@i_montaigne @i_montaigneEN @Institut_IHES Former chief economist AXA/ chief European economist Morgan Stanley -- Fond of science and maths

Joined July 2016

- Tweets 19,729

- Following 1,335

- Followers 3,701

- Likes 29,391

1,058 Photos and videos

Pinned Tweet

5 Jun 2022

My tribute to the victims of the #TiananmenSquareMassacre on 4 June 1989

👉🧵1/7

3

11

36

Eric L Chaney retweeted

6 Dec 2025

Non, l’antisémitisme, d’où qu’il vienne, n’est ni résiduel, ni une « fake-news » : la réponse de Juifs et juives révolutionnaires à Julien Théry.

juivesetjuifsrevolutionnaire…

65

85

303

88,459

6 Dec 2025

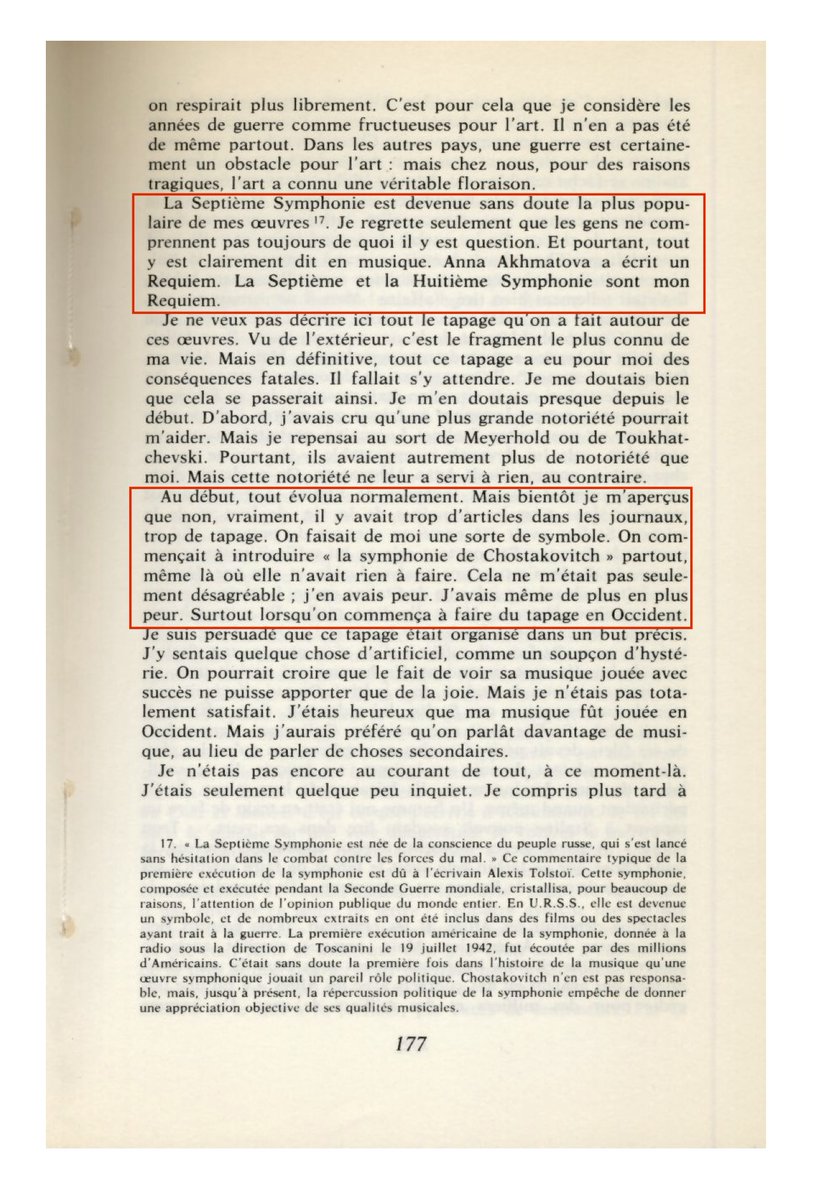

Entendu sur @francemusique : la 7e Symphonie de Chostakovitch est "le symbole de la résistance contre le fascisme"

Ce n'était pas du tout l'intention du compositeur

Il dit dans ses mémoires:

"La 7e et la 8e sont mon Requiem"

Le tapage à leur propos a failli lui couter la vie

5

176

Eric L Chaney retweeted

4 Nov 2025

Témoignage intéressant de Montebourg.

