Jun 11

$CC fluid for immersion cooling. AI racks hitting 100kW need this. Samsung, 2CRSi, LiquidStack onboard. Revenue coming H2 2026. Early stage, real potential. Solid find, Hunter.

1

1

122

Jun 11

$CC

5% today.

100$ Stock just chilling as next AI bottleneck at 21$

Found a cool one x fam. I got bored and went digging into another AI infrastructure layer that almost nobody is talking about.

DONT MISS X FAM😤

I would save this one & Subscribe to support. Thanks legends

Everyone is chasing GPUs, power generation, networking, and data centers, but very few investors are looking at the cooling fluid layer that may become increasingly important as AI rack densities move from the historical 10-20kW range toward 50kW, 100kW, and even 120kW per rack.

$CC (Chemours) could be one of the more overlooked AI infrastructure names if two-phase liquid cooling adoption accelerates from late 2026 through 2028.

The thesis is simple.

As $NVDA Blackwell, Rubin, and future AI systems push power consumption higher, air cooling becomes increasingly inefficient. Liquid cooling becomes another bottleneck that must be solved.

Chemours developed Opteon™ 2P50, a proprietary HFO-based dielectric fluid engineered for two-phase immersion and advanced direct-to-chip cooling. The fluid boils at roughly 49°C, allowing heat to be removed through phase change rather than relying primarily on airflow and traditional cooling methods.

The niche layer here is the fluid itself.

Without the cooling fluid, the tanks, cold plates, pumps, and servers don’t matter.

Opteon was designed with an ultra-low GWP of roughly 10, zero ozone depletion potential, non-flammable properties, strong dielectric performance, and a recoverable/reusable design that supports long-term deployment in high-density AI environments.

What caught my attention were the infrastructure benefits being discussed.

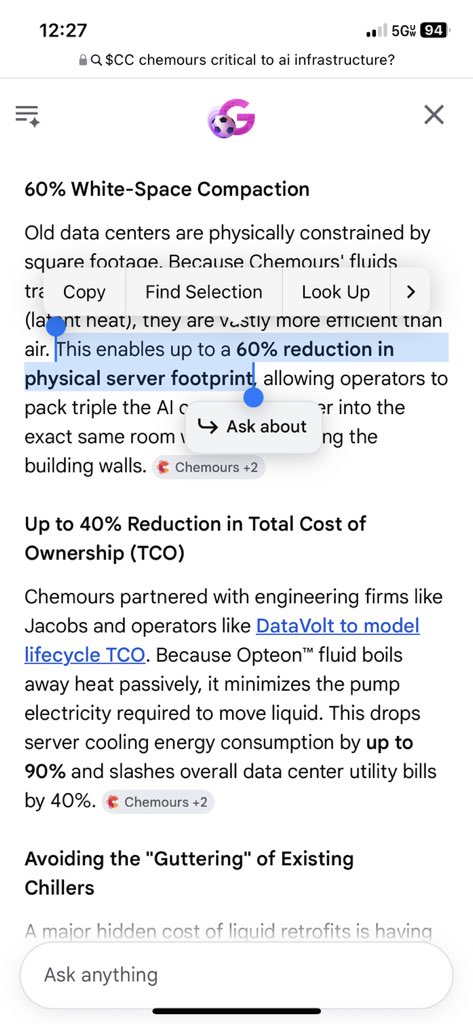

Chemours and its partners have cited up to 90% lower cooling energy consumption, PUE approaching 1.0-1.05, near-zero water usage, up to 40% lower total cost of ownership, and data center footprints that can be reduced by as much as 60% in certain deployments.

Thinking out loud…

If AI infrastructure continues scaling toward 100kW racks, cooling fluids stop being a small component expense and become critical infrastructure.

The ecosystem is already forming.

Samsung qualified Opteon as the first two-phase immersion cooling fluid approved for SSDs in 2025, removing a major adoption hurdle for storage systems.

2CRSi signed a Joint Development Agreement with Chemours in February 2026 after successfully qualifying the fluid in its server platforms, helping accelerate deployment of purpose-built AI and HPC systems including ultra-dense configurations using NVIDIA accelerators.

Chemours has also partnered with DataVolt, LiquidStack, and Navin Fluorine, with manufacturing capacity beginning in 2026 specifically to support commercialization of liquid cooling products.

Financially, this is still very early.

Q1 2026 Thermal & Specialized Solutions revenue reached $568M, up 22% YoY, while EBITDA climbed to $190M, up 35% YoY. Liquid cooling revenue is still too small to break out separately, which is exactly why the opportunity remains overlooked.

Management has previously referenced a liquid cooling technology opportunity of roughly $550M in the near term that could expand toward $3B over the next decade. Most expectations point toward initial revenue contributions beginning in H2 2026 as production capacity comes online, with more meaningful adoption and deployment wins expected during 2027 and beyond.

