Pertonet LNG - A 10 PE stock, Mcap 40k crore coming up with 18k CAPEX.

India imports more than half the natural gas it burns, and that share only goes up. Domestic output is flat while demand from fertiliser, power and city gas keeps climbing. The gap gets filled by ships carrying super-cooled gas from Qatar, the US and Australia. Each one has to dock somewhere and turn that liquid back into gas. In India, more often than not, it docks at Dahej. And Dahej belongs to Petronet.

Petronet LNG is the company nobody finds exciting and everybody depends on. It runs the country's largest LNG import terminal, the quiet toll booth of India's gas economy. Ships come in, gas goes out, Petronet takes a cut on every unit. The market treats it like a utility and prices it like one. Cheap multiple, fat dividend, nobody talks about it at parties.

But it is a deeply profitable toll booth. FY26 revenue was around Rs 43,500 crore, full year PAT about Rs 3,840 crore, and the March quarter was a record at roughly Rs 1,338 crore. Not a struggling business. A dull one.

And a toll booth is only as good as the road it sits on.

For years that road was wide open. Dahej ran near full capacity, contracts locked, cash flowing. The thesis was simple. India needs gas, the gas comes by sea, and it has to pass through our gate.

Now look at what is shifting.

The gate is no longer the only gate. New terminals are coming up along the coast, and the booth that once had the highway to itself now sees competition for the same traffic. Utilisation, the number that matters most for a regas business, becomes the thing to watch.

The management knows this. That is the real story. A company happy being a toll collector is now spending big to stop being just that. It is building a petrochemical plant at Dahej, the petchem project alone around Rs 7,500 crore. Total capex guidance is roughly Rs 9,000 crore each for FY27 and FY28, mostly petrochemicals and storage. Plus fresh long-term supply deals with ExxonMobil and Equinor to feed its own pipes.

This is a cash cow trying to become something more. Always the most interesting moment in a company's life. The question is whether nearly Rs 18,000 crore of capex over two years earns a return, or just turns a light, cash-rich toll business into a heavy industrial one.

And the world keeps interfering. The Gulf is tense, shipping gets disrupted. This year the flagship terminal saw utilisation crash to the low 50s in March because cargoes could not arrive on time. The supply the whole model depends on is hostage to geopolitics no Indian company controls.

So here is the tension. On one side, a debt-light, dividend-paying, monopoly-flavoured asset throwing off close to Rs 3,800 crore a year. On the other, a model facing its first real questions in a decade. More competition. Rs 18,000 crore going into a petrochemical bet that takes years to prove. A supply chain running through the most unstable region on the map.

Bull case: gas demand only goes one way, the dividend pays you to wait, and the petchem pivot is free optionality.

Bear case: the booth gets crowded, that Rs 18,000 crore does not earn its keep, and a defensive utility quietly turns capital-heavy.

That is the whole debate. A steady toll collector reinventing itself, or a comfortable monopoly walking into a tougher, more capital-hungry future than its calm valuation suggests.

The market has decided it is boring. The next few years decide whether boring was the right word.

Views are personal. For educational purposes only. Not investment advice.

1

51

💯👍 Well said. You also buy a BTCTC like Strategy for what they’ll DO with the #Bitcoin in the future, not just today’s BPS/CEBE snapshot.

Is Chevron more valuable, or did $CVX outperform crude over long periods? Much like a refinery adds value beyond the raw long asset via crack spreads & operations, the hope is that $MSTR execution, leverage, and relentless accumulation will do the same.

Sentiment-driven, future optionality engine. $BTC

7

🛵⚡ ATHER ENERGY — READ THE FOOTNOTE, NOT THE HEADLINE

Board just approved a ₹2,500 Cr raise. Everyone read the headline. The footnote is the real story.

📋 WHAT WAS APPROVED (June 12)

Up to ₹2,500 Cr, in two deliberate buckets:

• ₹1,500 Cr → QIP (equity, market-priced, fast)

• ₹1,000 Cr → flexible: FCCBs / preferential / rights (the optionality bucket)

🔑 THE NUMBER THAT REFRAMES EVERYTHING

As of 31 Mar 2026, Ather STILL had ₹1,617 Cr of IPO money UNSPENT — sitting in bank FDs.

So the real question isn't "is dilution bad?"

It's: WHY raise ₹2,500 Cr more when 62% of the IPO cash is still in the bank?

🧮 THE DILUTION (smaller than the noise)

• ₹2,500 Cr = ~6.3% of the ₹39,400 Cr m-cap

• Issued near ₹1,028 = ~3.2x the ₹321 IPO price

Raising EXPENSIVE equity to fund growth ≠ value destruction.

Ola raised ₹780 Cr from weakness. Ather raises from strength.

📈 WHY "FROM STRENGTH" IS EARNED (FY26)

• Revenue 66% → ₹3,672 Cr

• Net loss narrowed: ₹812 Cr → ₹517 Cr

• Operating cash flow turned POSITIVE (₹32 Cr)

• Market share 18.6%, record Q4 volumes

This is land-grab capital, not survival capital.

🏛️ GOVERNANCE-FIRST — WHAT I'M WATCHING

1️⃣ HERO MOTOCORP: holds ~30%, capped at 40% by a private pact. The ₹1,000 Cr preferential route is exactly how it could top up. If it does → related-party deal. Watch pricing the minority vote.

2️⃣ FCCB OPTION: foreign convertibles = future conversion overhang forex risk. Watch if they actually use it.

✅ Clean elsewhere: Deloitte (unmodified opinion, re-appointed), Hero's shares UNencumbered (no pledge), monitoring agency flags zero diversion.

