Jun 13

Labasics 2# Tapered Rubber Stoppers, 10 pcs Black Solid Plugs, Size: 0.59″ Bottle, 0.83″ Top, 1.02″ Length, for Airtight Sealing of Labware

verifiedpricedrops.com/labas…

7

Jun 12

It's so insane at things like this. From reverse engineering labware to setting up cameras to fixing my router.

1

3

613

Precision that powers industries. ⚙️

From spinnerets to platinum labware, Hindustan Platinum delivers engineered solutions trusted across pharma, glass, cement, R&D, and jewelry sectors.

🔗 𝐋𝐞𝐚𝐫𝐧 𝐦𝐨𝐫𝐞: hindustanplatinum.com/servic…

#EngineeredProducts #PrecisionEngineering

11

Jun 11

Hello Brazil!🇧🇷

We’re happy to #welcome Veritas Biotecnologia as our new authorized ibidi #distributor in Brazil.

👩🔬Researchers in #Brazil now have easier local #access to ibidi labware, instruments, and solutions for cell culture, microscopy, and live cell imaging #workflows

1

27

Jun 11

Euroz Hartleys Research Analyst Oliver Porter recently toured XRF Scientific’s Melbourne platinum manufacturing facility.

The visit provided insight into the production of platinum labware used in sample preparation, as well as platinum components supplied to industries including glass manufacturing, chemicals and crystal growth.

Thanks to the @XRF_Scientific team for hosting.

#EurozHartleys #ASX #Manufacturing #MiningServices

1

272

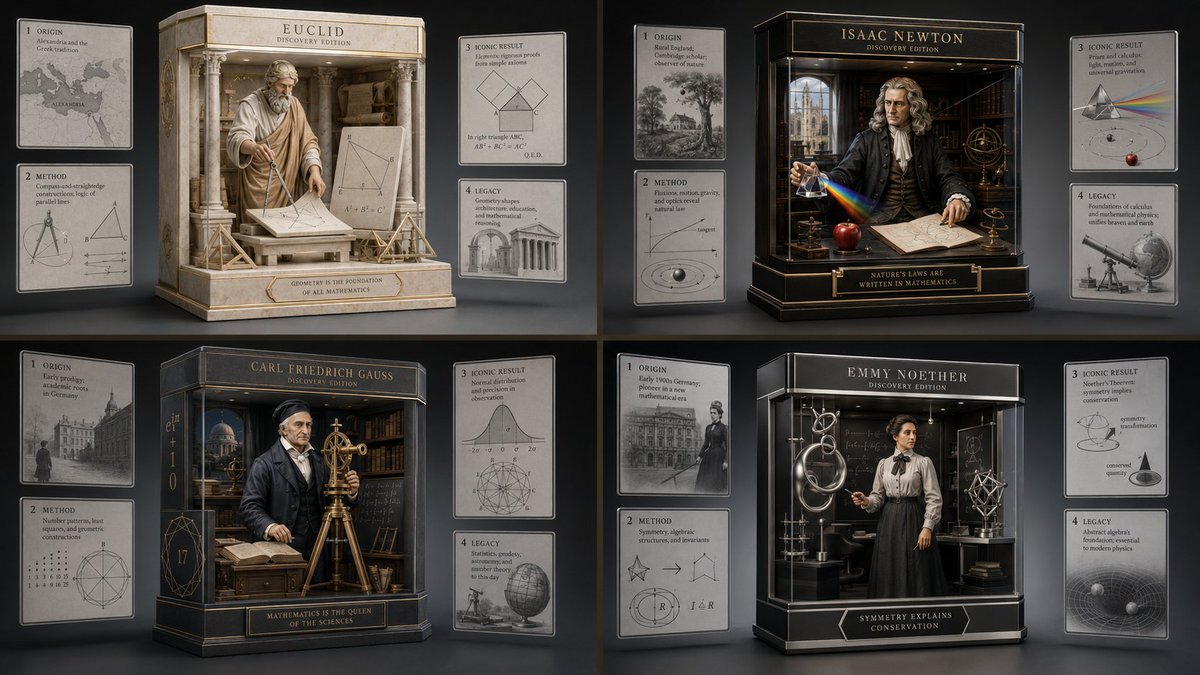

Turning mathematicians into collectibles.

Prompt:

2x2 grid, do this 4 for famous mathetmaticians, 16:9 input: [scientist / invention / discovery / theory / book / poem / art movement / cuisine / classic car / machine] anchor: a premium collectible “discovery edition” diorama box for the input topic. the box contains an ai-inferred central figure, artifact, apparatus, scene, vehicle, manuscript, dish, or machine depending on the subject. it must look like a luxury studio product photograph of a museum-quality collectible. system: infer the central subject’s canonical pose, tool, environment, or symbolic action include four floating grayscale figure panels that explain the topic through clean visual frames panels may become diagrams, maps, recipes, equations, mechanical sections, manuscript fragments, material samples, architectural elevations, or historical moments the display box behind the subject contains miniature native elements and premium packaging details no fake brand logos unless explicitly requested panel logic: panel 1 = origin / source panel 2 = mechanism / method panel 3 = iconic result / artifact panel 4 = legacy / influence weighted prompt: anchor collectible diorama::3.8 semantically accurate central subject::3.5 clean explanatory figure panels::3.3 premium packaging design::3.0 studio product photography::2.6 readable visual hierarchy::2.1 restrained symbolic props::1.8 morphology: stylized but premium figure or artifact geometry, crisp edges, miniature accuracy, clean silhouettes, field-specific diagrams, elegant micro-details material physics: glossy molded figure finish, matte paper panels, spot uv, foil edges, translucent window insert, glass labware or vitrines, machined metal, archival cardboard, lacquered base illumination: soft key light, gentle fill, rim separation, controlled reflections, clean cyclorama background, high-end product ad lighting render stack: collectible figure photography, isometric three-quarter angle, shallow depth of field but readable panels, sharp focus on central gesture or object negative: photoreal skin uncanny valley, messy stains, gibberish equations, fake unreadable labels, warped hands, extra limbs, dull packaging, cheap toy look, watermark, logos, clutter output: a luxury collectible diorama that teaches and mythologizes [input] without becoming childish or gimmicky.

