Family office. NFA

Joined May 2023

- Tweets 3,789

- Following 466

- Followers 1,761

- Likes 29,137

2,161 Photos and videos

Pinned Tweet

May 2

AI Capex Subsector | 2024-2030

Big Tech capex is going parabolic -$715B according to @KobeissiLetter

Below is our AI Capex Subsector chart for 2026-2030:

• 2026 - Gen 1 optics ( $LITE $COHR), HBM ramp ( $SNDK $TOWA), hyperscaler buildout itself ( $NBIS $CRWV $ORCL). Peaking now.

• 2027 - Cross-gen suppliers go dark. $IQE $TSEM $AEHR plus the Asian names. The companies feeding every architecture at once.

• 2028 - Gen 3 (CPO / interposer). $SIVE plus Ayar (private). Upstream today, two years before peak.

• 2029 - Gen 4 (QD / glass packaging). $LPK $ALRIB. The most pre-commercial lane on the chart.

• 2030 - Plateau across the board Capex digestion year.

Our goal is to identify and track which subsectors are driving this hot ball of money position ourselves upstream of next year's peak before consensus prices it.

Big Tech CapEx has reached unprecedented levels:

The combined CapEx of Amazon, $AMZN, Google, $GOOG, Meta, $META, and Microsoft, $MSFT, is expected to surge 98% YoY, to a record $715 billion in 2026.

This is nearly 3 TIMES the amount spent in 2024 and more than 5 TIMES 2023 levels.

Amazon now expects CapEx to approach a record $200 billion this year.

This is followed by Google and Microsoft which are both guiding $190 billion in CapEx for 2026.

Meta has also raised its expectations by $10 billion to $125-$145 billion.

To put this differently, each company is projected to spend nearly as much in 2026 as they did in the previous 2 years combined, or more.

The AI Revolution is set to accelerate.

1

10

61

10,632

MS2 Capital retweeted

10h

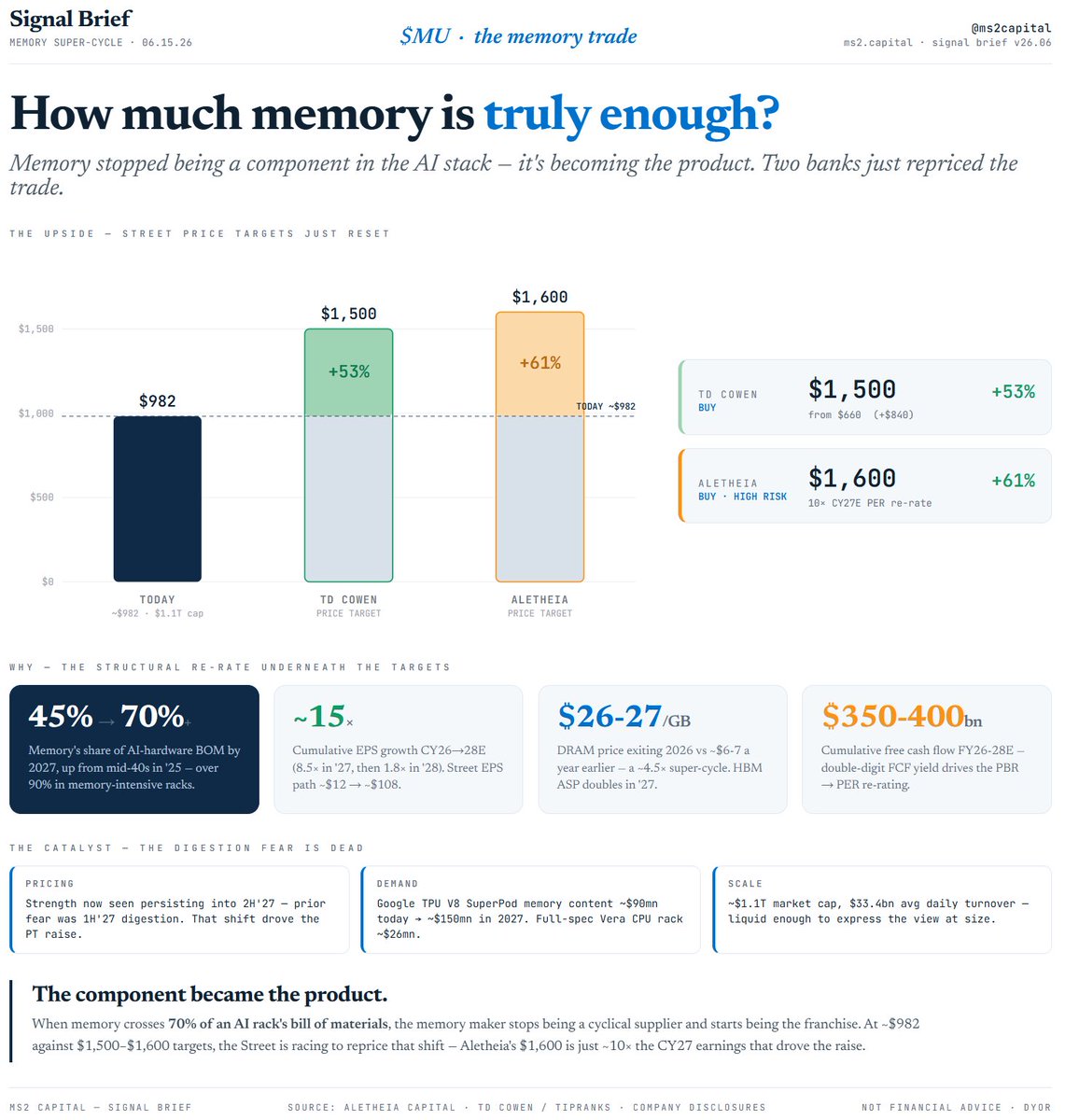

Aletheia on $MU:

PT raised to $1,600

> CY27 EPS expected to jump 8.5x

> CY28 EPS expected to expand another 1.8x

> $350–400B of FCF expected in FY26–28

Memory pricing is still accelerating:

> server DRAM ASP expected 30% QoQ in C3Q26

> HBM ASP expected to double YoY in CY27

The bigger point:

> memory content in AI hardware to > 70% in 2027

> up from the mid-40% range in 2025

> full-spec Vera CPU rack ~$26M ASP per rack

Memory go brrrrrr

16

40

316

31,530

$MU | The Memory Re-Rate

@MicronTech earnings are set to grow ~15x, yet the remains in single-digit territory.

• Memory is now the product, not a component: >70% of AI-hardware BOM by CY27 (vs ~45% in '25), >90% in memory-heavy racks

• EPS path ~$12 → ~$108: 8.5x in CY27E, then 1.8x in CY28E = ~15x cumulative

• Pricing strength now persists into 2H:C27 — the digestion fear is dead

• DRAM $/GB: ~$6-7 → ~$26-27 exiting 2026 (~4.5x). HBM ASP >2x YoY in '27

• $350-400bn cumulative FCF (FY26-28E) → the PBR-to-PER re-rate

🎯Two BUY-rated PT raises (from ~$982):

• TD Cowen → $1,500 ( 53%, via @TipRanks)

• Aletheia → $1,600 ( 61%)

The market is trading chips, when it might need to pivot to re-rating the supplier.

⚡️Micron $MU price target raised to $1,500 from $660 at TD Cowen

TD Cowen raised the firm's price target on Micron to $1,500 from $660 and keeps a Buy rating on the shares.

The firm said higher DRAM content per 1GW, even after SOCAMM de-specing, along with $150 CY27E EPS, keeps them constructive and drives their new price target.

