We are a community that loves Silver & Gold, Period.

Joined November 2024

- Tweets 343

- Following 42

- Followers 748

- Likes 12,698

247 Photos and videos

Pinned Tweet

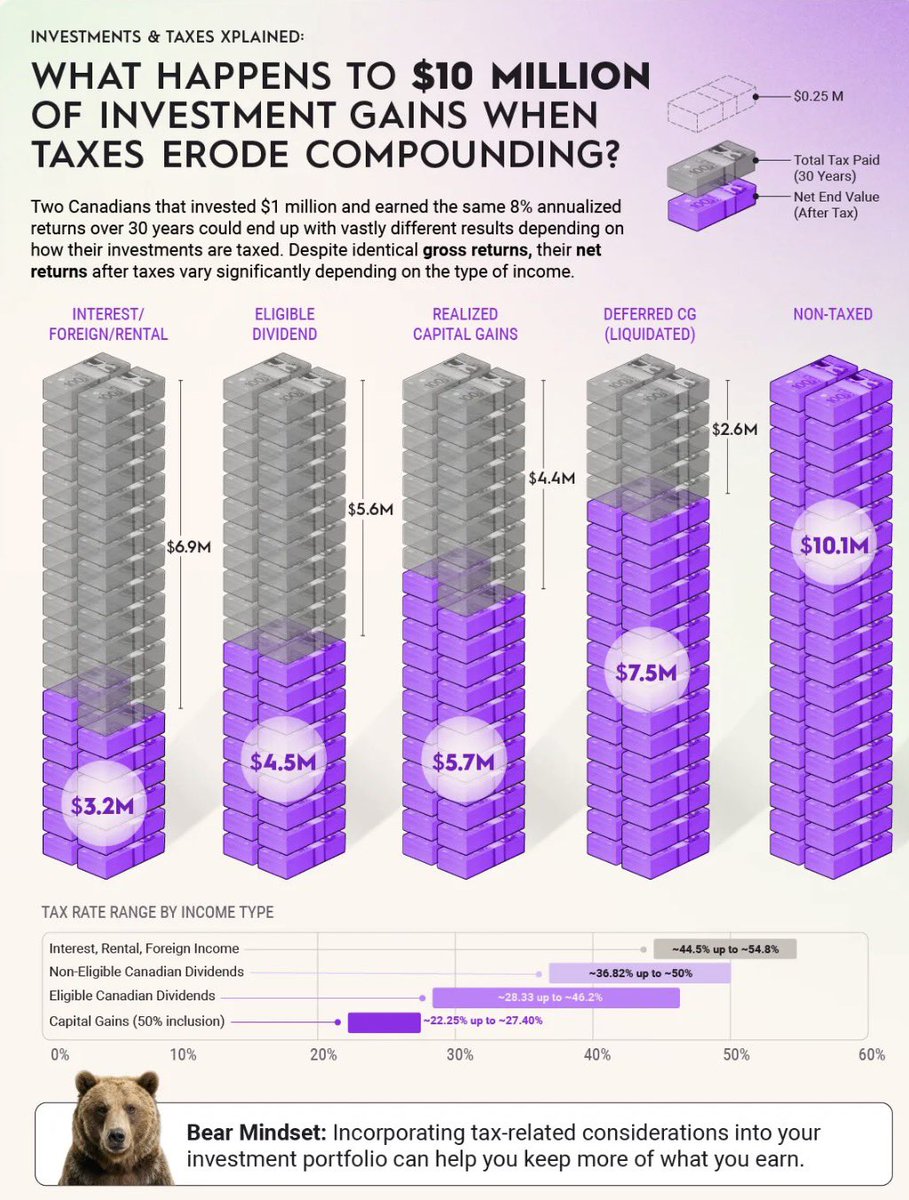

Taxes Can Destroy Your Wealth More Than Bad Investing Ever Will

Two Canadians can earn the exact same 8% annual return for 30 years and end up with wildly different outcomes — depending on how their gains are taxed.

That’s the part most investors ignore.

The chart says it all:

Interest / foreign / rental income can leave you with about $3.2M after tax.

Eligible dividends can get you to about $4.5M.

Capital gains can grow to about $5.7M.

Deferred capital gains can reach about $7.5M.

Non-taxed growth can leave you with about $10.1M.

Same return.

Very different result.

This is why smart investing is not just about chasing high returns — it’s about understanding tax efficiency, compounding, and after-tax wealth.

If you want to keep more of what you earn, taxes should be part of the investment conversation from day one.

#Investing #WealthBuilding #TaxPlanning #CompoundInterest #CapitalGains #DividendInvesting #FinancialLiteracy #PersonalFinance #TaxEfficiency #WealthManagement #MoneyMindset #PortfolioManagement #CanadianInvesting #InvestSmart #LongTermInvesting #FinancialFreedom #InvestingTips #TaxStrategy #BuildWealth #AfterTaxReturns #MoneyMatters #InvestorEducation #CanadaFinance #SmartMoney

1

46

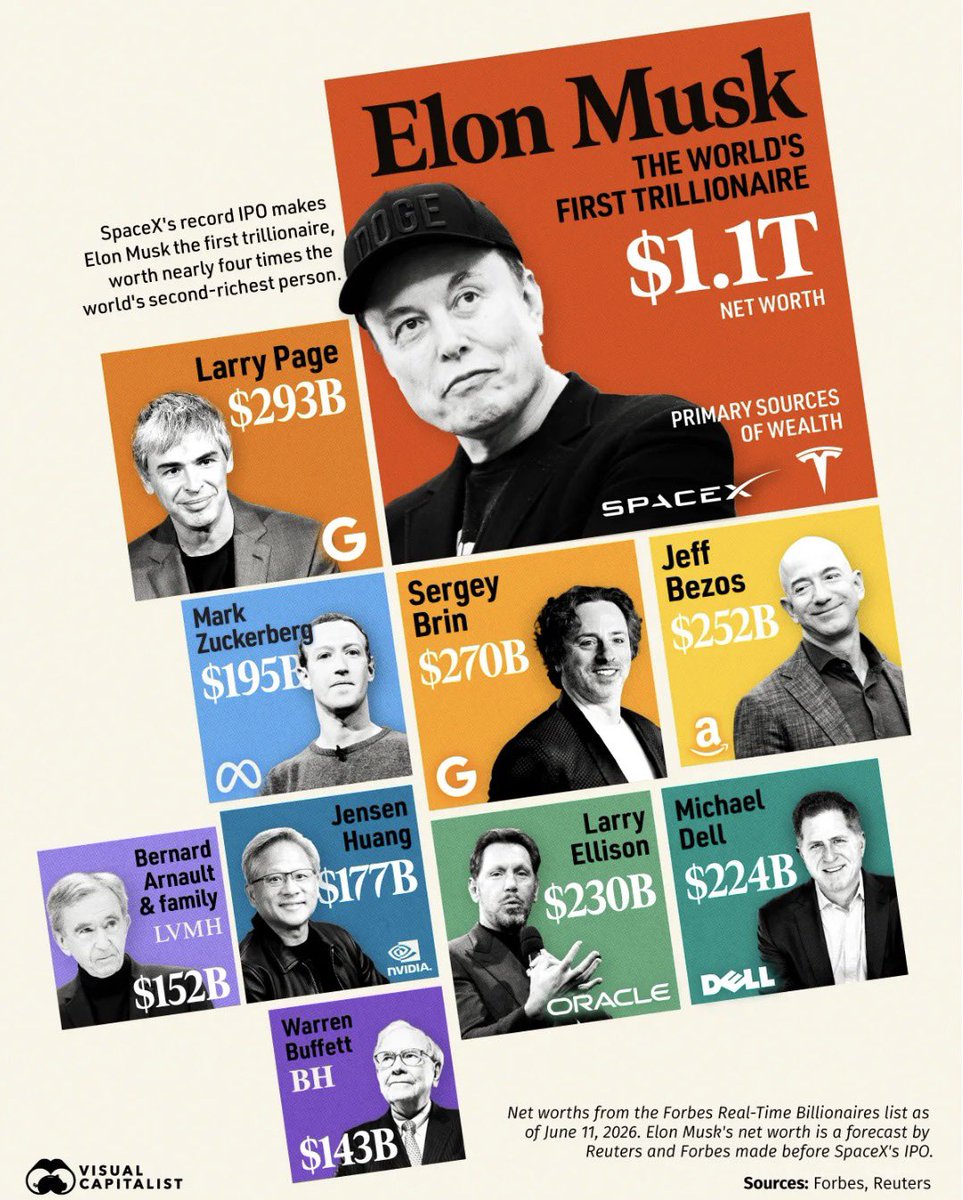

A Trillion Dollars Is Not “A Lot.” It’s a Different Species of Money.

