PracticalVC.com is a Silicon Valley secondary fund run by @DaveMcClure @AmanVerjee @LadyChutzpa @aFehrenbacher | a very bad VC podcast: @TradingVCs 💩

Joined December 2017

- Tweets 293

- Following 886

- Followers 2,233

- Likes 360

8 Photos and videos

Practical Venture Capital retweeted

Mar 25

Dave and Aman break down a packed week in VC and tech in ep28 of @TradingVCs:

OpenAI cancels sidequests, Kraken pulls its IPO, PayPal finally launches stablecoins in 70 countries, and a $55M prop bet on @iamcardib turns into a legal mess.

The Private Mag7 gets a full ranking debate: SpaceX is comfortably #1 at over a trillion, but @anduriltech's surprise $20B DoD contract has it punching into the top three.

Valuation Corner goes deep on the prediction market arms race: Kalshi vs Polymarket.

@davemcclure and @AmanVerjee stack them up against DraftKings and FanDuel — and make their call.

[ tech and vc news ]

0:33 — "you shall not pass" straits of hormuz ✋

2:58 — private mag7 rankings 🏆

6:04 — @elonmusk terafab in austin 🔋

7:21 — @Tesla x @SpaceX super merger? 🤝

10:26 — @OpenAI abandons sidequests 🫳

11:41 — who will take no. 7 🔔

14:57 — @krakenfx freezes IPO plan 🥶

16:25 — @PayPal expands stablecoin 🌏

[ valuation corner: prediction markets ]

18:07 — @Kalshi vs. @Polymarket 🥊

20:15 — the incumbents: @DraftKings & @FanDuel 👴🏻

27:42 — which is best bet? 💰

28:40 — the tale of cardi b 💃

30:45 — second takes 😂

5

6

2,755

Practical VC founder Dave McClure joins UI Charitable CEO Daniel Blake for a session on giving like an investor: why donating cash is usually the wrong choice, how Donor-Advised Funds (DAFs) actually work, and how to donate illiquid or complex assets. x.com/i/broadcasts/1RJjpzbqA…

3

1

4

139

Practical Venture Capital retweeted

Mar 3

Runnin’ Down a Dream: How to Succeed and Thrive in a Career You Love by @bgurley has been one of the most valuable talks l've ever heard.

For years I’ve been using ideas from that talk to build *this* podcast. Bill wrote a new book based on that talk. This episode explores the most valuable ideas from the book and talk.

10

10

266

81,357

Practical Venture Capital retweeted

Mar 3

As David notes, he was an early fan of the “beta” version of my new book. His support, alongside many others, gave me the confidence to invest five more years to deliver a richer, deeper, and hopefully more impactful piece of work. Much appreciation @FoundersPodcast.

Mar 3

Runnin’ Down a Dream: How to Succeed and Thrive in a Career You Love by @bgurley has been one of the most valuable talks l've ever heard.

For years I’ve been using ideas from that talk to build *this* podcast. Bill wrote a new book based on that talk. This episode explores the most valuable ideas from the book and talk.

9

17

286

64,391

Practical Venture Capital retweeted

Mar 4

OpenAI just closed a $110B funding round — the largest private raise in history.

Meanwhile Stripe is now worth $159B, ByteDance hit $550B, and Jack Dorsey just laid off 4,000 employees citing AI productivity.

In Episode 25 of Trading Places, @davemcclure and @AmanVerjee break down the biggest stories in AI, venture capital, and private markets.

Then Daniel Blake (@UI_Charitable) joins us to explain the donor-advised fund strategy founders and investors use to turn illiquid assets into major tax deductions.

00:00 - cold open

00:47 - [ tech & vc news ]

02:07 - @OpenAI historic $110B raise 😲

06:14 - @AnthropicAI $6B staff share sale 🕺

07:45 - Pentagon cancels Anthropic 🧨

11:08 - @sama grabs DoD AI bag💥

14:26 - SaaSpocalypse update 📉

18:20 - @jack Dorsey lays off 4,000 🚶➡️

21:37 - ByteDance @ $550B 💃

24:11 - @Plaid tender offer @ $8B 🔒

25:49 - @RobinhoodApp $1B private fund 🤺

27:24 - [ val corner: @stripe @ $159B ]