Risks remain. Single-phase cooling may continue dominating portions of the market, hyperscaler adoption could take longer than expected, and deployment costs still matter.

But if two-phase cooling becomes a preferred solution for ultra-dense AI clusters, Chemours has a legitimate shot at becoming a category leader in one of the most important and least discussed layers of AI infrastructure.

Everyone is focused on the GPUs.

I’m interested in the fluid that keeps them running.

$CC $ROG $CEG $AVGO $MSFT $GOOG $NBIS $NVDA $IREN $MU $AMD $CE $AAPL $TSLA $SPCX

15

6

43

2,982

Jun 8

closed-loop systems, dry cooling, or dielectric liquid immersion.

None of these methods use any water past the initial fill.

Companies like Vertiv, Zetacore, liquidstack, Submer, Iceotope, GRC... etc etc

All great stocks btw😁

44

Jun 8

Vertiv acquired Strategic Thermal Labs, Ecolab acq CoolIT Systems, Trane acq LiquidStack, Daikin acq Chilldyne, Schneider Electric acq Motivair, Johnson Controls acq Alloy Enterprises, Eaton acq Boyd Thermal, Carrier investment in ZutaCore, Alfa Laval AB, nVent

114

Jun 7

Now immersion, the wildcard.

This is the approach where the whole server gets submerged in dielectric fluid. The problem with playing it is that nearly every pure immersion company is private. GRC, Submer, Asperitas, LiquidCool, the specialists you read about, none of them are listed.

A few listed ways to get exposure do exist.

$DUG, DUG Technology, an Australian name and the most interesting niche play here. DUG is really a high performance computing and seismic software company, but it runs its own immersion cooling system, DUG Cool, and is building immersion cooled HPC campuses. Tiny, around 100 million Australian dollar cap, and immersion is one piece of a broader HPC story rather than the whole thing. A genuine curiosity for anyone who wants a pure-ish immersion angle.

For the larger, more diluted exposure, $TT, Trane, owns LiquidStack, one of the original two phase immersion pioneers. And $NVT, nVent, has an alliance with Iceotope for precision immersion. In both cases immersion is a small slice of a much bigger business, so it barely moves the needle on the stock.

Here is the honest read. Immersion is elegant and it is being deployed in real sites, but the industry has not committed to it the way it has to direct to chip. It demands a completely different data center design, and that is a high bar. Interesting, real, but the least settled of the three. I would not build a thesis on it alone.

Next, the picks and shovels, the layer that gets paid no matter which technology wins.

1

11

5,187

Jun 1

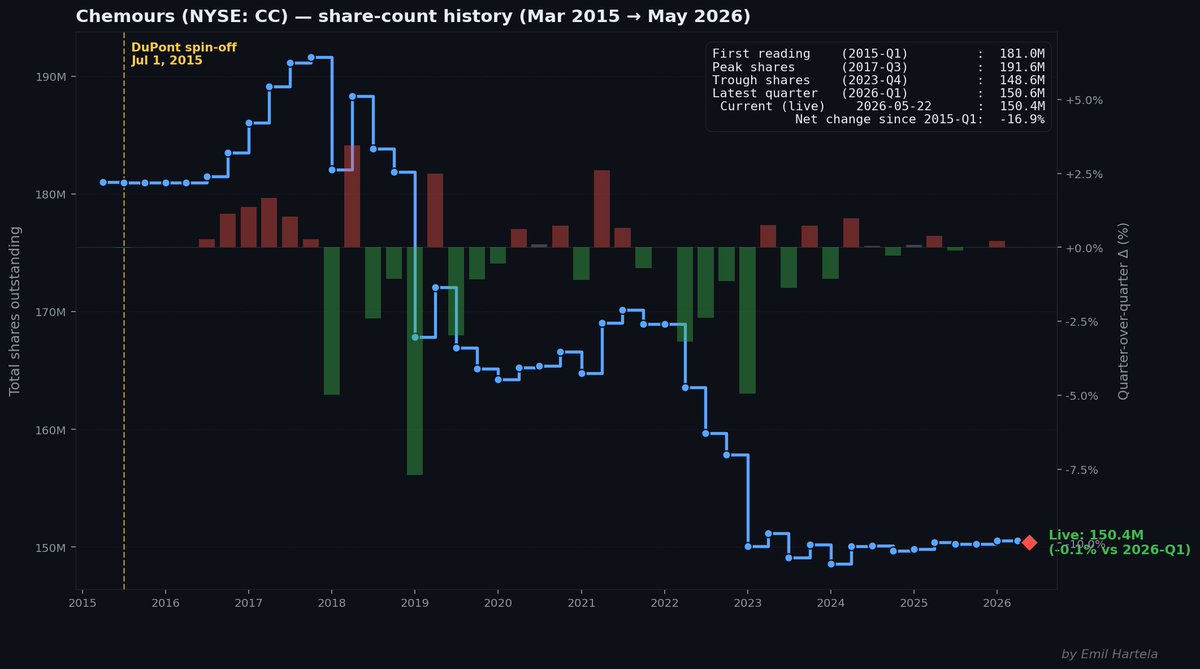

Long $CC at ~$3,33B market cap (~$22,16).