Une partie de la classe politique manifesterait donc un tel mépris pour ses électeurs qu'elle serait prête à flatter leurs bas instincts en proposant des mesures qu'elle sait délirantes, destructrices, spoliatrices et inapplicables pour le seul plaisir d'obtenir des voix.

Et si le cirque de la taxe Zucman obéissait à la même logique ?

Le pire de la politique.

3 Nov 2025

"Les fameux 75 % qu’avait inventés M. Hollande, c’était 75 % de papier parce qu’ils avaient imaginé un dispositif qui serait censuré par le Conseil constitutionnel". @montebourg

📺Extrait de #cdanslair spécial "Dette : un scandale français", le 9 novembre à 21h05 sur France 5

68

502

1,530

84,144

Eric L Chaney retweeted

4 Nov 2025

Bienvenue à Paris, bienvenue en France.

Les artistes y auront toujours toute leur place. La liberté de création y sera toujours défendue.

Les appels au boycott ou à la "recontextualisation" sont indignes.

4 Nov 2025

Bienvenue à l’Orchestre national d’Israël ce jeudi à la @philharmonie. Rien ne justifie un appel au boycott de ce moment de culture, de partage et de communion. La liberté de création et de programmation est une valeur de notre #République. Aucun prétexte à l’antisémitisme !

