Yesterday, I attended the dedication of the new Training and Joint Special Operations Prop with the El Paso Fire Department and Marathon Petroleum. Thank you for the invitation and your continued commitment to public safety. 🚒🇺🇸

#ElPaso #EPFD #District3

1

24

Comme chaque année, je participe aux EPFD !

Et si vous aussi, vous voulez y aller pour vivre une journée pleine d'émotions et de surprises, n'hésitez pas, il reste de la place !

Jun 13

Rejoignez dès maintenant notre serveur Discord !

➡️discord.gg/P8BFrfkMKA

C'est sur celui-ci que vous trouverez le lien pour les inscriptions à l'#EPFansDays 2026 qui démarrent aujourd'hui à 18h !

25

Jun 13

تريد التخفيض!

⎐كُـود⎐كـوبِون⎐خـِصم⎐

Special

⎐ايهرب⎐ايهيرب⎐اهرب⎐

⊵Ctz7563⊴

⎐وفرها⎐

⊵EX13⊴

⎐باث▬اند▬بودي⎐بدى⎐

⊵AQ5D⊴

⎐مفارش⎐الحبيب⎐

◗MH5◖

Star Lavender

___

ePfD

Jun 12

You are ignoring the FCC changes so the car analogy actually works against your point. The FCC didn't give Starlink a bigger gas tank — they changed the rule that said only one car could drive the road at a time. Under the old EPFD regulations from the 1990s, only one satellite could effectively serve a geographic area and frequency band simultaneously. The new rules allow up to eight. Same phased array hardware, same per-satellite limits — just eight times the satellites working the same patch of ground.

On the "no indication Starlink lacks capacity" — Starlink has been charging one-time demand surcharges in oversubscribed markets just to access residential plans. That's not a speculation about capacity constraints, that's SpaceX publicly pricing them.

The phased array bandwidth ceiling is real and you're right that it exists. But the regulatory change doesn't try to push more through a single beam — it stacks more beams on the same area. The bottleneck shifts from "one satellite serving this region" to the aggregate of eight. That's a meaningful difference, especially in dense suburban and urban coverage where the single-satellite rule was the actual binding constraint.

The urban competition argument may still hold long-term — nobody's claiming this makes Starlink a fiber replacement tomorrow. But the capacity problem was both real and regulatory, and the FCC just removed the regulatory half of it.

