IQE InP epiwafer-->Tower PH18DA process-->OpenLight Heterogeneous Integration Tech, the chart seems like 1.6t DR8 PIC lol

278

Bill W retweeted

Tower and IQE InP epiwafer deal is for Openlight-enabled tranceivers yes?

(open to someone telling me this guess is wrong)

5

1

73

13,463

May 26

CPO 밸류체인 정리

Jukan이 추천한 CPO에 관한 훌륭한 영상입니다. (얼마전에 유튜브 링크 추천함)

_______________________________________

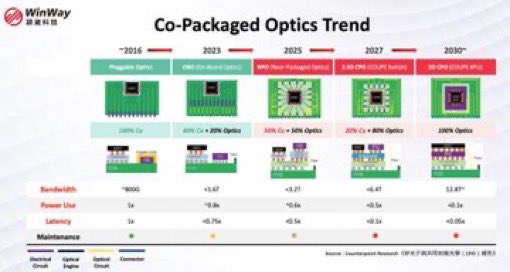

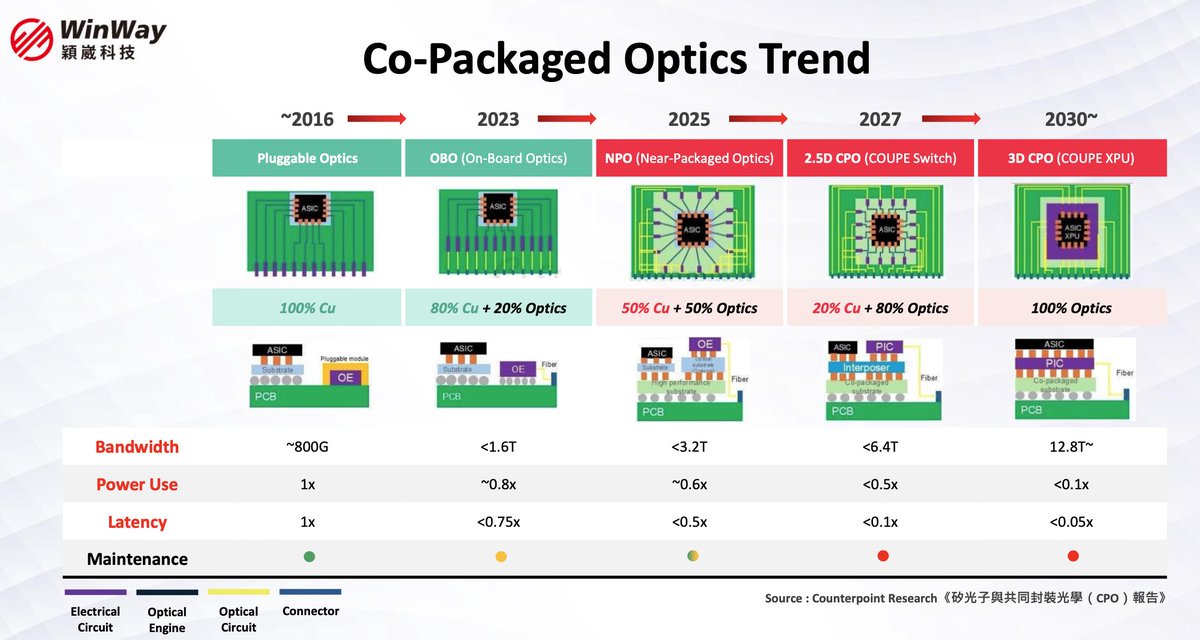

현재 NPO는 여전히 구리 50%, 광학 부품 50%로 구성되어 있습니다. 2.5D CPO가 구리 20%, 광학 부품 80%로 구성되는 2027년이 되어야 진정한 CPO의 확산이 시작될 것으로 보입니다.

2030년에는 3D CPO(COUPE XPU)에서 구리 비율은 0%가 되고 광학 부품 비율은 100%가 될 것입니다.

진정한 난관은 2027년과 2030년 CPO의 유지보수 문제입니다.

플러그형/OBO/NPO(녹색/노란색): 광학 레이저나 엔진이 고장 나면, 현장 기술자가 전면 패널에서 플러그형 모듈을 간편하게 핫스왑하거나, 고가의 ASIC을 폐기하지 않고도 보드상의 NPO 모듈을 교체할 수 있습니다.

2.5D 및 3D CPO (빨간색): PIC와 레이저/광학 부품이 패키지 내부에 물리적으로 결합되거나 ASIC 바로 아래에 적층되면, 더 이상 개별적으로 수리할 수 없습니다. 단일 광학 부품 하나라도 고장 나면, 고가의 컴퓨팅 엔진(XPU/스위치) 전체가 사실상 사용 불가능해집니다.

_______________________________________________________

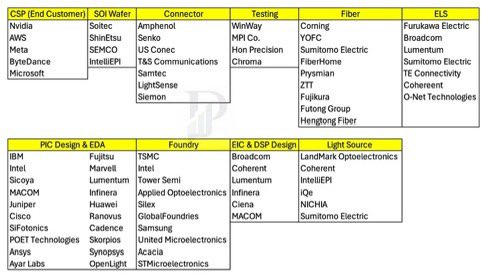

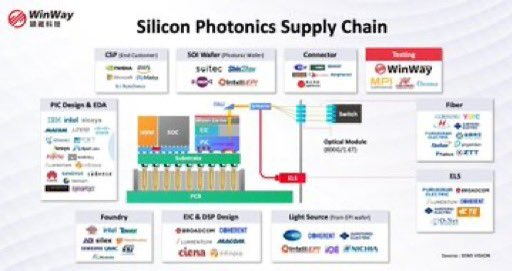

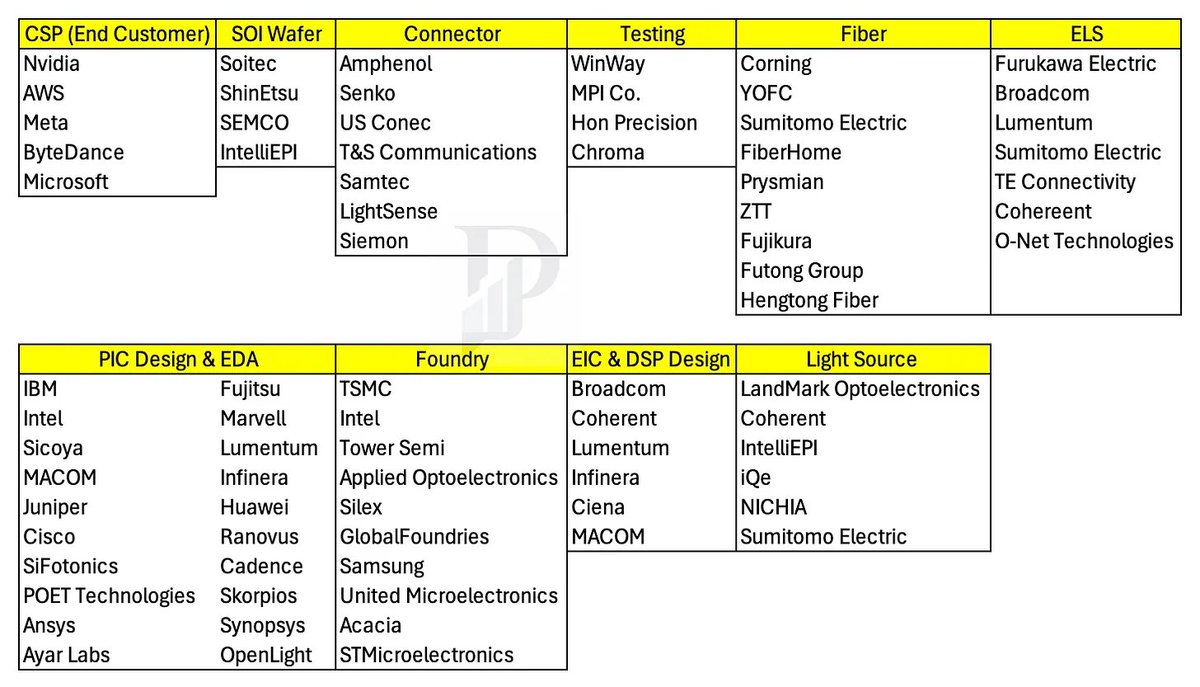

@semivision_tw에 따른 CPO 공급망:

1. CSP

Nvidia $NVDA

AWS $AMZN

Meta $META

ByteDance

Microsoft $MSFT

2. SOI 웨이퍼

Soitec

ShinEtsu

SEMCO

IntelliEPI

3. 커넥터

Amphenol

Senko

US Conec

T&S Communications

Samtec

LightSense

Siemon

4. 테스트

WinWay

MPI Co.