The incremental change is that CPU demand has increased buyers' expectations that pricing strength can persist into 2H:C27 versus. prior view of digestion in 1H:C27.

3

5

207

MS2 Capital retweeted

Jun 14

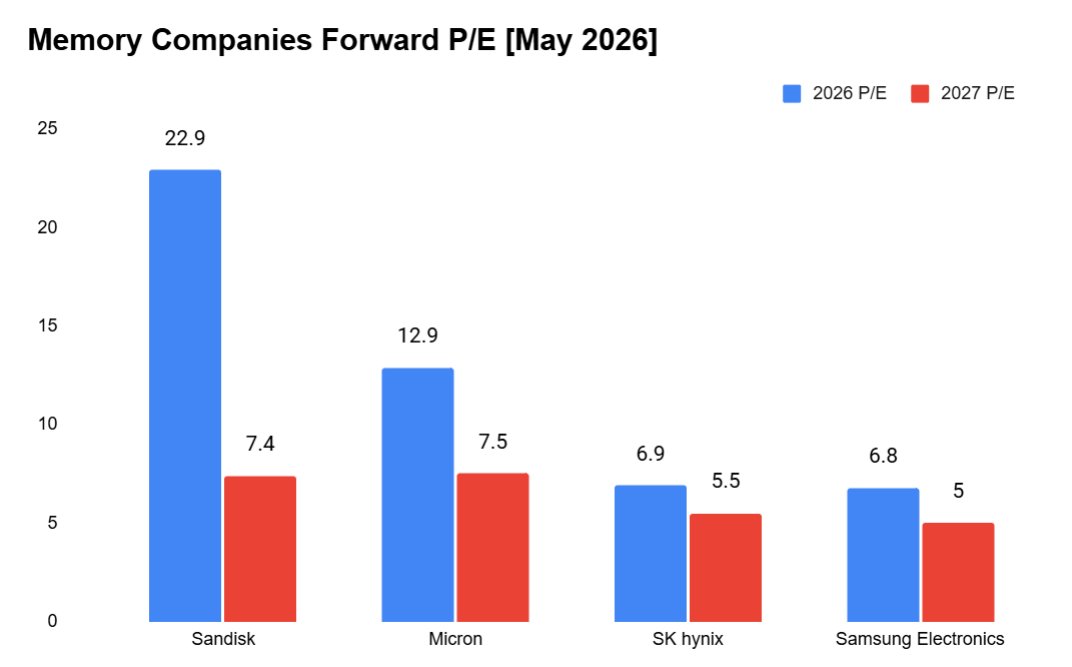

Do you understand how cheap memory stocks are?

$SNDK, $MU, SK Hynix and Samsung: all under 8x 2027 P/E.

Throw Kioxia & Nanya in there too.

Then you've got $NVDA CEO Jensen Huang saying that the memory shortage will persist for "several years."

This is probably the most fool-proof trade globally rn.

(NFA, DYOR)

63

84

884

97,581

Jun 12

⚡️THE GREAT GPU SHORTAGE (Breakdown)

The single most consensus trade in AI was "old GPUs depreciate fast." Wall Street modeled it, short sellers built theses on it, but depreciation never showed up.

🧾Check out receipts | $CRWV

■ H100 rentals: $1.70/hr Oct low → $2.35/hr now ( 40%, climbing 15-20%/month)

■ 3yr old chips renewing at ORIGINAL contract rates - some locked through 2028

■ Every GPU arriving before Sep '26 = already spoken for

■ Half of providers: zero Hopper left and AWS B200 spot: $14/hr

🤖WHY? Agents broke the model | $NBIS

■ Anthropic ARR: $9B → $30B in ONE quarter

■ Claude Code → 20% of all code commits on earth by year-end

■ The squeeze feeds itself: prices rise → clouds pre-buy the next hike → supply tightens → repeat

■ Ceiling nowhere close: AI tools return 5-10x their cost. Nobody blinks at $2.35 when the alternative is falling behind

The squeeze feeds itself: prices rise → clouds pre-buy ahead of the next hike → supply tightens → repeat.

The ceiling is nowhere close - AI tools return 5-10x what they cost renters don't blink at $2.35 when the alternative is falling behind.

⚠️Early warning signals we're watching | $ORCL

■ GB300 ramp outrunning token demand

■ AI lab ARR growth stalling

■ on-demand capacity reappearing

■ renewals printing below old rates

None currently ringing, and while beras got the depreciation math right, they priced a world without agents🚀

(data: @SemiAnalysis_ 100 provider survey)

Jun 12

Neos will rip harder

1

6

240

Jun 11

🧠 AI MEMORY SHORTAGE (60 SEC BREAKDOWN)

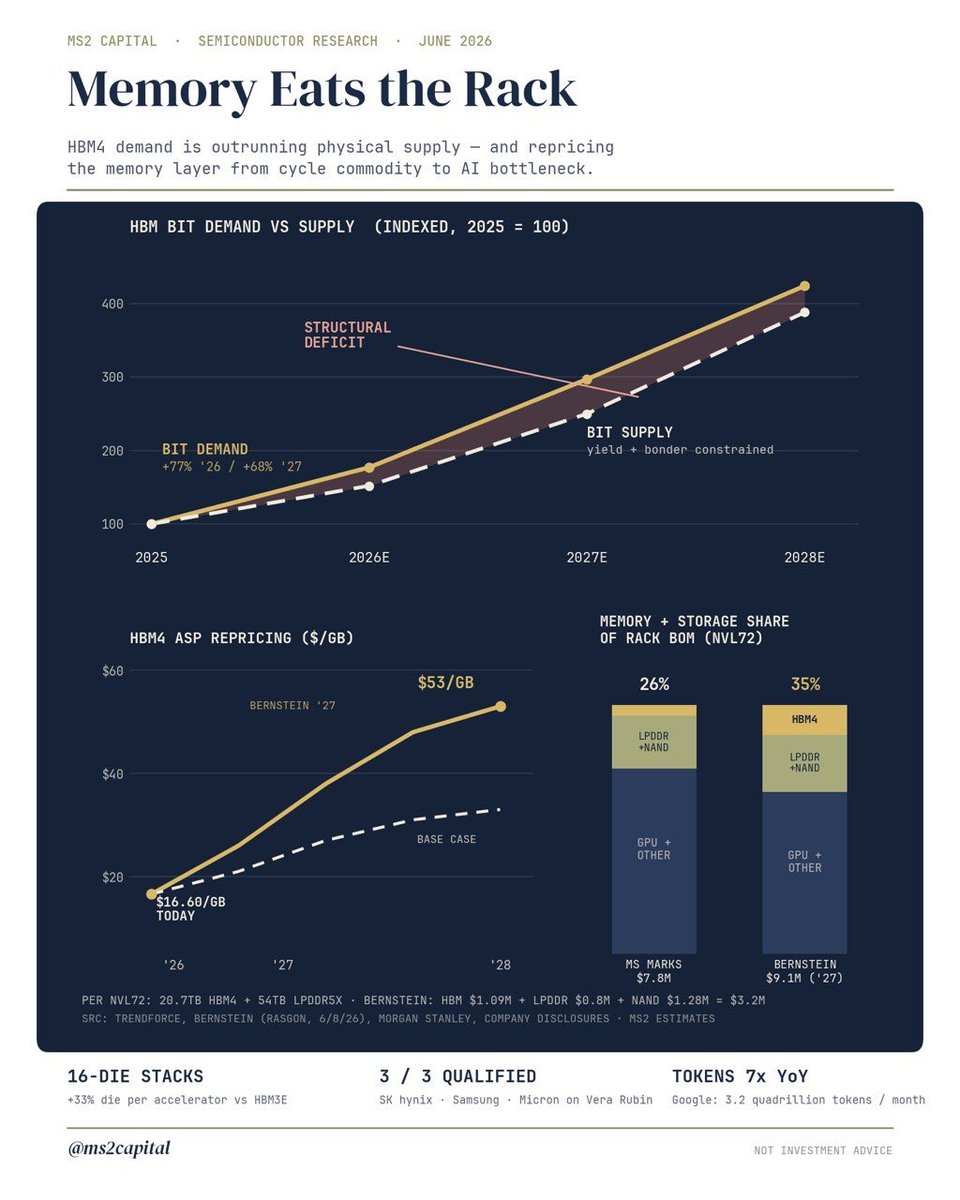

We modeled supply vs demand for HBM4 = the memory every AI chip is bolted to. Only 3 companies on earth make it - $MU is one of them.