140

122

507

26,170

Eric L Chaney retweeted

4 Nov 2025

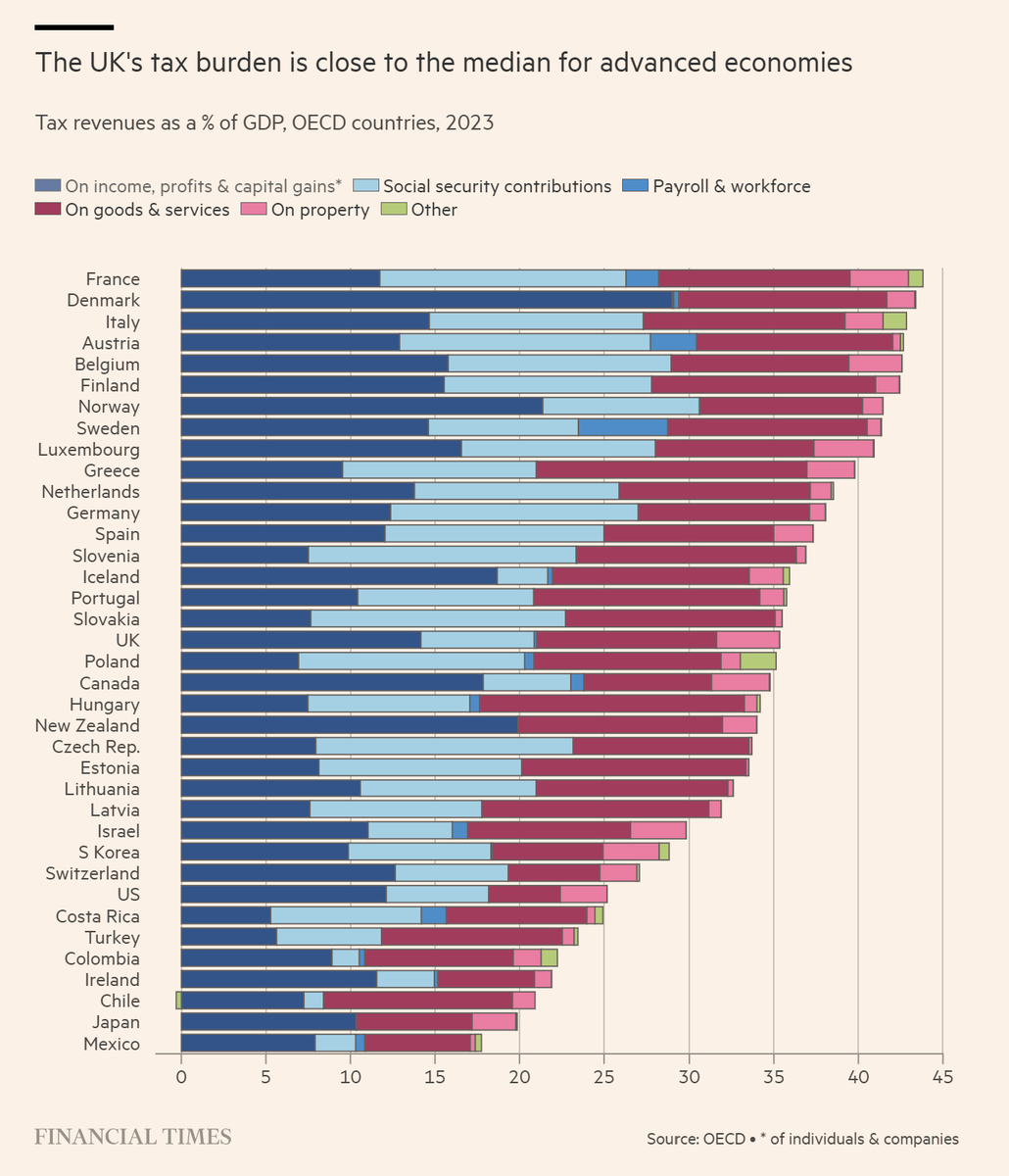

On the positive side --- I think this is an excellent graph in the FT on the breakdown of taxation in the countries of the OECD.

93

245

1,046

191,268

Eric L Chaney retweeted

4 Nov 2025

Zahra Tabari, une iranienne près de la potence.

Son crime? Un bout de tissu sur lequel sont inscrits les mots "Femme, Résistance, Liberté".

Aujourd'hui hélas, si vous n'êtes pas de Gaza, si Israël n'est pas à blâmer, personne n'entendra parler de vous, victimes de seconde zone.

99

1,188

2,872

37,487

Eric L Chaney retweeted

3 Nov 2025

If you have been curious about which topics are increasing in popularity in econ, @paulgp has a new tool for you!

paulgp.com/econlit-pipeline/…

This lets you search over AER and AEJ's 30k NBER WP!

Very neat!

2

89

345

50,243

5 Nov 2025

Meanwhile, a novel view of the Milky Way reveals stunning objects, remnants of exploded stars never seen before. Kudos to PhD candidate Silvia Mantovanini for her amazing work @ICRAR

1

1

4

190

Renonçant à toutes les précautions méthodologiques et épistémologiques, Wikipédia ratifie comme une évidence l'existence d'un "génocide à Gaza".

Il semble que Francesca Albanese, secondée par Rima Hassan et Aymeric Caron, ait rédigé ce document à charge.

C'est donc officiel : Wikipédia n'est plus qu'une officine de propagande férocement anti-israélienne (pour employer un euphémisme). Quand on sait le rôle que continue à jouer cette encyclopédie en ligne auprès des lycéens, des étudiants et même des enseignants, un article aussi éhontément orienté relève de la forfaiture.

fr.wikipedia.org/wiki/G�%A….

Début de l'article :

"Le génocide à Gaza est un génocide perpétré depuis octobre 2023 à l'encontre des Palestiniens de la bande de Gaza dans le cadre de la guerre qui s'y déroule. Il est orchestré par l'armée israélienne et découle de l'intention proclamée par de hauts dirigeants israéliens de détruire tout ou partie de la population gazaouie par le recours aux massacres, aux déplacements forcés de population, à la famine organisée et la destruction de la très grande majorité des infrastructures civiles et de la quasi-totalité des terres agricoles. D'abord contesté, l’usage de ce terme finit par s'imposer dans le débat académique pour désigner les actes de l'État d'Israël dans la bande de Gaza. Alors qu'une plainte auprès de la Cour internationale de justice est en cours d'instruction, il est reconnu comme génocide par l'International Association of Genocide Scholars en septembre 2025[29]."

