Joined June 2013

- Tweets 301

- Following 485

- Followers 53

- Likes 969

13 Photos and videos

2(-)! retweeted

大摩爆雷级报告:AI时代HDD不是夕阳产业,而是被低估的“数据粮仓”!

短缺直至2028年,希捷&西部数据目标价大涨很多人疑问:AI不是靠HBM、高带宽内存和GPU吗?机械硬盘HDD这么“老古董”,为什么在AI时代反而大缺、大涨?

答案很简单——AI需要的是“分层存储”:

HBM/GPU → 负责高速计算和即时推理(热数据)

企业级SSD → 负责高频访问的热/温数据

近线HDD → 才是AI数据洪流的真正“粮仓”!

它以极低成本存储海量冷/温数据(训练数据集、模型检查点、合成数据、推理日志、归档备份等)

据行业数据,云端80%左右的数据仍依赖HDD存储。

AI每训练一次大模型,就产生PB级甚至EB级的残留数据,这些不需要毫秒级访问,但必须长期、低成本保存。

HDD的每TB成本和容量密度仍是SSD无法替代的,TCO(总拥有成本)优势显著。AI巨头的“数据爆炸”直接把HDD从“夕阳”拉回“新贵”赛道。

摩根士丹利最新亚洲渠道调研(6月16日发布)直指:

近线HDD短缺至少延续至2028年,2026-2028年缺口持续扩大(2026年约300EB,后续或达400EB)。

需求:

年增长40%-50%

AI推理、智能体应用、云服务扩张 高容量新品刺激

供应:

年增长仅30%-35%

厂商谨慎,未新建绿地产能,2026年产能已基本售罄

定价大幅走强:

当前近线HDD低于每TB 15美元,厂商内部目标2027-2028年抬升至每TB 25-30美元(接近翻倍),提价更有秩序性和可持续性(NAND价格大涨也给HDD厂商更多底气)。

利好股票(大摩Top Pick):

希捷科技 (Seagate, blockstack:native ):

目标价从767美元上调至1035美元,维持增持。

西部数据 (Western Digital, $WDC ):

目标价从488美元上调至650美元,维持增持。

报告发布后,两股昨日齐创历史新高(西数一度涨超16%)。

大摩强调:

在乐观定价情景下,两家公司2025-2028年EPS有望增长10倍!HDD已成为其IT硬件领域“最看好的AI敞口”。

总结:

AI不是只烧GPU和HBM,而是全栈基础设施狂欢。

HDD作为底层海量存储,周期被AI强力拉长,盈利与估值中枢将显著抬升。这不是夕阳反弹,而是长期新周期起点!

