I'm kind of a big deal

Joined September 2021

- Tweets 3,824

- Following 326

- Followers 280

- Likes 15,458

531 Photos and videos

𝕄𝕒𝕥𝕣𝕚𝕔𝕜 retweeted

Battery storage is now the fastest-growing source of lithium demand, up 45% in consumption in 2026 - hugely important for AI. The window for domestic US producers is opening up. Century Lithium's Angel Island is ready. 🔋 $LCE.V $CYDVF

Read more: bit.ly/4uqnsb6

1

6

13

448

𝕄𝕒𝕥𝕣𝕚𝕔𝕜 retweeted

May 29

Trump has signed a memo allowing federal agencies to hire 400 experts to boost the federal government's critical minerals investments.

Top pay for these experts will be set at $400,000 annually, "consistent with market comparability and national security urgency."

20

70

481

67,321

𝕄𝕒𝕥𝕣𝕚𝕔𝕜 retweeted

May 23

Samuel Henderson, the autistic student with Tourette syndrome who has a knack for perfectly imitating the sounds of over 50 types of birds.

485

2,183

19,808

697,816

May 21

China will be the domino.

May 21

Chinese crude imports have fallen by roughly 5 million barrels per day between February and thus far through May.

May-to-date crude import pace is China's slowest since October 2016.

1,593

𝕄𝕒𝕥𝕣𝕚𝕔𝕜 retweeted

May 19

Hey @NevadaLithium executives…

Your turn!

They're still buying.

Three insiders at @SurgeBattery bought 850,000 shares on the open market in the past week.

$NILI.V $NILF

1

4

8

508

May 11

It's exhausting to read all the terrible takes by the self appointed geopolitical 𝕏perts. Ffs, stay in your lane.

4

29

May 10

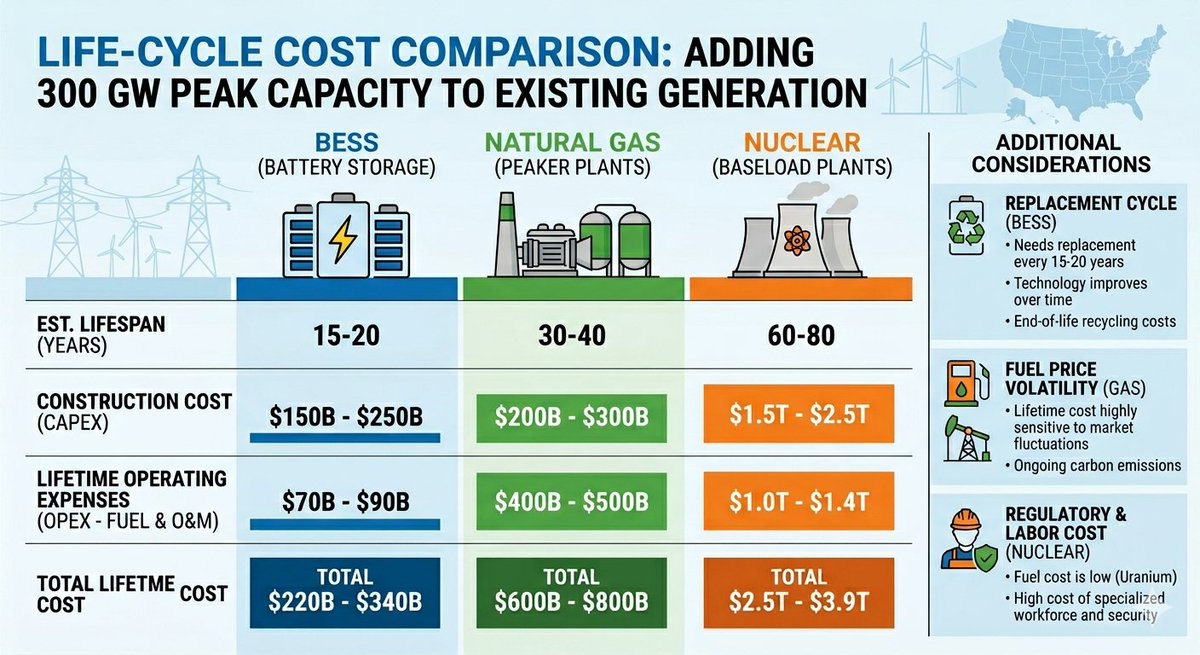

Hypothetically, utilities with enough BESS capacity to capture every excess watt produced during off-peak hours, they could increase peak-period output by 25% to 40% without building a single new power plant.

1

2

109

May 10

Adding BESS to existing generation is a no-brainer.