▪️Demand > supply every quarter through 2028

▪️Worst gap: late 2027 (only ~70% of orders filled)

▪️Bottleneck isn't fabs, it's stacking machines

▪️16 perfect layers per chip (1 crooked layer= trash)

📡SK hynix just panic-ordered more = the signal.

▪️Price path: $16.60 → $30 /GB. Bull: $53

▪️Buyers not bluffing: each $16.60/memory ~$29/yr AI revenue

▪️Micron at $900 looks expensive, but trades under 8x our 2028 estimate.

▪️Street EPS went $12 → $108 in a year.

The market believes the money, but it just doesn't believe it lasts - our model says it lasts through 2027, but 2028 is the fight.

🔔4 smoke alarms to get us out early:

▪️memory prices below model

▪️machine orders slowing

▪️AI revenue per GB rolling over

▪️ 94% YoY industry growth peaking

Every boom funds the overbuild that ends it - our alarms are built to ring 2 quarters before the top🚀

Jun 10

這個 $MU / HBM4 的新聞,不能只看成「SK hynix 跟 Hanmi 買了 442 億韓元設備」。

表面上是 TC Bonder 訂單。

但物理層看,其實是 HBM4 量產線開始被鎖死了。

你要做 HBM4,不是把 DRAM 多做一點就好。它不是便當店今天飯煮多一鍋,明天就可以多賣 100 份。HBM 是把很多層 memory die 疊起來,還要接得準、壓得穩、熱不要爆、良率不要崩。這裡卡的不是 demand story,是封裝、bonding、yield、throughput。

所以 SK hynix 買 Hanmi 的 TC Bonder 4.5 Griffin,重點不是 442 億韓元本身多大。重點是:這種設備不是拿來拍照用的,是拿來準備 volume ramp 的。

也就是說,HBM4 不是 PPT 裡面的 2027 故事,它已經開始進入 2026 的產線節奏。

然後更狠的是,Jensen 直接講 Samsung、SK hynix、Micron 三家 HBM4 都過了 Vera Rubin qualification,而且都進 production。

這句話很關鍵。

因為 NVIDIA 最怕什麼?不是 GPU 沒人買。不是 hyperscaler 不下單。最怕的是 Vera Rubin 要起量的時候,HBM4 卡在單一供應商,整個 rack 出不來。

AI factory 不是只缺 GPU。你 GPU 再猛,旁邊記憶體供不上,就像牛排館主廚很強,但冷藏庫沒有肉。你火開再大也沒用,最後出餐速度還是卡在食材。

所以三家都過認證,代表 NVIDIA 的 Vera Rubin 供應鏈開始 de-risk。SK hynix 可能還是拿大頭,Samsung 跟 Micron 補上來,這對 NVIDIA 是供應安全;但對 memory 廠來說,是進入下一輪高毛利門票。

這才是 $MU 這篇文真正 bullish 的地方。

因為 HBM4 現在大概 $16.60/GB,Bernstein 看到 2027 可能到 $53/GB。你想一下,memory 以前在很多人眼裡就是 commodity,景氣循環、庫存、砍價、毛利崩。

但 HBM 不是那種舊 DRAM 遊戲。

HBM4 更像是 AI rack 裡面的戰略零件。你不是隨便找一間廠就可以做,不是產能開下去良率就自動上來。它卡封裝、卡 bonding、卡散熱、卡測試、卡跟 NVIDIA 平台一起驗證。

這種東西一旦需求爆,pricing power 就會跑出來。

所以 Bernstein 把 Vera Rubin NVL72 rack 估到 $9.1M,Morgan Stanley 之前是 $7.8M。差在哪?很大一塊就是 memory price 用太低了,太舊了。

換句話說,以前大家看 AI rack,眼睛都盯 GPU。

但現在 memory 開始吃掉更大 BOM。

不是配角了。

HBM 正在從「GPU 旁邊的零件」變成「AI 系統成本跟利潤池的核心」。Memory storage 一台 rack 可能就幾百萬美元,這個東西最後 NVIDIA 大概率會 pass through 給 hyperscaler。因為 hyperscaler 買的不是一片 GPU,是整個 throughput,是模型能不能跑、更大的 context 能不能塞、更複雜的 agentic workload 能不能撐。

所以你說 rack 變貴,會不會 demand 掉?

要看 ROI。

如果 Vera Rubin 的 performance / watt、bandwidth、scale-out 效率真的大幅提升,那 hyperscaler 還是會買。因為對他們來說,貴不是問題,貴但沒有產出才是問題。AI factory 看的是每一瓦、每一 rack、每一美元 capex 能換多少 tokens、多少 inference、多少 training throughput。

這裡的循環很清楚:

SK hynix 買設備 → HBM4 ramp 進入實體產線 → NVIDIA 三家 memory vendor qualification 過關 → Vera Rubin supply chain 降風險 → HBM4 因為技術複雜跟需求強,ASP 有機會繼續上 → Micron、SK hynix、Samsung memory margin 爽到 → AI rack 成本上升,但 NVIDIA 把成本往下游傳 → hyperscaler 繼續買,因為算力 ROI 還在。

這就是正循環。

不是「AI 還有沒有 hype」。

是物理層瓶頸正在重新分配利潤。

以前 AI infrastructure 的主角是 GPU。現在你會發現,HBM、CoWoS、bonding equipment、advanced packaging,全部開始變成真正的卡點。

卡點在哪,錢就在哪。

所以這篇 X post 表面上很短,但其實它把幾個關鍵訊號串起來了:

一個是設備訂單,代表產能不是嘴巴講。

一個是 Jensen 認證三家供應商,代表 Vera Rubin 的 HBM4 supply 被打開。

一個是 Bernstein 的價格模型,代表市場開始重新估 HBM 在 rack BOM 裡面的價值。

最後就是 $MU 這種原本被當成 cycle stock 的 memory 廠,開始被市場用 AI bottleneck stock 重新定價。

當然風險也不是沒有。

如果 2027 產能開太快,或者 hyperscaler capex 突然轉保守,$53/GB 這種價格不一定守得住。HBM4 良率如果爬不上去,也會拖交付。地緣政治、韓國、台灣、先進封裝集中度,這些都還是風險。

但目前這組訊號看起來,不是在講需求見頂。

比較像是:AI supercycle 從 GPU chapter,慢慢進入 HBM4 / Vera Rubin chapter。

而這一章,memory 不再是旁邊那個小配件。

它變成水塔馬達。

GPU 是水管再粗,水塔馬達不夠力,整棟樓還是沒水。

所以你問為什麼 $MU、SK hynix、Samsung memory 這輪可能不一樣?