3

8

1,707

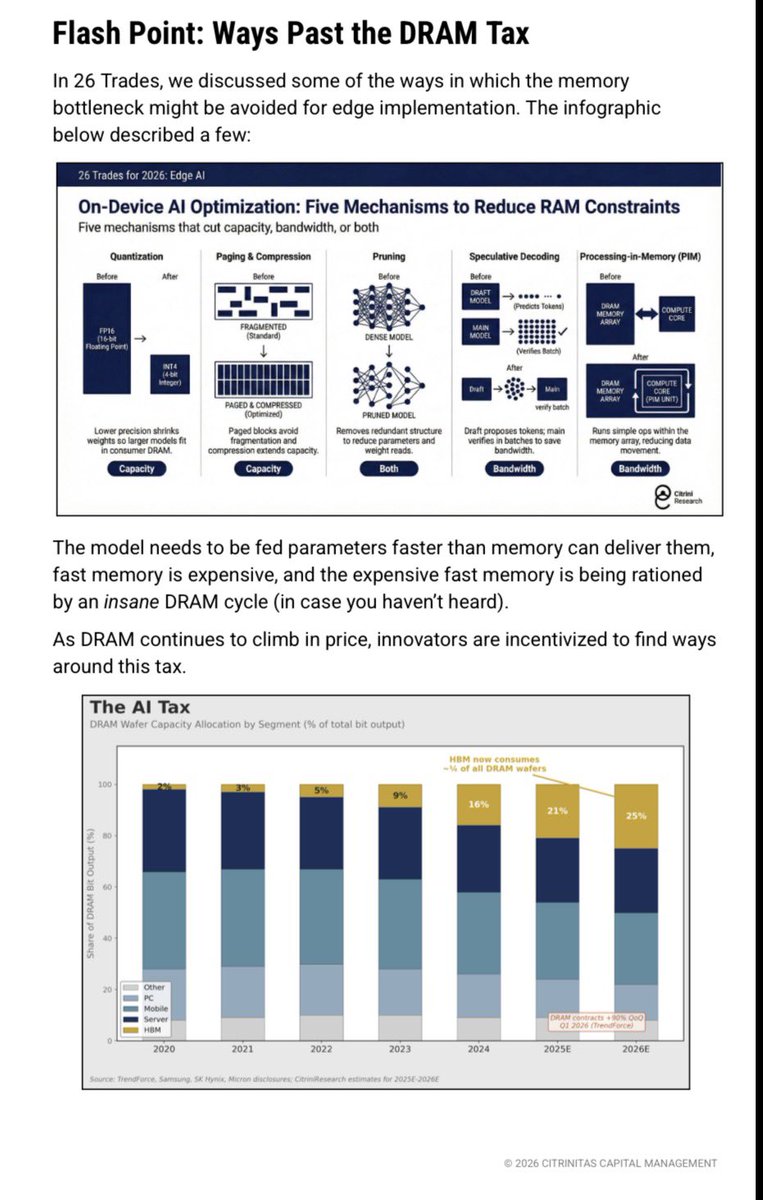

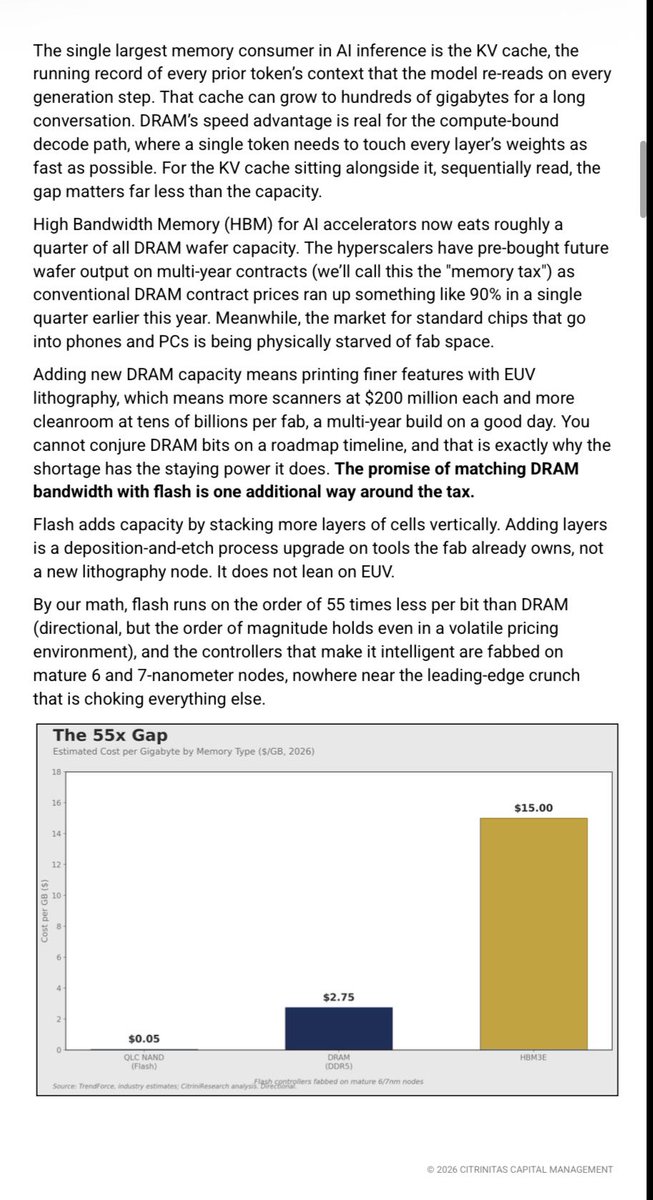

AMD and AAPL both, in different ways, have announced a focus on flash as a way to reduce the AI memory tax. We wrote about this in our State of the Themes last week.

Jun 15

$AMD is acquiring MEXT, an AI-driven memory optimization company for data center infrastructure. MEXT’s tech helps make flash storage behave more like DRAM, expanding usable memory capacity while maintaining performance.

24

84

895

193,221

2(-)! retweeted

Jun 15

AI太空算力產業

太空數據中心/軌道AI計算是將AI算力從地面遷移到低地球軌道(LEO)的新興賽道,主要利用太空的持續太陽能(無晝夜限制)、天然散熱(真空環境)和低延遲星間/星地通信,解決地面數據中心面臨的電力、土地、散熱和能耗瓶頸。

SpaceX( $SPCX )是當前最受關注的玩家,馬斯克計劃部署大量AI衛星(如AI1設計,單星峰值150kW算力),目標是構建軌道AI數據中心星座,甚至百萬顆規模,與Starlink網絡協同。

產業構成(主要環節)

產業鏈較長,融合航天、半導體、通信、能源等多領域,核心優勢在於抗輻射芯片、高效供能散熱、星間激光通信和低成本發射。

1上游:芯片與算力模塊

抗輻射加固AI芯片/GPU(太空環境輻射強,普通芯片易失效)

代表:英偉達(NVDA,與Starcloud合作送H100上天,後續Space-1 Vera Rubin模塊);谷歌TPU;SpaceX/Tesla自研D3芯片(專為太空優化)

2衛星平台與製造

衛星結構、總裝集成、熱控系統。

