So some collateralized loans should be taxed but some shouldn’t? Where’s the line? Mortgages? Second mortgages? Helocs? Car loans? CD loans? Life insurance loans? Pawnshop loans?

1

21m

🚀 AI Agents Just Got Their Financial Infrastructure.

Big move from @usddio and @BAI_AGI: USDD payments are now fully integrated across TRON, Ethereum, and BNB Chain, unlocking seamless transactions for autonomous AI agents.

This is bigger than a simple payment integration.

We're entering a world where AI agents can:

🔹 Hold self-custodied funds

🔹 Execute instant on-chain settlements

🔹 Pay other agents autonomously (A2A)

🔹 Access compute, services, and liquidity without human intervention

With USDD providing a decentralized, over-collateralized, and multi-chain stable payment rail, AI can finally participate in the economy as an active actor, not just a tool.

Imagine networks of agents earning, spending, negotiating, and collaborating 24/7 across borders with transparent, programmable value transfer.

That's the promise of the Agentic Economy.

The future of AI isn't just intelligence.

It's economic sovereignty.

Kudos to @usddio and @BAI_AGI for helping build the financial layer that autonomous agents need to thrive.

Are we witnessing the birth of machine-to-machine commerce at scale?

@usddio @justinsuntron

#TRONEcoStar

9

Official Elixir | Support Team ᵃᵈᵐⁱⁿ retweeted

31 Oct 2025

Our top pool on @CurveFinance is frxUSD/deUSD with @elixir.

Elixir powers deUSD, a fully collateralized, yield-bearing synthetic dollar, bringing funds from BlackRock, Hamilton Lane, and others to DeFi.

Get started: curve.finance/dex/ethereum/p…

12

12

73

19,866

I think you are asking a fair question. But if we take a step back to what Finney was describing, I think he was referring to a scalable economic architecture for BTC, not necessarily a scaling solution.

By moving the majority of activity into lighter, secondary “rails” (exactly what the Digital Asset Stack proposes), the base layer isn’t required to subsidize every marginal transaction. Instead, it becomes a high value settlement and finality layer whose security is increasingly backed by the total economic weight it secures and not solely by the volume of on-chain fees in any given block.

Bitcoins security ultimately rests on the hashrate securing it, which over time would have to be sustained by a combination of transaction fees and the growing economic value of what BTC protects.

Layers don’t replace that incentive structure, but they do expand the economic surface area and TAM anchored to BTC. Every additional layer (credit instruments, yield products, structured offerings) creates new reasons for capital to be custodied, collateralized, or settled against Bitcoin. This IMO will support a more robust long term fee market through selective high value on-chain activity.

In reality, the halving schedule was always intended as a transition mechanism; in many ways I think the design anticipated that security would increasingly rely on a mature fee market plus expanding economic importance of the network itself. Building disciplined rails on top grows that importance without altering the rules of Bitcoin or its supply.

I want to be clear that this doesn’t eliminate the challenge you’re pointing to, what I am saying is, instead of asking how we keep subsidizing every transaction on-chain forever, we should ask how we design layers that make Bitcoin worth securing at scale for centuries. This gives us a path where security and market incentives align, non-adversarially.

1

1

30

42m

🚀 A major leap for the AI economy!

USDD is now powering the next generation of autonomous finance through its integration with b.ai — the foundational financial infrastructure for AI agents.

⚡ AI agents can now:

🔹 Hold self-custodied funds

🔹 Execute autonomous on-chain payments

🔹 Settle transactions seamlessly across TRON, Ethereum & BNB Chain

🔹 Transact agent-to-agent (A2A) with speed, transparency, and reliability

This goes far beyond a simple payment integration. It's a critical step toward true economic autonomy, where intelligent agents can think, plan, act, and pay without intermediaries.

With USDD's over-collateralized stability serving as the settlement layer, AI-powered commerce, compute procurement, and open agent ecosystems can operate with trustless, borderless value transfer.

The Agentic Economy is no longer a vision, it's here, and it's running on decentralized money.