因為這次不是單純 DRAM cycle 反彈。

是 AI 的物理瓶頸,把 memory 變成新的定價權中心。

這才是重點。

1

20

84

24,900

Jun 11

$MU | HBM4 Demand

Memory is eating the rack - Bernstein's new Vera Rubin math👇

▪️ $3.2M memory storage per $9.1M rack ~35% of BOM vs 26% on stale marks

▪️ HBM4 alone: $0.34M → $1.09M per rack at $53/GB

Micron isn't a memory cycle trade anymore, it's a bottleneck stock🚀

Jun 10

這個 $MU / HBM4 的新聞,不能只看成「SK hynix 跟 Hanmi 買了 442 億韓元設備」。

表面上是 TC Bonder 訂單。

但物理層看,其實是 HBM4 量產線開始被鎖死了。

你要做 HBM4,不是把 DRAM 多做一點就好。它不是便當店今天飯煮多一鍋,明天就可以多賣 100 份。HBM 是把很多層 memory die 疊起來,還要接得準、壓得穩、熱不要爆、良率不要崩。這裡卡的不是 demand story,是封裝、bonding、yield、throughput。

所以 SK hynix 買 Hanmi 的 TC Bonder 4.5 Griffin,重點不是 442 億韓元本身多大。重點是:這種設備不是拿來拍照用的,是拿來準備 volume ramp 的。

也就是說,HBM4 不是 PPT 裡面的 2027 故事,它已經開始進入 2026 的產線節奏。

然後更狠的是,Jensen 直接講 Samsung、SK hynix、Micron 三家 HBM4 都過了 Vera Rubin qualification,而且都進 production。

這句話很關鍵。

因為 NVIDIA 最怕什麼?不是 GPU 沒人買。不是 hyperscaler 不下單。最怕的是 Vera Rubin 要起量的時候,HBM4 卡在單一供應商,整個 rack 出不來。

AI factory 不是只缺 GPU。你 GPU 再猛,旁邊記憶體供不上,就像牛排館主廚很強,但冷藏庫沒有肉。你火開再大也沒用,最後出餐速度還是卡在食材。

所以三家都過認證,代表 NVIDIA 的 Vera Rubin 供應鏈開始 de-risk。SK hynix 可能還是拿大頭,Samsung 跟 Micron 補上來,這對 NVIDIA 是供應安全;但對 memory 廠來說,是進入下一輪高毛利門票。

這才是 $MU 這篇文真正 bullish 的地方。

因為 HBM4 現在大概 $16.60/GB,Bernstein 看到 2027 可能到 $53/GB。你想一下,memory 以前在很多人眼裡就是 commodity,景氣循環、庫存、砍價、毛利崩。

但 HBM 不是那種舊 DRAM 遊戲。

HBM4 更像是 AI rack 裡面的戰略零件。你不是隨便找一間廠就可以做,不是產能開下去良率就自動上來。它卡封裝、卡 bonding、卡散熱、卡測試、卡跟 NVIDIA 平台一起驗證。

這種東西一旦需求爆,pricing power 就會跑出來。

所以 Bernstein 把 Vera Rubin NVL72 rack 估到 $9.1M,Morgan Stanley 之前是 $7.8M。差在哪?很大一塊就是 memory price 用太低了,太舊了。

換句話說,以前大家看 AI rack,眼睛都盯 GPU。

但現在 memory 開始吃掉更大 BOM。

不是配角了。

HBM 正在從「GPU 旁邊的零件」變成「AI 系統成本跟利潤池的核心」。Memory storage 一台 rack 可能就幾百萬美元,這個東西最後 NVIDIA 大概率會 pass through 給 hyperscaler。因為 hyperscaler 買的不是一片 GPU,是整個 throughput,是模型能不能跑、更大的 context 能不能塞、更複雜的 agentic workload 能不能撐。

所以你說 rack 變貴,會不會 demand 掉?

要看 ROI。

如果 Vera Rubin 的 performance / watt、bandwidth、scale-out 效率真的大幅提升,那 hyperscaler 還是會買。因為對他們來說,貴不是問題,貴但沒有產出才是問題。AI factory 看的是每一瓦、每一 rack、每一美元 capex 能換多少 tokens、多少 inference、多少 training throughput。

這裡的循環很清楚:

SK hynix 買設備 → HBM4 ramp 進入實體產線 → NVIDIA 三家 memory vendor qualification 過關 → Vera Rubin supply chain 降風險 → HBM4 因為技術複雜跟需求強,ASP 有機會繼續上 → Micron、SK hynix、Samsung memory margin 爽到 → AI rack 成本上升,但 NVIDIA 把成本往下游傳 → hyperscaler 繼續買,因為算力 ROI 還在。

這就是正循環。

不是「AI 還有沒有 hype」。

是物理層瓶頸正在重新分配利潤。

以前 AI infrastructure 的主角是 GPU。現在你會發現,HBM、CoWoS、bonding equipment、advanced packaging,全部開始變成真正的卡點。

卡點在哪,錢就在哪。

所以這篇 X post 表面上很短,但其實它把幾個關鍵訊號串起來了:

一個是設備訂單,代表產能不是嘴巴講。

一個是 Jensen 認證三家供應商,代表 Vera Rubin 的 HBM4 supply 被打開。

一個是 Bernstein 的價格模型,代表市場開始重新估 HBM 在 rack BOM 裡面的價值。

最後就是 $MU 這種原本被當成 cycle stock 的 memory 廠,開始被市場用 AI bottleneck stock 重新定價。

當然風險也不是沒有。

如果 2027 產能開太快,或者 hyperscaler capex 突然轉保守,$53/GB 這種價格不一定守得住。HBM4 良率如果爬不上去,也會拖交付。地緣政治、韓國、台灣、先進封裝集中度,這些都還是風險。

但目前這組訊號看起來,不是在講需求見頂。

比較像是:AI supercycle 從 GPU chapter,慢慢進入 HBM4 / Vera Rubin chapter。

而這一章,memory 不再是旁邊那個小配件。

它變成水塔馬達。

GPU 是水管再粗,水塔馬達不夠力,整棟樓還是沒水。

所以你問為什麼 $MU、SK hynix、Samsung memory 這輪可能不一樣?

