Mar 6

The U.S. is drafting rules requiring government approval before $NVDA and $AMD can ship AI chips globally.

This isn't national security. This is shooting yourself in the foot.

What's Happening:

New export controls would require:

• Government pre-approval for AI chip exports

• Country-by-country review process

• Restrictions beyond just China

$NVDA and $AMD would need permission to sell to customers in allied countries.

Why This Is Insane:

China already responded to U.S. export controls by:

• Building domestic alternatives (Huawei, Cambricon)

• Training DeepSeek V4 on non-NVIDIA chips

• Proving frontier AI doesn't require U.S. silicon

Now the U.S. wants to make it harder for NVDA/NVDA/ NVDA/AMD to sell to everyone else too?

The Strategic Failure:

U.S. semiconductor dominance came from:

• Best technology

• Fastest delivery

• Easiest to buy

New rules kill #3. If customers need 6-month government approvals to buy $NVDA GPUs, they'll source from:

• $GOOGL TPUs (manufactured domestically, no export hassle)

• Domestic alternatives in their own countries

• Chinese chips (if they can access them)

The Market Impact:

Export controls already forced geographic fragmentation:

• U.S. market: $NVDA dominance

• China market: Domestic alternatives

New rules extend fragmentation to allied countries. That creates:

• Parallel compute markets with different hardware

• Pricing divergence across regions

• Competitive advantage for non-U.S. silicon

What ByteStrike Tracks:

Geographic fragmentation = different pricing dynamics per region. We monitor U.S. GPU pricing at byte-strike.com

If export controls push customers to alternatives, transparent pricing across $NVDA, TPU, and regional alternatives becomes critical.

The U.S. built semiconductor dominance. Export bureaucracy risks giving it away.

$MSFT $GOOGL $META

byte-strike.com

Mar 5

The U.S. is drafting rules that would require government approval before AI chips from companies like $NVDA & $AMD can be shipped globally.

The US built the most dominant semiconductor ecosystem in history but now we're telling those companies they need government permission to sell globally.

I call BS because this is not how you win supercycles by making your own companies harder to buy from.

1

94

Mar 5

$AVGO just reported $19.3B Q1 revenue, up 29% YoY. AI semiconductors hit $8.4B, more than double last year.

Guidance: $22B next quarter. Revenue "well over $100B by 2027, almost all from AI products."

This is the picks-and-shovels layer nobody's watching.

The Numbers:

Semiconductor solutions: $12.5B (up 52%) AI chips: $8.4B (more than doubled YoY) 2027E revenue: $100B (almost entirely AI)

$AVGO isn't selling GPUs. They're selling the infrastructure that makes GPUs work:

• Custom ASICs for hyperscalers

• Networking chips for AI clusters

• Interconnect silicon for rack-scale systems

The Customer List:

CEO Hock Tan highlighted "ramps at five hyperscalers plus OpenAI."

Translation:

• $MSFT: Custom silicon for Azure AI

• $GOOGL: Networking for TPU clusters

• $META: ASICs for 6GW AMD deployment

• $AMZN: Trainium interconnect

• Likely $ORCL or another hyperscaler

$AVGO sells to everyone. $NVDA dominates GPUs, but $AVGO dominates everything around them.

Why This Matters:

$100B revenue by 2027 = $AVGO becomes one of the largest semiconductor companies on earth.

All from AI infrastructure. Not consumer chips. Not telecom. Pure data center silicon.

The Financial Layer:

$AVGO growing 50% YoY means hyperscalers are deploying custom silicon at unprecedented scale. That creates:

Diverse hardware platforms (not just $NVDA)

Complex pricing across vendors

Different depreciation curves per platform

Multi-vendor infrastructure = pricing complexity.

ByteStrike tracks this: byte-strike.com

$NVDA gets headlines. $AVGO builds the infrastructure layer. ByteStrike tracks what it costs to use.

Mar 4

$AVGO says it has line of sight to 2027 revenue “significantly above $100B” driven largely by AI silicon like accelerators, switch chips & DSPs.

Custom AI accelerator demand continues to ramp with $GOOGL TPUs strong, Anthropic scaling from ~1GW in 2026 to 3GW in 2027, $META targeting multi-GW deployments & OpenAI expected to deploy its first XPU at 1 GW in 2027.

1

2

152

Mar 1

$NVDA building 6G infrastructure for AI at the edge = moving compute from centralized data centers to distributed cell towers.

Every tower becomes an edge compute node with $NVDA silicon.

This creates new pricing dynamics:

• Cloud: Centralized, high-margin, predictable

• Edge: Distributed, lower-margin, volatile

ByteStrike tracks cloud GPU pricing now: byte-strike.com

As 6G scales edge compute, transparent pricing across centralized distributed infrastructure becomes critical.

Different deployment models need different hedging tools.

3

2

241

Feb 23

The $20B consulting business just became a $20/month API call.

But here's what nobody's tracking: Anthropic's compute cost to run this at Fortune 500 scale.

COBOL → Python conversions require massive inference workloads. Every enterprise migration burns thousands of GPU hours on $NVDA, $GOOGL infrastructure.

$IBM lost consulting revenue. Anthropic gained compute-intensive operations. The money shifted from labor to infrastructure and there's zero hedging tools for enterprise-scale inference costs.

