Jun 10

On the side note, why did AMD place NB outside of CPU package? overclocking NB gave noticeable bump. And being on MB, without active cooling, this shit was frying itself even under slightest OC.

ha, and placing NB chip with CPU would make it multichip SoC long before Zen.

218

Jun 2

เหย มานั่งนึก move นี้ของ Jensen Huang มันไม่ธรรมดา RTX Spark ที่มาทำ SoC มัดรวม CPU GPU ทำ Unified Memory นี่บี้ Intel กับ AMD ในระดับ consumer ในช่วง RAM ราคาแพง

เพราะ Nvidia รับจบใน chip เดียวไม่ง้อ Intel ไม่พอนะ

แต่ถ้ามองในแง่ multichip นำไปใช้กับ datacenter นี่รับจบอย่างโหด

3

10

28

2,969

May 27

NEUROMORPHIC GRID ARCHITECTURE

Event-Driven Processing

Unlike traditional computing, the neuromorphic grid operates on asynchronous spikes. This aligns perfectly with biological neurons, which only "fire" when stimulated, consuming minimal energy during idle states.

arxiv.org/html/2504.15371v3

Solid Oxide Fuel Cell (SOFC) Synapses

Recent breakthroughs feature the use of Solid Oxide Fuel Cells (SOFCs) to serve dual purposes. They function as both energy-conversion devices (powering the system via electrochemical reactions) and in-cell neuromorphic processing units that mimic synaptic weights.

cell.com/cell-reports-physic…

Neurogrid: A

Mixed-Analog-Digital Multichip

System for Large-Scale

Neural Simulations

Designed to emulate the human brain, it uses analog circuits to simulate ion channel activity and digital communication to route signals. It can simulate one million neurons and 6 billion synapses in real time while consuming just a few watts of power.

web.stanford.edu/group/brain…

The silicon neuron circuit consists of elements to model the soma, dendrite, shared synapse populations, and ion channel populations. Sharing synapse and dendrite circuits between neighboring neurons enables high connectivity while minimizing chip area. Secondary branching of axons is achieved through spatial signal decay in the shared dendrite circuit.

The system utilizes a multicast packet-switched routing protocol for low latency spike communication. Primary axon branching between arbitrary locations in different chips is supported through a separate FPGA-based daughterboard.

open-neuromorphic.org/neurom…

NeuroGrid

NeuroGrid, a decentralized neuromorphic AI framework leveraging spiking neural networks (SNNs) on edge devices to optimize energy distribution dynamically. Processing IoT sensor data in milliseconds, NeuroGrid ensures grid stability and scalability.

Evaluated on a novel UrbanGrid-2025 dataset with 75,000 energy consumption profiles from five global cities, the framework reduces peak load by 42% and latency by 58% compared to centralized AI models. With a modular architecture, it supports green, resilient urban energy systems, paving the way for sustainable smart cities.(digital prisons)

techrxiv.org/doi/10.36227/te…

NeuroGrid: AI based microgrid energy management system

youtu.be/NbxN9W-wmq0?si=alz9…

1

7

8

206

May 23

Anthropic is considering Microsoft’s Maia AI chips as it expands a multichip strategy designed to reduce reliance on Nvidia.

Full story: thein.fo/4nFtGBU

1

2

19

3,655

Apr 9

Buen capítulo por escuchar otros puntos de vista.

Solo añadir una cosa que creo que es importante.

Se habla mucho de la concentración del mercado. Las grandes tecnológicas pesan un 33% en el S&P 500.

Y sí, es mucho. Pero hay que mirar el otro lado de la balanza.

Estas empresas contribuyen más del 50% del crecimiento de beneficios del índice. Sus márgenes netos son del 25-26%, casi el doble que la media del S&P 500. Y si hablamos de beneficio económico real el que genera valor por encima del coste de capital las 10 mayores empresas del índice generan cerca del 70%.

No es concentración sin sentido. Es que son las mejores empresas del mundo por fundamentales.

¿Y valoraciones? Hoy, en plena corrección de algunas de las magníficas cotizan hasta por debajo de la media del índice.

Esto no es una burbuja. En la burbuja de las puntocom había empresas sin beneficios cotizando a múltiplos de ciencia ficción. Aquí tenemos empresas con beneficios récord, márgenes brutales y crecimiento esperado del 18% para 2026, cotizando por debajo de sus medias históricas.

Y hay algo más que mucha gente no está viendo.

