more worrying than a Germany growing at 1% from a base 5 times larger.

So, our growth targets are:

1) 2% GDP per capita growth for the countries at the tech frontier.

2) 2% GDP per capita growth for the less developed countries.

The latter is broadly in line, especially net of the sovereign debt crisis, which is unlikely to repeat, but Western Europe will likely act as a ceiling on others’ development, so missing (1) could mean reducing the room for (2).

C) Let’s identify the problems:

Why do developed European countries struggle to grow at the US pace of 2%, and instead grow closer to 1%? I would say the main differences are two:

1) Demography. Not just demographic growth: the effect is mainly driven by demographic composition, though the two are obviously linked.

GDP per capita is commonly understood as a proxy for production. That is not wrong if properly interpreted, but in my opinion it is misleading, especially when looking at long-term trends.

GDP per capita is essentially a proxy for the level of technological adoption. Historical growth in GDP per capita is not people consuming more wheat; it is people consuming, or investing in, increasingly diversified and complex products. Of course, in order to afford them, people must exchange things perceived as having comparable value, meaning they must also produce increasingly diversified and complex goods.

Demand determines supply as much as the opposite.

Ageing slows per capita growth long before population decline becomes visible, which then later hits aggregate GDP growth. Older populations have less dynamic consumption patterns and push the working population toward less dynamic forms of production.

The history of GDP per capita and wage growth in Japan and Italy has been remarkably similar, and the main things the two countries have in common are the timing of their catch-up phase and the fact that they are the two countries furthest ahead along the demographic curve.

Demography appears to be a dominant factor behind growth dynamics of developed countries in recent decades, and Germany, France, and the UK are entering a demographic environment similar to that of Italy and Japan 20 years ago.

The positive side is that many middle- and low-income countries have worryingly low TFRs relative to their level of development (another metric that must always be compared to development level in cross-country analysis). China is a disaster in this regard, but one of a moltitude.

Once again, the US seems to be the only major competitor with both a competitive TFR and a growing population stock.

2) Scale. The US dominates almost all scale-based frontier technology sectors, while China is becoming disruptively competitive in several scale-based mid-value sectors.

In many low-scale-dependent sectors, Europe retains extraordinary leadership.

The semiconductor industry is emblematic: Europe leads in the most complex and highly specialized segment, EUV lithography machines, which does not require scale and instead relies on a myriad of highly specialized SMEs spread across the European territory, mainly along the Blue Banana. But Europe remains weak in almost every scale-based segment of the industry. One should realize that this pattern repeats across multiple sectors.

The problem is that scale-based sectors are a major source of growth when competing against rivals capable of exploiting scale advantages, eventually also in military competition. Losing scale-intensive sectors can create significant employment stress, particularly in high-volume industries.

Most other problems ultimately derive from these two structural issues.

I honestly do not believe that regulation or taxation levels explain the growth differential, except insofar as they are linked to demographics and fragmented scale coordination.

To be clear, reforms in these areas matter and can play a big role in year over year competition, but I'd rule out the differences between the US and Europe are large enough to justify the structural growth gap, the US is neither a tax nor a regulation heaven, and many successfull States have effective tax rates very similar to those of Western Europe.

By contrast, even ignoring the Imperial muscles of the US (and one shouldn't), the broader effects of advanced ageing, weaker presence in scale-based sectors, and underinvestment caused by fragmented national systems are clearly large enough to explain the divergence in growth rates, both absolute and per capita.

D) Solutions?

This analysis leaves little room for hidden or quick solutions, and I do not believe such solutions exist. I know this is unpopular, but I think this is the reality.

Both demography and full European integration require decades.

The latter is 'slowly' ongoing, while for the former one can only speculate, and reversing ageing dynamics within the next 30y is practically impossible.

Again, paying less for a notary in order to launch a startup is good, but it is not enough to reverse long term growth macro-trends.

One may find hopium in tech developments, certain technological waves may indeed be better suited to ageing societies, automation being the obvious example; or in questions such as: “Could societies ageing earlier gain some kind of first mover advantage over societies ageing later?” as I was recently asked (so far the former are losing).

These and many others remain speculative or marginal considerations, and it is unclear how they could compensate for the broader structural disadvantages described above.

To solve Europe’s scale problem we need:

-Integration of regulations across as many sectors as possible;

-Fiscal convergence, either through convergence of national legislation or through a larger share of EU-level spending in total expenditure, or both, especially regarding subsidies and intra-EU tariff equivalents;

-Integration of infrastructure and capital markets;

-Regional security and a common European strategy.