29:58 - Competitive analysis 💪

32:40 - @PayPal acquisition target 🎯

39:23 - [ intvw: Daniel Blake - UI Charitable ]

40:09 - introducing Daniel Blake and UI Charitable 👋

40:43 - the problem with selling privately held complex assets 🧐

42:39 - intro to Donor-Advised Funds 🤲

49:03 - DAFs for founders employees 1️⃣

52:10 - DAFs for investors 2️⃣

1:01:54 - donate your crypto holdings 💛

1:03:43 - not all DAFs are created equal ≠

1:05:07 - case studies 📖

1:10:20 - get in touch with UI Charitable 📞

1:10:43 - second takes

Thanks for watching and sharing this horrible, no-good podcast with a friend.

2

3

6

2,360

Practical Venture Capital retweeted

Mar 2

How does OpenAI's projected $100B burn rate stack up historically?

"Meta ... burned to date something between 73 and $76 billion. ... OpenAI will jump that shark. ... OpenAI over three years will outspend the Great Wall of China. ... The point is a lot, a lot of money in a very short amount of time."

— @amanverjee with @davemcclure on @TradingVCs Ep.24

1

1

137

Practical Venture Capital retweeted

Mar 2

The AI funding race just hit a historic milestone.

"It is going to be the biggest round of all time, and I mean, not just the biggest private round, but it dwarfs the biggest IPO of all time... It's over a hundred billion.

Nvidia is now locked in for 30 billion. Amazon has already said they're in for as much as 50 billion and SoftBank and Microsoft and others are entered as well."

— @Amanverjee on @TradingVCs Podcast Ep.24

1

1

141

Practical Venture Capital retweeted

Mar 3

6) another strategy that can be used in SPVs is to manage liquidity (aka #DPI) within the SPV by gradually shifting ownership in progressing winners from the original fund position to other members of the SPV.

while this strategy may be complex and may limit some upside in the originating fund in exchange for (partial) liquidity, it allows for more predictable DPI in years 5-10 that isn’t dependent on exits or tenders or partial secondary sales to a 3rd party, and may avoid ROFRs and transfer restrictions by CEOs and boards that occur in an attempted secondary sale to a 3rd party.

more on this topic later… it also raises issues around RIA vs VC exemption, QSBS treatment, and potential tax consequences for LPs, but overall it still gives the GP more control over liquidity and DPI.

2

6

1,073

Practical Venture Capital retweeted

Mar 3

5) lastly, whether you recycle or not, it’s become pretty clear to me that a strategy like Everywhere / Hustle that uses SPVs to double-down is highly preferable to a big reserve budget in the originating fund.

5a) if you win with your SPVs, it leverages the additional capital for extra carry.

5b) if you LOSE with your SPV bets, they don’t affect the results of your original fund, and you’re not recycling $ into your losers or tweeners and delaying DPI

5c) in a mix of SPV wins & losses, the GP gets carry from the wins but does NOT subtract losses like they would in a normal fund with reserves.

(note: arguably this is bad for SPV LPs, however the market has spoken and doesn’t seem to care about this issue)

7

2

10

1,207

Practical Venture Capital retweeted

Mar 3

some thoughts on #reserves, #follow-on investing, #recycling, and #SPVs for emerging managers

(h/t to @credistick @JoinOdin and @pmoe for starting the convo)

credit to @fredwilson @joshk @bfeld @msuster @pmarca on these topics for excellent advice when starting 500 way back when, even if i didn’t always listen ;)

Mar 3

#recycling is a mixed bag, and altho we did it (mostly) successfully in all 4 of our first funds at 500 — all 4 recycled >20%, all 4 deployed >100% of raised capital, and in a few cases 120% — here’s what i learned about recycling: ♻️

1) it definitely delays DPI by 2-3 years

4

18

9,536

Stripe CEO Patrick Collison: "Software should be like pizza… cooked right then and there at the moment of use."

"You don’t want mass-produced industrial scale software. You want bespoke custom software made for you, that moment."

"Up until now, the economics of software have been conceived as fixed cost and then infinitely monetized."

"Once there are inference costs and custom creation involved, it really shifts. It’s kind of the non-Walrasian software regime."

@patrickc with @collision on @tbpn

131

137

1,823

343,147

Practical Venture Capital retweeted

Feb 24

🥊 $830B vs $380B 🥊 Welcome to Episode 24 of @tradingvcs

This week, @davemcclure & @AmanVerjee debate @OpenAI vs @Anthropic and make bets on who will ultimately win.