ByteStrike tracks real-time GPU pricing across inference workloads: byte-strike.com

The economics didn't disappear. They just moved to the compute layer.

9

6

3,579

Feb 23

$IBM down 10% after Anthropic launches AI tool that converts COBOL to modern languages.

This is not a feature launch. This is a $20B consulting business getting obliterated overnight.

What Just Happened:

$IBM's legacy modernization consulting: Charge enterprises millions to manually migrate COBOL → Java/Python over 12-24 months.

Anthropic's Claude: Upload COBOL. Get Python. 15 minutes. Near-zero cost.

The entire business model just evaporated.

The Brutal Economics:

Fortune 500 companies run billions of lines of COBOL code. Banks, insurance, government, all stuck on 60-year-old infrastructure.

$IBM sold "modernization" as a multi-year, high-margin consulting engagement. Anthropic just made it a $20/month API call.

Why This Matters for AI Compute:

Anthropic didn't build this on their own servers. They're running:

• $NVDA H100/H200 for model training

• $GOOGL TPUs for inference at scale

• $AMZN infrastructure partnerships

Every COBOL → Python conversion burns compute. Anthropic scaling this to Fortune 500 enterprises means billions in inference costs.

The Compute Arbitrage:

$IBM charged $10M for manual code migration. Anthropic charges $100 for automated migration. But Anthropic's compute cost? That's where the economics hide.

ByteStrike tracks this. Inference workloads at enterprise scale create massive operational costs. We monitor real-time GPU pricing at byte-strike.com

$IBM lost a consulting business. Anthropic gained a compute-intensive product. The money didn't disappear, it shifted to infrastructure.

$MSFT $GOOG $META

Feb 23

$IBM down over 10% after Anthropic launches an AI tool that converts old COBOL code to modern languages.

AI code translation directly competes with IBM's legacy modernization consulting.

4

115

Feb 23

$NVDA is quietly executing the most aggressive vertical integration play in tech history.

They're not just dominating data centers. They're taking the entire AI stack:

The Full Stack Takeover:

Training → H100, H200, Blackwell ($50K-$70K per unit)

Inference → Data center GPUs at scale

Edge → Jetson for robotics/IoT

Device → AI PCs with CUDA

$NVDA just re-entered laptops. Not for gaming margins. For CUDA lock-in.

Why This Matters:

Developers learn CUDA on AI PCs → Deploy workloads on $NVDA cloud GPUs → Scale inference on $NVDA data centers → Build edge apps on Jetson

The entire pipeline runs on Nvidia silicon. From your laptop to $MSFT's data centers.

The Economics:

Data center margins: 70% AI PC margins: 20-30%

Nvidia doesn't care about laptop margins. They care about ecosystem lock-in. Every AI PC ships with CUDA means every developer defaults to Nvidia for production workloads.

What Nobody's Watching:

This vertical integration creates pricing power at every layer. Training, inference, edge, device, all $NVDA, all with separate pricing dynamics, all depreciating on different cycles.

Companies building AI products now manage compute risk across 4 deployment tiers with zero hedging tools.

ByteStrike tracks the data center layer where the money flows. Real-time pricing for H100, H200, B200 at byte-strike.com

$NVDA owns the stack. ByteStrike builds the risk layer.

$MSFT $GOOG $META $AMD

Feb 22

$NVDA is re-entering the laptop market this year by pushing CUDA onto AI PCs.

Margins won’t look like data center but Nvidia now spans the full AI stack:

• Training (H100, Blackwell)

• Inference (data center)

• Edge (Jetson)

• Device (AI PCs)

1

3

68

Feb 22

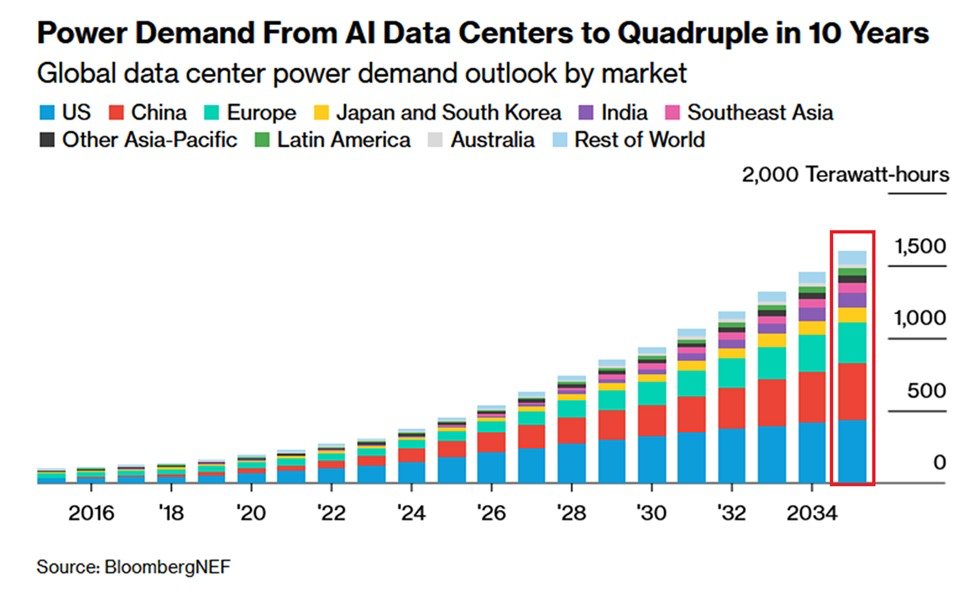

DRAM prices up nearly 10x in a year isn’t just a chip story: it’s an AI infra risk story.