Hon Precision

Chroma

5. 광섬유

코닝 $GLW

YOFC

스미토모 전기

파이버홈

프라이스미안

ZTT

후지쿠라

푸통 그룹

헝통 파이버

6. ELS

후루카와 전기

브로드컴

루멘텀

스미토모 전기

TE 커넥티비티

코히어런트

O-Net Technologies

7. PIC 설계 및 EDA

IBM $IBM

인텔 $INTC

시코야

MACOM $MTSI

주니퍼

시스코 $CSCO

SiFotonics

POET Technologies $POET

Ansys - 시노프시스 산하

Ayar Labs

Fujitsu

Marvell $MRVL

Lumentum $LITE

Infinera

Huawei

Ranovus

Cadence $CDNS

Skorpios

Synopsys $SNPS

OpenLight

8. 파운드리

TSMC $TSM

인텔 $INTC

타워 세미 $TSEM

애플라이드 옵토일렉트로닉스 $AOI

실렉스

글로벌파운드리 $GFS

삼성

유나이티드 마이크로일렉트로닉스 $UMC

아카시아

ST마이크로일렉트로닉스 $STM

9. EIC 및 DSP 설계

브로드컴 $AVGO

코히어런트 $COHR

루멘텀 $LITE

인피네라

시엔나 $CIEN

마콤 $MTSI

10. 광원

랜드마크 옵토일렉트로닉스

코히어런트 $COHR

인텔리EPI

iQe

니치아

스미토모 전기

This is an amazing video recommendation from Jukan about CPO.

_______________________________________________________

NPO is still 50% copper, 50% optics. The real CPO ramp is unlikely to begin until 2027 when 2.5D CPO will have 20% copper and 80% optics.

In 2030, the split will be 100% optics in 3D CPO (COUPE XPU)

The true hurdle is in maintenance for CPO in 2027 and 2030.

Pluggable/OBO/NPO (Green/Yellow): If an optical laser or engine fails, field technicians can easily hot-swap a pluggable module at the faceplate, or replace an NPO module on the board without tossing the expensive ASIC.

2.5D & 3D CPO (Red): Once the PIC and laser/optical components are physically bound inside the package or stacked directly under the ASIC, they can no longer be individually serviced. If a single optical component fails, the entire high-value compute engine (the XPU/Switch) is essentially bricked.

_______________________________________________________

CPO supply chain, per @semivision_tw:

1. CSP

Nvidia $NVDA

AWS $AMZN

Meta $META

ByteDance

Microsoft $MSFT

2. SOI Wafer

Soitec

ShinEtsu

SEMCO

IntelliEPI

3. Connector

Amphenol

Senko

US Conec

T&S Communications

Samtec

LightSense

Siemon

4. Testing

WinWay

MPI Co.

Hon Precision

Chroma

5. Fiber

Corning $GLW

YOFC

Sumitomo Electric

FiberHome

Prysmian

ZTT

Fujikura

Futong Group

Hengtong Fiber

6. ELS

Furukawa Electric

Broadcom

Lumentum

Sumitomo Electric

TE Connectivity

Coherent

O-Net Technologies

7. PIC Design & EDA

IBM $IBM

Intel $INTC

Sicoya

MACOM $MTSI

Juniper

Cisco $CSCO

SiFotonics

POET Technologies $POET

Ansys - part of Synopsys

Ayar Labs

Fujitsu

Marvell $MRVL

Lumentum $LITE

Infinera

Huawei

Ranovus

Cadence $CDNS

Skorpios

Synopsys $SNPS

OpenLight

8. Foundry

TSMC $TSM

Intel $INTC

Tower Semi $TSEM

Applied Optoelectronics $AOI

Silex

GlobalFoundries $GFS

Samsung

United Microelectronics $UMC

Acacia

STMicroelectronics $STM

9. EIC & DSP Design

Broadcom $AVGO

Coherent $COHR

Lumentum $LITE

Infinera

Ciena $CIEN

MACOM $MTSI

10. Light Source

LandMark Optoelectronics

Coherent $COHR

IntelliEPI

iQe

NICHIA

Sumitomo Electric

3

11

34

4,534

This is an amazing video recommendation from Jukan about CPO.

_______________________________________________________

NPO is still 50% copper, 50% optics. The real CPO ramp is unlikely to begin until 2027 when 2.5D CPO will have 20% copper and 80% optics.

In 2030, the split will be 100% optics in 3D CPO (COUPE XPU)

The true hurdle is in maintenance for CPO in 2027 and 2030.

Pluggable/OBO/NPO (Green/Yellow): If an optical laser or engine fails, field technicians can easily hot-swap a pluggable module at the faceplate, or replace an NPO module on the board without tossing the expensive ASIC.

2.5D & 3D CPO (Red): Once the PIC and laser/optical components are physically bound inside the package or stacked directly under the ASIC, they can no longer be individually serviced. If a single optical component fails, the entire high-value compute engine (the XPU/Switch) is essentially bricked.

_______________________________________________________

CPO supply chain, per @semivision_tw:

1. CSP

Nvidia $NVDA

AWS $AMZN

Meta $META

ByteDance

Microsoft $MSFT

2. SOI Wafer

Soitec

ShinEtsu

SEMCO

IntelliEPI

3. Connector

Amphenol

Senko

US Conec

T&S Communications

Samtec

LightSense

Siemon

4. Testing

WinWay

MPI Co.

Hon Precision

Chroma

5. Fiber

Corning $GLW

YOFC

Sumitomo Electric

FiberHome

Prysmian

ZTT

Fujikura

Futong Group

Hengtong Fiber

6. ELS

Furukawa Electric

Broadcom

Lumentum

Sumitomo Electric

TE Connectivity

Coherent

O-Net Technologies

7. PIC Design & EDA

IBM $IBM

Intel $INTC

Sicoya

MACOM $MTSI

Juniper

Cisco $CSCO

SiFotonics

POET Technologies $POET

Ansys - part of Synopsys

Ayar Labs

Fujitsu

Marvell $MRVL

Lumentum $LITE

Infinera

Huawei

Ranovus

Cadence $CDNS

Skorpios

Synopsys $SNPS

OpenLight

8. Foundry

TSMC $TSM

Intel $INTC

Tower Semi $TSEM

Applied Optoelectronics $AOI

Silex

GlobalFoundries $GFS

Samsung

United Microelectronics $UMC

Acacia

STMicroelectronics $STM

9. EIC & DSP Design

Broadcom $AVGO

Coherent $COHR

Lumentum $LITE

Infinera

Ciena $CIEN

MACOM $MTSI

10. Light Source

LandMark Optoelectronics

Coherent $COHR

IntelliEPI

iQe

NICHIA

Sumitomo Electric

I wasn’t planning to share this, but it’s such a high-quality explanation of CPO that I have to.