Each of these processes is already ongoing to some extent, but they are long and complex processes that depend on one another and involve significant transition costs.

As things stand, people and businesses plan within fragmented regulatory, infrastructural, financial, and strategic systems. Every additional step toward integration brings only marginal immediate gains. Positively there's high switching costs, and what is obtained is quite resilient.

E) Conclusions:

We're slow. Are we in a hurry?

There's a long pipeline of things to do and the sooner the better, but Europe has leverage and time to manage both enemies and allies.

I do not think it is an unambitious goal that, over the next 50 years, Europe should aim to remain as wealthy relative to the rest of the world as it is today, which requires a minimum level of sound political decision-making, while gradually bringing the main pillars of integration to functional completion.

Europe’s share of global GDP will continue to decline for some time simply because of demographics, but being rich matters far more than being numerous.

I cannot ignore the idea that a Eurasian order is inherently more stable for plenty of reasons, and such an order cannot ultimately be centered anywhere other than Europe. That moment may eventually come.

But today, everything still suggests that this will be another American century, and recognizing this is a strength, not an admission of weakness.

Europe’s main domestic objective is managing the difficult process of integration, a monumental task deserving of every available resource.

Its main foreign policy objective should increasingly be to speak as a Union, keeping Russia close and the US closer.

As for the rest, perhaps Europeans should complain less. I fully support self-criticism and the constant struggle to improve, but this should not become defeatism. Our problems concern how many euros to print to finance pensions and whether we can overtake the US in more frontier technologies. In Vietnam there are 100 million people producing goods for us for $500 a month, with a TFR below replacement level, no widespread pension or healthcare systems, and entirely dependent on the goodwill of the US and China. If French budget puzzle seem complicated, most fiscal situations around the world are generally worse.

Europe is not the land of decline; it is the land of hope. The current European leadership was born in a Europe still divided in two, and in just 30 years it has achieved an extraordinary number of successes in integration, while also lifting roughly 150 million people out of Soviet poverty.

People can debate convergence criteria all they want, but has there ever been a period in European history in which Europe was this uniformly developed and almost every country enjoyed such comparable prospects of long-term stability?

The founders of the modern European Union are pioneers of a new era that visionaries already foresaw as inevitable for Europe 150 years ago. They are not late administrators of decline.

The European Union therefore cannot be nostalgic. The past no longer exists; nostalgia can only be directed toward realities that are gone forever. Europe must not return to something, it must move toward something else.

The future is undefined and must be built. That makes things difficult, but it also makes Europe the only civilization with a truly open and elastic horizon of hope.

China’s “common prosperity” is a joke, and the whole world knows it; the Chinese themselves may soon realize it too.

The American Dream has become a crumpled cigar, that is the project genuinely at risk of turning into nostalgia.

The European Union has no existing social pact to preserve; it is building one out of many different social pacts, and that is why it moves slowly.

The final result may well be worthy of the ambition behind the project, but it will require an extraordinary civilizational effort, and such a process inevitably appears chaotic.

Is there a way to reverse the decline? With or without the euro?

4

12

49

7,642

Jürgen, Europe's strongest Eurocrat retweeted

I didn't know Helen of Troy could generate so much conflict.

1,381

9,808

82,321

2,910,702

Jürgen, Europe's strongest Eurocrat retweeted

May 19

this is video marketing aimed at investors, "look at how scared your potential future wage slaves are, that's how powerful our Product is". he doesn't code switch for the Poors because there's no need to, it's a commercial for other rich people to watch

May 18

Billionaire ex-CEO of Google Eric Schmidt fails to read the room, championing artificial intelligence’s restructuring of society at the University of Arizona graduation ceremony Friday night in his speech as commencement speaker. Schmidt was met with merciless boos and jeers from the graduating students at every mention of AI.

AI is expected to replace around 15 million U.S. jobs by 2030.

46

2,424

21,422

543,084

It's weird that two of the most common arguments against kids that I hear from young people are "It's irresponsible to put kids into a world heading for ecological catastrophe" and "We want to continue to use the most climate-hazardous form of transportation as often as possible"

69

This originally Tuscan company was bought by a Texan corporation 6 months ago and now manufactures the ornaments for Trump's White House ballroom

May 16

İtalya’da her gün 24 saat çalışan CNC mermer işleme makinesi, dev heykeli yaklaşık 15 günde tamamladı

1

2

37

1,211

Jürgen, Europe's strongest Eurocrat retweeted

May 17

Moscow started a completely unecessary war that resulted in massive suffering, after Moscow couldn't win quickly, it settled in for attrition and destruction, basically waging a war against Ukrainian civilians, to destroy and raze part of Ukraine, using tens of thousands of drones to attack Ukrainian civilians.