This graphic puts wealth into perspective in a way most people never stop to consider. Elon Musk being shown around the trillion-dollar mark is a reminder that once you get into the hundreds of billions, the numbers stop feeling human and start feeling almost abstract.

A trillion dollars is 1,000 billion dollars — or 1,000,000 million dollars. It’s more than the annual GDP of many countries, and it’s the kind of wealth that can reshape industries, markets, and even public conversation.

The real takeaway isn’t just how rich one person can become — it’s how fast capital concentrates at the top while most people are still thinking in thousands and millions. That gap is why financial literacy, ownership, and long-term investing matter more than ever.

Massive wealth is not just about luxury. It is about influence, leverage, and the power to move entire sectors with one decision.

#Trillionaire #ElonMusk #Wealth #Billionaire #Money #Finance #Investing #FinancialLiteracy #CapitalMarkets #Entrepreneurship #Business #Economy #Macro #WealthBuilding #AssetOwnership #WealthGap #FinancialFreedom #Markets #Technology #Tesla #SpaceX #LinkedIn #Leadership #FutureOfMoney #EconomicTrends #PersonalFinance #GlobalWealth #InvestmentMindset #StockMarket #BigMoney #Success

2

100

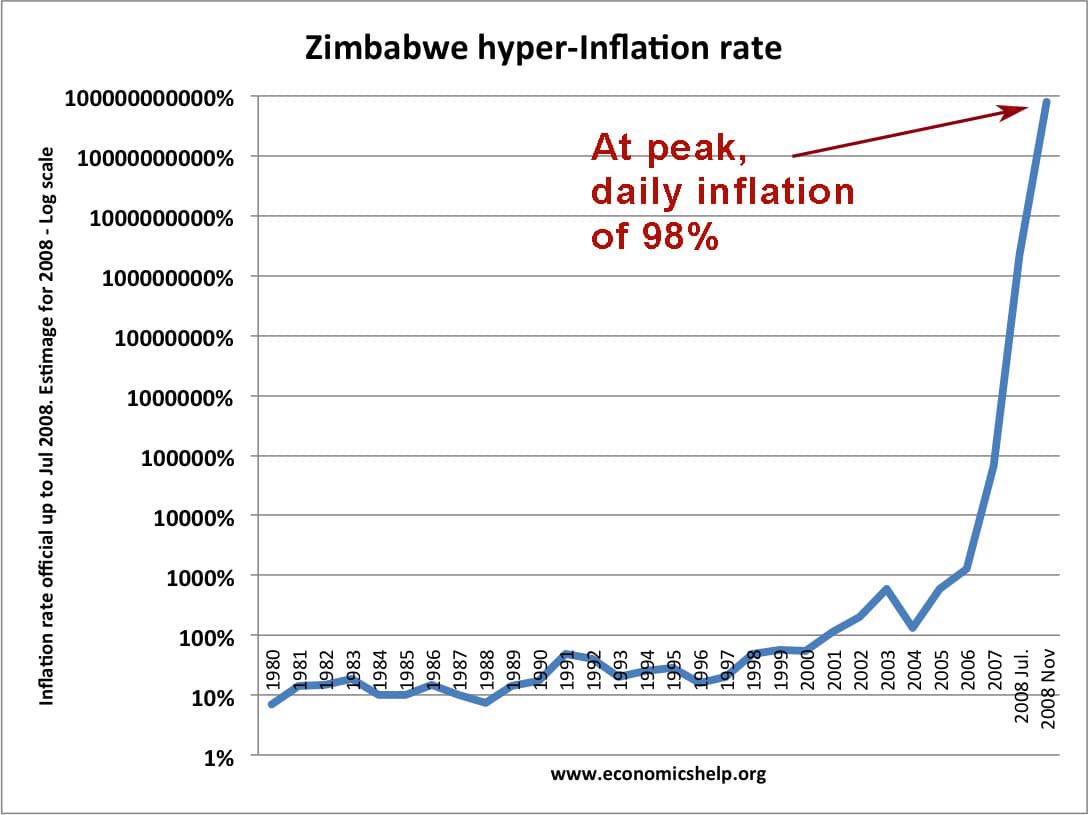

WARNING: The Inflation Trap Is Closer Than You Think.

Zimbabwe’s chart is a brutal reminder of how fast a currency can collapse once money printing gets out of control. Inflation doesn’t rise in a straight line — it can go from “manageable” to disaster very quickly.

The lesson for the USA is simple: printing endlessly has consequences. When trust in the currency erodes, the pain shows up everywhere — groceries, rent, wages, savings, and business costs.

This is why hard assets matter. Sound money matters. Fiscal discipline matters.

#Hyperinflation #Inflation #USDollar #MoneyPrinting #FederalReserve #Gold #Silver #PreciousMetals #HardAssets #Economy #FinancialSystem #Macro #Markets #WealthProtection #CurrencyDebasement #InflationWarning #USA #Geopolitics #Investing #WallStreetBullion

2

91

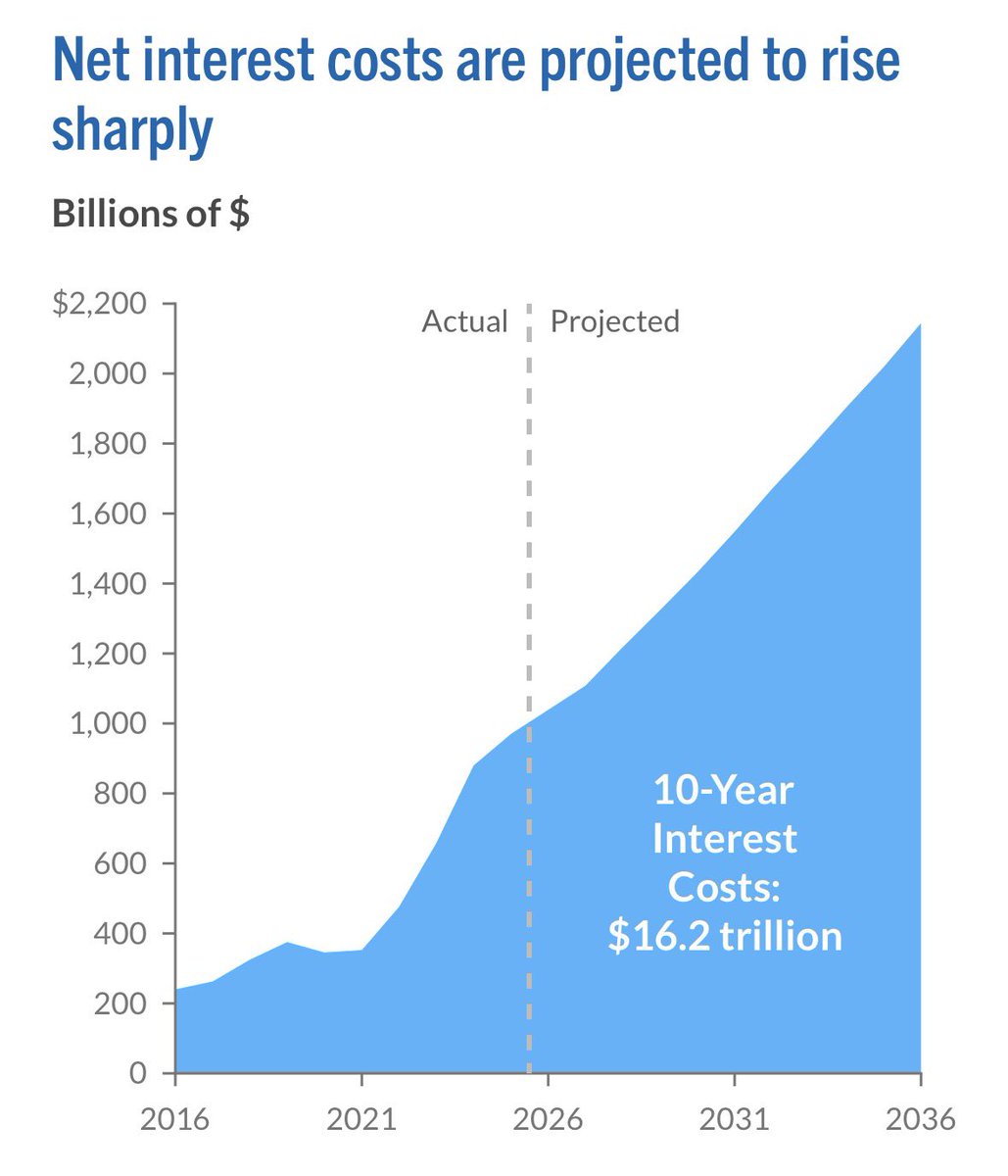

This Is How a Debt Crisis Turns Into Currency Destruction

This chart says it all: net interest costs on the U.S. debt are projected to explode over the next decade, reaching $16.2 trillion. That is not just a line on a graph — it is a flashing warning light for the entire financial system.