⚖️ VERDICT — PROCESS OVER OUTCOME

Thesis-confirming on operations. Mildly cautionary on capital discipline.

The bull case needs the ~₹4,100 Cr war chest (₹1,617 unspent ₹2,500 new) to ACTUALLY flow into Factory 3.0 the new EL & Zenith platforms.

🚩 MY INVALIDATION TRIGGER

If the raise completes but idle cash keeps GROWING with no matching capex draw-down over 2 quarters → the capital-allocation thesis weakens.

The operating story can be right while the allocation story drifts. Hold both in view.

Strong year. Fair structure. The discipline test starts now. 🧭

📌 Not investment advice. Do your own research. Views change as facts change.

The Antifragile Notebook 📓

@ARNABKANTIDHAR1

#AtherEnergy #ATHERENERG #EVStocks #StockMarketIndia #QIP #CorporateGovernance #Investing #DYOR

16

Lot of people as me why I study successful business models Globally across UK , US or EU

There are some tried and tested profit pools that have very high probabilities of winning and creating shareholder wealth , models that only need a decent to good promoter but with replicating economic conditions , there will be a long term tailwinds in few business models across some sectors , that if can be replicated in India , the rate of change can be really high , that automatically gives you positive optionality over long term , buying these select assets when markets correct can be a real source of positive optionality

Nature of capital returns remains the same , assets change , promoter changes and time changes

read Costco , Nick sleep letters to investors , global bottlers , 2W resale market in US , Pharma Distributors like CVS ,YKK, novo nordisk , Hims and Hers, Palantir some very interesting global business models to read

8

894

I have to say this was not pleasant to read as a $META shareholder.

There is probably some exaggeration at play here but still isn't something you want happening.

The way I see it is this company has had it's fair share of turbulence throughout it's history, and 2026 is no different. Like Zuck said in the memo he's made plenty of mistakes and will make plenty more.

But the company has still managed to get stronger over time through much more difficult challenges than employee morale.

I still think at this valuation the company is significantly derisked. The market knows about the CapEx and layoffs and everything else and has reacted accordingly. Underneath the surface though the fundamentals are strong, the moat is strong, and the optionality is still on the table. That's what really matters.

Stuff like this is worth keeping an eye on, but isn't a thesis breaker by any means.

Jun 13

META IS AN ABSOLUTE MESS INSIDE RIGHT NOW

Wired just dropped an exclusive, and the details are wild.

This week someone interrupted a livestreamed Meta meeting, open to thousands of employees, with an expletive-filled rant about "being the company's bitch." They told the presenters to find a specific Meta AI executive and "tell him that he's a piece of shit."

A presenter covered their face with their hands. Employees in the chat called the start "spicy."

Here is what's behind it.

Meta's AI restructuring cut 8,000 jobs last month, 10% of the company. The same restructuring feeds a unit called Applied AI, where 6,500 engineers and product managers have been drafted in waves since April. There is no application process. You get selected, and your options are join or leave the company. Members call themselves "draftees."

The new job: writing puzzles and coding problems to train Meta's AI models, two tasks a week. People hired to build apps for billions of users now assemble training data for hundreds of AI scientists.

"It's literally the gulag," one employee told WIRED. "You have zero purpose in life all of a sudden, you barely interact with anyone, you just have these tasks every week."

Another: "Most people find the work soul-crushing."

At the same time, Meta started recording US employees' clicks and keystrokes to generate more AI training data. Over 1,600 employees signed a petition demanding it stop. The concession: employees can pause the tracking for up to 30 minutes.

Zuckerberg's response came in an internal memo Friday: "We've made mistakes and will almost certainly make more." He repeated his promise of no more mass layoffs this year. His fixes: limits on the manager ratios Meta had deliberately pushed to 50-to-1 on some teams, bigger budgets for team events, a hackathon next month, and assigned desks by the end of the year.

That same memo says Meta's north star is "to be the best place for the most talented people in the world to make an impact."

The most talented people in the world are writing puzzles for a model and asking permission to pause the keystroke logger.

META declined to comment.

1

3

425

Cogent Biosciences: Buy the Pre-Approval Optionality; Trade Plan Into Decisional Catalysts

Cogent (COGT) is a cli...

tradevae.com/news/trade-idea…

#Tech #TradeIdeas #TradeVae

4

AXISCADES may have just announced one of the most ambitious strategic transformations in India's engineering and defence space.

The headline isn't just the sale of its Aerospace Engineering Services business.

The real story is what the company plans to do with the proceeds.

A ₹2,256 crore war chest

With the completion of Phase 1 and Phase 2 divestments, AXISCADES expects total proceeds of around ₹2,256 crore, creating the financial foundation for its long-term "Power 930" vision.

This is not an exit. It's a complete pivot.

Instead of being primarily an engineering services company, AXISCADES wants to become a manufacturing and deep-tech platform focused on:

- Aerospace Manufacturing

- Defence Solutions

- AI-driven Electronics & Semiconductor (XiDA)

- Space Systems

The capital allocation plan is equally interesting:

- ₹600 Cr for Defence manufacturing & system integration

- ₹600 Cr for Aerospace manufacturing, supply chain and MRO

- ₹300 Cr for AI-centric electronics & semiconductor initiatives

- ₹300 Cr for Space Systems

- ₹300 Cr for common dual-use manufacturing infrastructure

Additional balance sheet strengthening and strategic optionality

The strategic thesis

Management believes the same manufacturing backbone can serve aerospace, defence and space businesses simultaneously, creating operating leverage and long-term competitive advantages.