My read: this is the embedded fluid play on two-phase cooling that the market is treating purely as a refrigerants and TiO2 cyclical, ignoring the optionality sitting inside.

$CC owns Opteon 2P50, a purpose-built dielectric fluid for two-phase immersion, not a shoehorned legacy molecule like the Novec chemistry that stalled the category when 3M exited. That exit left a hole; Chemours built the replacement from scratch.

The setup is simple. AI and next-gen chips are pushing rack densities past what air and single-phase can handle. Two-phase immersion cuts cooling energy by up to 90%, nearly eliminates water, and shrinks data center footprint by up to 60%. $INV (Zutacore) and the system builders need the fluid, and the qualified fluid supply is narrow.

The qualification flywheel is already turning. Samsung qualified Opteon on its gen-four SSD; 2CRSi signed a JDA in Feb after qualifying it in current servers; DataVolt and LiquidStack partnerships in place; Navin Fluorine manufacturing capacity coming online in 2026. Every qualification is a recurring, designed-in consumable, not a one-off sale.

Why it's mispriced. TSS is already the crown jewel: Opteon refrigerants up 56% in 2025, now 75% of refrigerant sales, segment margins around 32%. The market pays for that refrigerant ramp but assigns roughly zero to the cooling-fluid optionality stacked on top. You get the refrigerant story at a reasonable multiple and the two-phase call option for free.

The DNA fits. 90 years of fluorochemistry and thermal management, the manufacturing base, and the regulatory know-how to run a sealed closed-loop fluid through PFAS scrutiny. That last part is the moat; it's exactly the barrier that keeps this from being a commodity.

Risks, because they're real: $4,4B debt load and a deleveraging story that has to work; PFAS litigation and regulatory overhang on fluorinated chemistry; two-phase immersion adoption is a bigger architectural leap for data centers than direct-to-chip, so the ramp is back-half loaded and slower than the hype; TiO2 cyclicality drags the consolidated multiple.

I genuinely don't get how the market pays full freight for the refrigerant ramp while treating the two-phase immersion franchise, the qualified fluid for the densest AI racks, as a rounding error. My guess is it stays buried because $CC screens as a tired chemicals cyclical with a debt problem, not an AI-cooling enabler. I think that shifts as immersion qualifications convert to volume and the recurring consumable revenue starts landing.

Position is my own.

DYOR, NFA.

TLDR: Two-phase immersion is where cooling goes when air and single-phase run out of room for AI racks. $CC built the purpose-made fluid; $INV (Zutacore) build the systems that need it. Already has Samsung, 2CRSi and DataVolt qualifications turning, and the market prices none of it because it sees a refrigerants and TiO2 cyclical. I'm long the embedded call option.

14

2,377

KI-Begriffe einfach erklärt — Teil 10: Thermomanagement

Gestern haben wir gelernt: Ein KI-Rack verbraucht so viel Strom wie 40 Haushalte. Aber Strom verschwindet nicht einfach — es wird zu Wärme.

Und Wärme ist der grösste Feind jedes Chips.

Zurück in die Küche:

Stell dir vor, deine Profiküche hat keine Lüftung. Keine Abzugshaube, keine Klimaanlage, keine Kühlung.

Die ersten Minuten: alles funktioniert.

Nach einer Stunde: Die Köche schwitzen, Fehler passieren.

Nach zwei Stunden: Die Hitze ist unerträglich, niemand kann mehr arbeiten.

Nach drei Stunden: Die Küche steht in Flammen.

Genau so verhält sich ein KI-Chip ohne Kühlung. NVIDIAs H100 erzeugt bis zu 700 Watt Wärme — auf einer Fläche kleiner als deine Handfläche. Ohne aktive Kühlung wäre er in Sekunden zerstört.

Drei Kühlmethoden — von klassisch bis revolutionär:

🟥 Luftkühlung — die Abzugshaube

Riesige Ventilatoren blasen kalte Luft durch die Server-Racks. Jahrzehntelang der Standard. Einfach, bewährt, wartungsfreundlich. Aber bei modernen KI-Chips schlicht nicht mehr ausreichend. Die Luftmengen die man bräuchte um einen GB200-Cluster zu kühlen wären so gewaltig dass die Gebäude strukturell versagen würden.