Lithium

Copper

Batteries

1

40

𝕄𝕒𝕥𝕣𝕚𝕔𝕜 retweeted

May 8

🇺🇸This clip is the absolute best. OMG does he nail it. His calm demeanor makes it even better. This is exactly how I picture these crazy liberals.🇺🇸

568

5,522

17,395

420,356

𝕄𝕒𝕥𝕣𝕚𝕔𝕜 retweeted

May 7

1) The SPR release is sending huge volumes of US crude into Europe, which is significantly dragging down the North Sea window diffs.

2) Panic bought cargoes from 1-2 months ago are arriving in Asia this month, giving Asian buyers some breathing room. There is a distinct lack of aggressive buying.

3) China's SPR release.

4) Due to the combination of points 2 and 3, buyers are holding off on bids and staying on the sidelines, hoping the Strait will open. If it doesn't open soon, they'll be forced back into bidding for barrels.

5) I don’t want to blame anyone for this wait and see attitude. Looking at the demand to ship out enriched uranium stocks, I believe the chances of reaching a deal are extremely low.

6) But others might think differently. Plus no buyer wants to risk looking like a fool. Refineries still running have gained a bit of breathing room with May arrivals, and the rest have already implemented run cuts. Opportunistic buying is only natural.

6) There is plenty of incentive for operational refineries to maintain max runs. European diesel spreads are still at insane levels, and the WTI 3-2-1 crack is nearing $54/bbl even while crude is swinging by ~$20/bbl.

7) Unless diplomatic progress creates actual change, I expect buyers will soon be forced to start bidding again.

8) I made massive profits on Brent for Apr, May, and June, but it's true I’m currently seeing a loss on the July contract.

I cut down my rollover volume knowing these headline swings would happen, and I added to my position yesterday.

Unfortunately even those additional entries are starting out in the red. I'm disclosing this bc transparency is important.

I'm open to hearing other perspectives.

#oott #iran

Hi boss any idea why the physical market has considerably weak-end over last 2

Weeks? Shouldn’t spreads and diffs hung in there? 🙏🏾

44

94

948

113,774

𝕄𝕒𝕥𝕣𝕚𝕔𝕜 retweeted

May 5

Worth the read.

May 5

As a final nod of appreciation to @SenThomTillis and @Sen_Alsobrooks on their efforts to find a compromise, I want to point out just how dishonest the bank trades are in their latest analysis of the yield issue, even in these waning hours.

Their joint press release complaining about the new language [1] mentions research that "demonstrates that yield-earning stablecoins could reduce all consumer, small-business, and farm loans by one-fifth or more, making it essential for the prohibition to be clear and transparent."

That "research" is a post in Open Banker by Andrew Nigrinis [2] which summarizes the paper he wrote on this issue [3].

The analysis in both is rather troubling, bordering on dishonest.

In the post, Nigrinis stated that any yield related to stablecoins could "siphon trillions of dollars from deposits." The word siphon is a link to a Reuters story about a Standard Chartered analysis that stablecoins could "..suck $1 trillion from EM banks in next three years." [4]

The emphasis is mine, because StanChart is talking about emerging market banks, not American community banks. It's right there in the headline! The article even mentions specific countries like Sri Lanka, Pakistan, and Kenya.

Nigrinis' conflation of the two is deceptive. If anything, stablecoins competing with offshore bank deposits will increase domestic deposits, as I argued in my response to the OCC on proposed rules for GENIUS. [5]

Next, Nigrinis references "The U.S. Treasury’s April 2025 report."

But as we all know, there is no such report. Instead what he links to is the Treasury Advisory Committee "thought experiment" [6], which was a private sector document (partially written by bank execs) that lacked rigor.

Lastly, he cites an influential paper on CBDCs by Whited et al (one that I also mentioned in my comment letter).

His reference doesn't mention the fact that this paper is. talking about a central bank digital currency, a far more radical product than a stablecoin. He quotes their analysis that $1 going into a CBDC may result in a loss of 80 cents in bank deposits, but leaves out their belief bank lending would only fall by only a quarter as much.

He also ignores the overall thrust of the paper, which is that banks can still adapt in such a (radical, unlikely) world if there is a loosening of regs and capital requirements, both of which are happening independent of CLARITY.

Sometimes, all you need to know when deciding who should win a debate is how badly one side is willing to ruin its own credibility to get its way.

The bank trade group arguments on this issue were always rather swampy. At this point you could smell the rot.