When a government is forced to spend more and more just to service its debt, it has fewer options left. More borrowing, more money creation, and more pressure on the currency usually follow. That is exactly how inflation becomes entrenched — and if this spiral keeps accelerating, the risk of hyperinflation cannot be ignored.

This is why hard assets matter. When confidence in debt, deficits, and currency management erodes, investors look for stores of value that cannot be printed away.

The math is getting harder to ignore.

#DebtCrisis #USDebt #InterestRates #Inflation #Hyperinflation #FiscalPolicy #FederalReserve #MoneyPrinting #DeficitSpending #MacroEconomics #Gold #Silver #PreciousMetals #HardAssets #FinancialMarkets #EconomicWarning #RecessionRisk #WealthProtection #SoundMoney #Investing

1

70

This Map Shows Credit Card Debt Is Quietly Destroying Younger Generations — Act Now Before It’s Too Late

The lifetime cost of credit-card use isn’t just a number on a chart — it’s a financial trap that stacks up into the hundreds of thousands by middle age, and the next generation is walking straight into it. The Visual Capitalist map (sourced to JG Wentworth) shows the average American will rack up roughly $388k–$398k in credit-card debt over a lifetime, with some states topping nearly $485k — that’s mortgage-sized damage from revolving balances and interest alone.

Why this matters right now

Revolving balances compound: carrying months of unpaid balances at high rates turns small purchases into massive lifelong costs.

Geographic gaps show policy and education work: states with financial-literacy requirements tend to have the lowest lifetime card totals — prevention scales.

Young people face higher real costs: wage stagnation, rising living expenses, and easy credit mean millennials and Gen Z will shoulder more of this burden unless behavior and systems change.

Three urgent actions every business owner and creator should share

Teach one clear rule: pay the full statement each month or the math destroys your future wealth.

Push financial literacy in your networks and hiring: small policy changes (courses, workshops) lower lifetime debt averages.

Build content that normalizes living below means and using credit responsibly — social proof beats advertising.

Quick example to share with your followers

If someone averages $400k in lifetime credit-card debt, that’s roughly $600–$700 a month in principal (before interest) stretched over decades — with interest, the true cost is far higher and compounds much earlier.

If you care about the next generation’s financial future, this map should be a wake-up call — not a shrug. Share this post, start the conversation in your company or community, and demand better financial education for students and employees today.

#CreditCardDebt #FinancialCrisis #PersonalFinance #MillennialMoney #GenZ #FinancialLiteracy #DebtTrap #VisualCapitalist #JGwentworth #MoneyMatters #DebtFree #WealthBuilding #FrugalLiving #BusinessOwner #Entrepreneurship #EdmontonBusiness #ContentCreator #Finance #Investing #Savings #Budgeting #PayYourBalance #StopRevolving #TeachFinancialLiteracy

2

2

120

The Quiet Recession No One Wants to Admit: People Are Working… But Still Can’t Afford to Live

This chart says a lot more than it looks like at first glance.

The industries with the highest quit rates right now are:

Accommodation & food services (4.3%)

Retail (3.1%)

Other services (2.7%)

Transportation & warehousing (2.3%)

These aren’t luxury jobs people are walking away from.

These are the exact sectors that millions of people rely on just to survive.

So what’s really happening?

People aren’t quitting because they’re thriving.

They’re quitting because the math no longer works.

Low wages rising rent expensive groceries unstable hours = burnout.

This is what a “quiet recession” looks like:

Employment numbers look fine on paper

But real purchasing power is collapsing

And more people are living paycheck to paycheck than ever before

Meanwhile, the lowest quit rates are in government jobs…

Why?

Stability. Predictable income. Benefits.

In today’s economy, stability is becoming more valuable than opportunity.

As a business owner, this should be a wake-up call.

If you want to attract and keep good workers today, it’s not just about pay — it’s about:

Consistent hours

Predictability

Respect

A path forward

Because people aren’t just chasing money anymore…

They’re trying to survive.

What are you seeing in your industry right now?

#economy #recession #inflation #jobs #labormarket #workforce #smallbusiness #entrepreneurship #hiring #leadership #canada #usa #finance #economictrends #businessgrowth #sidehustle #wealth #money #paychecktopaycheck #costofliving #housingcrisis #foodprices #macro #investing #gold #silver #wallstreetbullion

1

96

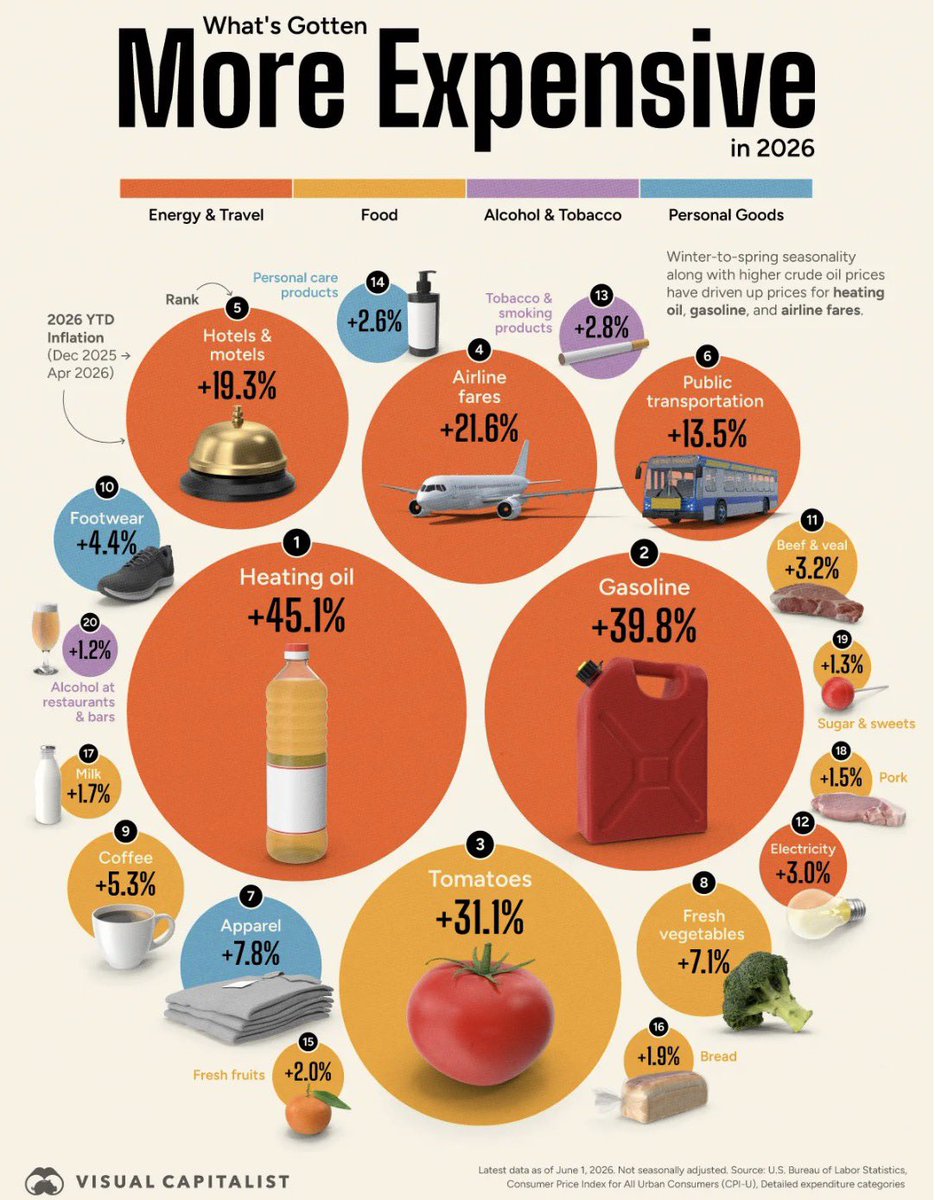

Warning: Your Money Is Getting Crushed Right In Front of You

This graphic says what a lot of people are feeling every time they buy fuel, food, travel, or even basic household items: the cost of living keeps climbing while the dollar buys less and less. When money is created faster than real productivity, inflation shows up everywhere — not just in headlines, but in your everyday life.

The uncomfortable part is that inflation is not evenly spread. Some categories like heating oil, gasoline, tomatoes, airline fares, and hotels have surged far beyond what most people expect, which is why a “normal” monthly budget can suddenly feel broken.

This is why people need to pay attention to saving, investing, and protecting purchasing power instead of just “working harder” and hoping prices stop rising. When currency is diluted, hard assets, businesses, and productive skills matter more than ever.

Warning: if your money is sitting still, it may be moving backward in real terms.