13

Jun 3

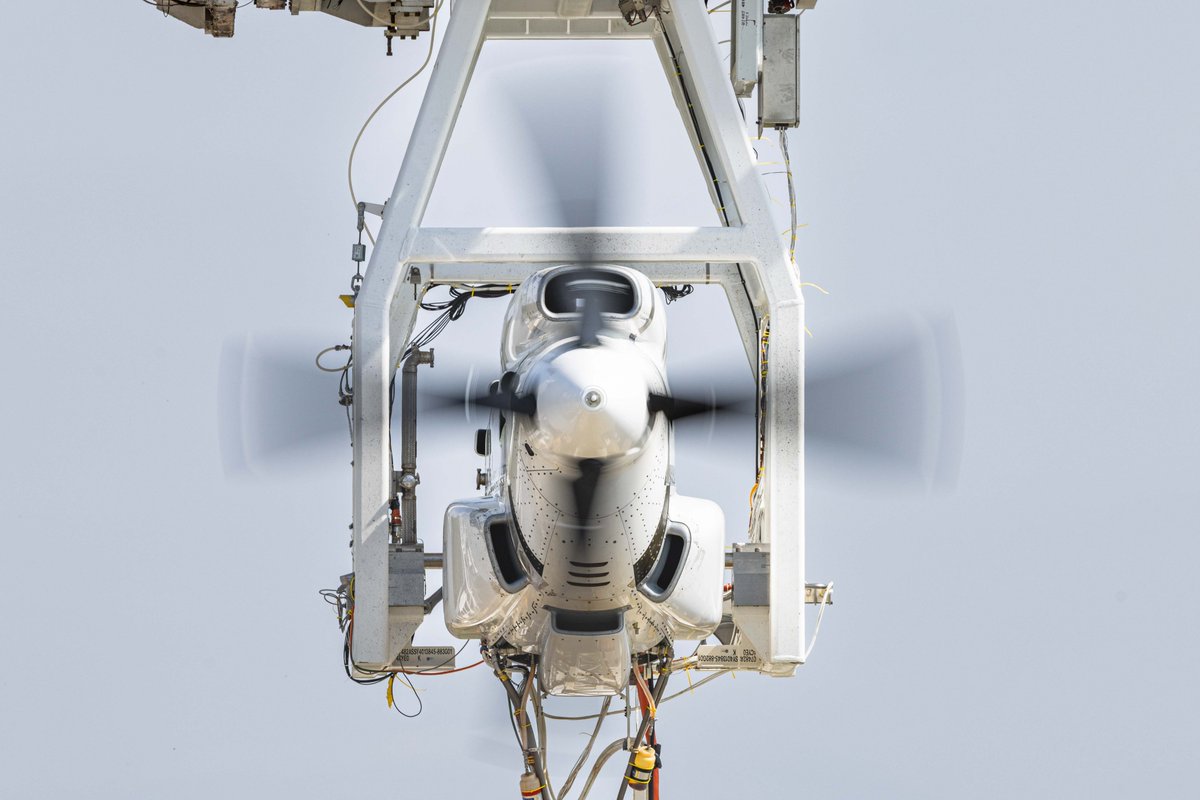

🇺🇸 GE Aerospace completed testing of a megawatt-class hybrid electric engine system developed through NASA’s Electrified Powertrain Flight Demonstration (EPFD) project, paving the way for flight tests. @GE_Aerospace @NASA

Throughout the test campaign at Peebles Test Operation in Ohio, teams simulated various flight phases such as taxi, takeoff, climb and cruise.

The ground test was the company’s first to validate the full integrated system, including GE Aerospace-developed motor/generators, power converters and inverters, controllers, Dowty propellers, Avio Aero gearboxes, and a CT7 engine. BAE Systems provided the batteries used and Boeing subsidiary Aurora Flight Sciences supplied the complete nacelle.

2

63

Jun 2

NEWS: It's electric ⚡

GE Aerospace has completed ground testing of its megawatt-class hybrid electric engine system developed through @NASA's Electrified Powertrain Flight Demonstration (EPFD) project. For the first time, the fully integrated hybrid electric powertrain was tested including the gas turbine and electric machines, power electronics, and energy storage. Throughout the test campaign, teams simulated various flight phases such as taxi, takeoff, climb and cruise.

It's a major milestone for the technology development of hybrid electric powertrains to help meet customer needs.

Learn more about how we’re advancing the #FutureOfFlight: bit.ly/4x5eTET

14

57

377

20,728

Jun 2

what if everyone moves on, living their own lives, while eddie built a new one with the EPFD?

what if they stay apart forever?

1

2

262

May 30

Still does have the capacity, we just need ground Station and an upgrade to the new FCC EPFD Power limits and number of beams per satellite then we good

4

4

24

6,816

May 24

Can easily be fixed by Tech.

Ground Stations , updated EPFD rules , and multiple Starlinks beaming to one location.

All the above only need approval

1

4

383

One overlooked UK-listed company is the critical hardware supplier behind SpaceX’s Starlink gateway network — and almost nobody is talking about it:

$FTC (Filtronic plc) — £857M market cap

It manufactures the E-band GaN Solid State Power Amplifiers that physically enable SpaceX’s Starlink gateway network. Not software. Not services. The actual hardware that closes the link budget between the ground and orbit.

The Physical Problem

LEO satellites orbit at 500–1,200km. Low altitude cuts latency to under 30ms but requires thousands of satellites. The real bottleneck isn’t the satellites — it’s the ground gateways backhauling orbital traffic to terrestrial fiber.

At E-band frequencies (71–86 GHz), free-space path loss scales quadratically. You cannot close a multi-gigabit link budget over hundreds of kilometers of atmosphere without extreme transmit power. Silicon and GaAs physically cannot deliver it. GaN-on-SiC is the only answer — and Filtronic is the sole-source supplier for Starlink’s entire gateway network.

Two Catalysts Just Collided

SpaceX is targeting a $2T public valuation. Brookfield already accumulated a $2B pre-IPO stake. Roadshow starts June 4, 2026. The prospectus revealed Starlink did $11.4B in revenue in 2025 while the legacy launch business — $4.1B revenue — still posts net losses. Starlink IS the $2T valuation. And Starlink’s profitability scales directly with gateway expansion. More subscribers = more gateways = more Filtronic SSPAs.

On April 30, 2026, the FCC voted 3-0 to scrap the 1990s-era EPFD power-limit regime — unlocking up to 7x more capacity for LEO operators. But you cannot realize 7x capacity with a software update. Every Starlink gateway on Earth needs physical hardware upgrades to high-power GaN SSPAs. The FCC ruling triggered a mandatory replacement cycle. Filtronic’s stock jumped double digits in a single session within a week of the vote.

The Moat

Filtronic’s proprietary “Cerus” SSPAs deliver 10–20W saturated output power in E-band with >20% Power Added Efficiency. Flip-chip packaging accurate to ±2µm on ceramic substrates. Competitors using conventional wire bonding exhibit high parasitic inductance at 80 GHz. That gap cannot be closed quickly.