Just watch it. You’ll regret it if you don’t.

youtu.be/wiH6d4m9o4o?si=hwEO…

1

48

230

42,653

May 20

1/ @QuantinuumQC 🇺🇸 · $839M · trapped-ion

2/ @QueraComputing 🇺🇸 · $230M · neutral-atom

3/ @MultiverseCompu 🇪🇸 · $219M · quantum software

4/ QuantWare 🇳🇱 · $178M · QPU hardware

5/ @QuantumQM 🇮🇱 · $170M · control hardware

6/ Quantum Motion 🇬🇧 · $164M · silicon qubits

7/ @sygaldry_tech 🇺🇸 · $105M · quantum hardware

8/ @Alice__Bob 🇫🇷 · $104M · cat qubits

9/ Quantum Art 🇮🇱 · $100M · trapped-ion

10/ SpinQ 🇨🇳 · $87M · full-stack systems

11/ Q.ANT 🇩🇪 · $72M · photonic chips

12/ @NuQuantumLtd 🇬🇧 · $71M · quantum networking

13/ eleQtron 🇩🇪 · $67M · trapped-ion

14/ OpenLight 🇺🇸 · $50M · silicon photonics

15/ @PhasecraftLtd 🇬🇧 · $34M · quantum algorithms

16/ Matrix Opto 🇨🇳 · $29M · photonic hardware

17/ @QuamCore 🇮🇱 · $26M · single-chip QPU

18/ Qedma 🇮🇱 · $26M · error mitigation

19/ @sparrow_quantum 🇩🇰 · $24M · single-photon sources

20/ Project Eleven 🇺🇸 · $20M · quantum-resistant crypto

21/ Quantum Brilliance 🇦🇺 · $20M · diamond qubits

22/ Orange Quantum 🇳🇱 · $18M · QPU testing

23/ QuiX 🇳🇱 · $18M · photonic processors

24/ @Quobly_ 🇫🇷 · $17M · silicon spin qubits

25/ Kiutra 🇩🇪 · $15M · cryogenic cooling

26/ Diraq 🇦🇺 · $15M · silicon spin qubits

27/ Liangyi Wanxiang 🇨🇳 · $15M · quantum software

28/ Taiyi Quantum 🇨🇳 · $15M · quantum computing

29/ MiQro Era 🇨🇳 · $14M · superconducting

30/ Nanofiber Quantum 🇯🇵 · $14M · neutral-atom

31/ TuringQ 🇨🇳 · $14M · photonic chips

32/ memQ 🇺🇸 · $10M · quantum networking

33/ Qunnect 🇺🇸 · $10M · quantum networking

2

1

2

458

May 15

Is anyone else getting like that podcast from the nuns (called openlight media) on their tiktok fyp like why are they so fun to listen to djddjdj

2

3

177

May 13

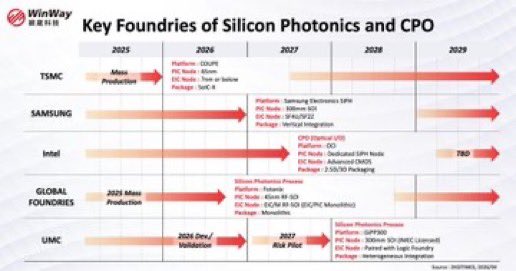

$TSEM KEY READ-THROUGHS FROM TOWER SEMICONDUCTOR Q1 2026 EARNINGS CALL

Tower Semiconductor’s Q1 2026 call was a high-signal event for AI optical infrastructure, specialty foundry competition, data center power delivery, RF front-end cyclicality, and Japan-based semiconductor capacity. The most important market implication is that AI optical interconnect demand is moving from forecast-driven optimism to cash-backed capacity reservation. Tower disclosed $1.3 billion of contractual 2027 silicon photonics revenue commitments, larger 2028 commitments, and approximately $290 million of prepayments from its largest SiPho customers. Management also stated that the $1.3 billion commitment is below both customer full demand and Tower’s internal 2027 SiPho forecast. The call therefore supports a positive read-through for AI optical component suppliers and next-generation networking architectures, while creating negative competitive read-throughs for alternative silicon photonics foundries and any company whose AI optical thesis depends on Tower losing share during the transition from pluggables to XPO, NPO, and CPO. The second-order read-through is that Tower’s demand bottleneck is shifting from customer interest to qualified capacity, materials supply, and architecture relevance.

AI OPTICAL TRANSCEIVERS AND SILICON PHOTONICS

COHERENT VALIDATION IN 400G/LANE SILICON PHOTONICS IS A DIRECT POSITIVE FOR HIGH-SPEED AI OPTICAL TRANSCEIVERS (READ-THROUGH 1)

Affected company: Coherent Corp. (COHR: US)

Directional impact and magnitude: Positive. High magnitude for near-term trading sentiment and medium-to-high magnitude for longer-duration fundamentals.

Supporting commentary: Tower stated that it “announced the demonstration of an all silicon 400 gigabit per lane” modulator with Coherent and described Coherent as “one of our customers having signed a high volume long-term contract.” In Q&A, management clarified that the specific 400G modulator was “off of a Coherent design,” that “this specific modulator performance was because of Coherent’s design tied to our platform,” and that the design was Coherent IP.

Transmission mechanism: The read-through to Coherent is direct because Tower identified Coherent as both a named technology partner and a high-volume long-term customer. The demonstration validates Coherent’s ability to design 400G/lane silicon photonics devices on a merchant foundry platform capable of scaling into volume. That matters because AI data center optical roadmaps increasingly require higher lane rates, lower power per bit, and more compact modulation schemes. Coherent’s design IP being specifically credited by Tower strengthens the read-through: the performance milestone is not merely Tower platform validation; it also validates Coherent’s internal silicon photonics design capability.

Near-term trading catalyst: The named association with Tower’s AI SiPho capacity commitments should support investor confidence in Coherent’s high-speed transceiver roadmap. The call does not disclose how much of Tower’s $1.3 billion 2027 commitment is attributable to Coherent, so the revenue uplift cannot be quantified from the material. The trading relevance is nonetheless high because Coherent is explicitly tied to a high-volume contract and a 400G/lane demonstration at a time when AI optics execution is a core investor debate.

Longer-duration fundamental shift: If Coherent’s 400G/lane design scales through Tower’s platform, Coherent gains a stronger position in next-generation 1.6T and higher-speed optical modules, with potential benefits to mix, share, and margin. The limiting factors are Tower capacity timing, the pace of 400G/lane adoption, and the evolution of competing modulation technologies such as thin-film lithium niobate and indium phosphide.

ARISTA’S XPO STRATEGY RECEIVES A POSITIVE SUPPLY-CHAIN AND ARCHITECTURE VALIDATION (READ-THROUGH 2)

Affected company: Arista Networks, Inc. (ANET: US)

Directional impact and magnitude: Positive. Moderate-to-high magnitude as a strategic validation, moderate magnitude as a near-term earnings catalyst.

Supporting commentary: Tower described “extra dense pluggable optics, XPO, being led by Arista” and said Tower silicon photonics was displayed in “leading XPO and Near Package Optics demonstrations.” Management also stated that pluggables are “not going away at all,” that pluggables should remain “extremely strong, at least through the 2030,” and that XPO and NPO form factors should transition with Tower “maintaining leadership.”

Transmission mechanism: Arista is the clearest public networking company explicitly linked to the XPO architecture in the call. Tower’s commentary supports Arista’s strategic premise that pluggable and extra-dense pluggable optical formats can extend meaningfully before CPO becomes dominant. That is important for Arista because its AI networking roadmap depends on practical, scalable, power-efficient optical interconnect rather than a premature wholesale architectural shift into CPO. Tower’s view that XPO and NPO can coexist with pluggables reduces the risk that Arista’s architecture becomes stranded by a faster-than-expected CPO transition.

Near-term trading catalyst: The call provides positive ecosystem validation for Arista’s AI networking narrative, but it does not disclose Arista revenue, order volumes, or a direct commercial relationship beyond Tower’s statement that XPO is being led by Arista. The near-term impact is therefore sentiment- and narrative-driven rather than estimate-driven.

Longer-duration fundamental shift: The more durable implication is that Arista’s XPO strategy may extend the life and economic relevance of pluggable-adjacent architectures into the next several years. If Tower’s capacity ramp enables higher-density optical supply at scale, Arista’s switch platforms could benefit from more practical AI cluster scaling, lower optical bottleneck risk, and improved confidence in next-generation port-density roadmaps.

NVIDIA GETS A POSITIVE ECOSYSTEM OPTIONALITY READ-THROUGH, BUT THE CALL ALSO HIGHLIGHTS DEPENDENCE ON EXTERNAL PHOTONICS INNOVATION (READ-THROUGH 3)

Affected company: NVIDIA Corporation (NVDA: US)

Directional impact and magnitude: Positive, with caveats. Moderate magnitude as a long-duration ecosystem read-through; low magnitude as a near-term trading catalyst.

