No-Code Embedded Finance. #EmbeddedFinance #Fintech #APIs #Banking #Payments

Joined November 2017

- Tweets 3,173

- Following 64

- Followers 9,139

- Likes 862

854 Photos and videos

Small Move, Big Impact: @Plaid’s API Migration Paves the Way for U.S. Open Banking Revolution

spr.ly/6017OgQSR

1

1

3

1,370

Hydrogen retweeted

13 May 2023

QED Partner and Head of Europe Yusuf Ozdalga (@yusufozdalga) shares why he's excited about three key #fintech themes:

1⃣ Embedded finance

2⃣ Back-office automation

3⃣ Cross-border payments

Full video: qedinvestors.com/blog/video-…

10

18

4,023

Hydrogen retweeted

12 May 2023

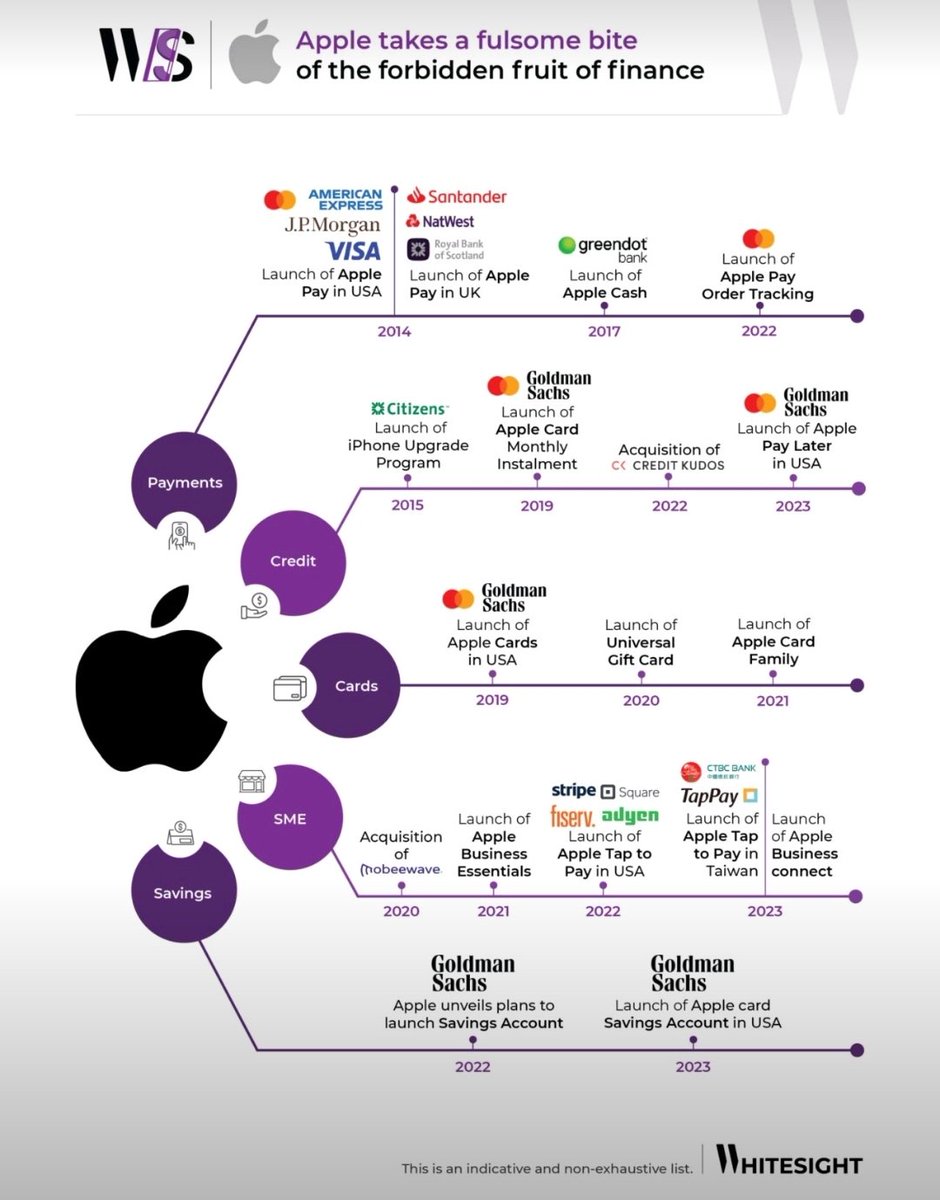

From iPhone to iBank: Analysing Apple’s Embedded Finance Initiatives #fintech

buff.ly/3I4jK1v

8

18

4,094

Hydrogen retweeted

10 May 2023

Top #fintech influencers and newsletters to follow in 2023

bit.ly/3Mdbn5Z

h/t @RAlexJimenez @SpirosMargaris @bayareawriter @sytaylor @mikulaja @LexSokolin @YuHelenYu @NikMilanovic @efipm @rshevlin @stratorob

3

5

16

1,719

Hydrogen retweeted

11 May 2023

"Over 50% of our sales are in embedded finance."

