FinTech enthusiast sharing daily insights, good reads and deep dives at the intersection of finance and technology

Joined November 2023

- Tweets 21

- Following 75

- Followers 18

- Likes 34

Photos and videos

FintechPod retweeted

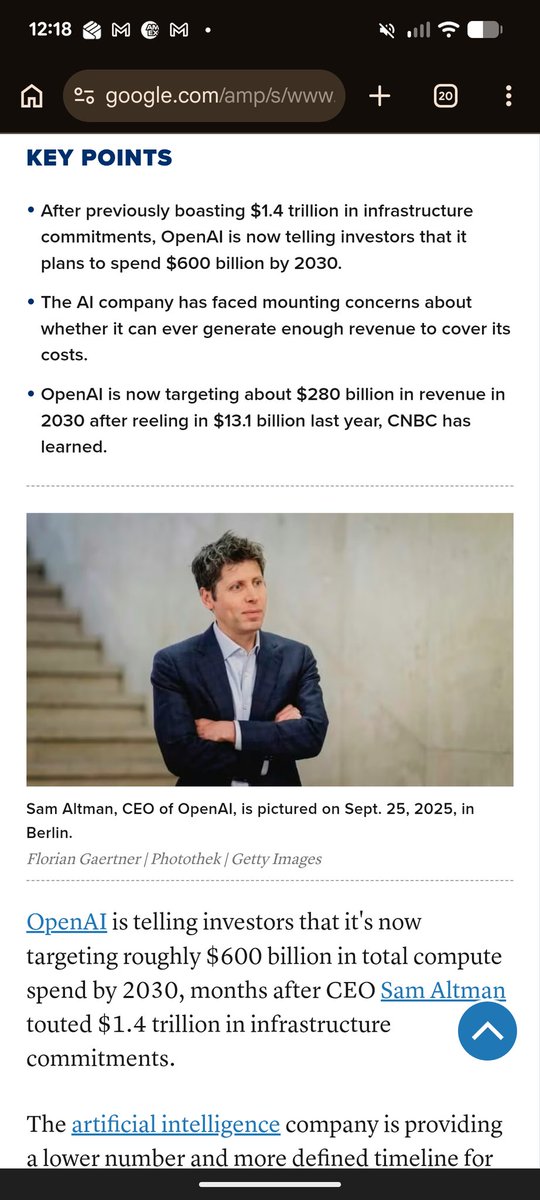

We are in a market that shoots first and reasons later. 6% decline in $DASH is an indication of market raising odds of disruption risk.

@benthompson put out a compelling case on $DASH not being an AI loser.

An expensive stock can derate even if biz is going to be fine.

2

1

410

FintechPod retweeted

Continue to believe that market is not giving any credit to data moats and just focusing on what can be automated.

Case in point, #Anthropic calling out $TRI as the only place to get Westlaw data.

If you have data, then you will be more insulated.