Supporting commentary: In Q&A, an analyst referenced Tower’s “recent relationship with NVIDIA at 1.6T” and asked about NVIDIA historically using TSMC while “also partnering with” Tower. Tower declined to discuss specific customer programs beyond the prior public NVIDIA release, but stated that NVIDIA “talked about us as a development partner.” Management also argued that Tower could add value in CPO by becoming the reference design for major integrators.

Transmission mechanism: The read-through to NVIDIA is not a disclosed revenue event. It is an ecosystem risk-reduction signal. NVIDIA’s accelerator roadmap increasingly depends on networking bandwidth, optical interconnect scale, and power-efficient connectivity. Tower’s comments indicate that NVIDIA is at least publicly aligned with Tower as a development partner in high-speed optical connectivity. That broadens NVIDIA’s supplier and technology optionality beyond fully integrated TSMC-centric paths and may help de-risk future optical architectures where photonic integrated circuits become a critical subsystem.

Near-term trading catalyst: Limited. Tower provided no NVIDIA-specific revenue, timing, product program, or volume commitment. The near-term implication is qualitative: NVIDIA’s optical ecosystem continues to broaden, and Tower’s SiPho platform is relevant enough to be discussed alongside NVIDIA’s 1.6T roadmap.

Longer-duration fundamental shift: The longer-term implication is more important. If NVIDIA’s AI systems increasingly require optical I/O, NPO, or CPO, validated external PIC suppliers could become strategically important to NVIDIA’s ability to scale bandwidth without unacceptable power or packaging constraints. The caveat is that Tower acknowledged TSMC’s unmatched position in “extreme deep digital content,” which means NVIDIA may still rely heavily on TSMC-led integration for full-system packaging.

SILICON PHOTONICS FOUNDRY COMPETITION AND CPO ARCHITECTURE

GLOBALFOUNDRIES FACES A NEGATIVE READ-THROUGH TO ITS SILICON PHOTONICS OPTIONALITY (READ-THROUGH 4)

Affected company: GlobalFoundries Inc. (GFS: US)

Directional impact and magnitude: Negative. Moderate magnitude for AI silicon photonics narrative; low-to-moderate magnitude for total company fundamentals given broader foundry diversification.

Supporting commentary: When asked about GlobalFoundries ramping scale and TSMC ramping CPO platforms, Tower stated: “I’m not going to give a percentage market share at present but I think that we’re certainly the leading market share and by far the leading market share in silicon photonics presently and I see no reason why that should change.” Tower also disclosed $1.3 billion of contractual 2027 SiPho commitments, larger 2028 commitments, approximately $290 million of customer prepayments, and more than 50 active SiPho customers.

Transmission mechanism: The negative read-through is that large SiPho customers appear to be reserving Tower capacity with cash-backed commitments, which can reduce the near-term addressable share available to alternative merchant foundries. Silicon photonics foundry relationships are process-specific, design-intensive, and qualification-heavy. Once customers commit design IP, prepayments, and multi-year roadmaps to a foundry platform, share shifts become slower and more expensive. Tower’s $1.3 billion commitment therefore represents more than demand visibility; it implies customer lock-in and process-roadmap alignment.

Near-term trading catalyst: Negative for GlobalFoundries’ AI photonics optionality if investors had expected GF to take rapid share in merchant SiPho during 2026–2028. Tower’s claim of “by far” leading share is management commentary rather than disclosed third-party market-share data, but the prepayments and contracts provide hard supporting evidence of Tower customer traction.

Longer-duration fundamental shift: The longer-term risk for GlobalFoundries is that Tower’s early leadership in pluggables transitions into XPO and NPO before GF achieves comparable scale. The offset is that total SiPho port growth appears large enough for more than one winner. This is not a negative read-through to GF’s entire foundry franchise; it is specifically negative to the probability that GF becomes the dominant merchant SiPho beneficiary over the next 2–3 years.

TSMC’S CPO STRATEGIC POSITION IS REINFORCED, BUT THE CALL ARGUES AGAINST A SIMPLE WINNER-TAKE-ALL OUTCOME (READ-THROUGH 5)

Affected company: Taiwan Semiconductor Manufacturing Company Limited (2330: Taiwan)

Directional impact and magnitude: Mixed-to-positive. Moderate magnitude as a long-duration strategic read-through; low magnitude as a near-term earnings catalyst.

Supporting commentary: Tower’s CEO stated that “TSMC as a one-stop shop” has an advantage and that “there’s nobody that can compete with TSMC with what they’re doing on the extreme deep digital content.” However, he also argued that Tower could still add value in CPO through superior photonic integrated circuits and modulators, stating that “there’s no reason that TSMC wouldn’t be buying our PIC” if Tower’s PIC were superior and became the reference design for major integrators.

Transmission mechanism: The positive read-through to TSMC is that CPO increasingly rewards deep CMOS, advanced packaging, and system-level integration, all areas where Tower explicitly acknowledged TSMC’s structural advantage. If CPO adoption accelerates materially, the value pool could tilt toward TSMC’s integrated logic-packaging ecosystem. That supports TSMC’s strategic relevance in AI networking and optical I/O, beyond GPUs and accelerators.

Near-term trading catalyst: Limited. Tower’s call does not indicate that TSMC won or lost specific business. The trading implication is mainly narrative: TSMC remains the most credible integrated CPO platform owner as architectures move closer to advanced digital content.

Longer-duration fundamental shift: The call also cautions against assuming TSMC captures the entire photonics value stack. Tower’s argument is that best-in-class PICs and modulators may still be sourced externally if integrators standardize on Tower reference designs. The read-through is therefore mixed: CPO is structurally favorable to TSMC, but differentiated photonics components may remain merchant-sourced rather than fully internalized.

TOWER’S COMMENTS UNDERCUT A BROAD MATURE-NODE FOUNDRY PRICING BULL CASE AND SUPPORT A DIFFERENTIATED-PLATFORM PRICING FRAMEWORK (READ-THROUGH 6)

Affected companies: GlobalFoundries Inc. (GFS: US), United Microelectronics Corporation (2303: Taiwan), Vanguard International Semiconductor Corporation (5347: Taiwan), X-FAB Silicon Foundries SE (XFAB: Belgium)

Directional impact and magnitude: Mixed-to-negative for broad mature-node pricing narratives; positive for differentiated specialty platforms. Moderate magnitude.

Supporting commentary: Asked whether analog foundry pricing power outside RF infrastructure should be assumed, Tower responded: “Pricing power is particularly done by having best-in-class platforms.” Management added: “We are not a company that likes to indiscriminately raise prices because of a capacity constraint.” The exception was a 13% price increase in 200mm BCD, which management described as a value reset rather than scarcity pricing.

Transmission mechanism: The implication is that pricing power in specialty foundry is not broad-based mature-node inflation. It is platform-specific. Foundries with differentiated BCD, SiPho, SiGe, RFSOI, imaging, or packaging-related capabilities can command premium pricing, while generic mature-node capacity may not see the same uplift. This is important for foundry peers because investor enthusiasm for utilization recovery can overstate wafer price leverage if the demand is not tied to differentiated process value.

Near-term trading catalyst: The read-through is mildly negative for investors expecting broad analog wafer price increases across mature-node foundries. Tower’s language suggests disciplined partnership pricing rather than aggressive allocation-driven repricing.

Longer-duration fundamental shift: The durable implication is that specialty foundry valuation should increasingly depend on process differentiation and customer co-development rather than capacity scarcity. Tower’s gross margin improvement supports this framework: newer higher-margin products, not generalized wafer inflation, drove the margin step-up.

PHOTONIC MATERIALS, MODULATORS AND EMERGING OPTICAL TECHNOLOGY

LIGHTWAVE LOGIC RECEIVES A POSITIVE COMMERCIALIZATION READ-THROUGH FROM TOWER’S ORGANIC POLYMER MODULATOR ROADMAP (READ-THROUGH 7)

Affected company: Lightwave Logic, Inc. (LWLG: US)

Directional impact and magnitude: Positive. High magnitude for company-specific narrative; medium magnitude for fundamentals pending production evidence.