Instead of building everything organically, they're planning acquisitions in India, the US and Europe and then replicating ("mirroring") those capabilities across the platform.

The long-term target

The company's FY2030 aspiration stands at:

- ₹9,000 crore Revenue

- ₹960 crore PAT

Of course, execution will determine whether these ambitions translate into shareholder value. But from a strategic standpoint, this is one of the more interesting transformation stories currently unfolding in the Indian listed space.

#AXISCADES #Defence #Aerospace #SpaceTech #Manufacturing #ArtificialIntelligence #Semiconductors #StockMarket #Investing

@AethosWealth

34

AXISCADES just closed the second and final leg of a transformation that quietly rewrites what this company is.

On 12 June 2026 the Board approved Phase 2 of its Engineering Services Divestment Programme, the sale of its Aerospace Engineering Services business. Combined with Phase 1 (signed 26 May 2026), AXISCADES has now monetised its entire legacy engineering services portfolio.

Phase 2 value: around ₹1,964 crore (around USD 206 million)

Of which minimum around ₹1,463 crore, plus contingent around ₹501 crore.

Combined Programme (Phase 1 plus Phase 2): around ₹2,256 crore (around USD 237 million).

USD to INR taken at 95.2.

The cash comes in tranches:

Q3 FY27: around ₹906 crore (Phase 1 and Phase 2 first tranches combined)

H1 FY28: around ₹126 crore

FY29: around ₹1,224 crore on residual stake transfer

AXISCADES retains a 49% economic interest until the Tranche 2 closing.

WHAT THEY ARE BUILDING WITH IT

Management calls it Power 930: a target of around ₹9,000 crore revenue and around ₹960 crore PAT by FY2030.

The around ₹2,256 crore is being deployed across four platforms:

Defence Solutions: ₹600 crore

Aerospace Manufacturing, SCM and MRO: ₹600 crore

XiDA Inc, the AI centric electronics and semiconductor arm: ₹300 crore

Space Systems, a new division: ₹300 crore

Common dual and tri use infrastructure: ₹300 crore

Balance sheet and strategic optionality: around ₹156 crore

Around ₹333 crore is set aside for tax.

This is not an exit. It is a capital and capability reallocation.

AXISCADES is moving from an engineering services house to a manufacturing and products platform spanning aerospace, defence, space and hardware driven AI. Founder Dr. S. Ravi Narayanan is back as Chairman and MD. The core pitch is that one certified manufacturing base serves three demand streams: commercial aerospace, defence and space.

Aerospace Engineering Services revenue will be reclassified as Discontinued Operations under Ind AS. So reported continuing revenue in FY27 will optically drop. Management says it plans to backfill this by accelerating its defence pipeline conversion, which carries higher margins and longer lifecycles. A quantified update is promised at the Q1 FY27 investor presentation.

A fully funded pivot into defence, space and manufacturing, with the funding now locked and a 49% retained stake keeping upside alive until FY29.

Disclaimer: This content is for educational and informational purposes only and is not investment advice. LNPR Capital is a SEBI Registered Research Analyst (RA No. INH000012953, BSE Enlistment No. 5843).

2

8

1,303

1h

Totally get it and trying to find my personal groove in that respect - I vacillate between no revenue spec and entrenched names with real FCF that have upside optionality

5

x.com/i/status/2065879131074…

好文

@Aktiehedonist 那篇 detailed scorecard,覺得很有趣。因為它不是跟我原本的 AAOI thread 走不同方向,反而是用另一種形式,把同一個核心問題拆得更細。

我那篇比較像是先從物理層抓瓶頸:不要被 800G、1.6T 訂單帶走,真正要看的是 InP laser fab。也就是說,AAOI 的重點不是 module headline,而是它有沒有握住整條供應鏈裡最難買、最難複製、最容易卡住的 laser capacity。

Aktiehedonist 那篇其實也收斂到這裡,只是他的包裝是 scorecard。他給 Supply Control 一個 Pass,因為 AOI 有自己的 InP laser fab、內製 laser、也自己做 production equipment。這跟我原本講的「laser 才是真正的 moat candidate」是同一件事,只是他用 filings 跟數字把它釘得更死。

但我們兩邊也同樣沒有直接把 bull case 講滿。這點才是最重要的呼應。

我說這是一個還沒被 inspected 的 engineering bet。意思是 moat 看起來有,但還沒被 gross margin、yield、cash flow 完整驗證。他那篇其實也是同樣結論:Supply Control 可以 Pass,但 Economic Capture 跟 Cash Conversion 還不能 Pass。Q1 revenue 創新高,需求看起來是真的,可是 non-GAAP gross margin 還壓在 29.2%,公司還在虧錢,capex 很重,股數也被稀釋。

所以兩篇文章真正相符的地方,不是「大家都 bullish AAOI」。不是這樣。比較精準的說法是:我們都認為 AAOI 的物理層位置很特殊,但也都在等財報證明這個物理瓶頸能不能變成股東拿得到的經濟價值。

Demand 這邊也一樣。hyperscaler 回來、800G/1.6T ramp、named orders,這些都不是空氣。但它們很多仍然是 forward-looking:guidance、run-rate、LTA negotiation、capacity expansion。這跟我的框架也一致:AI demand 可以是真的,但真正要驗的是 supply constraint 放大之後,margin 有沒有跟著動。

CPO / ELSFP 也是同一個呼應點。現在數字還沒完全反映,但如果下一代 architecture 把光源從 module 拉到 rack level,那 laser know-how 的價值可能被重新放大。這不是 base case,是 option。但它剛好又回到同一件事:AAOI 值得看的,不是它今天賣幾個 transceiver,而是它手上的 laser capability 會不會在下一代架構裡變更關鍵。