$MDB, $VEEVA, $TRI, $SNOW

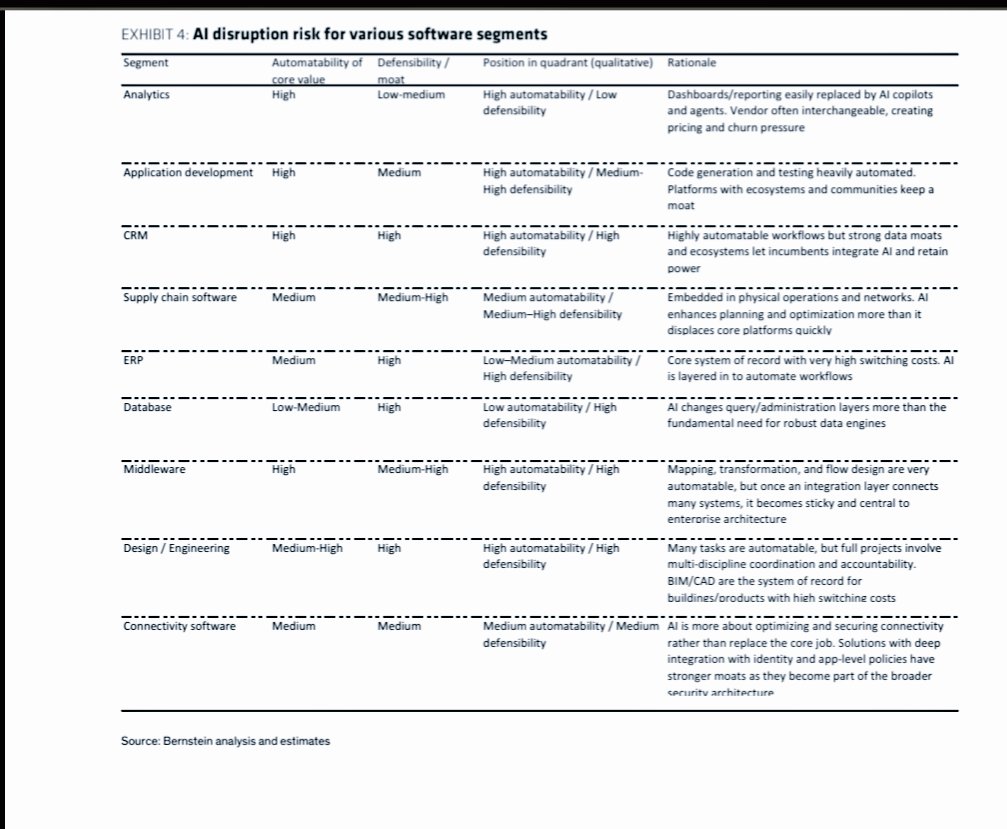

Bernstein put out a framework to evaluate disruption risk to software companies from AI. Framework uses

Automatability and Defensibility.

Seems like market is only focusing on automation risk right now and does not give any credit to data moats.

$CRM, $MDB, $NOW, $TEAM, $ADBE

1

8

1,315

FintechPod retweeted

19 Feb 2024

Never seen a commodity market where demand does not create its own supply. Right now, new housing construction is not concerning. If construction pace picks up and continues for few more years then we may have to start worrying about inventory. Nothing like GFC though.

1

2

7

2,405

FintechPod retweeted

24 Nov 2023

Celebrating Shopify merchants around the globe on the most important weekend of the year!

Absolutely stunning - thank you @SphereVegas 🤩🌎

9

17

248

52,268

24 Nov 2023

Asking all the FinTech influencers out there, For a young professional starting to write about FinTech. What will be your advice to get started?

@sytaylor @aakashgupta @AlexH_Johnson

@SamBobLev @PopularFintech @rshevlin

Please tag folks who can provide valuable input! Thanks!

4

1

5

400

24 Nov 2023

@pitdesi @TheRudinGroup @RAlexJimenez @mikulaja @alexxubyte @davidbrear @Arjun_Vir_Singh @BrettKing @siracusa @LexSokolin @MaryMWisniewski @NikMilanovic @obussmann @rexsalisbury

1

90

24 Nov 2023

1) Interesting read! In hyper competitive payment world where payment services are often considered commoditized there is still evidence that players who follow a clear value proposition do better than others

22 Nov 2023

When Adyen dropped 50% many said “payments is a race to the bottom.” Things are never so simple. Margin matters, but so does value. How do you drive both? 👇

🧠🧠🧠

The argument for race to the bottom

The thesis goes there are two paths.

👉 Compete for big contracts (Adyen). This "forces you to lowball" on price.

👉Go after small businesses (Stripe). This forces you to go wide to service the business that balloons expenses, killing margins in time.

The thesis says- This results in short-term growth spurts, but long-term payments companies are forced to compete their profits away.

But it's wrong.

That’s not the only dimension companies compete on.

🧠🧠🧠

The new battleground is performance

Payments are easy; but the edge cases are hard. Companies that solve the most edge cases increase conversion at checkout, which increases revenue for their clients.

What drives value depends on which of the 5 types of customer is buying.

👉 The price-sensitive juggernaut (e.g., Walmart). Wants the lowest possible price and will take on work and complexity to achieve it.

👉 The global tech enterprise (e.g. Airbnb). Values price, stability, and global reach.

👉 The mid-market retail, e-com brand. (e.g. Asos). Values market reach and conversion.

👉 Small and medium businesses. (e.g. boutique coffee shops). Values ease of use and breadth of offering like payroll or inventory.

👉 Legacy merchants coming to e-commerce late with “omnichannel.” (e.g. department stores). Needs to simplify their operations and reduce multiple platforms to a single platform.