1

4

15

691

Jun 10

Labasics 8# Tapered Rubber Stoppers, 5 pcs Black Solid Plugs, Size: 1.30″ Bottle, 1.61″ Top, 1.22″ Length, for Airtight Sealing of Labware

verifiedpricedrops.com/labas…

11

Jun 10

Fable not as good as gpt5.5 on my own vision benchmark (can it tell what labware is where on a top down image of a robot deck) but weirdly didnt flag anything "biology" related processing images of tubes pipette tips when Ive seen people get nerfed for "what is a mitochondria"

1

3

209

I'd Actually Love it if More Like Labware or Evil Scientist Themed Practical Use Stuff Was Made (Guy Who Considers Buying Beakers For Drinking)

9

This company is insane, they make so much shi. Originally established to manufacture high performance ceramic labware, they evolved into advanced materials, specializing in oxide ceramic components, high-temperature furnaces, and custom made industrial solutions.

Ants Innovation’s Chemical Vapour Deposition System(CVD), used to deposit thin films by chemically reacting vapour-phase precursors on heated substrates. Designed for both cold and hot well. Applications include- dielectric layers for semi-conductors and solar cell manufacturing.

3

38

714

May 26

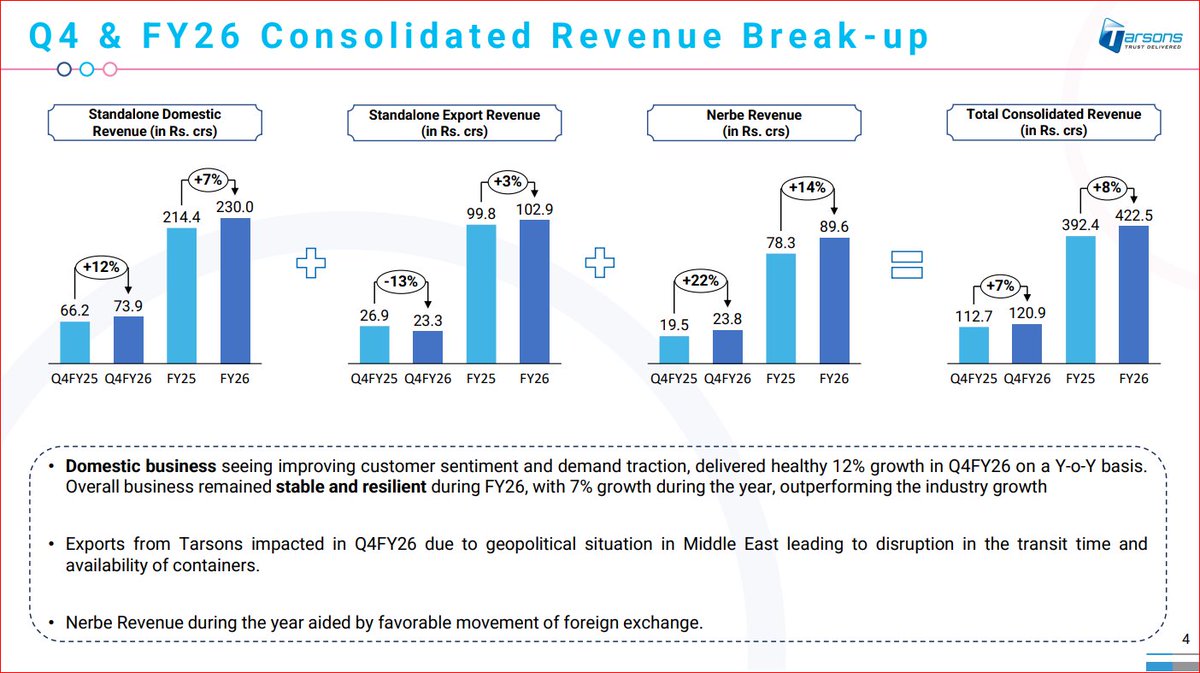

Tarsons Products Ltd Concall Summary for Q4FY26

MANAGEMENT COMMENTARY

• Company achieved highest-ever quarterly revenue in Q4FY26

• Heavy investment phase largely completed by management

• Focus shifting toward utilization and execution phase

• Leadership remains confident on long-term growth visibility

OUTLOOK

• Entire capex program expected fully commissioned in H1FY27

• New facilities expected to support higher revenue growth

• FY27 PAT likely to remain moderate due to high depreciation

• Debt-to-EBITDA targeted below 2x levels

INDUSTRY

• Global supply chain disruptions impacted export operations

• Freight and container costs remained elevated globally

• Raw material prices surged sharply during Q4FY26

• Industry overall witnessed year-on-year demand contraction

COMPETITIVE POSITION

• Tarsons outperformed broader industry growth trends

• Strong domestic brand and distribution remain key advantages

• Make-in-India positioning supports cost competitiveness

• Chinese competition remains intense in export markets

RISKS

• Middle East conflict impacting export demand and logistics

• Sustained raw material inflation may pressure competitiveness

• High depreciation and interest costs impacting profitability

• Export recovery visibility remains uncertain near term

GROWTH DRIVERS

• Panchla and Amta facilities entering ramp-up phase

• Cell culture and bioprocess lines becoming major focus

• Product basket expanding into higher-growth categories

• Global market expansion initiatives underway across regions

PRODUCT MIX

• Domestic business delivered strong double-digit growth

• Export business impacted by geopolitical disruptions

• Cell culture category expected to gain momentum from FY28

• Focus increasing on high-value biopharma labware segments

FINANCIALS

• Q4FY26 consolidated revenue stood at ₹121 crore

• FY26 adjusted cash PAT increased to ₹112 crore

• Gross margins remained healthy near 71-72%

• Operating cash flow improved to ₹118 crore

CONCLUSION

• Tarsons transitioning from capex cycle to growth phase

• Domestic business resilience offset export market weakness

• New product categories expected to drive future scalability

• Management remains optimistic on long-term growth trajectory

#sharemarket #Q4results #TarsonsProduct

1

4

300

#NATA is proud to welcome Gold Sponsor, #LabWare to #AccreditationMatters2026.

LabWare offers a suite of products and services to streamline lab documentation, data integrity, & compliance for various industries.

Register for Accreditation Matters 2026: accreditationmatters.com.au/

2

272

May 20

The Illinois Biological Foundry for Advanced Biomanufacturing (iBioFAB)