#Inflation #MoneyPrinting #PurchasingPower #CostOfLiving #Economy #CanadianEconomy #PersonalFinance #WealthProtection #HardAssets #Silver #Gold #FinancialFreedom #MacroEconomics #Recession #InflationHedge #SavingMoney #Investing #WealthBuilding #LinkedInPost #BusinessOwner #Entrepreneur

2

80

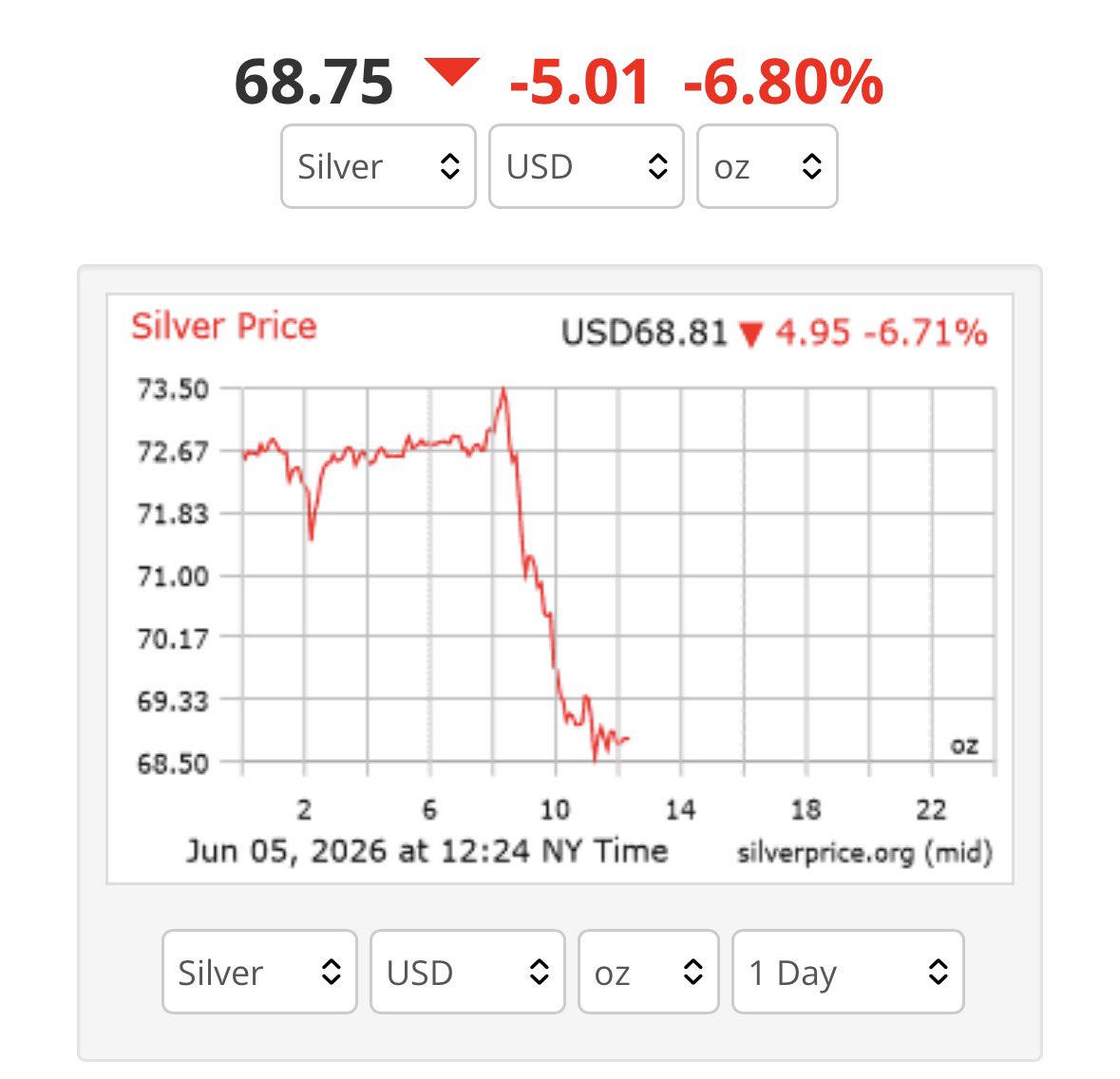

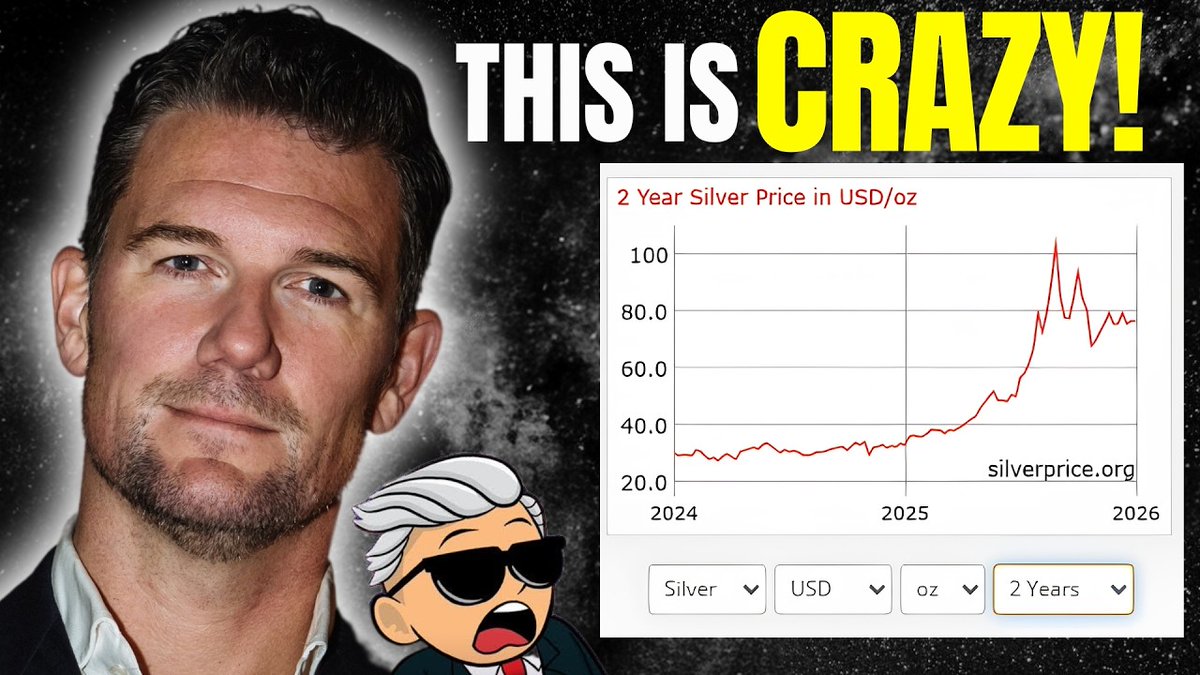

Silver just crashed — panic, manipulation, or a buying opportunity?

Silver got hit hard today, and moves like this usually happen when traders rush to de-risk, the dollar strengthens, rates shift, or profits get taken off the table fast. Silver also tends to move more violently than gold, so the downside can look brutal when momentum flips.

The bigger question is whether this is just a sharp shakeout in a volatile metal, or the market telling us something deeper about risk appetite, inflation expectations, and positioning. CME notes silver is used as a safe haven and is closely tied to broader risk management and volatility.

Is this a temporary flush, or the start of a much bigger move?

#Silver #SilverPrice #PreciousMetals #Investing #Markets #Commodities #Gold #Inflation #InterestRates #FederalReserve #Macro #Trading #Finance #Bullion #WealthPreservation #AssetProtection #MarketUpdate #EconomicNews #Metals #SilverStacking