Micron is warning of an “unprecedented” memory shortage lasting beyond 2026, with HBM demand consuming so much fab capacity it’s starving conventional DRAM for PCs and phones.

When $META, $MSFT, $AMZN, $GOOGL are dropping $600B CapEx into AI while $NVDA Blackwell racks are more memory‑hungry than ever, the real problem isn’t just “can we get GPUs?”, it’s “can we predict what any of this will cost six months from now?”

That’s where ByteStrike comes in:

We track live GPU pricing indices (H100, H200, B200, A100, T4) across 72 providers to turn opaque quotes into transparent benchmarks.

We’re building a regulated, cash‑settled futures/perps exchange so infra buyers can hedge AI compute costs instead of eating every price spike.

Hyperscalers, AI labs, and data centers can lock in future compute economics the same way airlines hedge fuel or utilities hedge power.

HBM gets the headlines.

The real story: AI memory GPU volatility is now a financial problem, ByteStrike is building the risk infrastructure to solve it.

byte-strike.com/

Feb 22

DRAM prices are up nearly 10x over the past year which is wild when you look at what's driving it:

• Memory shortages now expected to persist through 2027–2028

• HBM TAM now pegged at ~$100B by 2028 (pulled forward by two years)

• $MU guided Q2 ~30% above consensus & is turning away business due to capacity constraints

• $600B in 2026 $META, $MSFT, $AMZN & $GOOGL CapEx while every $NVDA Blackwell rack inference server is memory-hungry

HBM gets the headlines but the real story is that the entire memory stack is supply-constrained as AI demand overwhelms capacity across the board.

3

68

Feb 22

When Larry Ellison and Elon Musk are literally begging Jensen Huang for more chips, the overvalued $NVDA debate is over.

Forward P/E of 26. 70% revenue growth projected for 2026. And the two most aggressive capital allocators in tech cannot get enough of the product.

$GOOGL TPUs, $AMZN Trainium, $MSFT Maia. Interesting projects. Nobody is begging for them.

But here is what this story is actually about and nobody is connecting it.

When demand is this unhinged and supply is this constrained, you do not just have a hot stock. You have the most violently mispriced commodity market on the planet running without a single financial instrument around it.

H100 spot rates crashed from $8 to under $3 per hour while Ellison was still signing contracts at peak prices. B200 pricing swings week to week with no transparent benchmark anywhere. $ORCL is committing billions to GPU capacity with no way to hedge the cost of doing so. $AMZN is selling reserved compute on multi year terms into a spot market it cannot predict. $MSFT is pricing enterprise AI agreements today against a cost curve that Blackwell is about to completely redraw.

These are not small exposures. These are the largest unhedged commodity positions in corporate history sitting on balance sheets with no futures market, no options market, no forward curves, nothing.

ByteStrike is building what is missing.

Five live indices across the GPU stack, each one a benchmark that has never existed before in a market that has been priced through backroom deals and bilateral contracts since the beginning.

ByteStrike turns that into a real market.

Begging for GPUs is what happens when the most valuable commodity in the world has no functioning price discovery. Capital gets misallocated. Contracts get mispriced. Balance sheets carry risk nobody can quantify.

ByteStrike is the fix that the entire AI economy does not know it is waiting for.

byte-strike.com

$META $AMZN

Feb 22

For anyone saying $NVDA — trading at a forward P/E of 26, with 2026 revenue growth projected at 70% — is overvalued.

And that $GOOGL TPUs, $AZMN Trainium chips, or $MSFT Maia chips can compete and are coming for them…

Just listen to Larry Ellison.

He and Elon are literally begging Jensen for more $NVDA GPUs.

3

110

Feb 22

Michael Burry just asked the question nobody in tech wants to answer.

When does the AI spending end?

$ORCL, $GOOG, $META, $MSFT, $AMZN are burning cash, borrowing like never before, and now using accounting tricks to hide how deep the hole actually is. $635 to $700 billion in 2026 capex. $AMZN free cash flow going negative $28 billion. H100s going obsolete before the depreciation schedule runs halfway.

But Burry is asking the wrong question.

The real question is not when does the spending end. It is why are these companies spending at this scale with zero financial tools to manage the risk of it.

Every GPU fleet on every balance sheet right now is a completely unhedged position. No futures. No options. No forward curves. Just hundreds of billions in silicon with no mechanism to manage what happens when the next generation lands and cuts current fleet value by 40 percent overnight.

In any other asset class this would be unthinkable. ByteStrike is fixing it.

A regulated exchange for AI compute derivatives. Five live indices across the entire GPU stack.

Real price discovery. Real hedging. Real financial infrastructure for the most important commodity in the world right now.