Vamos a un mundo multinube, multichip y multi-IA. No va a haber un solo ganador. Las empresas usan AWS, Azure y Google Cloud a la vez. Los chips no son solo Nvidia Amazon tiene Trainium, Google tiene TPUs, Microsoft tiene Maia. Y los modelos de IA no son solo uno las empresas usan Claude, GPT, Llama, Gemini según la tarea.

El mercado es gigantesco y estamos solo en el comienzo. No es winner takes all. Hay sitio para varios ganadores y las grandes están mejor posicionadas que nadie para capturar ese crecimiento.

No estar en estas empresas a estas valoraciones, para mí, es un gran error.

Pero es solo mi opinión.

Un saludo.

1

2

19

2,023

Apr 9

Vamos hacia un mundo donde nadie quiere depender de un solo proveedor en ninguna capa.

Y esto aplica a las tres capas a la vez:

Multinube

Hace unos años las empresas elegían un cloud (AWS, Azure o Google) y metían todo ahí. Ahora las grandes empresas reparten carga entre dos o tres clouds. ¿Por qué? Poder de negociación (si AWS te sube precio, amenazas con mover carga a Azure), resiliencia (si un cloud se cae no muere todo tu negocio), y porque cada cloud es mejor en algo distinto (AWS en infraestructura, Azure en integración con Microsoft, Google en datos y analytics).

Por eso Uber tiene carga en AWS, Google Cloud y Oracle a la vez. Y por eso los tres hyperscalers siguen creciendo todos no es winner takes all.

Multichip

Mismo concepto pero en el hardware. Hasta hace poco era Nvidia o nada. Ahora tienes Trainium de Amazon, TPUs de Google, chips propios de Microsoft (Maia), AMD ganando cuota, y Broadcom haciendo ASICs a medida para empresas como OpenAI.

Las empresas quieren diversificar para no depender de Nvidia, negociar mejor precio, y optimizar costes según el tipo de tarea (entrenar un modelo necesita un chip distinto que hacer inferencia a escala).

Nvidia sigue siendo el líder claro, pero pasa de tener el 95% a tener quizá un 60-70% en unos años. Sigue siendo dominante, pero el pastel total crece tanto que vende más chips que nunca incluso con menos cuota.

Multimodelo de IA

Esto es lo más nuevo. Hace un año muchas empresas iban all-in con un solo modelo (GPT-4 de OpenAI, o Claude de Anthropic). Ahora la tendencia es usar varios modelos según la tarea.

Un modelo grande y caro para razonamiento complejo, uno pequeño y barato para tareas simples, uno especializado para código, otro para análisis de documentos.

El perdedor de este mundo es el que intente ser el proveedor único y cerrado. El ganador es el que ofrezca la mejor plataforma donde convivan múltiples opciones.

$MSFT $AMZN $GOOGL $META $NVDA

4

5

68

5,110

Mar 24

Multichip inference cloud startup Gimlet Labs receives $80M to solve one of AI's biggest bottlenecks - SiliconANGLE. siliconangle.com/2026/03/23/… #AI #Startup