Huge shoutout to @BAI_AGI for helping make this future a reality.

🔗 b.ai/

@usddio @justinsuntron

#TRONEcoStar

10/ 🔎 sUSDD Market Goes Live on @pendle_fi

The sUSDD market launched with over $300K in incentives available over a 91-day campaign. Participants can also enjoy a surprise TRX airdrop and a 30% boost in $PENDLE rewards.

x.com/usddio/status/20598024…

6

46m

Liar liar pants on fire.

@brian_armstrong

TL;DR: Backpack’s $SPCX is the real deal — a regulated U.S. broker-dealer issued, 1:1 backed tokenized stock with a clean, practical exit ramp: redeem the token → get actual SpaceX shares → transfer them via ACATS/DTCC to Robinhood, Fidelity, Schwab, or wherever you want. You keep full shareholder rights and portability.

The others (Ondo $SPCXon, xStocks $SPCXx, etc.) are mostly shitty trackers/derivatives in comparison:

• Collateralized for price tracking dividends (via total return mechanics), but no seamless redemption to real shares you can move to your brokerage.

• Redemption (when even available) is limited, often institutional/minimum-heavy, ecosystem-locked, or cash-settled — you’re stuck with on-chain exposure without true ownership portability.

• More synthetic/SPV structures with weaker claims, potential expirations, and no full TradFi bridge.

Backpack stands out as the breakthrough for a fresh NASDAQ listing because it actually delivers the bidirectional ownership you described, not just a DeFi wrapper pretending to be the stock. This makes it far superior for anyone wanting real equity that lives on Solana rails without getting trapped.

59

46m

Liar liar pants on fire.

@brian_armstrong

TL;DR: Backpack’s $SPCX is the real deal — a regulated U.S. broker-dealer issued, 1:1 backed tokenized stock with a clean, practical exit ramp: redeem the token → get actual SpaceX shares → transfer them via ACATS/DTCC to Robinhood, Fidelity, Schwab, or wherever you want. You keep full shareholder rights and portability.

The others (Ondo $SPCXon, xStocks $SPCXx, etc.) are mostly shitty trackers/derivatives in comparison:

• Collateralized for price tracking dividends (via total return mechanics), but no seamless redemption to real shares you can move to your brokerage.

• Redemption (when even available) is limited, often institutional/minimum-heavy, ecosystem-locked, or cash-settled — you’re stuck with on-chain exposure without true ownership portability.

• More synthetic/SPV structures with weaker claims, potential expirations, and no full TradFi bridge.

Backpack stands out as the breakthrough for a fresh NASDAQ listing because it actually delivers the bidirectional ownership you described, not just a DeFi wrapper pretending to be the stock. This makes it far superior for anyone wanting real equity that lives on Solana rails without getting trapped.

45

48m

Darn tootin! Still is first.

Besides, BASE is an L2, centralized garbage. Not even worth putting in the conversation.

TL;DR: Backpack’s $SPCX is the real deal — a regulated U.S. broker-dealer issued, 1:1 backed tokenized stock with a clean, practical exit ramp: redeem the token → get actual SpaceX shares → transfer them via ACATS/DTCC to Robinhood, Fidelity, Schwab, or wherever you want. You keep full shareholder rights and portability.

The others (Ondo $SPCXon, xStocks $SPCXx, etc.) are mostly shitty trackers/derivatives in comparison:

• Collateralized for price tracking dividends (via total return mechanics), but no seamless redemption to real shares you can move to your brokerage.

• Redemption (when even available) is limited, often institutional/minimum-heavy, ecosystem-locked, or cash-settled — you’re stuck with on-chain exposure without true ownership portability.

• More synthetic/SPV structures with weaker claims, potential expirations, and no full TradFi bridge.

Backpack stands out as the breakthrough for a fresh NASDAQ listing because it actually delivers the bidirectional ownership you described, not just a DeFi wrapper pretending to be the stock. This makes it far superior for anyone wanting real equity that lives on Solana rails without getting trapped.