Plus: guest @thetyson on pricing transparency, broker networks, and what’s really happening in secondaries.

Watch below:

00:53 - [ tech & vc news ]

02:09 - OpenAI @ $830B🥇

02:56 - Anthropic @ $380B🥈

04:02 - @stripe tender @ $140B 💸

06:38 - @databricks @ $134B 🧱

08:39 - @harvey @ $11B👨🏽⚖️

11:07 - SCOTUS rejects Trump Tariffs 🙅♂️

22:30 - [ intvw: Tyson Hendricksen / @noticedotco ]

23:17 - olympic training to 🍍 farmer

26:21 - founding Notice 💼

33:48 - product walkthrough 🚶➡️

37:58 - why people need transparent pricing 👀

55:50 - prediction markets 🎰

[ val corner: OpenAI vs Anthropic ]

1:03:20 - OpenAI raise history 🚀

1:08:04 - OpenAI vs. Anthropic 🥊

1:13:43 - who wins Gold 🥇

1:18:07 - second takes

Bonus - Don't miss the webinar on Donor-Advised Funds with Dave and Daniel Blake of UI Charitable. This Thursday, Feb 26th and Wed, Mar 4th, 11 a.m. PT. Sign up online via practicalvc website.

4

5

682

Practical Venture Capital retweeted

Feb 4

New episode of Trading Places Podcast with @davemcclure and @AmanVerjee out now! 🚨

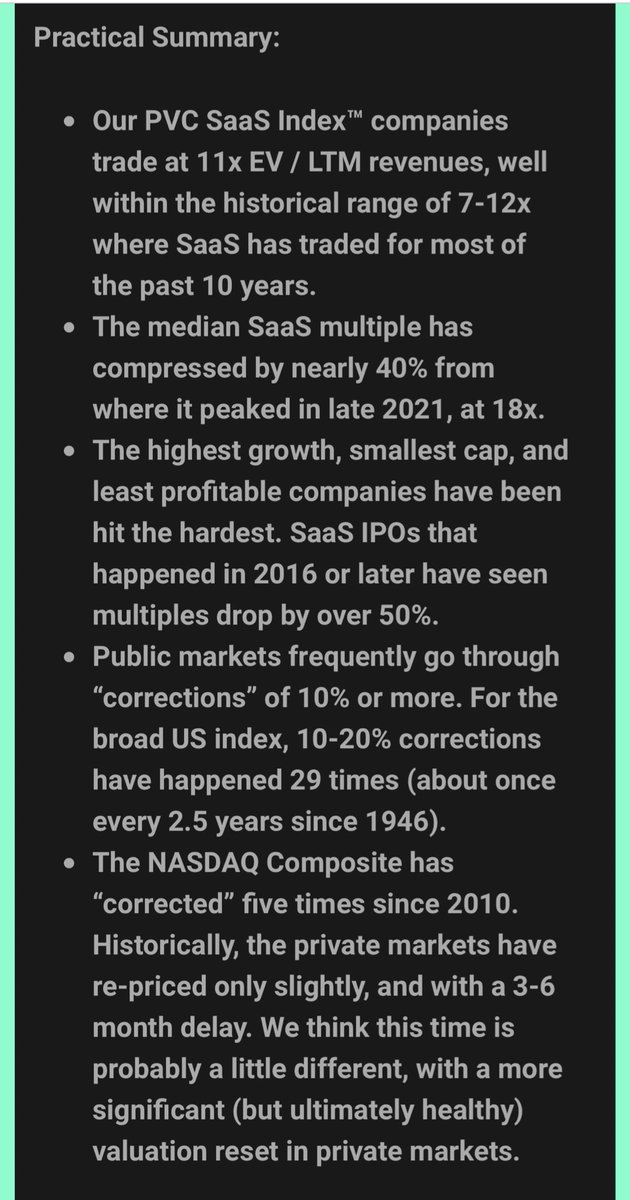

This week is a full-spectrum market tour: the latest rumors swirling around Elon’s empire, the mega-rounds and IPO chess games of Anthropic OpenAI, & the reality check hitting public SaaS multiples reported by @jaminball.