Moscow assumed this war will be easy apparently and accelerate the "decline" of the West; it assumed incorrectly that Ukraine couldn't hold out and that the West was weak and would crumble...but Moscow was wrong.

Maybe it's a lesson, don't start endless wars just for the sake of war.

May 17

Ukrainian Bars low cost cruise missile spotted flying over Russia’s capital, Moscow, early this morning.

11

32

221

16,135

Jürgen, Europe's strongest Eurocrat retweeted

May 14

The last few years have forced Europeans to understand one hard truth: for the first time since the imperial era, no European country is globally relevant on its own.

Germany is Europe’s largest economy. Yet in 2026, its nominal GDP is around $5.45T — almost 6 times smaller than the U.S. and almost 4 times smaller than China.

The same applies demographically. Germany, the EU’s most populous country, has around 83 million people, compared with roughly 349 million in the U.S. and more than 1.4 billion in China.

France, Italy, Spain, the Netherlands, Poland and Sweden are even smaller individually.

This is the central reality of the 21st century: European nation-states are too small to compete alone against continental powers. The only way Europe remains relevant is through scale.

Together, the EU and the UK represent around $27T in nominal GDP, making Europe one of the world’s largest economic blocs, second only to the U.S.

In PPP terms, Europe including the UK is around $35T, second only to China. Europe’s problem is not lack of wealth, talent, industry or technology.

Europe’s problem is fragmentation.

A fragmented Europe is a collection of medium-sized states.

A united Europe is a global power.

May 14

President Donald J. Trump meets with President Xi Jinping in China. 🇺🇸🇨🇳

190

128

794

92,688

Jürgen, Europe's strongest Eurocrat retweeted

May 13

This is… very unlikely and shows serious misunderstanding about how authoritarian rule works.

The bread and butter of any regime of this type is to project an image of success and invincibility.

The goal is to encourage the idea of permanence and inevitability so to discourage opposition. People are not only directly discouraged by this, their incentives to do anything is weakened by the expectation that nobody else would do anything against the regime.

Repression is a visible sign that resistance exists, and so is a sign of failure. It only really works if it’s massive and sustained, such which makes it even harder to carry out. Doing this in the middle of a disastrous war is even dicier and only a desperate regime would resort to it.

Moreover, if elites come to believe that Putin is vulnerable, they are much more likely to start jockeying for power among themselves, which will further destabilize his rule, which is, after all, based on being the main balancer among the various factions that his kleptocratic regime depends on.

While a coup remains a far-fetched scenario, the rumors that Putin is weakened aren’t a clever ploy to increase repression but a real sign that his rule is starting to shake.

May 12

Is Putin Really Vulnerable? Or are all the rumors swirling in Moscow just more dictator games with his loyal security services, only to justify further crackdowns and repression?

This is the subject of my opinion piece out today with @ForeignPolicy magazine. Below are a few of the key points I make. Please tune into FP for the full article, and more great content on Russia.

🚨With the Kremlin, every few months, a new rumor seems to emerge suggesting that Putin may be vulnerable. The Washington Post, Newsweek and other sources reported last week this may suggest Putin is weakened and concerned over potential coups. My take: nothing further from the truth…this is a lot of wishful thinking.

Unfortunately, after 25 years in power, Putin has built a system designed precisely to survive rumors, dissent, and internal intrigue. As I said in the article, during his years in power, Putin has learned from other dictators’ failures.

⚠️In a hypothetical ‘World Dictators and Autocrats’ course, Putin has earned straight A’s for the last quarter century! He knows what he is doing.

🚨My conclusion: coup rumors, investigations, and arrests serve Putin’s political purposes. They create uncertainty within elite circles keeping his followers fiercely loyal and the population frozen in fear.

⚠️The most likely outcome given today’s rumors of dissent and upheaval in Russia is therefore not imminent regime collapse but further repression.

👇In the article I also discuss the Prigozhin’s rebellion in 2023, tune into the full article for his and other key analysis!:

foreignpolicy.com/2026/05/12…

👉Please consider my book for further analysis like this on the Russian services!:

amazon.com/Tradecraft-Tactic…

#Russia #RussianIntelligence

#Ukraine

24

70

477

50,130