Accounting tricks cannot solve what Burry is seeing. Transparent derivatives markets can.

byte-strike.com

A question I have for $ORCL, $GOOG, $META, $MSFT, $AMZN, $NVDA, $CAT, and all the rest, “When does the spending for AI data center buildout actually end?”

It is consuming all your cash flow, you are borrowing, you are financing in ways you never have, apparently because it is so urgent, because it scales?

But if it scales, when does it end?

Now you are engaging in accounting tricks to hide expense, to protect earnings, as the impact is so severe. You will be tortuously adjusting your earnings in a new and sinister ways.

When does it end?

3

134

Feb 20

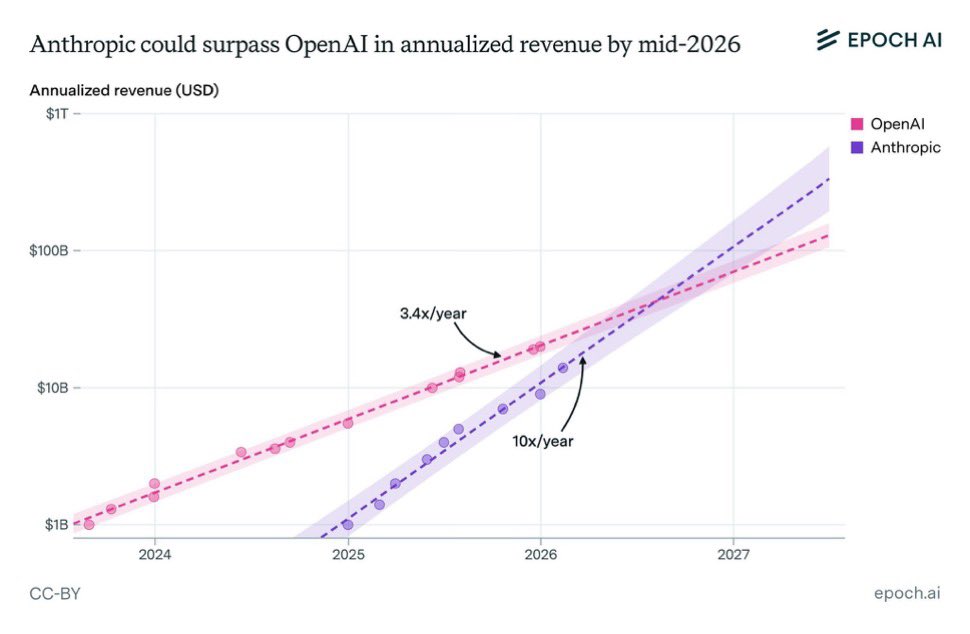

$ANTHROPIC is projected to surpass $OPENAI in revenue later this year.

Not because it has a better chatbot.

But because enterprise AI adoption is scaling faster than consumer AI.

And scaling enterprise AI means one thing:

Compute.

Anthropic already:

• Runs large Claude workloads on $AMZN AWS

• Secures TPU capacity from $GOOGL

• Commits billions in long-term infrastructure

In fact, partnerships with hyperscalers are expected to bring over a gigawatt of AI compute capacity online by 2026.

This isn’t a model race anymore.

It’s a compute procurement race.

Yet today, AI companies still:

– Can’t forward-price GPU capacity

– Can’t hedge compute exposure

– Can’t manage infra volatility

– Depend on opaque hyperscaler contracts

Imagine planning a multi-year AI deployment…

…without knowing what your most critical input will cost next quarter.

At ByteStrike, we’re building the market infrastructure to:

→ Financialize AI Compute

→ Enable price discovery for GPU capacity

→ Introduce forward contracts for compute

→ Unlock liquidity across fragmented global supply

Turning compute from a fixed cost…

…into a tradable digital commodity.

$NVDA builds the chips.

ByteStrike builds the market.

Financializing AI Compute.

byte-strike.com

#AI #Cloud #GPU #ComputeMarkets #DigitalCommodities #EnterpriseAI #AIInfrastructure #Datacenter

$META

Feb 20

NEW IN: Anthropic is projected to surpass OpenAI in revenue later this year.

4

79

Feb 20

ByteStrike now tracks 5 GPU indices with full transparent methodology.

Live Pricing:

• T4 Index: Production inference workloads

• A100 Index: Legacy training capacity

• H100 Index: Current-gen high performance

• H200 Index: Next-gen deployment costs

• B200 Index: Blackwell pricing

Each index aggregates real-time pricing across 72 providers: $MSFT Azure, $GOOG Cloud, $AMZN AWS, plus independent marketplaces and decentralized networks.

Full methodology published for each: byte-strike.com/methodology

The Market We're Building:

AI infrastructure spending hit $600B in 2026. Companies face:

GPU rental rates spiking 15% in weeks

Hardware generations compressing from 5 years to under 3

Memory costs up 246% in 6 months

Zero hedging tools for billions in capex

ByteStrike provides transparent price discovery. Next: regulated perpetual contracts to trade these indices.

How It Works:

Cash-settled futures with USDC

24/7 trading with instant settlement

Long/short positions on GPU pricing

Leverage (1-20x) for capital efficiency

Multi-chain support (Ethereum, Arbitrum, Base, Solana)

Who This Serves:

AI companies → Lock in training/inference costs

Data centers → Hedge GPU rental revenue

Traders → Capitalize on compute volatility

This is what NYMEX did for oil. What ICE did for power. Now compute.