代表:SpaceX(垂直整合)、中國衛星、航天智裝、銀河航天、國星宇航等

3能源系統

太空太陽能電池/組件(高轉換效率,如砷化鎵)、電源管理

代表:乾照光電(300102.SZ)、上海港灣等;SpaceX AI衛星依賴大型太陽能陣列。

4通信與互聯

星間/星地激光通信、射頻模塊、高頻PCB

代表:光迅科技、華為/中興相關、通宇通訊;SpaceX激光鏈路。

5發射與運載

低成本火箭發射(Starship是關鍵降本利器)

代表:SpaceX、Rocket Lab ( $RKLB )

6下游應用與服務

在軌數據處理、實時遙感AI、算力租賃、地球觀測等

代表:中科星圖、航天宏圖、BlackSky (BKSY)等

其他環節:

散熱系統、新材料、抗輻射元器件、地面站等

美股/國際

SpaceX ( $SPCX ):

核心標的,已IPO,市值曾超Broadcom和Tesla,AI衛星是增長敘事重點

NVIDIA ( $NVDA ):太空GPU/模塊供應商,生態延伸至軌道

Broadcom ( $AVGO ):AI芯片/網絡,可能間接受益(圖像中提到)

Rocket Lab ( $RKLB ):發射服務

Northrop Grumman ( $NOC )、Lockheed Martin ( $LMT ):航天系統集成

其他: $HPE (在軌計算)、 $CACI(星間鏈路)等

A股/港股/台股概念股(中國佈局活躍)

能源/電池:

乾照光電(300102.SZ)

衛星/航天:

中國衛星(600118.SH)、航天智裝(300455.SZ)、中科星圖(688568.SH)、航天宏圖(688066.SH)、航天環宇

通信/PCB:

通宇通訊、華通、燿華等(台股)

其他:

順灝股份(002565.SZ,數據中心項目)、普天科技、歐比特(抗輻射芯片)、光迅科技

台股供應鏈(低軌衛星延伸):

昇達科(射頻)、元晶(太陽能)等

1

4

719

2(-)! retweeted

Jun 14

2,796

7,887

40,019

64,503,404

2(-)! retweeted

3 Dec 2025

🚨There is a ton of momentum building in photonics right now.