因為這次不是單純 DRAM cycle 反彈。

是 AI 的物理瓶頸,把 memory 變成新的定價權中心。

這才是重點。

4

9

436

MS2 Capital retweeted

Jun 10

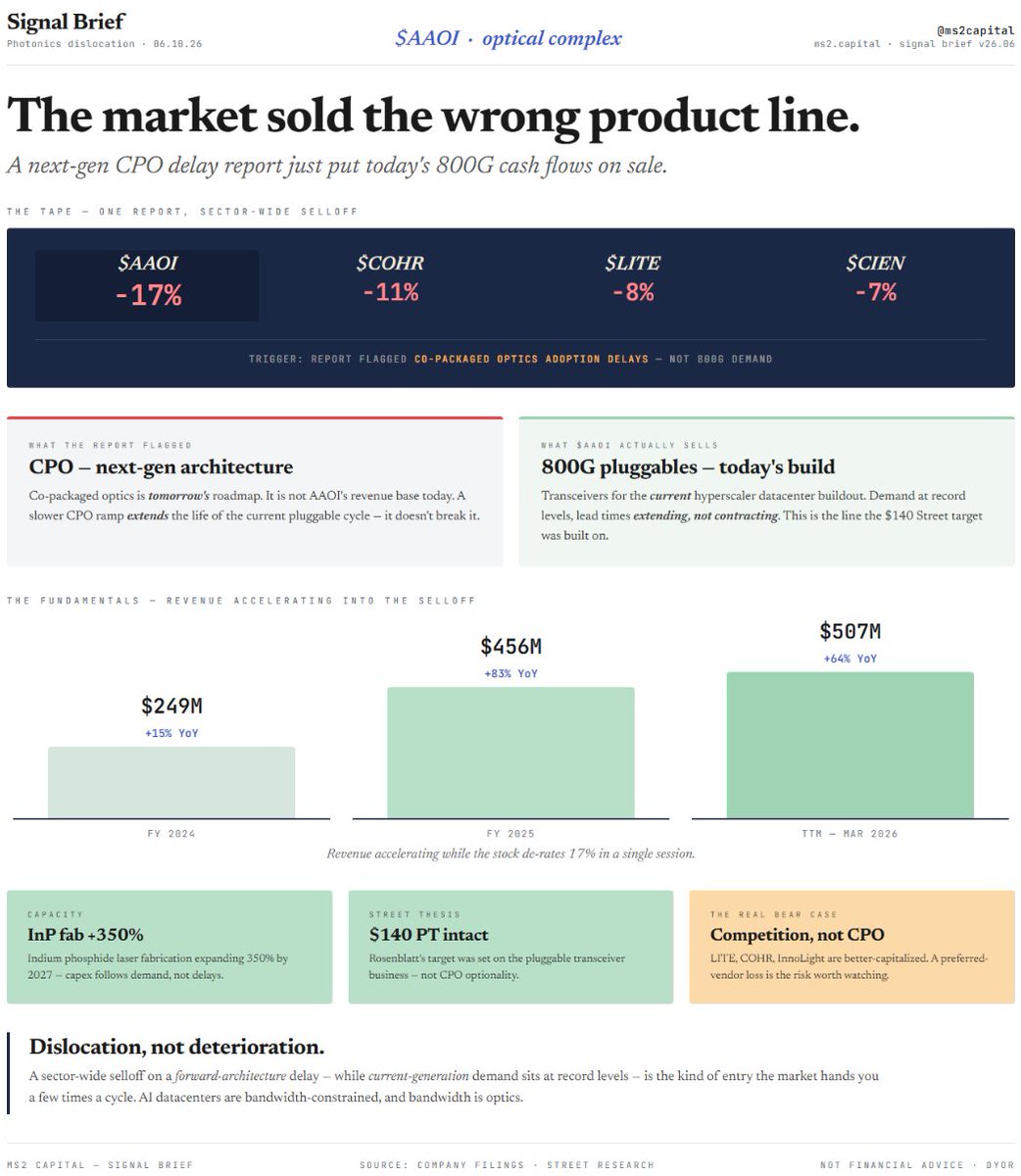

I have received a lot of DMs about SemiAnalysis’ CPO delay discussion and the optics sell-off that followed.

After looking into it, I am preparing a full article.

But the conclusion is simple: I bought optical stocks yesterday. I did not sell $SIVEF, $AAOI, $COHR, $LITE, $CIEN, or my broader optics exposure.

13

21

196

38,126

Jun 10

$AAOI | CPO Delay Headline

Yesterday @AppliedOpto dropped 17% on a CPO delay report. The market sold the wrong product line. Quick breakdown:

What actually happened:

Semi analysts flagged delays in co-packaged optics (CPO) adoption timelines -> entire optical complex sold off:

• $LITE -8%

• $COHR -11%,

• $CIEN -7%

Why the selloff didn't make sense for AAOI:

• CPO is NEXT-gen architecture. AAOI's business today is 800G pluggable transceivers for the current hyperscaler build.

• A CPO delay doesn't break the 800G story - it extends it.

• Rosenblatt's $140 target was built on pluggables, not CPO optionality.

What the fundamentals say:

• TTM revenue: $507M, 64% YoY

• FY2025 revenue 83%, accelerating off a 15% 2024

• InP laser fab capacity expanding 350% by 2027

• Hyperscaler 800G lead times extending, not contracting

The real risk (watch closely):

• Competition - LITE, COHR, and InnoLight are all better-capitalized

• A preferred-vendor loss caps the revenue ceiling. That's the bear case, not CPO

Why we stay bullish on photonics:

• AI datacenter buildout is bandwidth-constrained, and bandwidth = optics

• Record current demand a forward-architecture scare = sector-wide dislocation

• Selling today's cash flows over tomorrow's roadmap is how entries get made🚀

Jun 10

This was me today after a long day at work and a port at -10%.

At least I bought some good names… $MRVL and $AAOI

3

6

242

MS2 Capital retweeted

Jun 9

Most people think the AI buildout is just a couple of stocks – Memory, CPU, GPU, NeoClouds, Photonics..

$SNDK, $MU, $ARM $INTC, $AMD, $NBIS, $LITE, $AAOI, $TSEM, $SIVE

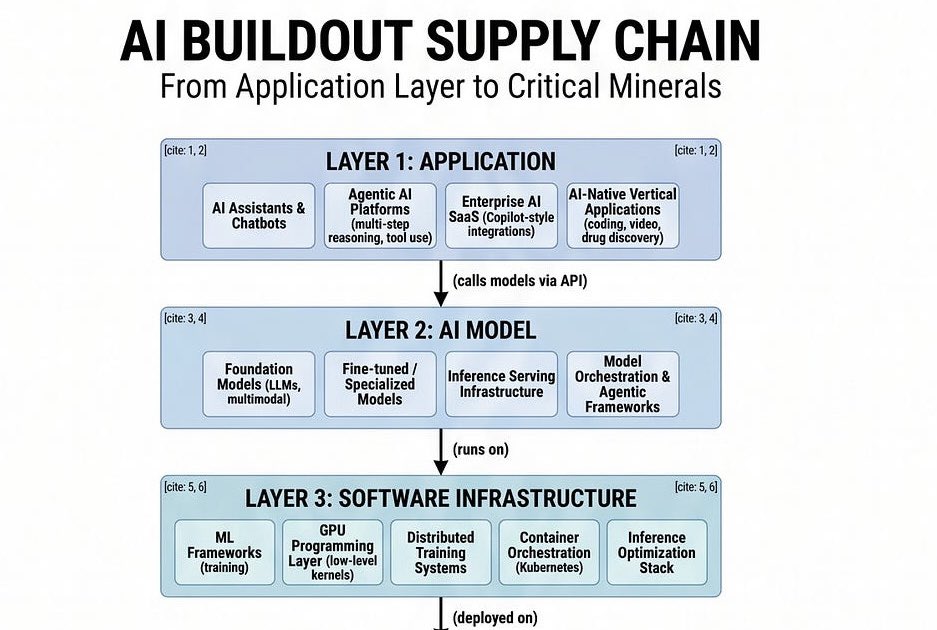

The reality is there’s so much more to it.. I built a complete map of the AI buildout – at least the one I’ve been trading around for the last year.. I put that map on my Substack… 12 layers deep.

Since I’ve seen it circulating on here, I’ll just post it myself.

The hard part isn’t knowing the full stack – it’s making sense of it.

Why is photonics down today but memory isn’t? Why is CPO so relevant in the AI buildout?

Bullish AF on AI infrastructure.

Go check out the full article for free on my Substack, and if you’re going to share it – please do, but link back to my article.

Here is the link: open.substack.com/pub/rensub…

Let’s go find the next 1000% stock ⚡️⚡️

39

114

834

83,481

Jun 9

🛰️ $AAOI | Applied Optoelectronics

The photonics market is still underpriced

Why photonics matters👇

AI clusters have outgrown copper. The fix is light- photonics converts electrons → photons to move data at GPU speed. It's a full stack (materials → packaging → optical engines → deployed networks), and bandwidth is now the bottleneck for every AI buildout.