所以我看完那篇的感覺不是「有人寫了一篇不同的 AAOI 分析」。比較像是:我原本用物理層直覺抓到的東西,他用五個測試跟 filings 又驗了一次。

兩邊講法不同,但都回到同一句話:

AAOI 的 thesis 不在 AI optics hype。

在 laser bottleneck。

而這個 bottleneck,現在還在等 economics 驗證。

真正卡住的東西,其實是 InP laser fab。

這才是我一開始看 AAOI 會停下來的原因。很多 optical module 公司都可以講 AI demand、data center upgrade、800G ramp,這些東西現在整個市場都會講,講到最後其實有點吵。但你往下拆一層,就會發現問題不是「模組有沒有需求」,而是「那顆最關鍵、最難複製、最容易變成瓶頸的 laser,到底誰控制?」

AAOI 的特殊點在這裡。它不是單純去外面買 merchant laser 回來組 module。它從很早以前就自己做 laser,InP laser fab 是它自己掌握的。這件事如果是真的跑得起來,那它就不是一般 AI optics module stock,而是卡在供應鏈更底層的那一段。

但我也不想把這件事講太滿。

因為 moat 看起來有,問題是 economics 還沒驗完。

這就是我一直講的:這是一個還沒被 inspected 的 engineering bet。市場現在有點像是先把「如果 laser bottleneck 轉成 pricing power」這件事當成已經發生。可是財報還沒有完全證明。Q1 revenue 創新高,需求看起來很強,但 gross margin 還壓在 29.2% non-GAAP,公司還在虧錢,capex 很重,股數也被稀釋。這就代表一件事:物理層 bottleneck 可能是真的,但它還沒有完整變成股東能拿到的錢。

這裡很重要。

不是有 bottleneck 就等於有好股票。

不是供給稀缺就一定爽到股東。

中間還卡著 yield、良率、設備效率、客戶議價、capex、cash conversion。

講白一點,AAOI 現在的問題不是「故事有沒有」。故事很完整。InP laser 自製、hyperscaler 回來、800G/1.6T ramp、Texas expansion、CPO / ELSFP optionality,全部都有。問題是這些東西放大之後,會不會真的變成 margin expansion。

如果產能上去,BH laser yield 穩住,GM 往 low-to-mid 30s 甚至更高走,長約簽下來,capex 開始轉成現金流,那這個 thesis 就會變很硬。那代表 AAOI 控制的不是一個漂亮敘事,而是真正的物理瓶頸。

但如果 revenue ramp 了,margin 還是卡在 20s;如果每一輪擴產都要繼續燒錢、繼續發股;如果 laser fab 或 equipment yield 出問題,那就很尷尬。那它可能最後只是 capital-intensive、low-margin manufacturer,只是剛好穿上一件 AI bottleneck 的外套。

所以我會這樣看 AAOI:

Supply control:目前最強。InP laser fab、內製 laser、自己做 production equipment,這是它跟一般 module house 不一樣的地方。

Demand:看起來是真的,但還有 concentration 跟 forward-looking 的問題。hyperscaler order 很重要,可是 top customers 太集中,也代表議價權不一定全在你手上。

Economics:還沒確認。這是最核心的驗證點。不要只看 revenue,要看 gross margin、有沒有 operating leverage、有沒有 cash conversion。

Manufacturing:這裡其實是我最想看下去的地方。因為如果它的自動化線跟自製設備真的可以從 Taiwan copy-paste 到 Texas,那這不是普通 onshoring story。這比較像你自己開了一家便當店,不只會煮飯,連產線、爐子、備料節奏都是自己調出來的。別人也可以開店,但別人不一定知道你那套爐火怎麼控。

CPO / ELSFP:這是 option,不是現在的 base case。但如果未來光源從 module 裡被拉到 rack level,那 high-power laser 的重要性會再上去。這就讓 AAOI 的 laser know-how 不只綁在今天的 transceiver cycle,而可能延伸到下一代 architecture。

所以我自己的結論沒有變:AAOI 最值得看的不是 AI optics hype,而是它到底能不能把 laser bottleneck 變成 owner economics。

現在這個 moat 還沒完全被財報驗過。

但它不是空氣。

它有物理層、有產能限制、有製程 know-how、有供應鏈位置。

接下來要看的也很簡單:不要被 order headline 帶著跑,看 margin。看 yield。看 capex。看 dilution。看長約。看 Texas ramp 到底是 copy-paste 成功,還是擴產後才發現工程問題開始冒出來。

如果這些數字開始對上,那 AAOI 會從「有趣的 engineering bet」變成真正被確認的 supply-chain moat。

但在那之前,我不會急著說它已經贏了。

我只會說:這家公司值得看,因為它卡的位置很底層。

而 AI 這條供應鏈,最後真正賺錢的,通常不是最會講故事的人。

是那個握住瓶頸的人。

2

11

2,782

This is the era of the cybernetic teammate.

The partner specialised in everything. The always-online associate. The agentic IR department.

AI amplifies the impact that a solo investor can have on the world, and provides a large enough lever to extract venture capital from a decades-long rut.

To understand this shift, consider the framing in Oliver Williamson's seminal work, Markets and Hierarchies, from 1975.

- In environments where transaction costs are high, with more focus on diligence, monitoring and execution risk, heirarchies are the natural solution.

- In environments where transaction costs are low, with more focus on speed, optionality and diversity with smaller investments, broader markets emerge.