iBioFAB is a fully integrated computational & physical infrastructure that supports rapid design, fabrication, validation/quality control, & analysis of genetic constructs & organisms. As the first "living foundry" in the world, the iBioFAB provides a new manufacturing paradigm for chemicals, materials, & biologics. It features a central robotic arm that transfers labware between instruments that perform distinct unit operations such as pipetting, incubation, or thermocycling.

ibiofoundry.illinois.edu/

CRISPR-COPIES

COmputational Pipeline for the Identification of CRISPR/Cas-facilitated intEgration Sites (CRISPR-COPIES) is a user-friendly web application & a command line tool for rapid discovery of neutral integration sites. Designed to work for any organism w/ a genome in NCBI & for any CRISPR system, CRISPR-COPIES can identify neutral sites in a genome-wide manner. The identified sites can be used for characterization of synthetic biology toolkits, rapid strain construction to produce valuable biochemicals, & human gene & cell therapy (editing).

github.com/Zhao-Group/COPIES

This tool leverages ScaNN, a state-of-the-art model on the embedding-based nearest neighbor search for fast & accurate off-target search and can identify genome-wide intergenic sites for most bacterial & fungal genomes within minutes. As a proof of concept, we utilized CRISPR-COPIES to characterize neutral integration sites in 3 diverse species: Saccharomyces cerevisiae, Cupriavidus necator, & a human cell line.

biorxiv.org/content/10.1101/…

PCR Primer Design & Variant Management

Mutagenesis provides streamlined primer design & worklist generation for site-directed mutagenesis workflows. The tool supports automated generation of mutation libraries, offering researchers a reproducible & scalable approach to engineering genetic variants.

github.com/Zhao-Group/Primer…

A generally applicable platform for autonomous enzyme engineering that integrates machine learning (ML) & large language models (LLMs) w/ biofoundry automation to eliminate the need for human intervention, judgement, & domain expertise.

Requiring only an input protein sequence & a quantifiable way to measure fitness, this automated platform can be applied to engineer a wide array of proteins.

nature.com/articles/s41467-0…

CLEAN

clean.platform.ibiofoundry.i…

CLEAN predicts Enzyme Commission (EC) numbers for enzyme sequences. This machine learning algorithm, Contrastive Learning enabled Enzyme ANnotation (CLEAN), was trained on high-quality data from UniProt, taking amino acid sequence as input & outputting a list of EC numbers ranked by the likelihood.

github.com/tttianhao/CLEAN

The contrastive learning framework empowers CLEAN to confidently (i) annotate understudied enzymes, (ii) correct mislabeled enzymes, & (iii) identify promiscuous enzymes w/ two or more EC numbers—functions that we demonstrate by systematic in silico & in vitro experiments.

science.org/doi/10.1126/scie…

Open Enzyme Database

openenzymedb.platform.molecu…

Open Enzyme Database: a community-wide repository for sharing enzyme data

academic.oup.com/nar/article…

The plasmid database (PLSDB)

Plasmids can be explored & filtered using the browsing tables. Nucleotide sequences can be searched in the database by either using Mash mash.readthedocs.io/en/lates… for longer sequences (e.g. contigs or long reads), or by using BLASTn blast.ncbi.nlm.nih.gov/Blast… for shorter sequences, e.g. genes.

ccb-microbe.cs.uni-saarland.…

PlasmidMaker_GuideDNA

Given any number of annotated '.DNA' file as an input, the code generates guides, primers & possible combinations of restriction enzymes for performing & verifying high-fidelity, scarless PfAgo-guided plasmid assembly. A standalone code to verify plasmids using restriction digestion enzymes is also provided.

github.com/Zhao-Group/Plasmi…

PlasmidMaker

A versatile, automated, & high throughput end-to-end platform for plasmid construction

nature.com/articles/s41467-0…

1

8

9

338

May 13

Arms and tracks are great. Some of the devices are terrible (very error prone) and should be rebuilt. Some stuff to do on reagents and labware eventually too.