119

302

879

74,704

Eric L Chaney retweeted

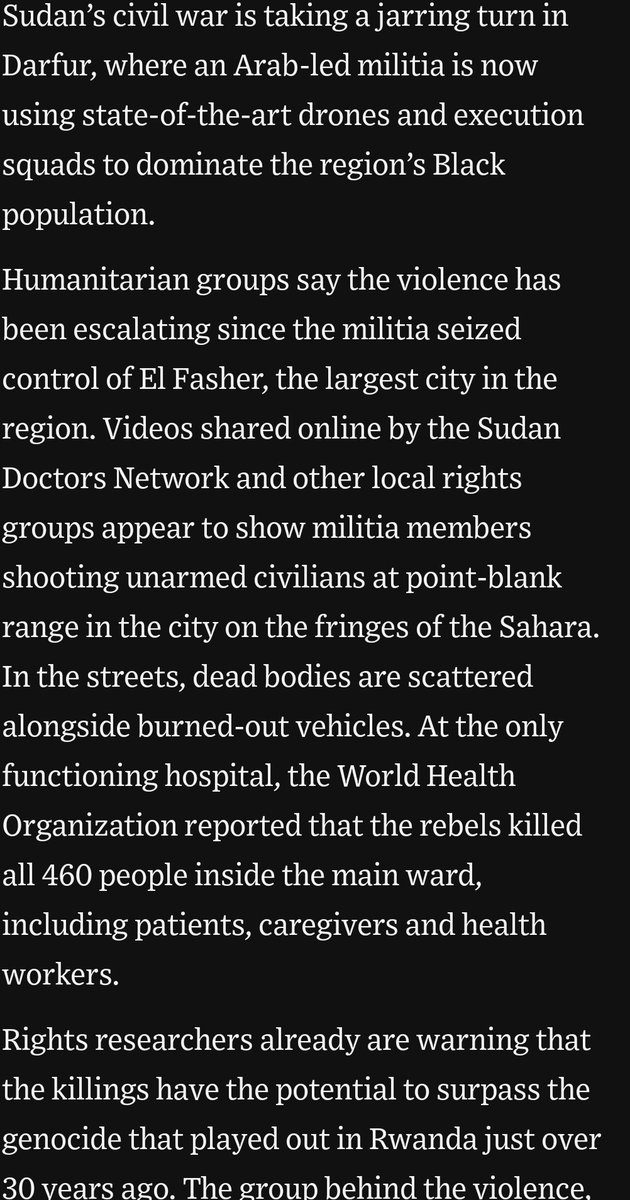

1 Nov 2025

A horrific mass murder is unfolding in Sudan, where no one can see it. The RSF are murdering civilians in el Fasher, after having finally defeated the Sudanese army forces holding out in the city. The BBC has managed to speak to a few who escaped

youtu.be/i7fC-Jf2V2g?si=Znbb…

91

1,320

3,050

522,804

Eric L Chaney retweeted

1 Nov 2025

The UAE is enabling a true genocide in Sudan that has the potential to be worse than what happened in Rwanda. Extremely shocking news. All the pressure of the world should be put on the UAE to stop. Source @wsj

1 Nov 2025

Sudan Militia, Armed With Drones, Hunts Down Black Population of Darfur. That headline says it all. Its pretty shocking that more attention isnt being paid to people actually being hunted down in broad daylight. wsj.com/world/africa/sudan-m…

2

35

98

12,486

Ozempic, MRI machines and flat screen televisions all emerged out of fundamental research decades earlier — the very types of study being slashed by the US government

go.nature.com/4nzp8vn

3

44

125

22,706

1 Nov 2025

Food for thought

31 Oct 2025

I crossed an interesting threshold yesterday, which I think many other mathematicians have been crossing recently as well. In the middle of trying to prove a result, I identified a statement that looked true and that would, if true, be useful to me. 1/3

282

1 Nov 2025

Meanwhile, there are economists doing serious work.

🙏 to @RevEconStudies for having published this brilliant paper

30 Oct 2025

Let me explain why I believe modern economics is such a powerful tool for understanding the world. I’ll do this by discussing a great paper by Simone Cerreia-Vioglio, @UncertainLars, Fabio Maccheroni, and Massimo Marinacci, “Making Decisions Under Model Misspecification,” published in the Review of Economic Studies a few months ago.

Imagine I want to drive from UC San Diego to UCLA, but I’ve never driven that route before. I need to build a “model of the world” to guide me, which we usually call a map. Maps are simplified representations of reality. They can’t include every detail if they’re to be useful. Borges, in his short story On Exactitude in Science, makes this point beautifully. (In practice, I don’t draw the map myself—I use an app—but someone still had to make it.)

Because maps simplify, I can’t fully rely on them. Maybe last night’s storm knocked down a tree and closed a street, or there’s construction and the ramp off the highway in LA is shut down.

This uncertainty matters. Suppose I’m driving to UCLA for an important talk at 11 a.m. If the ramp is closed, I might need 15 extra minutes. When should I set my alarm to arrive on time, while still getting enough sleep to give a good talk?

The problem is that I can’t assign precise probabilities to all these contingencies. How likely is the fallen tree? Or new roadwork? Even the best traffic apps can’t capture every disruption, and some might happen after I’ve already left.

In economic terms, my “model of the world” (the map) is misspecified—and no matter how hard I try, I can’t fully fix that.