@toly @martypartymusic

54

RWA collateral in DeFi has a huge liquidation problem.

The recent apxUSD stress test just showed it.

Let's explore what happened, how Silo v3 could handle it, and where we go from here ↓

apxUSD is a dividend-backed stablecoin by @apyx_fi, collateralized by STRC (Strategy's preferred stock), paying 11.5% annual dividend.

In early June, STRC quickly went down in price, causing apxUSD to depeg momentarily. The Apyx team pulled their protocol-owned liquidity from DEXs like Curve while U.S. equity markets were closed.

They did that to protect holders, because keeping the pools active over the weekend would have let some participants trade against a price that no longer tracked real collateral value (as U.S. equity markets don't work on the weekend).

They also deployed their own capital to stabilize lending markets, and published a full post-mortem. apxUSD hit $0.9 and recovered, with no bad debt.

Apyx did everything right, but this shows the structural differences between TradFi and onchain assets.

The side effect of removing secondary DEX liquidity, while still using apxUSD as collateral in Morpho, is that some markets can become difficult to liquidate if liquidators have nowhere to unwind collateral.

Standard liquidation works like this: someone pays off the borrower's debt, takes their collateral, and sells it on a DEX to recover the funds.

If you remove the DEX liquidity, this model breaks.

The Apyx team's own balance sheet became the backstop in this situation, and it worked. But it depends on the issuer having capital, acting fast, and having every incentive aligned at exactly the right moment.

Run the same situation with STRC dropping 30% over a weekend instead of 10%. Bad debt no resolution path to liquidate = lenders absorb the loss.

This is a category problem for RWAs. U.S. equities trade Monday to Friday. DeFi trades 24/7. Every RWA that brings TradFi yield onchain has the same structural problem: the underlying asset closes trading, DeFi doesn't.

Which means the DEX-dependent lending might turn off every weekend for RWA collateral.

Silo v3 has two liquidation paths per market, set at deployment:

→ DEX LT: collateral sold into external DEX liquidity for the debt asset

→ CDS LT: Collateral-Debt Swap. Collateral transfers directly to lenders at a discount, plus liquidation fees.

For most collateral, CDS is the fallback for rare stress conditions. For RWA collateral with TradFi trading hours, it's what can make RWA become the main collateral in lending markets.

Risk note: CDS does not guarantee same-asset repayment. Lenders receive collateral tokens at a discount, not the debt asset. Oracle integrity is a required system assumption. Risk is localized, not eliminated.

Not every asset can become RWA collateral, but apxUSD showed what a quality RWA asset looks like: reserve transparency, monthly attestation from a PCAOB-registered firm, onchain proof of reserves, and no bad debt records.

That is the profile of an asset that deserves a lending market, but it also showed the gap between TradFi and DeFi.

Silo's CDS was built to close it: docs.silo.finance/docs/users…

7

2

5

279

USDZ:

Fully collateralized native stablecoin acting as intermediary/rebalancing instrument between pools (e.g., USDT/USDZ, USDC/USDZ).

1

5

Goldfish (GGBR) = Real tokenized gold.Each token = 1/1000th troy ounce of physical gold reserves.

Over-collateralized, 24/7 tradable, on-chain proof, and redeemable.Affordable gold ownership on blockchain. Learn more: goldfishgold.com