$NVDA sells the hardware. ByteStrike builds the financial layer.

byte-strike.com

#AI #GPUCompute #ByteStrike #Nvidia #FinancialInnovation #Crypto #DeFi #AIInfrastructure #FuturesTrading

3

53

Feb 20

$GOOGL Cloud just grew 48% YoY with a $240B backlog.

And now we know why.

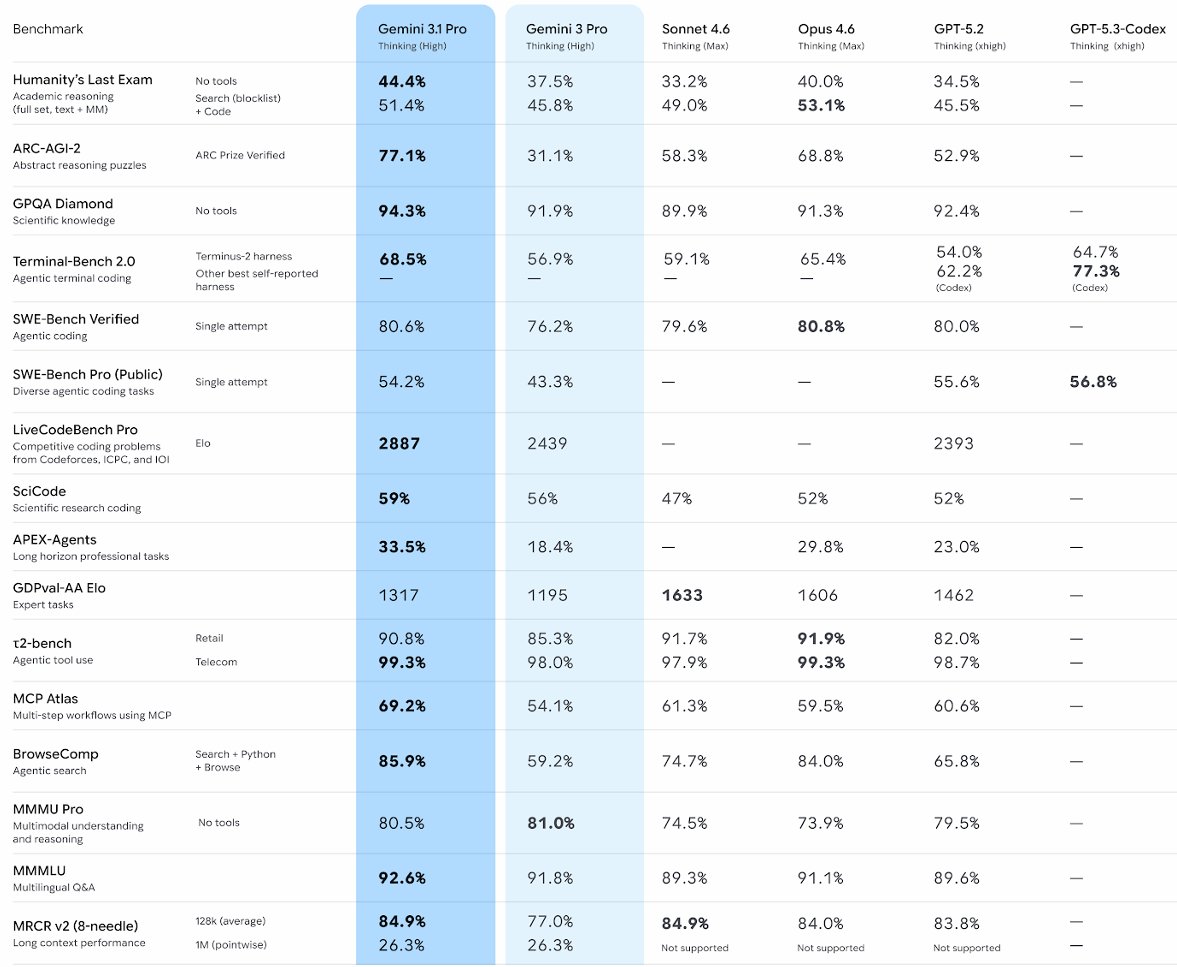

Gemini 3.1 Pro is leading across multiple reasoning, coding, and agentic benchmarks, pushing enterprise AI demand to new highs.

But here’s what most people are missing:

Google’s own CEO has already stated they are operating in a supply constrained environment due to surging compute demand across AI services.

This is no longer a model race.

It’s a compute race.

Every frontier model breakthrough, whether from $GOOGL $MSFT $AMZN or $NVDA, increases:

• GPU demand

• Power requirements

• Data center utilization

• Long-term infrastructure commitments

Yet AI compute, one of the most critical inputs to enterprise AI, is still procured through static cloud contracts with:

– No forward pricing

– Limited supply visibility

– Zero hedging mechanisms

– Vendor-locked ecosystems

Imagine scaling mission-critical AI workloads…

…on infrastructure you can’t reliably price 12 months out.