Supporting commentary: Tower stated that it “announced our partnerships with Lightwave Logic and NLM Photonics to bring organic polymers to high volume production for next generation compact modulators.” Management also emphasized reduced-size high-performance modulators as part of its CPO roadmap.

Transmission mechanism: The read-through to Lightwave Logic is direct because Tower named the partnership and framed organic polymers as part of the path toward high-volume production. For a photonics materials company, the key investor debate is not only whether the material performs in lab conditions, but whether it can be integrated into a scalable foundry process flow. Tower’s commentary supports the commercialization path by placing organic polymers inside a broader SiPho manufacturing roadmap.

Near-term trading catalyst: Positive. Public confirmation from a leading SiPho foundry can improve investor perception of Lightwave Logic’s relevance to AI optical interconnect. However, the call did not disclose production timing, revenue contribution, yield, customer qualification status, or volume commitments for Lightwave Logic-enabled products.

Longer-duration fundamental shift: If organic polymer modulators reach high-volume production on Tower’s platform, Lightwave Logic could benefit from foundry-enabled adoption in compact, high-speed, power-efficient modulators. The risk is that Tower remained technology-agnostic across multiple modulation paths, including silicon, thin-film lithium niobate, indium phosphide, and organic polymers. Lightwave Logic is validated as a candidate, not declared the winner.

INDIUM PHOSPHIDE-BASED MODULATION AND INTEGRATED LASERS RECEIVE A POSITIVE READ-THROUGH, WHILE PURE THIN-FILM LITHIUM NIOBATE NARRATIVES LOOK LESS DURABLE (READ-THROUGH 8)

Affected companies: OpenLight (Private: country not disclosed in source material), Coherent Corp. (COHR: US), Lightwave Logic, Inc. (LWLG: US)

Directional impact and magnitude: Positive for indium phosphide integration and heterogeneous laser/modulator ecosystems; mixed for thin-film lithium niobate-only approaches. Moderate magnitude.

Supporting commentary: Tower said it announced with OpenLight a “heterogeneously integrated 400 gigabit per lane indium phosphide electroabsorption modulator” on its silicon photonics platform. In Q&A, management said integrated lasers are not inherently less reliable than discrete lasers and that Tower is “very bullish about the integrated laser and additionally about an indium phosphide integrated modulator for 400 gig.” Management also said that thin-film lithium niobate may “come in fairly strong for one generation” but that it does not think it “will last for many generations,” expecting a shift toward indium phosphide.

Transmission mechanism: The implication is that the optical modulation market may not standardize around one material. Tower’s view favors an architecture-flexible roadmap, with indium phosphide gaining importance as channel count, form factor, and integration density increase. This supports companies and private platforms tied to heterogeneous integration and integrated laser/modulator strategies. It also makes a negative strategic point for any investment thesis predicated on thin-film lithium niobate being the dominant multi-generation solution.

Near-term trading catalyst: Moderate. The quote is pointed and may influence investor debate around which optical material platforms are durable. It does not disclose revenue wins or customer adoption curves.

Longer-duration fundamental shift: The key shift is toward integrated photonics architectures where laser integration, compact modulators, and form-factor efficiency become more important than standalone component performance. Companies that can integrate photonics materials into high-volume silicon platforms should gain strategic relevance; companies dependent on less integrated material stacks may face a narrower adoption window.

OPTICAL CIRCUIT SWITCHING AND AI SCALE-UP NETWORKS

OPTICAL CIRCUIT SWITCH STARTUPS RECEIVE A POSITIVE READ-THROUGH, BUT THE BIGGER PUBLIC-MARKET IMPLICATION IS THAT AI SCALE-UP NETWORKING IS BROADENING BEYOND CONVENTIONAL TRANSCEIVERS (READ-THROUGH 9)

Affected companies: Salience Labs (Private: country not disclosed in source material), Oriole Networks (Private: country not disclosed in source material), Arista Networks, Inc. (ANET: US), NVIDIA Corporation (NVDA: US)

Directional impact and magnitude: Positive for private optical switching platforms; moderate positive for public AI networking ecosystems; low near-term public estimate impact.

Supporting commentary: Tower stated that it announced partnerships with Salience Labs and Oriole Networks to manufacture “advanced silicon photonics based optical circuit switches,” using Tower’s platform with “heterogeneous integrated indium phosphide optical amplifiers” to achieve “high bandwidth and ultra low latency optical switch solutions for AI data center scaling.”

Transmission mechanism: The read-through is that AI data center networking demand is expanding into optical circuit switching, not just faster pluggable transceivers. Optical switching can become relevant where latency, power, and bandwidth constraints make electrical switching or conventional optical module scaling less efficient. This is positive for companies positioned around AI cluster networking and scale-up architectures, including Arista and NVIDIA at the ecosystem level, even though Tower did not disclose direct revenue exposure for these public companies through Salience or Oriole.

Near-term trading catalyst: Limited for public equities because the named optical circuit switch companies are private and the call did not quantify revenue. The sentiment read-through is that AI networking architecture experimentation remains active and photonics is becoming more central.

Longer-duration fundamental shift: The longer-duration implication is more material. If optical circuit switching becomes part of AI cluster scaling, photonic foundry capacity and heterogeneous integration become critical infrastructure. That favors companies with credible optical networking platforms and could create new competitive vectors against traditional electrical switching bottlenecks.

May 13

$TSEM EXECUTIVE CALL SUMMARY: Tower Semiconductor Ltd. (05/13/26)

EXECUTIVE CALL SUMMARY

Tower Semiconductor delivered a positive, investment-relevant call, but the quarter itself was not the core event. Q1 revenue of $414 million was broadly in line with prior company guidance of $412 million /- 5% and up 15% YoY, while Q2 guidance of $455 million /- 5% implies a company-record quarter, 10% sequential growth, and 22% YoY growth. The more material development was the formalization of silicon photonics commitments: $1.3 billion of contracted 2027 SiPho revenue from the largest customers, approximately $290 million of customer prepayments already received, and management’s statement that the contractual reservation is below both customer full demand and Tower’s internal 2027 SiPho shipment forecast. This materially improves medium-term visibility and shifts the debate from whether AI optical demand is real to whether Tower can add qualified capacity fast enough, maintain yields, and defend share as architectures evolve from pluggables to XPO, NPO, and eventually CPO.

The quality of the quarter was high at the gross and operating profit levels. Revenue declined 6% sequentially from the Q4 2025 record, but gross margin held essentially flat at 26.8%, up from 20.4% in Q1 2025, demonstrating mix-driven profitability rather than simple fixed-cost absorption. Gross profit increased 52% YoY and operating profit increased 96% YoY on 15% revenue growth, which validates management’s argument that incremental SiPho and SiGe revenue carries structurally higher margins. The caveat is that net profit benefited from a non-recurring TPSCo-related tax benefit, and cash flow was heavily inflated by customer advances. Excluding customer prepayments, operating cash flow remained positive, but the optics of $510 million of operating cash flow should not be interpreted as a normalized quarterly run rate.

The call likely drives upward estimate revisions for Q2 and increases investor conviction in the 2028 model, but the larger implication is that the February 2026 model may already be stale. Management reiterated the built-out model of approximately $2.84 billion revenue, $1.12 billion gross profit, $900 million operating profit, and $750 million net profit, but also indicated that the 2027 focus on incremental 300mm SiPho and SiGe capacity is not included in the current model and that a model update could come within the next quarter. This is the most important non-consensus element. The stock reaction should be positive because Q2 guidance exceeded external consensus, the SiPho demand signal is backed by cash prepayments rather than soft backlog commentary, and management sounded unusually confident on technology leadership and customer alignment. The sector read-through is positive for AI optical connectivity, SiPho foundry demand, SiGe driver/TIA content, and data center power-management content, while creating competitive pressure on specialty foundry peers and raising the strategic question of whether TSMC’s integrated CPO approach eventually compresses Tower’s standalone photonics opportunity.