542

Feb 18

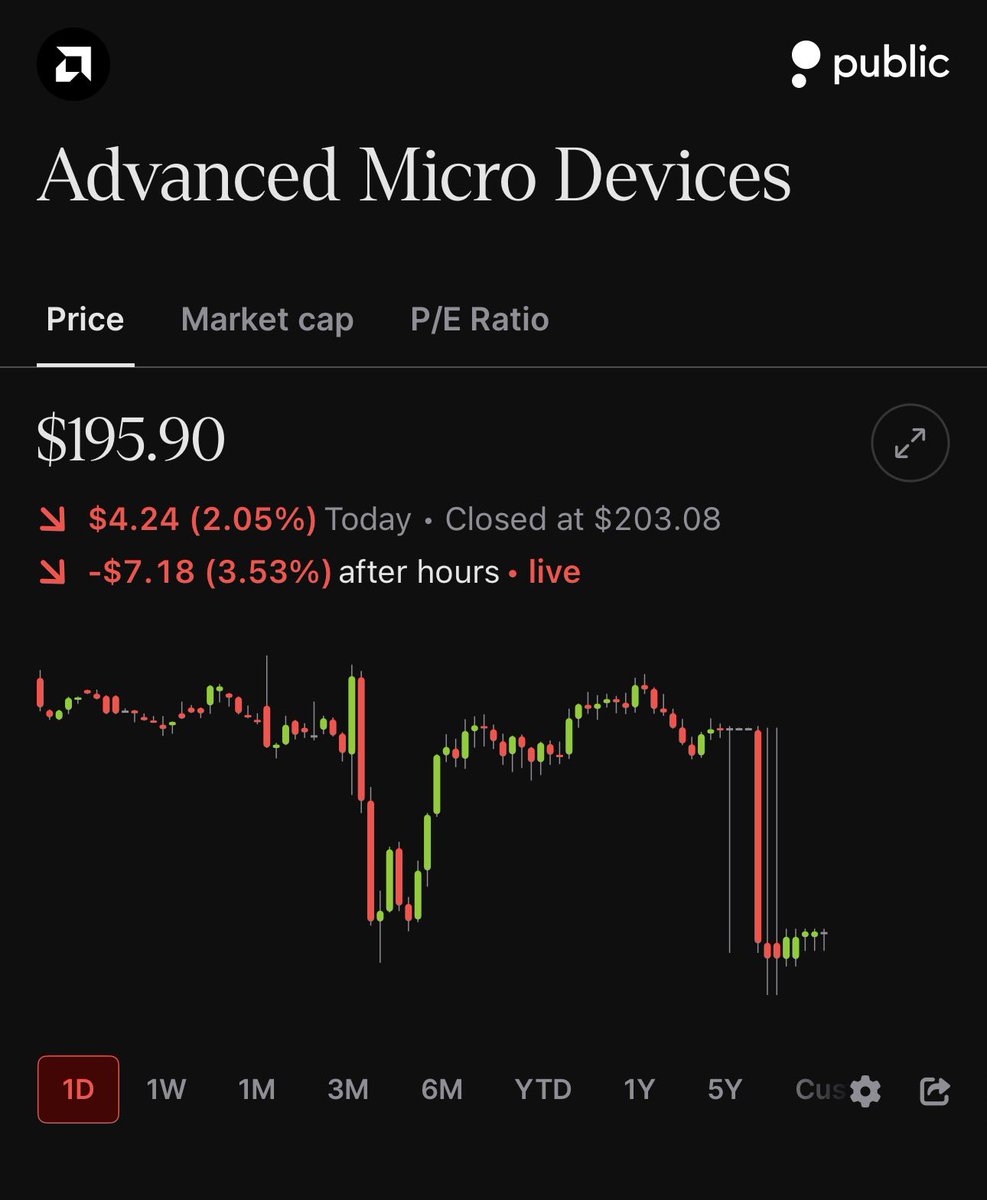

$AMD -4% after $META and $NVDA announce expanded partnership: millions more Blackwell/Rubin GPUs locked in.

NVIDIA wins the compute battle for now. But multi-chip is still the future: MI300X inference, Trainium training, TPU backups.

The real problem? Every hyperscaler stack shift = GPU pricing chaos.

META goes deeper NVDA, AMD exposed.

Next Anthropic model favors MI300, NVDA exposed.

No single vendor owns AI compute forever. But without hedging, you're exposed to every pricing pivot across the stack.

ByteStrike fixes this:

Regulated derivatives tracking real-time pricing for:

• $NVDA H100/H200/B200/T4

• Multi-cloud inference baskets

Hedging tools so operators can:

• Neutralize vendor-specific volatility

• Lock rates across training/inference cycles

• Trade compute as a commodity, not vendor lottery

META’s $NVDA bet is smart today.

ByteStrike makes tomorrow’s pivot survivable.

byte-strike.com

$AMD $NVDA $META $MSFT $GOOGL #AIInfra #GPUs #MultiChip #DataCenters #Derivatives #RiskManagement #ByteStrike

3

136

Jan 15

Supercharge multichip systems with Intel Foundry’s advanced packaging, chiplet integration, and end-to-end test designed to boost performance, maximize yields, and remove stack bottlenecks. ms.spr.ly/6013t7VlP

#IntelFoundry #Semiconductors

3

15

82

3,375

Jan 6

In 2025, D-Wave Quantum Inc. announced a landmark initiative in advanced cryogenic packaging, achieving an industry-first demonstration of scalable, on-chip cryogenic control for gate-model qubits.

Key details of this development include:

Strategic Initiative: Launched in July 2025, the program focuses on advancing multichip packaging and processes to scale both annealing and gate-model quantum processors.

Technological Breakthrough: D-Wave demonstrated end-to-end superconducting interconnects between chips, a critical foundation for building systems that can scale up to 100,000 qubits.

NASA Collaboration: The initiative leverages high-density superconducting bump-bond technology developed at NASA's Jet Propulsion Laboratory (JPL).

On-Chip Control: The "industry-first" refers specifically to the successful demonstration of scalable on-chip cryogenic control for gate-model qubits, a major hurdle in moving beyond current laboratory-scale quantum devices.