📊See stack framework from @crux_capital_

Where AAOI sits: top of the stack - the 800G/1.6T transceivers that physically wire GPUs together.

• Q1'26 rev $151M, 51% YoY — 5th straight record quarter

• Datacenter rev $81M, 154% YoY - first volume 800G shipments to a hyperscaler

• FY'26 guide raised to >$1.1B, more than 2x last year

• $324M in 800G/1.6T orders booked; first 1.6T order in hand

• Capacity scaling ~100K → 500K units/mo by year-end

The $NVDA angle 🟢

• Every NVDA GPU needs optical interconnect - AAOI builds exactly that plumbing

• NVDA's ~$4–6.5B optical bet (Lumentum, Coherent, Corning) confirms bandwidth = the new gold

• AAOI is the one major transceiver name without an NVDA equity check yet → asymmetric upside if that changes

Photonics is the AI backbone. At ~$14.6B, AAOI isn't priced like it🚀

Jun 9

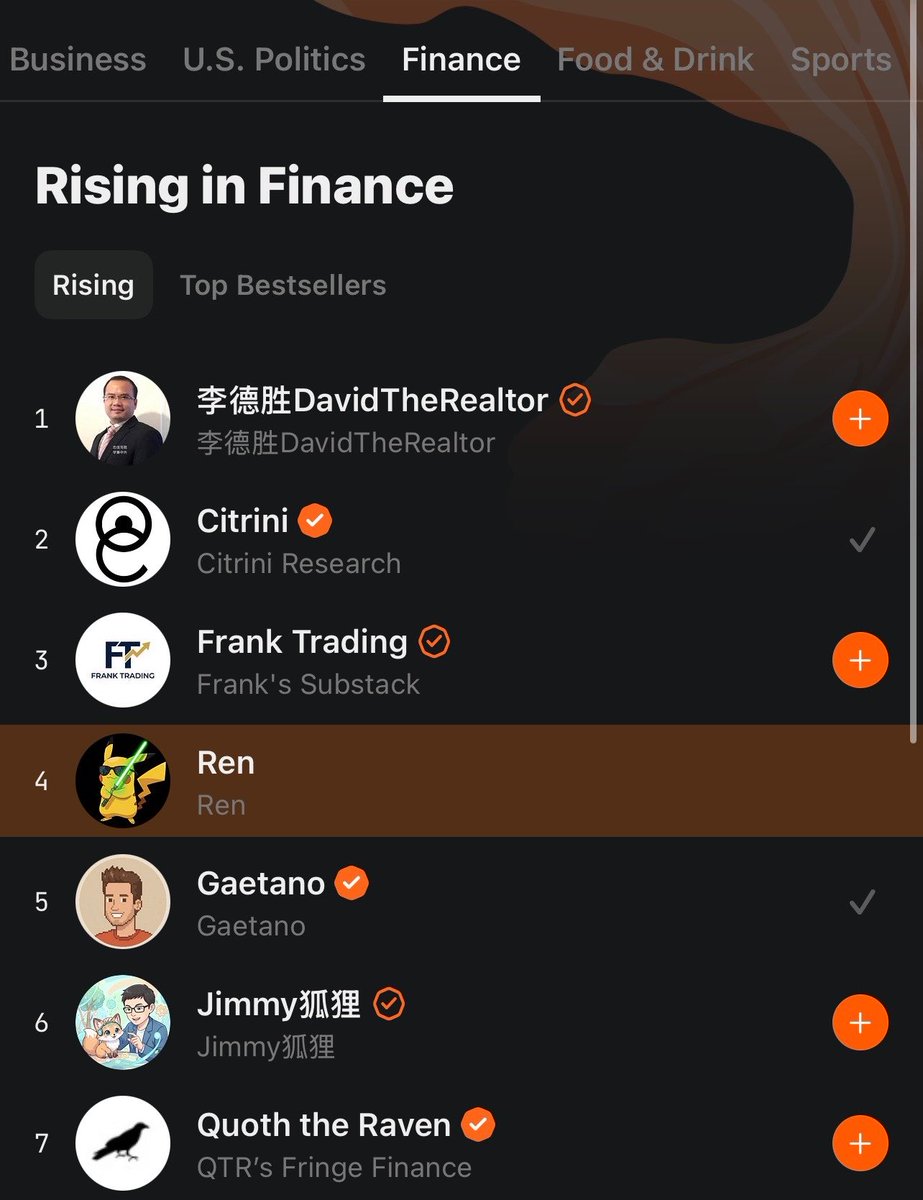

Holy… it’s been one day since I opened my Substack… and I’m already trending at #4 for finance.

When investing in the AI buildout – be it $AAOI, $NVTS, $SIVE, $SNDK, $NBIS – I always think of them in layers.

I’ve created a diagram that compiles what I have been investing in for the past year, with 12 layers from the allocation stack all the way to the minerals.

Whether you are a savvy investor or a newbie, believe me – this map will give you the clarity you need to see how each layer correlates with the others.

Read my complete post and check out my framework, which focuses on 4 main themes I research before buying a stock.

It would be too funny if a Pikachu hit number one on Substack – serious platform, huh.

Go give me some love.

Bullish Ren Pika ⚡️

open.substack.com/pub/rensub…

1

3

6

623

MS2 Capital retweeted

95

146

667

245,732

MS2 Capital retweeted

Jun 5

There's a lot of confusion about the recently patched Zcash bug. Here's how to actually understand it.

If the bug had been exploited before the patch (very unlikely it was), it would have looked like the shielded pool getting drained. Whoever minted the counterfeit shielded ZEC would want to sell fast, before anyone else found the same bug. And remember, the market for ZEC is almost entirely transparent ZEC, not shielded. You can't dump freshly minted shielded ZEC on Binance or Coinbase without unshielding it first.

The losers in that scenario are shielded holders who sit still. The transparent portion of Zcash is fully visible, so it's trivial to enforce that transparent ZEC never exceeds max supply. If you try to unshield more than the cap, you'll get stopped at the door.

So if you hold transparent ZEC (anyone trading, on an exchange, or doing price discovery on ZEC) there's no marginal effect on you. The loss falls entirely on shielded holders.

The team's next step is a new turnstile and a fresh shielded pool in the coming upgrade, which will confirm the shielded pool was not inflated. Think of it as taking headcount at the end of the field trip--that will make sure no extra kids snuck onto the bus.

But while AI found this bug, AI will also deliver the fix for the whole category: formal verification. I'm very bullish on this as the path to harden all software across the industry. Formally verified cryptography can't have implementation bugs by construction.

Right now AI is surfacing vulnerabilities across all our software--browsers, OSes, and blockchains are no exception. We're in the awkward adolescence where every wart is getting magnified and put on full display. But formally verified software is the only path forward for mission-critical software, and Zcash has put it front and center on their roadmap to deliver.

Privacy is too important not to.

(Dragonfly holds $ZEC and continues to. I'm personally an investor in ZODL.)