$POET $MRVL $LITE $COHR $AAOI $TSEM $CIEN

Every part of the stack is heating up, and management teams have basically spent the last month broadcasting the same story.

Let’s dig into some of the recent bits I’ve been watching...

$LITE

Q1 revenue up 58% YoY to $533.8M with next quarter guided to ~$650M, hitting their mid-2026 target two quarters early.

Management pointed to cloud-optics demand running well above supply with transceivers, optical circuit switches, and early co-packaged optics driving the next leg.

$COHR

“AI data centers and communications remain strong long-term growth drivers.”

They just posted $1.58B in revenue, 17% YoY, and highlighted accelerating hyperscale DCI demand across their ZR / ZR lineup and their 400G / 800G ramps.

$MRVL

“AI infrastructure is transforming faster than ever.”

“We’re going to have a silicon-photonics powerhouse at Marvell when this is all done.”

The $3.25B Celestial AI acquisition comes with a modeled $500M run-rate by FY28 and $1B by FY29

Celestial AI

“Marvell is the ideal home for our Photonic Fabric… the scale and customer reach to take this platform into high-volume production.”

$POET

Their optical-engine technology is already designed into Celestial AI’s Photonic Fabric, the same platform Marvell just paid $3.25B to acquire.

As AI systems move toward denser, more integrated optical engines, POET sits directly inside one of the most advanced photonics architectures in the market - now part of Marvell’s silicon-photonics roadmap.

$AAOI

Revenue up 82% YoY.

They’re on track to build what they believe will be the largest domestic production capacity for 800G and 1.6T transceivers by year-end, roughly 35k parts per month, all inside their Texas footprint.

$TSEM

Expecting silicon-photonics revenue to more than double off last year’s base.

They’re investing $300M into photonics and AI-focused expansion and calling for ~75% growth in that segment.

$CIEN

“We delivered record orders. Cloud and AI providers continue to invest in high-capacity optical transport.”

DCI and long-haul momentum continue to show up directly in the numbers.

...

But you can’t just look at the transceiver and laser makers.

Some of the clearest signals are coming from the companies building the architecture and the supply chain behind it.

$AVGO

AI revenue moving from ~$11B to $20B .

They’re doubling down on silicon photonics

Controlling the switch silicon, the optical DSP, and the optical engines at the heart of modern AI racks.

If you’re bullish on photonics, this is one of the companies defining the socket.

$ANET

Building the “AI spine.”

Their Ethernet-based AI networking platform relies entirely on high-speed optics to stitch together massive GPU clusters

100k-GPU scale and up.

As clusters get larger, copper falls out of the system and optics takes over.

$FN

Record ~$980M in revenue.

They manufacture optical engines for some of the largest players in the space - $NVDA, $LITE, $COHR, and others.

When Fabrinet says demand is exceptional, it means the orders are already in the building.

$GLW

Optical Communications revenue up 33% YoY.

AI racks require roughly 10x the fiber density of legacy cloud racks.

Corning is supplying the physical layer that makes 800G and 1.6T optics viable at scale.

$SMTC

Solid print tied to growing traction in Linear Pluggable Optics (LPO).

They sit in the analog layer, drivers and TIAs that fire the lasers, and are positioned directly under the 800G / 1.6T cycle.

$MTSI

Revenue up 30% YoY.

They build the high-speed analog components that sit behind next-gen optical engines and are essential for 1.6T designs.

....

This is all widespread.