🧠🧠🧠

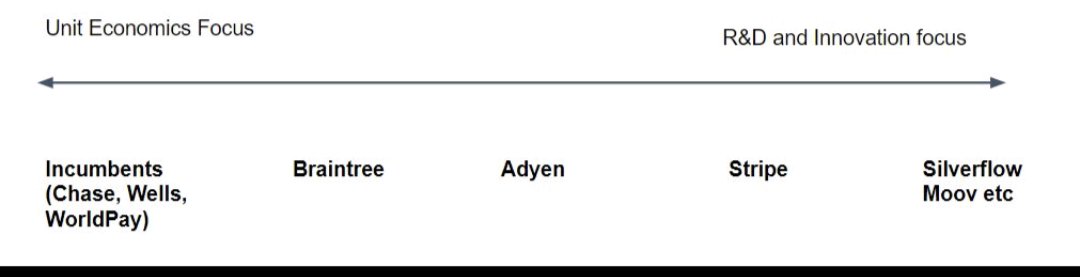

Different providers compete more on price or more on R&D and performance depending on a number of factors.

👉 Incumbents like Chase Paymentech offer strong unit economics by packaging the whole offering as a bank (Chase) that can cross-sell much more.

👉 Scale digital companies like Adyen offer a single global platform, but compete on unit economics.

👉 Scale players like Stripe are the default choice for small companies and platforms.

👉 New entrants like Nuevi, Checkout and Moov are pushing the R&D and performance barrier to win younger companies.

🧠🧠🧠

Payment’s isn’t a race to the bottom it’s a two dimensional axis. Price vs performance.

What drives performance depends on what your goals are as a business.

Find more on the blog (you know where to get it)

1

1

2

189

24 Nov 2023

2) And, I believe as merchants are putting more emphasis on customer remittance experiences rather than just pricing, there is still opportunity for payment service providers to differentiate on value rather than just margins

1

1

78

FintechPod retweeted

22 Nov 2023

When Adyen dropped 50% many said “payments is a race to the bottom.” Things are never so simple. Margin matters, but so does value. How do you drive both? 👇

🧠🧠🧠

The argument for race to the bottom

The thesis goes there are two paths.

👉 Compete for big contracts (Adyen). This "forces you to lowball" on price.

👉Go after small businesses (Stripe). This forces you to go wide to service the business that balloons expenses, killing margins in time.

The thesis says- This results in short-term growth spurts, but long-term payments companies are forced to compete their profits away.

But it's wrong.

That’s not the only dimension companies compete on.

🧠🧠🧠

The new battleground is performance

Payments are easy; but the edge cases are hard. Companies that solve the most edge cases increase conversion at checkout, which increases revenue for their clients.

What drives value depends on which of the 5 types of customer is buying.

👉 The price-sensitive juggernaut (e.g., Walmart). Wants the lowest possible price and will take on work and complexity to achieve it.

👉 The global tech enterprise (e.g. Airbnb). Values price, stability, and global reach.

👉 The mid-market retail, e-com brand. (e.g. Asos). Values market reach and conversion.

👉 Small and medium businesses. (e.g. boutique coffee shops). Values ease of use and breadth of offering like payroll or inventory.

👉 Legacy merchants coming to e-commerce late with “omnichannel.” (e.g. department stores). Needs to simplify their operations and reduce multiple platforms to a single platform.

🧠🧠🧠

Different providers compete more on price or more on R&D and performance depending on a number of factors.

👉 Incumbents like Chase Paymentech offer strong unit economics by packaging the whole offering as a bank (Chase) that can cross-sell much more.

👉 Scale digital companies like Adyen offer a single global platform, but compete on unit economics.

👉 Scale players like Stripe are the default choice for small companies and platforms.

👉 New entrants like Nuevi, Checkout and Moov are pushing the R&D and performance barrier to win younger companies.

🧠🧠🧠

Payment’s isn’t a race to the bottom it’s a two dimensional axis. Price vs performance.

What drives performance depends on what your goals are as a business.

Find more on the blog (you know where to get it)

1

3

30

5,527

24 Nov 2023

1) I agree and I think most PFMs struggle:

👉To offer features that maintain daily user retention

👉To monetize services aimed at "expense management" and "saving"

👉To stand out when PFM is already available on most bank's platforms

8 Nov 2023

Heard of a few people building a new version of @mint now that Intuit shut it down. I wouldn't recommend it if you want to build a venture-scale business.

There aren't that many people who want to actively manage their finances; startup graveyard is littered with PFM's.

1

2

3

572

24 Nov 2023

2) 👉To accurately categorize expenses without unified transaction data (maybe OpenAI will help!)

Another good and slightly different perspective on the topic by @AlexH_Johnson

workweek.com/2023/11/10/pfm-…

2

46