Jun 5

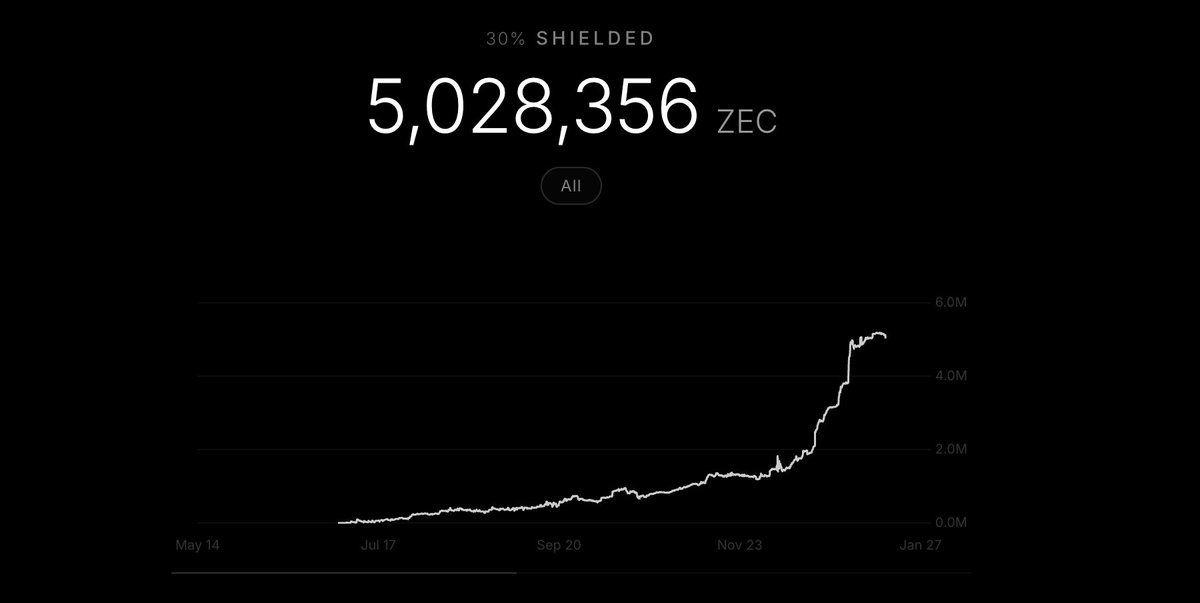

In the last 48 hours, amid all the FUD, the size of the Zcash shielded pool has dropped from 31% of supply to 30%.

Down ~1%.

150

145

934

417,425

Jun 5

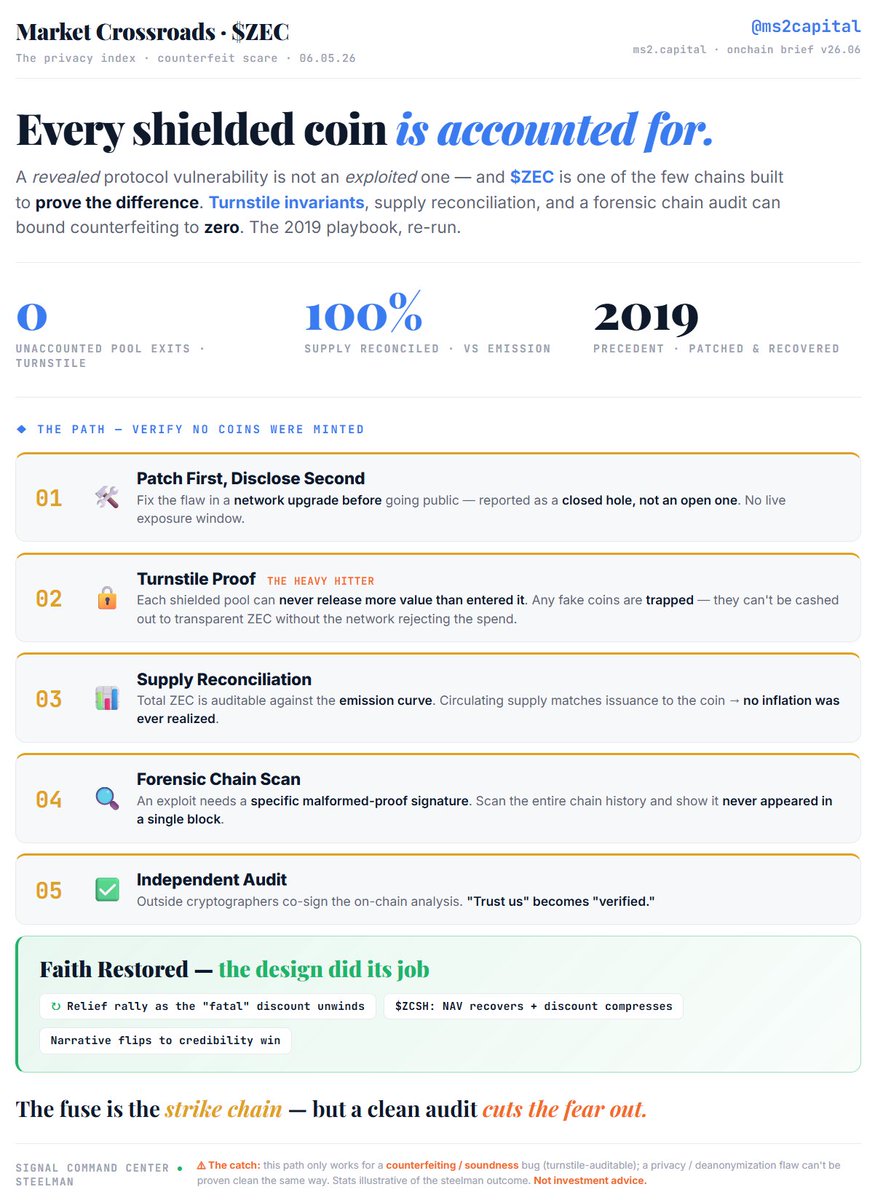

$ZEC | Steelman Argument

Most chains can not prove a bug wasn't exploited, but Zcash is one of the few built to - here's how the foundation could salvage this👇

🔒Turnstiles: shielded pools can't release more value than what entered, so even if a soundness bug minted fake coins, that value is trapped - it can't be cashed out to transparent ZEC without the network rejecting it.

📊Supply reconciliation: total ZEC is auditable against the emission curve. Supply matches issuance → no inflation was ever realized.

🔍Forensic search: scan all chain history for the malformed-proof signature an exploit requires - show it never appeared in a single block.

🛠Patch-first disclosure: fixed in a network upgrade before the reveal = a closed hole, not an open one.

✅Independent audit: outside cryptographers co-sign the analysis. "Trust us" becomes "verified."

📜Precedent: In 2018–19, ECC found a counterfeiting flaw, patched it in Sapling, then disclosed the finding - credibly proved no exploitation via the turnstiles. ZEC survived and recovered.

If they run that playbook:

• Violent relief rally as the "this is fatal" discount unwinds

• $ZCSH double tailwind - NAV recovers and its current ~24% discount to NAV compresses back toward ~11% or less

• Narrative flips to "the turnstile design did its job" - arguably stronger than before.

⚠️ The catch: this only works if it's a counterfeiting/soundness bug (turnstile-auditable). If it's a privacy/deanonymization flaw, you can't prove a clean negative - different, murkier story.

Jun 5

The Holy Trinity is dead. Sadly due to the Orchard Pool exploit, I had to dump our entire $ZEC bag.

- While I think it's extremely unlikely of any minting, it cannot be formally cryptographically proved impossible

- The privacy from AI, govt, big tech narrative demands perfection not improbability

- I read about the exploit yday, and didn't appreciate how it violated my narrative mental map. The 30% dump, made me rethink, and I had to take profit on the entire position

- We will consistently re-evaluate our thinking and if my assumptions are proven incorrect, will rebuy, hopefully at lower prices.

- Privacy is priceless and I have no issue eating humble pie and rebuying much higher.

We still hold $WLD and are excited for Lord Elon to pump our bags.