1

2

382

May 12

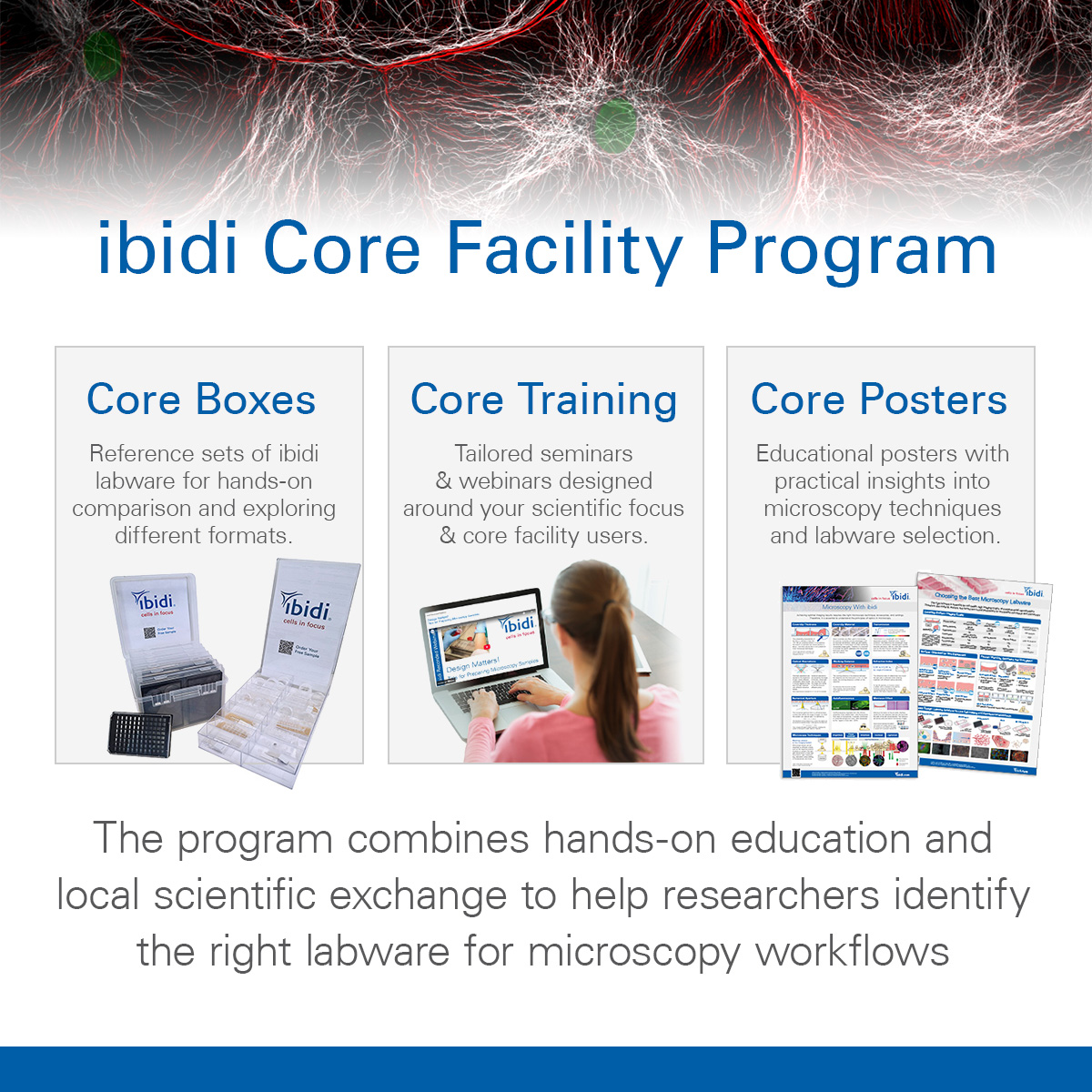

🔬 A microscope alone doesn’t solve imaging challenges. The right labware matters too.

That’s why we created the ibidi Core Facility Program for imaging core facilities.

🥼Work in or with a microscopy #corefacility?

We’d love to connect.

🔗zurl.co/D0lGB

#microscopy

1

2

43

May 11

They also introduce AugSmolVLA for wet-lab robustness.

Training includes online augmentation for:

• transparent labware

• reflections

• illumination shifts

• overexposed scenes

This improved placement, disposal, and dual-arm manipulation performance compared to ACT, X-VLA, and standard SmolVLA.

1

1

10

481

May 6

Si eres recién egresado o estudiante de último semestre, te invitamos a la sesión informativa de reclutamiento de la empresa Labware.

Te esperamos este viernes 8 de mayo a las 12 PM en el Auditorio de la ESCOM.

3

409

May 5

Welcome to Day 5 of "Build Your Portfolio with Aniket." Use the trackers #BYPwithAK #Bharat2040AK to find other research posts & stock picks in this series.

Today, we decode

Theme 5: Global Healthcare, CDMO & MedTech (The Global Pharmacy Upgrade).

The catalyst here is not a new drug discovery; it is a geopolitical weapon called the U.S. BIOSECURE Act. The United States government is legally prohibiting its pharmaceutical giants from doing business with Chinese biotechnology and contract manufacturing companies due to national security concerns.

Billions of dollars in global R&D and manufacturing contracts are being forcibly evicted from China. There is only one country on earth with the FDA-approved infrastructure, the chemical engineering talent, and the scale to absorb this massive capital flight: India.