6

316

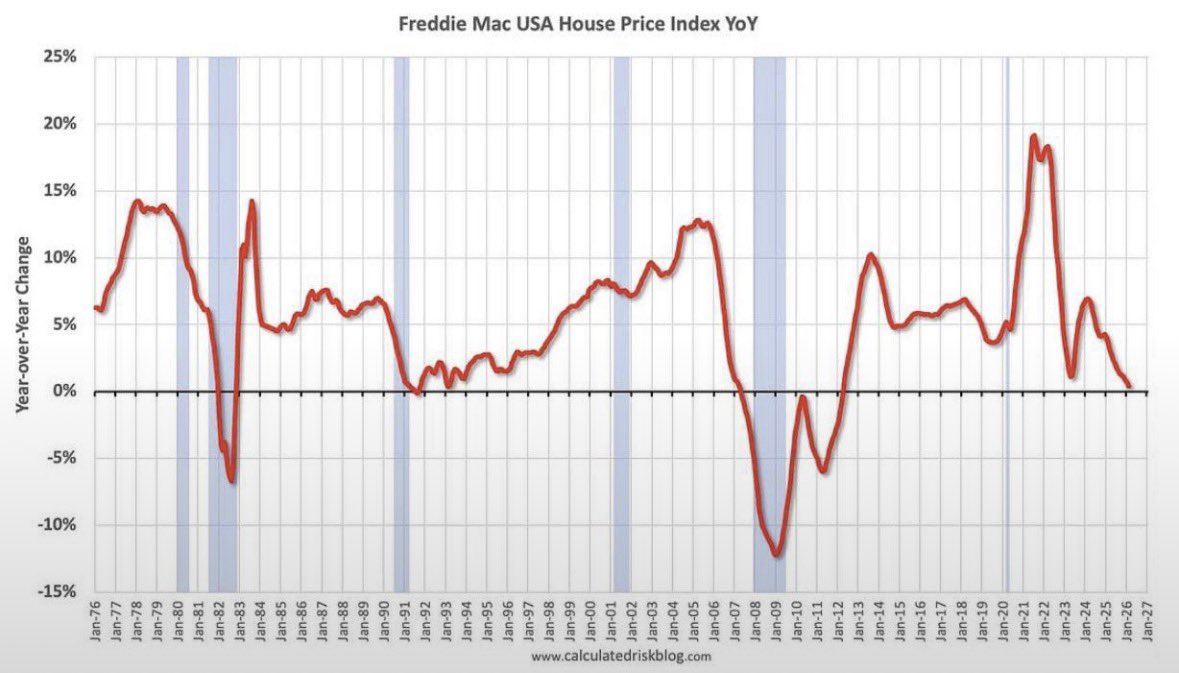

U.S. Home Prices Are About to Go Negative for the First Time Since 2007

The Freddie Mac House Price Index is showing a major slowdown, and the next move could be a big one. According to Freddie Mac’s own index, national home price growth was up just 0.7% year-over-year in March 2026, a new cycle low, and analysis from Calculated Risk says house prices are under pressure and could turn negative sometime in 2026.

That matters because the last time U.S. home prices went negative on a sustained basis, it came before the 2008 financial crisis. This does not mean we are replaying 2008 exactly, but it does mean the housing market is under real stress from higher mortgage rates, weaker affordability, and slowing demand.

The key question now is simple:

Are we watching a normal cooldown, or the start of a deeper reset?

For investors, homeowners, and anyone watching the economy, this is one chart worth paying attention to.

#HousingMarket #RealEstate #USHousing #FreddieMac #HomePrices #MarketUpdate #Economy #Recession #RealEstateInvesting #FinancialMarkets #MacroEconomics #Inflation #InterestRates #MortgageRates #AssetPrices #WealthBuilding #Investing #HousingCrash #RealEstateMarket #MarketTrends

1

2

137

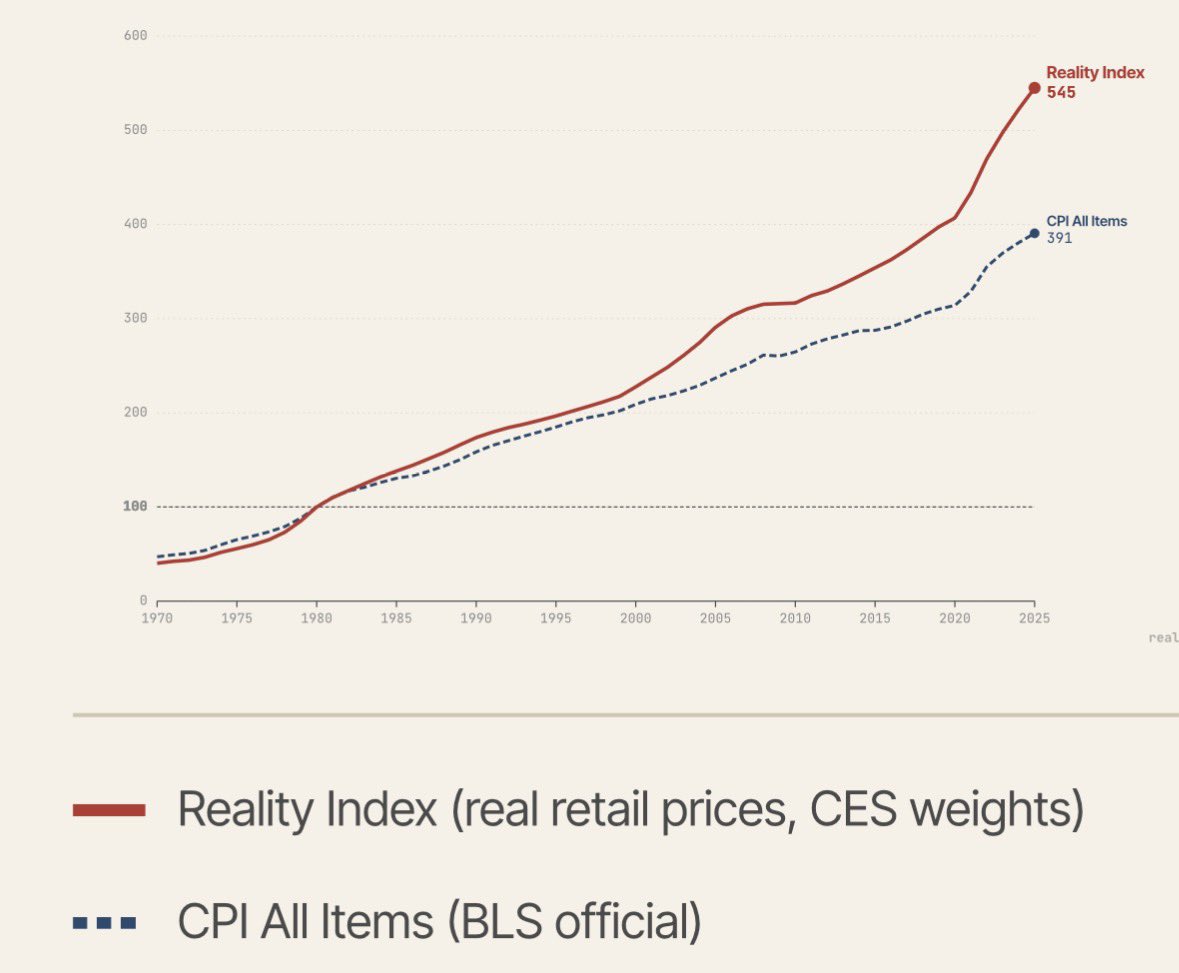

WE HAVE BEEN IN A DEPRESSION SINCE 2020

What we’re being told and what people are actually living through are not the same thing.

This chart is a reminder that official numbers often don’t tell the full story. When real-world prices keep climbing faster than what’s reported, everyday families feel it first. That’s why so many people think we’re already in a recession, or worse, a depression.

When the cost of living rises, savings lose value, and wages don’t keep up, people get squeezed hard. The truth is simple: you cannot build wealth by ignoring what is happening to purchasing power.

Pay attention to real assets. Pay attention to hard money. Pay attention to what protects wealth when the system gets shaky.

#RealityCheck #Inflation #CPI #CostOfLiving #Recession #Depression #Economy #EconomicTruth #Finance #Investing #MoneyPrinting #PurchasingPower #WealthProtection #HardAssets #Gold #Silver #PreciousMetals #SoundMoney #MacroEconomics #FinancialFreedom #AssetProtection #MarketTrends #EconomicCollapse #RealPrices #LinkedInFinance #BLS #RetailPrices #MiddleClass #WealthPreservation #EconomicData #Truth