— Simon Khalaf, Marqeta

#nexus2023 #fintechnexus #keynote @Simonkhalaf @AllenOvery

2

5

563

Hydrogen retweeted

5 May 2023

Looking for insight into open banking? Read our white paper to learn how open banking is transforming the banking sector and unlocking a growing Banking as a Service market: bit.ly/41BcCl1

1

1

368

Hydrogen retweeted

6 May 2023

Reach new customers with embedded banking and Banking-as-a-Service (BaaS). Author and expert Matthias Biehl explains how. View the webinar: bit.ly/3YSbhUM

#baas #fintech #webmethods

2

2

605

Hydrogen retweeted

3 May 2023

Banking as a Service and Embedded Finance are in crossroads.

I’ve been thinking lately whether the current, popular business model needs to evolve and how. So I wrote something about it.

#embeddedfinance #bankingasaservice #fintech #businessmodels

fttembeddedfinance.com/shoul…

3

4

9

1,094

Hydrogen retweeted

30 Apr 2023

Banking as a service: the key to the future of financial institutions

Read more ➡️tinyurl.com/274e6de8

#BankingAsAService #Fintech #FinancialInnovation

1

290

Banking-as-a-Service is transforming the lending industry, enabling traditional banks to partner with fintech and non-banking companies to improve their services and stay ahead of the competition. bit.ly/424QWO4 #BaaS #BankingAsAService #Fintech #DigitalBanking

2

1

241

Hydrogen retweeted

2 May 2023

Banking-as-a-Service represents a $7 trillion market opportunity, yet FI leaders remain split on how to implement a #BaaS framework that delivers ROI. Our BaaS playbook shares how to achieve a model for FI revenue growth: bit.ly/3UiaJ9R #bankingasaservice

4

17

1,197

Hydrogen retweeted

4 May 2023

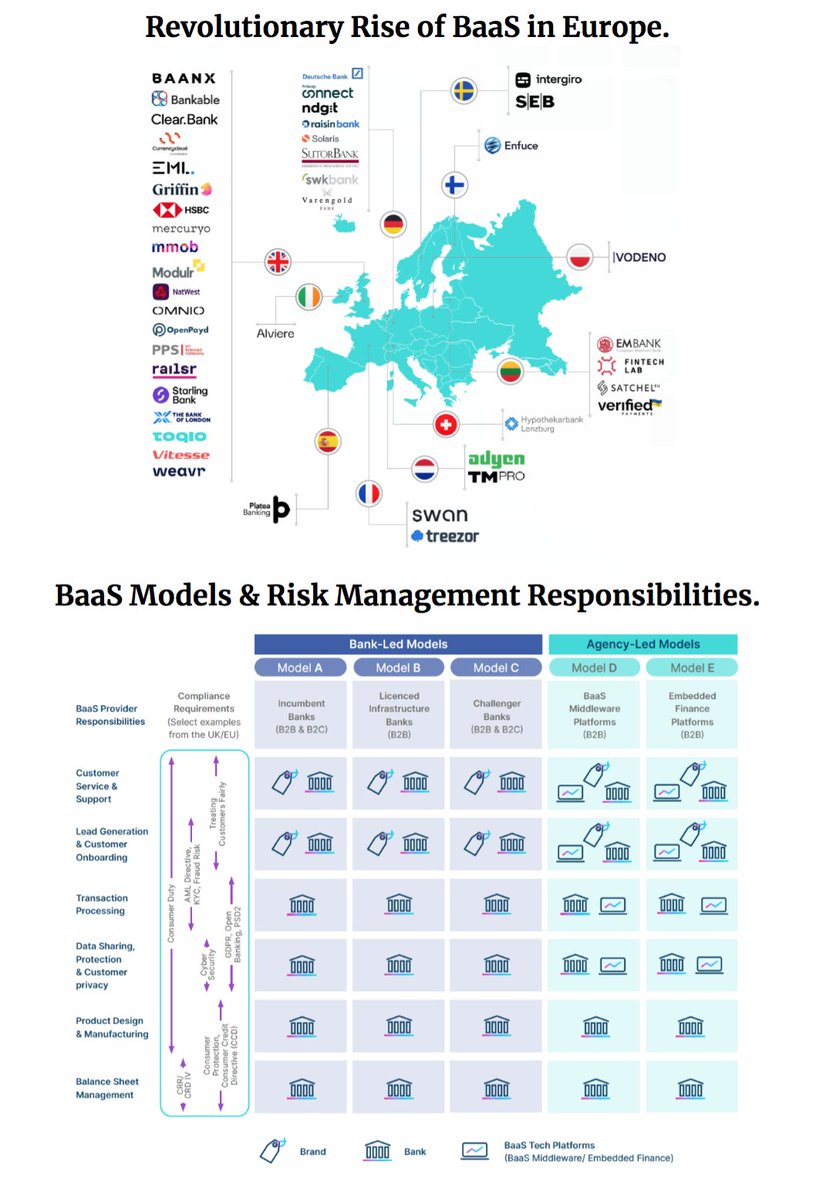

The State of Banking-as-a-Service in the UK & Europe

bit.ly/3p7RLqX

@WhiteSight_

#Innovation #Fintech #Banking #Neobanks #OpenBanking #EmbeddedFinance #OpenAPIs #BaaS #FinServ #CoreBanking #Payments #Cloud #SaaS #KYC #AML