We are moving from basic generics to high-margin complex biologics, precision med-tech, and elite medical tourism. Here is the deep institutional teardown of the 4 sub-themes, the exact data driving them, and the fundamentally robust stocks positioned to capture this biological supercycle.

𝟓.𝟏. 𝐂𝐃𝐌𝐎 / 𝐂𝐑𝐀𝐌𝐒 (𝐓𝐡𝐞 𝐆𝐥𝐨𝐛𝐚𝐥 𝐑&𝐃 𝐎𝐮𝐭𝐬𝐨𝐮𝐫𝐜𝐢𝐧𝐠 𝐁𝐨𝐨𝐦)

The Sub-Theme Thesis: Developing a new drug costs billions of dollars and takes a decade. Global innovators (like Pfizer and Merck) no longer want to build their own massive chemical factories to test and produce these molecules. They outsource the chemistry to Contract Development and Manufacturing Organisations (CDMOs) and Contract Research and Manufacturing Services (CRAMS). With China's WuXi AppTec being essentially blacklisted by the US, global innovators are rushing to Indian CDMOs to secure their supply chains. The companies that hold the IP trust and the FDA-cleared facilities are entering a multi-year margin expansion cycle.

The Stock Picks:

𝟏. 𝐃𝐢𝐯𝐢'𝐬 𝐋𝐚𝐛𝐨𝐫𝐚𝐭𝐨𝐫𝐢𝐞𝐬 (𝐋𝐚𝐫𝐠𝐞 𝐂𝐚𝐩)

The Fundamentals: Divi's is the apex predator of the global API and custom synthesis (CDMO) market. They do not sell generic pills; they manufacture the highly complex active ingredients for the world's biggest innovators. When the global cycle dipped, Divi's didn't panic—they executed a massive ₹2,000 Crore capex entirely from internal cash flows. They operate with zero debt, and their historical EBITDA margins routinely hover in the god-tier 35-40% range. They hold a global monopoly on several key molecules (like Naproxen).

The Valuation & Entry Play: The stock endured a brutal 2-year correction as COVID-era revenues normalised. It has now bottomed out and is catching the new capex upcycle. It is a core portfolio anchor. Accumulate on any minor dips; the downside is heavily protected by its fortress balance sheet.

𝟐. 𝐒𝐲𝐧𝐠𝐞𝐧𝐞 𝐈𝐧𝐭𝐞𝐫𝐧𝐚𝐭𝐢𝐨𝐧𝐚𝐥 (𝐌𝐢𝐝/𝐋𝐚𝐫𝐠𝐞 𝐂𝐚𝐩)

The Fundamentals: Backed by Biocon, Syngene is a pure-play contract research powerhouse. If a US biotech startup has a drug concept, Syngene provides the scientists, labs, and manufacturing to bring it to life. Their transition from just "Discovery Services" to full-scale "Development and Manufacturing" (especially in high-value biologics) is driving massive operational leverage. They recently acquired the massive Stelis Biopharma facility, instantly upgrading their biologics capacity without the 3-year wait time required to build a greenfield plant.

The Valuation & Entry Play: Syngene commands a premium P/E because it operates like an IT-services company for biology—highly predictable, recurring client retainers. It is currently consolidating—an excellent zone to start a systematic accumulation plan.

𝟑. 𝐍𝐞𝐮𝐥𝐚𝐧𝐝 𝐋𝐚𝐛𝐨𝐫𝐚𝐭𝐨𝐫𝐢𝐞𝐬 (𝐒𝐦𝐚𝐥𝐥/𝐌𝐢𝐝 𝐂𝐚𝐩)

The Fundamentals: Neuland executed one of the most brilliant strategic pivots in the sector. They completely stepped away from high-volume, low-margin prime APIs and aggressively targeted Complex Peptides and Custom Manufacturing Solutions (CMS). Because peptides are incredibly difficult to synthesise, Neuland commands absolute pricing power. Look at the numbers: over the last three years, their ROCE has exploded from single digits to over 30%, and free cash flow is accelerating violently.

The Valuation & Entry Play: The market recognised the pivot and re-rated the stock into a multi-bagger. It is currently technically stretched and digesting the gains. Do not FOMO buy at the top. Wait for the stock to test its 100-day moving average before initiating a position.

𝟒. 𝐃𝐢𝐬𝐡𝐦𝐚𝐧 𝐂𝐚𝐫𝐛𝐨𝐠𝐞𝐧 𝐀𝐦𝐜𝐢𝐬 (𝐌𝐢𝐜𝐫𝐨/𝐒𝐦𝐚𝐥𝐥 𝐂𝐚𝐩)

The Fundamentals: This is a high-risk, deep-value turnaround bet. Dishman owns highly prized, FDA-approved oncology (cancer) manufacturing facilities in Switzerland and India. Operationally, they have been a disaster for years, plagued by debt and poor execution. However, they are currently restructuring, monetising non-core assets, and seeing their high-margin CDMO order book finally stabilise.

The Valuation & Entry Play: The stock is trading at distressed valuations. It is a pure asymmetric bet on the management executing the turnaround. Allocate no more than 1-2% of your risk capital here, buying only at the absolute technical support levels.