QUARTERLY PERFORMANCE AND QUALITY OF RESULTS

Q1 2026 revenue was $413.6 million, up 15.5% YoY from $358.2 million and down 6.0% sequentially from $440.2 million in Q4 2025. The sequential decline was not a sign of demand deterioration; Q4 2025 was an exceptional quarter, and Q1 landed slightly above the prior guidance midpoint. The quarter’s investment quality came from margin resilience and technology mix, not from an outsized revenue beat.

Gross profit was $111.0 million, up 51.6% YoY and down 5.7% sequentially. Gross margin was 26.8%, up approximately 640 bps YoY from 20.4% and essentially flat versus Q4 2025. That is the cleanest evidence that the model is migrating toward higher-value technology platforms rather than merely recovering from cyclical underutilization. Cost of revenue declined sequentially faster than revenue, which is consistent with mix improvement and operational discipline. Management attributed the margin improvement primarily to newer, higher-margin products, especially SiPho and SiGe.

Operating profit was $64.6 million, up 96.3% YoY and down 8.8% sequentially. Operating margin was 15.6%, up from 9.2% in Q1 2025 and slightly below 16.1% in Q4 2025. Operating expenses were $46.4 million, nearly flat sequentially and up YoY from $40.3 million, reflecting increased R&D and SG&A investment without undermining operating leverage. This cost structure supports the thesis that Tower can absorb higher engineering intensity while scaling high-margin photonics and RF infrastructure revenue.

Net profit attributable to Tower was $65.0 million, or $0.58 basic EPS and $0.57 diluted EPS, up 62.0% YoY from $40.1 million. Adjusted net profit was $74.5 million, or $0.65 diluted adjusted EPS, up from $50.5 million and $0.45 in Q1 2025. The net income quality was lower than the gross and operating profit quality because the quarter included a non-recurring TPSCo-related income tax benefit. The reported 9% effective tax rate should not be treated as normalized; management guided investors to a recurring 15% to 18% tax rate due to Pillar Two and higher-tax jurisdictions such as the US, Japan, and Italy.

Cash generation was optically very strong but requires adjustment. Operating cash flow included approximately $290 million of SiPho customer prepayments, and the official release quantified net cash from operating activities at $510 million, including a $285 million increase in customer advances. Excluding the increase in customer prepayments, operating cash flow was $225 million. Net investments in property and equipment were $156 million. On that basis, normalized free cash flow excluding advance payments was materially lower than headline free cash flow but still positive, which is important given the heavy investment phase.

The balance sheet remains a core strategic asset. Cash and short-term deposits totaled approximately $1.50 billion at quarter-end, against $156 million of short- and long-term debt. Total assets were $3.7 billion, shareholders’ equity reached $3.0 billion, and the current ratio was approximately 5.6x. Customer advances and deferred revenue increased sharply, with current customer prepayment/deferred revenue of $127 million and long-term customer advances of $215 million. The liability recognition is important: prepayments validate demand and reduce funding risk, but they also create execution obligations tied to capacity delivery.

Inventory was $255 million, down slightly from $257 million at year-end 2025, while Q2 revenue guidance implies a sharp sequential revenue increase. This is favorable because it suggests that the expected Q2 ramp is not being manufactured through obvious inventory accumulation. The transcript did not disclose bookings, backlog, RPO, wafer ASPs, wafer shipment units, customer concentration by revenue, or detailed geographic revenue. No evidence was provided of channel pull-forward, distributor inventory distortion, or accounting-driven revenue recognition. The main one-time item disclosed was the TPSCo-related tax benefit.

SEGMENT AND PRODUCT ANALYSIS

RF Infrastructure was the dominant growth engine. Based on the company slide percentages, RF Infrastructure represented approximately 38% of Q1 2026 revenue versus 22% in Q1 2025, implying roughly $157 million of quarterly revenue versus approximately $79 million a year ago, subject to rounding. This category effectively accounted for more than the entire YoY revenue increase, offsetting declines or slower growth in less strategic categories. The segment’s momentum is tied to SiPho and SiGe demand for AI data center optical connectivity, including pluggable transceivers, XPO, NPO, and future CPO architectures.

Silicon photonics was the central product story. Management stated that SiPho revenue grew 3x YoY and that Tower is ramping production across Fab 2 in Migdal HaEmek, Fab 3 in Newport Beach, Fab 9 in San Antonio, and Fab 7 in Uozu, Japan. The company achieved first-flow SiPho revenue shipments from both Fab 2 and Fab 7, with Fab 7 reportedly achieving 95% yield on the first SiPho wafers leaving the factory. The 95% first-flow yield is a meaningful data point because the investment debate increasingly depends on whether Tower can translate customer demand into qualified, repeatable 300mm output without yield drag.

Silicon photonics capacity is being expanded aggressively. Management reiterated that SiPho capacity is on track to grow 5x by the end of 2026 from the Q4 2025 wafer revenue shipment base. In 2027, the capacity focus shifts to additional 300mm expansion in Fab 7 in Uozu, supported by expected full factory ownership. The key operational point is that Tower is not attempting to build an unqualified greenfield platform from scratch; Fab 7 already runs multiple qualified high-volume flows and is already profitable at current volumes. The strategic question is whether the existing fab, interim expansion options, and eventual new shell can bridge demand before capacity becomes the binding constraint.

SiGe also strengthened materially. Management stated that Silicon Germanium revenue grew 24% YoY, with demand tied to drivers and trans-impedance amplifiers for optical transceivers, active copper cables for short-distance scale-up architectures, and low-noise amplifiers for a Tier 1 mobile platform. SiGe is not merely an adjacent legacy RF technology; it is increasingly attached to the same data center port growth that drives SiPho. Management explicitly said that SiPho and SiGe units “pretty much go hand-in-hand,” although SiPho carries a higher margin and therefore higher revenue growth.

RF Mobile is in transition and remains the main near-term weak spot. RFSOI revenue was described as up 12% YoY, but the Q&A disclosed that RF Mobile was down approximately 36% QoQ. Management framed Q4 2025 as an exceptional SOI ramp and stated that full-year 2026 RF SOI revenue is expected to be down versus 2025, even at 300mm, before record growth in 2027 and 2028. The strategic logic is sound: Tower is moving RFSOI from 200mm to 300mm to access finer-line and enhanced capabilities while repurposing 200mm capacity for higher-margin SiPho and SiGe. The near-term consequence is a revenue air pocket while mobile design wins convert into future phone platforms.

Power Management was a steady contributor. Management stated that Power revenue grew 10% YoY, with growth in both 200mm and 300mm BCD offerings. The company highlighted its Gen 3 power platform, with on-resistance below 1.5 milliohm-millimeter squared for key devices above 10 volts, and claimed customer-demonstrated 15% reductions in power-conversion losses versus high-efficiency alternatives. Management also disclosed a 13% price increase in 200mm BCD, not as opportunistic scarcity pricing but as a value reset after prior reductions. The emerging AI data center opportunity is rack-level 800V DC distribution, where smart power stages and point-of-load converters could become a meaningful BCD growth vector.

Image sensors grew 9% YoY, according to management, with demand concentrated in automotive, industrial, machine vision, and high-end video cameras. Tower emphasized high-resolution, high-dynamic-range, low-light, and global-shutter requirements. The company won a second high-performance automotive product during the quarter and is fully qualified with a next-generation high-end video sensor for a leading photography camera maker, pending that customer’s product launch. The investment relevance is optionality: image sensors are not the current stock driver, but hybrid bonding and global shutter technology provide differentiated margin opportunities outside AI optics.

Discrete and MS/CMOS/Misc appear to be de-emphasized or underperforming. Based on rounded slide data, Discrete declined from 16% of Q1 2025 revenue to 10% of Q1 2026 revenue, while MS/CMOS/Misc declined from 8% to 4%. The transcript provided limited discussion of these categories. The decline in mix is not necessarily negative if capacity is being reallocated to higher-margin SiPho, SiGe, and BCD platforms, but it increases portfolio dependence on AI optical infrastructure.