1

3

8

373

Jun 4

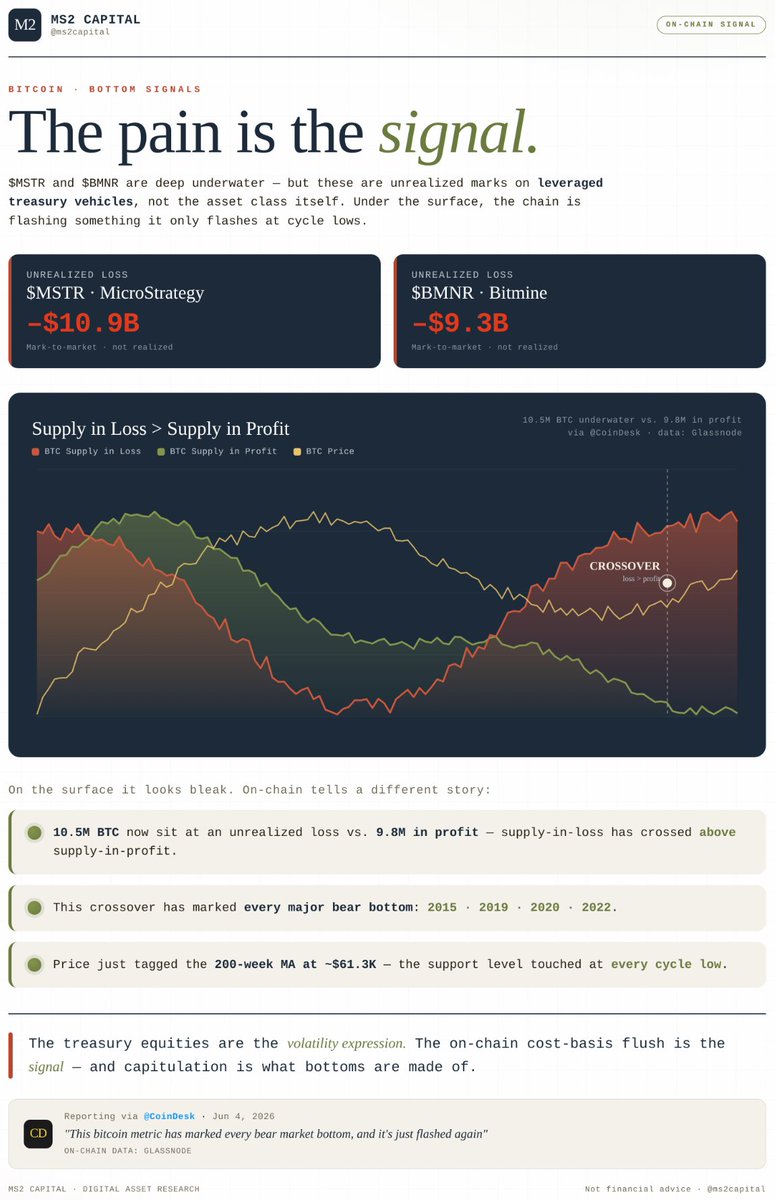

$BTC | Bear Market Bottom Signals

While @MicroStrategy and @BitMNR are deep underwater, these are unrealized marks on leveraged treasury vehicles - they don't represent the entire asset class:

🔴MSTR unrealized loss: –$10.9B

🔴BMNR unrealized loss: –$9.3B

On the surface it looks bleak, but @CoinDesk reminds us to check what onchain is signaling:

🟢10.5M BTC now sit at an unrealized loss vs. 9.8M in profit - supply-in-loss > above supply-in-profit

🟢This crossover has marked every major bear bottom: 2015, 2019, 2020, 2022

🟢 Price tagged the 200-week MA at ~$61.3K - the support level touched at every cycle low

The treasury equities are the volatility expression, but the onchain cost-basis flush is the signal of capitulation and what marks cycle bottoms🚀

LATEST: More than half of all $BTC in circulation is now held at an unrealized loss, a signal that has coincided with every major bear market bottom in history.

1

4

9

276

Jun 2

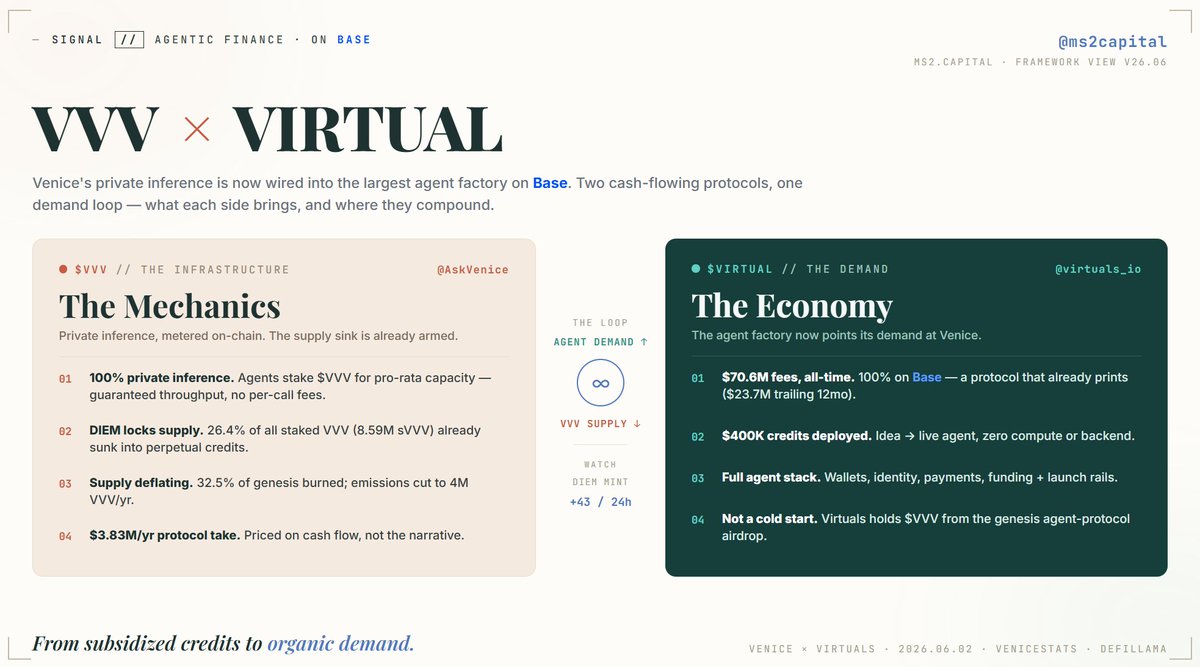

$VVV x $VIRTUAL - Agentic Finance on @base🚀

@AskVenice now powers private inference for every @virtuals_io agent.

🔥 $VIRTUAL: $70.6M fees all-time (100% on Base)

🔥 $VVV: $3.83M/yr take, 32.5% of supply burned

Agents stake → mint $DIEM → VVV leaves supply. 26.4% already locked.

$400K in inference credits: lower bar for ideas → live agent.

Same chain same demand - we'll be watching DIEM mints...👀

Virtuals Protocol is integrating @AskVenice to power AI agent building with private, uncensored inference, available to anyone, anywhere on @base.

Venice brings best-in-class privacy-first inference. Virtuals EconomyOS brings the full agent infrastructure stack: wallets, identity, payments, commerce, funding rails, and launch infrastructure.

We are deploying up to $400,000 in private inference credits so anyone can move from idea to working agent without compute or backend complexity getting in the way.

Start your AI journey. Inference and infra are on us.

Program details soon.

8

26

121

4,045