[1] bpi.com/banking-trades-state…

[2] openbanker.beehiiv.com/p/sta…

[3] papers.ssrn.com/sol3/papers.…

[4] reuters.com/business/finance…

[5] regulations.gov/comment/OCC-…

[6] home.treasury.gov/system/fil…

1

1

44

𝕄𝕒𝕥𝕣𝕚𝕔𝕜 retweeted

5

6

1,538

𝕄𝕒𝕥𝕣𝕚𝕔𝕜 retweeted

Apr 30

Big funds bet billions on mining supercycle reuters.com/legal/transactio…

1

13

47

2,484

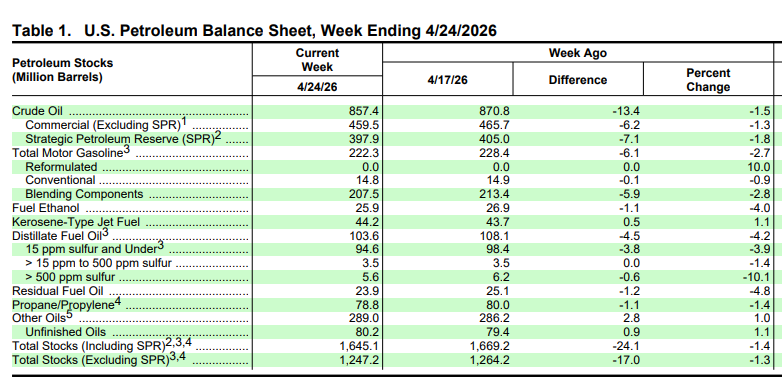

Apr 30

RT @HFI_Research: US total liquids fell -24.1 million bbls.

US crude storage fell -13.4 million bbls.

BACD is here.

60

𝕄𝕒𝕥𝕣𝕚𝕔𝕜 retweeted

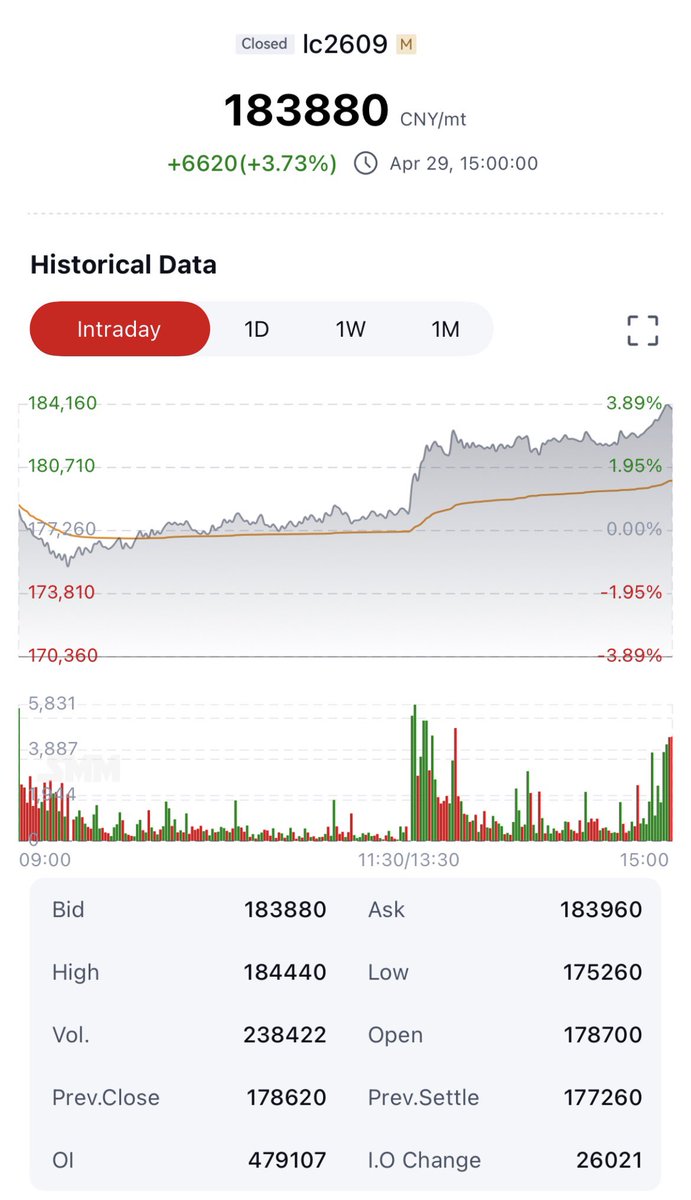

Apr 29

🚀 Lithium Unstoppable: Nothing Holding GFEX Back From ¥200K 🚀

GFEX lithium surging to 183,880 CNY/mt 📈🔥 and the trend is only getting stronger…

Yes, there’s chatter around CATL small scale sodium iron batteries 🔋 and even a rumored lepidolite plant restart in May 🏗️⛏️ but let’s be clear: none of this is enough to stop a move toward ¥200,000 💥

Why? Because the macro story is bigger 🌍👇

EV and BESS demand keeps accelerating 🚗⚡ and high quality lithium supply is still structurally tight 💎📉

Short-term noise vs long-term reality 📊 and the reality is a supply gap that isn’t closing anytime soon

That’s where smart capital is looking 👀💰

Not just producers, but emerging developers with scalable, low cost assets ready to step in 🔄

Names like Lake Resources and peers sit right in that sweet spot for potential rerating 📈🚀 as prices push higher

