Auto components maker Chamundi Die Cast seeks up to ₹1,500 crore as PE interest returns to manufacturing

#Livemint #ChamundiDieCast #AutoComponents #PrivateEquity #IndianManufacturing #MintPremium

9

19h

🔥 NRB Bearings Clears Major Resistance – Watching for Retest 👀📈 🔥

Strong weekly breakout above a multi-month resistance zone with momentum expanding. ⚡

✅ Weekly breakout confirmed

✅ Resistance zone cleared

✅ RSI showing strength

✅ Strong price expansion

✅ Watching for a healthy retest of the breakout area

No buying or selling recommendation — simply a chart worth keeping on the radar for price action around the breakout zone. 👀

📚 For Study & Educational Purposes Only

🚫 Not SEBI Registered

🚫 Not Financial Advice

🚫 Not a Buy/Sell Recommendation

#NRBBearings #NRB #BearingsSector #AutoAncillary #AutoComponents #Manufacturing #IndustrialStocks #BreakoutStocks #StocksToWatch #Watchlist #TechnicalAnalysis #PriceAction #VolumeAnalysis #MomentumTrading #MomentumInvesting #RSI #RelativeStrength #TrendFollowing #ChartAnalysis #SwingTrading #PositionTrading #MarketStructure #IndianStocks #StockMarketIndia #NSE #InvestingIndia #TradingView #WealthCreation #MultibaggerWatch #BullishCharts 👀📈🔥⚡🚀

18

Jun 13

Hi Friends

Banco Products is setting up for its next leg upward. If the price sustains this breakout, it can easily attain its All-Time High (ATH). Watching closely for sustained momentum above the breakout level.

Disclaimer: I am not SEBI registered. The content shared here is purely for educational and informational purposes. These are my personal views and should not be construed as a buy, sell, or investment recommendation. Please do your own research before making any investment decisions.

#banco #autocomponents #automobile #nifty

65

Jun 13

Talbros Auto: Is growth making a comeback?

One interesting point from the latest management commentary is the guidance for at least 18% consolidated revenue growth in the coming year.

What's notable is the pace of change.

After relatively soft growth in FY25 and FY26 (around 5%), management is now talking about a sharp acceleration to 18%, driven by delayed order execution, export opportunities, EV programs, and capacity expansion.

The last time Talbros delivered ~20% growth in FY24, the stock moved from around ₹97 to ₹370. That rally wasn't driven by just earnings growth—it was a combination of earnings expansion and valuation re-rating.

Now, with:

1. 18% growth guidance

2. Strong export tailwinds

3. Increasing EV content per vehicle

4. Capacity expansion in forging and gaskets

5. And a technically strong price breakout

...the setup is becoming increasingly interesting.

Of course, management guidance needs to translate into actual execution, but if growth accelerates as indicated, Talbros could be a stock worth watching closely over the next 12 months.

#Talbros #TalbrosAuto #AutoAncillary #AutoComponents #StockMarket #Investing #EV #Manufacturing #IndiaGrowth #LongTermInvesting

@AethosWealth

x.com/AethosWealth/status/20…

Jun 9

Talbros Automotive Components Ltd Q4 Result and Earning's call Analysis

1. Talbros delivered its strongest quarterly performance in Q4 FY26, with consolidated revenue ₹237 crore, EBITDA of ₹45 crore, EBITDA margin of 18.7%, and PAT of about ₹32 crore.

2. FY26 was more moderate than Q4 suggests: consolidated FY26 revenue was about ₹888 crore, up roughly 5% YoY, while EBITDA reached ₹155 crore and PAT crossed ₹104 crore.

3. The biggest positive was business mix and operating leverage, especially in gaskets/heat shields and in both JVs, which posted strong growth and margin progression.

4. Gasket & Heat Shield remains the profit anchor, contributing 52% of revenue and benefiting from OEM demand, premium vehicle exposure, exports, and higher-margin heat shield products.

5. Forging recovered in Q4 after export weakness in Q2/Q3, but margins were softer due to pass-through pricing resets and FX adjustments, so the segment is improving but not yet fully normalized.

6. Marelli Talbros Chassis Systems was the standout growth engine, with FY26 revenue up 21% and EBITDA up 35%, suggesting the JV is scaling faster than the parent standalone business.

7. Management’s central message is that Talbros is shifting from an “order win” phase to an “execution/commercialization” phase, with several delayed programs now expected to begin in FY27.

8. FY27 guidance is clear: revenue growth of 15–20% and EBITDA margin of 17–18%, supported by ₹150–160 crore of new business commercialization plus underlying industry growth.