1

7

178

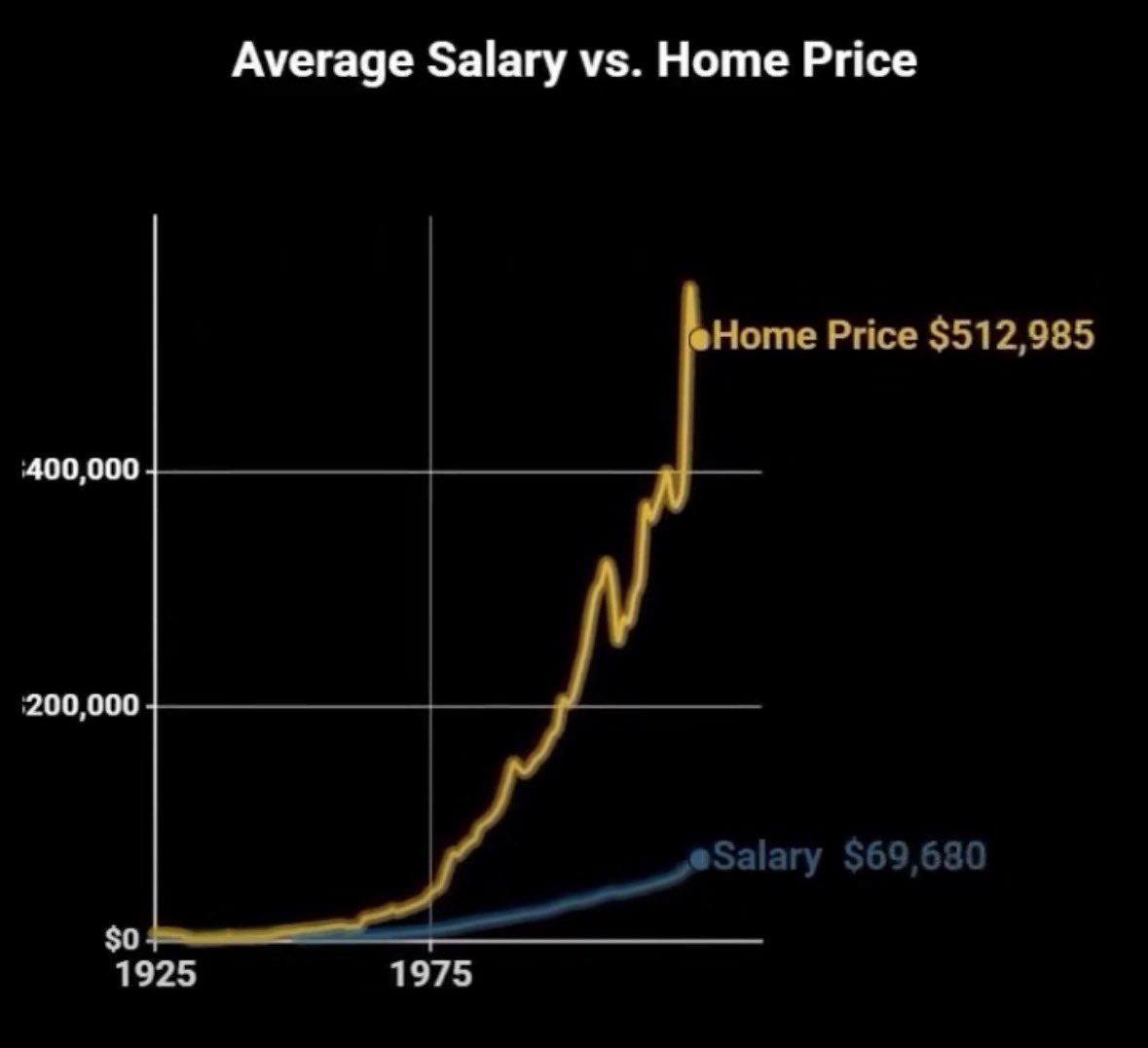

Why Is Owning a Home So Out of Reach Now?

This chart says what so many people are feeling right now: home prices have raced far ahead of wages, and the gap keeps widening. When the average home is priced above half a million dollars while average salary growth lags far behind, ownership stops feeling like a milestone and starts feeling impossible.

This is the real affordability crisis. It is not just about interest rates or short-term market swings. It is about a basic mismatch between what people earn and what housing now costs, and that disconnect has been building for decades.

For younger buyers, first-time buyers, and even established workers trying to move up, the question is simple: how is anyone supposed to catch up when wages have not kept pace with the cost of shelter? If incomes do not rise meaningfully while housing keeps climbing, affordability will keep breaking down.

The hard truth is that a market can stay expensive longer than people expect, but it cannot stay disconnected from reality forever. The longer this gap lasts, the more pressure builds on households, renters, and the broader economy.

#HousingCrisis #AffordableHousing #RealEstate #HomePrices #Wages #CostOfLiving #Inflation #FirstTimeHomeBuyer #Economy #PersonalFinance #CanadianRealEstate #HousingMarket #LinkedInFinance #FinancialFreedom #Investing #WealthBuilding #MiddleClass #InterestRates #Renting #RealEstateMarket

2

127

WARNING: Your electric bill may not be the same next month.

This chart makes the trend hard to ignore: electricity prices are climbing fast in several states, and in some places they’re surging far above the U.S. average.

That matters because electricity isn’t a luxury expense — it’s a basic cost of modern life. When power gets more expensive, the impact spreads everywhere: households, small businesses, transportation, manufacturing, and overall inflation.

The biggest concern is that these increases often show up quietly at first, then hit hard all at once.

If energy costs keep rising like this, the pressure on consumers will only get worse.

#Electricity #EnergyCosts #Inflation #UtilityBills #CostOfLiving #ElectricRates #HousingCosts #Economy #FederalReserve #PriceGrowth #EnergyInflation #HomeCosts #StateEconomy #ConsumerCosts #Budgeting #WealthProtection #LivingCosts #PowerPrices #USEconomy #FinancialAwareness

4

106

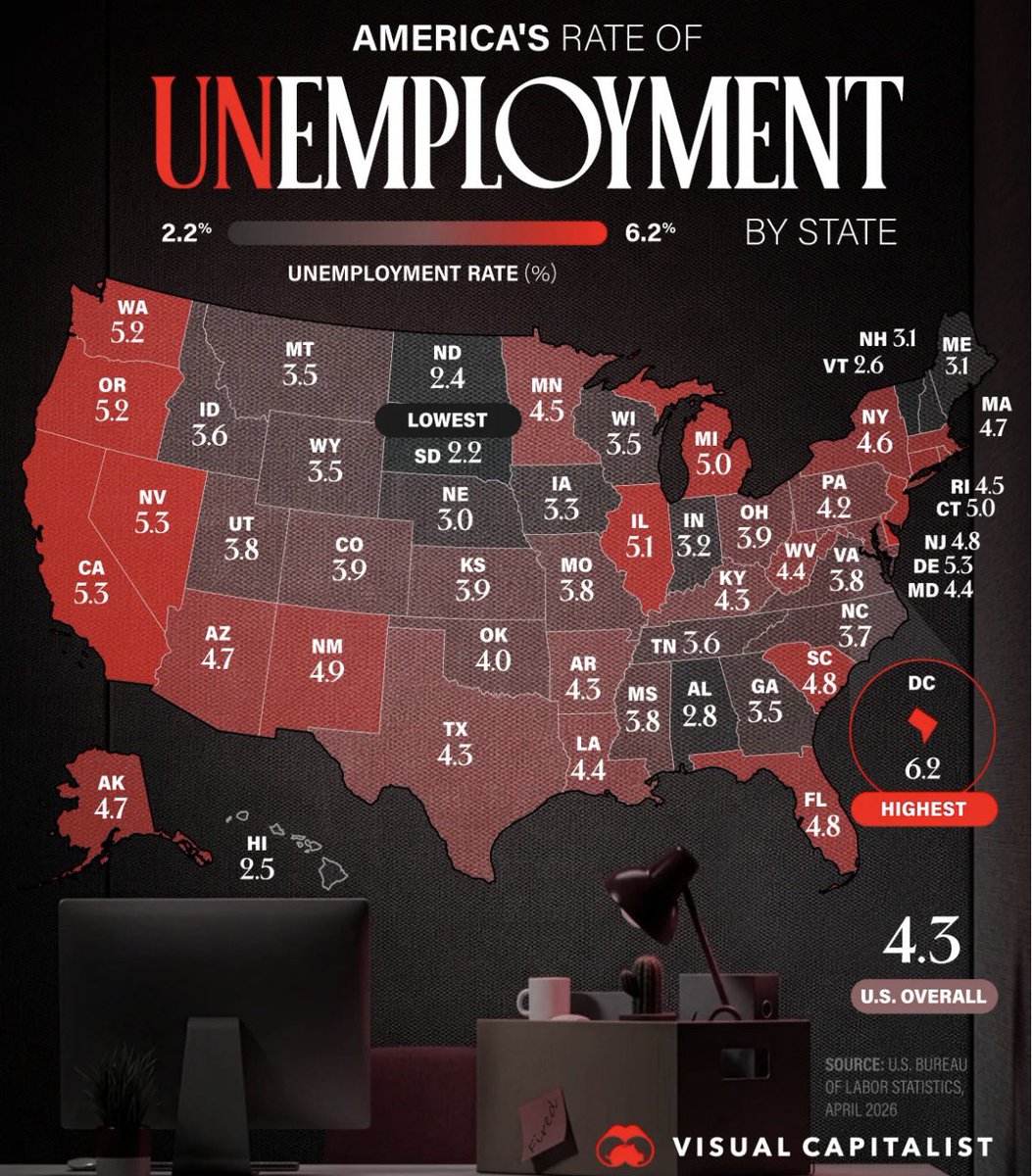

The Real Unemployment Rate Is Higher Than You Think… And It’s Signaling Something Bigger.

Take a closer look at this map.

At first glance, a 4.3% U.S. unemployment rate doesn’t seem alarming. In fact, it sounds relatively healthy.

But here’s the problem: headline numbers don’t tell the full story.

They don’t account for:

People who’ve stopped looking for work

Underemployed workers stuck in part-time roles

Those forced into lower-paying jobs just to stay afloat

When you factor those in, the real economic picture starts to shift.

Across multiple states, unemployment is quietly rising. Higher-cost regions are feeling the pressure the most, and even traditionally stable areas are beginning to crack.