This isn’t the top, it’s the setup 🔥

#Lithium #EV #BatteryMetals #CATL #GFEX #EnergyTransition $LKE $LLKKF #ALB #PLS #ELV #A11 #LILAC #UBS #Argentina #USA #Commodities #Investing #CleanEnergy #Mining #Stocks #Bullish 🚀

5

14

81

7,936

𝕄𝕒𝕥𝕣𝕚𝕔𝕜 retweeted

Apr 29

Incredible EIA numbers

> 4% of US diesel inventories gone in a single week

A nearly 3% drawdown in gasoline inventories and summer driving season hasn't even started yet

Nearly 2% of US strategic reserve drawn down in one week

10

124

487

53,019

Apr 30

RT @HFI_Research: On April 12, we published a piece with a section titled, “Why aren’t oil prices higher?”

Here’s what I wrote:

Over the…

138

𝕄𝕒𝕥𝕣𝕚𝕔𝕜 retweeted

Apr 27, 2026

#Lithium Carbonate 99.5% Min China Spot

Price: $25,709.95

1 day: $ 438.24 ( 1.73%) 📈

YTD: 52.08%

#Spodumene Concentrate (6%, CIF China)

Price: $2,507.00

1 day: $ 38.00 ( 1.54%) 📈

YTD: 61.95%

Sponsored by @LibraEnergyMats

3

24

129

11,992

𝕄𝕒𝕥𝕣𝕚𝕔𝕜 retweeted

JUST IN: At dawn on Sunday, the Suezmax tanker OTIS arrived in Tokyo Bay carrying 910,000 barrels of Texas light crude that had loaded in Houston on March 22 and transited the Panama Canal. The cargo was pumped through an undersea pipeline to Cosmo Oil’s Chiba refinery, the same plant that has historically run UAE and Saudi medium-sour crude. It was the first US shipment of crude to Japan since the start of the Iran war on February 28.

The volume is approximately half a day of Japan’s domestic consumption, per Cosmo and METI’s own framing.

That is the part the headlines are pricing. The headline is the wrong story.

The actual story is that Japan, which sourced 94.2 percent of its crude from the Middle East as recently as February, has begun physically reconfiguring a seventy-year energy architecture in fifty-five days. METI confirmed yesterday that barely half of May’s crude requirement has been secured. Refiners, already running at sixty-seven to sixty-eight percent utilization before the crisis, have begun reducing operating rates further because they cannot find enough Middle East-equivalent crude. Japan begins drawing 36.48 million barrels from its Strategic Petroleum Reserve on May 1, valued at three point four billion dollars. It is the second draw since the war began.

The OTIS is the photograph of a pivot. The pivot itself is structural.

Japanese refineries were built around the API gravity and sulfur profile of Persian Gulf crude. Texas WTI is roughly 40 API and 0.4 percent sulfur. Saudi Arab Light is 33 API and 1.8 percent sulfur. Running light sweet through a hydrotreater configured for medium sour produces the wrong product mix: more naphtha and gasoline, less diesel and jet. Japan’s transport fleet runs on diesel and jet. The yield distortion shows up as inventory drawdowns on the products Japan actually consumes.

This is why the refineries are cutting runs. Not because they lack crude. Because they lack the right crude.

Three more US tankers are scheduled to deliver to Japan in May. US crude exports to Asia have surged from 1.1 million barrels per day pre-war to a forecast 3.29 million in May. Panama Canal crude transits hit a four-year high in early April. Auction premiums to skip the queue have reached four million dollars per slot. The two largest Japanese investments announced at the March 19 Trump-Takaichi summit were forty billion dollars in GE Vernova small modular reactors and thirty-three billion in natural gas facilities, both on US soil. Japan hit two percent of GDP in defense spending in fiscal 2025, two years early. The FY2026 defense budget is a record 9.04 trillion yen, including stand-off missile capabilities and a SHIELD coastal drone network. Japan, holding 1.239 trillion dollars in US Treasuries, is financing US energy capacity, buying US energy in dollars, accelerating its rearmament under US tech transfer, and recycling those dollars back into Treasury markets that fund the carrier groups enforcing the blockade that closed Hormuz.

Three readings of the OTIS arrival.

A symbolic shipment that fills less than half a day of demand. Priced.

Tactical diversification that ends if Hormuz reopens. Narrow.

The first publicly verifiable photograph of the United States repositioning itself from Middle East security guarantor to Indo-Pacific energy supplier inside a sixty-day window, with Japan financing the substitution and Beijing three weeks away.

The headlines are pricing the first.

Cosmo just refined the third.

open.substack.com/pub/shanak…

32

175

853

280,830

Apr 26

RT @HFI_Research: “From now to the end of July, visible US crude inventories will decline by ~213 million bbls, the largest and fastest dec…

122