#Talbros #Q4Results #EarningsCall #AutoComponents #IndianStocks #FundamentalAnalysis #LongTermInvesting #StockMarketIndia

@AethosWealth

1

109

Jun 13

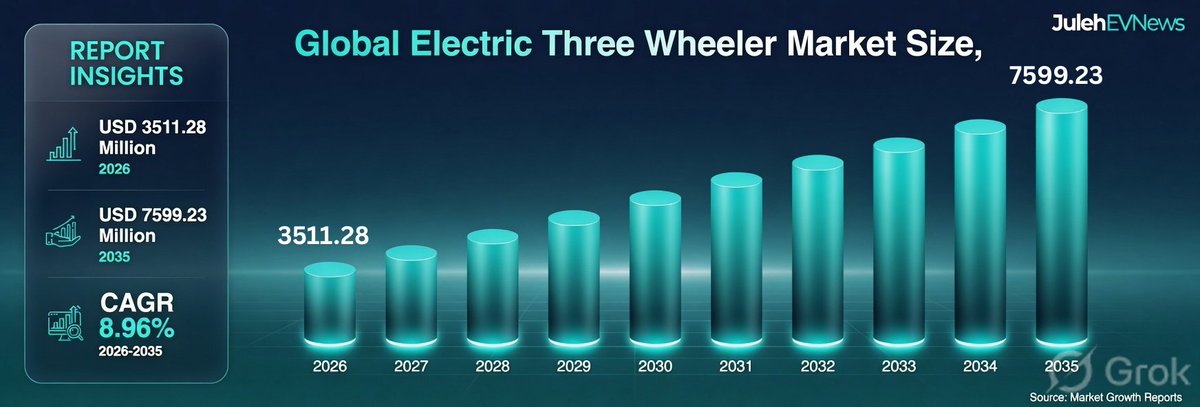

The Electric Three-Wheeler segment is driving change in vehicle systems. While >92% of ICE vehicles still rely on mechanical oil pumps, 68% of hybrids use electric coolant pumps for better efficiency.

Source @MarketGrowthReports

In 2025, over 81 million passenger vehicles used at least 4 pumps each. Electric water pumps cut parasitic losses by 4.8%, and advanced fuel pumps boosted atomization by 18%!

#EVIndia #ElectricThreeWheelers #AutoComponents #JulehEVNews

1

2

19

Commerce and Industry Minister Piyush Goyal has expressed confidence that India’s auto component exports will reach $100 billion by 2030, praising the sector’s Make in India success and growing global footprint. He said the industry will play a key role in achieving the Viksit Bharat 2047 vision.

#PiyushGoyal #AutoComponents #MakeInIndia #Exports #Manufacturing #AutomobileIndustry #ViksitBharat #IndianEconomy #ACMA #IndiaNews

19

Samvardhana Motherson (NSE: MOTHERSON) deepens renewable energy push with first Uttar Pradesh solar project business-news-today.com/samv… #MOTHERSON #SamvardhanaMotherson #CaptiveSolar #RenewableEnergy #AutoComponents #NSE #BSE #UttarPradesh #ibvogt #IndianStocks

413

Jun 12

Every advancement in mobility begins with the technologies like precision components and engineered systems to electronics, materials and manufacturing solutions, which depends on businesses that help vehicles perform better, safer and smarter.

At CII WR 4th Edition NexGen Mobility Show 2026, OEMs, suppliers, component manufacturers, technology providers and industry decision-makers come together to discover new solutions and build the partnerships shaping the future of mobility.

If your technology powers mobility innovation, this is where your business needs to be seen.

🔗 Register to Exhibit:

forms.mycii.in/form/e293b0a5…

🌐 Website:- ciinexgenmobility.com/

📅 Nov 19–21, 2026

📍 Auto Cluster Exhibition Centre, Chinchwad, Pune

For enquiries:

ashwani.singh@cii.in | 91 99934 46238

vaibhav.baraskar@cii.in | 91 84509 48169

#CIINexGenMobility2026 #NGM2026 #AutoComponents #AutomotiveTechnology #OEM #MobilityIndustry #AutomotiveManufacturing #EVIndia #IndiaManufacturing

1

24

Jun 12

#BrokerageCallOfTheDay

@UBS Initiates Buy On #MotilalOswal

* Transition to an AUM-led platform supports non-linear earnings growth

@HSBC Upgrades #HonasaConsumer To Hold

* Sees revenue CAGR of 18% and EBITDA CAGR of 28% over FY26-31

@Jefferies Positive On #AutoSector & #AutoComponents

* Portfolio expansion tailwinds support growth outlook

@sudarshankr #CNBCTV18Market

2

1

1

1,118

Jun 10

Behind every vehicle is a network of manufacturers, suppliers and innovators working together to turn engineering into mobility.

At CII WR 4th Edition NexGen Mobility Show 2026, component manufacturers, technology providers, OEMs, Tier 1 suppliers and industry decision-makers come together to explore new opportunities, strengthen partnerships and drive the future of mobility.

If your solutions support automotive manufacturing, this is where your next business conversation begins.