But sitting down and crying about misspecification doesn’t answer my basic question: when do I set the alarm? Too early, and I’m exhausted. Too late, and I’m late.

Simone and his co-authors offer a way to think about this. They start from the idea that we often hold several structured models of an economic phenomenon, grounded in theory. For example, a central bank might use a standard New Keynesian model and a search-and-matching model of money.

Yet, aware that each model is misspecified by design, the bank adds a protective belt of unstructured models—statistical constructs that help it gauge the consequences of misspecification.

The beauty of the paper is that it provides an axiomatic foundation for this protective belt (and even generalizes it to include a Bayesian approach). It shows that if a decision-maker’s preferences meet certain conditions —reflecting both rational and behavioral features— then those preferences can be represented by an augmented utility function that formally accounts for misspecification.

Crucially, we don’t assume that augmented utility function; we derive it. We start with general, plausible properties of preferences and prove that they imply such a representation.

That’s real progress. Instead of writing endless critiques of expected utility or rational expectations (as many have done for decades, with little to show), we now have a formal way to reason about misspecification—precise definitions, clear boundaries of validity, and awareness of what we still don’t know.

Take, for instance, a brilliant Penn graduate student on the market, Alfonso Maselli

economics.sas.upenn.edu/peop…

His job-market paper pushes this frontier further. He studies cases where a decision-maker not only faces model misspecification but is also unsure which model best fits the data and can’t assign probabilities to them—what we call model ambiguity. In my example, the central bank is unsure whether the New Keynesian or the search-and-matching model fits better, and it worries that both might be incorrect.

If you read Simone et al. or Alfonso’s paper, you’ll see how misguided—and, frankly, cartoonish—many of the recent criticisms of economics on X have been.

First: the idea that economists don’t understand math or have “physics envy.” The math in these papers is subtle and advanced—utterly different from what physicists do (neither better nor worse, just distinct). An engineer transitioning into economics would find these tools unfamiliar.

Second: claims of ideological bias are unfounded. I have no idea about the political views of the authors, and I’d be surprised if anyone could infer them from the analysis—beyond vague guesses about typical academics.

Third: This has almost nothing to do with what one learns as an undergraduate, or even in first-year graduate school. If your knowledge of economics stops at an intro textbook, it’s best not to pontificate on the field’s frontiers.

Fourth: Is this science? Debating that word’s boundaries is pointless; every definition of “science” breaks down somewhere.

The Germans solved this long ago with the idea of Wissenschaft—the systematic pursuit of knowledge, whether of nature, society, or the humanities. By that measure, modern mainstream economics is clearly a Wissenschaft: a disciplined, cumulative, and highly useful effort to understand how the world works. Simone and his co-authors have demonstrated that beyond any reasonable doubt.

280

1 Nov 2025

Si on taxe les fonds d’assurance-vie en euros, largement investis en obligations publiques, comme étant « improductifs », c’est donc qu’on estime les dépenses publiques improductives.

J’ai du me tromper quelque part, c’est sûr🤔

5

27

80

2,855

1 Nov 2025

(fatiguant à la longue … devoir partager presque chaque post de @sc_cath, auquel il n’y a rien à ajouter)