#Goldfish #GGBR #TokenizedGold #Gold

7

1h

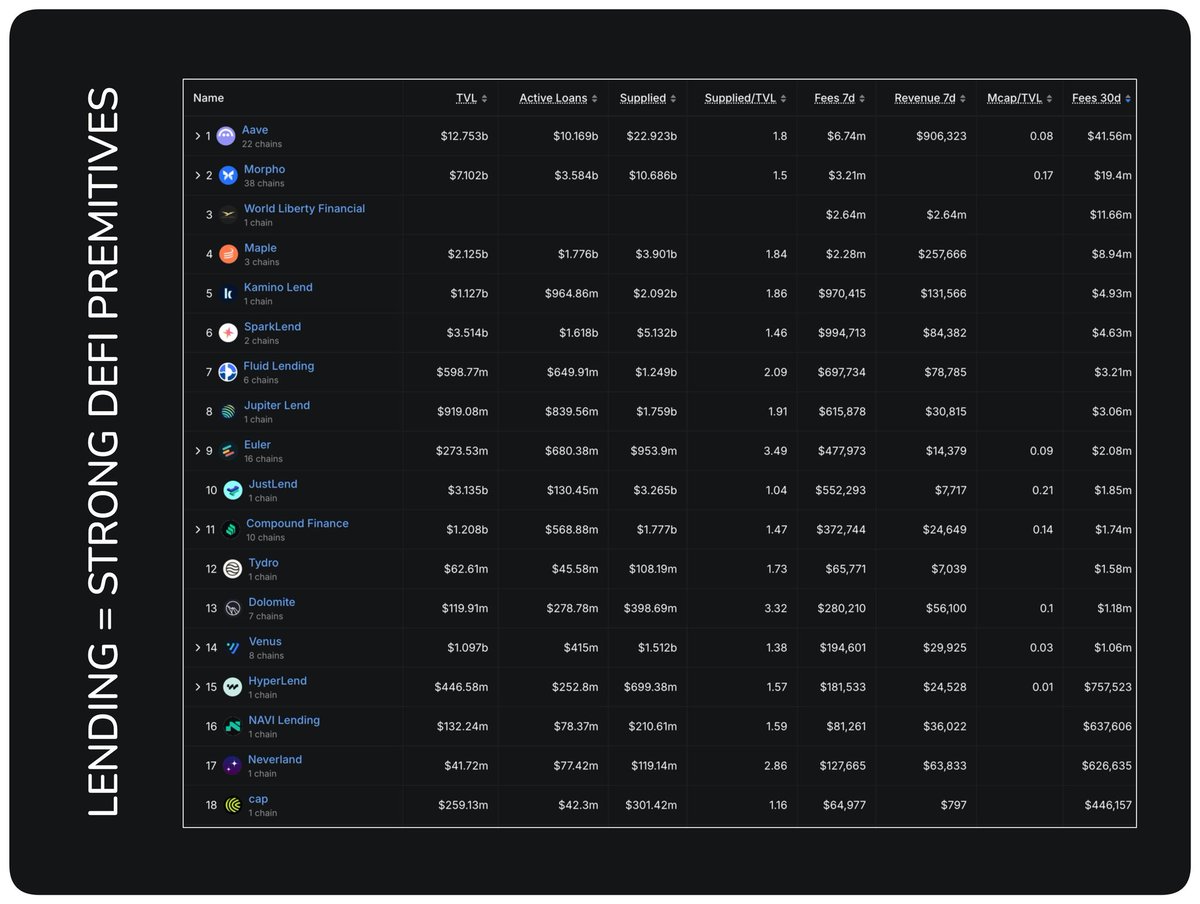

Lending markets are still one of the strongest DeFi primitives because they sit closest to real financial demand.

When I look at DeFi today, TVL can be passive. However I care more about whether capital is being used, borrowed, repriced, and generating fees.

Lending does that better than most sectors.

From the current lending market data:

– @aave still leads with around $12.75B TVL, $10.17B active loans, and $41.56M fees in 30 days

– @Morpho has around $7.1B TVL and $3.58B active loans, showing strong demand for more efficient lending markets

– @maplefinance is smaller by TVL at around $2.13B, but still produced nearly $8.94M in 30d fees

– @kamino, @sparkdotfi, @0xfluid, @JupiterExchange Lend, and @eulerfinance all show that lending demand is no longer limited to one chain or one model

– Several protocols have Supplied/TVL above 1.5x, meaning capital is being actively reused instead of sitting idle

This is why I still consider lending a core DeFi primitive.

In macro and TradFi, credit is the engine of liquidity. When risk appetite returns, users want leverage.