🔗 Register to Exhibit: forms.mycii.in/form/e293b0a5…

📅 Nov 19–21, 2026

📍 Auto Cluster Exhibition Centre, Chinchwad, Pune

For enquiries:

ashwani.singh@cii.in | 91 99934 46238

vaibhav.baraskar@cii.in | 91 84509 48169

#CIINexGenMobility2026 #NGM2026 #AutoComponents #AutomotiveManufacturing #OEM #Tier1Suppliers #AutomotiveTechnology #MobilityIndustry #IndiaManufacturing #EngineeringExcellence

38

Ashish Raj retweeted

Jun 9

✅Important sectors to focus

#pharma

#autocomponents

#specialitychemicals

#wires&cables

Most of the clean movers are coming from these sectors

1

2

447

Jun 9

Talbros Automotive Components Ltd Q4 Result and Earning's call Analysis

1. Talbros delivered its strongest quarterly performance in Q4 FY26, with consolidated revenue ₹237 crore, EBITDA of ₹45 crore, EBITDA margin of 18.7%, and PAT of about ₹32 crore.

2. FY26 was more moderate than Q4 suggests: consolidated FY26 revenue was about ₹888 crore, up roughly 5% YoY, while EBITDA reached ₹155 crore and PAT crossed ₹104 crore.

3. The biggest positive was business mix and operating leverage, especially in gaskets/heat shields and in both JVs, which posted strong growth and margin progression.

4. Gasket & Heat Shield remains the profit anchor, contributing 52% of revenue and benefiting from OEM demand, premium vehicle exposure, exports, and higher-margin heat shield products.

5. Forging recovered in Q4 after export weakness in Q2/Q3, but margins were softer due to pass-through pricing resets and FX adjustments, so the segment is improving but not yet fully normalized.

6. Marelli Talbros Chassis Systems was the standout growth engine, with FY26 revenue up 21% and EBITDA up 35%, suggesting the JV is scaling faster than the parent standalone business.

7. Management’s central message is that Talbros is shifting from an “order win” phase to an “execution/commercialization” phase, with several delayed programs now expected to begin in FY27.

8. FY27 guidance is clear: revenue growth of 15–20% and EBITDA margin of 17–18%, supported by ₹150–160 crore of new business commercialization plus underlying industry growth.

#Talbros #Q4Results #EarningsCall #AutoComponents #IndianStocks #FundamentalAnalysis #LongTermInvesting #StockMarketIndia

@AethosWealth

2

193

UNO MINDA: ₹1,720 Crore Cashflow | Q4 FY26 |

#unominda #q4fy26 #q4fy26results

📺 Full in-depth analysis here- youtube.com/watch?v=Ec7txzAC…

🚀 Ready for a 4W EV shift? 📈

@UnoMinda's Q4 revenue jumps 18% to ₹5,336Cr

✨Net debt/equity drops to 0.30x

✨Massive new ₹600Cr IVI order

✨2 new EV powertrain plants coming

Watch high-kit-value auto ancillaries

Link to the Earnings Document: bseindia.com/xml-data/corpfi…

#autosector #alloywheels #autoindustry #automobile #EV #lighting #switches #carparts #autocomponents #StockMarketIndia #StockMarket #zinvestz #finance #investing

🔔 Follow @zinvestz for more powerful investing stories & deep-dive analyses! 💼📈

(Disclaimer: This post is for informational purposes only. DYOR before investing! 📈)

1

55

Jun 9

Steel Strip Wheels 4% up. Keep an eye. It must sustain above 236 for next big upmove...

I am not SEBI registered. All posts are for educational purposes only and reflect my personal views. Nothing shared here should be considered a buy or sell recommendation. Please do your own research before investing.

#sswl #nifty #niftysmallcap #Autocomponents #consumer

Jun 5

Steel Strip Wheels, good to add for the target of 251 , 280 if it crosses 236 and sustains. Huge volume. SL- 219.

2

91

📊 HAITONG ON MINDA CORP

Haitong initiates coverage on #MindaCorp with an OUTPERFORM rating and a target price of ₹841. The brokerage sees strong growth potential driven by the company’s focus on premiumisation and automotive electrification trends. 🚗⚡📈

Minda Corp’s diversified and sticky OEM relationships provide strong order-book visibility, while new business segments are entering a key revenue ramp-up phase. Haitong believes the company is well-positioned to benefit from rising content per vehicle and increasing adoption of advanced automotive technologies. 🚀🔧

#StockMarket #IndianStockMarket #MindaCorp #Haitong #BrokerageRadar #AutoAncillary #EV #Electrification #AutomobileSector #AutoComponents #Premiumisation #OEM #StockResearch #MarketInsights #NSE #BSE #Investing #SOCTR #MarketUpdate

155

Jun 8

Top 10 Auto Component Manufacturers in India:

1. Samvardhana Motherson

2. Bosch

3. Uno Minda

4. Bharat Forge

5. Endurance Technologies

in.kompass.com/businessplace…

#Kompass #B2BDirectory #Top10 #AutoComponents #AutomotiveComponents #AutoParts #AutomotiveParts #VehicleComponents

85

Jun 7

S.J.S Enterprises is showing good momentum. Try to accumulate if it comes in the range of Rs1890-1910. Fundamentally strong. FIIs and DIIs have increased their stake. #SJS #AUTOCOMPONENTS #CONSUMER

6

264