Geographic disclosure was limited. The operational footprint matters more than customer geography in this call. Fab 2 was at approximately 60% utilization as SiPho and SiGe qualifications continue. Fab 3 was at 80%, with utilization temporarily constrained by new SiPho and SiGe process additions, and management expects higher utilization and output in Q2. Fab 5 was at 75%. Fab 7 was fully utilized and above the 85% model level. Fab 9 was at 80%. The utilization profile shows both opportunity and bottleneck: underutilized fabs can support near-term output increases, but Fab 7 is already above model utilization and is the strategic capacity constraint.

GUIDANCE AND FORWARD OUTLOOK

Q2 2026 revenue guidance is $455 million /- 5%, implying a range of approximately $432 million to $478 million. At the midpoint, revenue increases 10.0% sequentially from Q1 2026 and approximately 22.3% YoY from the rounded Q2 2025 revenue of $372 million shown in the company slides. The low end still implies sequential growth of approximately 4.5%, while the high end implies approximately 15.5% sequential growth. The midpoint is also approximately 3.4% above the prior Q4 2025 revenue record.

The guidance quality is strong because management also reiterated sequential revenue and margin growth throughout 2026. A record Q2 guide alone could reflect a one-quarter catch-up; the more important statement is that management continues to expect sequential margin expansion across the year despite heavy capex, technology qualifications, and multi-fab ramp activity. The assumptions behind that target are clear: continued SiPho growth, SiGe attach, higher Fab 3 output in Q2, ongoing Fab 7 utilization, product mix enrichment, and new high-margin platforms ramping faster than legacy RF Mobile or Discrete headwinds.

The prior Q1 guidance was $412 million /- 5%, so the actual $413.6 million result was only a modest revenue outperformance versus company guidance. External consensus context was more favorable: Reuters reported Q1 revenue exceeded LSEG consensus of $411 million and adjusted EPS of $0.65 exceeded the $0.56 estimate, while Q2 revenue guidance of $455 million exceeded the $436.4 million estimate. This reinforces that the stock reaction is less about the Q1 revenue beat and more about Q2 guidance, SiPho commitments, and model upside.

The 2028 model remains the anchor but is increasingly likely to be revised. The supporting slides show a built-out capacity model at 85% utilization of $2.84 billion revenue, $1.12 billion gross profit, 39.4% gross margin, $900 million operating profit, 31.7% operating margin, $750 million net profit, and 26.4% net margin. The model implies incremental revenue of $1.274 billion versus FY 2025 and incremental gross, operating, and net profit flow-through of 59%, 55%, and 42%, respectively. Management stated in Q&A that 2027-focused 300mm SiPho and SiGe expansion is not included in the model and that an update to higher numbers could occur within the next quarter.

The capex plan is large but increasingly supported by customer funding. Tower is executing a $920 million SiPho and SiGe investment plan across 8-inch fabs in Israel, Newport Beach, and Texas, plus 12-inch Uozu in Japan. Approximately 40% has already been paid, and the remaining 60% is expected to be paid through 2026 and 2027. The program is on track in purchase orders, process qualifications, and ramp planning. The $290 million of prepayments reduces funding risk and strengthens demand credibility, but it also raises execution stakes because failure to deliver capacity could create repayment, penalty, customer-loss, or reputational risk.

The Japan strategy is central to the forward outlook. Full ownership of 300mm Fab 7 creates a more focused platform for optical photonics and other differentiated technologies. Management expects access to adjacent land to allow expansion up to 4x current levels, subject to grants and approvals. The new shell timeline is likely first half 2028 in a best-case scenario after METI approval and permitting, with an estimated 18-month build from breaking ground to tool acceptance. To bridge near-term demand, Tower is evaluating expansion within the existing Fab 7 footprint and potentially using the previously shut Arai factory for selected tools. This is operationally complex but strategically necessary.

Guidance appears credible for 2026 and ambitious but increasingly substantiated for 2027–2028. The near-term guide is supported by demand, prepayments, visible capacity actions, and utilization upside in Fab 2 and Fab 3. The medium-term outlook remains execution-sensitive because the revenue opportunity is now outrunning the current capacity base. The clearest evidence of conservatism is management’s statement that the $1.3 billion contractual 2027 SiPho commitment is below the internal 2027 shipment forecast. The clearest evidence of risk is the same fact: demand visibility only creates value if capacity, yield, materials supply, and customer product ramps converge.

MANAGEMENT COMMENTARY AND IMPORTANT QUOTES

“Looking ahead, we guide the second quarter of 2026 to be the highest revenue in the company’s history with a mid-range revenue guidance of $455 million, plus or minus 5%, representing a 22% increase as compared to the second quarter of 2025 and a 10% growth quarter-over-quarter. We strongly reiterate our target of quarter-over-quarter revenue and margin growth throughout 2026.”

This matters because management is guiding to both record revenue and sequential margin expansion, not just a temporary revenue rebound. The market should treat the 2026 setup as improving earnings power, assuming mix and capacity execution remain intact.

“We continue to strengthen our alignment and partnerships with our photonics customers through the execution of long-term customer commitments, contractually representing $1.3 billion revenue in 2027, with significantly larger valued contracts for 2028, backed by approximately $290 million in prepayments already received from our largest SiPho customers.”

This is the key demand-validation quote. Customer prepayments materially differentiate these commitments from ordinary backlog commentary. The phrase “largest SiPho customers” also highlights concentration risk, but the cash commitment gives management’s demand claims more credibility.

“Importantly, these reservations do not represent the entire express demand of these customers nor the extent of our planned shipment to these customers, and do not include additional wafer shipments to our broader base of more than 50 active SiPho customers.”

This is the most important upside statement in the call. The $1.3 billion figure is not presented as a ceiling. It is a contractual floor from the largest customers, excluding broader customer-base demand. If accurate, the current 2028 model likely understates the achievable revenue base.

“The $1.3 billion is a contractual commitment. It is not, even with those customers that we have that contractual commitment from and with, it is not their full volume demand… that $1.3 billion is not what we’re forecasting for SiPho in 2027, meaning it’s forecasting substantially higher.”

This quote directly addresses the modeling debate. Investors should not simply insert $1.3 billion of 2027 SiPho revenue and stop. Management is pointing to a larger internal forecast, although the transcript does not disclose the exact number.

“The timing of updating a model to higher numbers, I would believe, will be within the next quarter.”

This creates a near-term catalyst. The market will likely begin discounting a model revision before the company formally publishes it. The risk is that expectations may run ahead of the actual revision.

“Our expansion remains on track to grow SiPho capacity five times from the base of our Q4-25 wafer revenue shipments by the end of this year, 2026.”

This is the principal execution milestone. Demand is no longer the gating variable in the bull case; capacity and yield are. Failure to hit this capacity target would directly impair the thesis.

“This quarter, we already achieved 27%. So like you said, it’s very nice that we already are up from the 20% to 27%. And that’s the linear progression that we expect towards the 39% when we achieve the 2.8.”

This CFO comment explains why the quarter was high quality. Gross margin expanded sharply YoY even with sequential revenue down. The gross margin trajectory is the financial translation of the mix thesis.

“Plugables are not going away at all. Plugables will stay extremely strong, at least through the 2030… the first things to come on at a higher rate is the near package optics, where we have multiple design wins presently.”

This addresses a core investor concern: whether Tower’s pluggable strength becomes stranded as the industry migrates to CPO. Management’s answer is that pluggables remain durable, NPO ramps first, and Tower has design wins across form factors. The unresolved issue is whether Tower can maintain share when CPO becomes more integrated with advanced logic and packaging ecosystems.

“Pricing power is particularly done by having best-in-class platforms… We are not a company that likes to indiscriminately raise prices because of a capacity constraint.”

This matters for margin durability. Management is presenting Tower’s pricing strategy as technology-value pricing rather than scarcity pricing. That supports customer relationship quality, but it may limit upside if specialty foundry capacity tightens broadly.

1

4

11

4,111

OpenLight, which designs custom application-specific photonic chips, raised $50M in a Series A extension, after raising $34M in August 2025 (@charrindisguise / DatacenterDynamics)

(Visit Techmeme dot com for the link and full context!)