In April 2024, SpaceX signed a 5-year exclusive partnership and was granted warrants for up to 10% of Filtronic’s share capital — vesting in tranches tied directly to purchase order volume up to $19.7M cumulative spend. SpaceX earns equity as it buys more hardware. Competitors are structurally locked out.

Tranches 1 and 2 already fully vested. Tranches 3 and 4 expected Q3/Q4 2026.

The Numbers

Space & Satcom revenue went from £2.1M in FY23 to £28.5M in FY25 to £58.4M projected FY26. Total revenue hits £78.2M projected. Gross margins expanding from 31.9% to 52.9%. Zero long-term debt. £18M projected net cash. Self-funded entirely from organic free cash flow.

The Valuation Gap

$GLW (Corning): 86.8x forward P/E, <5% space exposure, priced off one Nvidia fiber deal.

$MTSI (MACOM): 38.2x forward P/E, <20% LEO exposure.

$POET: unprofitable, retail meme volatility.

$FTC: 16.5x forward P/E, 2.3x P/S, ~75% direct LEO revenue exposure, profitable, debt-free, sole-source SpaceX gateway supplier.

Re-rate to a conservative 6x P/S on £78.2M FY26 revenue → £469M implied market cap → 150% upside before the SpaceX roadshow even opens.

Before a single sovereign contract. Before Tranches 3 and 4 vest. Before US institutional money discovers it post-IPO.

The physical backhaul of the entire space internet runs through one packaging line in Sedgefield, UK. SpaceX has 10% equity tied to keeping it that way.

Not financial advice. DYOR.

3

3

28

4,519

May 22

EPFD responds to condition 2 fire in Central El Paso. No injuries reported.

bit.ly/4dFRQrB

1

1

461

No ,starlink only need to match their offerings to be able to compete

The current starlink constellation is not capable of that ,but they are launching New V3 sats which are 10X more capable the fact that EPFD rules have been relaxed means they can serve 8x per unit area.

1

3

334

May 13

Career Day was a success! Students dressed as their future careers, explored vehicle displays from EPPD, EPFD & SWAT, and got inspired through class presentations & the Career Fair! Students loved interviewing presenters & hands on learning!🌟 #CareerDay @EsHeight @rachblair11

1

4

16

1,768

Chester E. Jordan Student Council and the community proudly helped “Fill the Boot” for the Muscular Dystrophy Association and showed the power of teamwork❤️

Thank you to EPFD and everyone who donated! 🔥

#FillTheBoot #LionCommunity #MDA #EPFD #TeamSISD #HappiestStuCoOnEarth

6

13

397

May 10

SpaceX 在最新一轮 secondary 中摸到的 4000 亿美元估值,已经让它成为全球未上市企业中的异类。如果你仍然用“商业航天”或“火箭公司”的框架来理解这个数字,我认为你会在未来 12 到 24 个月里误判方向。我倾向于把这个估值拆解为三部分:星链(Starlink)的消费级电信现金流、星盾(Starshield)的主权级国防溢价,以及马斯克个人政治头寸的隐含波动率。当前市场过度交易了第三部分,而忽略了第一部分的边际减速和第二部分的合规成本。

先看星链的基本面。公开渠道显示,Starlink 全球订阅用户在 2024 年末突破 450 万,年化营收大致落在 70 亿到 90 亿美元区间。我在约翰内斯堡亲眼见证了这家公司在非洲的渗透:当南非固网运营商还在因为电缆盗窃和 Eskom 供电不稳定而瘫痪时,Starlink 的终端已经在豪登省郊区和西开普的农场里运行。但这里有一个监管细节:南非独立通信管理局(ICASA)至今对 Starlink 的直连业务持保留态度,原因是《电子通信法》下的频谱许可和本地股权要求。这不是孤例。印度、印尼、津巴布韦等市场的准入摩擦,说明 Starlink 的“全球覆盖”在物理层已实现,在法律层远未完成。

用户量增长的故事正在从“爆发期”进入“渗透期”。我判断,2025 年全球订阅数若不能突破 800 万,年化营收增速跌破 40%,那么当前估值中嵌入的消费互联网叙事就会出现裂缝。ARPU 是另一个隐忧。北美市场的 ARPU 大约在 100-120 美元/月,而非洲和拉美市场一旦大规模推广,必然会通过本地化定价和分销商补贴来获客,实际 ARPU 可能腰斩。更关键的是,星链并非不可替代:在美国本土,Verizon 和 T-Mobile 的卫星直连手机服务已经开始蚕食“应急通信”这一高利润场景;在欧洲,OneWeb 与本地运营商的捆绑更具合规优势。所以我对 Starlink 消费者业务的方向性判断是:它是一门好生意,但已经不是两年前那种指数级增长的生意。如果 SpaceX 不能在未来 18 个月内将星链的 EBITDA 利润率稳定推升到 25% 以上,4000 亿估值里的“电信现金流”模块就需要打折。