Essentially, the larger/later part of the venture market is drifting further towards larger and more hierarchical firms, as should be expected.

However, the smaller/earlier segment is drifting in the opposite direction, towards a market of many independent actors with extreme agency.

This is the other half of the "barbell" emerging, as AI spurs a cambrian explosion of rugged solo capitalists.

Scaled capital is mostly a solved problem. Next up, inception capital.

1

2

5

308

Doesn't China bid oil either way heavily?

China sees

-Oil logistics

-Oil total value (removed from west value add China, relative gain)

etc etc long list

Small example: "If we route from inventories get port filled we get logistical throughput value & routing optionality"

Be careful in thinking oil “crashes” if this fake deal is signed. Trump has been selling SPR this entire time.

1

59

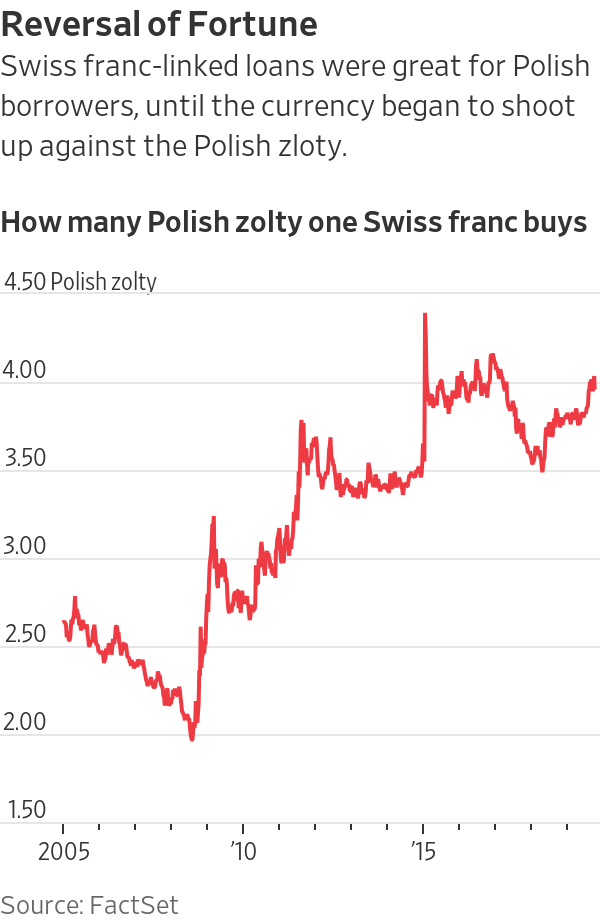

The Swiss Franc Mortgage Crisis: How Poland's Banks Spent a Decade Paying for the Sins of the 2000s — and What Happens Now

700,000 Polish households. PLN 100 billion in estimated costs. Fifteen years of courtrooms, provisions, and political paralysis. The saga that has weighed on every Polish banking stock since 2015 is approaching its end — and the earnings implications are enormous.

The Early 2000s Mortgage Boom — and the Trap Hidden Inside It

In the early 2000s, Polish banks began offering a product that seemed, on every available metric, almost irresistibly attractive: mortgage loans denominated in Swiss francs. The logic was straightforward — Swiss interest rates were dramatically lower than Polish złoty rates, meaning a borrower taking out a CHF mortgage paid significantly less each month than one taking out an equivalent PLN loan. For Polish households in a rapidly growing economy, buying their first home or upgrading from communist-era housing, the monthly saving was real, substantial, and immediate.

The Swiss franc had been one of the most stable currencies in the world for decades. It was pegged, for most of the relevant period, to the euro at a floor of 1.20 CHF per euro — a floor the Swiss National Bank defended explicitly to prevent the franc's chronic appreciation from damaging Swiss exporters. Polish borrowers were told, accurately, that CHF was stable. They were told, less completely, that their monthly repayments were denominated in a foreign currency that they earned no income in — meaning any change in the CHF/PLN exchange rate would directly and immediately change the real cost of their debt, independent of any decision they made themselves.

Banks marketed these products aggressively throughout the mid-2000s. Hundreds of thousands of Polish households took out CHF mortgages between roughly 2002 and 2008 — estimates of the total affected population run to approximately 700,000 households, commonly known in Polish public discourse as the frankowicze. The total outstanding CHF mortgage portfolio at its peak reached approximately €31.5 billion — around 8% of Polish GDP. The product was not marginal or niche. It was the dominant mortgage instrument for an entire generation of Polish homebuyers.

"Initially convinced by banks that the franc was a stable currency, debtors saw their outstanding debt and monthly repayments soar after the czarny czwartek — Black Thursday — event in 2015 when the Swiss National Bank unpegged the franc from the euro."

Black Thursday — January 15, 2015 — and the Day Everything Changed

On 15 January 2015, the Swiss National Bank made one of the most sudden and consequential decisions in post-war monetary history. Without warning, it abandoned the 1.20 CHF/EUR floor it had maintained since September 2011. The franc immediately appreciated by more than 20% against the euro in a single day — and by a comparable magnitude against the Polish złoty. The day entered Polish mortgage vocabulary immediately as czarny czwartek: Black Thursday.

The arithmetic impact on Polish CHF mortgage holders was brutal and instantaneous. A borrower who had taken out a CHF mortgage when the exchange rate was 2.00 PLN per franc now found that the same franc bought 3.50 or more złotych. Their outstanding balance — denominated in francs, measured in złotych — had grown by 50–75% overnight. Their monthly repayments had increased proportionately. They had made no decision, changed no behaviour, and done nothing wrong. The currency they had no control over had simply moved against them — spectacularly, permanently, and in a direction that banks' marketing materials had implicitly suggested was impossible.