1

3

1,500

Silicon photonics startup OpenLight raises additional $50m in extended Series A funding round dlvr.it/TSGW02

2

131

OpenLight Secures $50M in Series A-1 Funding to Accelerate Global Deployment of Next-Gen Photonics

#Photonics #HPC

ow.ly/VREh50YR3xi

2

177

Apr 15

No. This type of BS mindset needs to stop.

What I do is point them out to retail first before the 100-500% returns.

US institutions like Point72 or Apollo would have bought them out eventually.

1. $IQE went up because they're sitting on the most latent merchant capacity in the world for InP reactors back at a 100M euro marketcap. While companies like Landmark were trading at $3.8B.

They were also the supplier to $LITE, and photonics/epiwafer demand took off this year.

2. $SIVE went up because they had new deals with $JBL and O-Net.

But they were already unknown as the laser supplier to $MRVL's CPO program when I first went long.

American institutions like $AVGO would have likely just bought the company directly like what Qualcomm did with Alphawave over in the openlight side of things if I didn't bring attention to it.

Then Swedish retail investors wouldn't get any of the upside.

3. $ALRIB went up because their earnings sent their P/E down to fwd 26, despite holding a duopoly in the MBE category with $VECO.

This combined with new SiPH equipment, as well as $IQE QD Laser (for quantum dot) being their customers.

This was combined from raw information discovery of the decade that $MSFT Quantum was their buyer.

You don't see direct hyperscaler frontier programs in quantum computing dependant on some <$1B MC company.

4. $SOI is up 208% because it has an unknown monopoly over SOI substrates for silicon photonics and CPO.

This was more information synthesis combined with timing the bottom of their legacy cycle.

5. $RPI went up because of earnings and AI hardware usage.

I was just the very first person to point it out.

I projected 55% revenue growth compared to 14% from analysts. They did 58%.

I just gave retail the chance to buy it before institutions.

The stock would have gone up off of pure fundamentals without me posting my thesis because you don't do $511m in revenue off a $500m MC as a fabless company.

I'm just giving retail the all the information discovery before institutions have a chance to find it and price it in.

This is a completely different model than the same institutions telling you to buy index funds or stocks that already went up 1500% so you're exit liquidity.

They only went up those percentages because of your and other X accounts attention to those stocks combined with them being undervalued

101

46

1,151

219,532

♰🎶 Sing the Anima Christi in Latin! Demons HATE Latin! 🎶♰

🇻🇦 Anima Christi, sanctifica me.

Corpus Christi, salva me.

Sanguis Christi, inebria me.

Aqua lateris Christi, lava me.

Passio Christi, conforta me.

O bone Jesu, exaudi me.

Intra tua vulnera absconde me.

Ne permittas me separari a te.

Ab hoste maligno defende me.

In hora mortis meae voca me.

Et iube me venire ad te, Ut cum Sanctis tuis laudem te, In saecula saeculorum. Amen

🇺🇸 Soul of Christ, sanctify me.

Body of Christ, save me.

Blood of Christ, inebriate me.

Water from the side of Christ, wash me.

Passion of Christ, strengthen me.

O Good Jesus, hear me.

Within your wounds hide me.

Permit me not to be separated from you.

From the wicked foe, defend me.

At the hour of my death, call me

and bid me come to you

That with your saints I may praise you

For ever and ever. Amen.

🎥 Sung by Sr. Miriam, Sr Maria Karol, Sr. Mariana, Dominican Sisters of Mary

Video Openlight Media

17

144

570

42,666

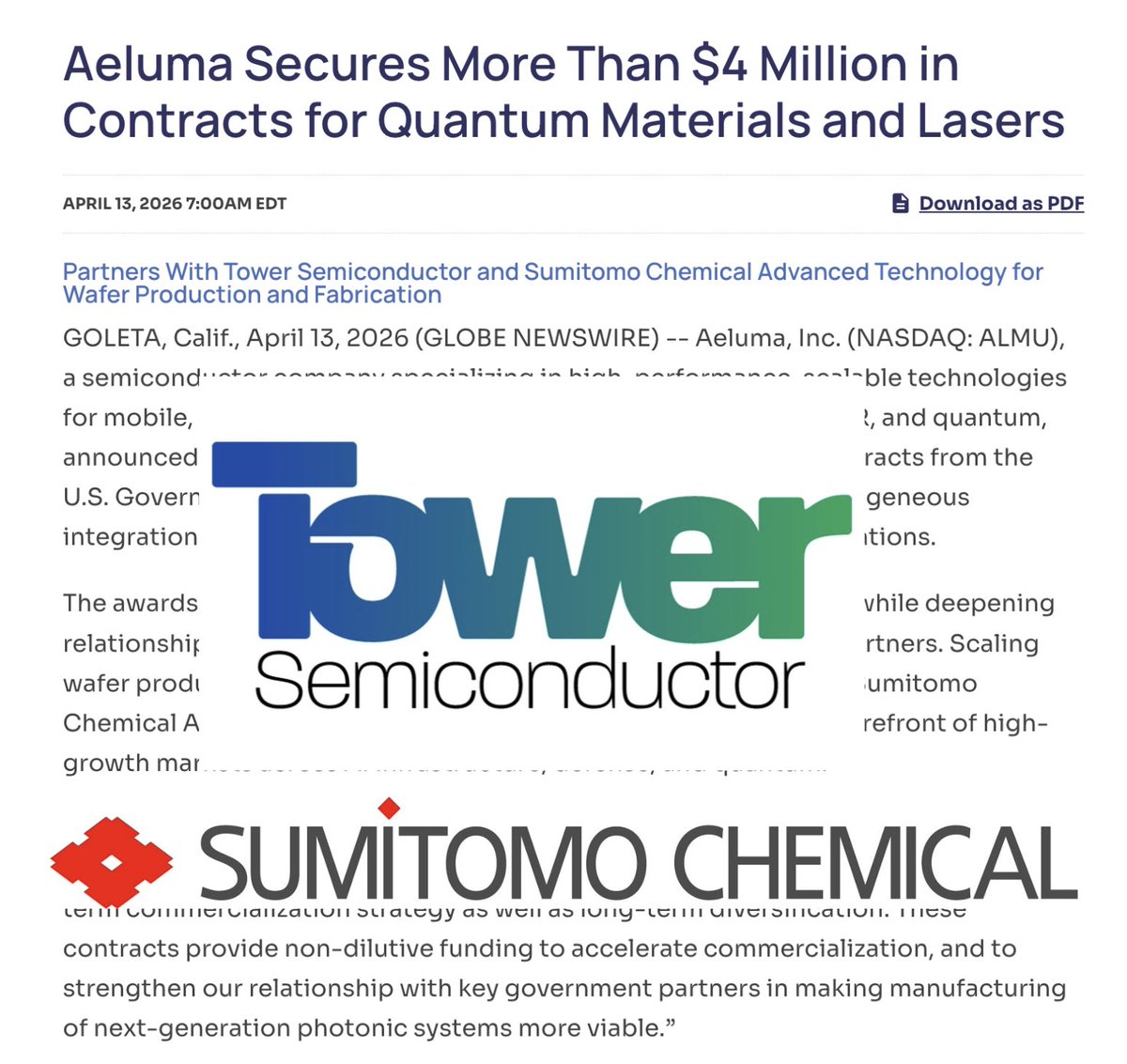

Apr 13

Wow, not only did $ALMU secure a $4M government contract for Qdot lasers on scalable aluminum gallium arsenide (AlGaAs), they just confirmed two of their supply chain partners:

$TSEM and Sumitomo Chemical Advanced Technology!

While a partnership with $TSEM has been wildly speculated (and in hindsight, OpenLight announcing that they were working with $TSEM should have been an obvious giveaway). I definitely did not expect to see this confirmation come (so soon). Especially given the way management has been manoeuvring lately...

For transparency's sake, I did reduce my position in $ALMU some time back, but very happy to see that management is taking shareholder criticism to heart and starting to be more transparent! Incredible news!

(Also for those holding $ALMU; How do you interpret them advancing a scalable aluminum gallium arsenide (AlGaAs) nonlinear materials platform for generation and manipulation of photons for quantum communication, computing, and sensing? Are we transitioning away from InGaAs?)

aeluma.com/news-media/press-…

1

4

37

12,506