🟡 Liquid Cooling — Wasserкühlsystem direkt am Herd

Kaltes Wasser fliesst durch Kühlplatten die direkt auf den Chips sitzen — wie eine Wasserpfeife die Wärme abführt bevor sie sich ausbreitet. Deutlich effizienter als Luft, weil Wasser Wärme 25x besser leitet. Google, Meta und Microsoft rüsten ihre Rechenzentren gerade massenhaft auf Liquid Cooling um. NVIDIAs neue GB200-Racks sind ab Werk für Liquid Cooling ausgelegt — Luftkühlung ist keine Option mehr.

🟢 Immersion Cooling — der Koch taucht ins Kühlbad

Die radikalste Lösung: Server werden komplett in eine spezielle nicht-leitende Flüssigkeit getaucht — ähnlich wie Frittieröl, aber für Elektronik. Die Flüssigkeit nimmt die Wärme direkt auf, wird abgekühlt und wiederverwendet. Extrem effizient — bis zu 95% weniger Energieverbrauch für Kühlung. Microsoft und mehrere grosse Cloud-Anbieter testen das bereits in Pilotprojekten. Die Herausforderung: Wartung ist aufwendig, und nicht jede Hardware ist dafür ausgelegt.

Warum Thermomanagement plötzlich Milliarden wert ist:

Bis vor wenigen Jahren war Kühlung ein nachgelagertes Problem — irgendjemand kümmert sich schon darum. Heute ist es eine der grössten Kostenpositionen beim Bau und der Verwaltung eines Rechenzentrums.

Bis zu 40% des gesamten Stromverbrauchs eines klassischen Rechenzentrums entfallen auf Kühlung. Bei einem 100-Megawatt-Rechenzentrum sind das 40 Megawatt die nichts rechnen — sondern nur kühlen. Jedes Prozent Verbesserung bei der Kühleffizienz spart Millionen Dollar pro Jahr.

Dazu kommt: Rechenzentren entstehen heute oft dort wo Strom günstig ist — Skandinavien, Island, Kanada. Nicht zufällig sind das auch Kühlklimate. Microsoft hat ein Rechenzentrum unter Wasser vor der schottischen Küste getestet — das Meer als natürliche Kühlung.

Wer davon profitiert:

🌡️ Vertiv $VRT — weltgrösster Spezialist für Rechenzentrum-Kühlinfrastruktur, direkt im Zentrum des Booms

🌡️ Eaton $ETN — Power- und Kühlmanagement für Rechenzentren

🌡️ Schneider Electric — europäischer Marktführer für Rechenzentrum-Infrastruktur

🌡️ Alfa Laval & Modine Manufacturing $MOD — Spezialist für Wärmetauscher, stark bei Liquid Cooling

🌡️ LiquidStack & GRC (Green Revolution Cooling) — Pioniere bei Immersion Cooling

Diese Unternehmen bauen keine Chips. Aber ohne sie läuft kein einziger KI-Chip länger als ein paar Sekunden.

Kurz zusammengefasst:

🌡️ Wärme ist der grösste Feind des Chips — ohne Kühlung kein KI

💨 Luftkühlung stirbt — zu schwach für moderne KI-Chips

💧 Liquid Cooling wird Standard — direkt auf dem Chip, ab Werk eingebaut

🛬 Immersion Cooling kommt — radikal effizient, noch in der Einführungsphase

📈 Vertiv, Schneider Electric, Modine — die stillen Gewinner des KI-Booms

KI-Begriffe einfach erklärt — Teil 8: Precision Timing ICs

Wir haben unsere Küche optimiert: Chefkoch und Hilfskräfte arbeiten eng zusammen, Bestellungen kommen per Lichtstrahl rein. Aber heute geht es um etwas das jeder vergisst — und ohne das alles sofort zusammenbricht.

Den Takt.

Stell dir vor, die Küche hat kein gemeinsames Timing.

Hilfskraft 1 brät das Steak. Hilfskraft 2 macht die Sauce. Hilfskraft 3 wärmt den Teller. Aber alle arbeiten nach ihrer eigenen Uhr — eine läuft eine Sekunde vor, eine andere eine Sekunde nach.

Das Ergebnis: Das Steak ist fertig, die Sauce noch nicht. Der Teller ist kalt. Das Gericht landet nie gleichzeitig auf dem Tisch.

In einer Profiкüche löst das der Chefkoch — er gibt den Takt vor. „In 3 Minuten geht Tisch 7 raus — alle fertig!“

In einem KI-Rechenzentrum übernimmt das der Precision Timing IC.

Was Precision Timing ICs genau machen:

Ein modernes Rechenzentrum besteht aus tausenden Chips und Servern die alle gleichzeitig rechnen. Damit das funktioniert müssen alle exakt denselben Takt haben — synchronisiert auf die Nanosekunde.