Unified Architecture: This packaging technology is designed to support D-Wave's unique position as a developer of both quantum annealing and fluxonium-based gate-model architectures. $QBTS

4

116

Jan 6

☀️ Good morning to $QBTS investors

D-Wave just filed a press release claiming an industry-first: scalable, on-chip cryogenic control for gate-model qubits.

Why it matters:

▫️Cuts wiring needed to control large qubit counts without hurting fidelity (one of the biggest scaling bottlenecks).

▫️They say their annealing “on-chip control multiplexing” tech (used to control “tens of thousands” of qubits/couplers with ~200 bias wires) can translate to gate-model systems.

▫️Built via a multichip package combining a fluxonium qubit chip multilayer control chip, with key components fabricated leveraging NASA JPL/Caltech expertise.

Quantum scaling is turning into an engineering war (wiring, packaging, cryo)… not just a physics problem.

TLDR; D-Wave says it hit an “industry-first” by demonstrating scalable on-chip cryogenic control for gate-model qubits, aiming to slash wiring complexity without hurting fidelity while scaling.

2

2

3

597

Jan 6

D-Wave $QBTS says it hit an “industry-first” by demonstrating scalable on-chip cryogenic control for gate-model qubits, cutting the wiring needed to scale systems while maintaining fidelity.

The setup used multiplexed DACs to control “tens of thousands” of qubits/couplers with ~200 bias wires, and was built as a multichip package with JPL-fabricated components.

5

3

37

7,574

25 Dec 2025

[Blog] Intel enseña su futuro multichip: retícula con escalabilidad 12x, Compute Base Die en 18A-PT, Intel 14A-E, 24 módulos HBM5, EMIB-T y Foveros 3D Direct

blog.elhacker.net/2025/12/in…

2

13

2,563

22 Dec 2025

From cutting-edge interconnects to system-level assembly and test, Intel Foundry delivers the scale and integration needed to power next-generation multichip platforms. ms.spr.ly/6018tow1u

#IntelFoundry #Semiconductors

1

26

119

46,780

10 Dec 2025

Yep! But if you never worked on a PCB, please start from the basic:

-practicing board (more you make better will be)

-Bitaxe gamma/NerdGamma (more you make better will be)