When markets are uncertain, users want collateralized liquidity without selling spot. In both environments, lending protocols stay relevant.

That is the key difference between lending and many seasonal DeFi narratives.

A DEX benefits when trading volume spikes. A perp exchange benefits when volatility rises. A lending market benefits from a wider range of behavior:

– Long-term holders borrow against assets instead of selling.

– Traders use collateral to access leverage.

– Stablecoin demand increases when users rotate into yield or margin.

– Institutions and whales need on-chain credit rails.

– New ecosystems use lending markets as base liquidity infra.

This gives lending protocols better durability across market cycles.

The strongest signal for me is the combination of TVL, active loans, and fees.

A protocol with high TVL but weak borrowing demand may look big but not productive.

A protocol with active loans and consistent fees shows real financial usage.

Aave remains the benchmark because it has scale, multi-chain reach, and strong fee production.

Morpho is notable because it pushes lending toward more efficient, modular markets.

Maple shows that credit demand can move beyond pure retail DeFi.

Kamino and Jupiter Lend show how Solana lending is becoming more serious as liquidity deepens.

I also think lending markets are becoming more important as DeFi matures.

Early DeFi was mainly about incentives. Mature DeFi needs credit markets, risk pricing, collateral management, and yield curves.

→ Lending protocols provide the foundation for that.

As more assets move onchain, users will need ways to borrow, lend, hedge, and manage liquidity without leaving crypto rails.

Lending markets are one of the few DeFi categories that directly map to real financial behavior.

May 29

Even after Stream, Resolv, Kelp DAO nuked confidence and erased billions, capital didn’t leave vaults. It just rotated toward safer and better collateral design.

I don’t really hear anyone saying crypto-native yield will replace TradFi yield anymore.

Instead the market slowly realized the most durable yield in crypto right now is literally tokenized treasuries, institutional credit, and stablecoin carry.

I split vaults into 8 major tracks and each one kinda became its own little economy.

1/ Lending vaults: the biggest and most important track because everything else eventually routes through them somehow.

@aave - $AAVE: the giant with ~$14.5B TVL. V4 hub-and-spoke architecture is basically Aave trying to modularize risk without losing institutional trust.

@Morpho - $MORPHO: curator economy completely changed lending dynamics. Curators became the new fund managers while Morpho itself became infra.

2/ Liquid staking vaults

@LidoFinance - $LDO: dominant with ~8.7M ETH staked and ~24% ETH staking share. stETH integrated literally everywhere, so its moat is composability now.

@jito_sol - $JTO: JitoSOL became default collateral across the Kamino/JLP ecosystem because MEV capture actually adds meaningful yield.

3/ Restaking vaults: depends more on future promise than present cashflow.

@eigencloud - $EIGEN: dominates with ~$7.8B, but actual AVS revenue is still tiny relative to the security pool. EigenDA processed massive data usage while cumulative fees stayed hilariously low.

@ether_fi $ETHFI: strongest distribution among LRTs because they pushed beyond staking into cards, payments, and consumer finance.

4/ Risk curated vaults: the new asset management layer.

@SteakhouseFi: the institutional-grade conservative allocator. Coinbase integration gave them insane credibility.

@gauntlet_xyz: evolved from risk consultant into an actual allocator empire. Big winner from the post-Kelp flight-to-safety.

5/ yield optimizers: the boring backend is where a lot of value hides.

@Veda_labs: powers billions across EtherFi Liquid, Lombard, Mantle cmETH, Kraken DeFi Earn, Lido Earn and other branded products.

@upshift_fi: more like an onchain hedge fund allocator now than a classic optimizer. Multi-strategy exposure across basis trades, RWAs, lending, and arbitrage.

6/ RWA credit vaults: where institutional money actually wants exposure.

@maplefinance - $SYRUP: syrupUSDC and syrupUSDT became composable yield assets, then Pendle, Aave, Kamino and other loops turned them into DeFi lego.

@centrifuge - $CFG: JAAA and JTRSY make it one of the more serious bridges between TradFi settlement and DeFi composability.