1 Nov 2025

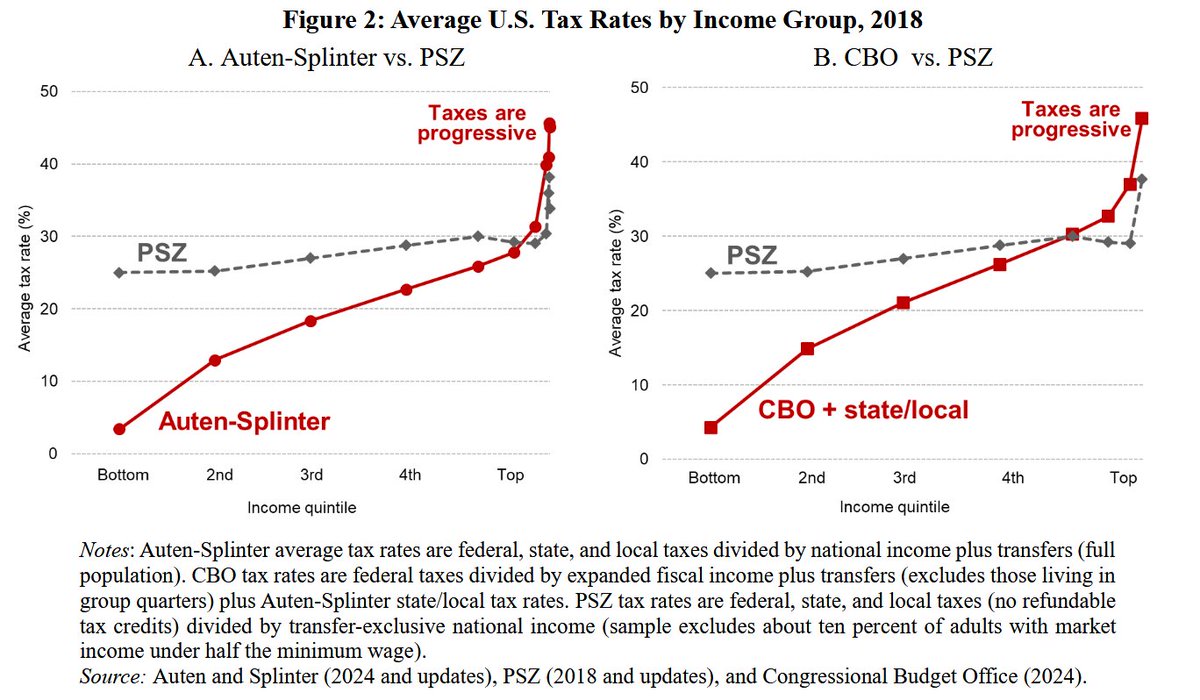

Même si les choix sont politiques, ils doivent être informés par des données et des arbitrages dont la présentation est, par nature, technique.

Or, dès lors qu’une proposition s’appuie sur une description politique des données, cela devient problématique.

La décision politique du citoyen doit être éclairée. Or, lorsque des économistes présentent des graphiques de taux de prélèvements obligatoires dont la méthodologie implique que recevoir une aide sociale ou un crédit d’impôt *augmente* le taux d’imposition des classes populaires et donne une apparence régressive au système fiscal, il y a de toute évidence un souci. On prive alors le citoyen de sa capacité à faire un choix éclairé, en le traitant comme un abruti.

Que le service public de l’audiovisuel déploie de telles ressources pour participer à cette entreprise constitue également un problème.

1

1

9

1,243

Eric L Chaney retweeted

26 Oct 2025

C’est marrant de suivre ce débat dans deux pays.

Tiré d’un papier d’octobre 2025 de David Splinter : en gris, le fameux graphique de Piketty, Saez et Zucman du taux moyen d’imposition par quintile de revenu dans sa version américaine. En rouge, la version corrigée des transferts, des crédits d’impôt et de la neutralisation de certains choix méthodologiques bizarres.

Parmi ces choix bizarres, on retrouve le fait que, plus les ménages à faible revenu reçoivent d’allocations sociales ou de crédits d’impôt, plus la méthode de PSZ conclut que leur taux d’imposition est élevé.

Je traduis : « Pour les ménages à faible revenu, les taux d’imposition PSZ sont surestimés, car ils incluent les taxes sur les ventes dans le numérateur mais omettent, au dénominateur, les revenus de transfert utilisés pour financer ces achats. Ils ne tiennent pas non plus compte des crédits d’impôt remboursables. »

25 Oct 2025

Sur la taxe Zucman, je ne comprends plus rien. On est parti d’un trou dans la raquette pour les gens qui ont plus de 100 millions d’euros de patrimoine.

Même les chercheurs les plus idéologues s’accordent pour reconnaître qu’hormis ce trou précis dans la raquette, notre système est très progressif pour les autres ! Je répète, excepté ce problème très précis et circonscrit, il n’y a AUCUN problème de justice fiscale. Les riches payent énormément.

Avec la taxe Zucman « Light », c’est du délire, on crée en fait un super ISF (3% !) sur les patrimoines 10 fois plus modestes, dont le rendement peut tout à fait être à peu près nul. C’est une expropriation en quelques années. Au secours.

43

441

1,560

421,698

Eric L Chaney retweeted

26 Oct 2025

🚨Condamnée à mort pour avoir écrit

Femme, Résistance, Liberté ✍️

Au procès de 10 min, Zahra Shahbaz Tabari ingénieure électricienne (67 ans) est accusé de soutenir l’opposition démocratique OMPI

📢 Soyons sa voix

✊Partageons #FemmeRésistanceLiberté !

fr.ncr-iran.org/communiques-…

8

267

310

20,706