Eine Nanosekunde ist eine Milliardstel Sekunde. Das klingt unvorstellbar klein. Aber bei Chips die Milliarden Operationen pro Sekunde durchführen bedeutet selbst eine winzige Abweichung: falsche Berechnungen, Datenverlust, Systemabsturz.

Precision Timing ICs sind die Taktgeber — hochpräzise Oszillatoren und Taktverteiler die sicherstellen dass jeder Chip im richtigen Moment arbeitet. Sie sind winzig, kosten manchmal nur wenige Dollar — aber ohne sie läuft gar nichts.

Warum KI das Problem drastisch verschlimmert:

Früher hatte ein Server vielleicht einen oder zwei Chips die synchronisiert werden mussten. Ein normaler Taktgeber reichte.

NVIDIAs GB200 NVL72 — ein einziges KI-Rack — verbindet 72 GPUs direkt miteinander. Alle 72 müssen nanosekunden-genau synchron laufen. Über tausende solcher Racks hinweg wird das zu einer der grössten Präzisions-Herausforderungen der gesamten Industrie.

Dazu kommt: Optical Transceivers — über die ich im letzten Post geschrieben habe — brauchen ebenfalls hochpräzises Timing. Licht reist unglaublich schnell. Wenn der Takt auch nur minimal falsch liegt kommen Datenpakete in der falschen Reihenfolge an.

Der unsichtbare Markt mit riesigem Wachstum:

Precision Timing ist einer der am wenigsten bekannten Bereiche der Halbleiterindustrie — und gleichzeitig einer der am schnellsten wachsenden.

Die dominanten Unternehmen:

⏱️ Renesas Electronics — weltweiter Marktführer bei Timing-Chips, liefert an praktisch jeden grossen Rechenzentrum-Betreiber

⏱️ Silicon Laboratories $SLAB — spezialisiert auf hochpräzise Oszillatoren für KI-Infrastruktur

⏱️ Microchip Technology $MCHP — breites Timing-Portfolio, stark in Telekommunikation und Rechenzentren

⏱️ Skyworks & Murata $SWKS — Quarzoszillatoren als physische Basis für alle Timing-Systeme

Diese Unternehmen sind systemkritisch — kein einziges KI-Rechenzentrum funktioniert ohne ihre Produkte.

Kurz zusammengefasst:

⏱️ Precision Timing ICs — synchronisieren tausende Chips auf die Nanosekunde

⚡ Ohne Takt: falsche Berechnungen, Datenverlust, Absturz

📈 KI vergrössert das Problem massiv — mehr Chips, höhere Präzision nötig

🤵 Systemkritisch aber kaum bekannt — Renesas, Silicon Labs, Microchip Technology profitieren

1

3

15

3,252

May 28

did some digging so you don't have to, and how crazy is this?

One little AI accelerator touches dozens of hyper-specialized companies across three continents, and we’re talking thousands of engineers, chemists, and machinists who’ve never met each other but have to hit their exact tolerances or the whole thing doesn’t work.

If you map every layer of an AI accelerator package and name the under-followed supplier at each layer, the map looks like this:

The fiberglass that goes inside ABF substrates: Nittobo Industries (Japan, private), Asahi Kasei (3407.T), Owens Corning (OC) on the lower-end grades. Unimicron just warned that low-CTE supply is the next constraint.

The ABF film itself: Ajinomoto (2802.T) holds 98% of the IP and licenses it to five substrate makers.

The substrate fabricators: Ibiden (4062.T), Unimicron (3037.TW), Nan Ya PCB (8046.TW), Shinko (7820.T), Kinsus (3189.TW). Ibiden's share is 85% to 55% over three years.

The interposer and CoWoS process: TSMC (TSM), with outsourced spillover to ASE / SPIL (3711.TW), Amkor (AMKR), Powertech (6239.TW).

The hybrid bonding step: BESI (BESIY / BESI.AS), with KLIC (Kulicke and Soffa) as the secondary equipment vendor.

The 3D metrology for HBM stacking: Onto Innovation (ONTO), Camtek (CAMT), Nova (NVMI).

The encapsulation chemistry that prevents the package from melting: Sumitomo Bakelite (4203.T), Shin-Etsu (4063.T), Nitto Denko (6988.T).

The PCB the package sits on: TTM Technologies (TTMI), Unimicron (cross-listing), Ibiden (cross-listing).

The 800G/1.6T optical chipsets: MACOM (MTSI), AAOI, Marvell (MRVL), Credo (CRDO).

The lasers feeding optical engines: Lumentum (LITE), Coherent (COHR), Sivers (SIVE.ST), IPG Photonics (IPGP), nLight (LASR).

The InP substrate underneath the lasers: AXT (AXTI), Sumitomo Electric (5802.T / SMTOY), IQE plc (IQE.L), Freiberger (private).