7/ Perp LP / basis vaults: giant category because crypto basically turned into one giant leveraged price discovery machine.

@HyperliquidX HLP - $HYPE: community-owned market-making engine directly monetizing trading activity itself.

@JupiterExchange JLP - $JUP: Solana version, but structurally more conservative with majors-only exposure and cleaner oracle design.

8/ Options vaults: the fallen track, maybe slowly becoming useful again.

@DeriveXYZ - $DRV: the survivor that actually evolved, with V2 bringing CLOB matching, institutional features, and multi-collateral support.

@ryskfinance: Hyperliquid-native options vault with nearly $1B notional processed at one point.

The bigger pattern across all 8 vault tracks is that DeFi stopped rewarding raw emissions and started rewarding actual capital efficiency.

I only picked 2 leaders from each track btw, the full map below 👇

15

4

69

3,529

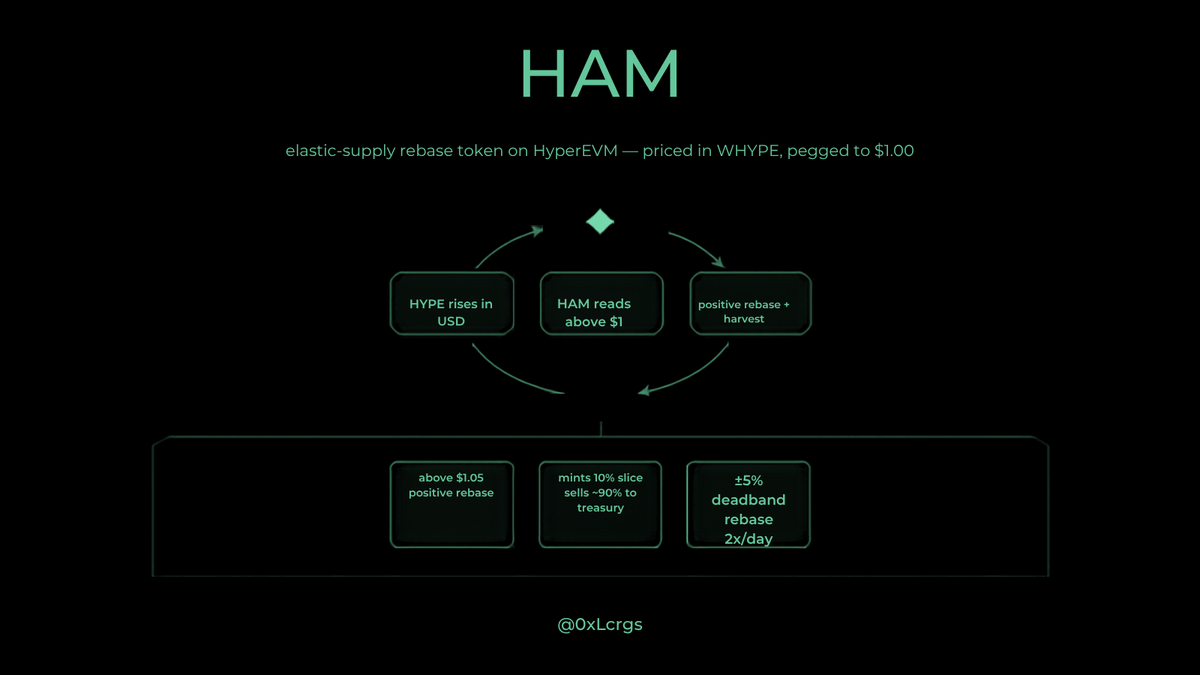

$HAM holds $1 while the protocol quietly farms HYPE's upside for itself.

probably @AgentChud is going to like this, it's not a collateralized stablecoin, an @AmpleforthOrg-style rebase token on HyperEVM that skims $HYPE appreciation into a treasury.

read the contract. the mechanic:

1

2

7

299

𝐔𝐒𝐃𝐃: 𝐀 𝐂𝐨𝐦𝐩𝐫𝐞𝐡𝐞𝐧𝐬𝐢𝐯𝐞 𝐎𝐯𝐞𝐫𝐯𝐢𝐞𝐰 𝐨𝐟 𝐭𝐡𝐞 𝐃𝐞𝐜𝐞𝐧𝐭𝐫𝐚𝐥𝐢𝐳𝐞𝐝 𝐒𝐭𝐚𝐛𝐥𝐞𝐜𝐨𝐢𝐧

USDD (Decentralized USD) is a decentralized, over-collateralized stablecoin designed to maintain a 1:1 peg with the US dollar. Originally launched on the TRON blockchain and managed by the @trondao Reserve, USDD has evolved from an algorithmic model into a more robust multi-chain stablecoin solution. As of June 2026, USDD's circulating supply stands at approximately 2 billion and a healthy collateralization ratio of 154.65% .

𝐓𝐡𝐞 𝐔𝐒𝐃𝐃 𝟐.𝟎 𝐔𝐩𝐠𝐫𝐚𝐝𝐞: 𝐀 𝐒𝐭𝐫𝐚𝐭𝐞𝐠𝐢𝐜 𝐄𝐯𝐨𝐥𝐮𝐭𝐢𝐨𝐧

The transition from USDD 1.0 to USDD 2.0 marked a fundamental redesign of the protocol's stability mechanisms. While USDD 1.0 relied primarily on algorithmic adjustments and market arbitrage to maintain its peg a model susceptible to confidence-driven volatility USDD 2.0 introduced over-collateralization as its core stability framework . Under this model, all issued USDD tokens are backed by assets exceeding 100% of the circulating supply, providing a substantial safety buffer against market fluctuations .

This architectural shift reflects a broader industry trend toward security-first stablecoin designs. Unlike purely algorithmic models, USDD 2.0's multi-asset reserve structure comprising TRX, sTRX, USDT, and other crypto assets enables protocol-level intervention during market stress periods .

𝐂𝐨𝐫𝐞 𝐒𝐭𝐚𝐛𝐢𝐥𝐢𝐭𝐲 𝐌𝐞𝐜𝐡𝐚𝐧𝐢𝐬𝐦𝐬

𝐎𝐯𝐞𝐫-𝐂𝐨𝐥𝐥𝐚𝐭𝐞𝐫𝐚𝐥𝐢𝐳𝐚𝐭𝐢𝐨𝐧 𝐅𝐫𝐚𝐦𝐞𝐰𝐨𝐫𝐤

USDD 2.0 employs a dual-layer protection system combining over-collateralization with multi-asset reserves. Users can mint USDD by depositing collateral into publicly verifiable vaults, with minimum collateralization ratios varying by asset type . As of January 2026, TRX vaults maintained collateralization between 238.45% and 293.43%, while USDT-A operated at a 120.34% ratio . When vaults fall below required thresholds, permissionless liquidations through open auctions restore system solvency without discretionary intervention .

𝐏𝐞𝐠 𝐒𝐭𝐚𝐛𝐢𝐥𝐢𝐭𝐲 𝐌𝐨𝐝𝐮𝐥𝐞 (𝐏𝐒𝐌)

The Peg Stability Module is a cornerstone of USDD's stability architecture, enabling instant, 1:1 zero-slippage swaps between USDD and supported stablecoins (USDT and USDC) . The PSM mechanism works through arbitrage: when USDD trades below $1, arbitrageurs can buy discounted USDD and redeem it at par through the PSM, pushing the price back toward the peg . This eliminates the slippage and friction traditionally associated with large stablecoin conversions, providing certainty for institutional traders and high-volume transactions .

𝐌𝐮𝐥𝐭𝐢-𝐂𝐡𝐚𝐢𝐧 𝐄𝐱𝐩𝐚𝐧𝐬𝐢𝐨𝐧

USDD has successfully expanded beyond its TRON origins into a multi-chain ecosystem:

➞ TRON: The primary issuance chain, with approximately $1.08 billion in supply, primarily driven by vault-based borrowing against volatile collateral .