星盾是估值跃迁的真正引擎,但也是法律风险最密集的板块。Starshield 与 NRO、Space Force 的集成,意味着 SpaceX 从 NASA 的货运承包商升级为美国国家侦察和军事通信的关键节点。我读过 DoD 的预算摘要,Starshield 相关收入可能在 2024 年已经达到 20 亿美元量级,且毛利率远高于消费者业务。但请注意:一旦你的载荷开始承载加密军事情报链,你就彻底落入了 ITAR 和《国家侦察局安全条例》的覆盖范围。

从法律角度,SpaceX 面临的核心矛盾是“商业公司的敏捷性”与“国防承包商的安全合规”之间的冲突。ITAR 要求对 USML 物项的每一个环节进行 citizenship 和访问权限控制;Starshield 的卫星间激光链路和抗干扰波形,几乎必然被归类为 USML Category XV(a) 的防御物项。这意味着任何外国公民——包括马斯克本人的南非/加拿大背景——在特定技术会议中的参与,都可能需要 DDTC 的豁免。此外,当星盾向北约盟国或印太伙伴(如日本、澳大利亚,甚至未来潜在的台湾)提供数据中继时,每一次跨境传输都需要单独的出口许可。我处理的跨境合规案例告诉我:这种许可不是走流程,而是可以被国务院随时暂停的政治工具。

CFIUS 在这里是沉睡的巨兽。虽然 SpaceX 是美国注册公司,但星盾业务涉及的外国政府客户、外国供应链环节,以及马斯克个人与多国的商业往来,足以触发 CFIUS 对“敏感个人数据”和“关键技术”的管辖。特别是在 Starshield 处理盟国军事数据的场景下,如果数据存储或加密密钥管理涉及非美国实体,CFIUS 完全有权强制要求缓解措施,例如设立独立安全董事会(Security Board)或数据本地化。这些措施不会终结合同,但会压缩利润率,并降低 SpaceX 作为“灵活承包商”相对于 Lockheed Martin 或 Boeing 的比较优势。

卫星发射节奏是护城河,也是紧箍咒。Falcon 9 在 2024 年完成了超过 100 次发射,回收复用已经工业化了。但轨道不是无限长的停车场。SpaceX 目前在轨卫星接近 6000 颗,占全球活跃航天器的半数以上。FCC 对 Part 25 许可的频谱分配和 debris mitigation 要求,正在成为实质瓶颈。2024 年 FCC 对 Gen2 星座的修改许可中,已经将部分频段的共享义务和离轨时限收紧。随着 Amazon Kuiper、中国 GW 星座以及欧洲 IRIS² 的加速部署,同频干扰和碰撞规避的行政成本会指数级上升。我预计 FCC 在 2025 年会对 V 波段和 E 波段的申请施加更严格的 Equivalent Power Flux-Density(EPFD)限制,这将直接降低星链单星的吞吐量,或迫使 SpaceX 发射更多卫星来维持承诺带宽。

星舰(Starship)是更大的变量。没有星舰,星链 V2 卫星的完整部署和未来的火星载荷都无法实现。但目前 FAA 对 Boca Chica 发射场的监管仍是逐案审批,且受 NEPA 诉讼困扰。

1

1

382

May 8

We’re gonna post our analysis on the EPFD vote tomorrow! It raises the roof for what V3 will be able to deliver per cell! All of a sudden satellite broadband isn’t so niche…

2

137

May 8

Yes 700 Tbps for current Starlink but doubling by end of year is possible.

Just 10 launches in 2026 after flight 12,with engine relight means SpaceX can go to orbit from flight 13 onwards and start deploying live V3 satellites even without rocket reuse. Can almost double the Tbps with 60 tbps per launch and another 80-90 F9 for another 15-20% from current levels.

FCC EPFD/flux density update. Starlink can run up to 8 satellites serving the same area/frequency band simultaneously. Decrease the size of the receiving dish for lower cost and increased volumes. @aaronburnett @elonmusk @spacex @starlink Faster increase in dish production can be done, more aggressive pricing and more aggressive bandwidth plans. And 6X increase in capacity in 2027 with 100 Starship Starlink launches. FAA already permitting 145 launches at three launch sites. Funding this year to enable more sites and launch towers to be built. 6 month to build a Mechazilla tower and need to speed up Deluge and launch facility construction.

1

1

11

699