We’re joined by Anurag Chandra (trustee of San Jose Pension Fund) for a rare look inside how real capital allocators think: risk budgets, time horizons, pension constraints, and why governance incentives matter more than “manager genius.”

Then we head to Valuation Corner LATAM with Karin Tenenbaum @LadyChutzpa from the @PracticalVC team for a breakdown of Latin America unicorns, the IPO window reopening, and what could be next after PicPay’s IPO.

Timestamps:

0:00 – cold open

00:53 – [ news ]

1:13 – Elon Inc: xAI SpaceX Tesla 🚀

6:06 – @AnthropicAI doubles to $350B 💰

8:16 – @OpenAI Q4 IPO 🏁

12:25 – @get_Ethos $200M US IPO 🔔

13:55 – AI eats SaaS 🍽️ @jaminball inspired

16:00 – Kevin Warsh Fed chair nod 🪑

19:04 – @Waymo $110B valuation 🚕

21:37 – social media goes on trial 👩🏽⚖️

24:11 – moltbot viral swarm AI 🦞

30:31 – [ intvw: Anurag Chandra ]

32:05 – $2B VC money managed 💪

33:12 – Family office fundamentals 💼

37:40 – San Jose Pension Fund success 🙌

38:17 – Future of San Jose 🔮

1:01:32 – [ val corner: @picpay $2.5B IPO ]

1:02:07 – Analysis: LatAm exit market & liquidity history

1:03:43 – top LatAm unicorns 🦄

1:11:44 – PicPay & fintech competition

1:17:46 – second takes

1

4

8

7,738

Practical Venture Capital retweeted

Jan 22

The center of gravity in venture has shifted from IPOs to secondaries.

CEO @noelregrets & Co-Founder @adamcrawley1 joined @PracticalVC alongside our research partner, Sacra’s @ballve, to unpack the new mechanics of venture liquidity:

🤖 Capital concentration in AI infra & model platforms

🏛️ Companies staying private far longer

📉 Valuations vs. fundamentals in late-stage AI

📊 Data-driven coverage of private markets

🧱 Augment’s role vs. banks & brokers as infra

💸 Explosion of SPVs & structured secondaries

Catch the full episode here: vist.ly/4nu78

#VC #Secondaries #AI #FinTech

1

4

3

1,751

Practical Venture Capital retweeted

Jan 22

Thanks @PracticalVC for having me on the pod, and to @ballve from Sacra for the research firepower. 🎙️

We got into:

⚙️ Capital concentration in AI infra & model platforms

🏦 Why companies are staying private way longer

📉 Valuations vs. fundamentals in late-stage

📊 AI Data-driven coverage of private markets

🧩 Augment’s role vs. banks/brokers in secondaries

💸 Explosion of SPVs & structured secondaries

Catch the full episode here: youtu.be/KD4PTYpOEg0?si=aVfk…

2

6

1,725

Practical Venture Capital retweeted

Jan 14

Episode 19 of [trading places] is here. @davemcclure and @AmanVerjee break down what’s actually happening in venture right now.

we start with the reopening IPO market in 2026, @a16z raising another $15B, @bgurley's latest AI takes, and why everyone suddenly cares about private-market liquidity again.

then we’re joined by @nathanlustig (@MagmaPartners) and @LadyChutzpa (@PracticalVC) for a deep dive on latin america — the exits, the capital cycles, Pix payments in brazil, verticalized plays like Mottu, and why LatAm may be the most misunderstood venture market of the last decade.

we wrap with a valuation corner on @discord — its rejected Microsoft offer, the $15B 2021 valuation, and what it might actually be worth now in a very different market.

0:00 - cold open

[ tech & vc news ]

1:24 - 2026 IPO market opens 🏁

4:31 - a16z raises $15B across several funds 🥇

6:38 - Top 10 VC firms in the world

12:36 - China blocks @ManusAI ✋

16:16 - Bill Gurley on AI

24:15 - @AnthropicAI, @OpenAI, @xai valuations 💸

32:15 - Discord & @Strava IPOs 🔔

37:29 - G Squared Nasdaq team up for private market liquidity 🤝

[ intvw: Nathan Lustig / Magma Partners ]