➞ Ethereum: Native ERC-20 issuance launched in September 2025, with roughly $262 million in supply supported by PSM-based stablecoin swaps and protocol-managed reserves .

➞ BNB Chain: Deployed in October 2025 with approximately $15.6 million in supply, following the same PSM-backed issuance model .

This multi-chain strategy disperses systemic risk while expanding USDD's accessibility across the DeFi ecosystem .

𝐘𝐢𝐞𝐥𝐝 𝐆𝐞𝐧𝐞𝐫𝐚𝐭𝐢𝐨𝐧: 𝐬𝐔𝐒𝐃𝐃 𝐚𝐧𝐝 𝐒𝐦𝐚𝐫𝐭 𝐀𝐥𝐥𝐨𝐜𝐚𝐭𝐨𝐫

USDD distinguishes itself through its focus on yield as a core product strategy. The protocol introduced sUSDD, an interest-bearing representation of USDD that accrues yield through an increasing redemption rate rather than explicit reward distributions . As of January 2026, sUSDD offered 8% APY on Ethereum and 6% on BNB Chain, with staking TVL of $314.5 million on Ethereum .

The Smart Allocator mechanism deploys a portion of protocol reserves into vetted DeFi protocols (Aave, JustLend) to generate sustainable, recurring protocol revenue that supports incentives and savings products . This approach transforms USDD from a passive stable-value tool into an actively yield-generating asset.

𝐓𝐫𝐚𝐧𝐬𝐩𝐚𝐫𝐞𝐧𝐜𝐲 𝐚𝐧𝐝 𝐒𝐞𝐜𝐮𝐫𝐢𝐭𝐲

USDD emphasizes transparency through publicly verifiable smart contracts and on-chain reserve visibility . The protocol has undergone multiple external audits: ChainSecurity audited USDD v2 and the PSM on TRON, while CertiK audited the Ethereum deployment . A public treasury dashboard, updated quarterly, disclosed $3.8 million in revenue, $631,000 in expenditure, and $3.2 million in profit for Q4 2025 .

𝐌𝐚𝐫𝐤𝐞𝐭 𝐏𝐨𝐬𝐢𝐭𝐢𝐨𝐧𝐢𝐧𝐠 𝐚𝐧𝐝 𝐑𝐢𝐬𝐤𝐬

USDD competes in a stablecoin market exceeding $315 billion in total value . Its strengths lie in its over-collateralization model, zero-slippage PSM mechanism, and sustainable yield generation. However, challenges remain, including governance concerns such as the removal of 12,000 BTC from collateral without a DAO vote and risks tied to collateral asset volatility . Compared to DAI, USDD maintains a higher collateralization ratio, offering stronger backing, though it relies more heavily on TRON-native assets .

𝐂𝐨𝐧𝐜𝐥𝐮𝐬𝐢𝐨𝐧

USDD represents a deliberate tradeoff: pursuing above-market savings yields to drive adoption while using explicit collateral buffers, rate controls, and transparency to manage associated risks . Its evolution from algorithmic stablecoin to over-collateralized, multi-chain yield-bearing asset demonstrates the protocol's commitment to stability and innovation in the decentralized finance ecosystem. For institutions, traders, and long-term holders, USDD offers an efficient, transparent, and robust capital management solution in the evolving stablecoin landscape .

Explore: usdd.io

@justinsuntron @usddio #TRONEcoStar

27

Credit vs. Equity: which scale faster on chain?

- Private credit: higher yield demand, over-collateralized lending, institutional proven

OR

- Tokenized equities: public stock tokens growing fast, composability unlocking adoption

Watch the debate and pick your side youtu.be/jVGvc_lW3so

🎙️ @MunamWasi @syrupsid @johnjdagostino @iandebode Todd Stevens @nathanpaitchel

@inkonchain @maplefinance @CoinbaseInsto @OndoFinance @Figure @OpenEden_X

1

23