The consumer argument against the banks was simple and, as it turned out, legally powerful: CHF mortgage contracts contained clauses allowing banks to set the conversion rate between CHF and PLN for repayment purposes at their own discretion, using their own internal exchange rate tables rather than market rates. The spread between the bank's rate and the market rate was an additional, undisclosed cost that consumers had not been informed of. The CJEU and Polish courts progressively concluded that these "abusive clauses" — as defined under EU consumer protection law — rendered the contracts void. If the conversion clause is void, the entire mechanism for converting CHF to PLN fails. If that mechanism fails, the loan cannot function as written. Therefore: the entire contract is null and void from inception. That is a radically pro-consumer outcome with an equally radical financial consequence for the banks.

The Courts Decide — A Decade of Verdicts Going One Way

The litigation that followed Black Thursday was unlike anything the Polish judicial system had previously processed at scale. Individual consumers — some represented by specialised law firms operating on a no-win-no-fee basis, others through consumer protection organisations — began filing lawsuits claiming their CHF mortgage contracts were void due to abusive clauses. The cases moved slowly at first. Then, starting in 2019, a sequence of CJEU and Polish Supreme Court rulings transformed the legal landscape so decisively that the outcome became, in practical terms, a foregone conclusion.

3 OCTOBER 2019 · CJEU RULING

Dziubak vs. Raiffeisen — The Landmark

The Court of Justice of the European Union rules in Kamil and Justyna Dziubak v. Raiffeisen Bank: if a CHF mortgage contract contains abusive conversion clauses and those clauses cannot be removed without destroying the contract's essence, the entire contract can be declared null and void from inception. This ruling opens the legal door that hundreds of thousands of Polish borrowers subsequently walk through. Prior to this, courts had been uncertain whether to void the clauses or the whole contract. The CJEU answers: the whole contract.

2020–2022 · LITIGATION SURGE

The Flood — Case Volumes Overwhelm the Court System

Following the Dziubak ruling, new CHF mortgage lawsuits are filed at an accelerating rate. By end of 2022, tens of thousands of active cases clog the Polish courts. Polish common courts rule in consumers' favour in approximately 90–97% of verdicts. Banks begin emergency provisioning as their in-house legal teams and external counsel make clear that the litigation trajectory is essentially one-directional. PKO BP, mBank, Bank Millennium, BNP Paribas Poland, and Santander Poland all announce significant provision increases. mBank reports a PLN 2.3 billion legal provision in Q3 2022 alone, pushing it to a quarterly net loss.

JUNE 2023 · CJEU COMPOUND RULING

Banks Cannot Claim Additional Remuneration — The Final Nail

The CJEU rules in June 2023 that when a CHF mortgage contract is declared void, banks cannot seek additional remuneration or compensation beyond the return of the nominal principal. They cannot claim interest on money lent. They cannot claim valorisation of the capital. The ruling removes the banks' last meaningful legal counter-argument and forces them to set aside approximately PLN 42 billion in additional provisions across the sector through 2025, according to the Polish Bank Association's own estimate at the time.

2024 · CJEU CASES C-488/23 AND C-348/23

Further Pro-Consumer Clarifications — Simplifying Procedure

Two additional CJEU rulings in 2024 close remaining procedural gaps. C-488/23 confirms banks have no grounds to demand valorisation of returned principal. C-348/23 removes the requirement for borrowers to make a formal declaration before courts can treat contracts as permanently void — simplifying the path to judgment and accelerating case processing. By Q3 2024, 120,500 active lawsuits are pending in Polish courts, up 14,000 from end of 2023. Average waiting time for a ruling: 550 days. Courts rule for consumers in 97% of verdicts.

2025 · PROCEDURAL REFORM AND SETTLEMENT ACCELERATION

The Polish Commission for Civil Law Proposes Efficiency Reforms

Recognising the systemic burden on the court system — 120,500 cases at 550 days average waiting time represents a structural judicial crisis — Polish authorities implement procedural reforms including automatic suspension of loan repayments during trials and immediate enforceability of first-instance judgments. Banks accelerate voluntary settlements to reduce case volumes. PKO BP reports 90% of its CHF portfolio now covered by settlement, judgment, or active litigation. Provisions for CHF in 2025 are PLN 0.5 billion lower than 2024. The curve is finally bending.

What It Cost — Bank by Bank, Year by Year

The total financial cost of the CHF mortgage saga to the Polish banking sector is measured in the hundreds of billions of złotych — the Polish Financial Supervision Authority (KNF) estimated in 2021 that the medium-scenario total cost for the entire sector was PLN 100 billion, equivalent to approximately €22.4 billion. That estimate has proven, if anything, conservative as the volume of successful consumer claims has exceeded initial projections.

For PKO BP specifically, the numbers tell the most dramatic story. The bank created PLN 23.6 billion in cumulative legal risk provisions between 2019 and 2025 — a figure confirmed in the bank's own 2025 earnings presentation. In 2024 alone, PKO BP increased its CHF provision by PLN 4,899 million (PLN 4.9 billion) in a single year. These are not theoretical reserves against hypothetical losses. They are real capital set aside to pay real people who won real court cases — PLN 23.6 billion that went to borrowers and lawyers rather than to PKO BP's shareholders as dividends or retained earnings.