The wafer-level burn-in tooling: Aehr Test Systems (AEHR).

The retimers that keep the signal alive: Astera Labs (ALAB), Credo (CRDO).

The CXL controllers for system-level memory: Astera Labs (ALAB again), Marvell (MRVL again), Samsung Electro-Mechanics (009150.KS), SK Hynix (000660.KS).

The HBM itself: SK Hynix (000660.KS, 62% share), Micron (MU), Samsung (005930.KS).

The cooling at rack scale: Vertiv (VRT), Modine Manufacturing (MOD), LiquidStack via Trane Technologies (TT), CoolIT now inside Ecolab (ECL), Boyd (private).

The power semis converting 800V to 1V on the GPU rack: Power Integrations (POWI), Innoscience (2577.HK), Navitas (NVTS).

The high-voltage transformers feeding the substation: Siemens Energy (ENR.DE), GE Vernova (GEV), Hitachi (6501.T), Eaton (ETN), Virginia Transformer (private).

That is the supply chain

The names most generalists could pronounce are the GPU vendor and three or four ETF-level large caps. The actual binding constraints sit in the smaller names two and three layers below.

May 7

built a dashboard to track ai related bottlenecks: aibottlenecks.app/

12

34

274

49,656

May 26

❄️AI時代に必要な「冷却技術」と強みを持つ海外企業🌏

・Vertiv 🇺🇸

・STULZ 🇩🇪

・nVent 🇬🇧

・Schneider Electric 🇫🇷

・CoolIT Systems 🇨🇦

・Asetek 🇩🇰

・LiquidStack 🇳🇱

・Submer 🇪🇸

・GRC / Green Revolution Cooling 🇺🇸

・Iceotope Technologies 🇬🇧

・Motivair 🇺🇸

・Atos 🇫🇷

・Alfa Laval 🇸🇪

・SPX Technologies 🇺🇸

・Kelvion 🇩🇪

・SWEP 🇸🇪

・Veolia 🇫🇷

・SUEZ 🇫🇷

・Ecolab 🇺🇸

・Pentair 🇬🇧

#株 #投資 #日本株 #米国株 #AI #半導体

2

3

6

405

May 24

$IREN: Misconceptions on Design vs Vertical Integration

Posts like this one from @CernunnosCap are false FUD from people who understand nothing about engineering. All Hyperscalers, Neoclouds "design" their own cooling at the facility and rack level but none of them have vertical integration down to the components themselves. The components themselves are sourced from Vertiv, Schneider/Motivair, CoolIT, Boyd, nVent, Delta, Asetek, LiquidStack, ZutaCore, Accelsius. Among HS/Neoclouds that disclose their solution let's take a look at what's actually happening.

Amazon

In 2025, Amazon revealed their "in-house-engineered IRHX, a rack-level-cooling platform" (1). However, if you read the article beyond the headline, you'll see "Second, while AWS is an engineering powerhouse, it rarely develops these solutions in isolation. It typically partners with established vendors to co-design its proprietary systems, which are also manufactured by third parties. IRHX may carry the AWS name, but it is likely being built in the facilities of well-known cooling equipment suppliers" (1).

(1) delloro.com/awss-new-liquid-…

What's actually happening is that Amazon is "designing" through driving the specifications and mixing and matching components that are made by vendors. They do not design any of the components themselves.

Google

Project Deschutes is the most verticle integrated datacenter cooling among all Hyperscalers and Neoclouds but at the end of the day Google driving the specifications and mixing and matching components. "Project Deschutes is a collaborative effort, with prototypes already demonstrated at OCP and SC2025 by vendors including Boyd, Coolermaster, Delta, Envicool, Nidec, nVent, Stulz, and Vertiv" (2).

arpa-e.energy.gov/sites/defa…

IREN

$IREN also designs their cooling at the facility and rack level and uses components and IP blocks from both Motivair, Vertiv for Frontend cooling, and other components for backend cooling. Motivair parts you can see from Dan's Post. The other components can be found in @FransBakker9812 subgroup.

NBIS

Likewise $NBIS their cooling at the facility and rack level but I guarantee you they use components and IP blocks from vendors. How do I know this? I know how "cooling design" engineering works at SMCI - design is a fancy way of driving specifications and mix-matching components and IP from vendors. You can see public evidence of that Amazon and Google doing exactly that.

Summary

Don't get confused by heavy buzzwords like vertical integration. Most people throw that term around without knowing what it really means.

There are people who falsely think that by integrating Nvidia chips that NBIS is vertically integrated down to the hardware. Integration is not vertical integration. Even Google TPU's rely on many $AVGO IP blocks for networking, advanced packaging and even some IP Cores for the ASIC design itself. There are very few companies that have substantial true vertical integration down to the components: $TSLA and $NVDA are two.