At ByteStrike, we’re building the market infrastructure to:

→ Financialize AI Compute

→ Enable price discovery for GPU capacity

→ Introduce forward contracts for compute

→ Unlock liquidity across fragmented global supply

Turning compute from a fixed cost…

…into a tradable digital commodity.

The next phase of AI won’t be bottlenecked by models.

It will be bottlenecked by access to compute.

Financializing AI Compute.

byte-strike.com

#AI #Cloud #GPU #ComputeMarkets #DigitalCommodities #AIInfrastructure #EnterpriseAI #Datacenter #NVIDIA

Feb 19

$GOOGL Cloud grew 48% last quarter with a $240B backlog and now we know why.

Gemini 3.1 Pro just took the #1 spot across multiple agentic AI and coding benchmarks.

1

3

127

Feb 19

$OPENAI is reportedly closing in on a ~$100B funding round at an ~$850B valuation.

With backing from $MSFT $AMZN $NVDA and SoftBank, this isn’t venture funding.

It’s infrastructure financing for the AI arms race.

Because scaling frontier models isn’t just about better algorithms anymore.

It’s about who can secure:

• GPU supply

• Power capacity

• Data center access

• Long-term compute availability

And today, AI compute is:

– Scarce

– Regionally fragmented

– Price volatile

– Locked inside hyperscaler ecosystems

Yet enterprises are still procuring one of their most critical AI inputs through static cloud contracts with zero price transparency or hedging mechanisms.

Imagine running a trillion-dollar AI roadmap…

…on infrastructure you can’t forward-price.

At ByteStrike, we’re building the market layer to:

→ Financialize AI Compute

→ Enable price discovery for GPU capacity

→ Introduce forward contracts for compute

→ Unlock liquidity across fragmented global supply

Turning compute from a fixed cost…

…into a tradable digital commodity.

The next phase of AI won’t be bottlenecked by models.

It will be bottlenecked by access to compute.

ByteStrike is building the rails for that future.

Financializing AI Compute.

byte-strike.com

#AI #Cloud #GPU #ComputeMarkets #DigitalCommodities #AIInfrastructure #Datacenter #EnterpriseAI #NVIDIA

Feb 19

OpenAI is finalizing a new ~$100B funding round that would value the company at ~$830B.

For context, $META is ~$1.6T with 3.6B daily users & $200B in revenue while OpenAI is ~$12B ARR with ~800M weekly users and still burning cash.

Make this make sense.

1

3

149

Feb 19

$AMZN ($717B) just passed $WMT ($713B) as the world's largest company by revenue.

This is what happens when you own:

• Cloud (AWS)

• AI infrastructure (Trainium, Bedrock)

• Advertising ($56B)

• Logistics

• Enterprise AI platform

$AMZN controls the full AI stack. They're not just buying $NVDA GPUs, they're building custom silicon to eliminate the dependency.

The Compute Strategy:

AWS Trainium for training

AWS Inferentia for inference

$NVDA for peak performance workloads

Multi-chip approach to avoid monopoly pricing

Companies deploying on AWS face:

• Custom silicon with unknown depreciation curves

• Trainium pricing disconnected from $NVDA market rates

• No liquid hedging markets for AWS-specific capacity

The $717B Revenue Machine:

AWS dominates enterprise cloud. Bedrock powers agentic AI. Advertising funds compute buildout. Logistics scales globally.

But the compute layer underneath? Zero financial infrastructure. No futures. No hedging. No standardized pricing.

ByteStrike changes this. We track real-time GPU pricing for $NVDA H100, H200, B200, A100, T4. Expanding coverage to $AMZN Trainium and $GOOGL TPU market dynamics.

$717B in revenue built on compute infrastructure with no risk management layer.

ByteStrike is building it.

byte-strike.com

$MSFT $GOOG $META $NVDA

#AI #AWS #Amazon #CloudComputing #AIInfrastructure #Trainium #GPUCompute #ByteStrike #FinancialInnovation #Enterprise #DataCenters #TechNews #Semiconductors #AICompute

Feb 19

$AMZN ($717B) just passed $WMT ($713B) as the world's largest company by revenue.

This is what happens when you own cloud (AWS), AI infrastructure (Trainium, Bedrock), advertising ($56B), logistics and the enterprise AI platform companies are building on.

2

3

88

Feb 18

$NVDA Vera Rubin timeline pulled forward by 3-6 months. Evercore says shipments could arrive as early as end-Q2 2026, originally planned for Q4 2026.

China export bans freed up supplier capacity. $NVDA locked in wafers and memory ahead of schedule.

The Hardware Acceleration:

GPU generations are compressing faster than expected:

• H100: Launched 2022

• H200: Shipping now

• B200 Blackwell: Ramping 2026

• Rubin: Now Q2 2026 (previously Q4 2026)

That's 4 major generations in 4 years. Hardware depreciation cycles collapsing from 5 years to under 3.

The Financial Impact:

Companies deploying B200 Blackwell systems in Q1 2026 face accelerated obsolescence. Rubin arriving 6 months early means:

• Faster performance per dollar decline

• Shortened competitive advantage window

• Accelerated hardware depreciation

Hyperscalers getting 80% of Blackwell needs means constrained supply. Wait times: 12-26 weeks. Companies can't get capacity now, and what they do get depreciates faster.