This isn’t just a labor market story — it’s a demand story.

When people aren’t earning enough, they don’t spend.

When they don’t spend, businesses slow down.

And when that happens across the board… you’re no longer in a “strong economy.”

You’re in the early stages of a recession.

The disconnect between official data and real-world experience is growing. More people are feeling it in their day-to-day lives — even if the headlines say otherwise.

Pay attention to what’s happening beneath the surface.

That’s where the real signal is.

#economy #recession #unemployment #jobsreport #labormarket #economicoutlook #financialmarkets #macroeconomics #inflation #interestrates #investing #gold #silver #wealth #personalfinance #marketinsights #economicdata #businesscycle #entrepreneurship #linkedinfinance

1

3

96

Wall Street Bullion retweeted

May 28

"This Silver Price Move Has Me SERIOUSLY Worried Right Now" 👀

Our very own precious metal expert, @BartBrands1982, was on the official @WallStBullion podcast to talk about silver.

A must-see for anyone invested in AG! 👇

1

2

3

426

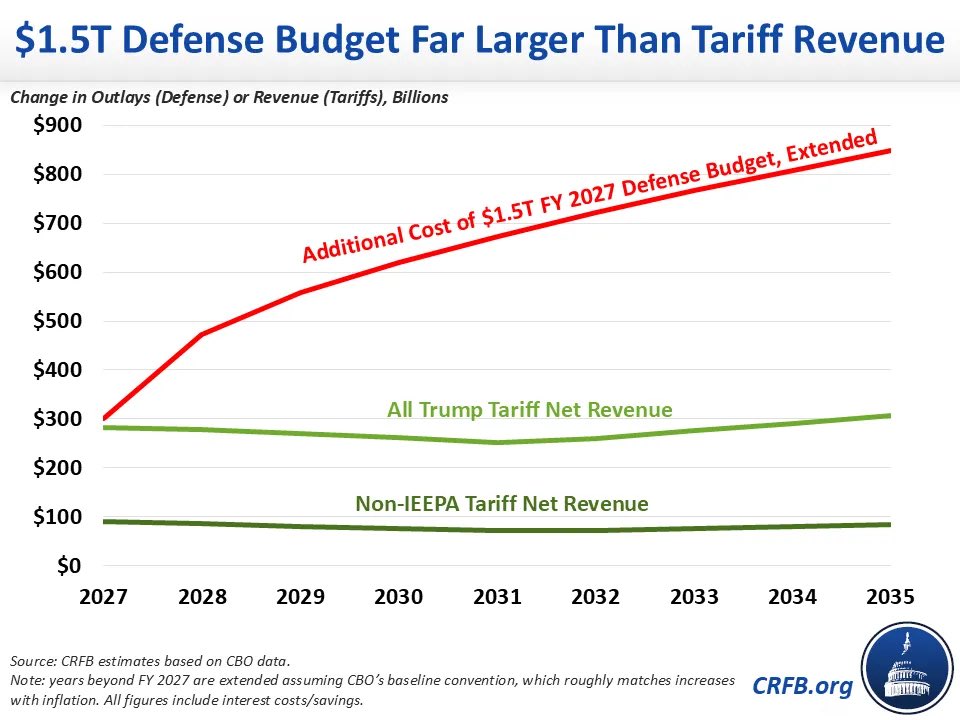

WARNING: The U.S. Is Now Spending $1 TRILLION on Interest… and $1 TRILLION on War — Is This How Empires Collapse?

Take a hard look at this chart.

The U.S. is on track to spend roughly $1.5 TRILLION annually on defense… while debt servicing alone is already approaching $1 TRILLION per year.

Let that sink in.

We are entering a phase where:

Interest on the debt rivals military spending

Military spending massively outpaces revenue sources like tariffs

Deficits are structurally locked in — not cyclical

Historically, this is not how rising empires behave.

It’s how late-stage empires operate.

The Roman Empire didn’t collapse overnight.

It eroded slowly under:

Rising military costs

Currency debasement

Unsustainable debt burdens

Sound familiar?

The real issue isn’t just the size of spending — it’s the composition.

When a nation spends more servicing past debt than investing in future productivity…

when defense budgets dwarf actual revenue streams…

when deficits become permanent…

You don’t get stability.

You get fragility.

Markets may ignore this today.

But math doesn’t negotiate forever.

The question isn’t if this matters.

The question is when does the system begin to break?

And more importantly…

How are you positioned if it does?

#Economy #DebtCrisis #MacroEconomics #Inflation #FederalReserve #USD #Gold #Silver #Investing #WealthProtection #FinancialFreedom #StockMarket #Recession #EconomicCollapse #Geopolitics #FiscalPolicy #Deficit #MoneyPrinting #HardAssets #PreciousMetals #Macro #Finance #GlobalEconomy

1

82

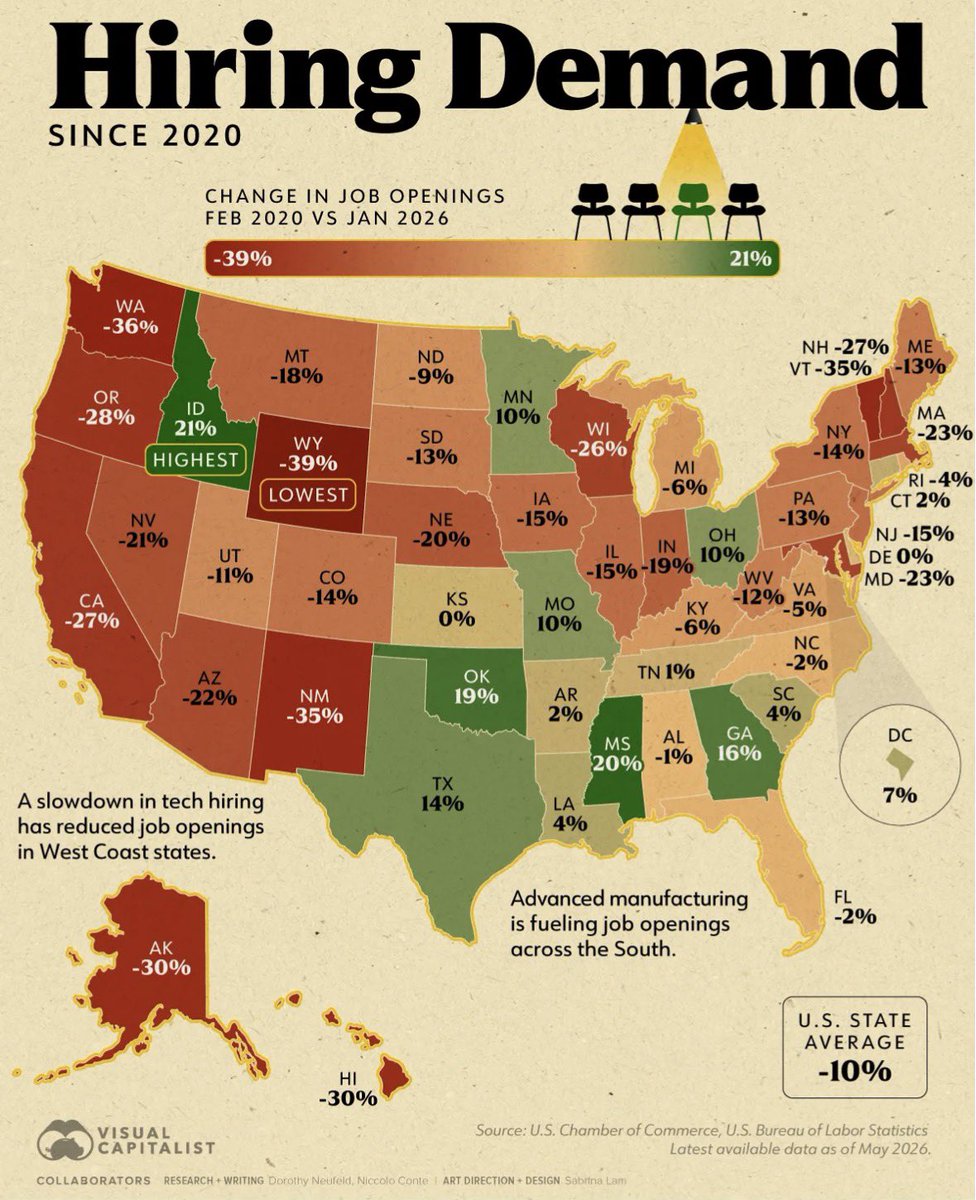

How Are People Supposed to Survive This Economy? Are We Already in a Hidden Recession?

Hiring demand has been weakening across much of the country since 2020, and for a lot of people, the real economy feels completely disconnected from the headlines. When job openings fall, costs keep rising, and day-to-day life gets tighter, people start realizing that survival is getting harder — even if the official story says things are “fine.”