May 24

$IREN Congratulations on figuring out Liquid Cooling 👏

Well, now we know where they are buying their liquid cooling equipment from - Motivair by Schneider Electric.

So they are buying:

Server racks from $DELL $SMCI

Liquid cooling from Schneider

Can someone explain how this is Vertically Integrated? And won’t hurt their margins.

Compared to companies like $NBIS, which designs its own proprietary racks, servers, and cooling systems entirely in-house.

People were quick to jump on the Nebius x Bloom partnership, even though it’s half the price of Traditional Colocation.

The path to profitability is clearer for a company like Nebius.

#ai #Datacenters

25

19

253

55,345

Why Water(H₂O) is the Next Big Bottleneck in AI Infrastructure?

Power gets all of the attention, but water is an increasingly important issue for artificial-intelligence data centers, which require massive amounts of H₂O for cooling.

Water, water everywhere, but...is too much going to artificial-intelligence data centers? That’s the challenge and opportunity—facing industrial stocks that specialize in H₂O

AI is the growth engine of this stock market, driving everything from utility earnings to SpaceX’s planned $2 trillion initial public offering. That makes it important for investors to understand any potential AI bottlenecks. While power gets all of the attention, water is a growing issue. More-powerful AI chips need water to cool them, and managing that increasingly scarce resource is now mission-critical for any hyperscaler that wants to maintain good public relations and be a reasonable steward of the environment.

The issue is only going to get more critical. Nvidia’s H100 chips are currently the most widely deployed AI chip. They can still be cooled by what are essentially big fans blowing air from a giant air conditioner. Such air conditioners, like home ACs, are essentially closed-loop systems, in which a refrigerant circulates within a sealed system. Newer chips use more power, necessitating new cooling solutions, including direct-to-chip cooling, where a plate is attached to the processor. It’s a bit like the way car engines are cooled, with coolant circulating through the equipment. Eventually, chips will need to be cooled by immersing the server in a liquid and with special evaporating liquids, though that’s still years down the road.

This will require lots of water. Morgan Stanley estimates that AI water use will grow to more than one trillion liters by 2028, or 400,000 Olympic-size swimming pools. That includes water for power generation, much of which gets recirculated, as well as for cooling and other purposes, so the ultimate amount may be less. Still, it will be up to industrial companies to build systems that can cool chips in efficient closed-loop systems, with as little water as possible. Here are six stocks that should benefit.

These six companies stand to benefit from the sector’s burgeoning growth.

--------------------------------------

1. Eaton (ETN / NYSE)

Recent Price: $395.06

Market Value: $153.3 B

Forward P/E: 29.7

52-Week Return: 44.3%

Packaging power and cooling together is a competitive advantage—and Eaton is on its way to doing just that. In March, Eaton closed on its acquisition of Boyd Thermal, which provides both power and cooling for AI data centers. That makes the company a system provider, giving it an edge over rivals that provide only components, says Janus Henderson research analyst William Brothers. The deal also gives Eaton 500 more engineers specializing in cooling tech. With expected earnings growth and its recent valuation, shares could fetch about $470 in a year, up 19% from recent levels.

--------------------------------------

2. Modine Manufacturing (MOD / NYSE)

Recent Price: $238.14

Market Value: $12.6 B

Forward P/E: 34.7

52-Week Return: 209.5%

Modine Manufacturing isn’t a household name, but D.A. Davidson’s Matt Summerville calls it a "best in class" data-center play. Modine provides everything that data centers need to cool chips: rear-door heat exchangers, AC units, chillers, coolant distribution units. Overall sales grew 7% in fiscal 2025, driven by 28% growth in its Climate Solutions unit; earnings before interest, taxes, depreciation, and amortization grew 25%. That growth justifies its price/earnings ratio of 32 times over the next 12 months. After divesting its auto-parts business later this year, Modine will be a pure-play cooling company.

--------------------------------------

3. Schneider Electric (SBGSY / OTC)

Recent Price: $62.82

Market Value: $181.3 B

Forward P/E: 28.6

52-Week Return: 36.1%

Like Eaton, Schneider Electric provides both electrical hardware and software for data centers. That is the result of its acquisition of 75% of Motivair in February 2025, which brought expertise in cooling distribution units and direct-to-chip cooling plates in house. The deal has been a tailwind for Schneider. RBC Capital Markets analyst Mark Fielding forecast total sales growth of 9% a year through 2030, up from roughly 6% annually over the past three years. He rates shares Buy and has a $68.40 target for the U.S.-listed American depositary receipt, up 10% from recent levels.