The Volatility Layer:

Meanwhile $AMD promises MI455X for late 2026. Multi-vendor strategies mean tracking depreciation across $NVDA and $AMD hardware cycles with different timelines.

ByteStrike tracks this accelerating complexity. We monitor real-time GPU pricing for H100, H200, B200 at byte-strike.com

Hardware cycles compressing. Supply constrained. Pricing volatile. Companies need financial infrastructure to manage this.

$MSFT $GOOG $META

byte-strike.com

Feb 17

Evercore says $NVDA Vera Rubin timeline has been pulled forward by 3–6 months.

China export bans freed up supplier capacity, opening the door to shipments as early as end-Q2 2026.

3

92

Feb 18

Adani Group plans to invest $100B to build sovereign AI data centers across India by 2035. The investment expects to catalyze an additional $150B in related investments and result in a $250B AI infrastructure ecosystem in India over the decade.

The plan calls for deploying up to 5 gigawatts of data-center capacity in Visakhapatnam, Noida, Hyderabad, and Pune, with partnerships with $GOOG, $MSFT, and Flipkart. The effort builds on AdaniConneX, which has already developed about 2 gigawatts of data-center capacity across India.

India is positioning itself as the sovereign AI hub for Asia. This follows $AMD partnering with Tata Consultancy and signals massive regional compute buildout outside US/EU markets.

The Geographic Shift:

Companies are diversifying infrastructure beyond traditional markets:

• Adani: 5GW in India ($100B)

• $MSFT: Saudi Arabia East region (Q4 2026)

• $NBIS: Missouri 1.2GW, Israel 80MW

Geographic expansion creates pricing complexity. Each region has different:

• GPU availability

• Power costs

• Regulatory requirements

• Local pricing dynamics

ByteStrike tracks this global fragmentation. We monitor real-time GPU pricing across regions and providers at byte-strike.com

As AI infrastructure scales globally, transparent pricing becomes critical.

$NVDA $META $AMZN

byte-strike.com

Feb 17

🇮🇳 LATEST: Adani Group plans to invest $100B to build sovereign AI data centers across India.

1

3

30

Feb 18

$AMD -4% after $META and $NVDA announce expanded partnership: millions more Blackwell/Rubin GPUs locked in.

NVIDIA wins the compute battle for now. But multi-chip is still the future: MI300X inference, Trainium training, TPU backups.

The real problem? Every hyperscaler stack shift = GPU pricing chaos.

META goes deeper NVDA, AMD exposed.

Next Anthropic model favors MI300, NVDA exposed.

No single vendor owns AI compute forever. But without hedging, you're exposed to every pricing pivot across the stack.

ByteStrike fixes this:

Regulated derivatives tracking real-time pricing for:

• $NVDA H100/H200/B200/T4

• Multi-cloud inference baskets

Hedging tools so operators can:

• Neutralize vendor-specific volatility

• Lock rates across training/inference cycles

• Trade compute as a commodity, not vendor lottery

META’s $NVDA bet is smart today.

ByteStrike makes tomorrow’s pivot survivable.

byte-strike.com

$AMD $NVDA $META $MSFT $GOOGL #AIInfra #GPUs #MultiChip #DataCenters #Derivatives #RiskManagement #ByteStrike

3

136

Feb 17

$META x $NVDA: Multi-year deal to deploy millions of Blackwell Rubin GPUs, Grace CPUs, and Spectrum-X networking across Meta’s data centers.

Zuck: Building “leading-edge clusters using Vera Rubin” for personal superintelligence.

This is multi-generational AI infra lock-in, but it’s also multi-generational risk.

Blackwell ramps, Rubin follows, Rubin Ultra after that. Each gen shift means new pricing, new supply dynamics, new volatility for training inference.

ByteStrike solves exactly this for hyperscalers like $META:

Regulated GPU derivatives to:

• Hedge rental pricing across Blackwell/Rubin cycles (before the next announcement moves markets)

• Lock in compute costs for multi-year builds when spot rates swing 15-20% post-model launch

• Trade capacity as a liquid commodity, not scramble for allocations during ramps

Hyperscalers are committing billions to hardware roadmaps years out.

Without a hedging layer, they’re exposed to every GPU pricing pivot, by default.

ByteStrike: Financializing AI compute so $META-scale infra can scale without the volatility tax.

byte-strike.com

$META $NVDA $MSFT $GOOGL $AMZN #AIInfra #Blackwell #Rubin #GPUs #DataCenters #Derivatives #RiskManagement #ByteStrike

Feb 17

$META and $NVDA expand their partnership to deploy Nvidia’s full AI stack across Meta’s hyperscale data centers.

Meta is rolling out millions of Blackwell Rubin GPUs alongside Grace CPUs Spectrum-X networking to scale training and inference across its platforms.

3

99

Feb 17

Global data center power demand is set to 4x over the next decade as AI workloads explode.

$IREN controls gigawatts of low-cost power and has only monetized a fraction of it so far, exactly the kind of “AI power landlord” the market is waking up to.

But here’s the catch:

Owning power and build-to-suit AI campuses is just the first step. The real risk sits in volatile GPU and compute pricing layered on top of that power.