𝟓.𝟐. 𝐀𝐜𝐭𝐢𝐯𝐞 𝐏𝐡𝐚𝐫𝐦𝐚𝐜𝐞𝐮𝐭𝐢𝐜𝐚𝐥 𝐈𝐧𝐠𝐫𝐞𝐝𝐢𝐞𝐧𝐭𝐬 (𝐀𝐏𝐈𝐬) & 𝐈𝐧𝐭𝐞𝐫𝐦𝐞𝐝𝐢𝐚𝐭𝐞𝐬 (𝐓𝐡𝐞 𝐂𝐡𝐞𝐦𝐢𝐜𝐚𝐥 𝐁𝐚𝐜𝐤𝐛𝐨𝐧𝐞)

The Sub-Theme Thesis: During the pandemic, the world realised a terrifying truth: if China stops exporting basic chemical intermediates, the entire global pharmacy shuts down in weeks. The Indian government immediately launched PLI schemes for critical starting materials (KSMs) and APIs to force import substitution. The companies that manufacture these core chemical ingredients form the base layer of the healthcare ecosystem, and they are currently scaling up capacity to meet the "China Plus One" mandate.

The Stock Picks:

𝟓. 𝐋𝐚𝐮𝐫𝐮𝐬 𝐋𝐚𝐛𝐬 (𝐌𝐢𝐝 𝐂𝐚𝐩)

The Fundamentals: Laurus historically dominated the global ARV (HIV drug) API market. The market punished them recently because ARV pricing collapsed. But institutional money is looking to the future, not the past. Laurus has poured thousands of crores into a massive capex cycle to build synthesis capabilities (CDMO), biologics (Laurus Bio), and non-ARV APIs. As these massive new facilities come online and capacity utilisation increases, the operating leverage will drive a violent expansion in Return on Capital.

The Valuation & Entry Play: The stock has been heavily battered and has spent a year building a massive technical base. The worst of the earnings downgrades is priced in. This is a classic accumulation zone before the new capex begins generating revenue.

𝟔. 𝐆𝐥𝐞𝐧𝐦𝐚𝐫𝐤 𝐋𝐢𝐟𝐞 𝐒𝐜𝐢𝐞𝐧𝐜𝐞𝐬 (𝐌𝐢𝐝 𝐂𝐚𝐩)

The Fundamentals: Recently acquired by the Nirma Group, GLS is an absolute cash-generating machine. They focus on high-value, non-commoditised APIs (like cardiovascular and central nervous system molecules) for regulated markets (US/Europe). Their fundamentals are pristine: zero debt, ROCE consistently above 30%, and a management philosophy focused on high-margin product mix. Furthermore, they pay an incredibly generous dividend yield.

The Valuation & Entry Play: The stock rarely trades at the hyper-premiums of its CDMO peers because it is viewed as a steady API compounder. It is a fantastic, low-volatility anchor for your pharma allocation. Buy and hold for the dividends and steady compounding.

𝟕. 𝐒𝐮𝐩𝐫𝐢𝐲𝐚 𝐋𝐢𝐟𝐞𝐬𝐜𝐢𝐞𝐧𝐜𝐞 (𝐒𝐦𝐚𝐥𝐥 𝐂𝐚𝐩)

The Fundamentals: Supriya operates in a highly specific niche: anti-histamines, anaesthetics, and vitamin derivatives. They are the largest exporter of Salbutamol Sulphate from India. Because they hold dominant global market shares in these specific molecules (often 60% ), their pricing power is robust. They operate with high EBITDA margins (historically ~28-30%), zero debt, and are aggressively expanding their manufacturing blocks.

The Valuation & Entry Play: The stock corrected significantly from its IPO highs and has now fundamentally aligned with its earnings growth. It is an excellent mid-risk entry point to capture the API export boom.

𝟓.𝟑. 𝐀𝐝𝐯𝐚𝐧𝐜𝐞𝐝 𝐌𝐞𝐝𝐓𝐞𝐜𝐡 & 𝐃𝐢𝐚𝐠𝐧𝐨𝐬𝐭𝐢𝐜𝐬 𝐇𝐚𝐫𝐝𝐰𝐚𝐫𝐞 (𝐓𝐡𝐞 𝐈𝐦𝐩𝐨𝐫𝐭 𝐒𝐮𝐛𝐬𝐭𝐢𝐭𝐮𝐭𝐢𝐨𝐧)

The Sub-Theme Thesis: India is a global pharmacy, but we are embarrassingly dependent on imports for medical hardware. Over 75% of high-end medical devices and diagnostics consumables are imported. The government is forcefully correcting this via the National Medical Devices Policy and targeted PLIs. The domestic MedTech market is expected to surge from $11 Billion to $50 Billion by 2030. The domestic manufacturers stepping in to replace imported plasticware, syringes, and imaging machines are sitting on a gold mine of import substitution.

The Stock Picks:

𝟖. 𝐏𝐨𝐥𝐲 𝐌𝐞𝐝𝐢𝐜𝐮𝐫𝐞 (𝐏𝐨𝐥𝐲𝐦𝐞𝐝) (𝐌𝐢𝐝 𝐂𝐚𝐩)

The Fundamentals: Poly Medicure is the undisputed king of medical consumables in India. They manufacture IV cannulas, blood bags, and renal care plastics. They export to over 120 countries, demonstrating that their quality meets global standards. The fundamental trigger is their aggressive pivot from basic consumables into high-margin oncology, cardiology, and respiratory devices. Their financial discipline is flawless, maintaining 20% ROCE and generating consistent free cash flow to fund their continuous capex entirely debt-free.

The Valuation & Entry Play: This is a high-quality compounder. The market knows its worth, so it rarely trades cheaply. It consolidates, breaks out, and consolidates again. Use any 8-10% market-driven dip to accumulate.