3

9

589

Hydrogen retweeted

1 May 2023

Banks Not Delivering the Financial Wellness Tools Consumers Crave.

bit.ly/42897Tn

#banking #fintech #PFM

@SpirosMargaris @rshevlin @HaroldSinnott @jblefevre60 @Xbond49 @TheRudinGroup @psb_dc @EvanKirstel @KirkDBorne @helene_wpli @efipm @sallyeaves @personetics @forrester

2

26

26

5,125

Hydrogen retweeted

9 May 2023

How #EmbeddedFinance

Is Revolutionising #FinancialServices in #SoutheastAsia

fintechnews.sg/72383/sponsor… #fintech #finserv #banking @FintechCH @FintechSIN

8

5

1,497

Hydrogen retweeted

9 May 2023

Discover how BaaS and #embeddedfinance are changing the game for #businesses and #consumers alike!

Kanika Hope, chief strategy officer at @Temenos , explores what this means for the future of #financialservices.

Click here to read more 👇

fintechfutures.com/2023/05/i…

2

862

9 May 2023

Notice to Crypto Asset Trading Platforms to Remove HYDRO Smart Contracts Ending afBa and 49bc. Please see the list of crypto asset trading platforms requested to comply with the order on our website here: hydrogenplatform.com/blog/no…

2

5

223

Hydrogen retweeted

The rise of Banking-as-a-Service and embedded finance is signaling the end of #finance and banking as we know it, in a twist that entails both a threat and an opportunity. Let’s take a look.

While the term embedded finance is relatively new, its precursors have been around for decades (i.e. store and branded credit cards offered by retailers or airlines). In these cases, traditional financial products were offered via alternative channels or different branding, but without the embedded concept. The game changer today is the ability to directly integrate financial offerings into any (non-finance) environment, via interactive distribution rails that we call #APIs.

BaaS and embedded finance are often used interchangeably but are not the same thing: BaaS is the bottom, infrastructure layer that feeds into the various embedded finance offerings on the outcome, front-end side. The combination of these two distinctive layers into one unique (bundled) offering is a paradigm shift that builds and further expands on a revolutionary development that has been driving the FinTech revolution of the past years and is an equally disruptive "embedded" force: the decoupling of the customer experience from infrastructure.

In such an environment, we are witnessing the metamorphosis of a few, scattered, fast-moving concepts into business models that are gradually re-writing the #future of the industry. And whereas there is a multitude of variations to be found across the entire end-to-end spectrum, they are all defined by two major parameters:

— Licensing together with all the obligations connected to it (compliance, risk #management, balance sheet, etc)

— A back-end #technology stack than seamlessly connects to diverse environments acting as an enabler

The diversity of the models on the market today is directly linked to the fact that whereas both parameters are needed to synchronize in a bundled way, they do not (necessarily) have to be offered by the same provider. From traditional banks leveraging (only) their #banking license to #FinTechs acting as #technology bridges to full stack #BaaS players leveraging both #licensing and technology in end-to-end vertically integrated models to niche providers or to segment specialists, the sheer number of combinations is telling.

To cast further complexity, in many cases layers can be added or removed depending on the positioning of the partners along the value chain: i.e. Goldman Sachs’ partnership with Apple is a classical #B2B2C offering, whereas Stripe operates with Stripe Treasury a B2B2B2C set-up, where Stripe acts as a provider in its own right behind marketplaces or platforms (i.e. }#Shopify).

In a world where customers are increasingly making #finance decisions in non-financial contexts, we have just started scratching the surface of embedded finance's potential and the myriad ways in which it is changing business and the #economy.

#GSB #Revolut #SEB #Amazon #Apple #ebay #bmw #BBVA #HSBC

1

7

386

Hydrogen retweeted

5 May 2023

Embedded finance offers significant opportunities for banks to generate new revenue streams and enhance the user experience.

Read more 📑tinyurl.com/27rdz7nk

#embeddedfinance #fintech #banking

1

259

Hydrogen retweeted

1 May 2023

Embedded Finance at scale 🤩

Apple's saving account reached $1B in deposist in... only 4 days!

What a competitive edge third parties have in terms of distribution over pure FinTech players.

And that's another data point supporting tech giants' move into Financial Services.

4

4

23

2,656

Hydrogen retweeted

2 May 2023

Discover how banks can leverage Banking as a Service (BaaS) and Embedded Finance to provide a wider range of financial services.

#fiorano #financialservices #digitalbanking #openbanking #banks #apimanagement #api #baas #embededfinance #apibanking

2

1

238