This is what economic stress looks like in real life: fewer opportunities, more pressure, and households stretched to the limit. The public may call it a slowdown. Many people living it would call it a recession.

The scary part is that this pain is not evenly distributed. Some regions are still holding up, but others are seeing a major drop in hiring demand, which means more uncertainty for workers, families, and small businesses.

People do not need more spin. They need honest numbers, real wages that keep up, and an economy that works for everyday people again.

#Recession #Economy #Inflation #Jobs #JobMarket #Hiring #CostOfLiving #MiddleClass #WorkingClass #SmallBusiness #FinancialStress #USEconomy #LaborMarket #EconomicReality #PersonalFinance #WealthGap #Macroeconomics #EconomicCrisis #StayHumble #Truth

2

3

168

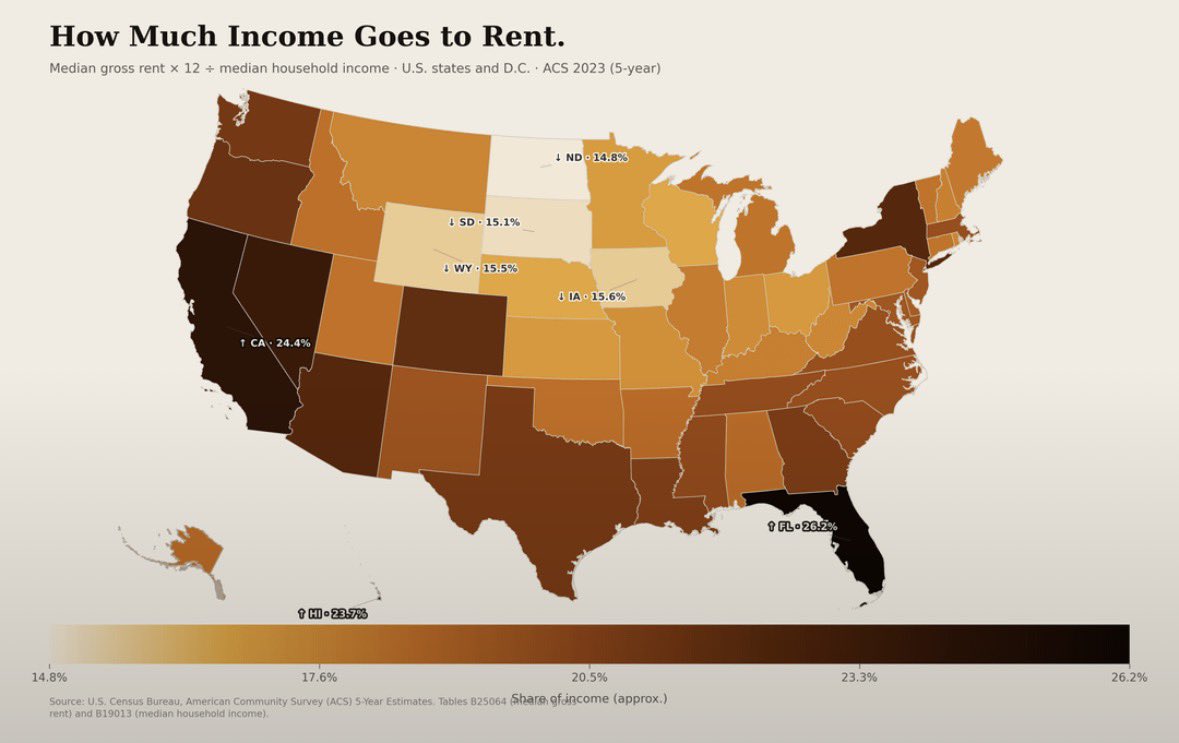

🚨 HOUSING CRISIS: AMERICANS ARE BEING PRICED OUT OF BOTH OWNING AND RENTING 🚨

This chart says everything.

Across the United States, a massive share of household income is now going directly to rent. In some states, it’s pushing well beyond what was once considered “affordable.”

The traditional rule was simple:

Spend no more than 30% of your income on housing.

But today, millions are already there—or dangerously close—just to rent.

Homeownership? For many, it’s no longer even on the table.

This isn’t just a housing issue. It’s a financial pressure cooker:

Less disposable income

Lower savings rates

Increased reliance on debt

Delayed life milestones

And when rent keeps rising faster than wages, people don’t just struggle—they fall behind permanently.

This is how wealth gaps widen.

This is how the middle class gets squeezed.

The real question is:

👉 How sustainable is this?

Because when people can’t afford shelter, the system is already breaking.

#HousingCrisis #RealEstate #RentPrices #CostOfLiving #Inflation #Economy #FinancialFreedom #MiddleClass #WealthGap #PersonalFinance #Investing #Gold #Silver #Macro #EconomicTrends #HousingMarket #Recession #Debt #Savings #WallStreetBullion

2

6

174

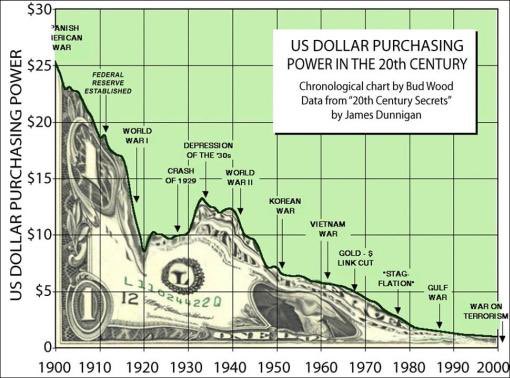

Wake Up Call: The Dollar’s Purchasing Power Is Being Quietly Destroyed

This chart says what most people feel but don’t want to admit: the US dollar has been losing purchasing power for decades. What once bought a meaningful share of goods and services now buys far less, and the decline has been relentless.

Inflation isn’t just a headline. It’s a hidden tax on workers, savers, retirees, and anyone holding cash while governments keep printing, spending, and devaluing the currency. The chart is a warning that “stability” in fiat money is often an illusion over long periods of time.

If you’re saving in dollars alone, you are not preserving wealth, you are slowly leaking it.

Hard assets matter. Cash flow matters. Ownership matters. And understanding monetary debasement matters more than ever.

The real question is not whether the dollar loses value, but how much more purchasing power we’ll sacrifice before people finally pay attention.

#USDollar #Inflation #PurchasingPower #MoneyPrinting #FiatCurrency #CurrencyDebasement #Gold #Silver #PreciousMetals #WealthProtection #FinancialLiteracy #EconomicWarning #SoundMoney #HardAssets #Investing #MacroEconomics #InflationHedge #WealthPreservation #CentralBanks #FederalReserve #DollarCollapse #MarketInsights #Finance #EconomicFreedom

2

1

5

107

History Doesn’t Repeat, But 2008’s Warning Is Still Loud

2008 is the reminder that markets can go from “everything is fine” to full panic very fast. The S&P 500 fell about 57% from its 2007 peak to its 2009 low, and Lehman Brothers’ collapse in September 2008 became the moment fear turned systemic.

Could something like that repeat? Yes — not in the exact same way, but the ingredients can rhyme: too much leverage, liquidity stress, crowded trades, and investors assuming central banks will always contain the damage.

The lesson is not to predict the exact day of the next crash. The lesson is to respect risk before the crowd does.

2008 didn’t just punish speculation. It showed how quickly confidence can vanish once credit freezes and forced selling begins.

That’s why cash flow, balance sheet strength, and risk management matter more than hype when markets get stretched.

#valueinvesting #growthinvesting #diversification #longterminvesting #financialfreedom #generationalwealth #wealthbuilding #compoundinterest

3

169

WARNING: Is Homeownership About to Become Out of Reach for the Middle Class?

Sixty years ago, the math looked very different. In 1965, a median family income covered a far larger share of a new home’s price than it does today, while by 2025 the affordability gap had widened sharply. New home prices rose about 1,975% from 1965 to 2025, while median family income rose about 1,478% over the same period.

And the purchase price is only part of the story. Ongoing homeownership costs also stack up fast: mortgage payments, property taxes, home insurance, utilities, maintenance, and unexpected repairs can add thousands per month depending on the home and market.

The result is simple: for many families, owning a home now means committing to a much larger share of income than previous generations ever faced. That is why affordability is no longer just a housing headline — it’s a household balance-sheet problem.

#Housing #RealEstate #Homeownership #Affordability #CanadianRealEstate #HousingMarket #MortgageRates #PropertyTaxes #HomeInsurance #CostOfLiving #FinancialFreedom #FamilyBudget #Inflation #WealthBuilding #Investing #Economy #InterestRates #CalgaryRealEstate #CanadaHousing #RentVsBuy #NewHome #HousingCrisis #PersonalFinance #MiddleClass #Money #Wealth #Markets #HomeBuying #AffordableHousing #Economics #Lifestyle

2

90