That’s where ByteStrike comes in.

ByteStrike is financializing AI compute with regulated GPU derivatives so infra players like $IREN can:

• Hedge H100/H200/B200 rental price swings that can move 20–25% in weeks

• Lock in future compute pricing before capacity is fully built out

• Offer customers not just power racks, but predictable all‑in compute economics

Tier 3 infra (names like $IREN) is one of the most underappreciated parts of the AI trade, but without a hedging layer for GPU and compute volatility, operators are wearing the full cycle risk on their balance sheets.

ByteStrike exists so the companies that control the power and the racks can also control their exposure to the most volatile input of the AI era: compute.

byte-strike.com

$IREN $NVDA $MSFT $AMZN $GOOGL #AIInfra #DataCenters #Power #GPUs #Derivatives #RiskManagement #ByteStrike

Feb 17

$IREN AI needs power. A lot of it.

Global data center electricity demand is set to quadruple over the next decade. The companies that own the power infrastructure are going to win this cycle.

IREN controls 4.5 GW of power capacity and has only monetized around 10% of it so far. The upside here is enormous.

I believe, this is one of the most underappreciated setups in the entire AI infrastructure trade right now.

4

427

Feb 16

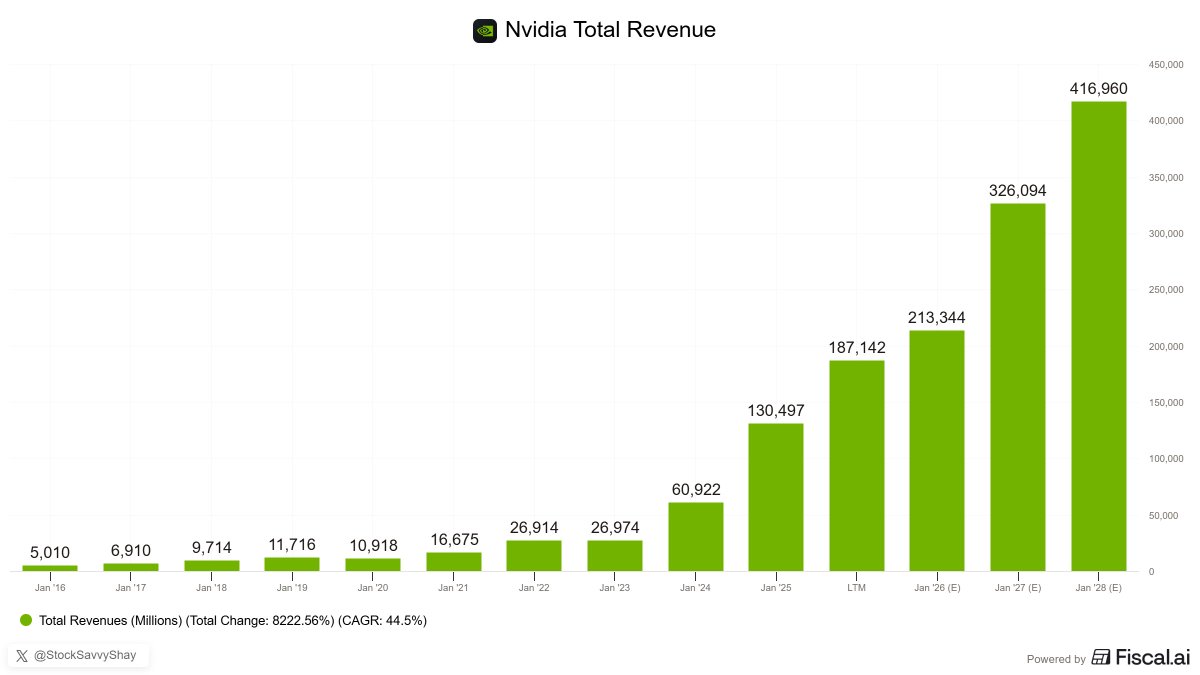

$NVDA could be generating over $1B in revenue per day by 2028.

That's $365B annually. For context:

• 2023: $61B revenue

• 2024: $130B revenue (2.1x growth)

• 2025: $200B revenue (1.5x growth)

• 2026: $270B revenue (1.4x growth)

• 2028: $365B revenue

What This Means:

Every hyperscaler is buying:

• $MSFT: Blackwell, Rubin platforms

• $GOOGL: Complementing TPUs with NVIDIA for workload diversity

• $META: Multi-gigawatt deployments

• $AMZN: AWS capacity expansion

$365B annual revenue means millions of GPUs shipping with 3-year depreciation cycles. Companies are committing tens of billions in procurement with no liquid resale markets.

The Risk Layer:

Companies buying $NVDA GPUs face:

• Hardware depreciation (H100 → H200 → B200 → Rubin)

• Pricing volatility (H100 up 15% in 8 weeks)

• Supply constraints (sold out through 2026)

• No standardized hedging tools

ByteStrike provides the missing financial infrastructure. We track real-time GPU pricing for $NVDA H100, H200, B200, A100, T4. Our regulated perpetual exchange enables hedging across the $365B buildout.

Live pricing at byte-strike.com

$AMD $INTC

byte-strike.com

1

2

48