𝟗. 𝐓𝐚𝐫𝐬𝐨𝐧𝐬 𝐏𝐫𝐨𝐝𝐮𝐜𝐭𝐬 (𝐒𝐦𝐚𝐥𝐥 𝐂𝐚𝐩)

The Fundamentals: Tarsons does not make drugs; it makes the plastic labware (pipettes, centrifuge tubes, petri dishes) required for every pathology lab and biotech R&D centre in the country. It is a classic "pick and shovel" play. As Indian CDMOs and hospitals scale, Tarsons' revenue scales automatically. They recently executed a massive capex to build a state-of-the-art facility in Panchla, which will double their capacity and allow them to target the export market against European legacy brands aggressively.

The Valuation & Entry Play: The stock was brutally punished post-IPO due to margin compression from high raw material (polymer) costs. The stock is currently trading near its historical lows, offering a massive margin of safety. As the new Panchla facility ramps up utilisation, the operating leverage will trigger a sharp re-rating. Deep value entry.

𝟏𝟎. 𝐊𝐫𝐬𝐧𝐚𝐚 𝐃𝐢𝐚𝐠𝐧𝐨𝐬𝐭𝐢𝐜𝐬 (𝐌𝐢𝐜𝐫𝐨/𝐒𝐦𝐚𝐥𝐥 𝐂𝐚𝐩)

The Fundamentals: Krsnaa is fundamentally disrupting the Indian diagnostics space. Unlike Dr Lal PathLabs or Metropolis, which fight for urban retail walk-ins, Krsnaa operates entirely on a B2G (Business-to-Government) Public-Private Partnership (PPP) model. They set up radiology and pathology centres inside government hospitals. Because the government provides the space and captive patient flow, Krsnaa operates at disruptive pricing (often 40% cheaper than retail labs) while maintaining excellent ROCE. They are expanding aggressively across tier-2 and tier-3 India.

The Valuation & Entry Play: The stock is highly volatile because the market gets spooked by government receivables (delayed payments). However, their execution is phenomenal. Use volatility to your advantage—buy heavily when the stock gets irrationally dumped amid temporary receivables fears.

𝟓.𝟒. 𝐏𝐫𝐞𝐜𝐢𝐬𝐢𝐨𝐧 𝐇𝐨𝐬𝐩𝐢𝐭𝐚𝐥𝐬 & 𝐌𝐞𝐝𝐢𝐜𝐚𝐥/𝐒𝐩𝐢𝐫𝐢𝐭𝐮𝐚𝐥 𝐓𝐨𝐮𝐫𝐢𝐬𝐦 (𝐓𝐡𝐞 𝐂𝐚𝐫𝐞 𝐀𝐫𝐜𝐡𝐢𝐭𝐞𝐜𝐭𝐮𝐫𝐞)

The Sub-Theme Thesis: The Indian middle class is expanding, and health insurance penetration among them is rising dramatically. When insurance pays the bill, patients abandon government clinics and demand premium corporate hospitals. Furthermore, India has become the apex destination for global Medical Value Travel (MVT). Patients from the Middle East, Africa, and Southeast Asia are flying to India for complex organ transplants and oncology surgeries at a fraction of Western costs. The metric that matters here is ARPOB (Average Revenue Per Occupied Bed). The hospitals that optimise ARPOB while scaling their bed capacity are printing wealth.

The Stock Picks:

𝟏𝟏. 𝐀𝐩𝐨𝐥𝐥𝐨 𝐇𝐨𝐬𝐩𝐢𝐭𝐚𝐥𝐬 𝐄𝐧𝐭𝐞𝐫𝐩𝐫𝐢𝐬𝐞 (𝐋𝐚𝐫𝐠𝐞 𝐂𝐚𝐩)

The Fundamentals: The undisputed apex predator of Indian healthcare. They are not just a hospital chain; they are an integrated omni-channel healthcare ecosystem. Their legacy hospital business generates massive, stable cash flows with industry-leading ARPOB. The true alpha is "Apollo 24/7" (their digital health app) and their aggressive pharmacy rollout (Apollo HealthCo). They are capturing the patient at every touchpoint—from online consultation to pharmacy delivery to complex surgery.

The Valuation & Entry Play: the ultimate defensive growth anchor. The market occasionally penalises the stock due to cash burn in Apollo 24/7's digital segment. Those exact moments of punishment are your window to accumulate. It is a core holding.

𝟏𝟐. 𝐍𝐚𝐫𝐚𝐲𝐚𝐧𝐚 𝐇𝐫𝐮𝐝𝐚𝐲𝐚𝐥𝐚𝐲𝐚 (𝐌𝐢𝐝/𝐋𝐚𝐫𝐠𝐞 𝐂𝐚𝐩)

The Fundamentals: Founded by Dr Devi Shetty, Narayana is famous for its brutal operational efficiency and cost-control in India. However, the financial genius of this company lies offshore. They own a highly lucrative hospital in the Cayman Islands. The Cayman facility targets US-based patients and generates massive, dollar-denominated cash flows with incredibly high margins. They use the cash cow in the Caymans to aggressively fund their expansion in the domestic Indian market without taking on crippling debt. The result? A ROCE exceeding 25% in a traditionally capital-heavy sector.

The Valuation & Entry Play: The stock has performed exceptionally well and is currently in a steady phase of compounding. It trades at a reasonable multiple compared to its elite return ratios. Accumulate systematically; it is one of the best-managed hospital chains on the planet.