40:26 - Nathan Lustig background and moving to Chile

40:34 - Karin Tenenboim on PVC LatAm strategy 🌎

49:25 - Brazil Pix payments breakthrough

52:45 - Mottu vertical stack (Motorcycle leasing/logistics) 🏍️

1:07:30 - Investing strategy in LatAm

1:08:56 - PVC Magma LatAm 2ndry Fund partnership 🥳

[ val corner: Discord IPO ]

1:34:36 - What is Discord 🗣️

1:42:07 - 2021 valued at $14.7B / $15B 📈

1:43:24 - Rejected $12B Microsoft offer 🚫

1:43:24 - Valuation today 🤔

1:44:19 - second takes

thank you for watching our very bad podcast on VC secondary

4

11

7,922

Practical Venture Capital retweeted

Jan 14

#TradingPlaces Pod: Top 5 Reasons People Sell #Secondaries in VC youtu.be/zUxf0y84gok?si=9gMR… via @TradingVCs cc #BenBlack #AkkadianVC @raiseconference

5

2

8

2,903

Practical Venture Capital retweeted

23 Dec 2025

Episode 17 of Trading Places Pod featuring @JavierCAvalos of @CaplightData is out now!

This week: the IRS as your hidden secondary buyer, why banks need private market solutions, how platform acquisitions are reshaping secondaries, and whether AI companies are in a bubble or just getting started. Plus, @Oracle's cash flow crisis, @tiktok_us's $38B deal, and why mega VC funds might be destroying returns.

Hosts @davemcclure and @AmanVerjee dive deep with Javier Avalos, CEO and co-founder of Caplight, on the explosive growth in VC secondary markets, transaction data from $3.5B in deals, and why 83% of trading volume concentrates in just 15 companies.

[ timestamps ]

0:00 – cold open

1:04 – intro

[ tech & vc news ]

02:05 – TikTok new owners 🕺

07:07 – 2025 AI hype cycle review 🤪

10:02 – @ttunguz on AI junk bonds 🗑️

12:33 – @elonmusk launches DATA CENTERS IN SPACE!!! 🚀🛰️

14:29 – @lightspeedvp $9B megafund ⚡️

16:53 – Dragoneer raises $4.3B 🐉

17:39 – @OpenAI $750B val & deal with @amazon 💃

21:51 – @databricks $134B valuation 🧱

23:22 – @Waymo $100B val drive 🚕

24:14 – @Lovable, @unconvAI & @NotionHQ 💰

[ intvw: Javier Avalos / Caplight ]

30:27 – from Forge to Caplight 👨💼

35:30 – top 20 startups vs the rest 🌎

36:26 – $3.5B closed trade data in 2025 💵

39:07 – concentrated VC funds 🎅🏼

40:10 – good SPV check list ✅

[ val corner: xAI @ $230B ]

1:15:11 – what actually is @xai? 🤖

1:18:02 – financial analysis 📊

1:21:34 – xAI big backers 🧑🧑🧒

1:24:48 – which Elon company to back? 💸

Pod Highlights This Week:

Secondary markets = new exit option: Javier reveals Caplight is tracking $3.5B in closed trades in 2025—up 50% YoY—making secondaries a viable third leg alongside IPOs and M&A

Concentration is extreme: Top 5 companies = 54.7% of all trading volume; top 20 = over 80%; if you're not in the top 50, you're less than 10% of the market

AI pure play thesis: Only place to get direct AI model exposure—public markets bundle it with advertising, cloud, social media

Banks racing to acquire platforms: Schwab/Forge ($660M), Morgan Stanley/EquityZen, Goldman/Industry Ventures—if you don't have a private markets solution for clients, you're behind

SPV explosion: Now 50% of market activity (up from 15% in 2021) as mega AI rounds require co-investment vehicles—but beware triple-layer 4-and-40 structures

Oracle's cash flow crisis: Went from $14B free cash flow (2021) to NEGATIVE as CapEx commitments balloon—bet on OpenAI backfiring?

AI bubble or justified?: 25% of volume but 50% buyer interest; if more sellers come to market, 2026 could see even more deals

Mega funds destroying returns?: Lightspeed $9B, Dragoneer $4.3B—history shows mega funds underperform smaller strategic funds

Notion's patient playbook: Raised at $11B in 2021 bubble (100x revenue), then grew revenue 10x to "only" 20x multiple—rare flat round success

@ at $230B: Is this about Elon's network or fundamentals? Valor, Ira, Jensen, Sequoia, a16z all in—do you bet with or against them?