-Than multichip and here you can have a nice choice

2

25

7 Dec 2025

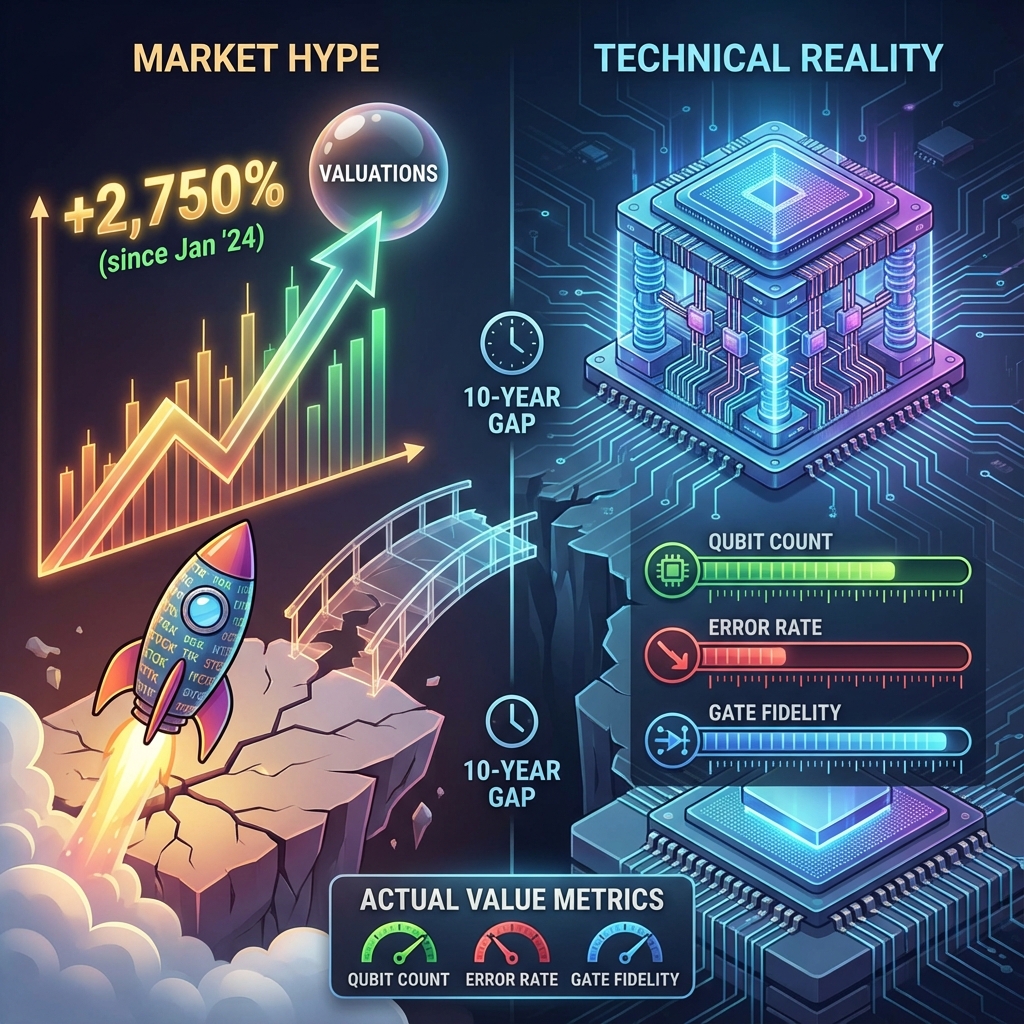

Quantum stocks are having a moment, with some valuations up 2,750% since January 2024. But here is the reality check buried in the hype: we are likely a decade away from fault-tolerant systems at scale.

The technology is genuinely promising. Vertical integration and multichip architectures represent massive engineering advances. However, market enthusiasm is currently sprinting far ahead of the physics.

For those watching this space, the key metrics are not on the stock chart. They are qubit counts, error rates, and gate fidelity. That is where the actual value is being created #QuantumComputing

1

2

50

30 Nov 2025

そういえば、今回nsfのエクスポート時にエラーが出たので、@Rui8bit さんによるfamitrackerの改良版を利用させていただきました。instrumentデータが肥大化しがちなmultichipでは特に便利かも

github.com/Ruikaj/Dn-FamiTra…

1

6

168

29 Nov 2025

Kaynes Technology Q2FY26 Concall Insights :

Kaynes Technology delivered a standout performance in Q2 FY26, with revenue rising 58% YoY to ₹906 crore, while operational EBITDA jumped 80% YoY to ₹148 crore, leading to a strong margin of 16.3% (up by 1.9%).

PAT stood at ₹121 crore, reflecting a healthy 13.4% margin.

The momentum continued through H1 FY26 with revenue of ₹1,580 crore (up 47% YoY), operational EBITDA of ₹261 crore (up 75% YoY), and margins expanding to 16.5%.

Kaynes closed the quarter with an excellent order book of ₹8,099 crore, up 49% YoY, providing strong visibility for upcoming quarters.

Management credited this performance to its evolution from a pure EMS player to a fully integrated ESDM company with strengths across PCB manufacturing, OSAT packaging, embedded design, and system-level manufacturing.

Strategic achievements - including delivering India’s first commercially manufactured multichip module with Alpha & Omega Semiconductor, progress in HDI PCB facilities, and MEMS packaging partnerships - further cement Kaynes' role in India’s semiconductor and electronics ecosystem.

Leadership emphasized creating a globally respected high-tech manufacturing enterprise through execution excellence, automation, and digital integration.

Initiatives such as enterprise-wide process harmonization, Total Predictive Maintenance (TPM), IoT 4.0-based automation, and upgraded quality systems are designed to strengthen scale, reliability, and cost efficiency across verticals like automotive, industrial, defense, and consumer electronics.

On working capital, the management acknowledged the increase in receivables - up roughly ₹600 crore - which contributed to a negative operating cash flow of ~₹180 crore in Q2.

However, they outlined a clear plan to normalize cash flows through aggressive receivable discounting. Around ₹60 crore has already been discounted, and the remaining ₹300 crore of legacy smart meter receivables is expected to be resolved by mid-FY26.

With a major H2 volume ramp - expected to be 50–60% higher than H1 - and liquidity unlocking through discounting, management expressed confidence in delivering strong positive OCF by year-end.

Overall, the management tone remained highly optimistic.

While they avoided specific FY26 revenue or EBITDA guidance, they reiterated strong execution visibility, a solid order book, and sustained 16% EBITDA margins supported by backward integration and operating leverage.

With the OSAT plant scaling, the HDI PCB project progressing, and deep partnerships with global semiconductor and electronics players, Kaynes is strongly positioned to capitalize on India’s 20% PCB CAGR, expanding EV and industrial markets, defense electronics demand, and broader semiconductor ambitions.

DISCLAIMER : This post is purely for educational purposes and is NOT a recommendation in any form.

1

23

1,670