𝟏𝟑. 𝐀𝐫𝐭𝐞𝐦𝐢𝐬 𝐌𝐞𝐝𝐢𝐜𝐚𝐫𝐞 𝐒𝐞𝐫𝐯𝐢𝐜𝐞𝐬 (𝐌𝐢𝐜𝐫𝐨/𝐒𝐦𝐚𝐥𝐥 𝐂𝐚𝐩)

The Fundamentals: Promoted by the Apollo Tyres group, Artemis operates a massive, ultra-premium quaternary care hospital in Gurugram (NCR). They are a major beneficiary of medical tourism. Their fundamental strategy is brilliant: instead of taking on massive debt to build new hospitals from scratch (greenfield), they are executing an "asset-light" expansion. They are adding beds to their existing Gurugram facility and managing smaller boutique centres. This ensures their ROCE expands rapidly without diluting equity.

The Valuation & Entry Play: An undiscovered micro-cap gem in the hospital space. It trades at a significant discount to the EV/EBITDA multiples of larger peers like Max Healthcare or Medanta. It is currently breaking out of a long consolidation zone. Excellent entry point for asymmetric growth.

𝐓𝐡𝐞 𝐏𝐨𝐫𝐭𝐟𝐨𝐥𝐢𝐨 𝐀𝐜𝐭𝐢𝐨𝐧 𝐏𝐥𝐚𝐧:

Healthcare requires a balance of aggressive growth and absolute defensive stability.

1. The Core Base: Anchor 50% in the monopolies (Divi's Lab, Apollo Hospitals). They will protect your capital when the broader index crashes.

2. The Growth Pivot: Allocate 35% to the companies executing massive capex or strategic pivots (Laurus Labs, Syngene, Poly Medicure).

3. The Value Discovery: Reserve 15% for the distressed micro-caps and import-substitution plays (Tarsons, Artemis, Dishman) where the margin of safety is highest.

Bookmark this thread. The global pharmacy is open for accumulation. Comment or DM for any clarifications.

Tomorrow, we move to

Theme 6: Smart Mobility, Auto-Ancillaries & Railway Modernisation (The Network). Follow and turn on your notifications so you don't miss it.

IMPORTANT NOTE:

First, validate the stock through fundamental analysis. Learn how: x.com/AniketFiles/status/205…

Only then, enter using technical analysis. Strictly use the risk management process (stop-loss) and position sizing (number of shares). Learn how: x.com/AniketFiles/status/205…

Disclaimer: I am not a SEBI-registered analyst. Any stocks mentioned in this post are not an investment recommendation but only for educational purposes. Invest at your own discretion and strictly practice effective position sizing and risk management. Consult a registered financial advisor before any investment.

#BYPwithAK #Bharat2040AK #StockMarketIndia #Investing

May 4

Technical Analysis & CHART-BASED RULES for Stock ENTRY, EXIT & STOP LOSS

(Timeframe - MONTHLY

Investment Horizon > 3 YEARS

Tool Used for stock screening - CHARTINK/SCREENER

Use this only on fundamentally good stocks. Read about fundamental analysis here: x.com/AniketFiles/status/205…)

Technical Analysis Steps:

1. Run a scan on all stocks for the monthly RSI crossing above 60. The monthly candle on which RSI crosses above 60 becomes your alert candle.

2. Ensure these conditions are satisfied.

- ADX positive > ADX negative

- Monthly close price > Monthly SMA [close] (20)

3. The conditions below are not mandatory, but if they are there, they make the conviction stronger.

- Monthly close price > Monthly SMA [close] (50)

- Monthly SMA [close] (20) > Monthly SMA [close] (50)

- Monthly Volume > Monthly SMA [volume] (20)

4. Set a Buy GTT with the trigger price just above the high of your alert candle.

[If you miss the bus here, don't chase it. You will get opportunities later or in other stocks]

5. Set the Stop Loss = value of the monthly SMA 50 of the same month as the alert candle.

6. Calculate your Risk per trade. We typically take it as 1% to 2% of the total capital we will deploy for investment.

E.g. If your initial investing capital is INR 10 lakhs, your risk per trade (RPT) is 1% of 10 lakhs = Rs. 10,000/-

7. Calculate the total number of shares you will buy using this formula.

No. of shares = [RPT / (Buy Price - Stop Loss)]

8. Keep updating your stop loss to the monthly SMA50 value every month end, till the time the trade lasts. Use the sell GTT feature for putting the stop loss. Enable DDPI authorisation for auto-sell of the particular stock(s) if the stop-loss is breached.

9. If the stock dips and again crosses the monthly RSI 60, pyramid your position and follow all the above steps again.

10. If the stock price goes below the monthly SMA 20, book partial profits. If the price breaches the SMA 50, exit completely.

11. If the stock is newly listed, you can follow the same strategy on the weekly chart, as the monthly lines would not have been formed.

12. Another combo-strategy is to buy a small quantity of the stock at the monthly SMA 50 support (to test the waters) and buy the remaining quantity when the above conditions (1-10) are fulfilled / or when a chart pattern breakout happens.

13. Follow this strategy like a robot without any emotions of panic or fear. greed or hope. If the stop loss is hit, exit. Do not keep holding on to false hope.

One sample chart with buy, SL & exit is given in this post thread. You can apply the same strategy to any stock (Indian or US). Try it out.

Comment your stock name and start date, and I will show you how.

Important NOTE: Use this technical strategy only on fundamentally good stocks. Read this post to know how to do fundamental analysis for any stock.

x.com/AniketFiles/status/205…

1

2

814