It’s lasers, transceivers, optical switches, silicon photonics, scale-up fabrics, DCI, long-haul transport, Ethernet AI spines, fiber density, and the analog chips behind every laser all moving in the same direction.

If you’re tracking AI infrastructure, photonics continues to gain strength week after week.

47

184

958

523,283

2(-)! retweeted

$AMKR (Amkor Technology, Inc.) 是全球最大的美國總部 OSAT(外包半導體組裝與測試)公司,成立於 1968 年,總部位於亞利桑那州 Tempe

它專注於半導體價值鏈的後段製程:將晶圓廠(fab)生產的晶圓,進行封裝(packaging)、測試(test),並轉化為可直接組裝到電子產品上的成品晶片。Amkor 是先進封裝領域的重要玩家,尤其受益於 AI、高性能運算(HPC)、5G、汽車電子和消費性電子需求。

主要業務與商業價值核心服務:

先進封裝(Advanced Packaging,如 High-Density Fan-Out HDFO、2.5D/3D 整合、System-in-Package SiP)、Flip Chip、Wafer-Level Packaging、Wirebond、功率封裝,以及完整測試服務。

先進封裝占比:

已成為主要成長引擎,約占營收 75% 左右,高毛利、高技術含量。傳統 Wirebond 仍占一定比例,但公司正積極轉型。

終端市場:

通訊(含手機,約 46%)、消費電子、運算(AI/HPC)、汽車與工業。AI 伺服器和高性能晶片是關鍵成長動能。

商業價值:

Amkor 是晶片從裸晶到可用產品的關鍵橋樑。

AI 時代下,先進封裝已成為系統性能瓶頸(chiplet 整合、散熱、訊號完整性),Amkor 因此成為供應鏈 choke point(關鍵節點),議價能力提升。

2025 年全年營收約 67 億美元(YoY 6%),2026 Q1 營收 16.85 億美元(YoY 27%),毛利率約 14.2%。公司積極擴產(2026 CapEx 25-30 億美元),特別是美國亞利桑那廠。

長期來看,AI 帶動先進封裝 CAGR 高成長,公司定位為 TSMC 等晶圓廠的互補夥伴,提供高容量、先進封裝解決方案。

護城河(Moat)Amkor 有以下幾大競爭優勢:

技術與 IP 護城河:

擁有 3000 項專利,專有技術如 S-Connect(矽橋接技術,提升訊號完整性與散熱)、S-SWIFT(高密度扇出)、HDFO 等,在 AI 加速器和 HPC 晶片上有優異性能。早期與客戶共同開發(co-development),形成高轉換成本

美國本土優勢:

唯一具規模的美國總部 OSAT,在亞利桑那興建大型先進封裝廠(Phase 1 預計 2028 量產,總投資數十億美元,獲 CHIPS Act 支持)。這對 Apple、NVIDIA、AMD 等追求供應鏈安全(去風險化)的客戶極具吸引力,是對抗中國 OSAT 的關鍵差異化。

全球足跡 規模:

亞洲(韓國、越南、菲律賓等)有成熟產能,美國新廠補足地緣風險。長期客戶關係(30 年,含 Qualcomm、Broadcom 等),高良率製程降低客戶風險。

資本密集 執行力:

先進封裝需要巨額投資與 know-how,新進者難以快速追趕。

毛利率目前仍低於晶圓代工(TSMC ~50% ),但先進封裝占比提升正帶動毛利擴張。主要競爭對手OSAT 市場高度集中,前幾大占大部分份額:

ASE Technology Holding(日月光,全球最大):

規模最大(營收遠高於 Amkor),技術全面,但在美國本土布局較弱。Amkor 在先進封裝與美國優勢上更具差異化。

JCET(江蘇長電):

中國主要玩家,成本優勢明顯,但地緣政治風險高,受美中緊張影響。

其他:

Siliconware Precision(SPIL,已與 ASE 合併)、Powertech、中國其他 OSAT 等。

間接競爭:

TSMC、Intel、Samsung 等晶圓廠的內部先進封裝能力(例如 TSMC CoWoS)。這些廠商掌控最尖端部分,但容量有限,Amkor 常作為補充或合作夥伴。

Amkor 相對優勢:

美國布局 對 fabless(無晶圓廠)客戶的靈活性高;缺點是規模略小於 ASE,毛利率仍有提升空間。

總結與風險Amkor 是 AI 基礎設施的重要受益者,先進封裝需求強勁、美國本土化趨勢助攻,長期商業價值高。

2

17

5,435

2(-)! retweeted

May 29

What's happening in the MLCC market

First off, MLCC as a whole is a $15B market. MLCCs for servers were a $1.3B market in 2025 ($600m for AI servers, $700m for general servers)

The AI server MLCC market is growing at 80% CAGR, and the general server MLCC market will also accelerate due to agentic AI increasing CPU demand (around 30%-40% CAGR)

We will see negative growth in the smartphone/mobile MLCC market for at least 2026-27.

Humanoids are another future high-growth market for MLCCs

Book-to-bill ratio for most MLCC suppliers is over 1 now

Reasons for price hikes-

High Nickel & Silver are affecting all segments

There is a supply-demand mismatch in the high-end (high capacitance, high voltage) segment, which is used in autos & servers

High-end MLCC lead time is over 20 weeks

Spot/distributor prices have increased by 20%-40% for low capacitance & consumer device MLCCs due to hoarding and double booking, especially in China

OEM contracts have not seen large price hikes yet

What's happening now:

Rapid capacity expansion happening across the industry

Murata expects blended ASP prices to remain flat (ASP going down in consumer electronics, expansion in AI server market)

Tier 1 players like Murata, Taiyo Yuden, SEMCO building capacity to serve AI server MLCC market

This will create opportunities for Tier 2/3 and Chinese suppliers to expand in the mid to low end market (Macronix effect)

Future:

MLCC production equiment & raw materials suppliers will be the biggest beneficiary of this CAPEX boom

MLCC producer stocks have performed well, and it is finally spilling to raw material/equipment producers

I expect them to outperform MLCC producers now

30

254

1,502

620,570

半導體測試設備製造商正面臨前所未有的零組件危機,甚至出現「沒有半導體能製造測試設備」的窘境。

根據5月29日業界消息,FPGA交期已從原本8-10週暴增至最長52週,由AMD主導的市場供應極度吃緊;測試用驅動IC(Analog Devices為主)也從現貨變成至少10週交期。x86伺服器CPU與GPU同樣短缺,英特爾Xeon處理器因優先供應資料中心大廠,導致其他市場貨源銳減,價格更暴漲最高3倍。下一代Xeon「Diamond Rapids」量產時程也延後至明年中,直接衝擊新一代測試設備開發。

某廠商與三星簽下逾100億韓元合約,卻因零件短缺被迫延遲交貨3個月。業界指出,這已非單一零件問題,而是整個非記憶體半導體供應鏈全面瓶頸。

主因來自AI與資料中心投資熱潮,同時推升晶片與測試設備需求。設備商已提前數月與客戶討論訂單以鎖定零件,但供應仍難穩定。業界預期短缺將持續一段時間,晶片廠與設備商須更緊密合作才能因應。

May 30

FPGAがついに不足してきた

特に産業機器は痛い

半導体試験装置メーカーが「史上最悪」の部品不足に直面

FPGAのリードタイムは52週間にまで延びており、供給ボトルネックはメモリ以外のチップにも広がっている。

半導体試験装置メーカーは深刻な部品供給不足に直面しており、「半導体試験装置を製造するための半導体が入手できない」という不満の声が上がっている。

業界関係者によると、5月29日時点で、半導体試験装置に使用される主要部品の調達状況が急激に悪化している。フィールドプログラマブルゲートアレイ(FPGA)、中央処理装置(CPU)、ドライバ集積回路(IC)などの非メモリチップのリードタイムが大幅に延びている。