Javier's insider wisdom: "If you're buying a triple-layer SPV with 3-and-30 that closes in 24 hours, just say no—there's no FOMO worth that"

IRS = secret liquidity: Donating underwater 2021 vintage to DAFs can generate 30-50¢ on the dollar in tax savings vs holding to zero

The Trading Places Podcast is a Practical Venture Capital production.

3

6

9,174

Practical Venture Capital retweeted

16 Dec 2025

Episode 16 of @TradingVCs featuring Adrien Gautier of Bridgespan VC is out now!

This week: @Oracle's debt crisis sends shockwaves through AI infrastructure stocks, the IPO market heats up for 2026 with @SpaceX, @OpenAI & @AnthropicAI eyeing historic exits, and Adrien Gautier reveals how Bridgespan's unique employee stock option financing strategy gets them 30-70% discounts vs. preferred share pricing 💰

Hosts @davemcclure and @AmanVerjee break down market volatility, the Fed's rate cut uncertainty, Oracle's leverage problem, and the explosive IPO pipeline for 2026—before diving deep with Adrien Gautier on how employee stock option financing creates a capital-efficient secondary strategy with built-in downside protection.

In Valuation Corner, the team tackles the autonomous vehicle wars: @Waymo vs. @Tesla vs. @AppliedInt vs. the rest of the auto industry, exploring whether software-first companies deserve their premium valuations and why traditional OEMs can't catch up.

[ TIMESTAMPS ]

00:00 – cold open

00:53 – [ tech & vc news ]

01:15 – Oracle’s bad week

06:09 – 2026 IPO market

11:49 – SpaceX IPO update

13:15 – @Wealthfront flat IPO

14:56 – @Medline $55B valuation

22:51 – @boomsupersonic raises $300M

23:49 – @GoldmanSachs invests in Harness at $5.5B

25:19 – New fed chair & rate cuts

30:44 – Invest Act coming soon

33:07 – China rejects US @nvidia H200s

35:43 – [ interview: adrien gautier / bridgespan ]

36:12 – Bridgespan VC focus

42:15 – tender offers

43:24 – when can companies IPO

46:16 – @EquityBee partnership

47:54 – portfolio management strategy

1:12:45 – [ val corner: waymo @ $45B ]

01:28:29 – second takes

POD HIGHLIGHTS THIS WEEK:

-Oracle's leverage trap: 500% debt-to-equity ratio means a 50% drop in enterprise value = 60% equity wipeout. Credit default swaps hit highest since 2008

-2026 = IPO supercycle: SpaceX ($800B), OpenAI ($500B), Anthropic ($350B) could each break Alibaba's $25B IPO record

-Bridgespan's edge: Employee stock option financing gets 50-70% discounts vs. latest preferred rounds—with non-recourse downside protection

-6 exits in year 1: Bridgespan's Fund I generated DPI from 36 investments, with Firefly Aerospace delivering 10x in 60 days

-Disney OpenAI = new playbook: Characters licensed to Sora (minus voices)—Ursula's contract confirmed

-Fed uncertainty: Only 8-10 of 12 voters likely support December rate cut; jobs data showing negative growth 3 of last 5 months

-Invest Act passes: House approves 49% secondary cap for VC funds (up from 20%), 250→500 LP limit, $10M→$50M emerging manager threshold

-Tender offer trends: Now standard for companies $10B with $100M revenue—Bridgespan's primary exit strategy alongside IPOs

-Autonomous driving wars: Tesla/Waymo trade at 15x revenue; GM/Ford at 0.5x. Software > hardware. @helm_ai aims to democratize FSD for legacy OEMs

-Adrien's wisdom: "If you don't like the public market valuation 6 months post-IPO, we may hedge. But our strategy? 1) sell at lockup 2) return capital to LPs 3) repeat."

4

5

7,216

Practical Venture Capital retweeted

15 Dec 2025

Dave McClure tries to count Bay Area millionaires.

Ben Black explains why so many of them are stuck with illiquid bags and why they call wealth managers for help.

"At least one out of 10 of them hits the big time... we're talking at least, I would say tens of thousands of people who have illiquid position concentrated in a single asset."

— @davemcclure & @benjamindblack on @TradingVcs Ep.15

3

6

1,412