How the CHF Crisis Has Suppressed Polish Bank Valuations for a Decade

The mechanism by which the CHF saga depressed Polish bank stock prices is straightforward but compound in its effects. At the most basic level: provisions are a charge against earnings. Every PLN set aside as a CHF legal provision is PLN that does not appear as profit. Every PLN that does not appear as profit is PLN that cannot be distributed as dividend or retained as capital. If you reduce profits, you reduce both the price/earnings multiple the stock trades at and the dividend that attracts income investors. The CHF provision has been a systematic, recurring earnings headache for the better part of a decade.

At the regulatory level, provisions reduce capital ratios. PKO BP's Tier 1 capital ratio fell to 15.8% in Q2 2025 from 16.5% a year earlier, directly attributable to the PLN 1.25 billion Q2 2025 CHF provision. Lower capital ratios constrain dividend capacity — the regulator KNF must approve dividend payouts and will not permit distributions that threaten capital adequacy buffers. PKO BP sat on approximately PLN 11 billion in undistributed profits from previous years at various points — capital that was generated but could not be returned to shareholders because CHF uncertainty made regulators conservative about approvals.

At the sentiment level, the open-ended nature of the liability was perhaps the most damaging element of all. Investors can price a known loss. They struggle to price an uncertain but potentially enormous liability whose final magnitude depends on how many people choose to sue, how courts interpret evolving CJEU rulings, and what settlement rates the banks can achieve in mediation. That uncertainty premium — the discount applied to stocks whose earnings trajectory cannot be modelled with confidence — is itself a quantifiable drag on valuation, entirely separate from the actual provisions taken.

The government dimension: The Polish State Treasury owns approximately 29.4% of PKO BP. A bank that cannot distribute its full earnings capacity because of CHF litigation is a bank whose largest shareholder — the government — is also foregoing dividends. The Tusk government's need for PKO BP dividend income (to fund, among other things, defence spending) creates a direct political incentive to see the CHF saga resolved. The government is simultaneously the regulator's political principal, the bank's largest shareholder, and the institution most motivated to accelerate a clean resolution. That alignment of incentives is one reason the settlement programme has accelerated under the current administration.

How Poland's Banks Are Escaping — Settlement, Demerger, and the Provision Cliff

There is no single legislative resolution to the Polish CHF mortgage crisis — no equivalent of Hungary's forced conversion law or Croatia's legislative settlement. Poland's political system proved unable to deliver a clean statutory solution, partly because the frankowicze constituency is large and vocal enough to make any outcome that disadvantages them politically toxic, and partly because the banking sector's lobbying was effective enough to prevent any outcome that disadvantaged them beyond what courts were already awarding. The resolution is therefore coming through three parallel mechanisms, each operating simultaneously.

Voluntary Settlement — Converting CHF Loans to PLN at Historical Rates

The primary resolution route is voluntary mediation and settlement. Under the PKO BP programme — which has become a template across the sector — borrowers are offered conversion of their CHF mortgage to a PLN loan, as if the loan had always been a złoty loan, at the interest rate (WIBOR plus margin) that would have applied from inception. The financial effect for the borrower: their outstanding balance is recalculated in PLN at the historical rate, their repayment history is recharacterised, and the difference between what they actually paid and what they would have paid on a PLN loan is refunded or credited. The financial effect for the bank: certainty. The settlement cost is calculable, provisions can be taken, and the case is closed. By end of 2025, 90% of PKO BP's CHF portfolio is covered by settlement, court judgment, or active litigation — meaning only 10% remains in genuine uncertainty.

Settlement proceedings were initially managed through the Court of Arbitration at the Polish Financial Supervision Authority (KNF). PKO BP has concluded tens of thousands of mediation settlements and expects to conclude 2,000–3,000 additional court settlements per quarter until the portfolio is exhausted. The number of pending court proceedings declined through 2025 as new mediation motions replaced contested litigation.

PKO BP Demerger — Isolating the Liability in a Separate Legal Entity

In Q1 2025, PKO BP announced a structural solution to the ongoing CHF exposure: a demerger plan that transfers CHF-denominated loans and related litigation liabilities to the parent bank, separating them from the core operating banking business. By compartmentalising the CHF portfolio, PKO BP aims to ring-fence the legacy liability from its forward earnings trajectory, allowing the core business — retail banking, mortgage lending, corporate banking, wealth management — to be valued and operated independently of the CHF tail risk. This is the same structural logic that drove the creation of "bad banks" in the post-2008 European banking sector. It does not eliminate the liability, but it makes it manageable and prevents it from contaminating the operating business's capital metrics indefinitely.

The Provision Cliff — When the CHF Charge Simply Disappears from the P&L

The most important and least discussed element of the exit strategy is the simplest: provisions must eventually stop. You cannot provision for cases that no longer exist. As the portfolio of unresolved CHF cases shrinks — through settlements, through court judgments, through the gradual exhaustion of borrowers willing to sue — the annual charge to the income statement for CHF legal risk falls. In 2024, PKO BP provisioned PLN 4.9 billion for CHF risk. In 2025, it provisioned PLN 4.4 billion — PLN 0.5 billion less. Management has guided that provisions will continue to fall as more cases are settled. At some point in 2026 or 2027, the residual CHF portfolio will be small enough that the provision charge becomes insignificant — a rounding error rather than a material drag on earnings. At that point, the earnings that were being consumed by provisions instead flow to the bottom line as profit. The provision cliff is the cleanest re-rating catalyst in Polish banking.