--------------------------------------

4. Solstice Advanced Materials (SOLS / Nasdaq)

Recent Price: $79.24

Market Value: $12.6 B

Forward P/E: 29.7

52-Week Return: 62.7%*

Solstice Advanced Materials, which makes chemicals used in chip making, uranium hexafluoride for nuclear power, and refrigerants and coolants, was spun out of Honeywell International in October 2025. It serves a variety of industries, including data centers. Wall Street wasn’t a huge fan of the stock when it spun out, expecting earnings to grow at just 15% annually. Investors were quicker to realize Solstice’s potential. Shares are up 65% year to date, and analysts have come around, too—they now see earnings growing at a 20% clip annually through 2028.

--------------------------------------

5. Trane Technologies (TT / NYSE)

Recent Price: $462.56

Market Value: $102.4 B

Forward P/E: 31.3

52-Week Return: 35.7%

Heat is one problem. But data centers also need to manage and cool water. That’s Trane Technologies’ business. It builds coolant distribution units and air handlers, and invested in immersion cooling by buying LiquidStack in March. Wall Street expects sales and earnings to grow by 8% and 13% a year on average, respectively, for the next three years. Above-average earnings is why shares trade for 31 times estimated earnings over the next 12 months. Next-generation cooling could push profits higher. Bookings in Trane’s Applied Solutions, which serves data centers, grew 120% in the fourth quarter.

--------------------------------------

6. Vertiv Holdings (VRT / NYSE)

Recent Price: $301.16

Market Value: $115.2 B

Forward P/E: 49.1

52-Week Return: 314.7%

Vertiv Holdings didn’t need to make acquisitions to merge power and cooling technologies—it already had. The stock returned 70% annualized over the past five years, but there’s no reason it can’t keep rising. Shares jumped 25% on Feb. 11 after fourth-quarter numbers, which showed that orders had grown 252% year over year. Earnings estimates for 2026, now at $6 per share, rose 40% over that span. The stock trades at 46 times expected earnings over the next 12 months, but profits should grow by 34% annually over the next three years. And Wall Street tends to underestimate Vertiv’s earnings.

Sources: Bloomberg.

Disc: No buy and sell. This information only for education purpose only.

3

24

2,386

Mar 16

With the introduction of the $INV @AccelsiusATX NeuCool IR150 I ask my LLM what other products they could introduce with their technology:

1. Two-Phase Immersion Cooling Tanks

While Accelsius currently focuses on "Direct-to-Chip" (where fluid only touches the cold plate), the market is shifting toward Full Immersion.

The Opportunity: For "extreme density" scenarios where even the motherboard components (VRMs, memory, networking chips) generate significant heat, full immersion is the only solution.

The Fit: Accelsius already has the specialized dielectric refrigerant and the two-phase CDU technology. Introducing a NeuCool Immersion Tank would allow them to compete with companies like GRC and LiquidStack, offering a "zero-water" alternative for military, edge, and sovereign AI clouds.

2. "Ruggedized" Edge AI Micro-Data Centers

As AI moves to the "Edge" (factories, oil rigs, cell towers), there is a massive need for high-performance compute in environments with no water and no HVAC.

The Opportunity: A self-contained, fan-less 2-phase micro-rack (5kW–20kW) that is completely sealed from the outside environment.

The Fit: Accelsius’s technology is uniquely suited for this because it doesn't require a constant supply of facility water and can reject heat to the ambient air much more efficiently than standard air-cooled edge units.

3. Co-Packaged Optics (CPO) Precision Cold Plates

With NVIDIA’s $4B investment in photonics (lasers), the industry now has a "thermal stability" problem. Lasers fail if their temperature drifts by even a few degrees.

The Opportunity: Ultra-thin, high-precision cold plates specifically designed for "optical engines" and CPO-enabled chips.

The Fit: Two-phase cooling is inherently "isothermal" (it stays at exactly the same temperature across the entire surface). Accelsius could create a specialized line of NeuCool-Optics cold plates that provide the sub-degree temperature stability required by next-gen laser-powered chips.

4. AI-Driven "Smart" CDUs (Cooling-as-a-Service)

The market is demanding more than just hardware; they want automated thermal management.

The Opportunity: A software-defined CDU that uses AI to predictively adjust boiling pressures based on incoming AI workloads (e.g., ramping up cooling before a large LLM training run hits the chip).

The Fit: By integrating sensors more deeply into the "NeuCool" stack, Accelsius could offer a SaaS layer that optimizes Power Usage Effectiveness (PUE) in real-time, essentially "cooling AI with AI."

5. Waste Heat Recovery Modules

In 2026, sustainability is a core KPI for hyperscalers.

The Opportunity: A specialized Heat-Exchanger Module that captures the high-grade heat (60∘C ) coming off the two-phase return line and converts it for district heating or industrial use.

The Fit: Because two-phase systems return heat at much higher temperatures than water-based systems (60∘C vs. 35∘C), the heat is "higher grade" and more valuable. This would allow Accelsius to market their system not just as a cost-saver, but as a revenue-generator for data center owners.

1

5

403