What Happens to PKO BP When the Provisions Stop — The Earnings Mathematics

PKO BP reported a record net profit of PLN 10.7 billion in 2025 — and that result was achieved with PLN 4.4 billion in CHF provisions still charged against earnings. The bank's ROE was 19.5% despite that charge. Its net interest margin was 4.76%. Its cost-to-income ratio was 31.1% — exceptionally efficient by any European banking standard. Its CET1 capital ratio was 15.57%, well above regulatory requirements. Its order backlog — the PLN 314.7 billion household deposit franchise, the 20.5 million customers, the IKO mobile banking platform with 8 million active users — is structurally intact.

Now consider what happens when the PLN 4.4 billion annual CHF provision charge approaches zero. At a 19% corporate tax rate (rising to 26% under new legislation), PLN 4.4 billion in provision reversal flows through to approximately PLN 3.6 billion of additional after-tax net profit. Against a current net profit base of PLN 10.7 billion, that is a 34% earnings uplift from a single factor — the removal of a provision charge whose underlying liability is already 90% resolved.

PKO BP's shares trade at a 1.2 times price-to-book ratio, a discount to its historical average and a fraction of regional peers — with a dividend payout ratio of 75% within its 50–75% target corridor and a Tier 1 capital ratio of 16.2%. That combination — profitable, well-capitalised, dominant market position, cheaply valued — has historically been the setup for significant re-rating in European banking stocks when the specific headwind causing the discount is removed.

Management has guided for ROE above 18% by 2027, assuming the new 26% corporate tax rate is in effect. That target is set on a conservative basis — it does not assume the full elimination of CHF provisions within the forecast period. If provisions decline faster than guided, the ROE and earnings outcomes will exceed those targets. The PLN 11 billion in previously undistributed profits — capital that sat on the balance sheet rather than being returned to shareholders during peak CHF uncertainty — now provides additional optionality for special dividends or buybacks as the regulatory picture clears.

The End of the Beginning — and the Beginning of the Re-Rating

The Polish CHF mortgage saga is one of the most consequential unresolved financial stories in Central European banking history. It has consumed more capital, more management attention, more court time, and more political bandwidth than almost any other single issue in Polish financial services since the transition of 1989. And it is, finally, approaching its end — not with a legislative bang, but with the quiet arithmetic of a provision charge that is declining year by year as a portfolio that is 90% resolved works its way toward conclusion.

The investment implication is not subtle. A bank that earned PLN 10.7 billion in 2025 despite a PLN 4.4 billion provision headwind is a bank with an earnings base of approximately PLN 15 billion when that headwind fades. It trades at 1.2 times book value. It pays 75% of earnings as dividends. It is the dominant retail, mortgage, and corporate bank in the fastest-growing major economy in the European Union. The CHF crisis did not permanently damage the business. It temporarily obscured it.

Structural Re-Rating in Progress — The Provision Cliff Is the Catalyst

The Swiss franc mortgage crisis cost PKO BP PLN 23.6 billion in provisions over seven years. It suppressed dividends, constrained capital, depressed the stock price relative to peers, and created an earnings uncertainty that institutional investors priced as a permanent discount. None of those things are permanent. The portfolio is 90% resolved. Provisions are falling. The demerger plan isolates the remaining tail. The court system is accelerating settlements through procedural reform. The 90% resolved figure is the most important number in the entire PKO BP investment case — it means the margin of uncertainty has shrunk from "how much will this ultimately cost" to "when do the last 10% resolve, and at what cost."

The answer is: they resolve in 2026 and 2027, at costs that are increasingly well-modelled because the legal framework is now settled. When they do, PKO BP's earnings step up by approximately one third from a single mechanical change: the absence of a provision charge that was always temporary and is now departing. A bank already earning record profits — already at ROE of 19.5% — with that additional earnings capacity unlocked, at 1.2 times book value, is the kind of re-rating setup that European banking investors encounter once or twice per cycle. The CHF saga is over. The stock has not yet fully priced that fact.

I spend my time looking for needles in haystacks....Polish haystacks specifically, which most people don't bother searching at all. While the rest of the investment world debates AI valuations, I'm reading KRS filings for ammunition factories in Nowa Dęba and checking Polish-Egyptian frozen strawberry trade volumes. Some of it leads nowhere. Some of it leads somewhere the market hasn't looked yet.

1

4

336

As to the "moonshots" Morningstar notes:

SpaceX has a long list of other projects and ambitions, including actual moonshots and interplanetary colonization. These would most probably absorb massive investment, could come with dilution to stockholders, and have a wide range of possible payoffs, positive or negative. In this way, we view them all as having potential “optionality” value, and it’s a matter for investors to decide what they think the payoffs could be and what premium they assign to each project.

As with orbital AI computing clusters, we see SpaceX as the firm best-positioned to pursue such ambitious projects.

One way to evaluate the value of these opportunities is to use the logic of pricing call options, wherein an investor pays a premium upfront to buy into a project at a predetermined price. If the project works out and is worth more than the strike price, the investor wins. But if it doesn’t, the investor loses their premium and the option expires without value.

If our weighted $63 fair value estimate of SpaceX is accurate, at the offering price of $135, investors are adding $72 per share of “option premium” to their investment, for the right to participate, come what may, in the long list of future projects SpaceX may undertake. The more likely you believe cost-competitive orbital AI data centers will be, the closer to the offering price a reweighted valuation of SpaceX gets, and those extra projects could be seen as free options.

251

For once someone is accurate with the real NAV here. Most forget about future taxes on SPCX shares or assign values for future spectrum sales. That should be considered optionality upside as arb funds won’t care about that.

Attached is our price matrix based on appropriately very conservative NAV which is in-line with your figure.

105

treating stablecoins as exciting is a misguided approach, it's about preserving optionality after all

13