テストシステムに使用されるFPGAのリードタイムは、以前は約8~10週間だったのが、最近では52週間にも及んでいる。「リードタイムは仕様によって異なりますが、多くは52週間前後です」と販売代理店の担当者は述べた。「供給状況は極めて困難になっています」。FPGAは、検査データをリアルタイムで分析し、欠陥を迅速に特定するために使用される。この市場は、AMDがXilinxを買収して以来、AMDが圧倒的なシェアを占めている。

試験装置用ドライバICも同様の供給不足に直面している。以前は販売代理店を通じてすぐに入手できたこれらのチップも、現在では少なくとも10週間かかるようになっている。特にアナログ・デバイセズの自動試験装置(ATE)向け製品群は深刻な供給不足に陥っている。同社は半導体試験システムで使用される集積型ピンドライバを供給している。

供給不足はx86ベースのCPUやグラフィックス処理ユニット(GPU)にも影響を及ぼしている。「一部の製品は入手が非常に困難になり、価格が100万ウォン前後から300万ウォンへと3倍にまで高騰している」と半導体製造装置業界関係者は述べた。「特にインテルのサーバー用CPUは入手が困難だ」。

インテルの次世代Xeon CPU「Diamond Rapids」の量産開始時期が、今年後半から来年半ばに延期された。(出典:インテル)

インテルは最近、Xeonサーバープロセッサの供給を高収益のハイパースケーラーやデータセンター事業者に優先的に提供しており、他の市場への供給を制限している。また、インテルの次世代Xeonプロセッサ「Diamond Rapids」の量産開始時期も、今年後半から来年半ばに延期された。この遅延は、プロセッサの高性能化と新機能を必要とする次世代テストシステムの開発および出荷スケジュールに影響を与えている。

ある事例では、半導体検査装置メーカーがサムスン電子と100億ウォンを超える供給契約を締結したが、部品不足のため納入を3ヶ月延期せざるを得なくなった。「現状はFPGAやCPUといった特定の部品の不足だけにとどまらない」と業界関係者は語る。「メモリ以外の半導体サプライチェーン全体で深刻なボトルネックが発生している」。

機器メーカー各社は、部品の発注時期を早めることで対応しようとしている。正式な発注書が確定する数ヶ月前から、顧客と機器の数量や納期について協議し、部品を事前に確保しようとしているのだ。しかしながら、納期遅延の悪化により、安定供給は依然として困難な状況にある。

業界関係者は、AIとデータセンターインフラへの投資が活況を呈する中で、半導体と半導体試験装置の需要が同時に増加していることから、試験装置に使用される非メモリ部品の供給不足が当面続くと予想している。

半導体メーカーが試験装置を購入する際も、プレッシャーにさらされている。「半導体メーカーと装置メーカー間の緊密な協力と積極的な対応は、ますます新たな常識になりつつある」と業界関係者は述べた。

7

18

145

24,560

2(-)! retweeted

May 27

所有跟单Serenity的,再次隆重介绍一个专门针对他的监控网站给你们:

analysissite.vercel.app

详细得不得了

123

520

2,812

310,259

2(-)! retweeted

May 26

UBS Raises $MU PT to $1,625 from $535, Maintains Buy Rating

Analyst comments: "With LTAs now firmly in place across most of the industry, we are again raising C2027-2029 estimates and expect EPS to remain comfortably >$100 throughout the period, with MU generating over $400B in FCF across the same timeframe. We believe the market will start to put a more normal multiple on the stock, and MU will continue to re-rate higher as more details emerge about the structural changes AI has driven to the entire memory complex. Our supply chain work on Long Term Agreements (LTAs) across the memory industry suggests that up to 30% of DDR volumes industry-wide will soon be locked in at pricing that is just slightly below current levels, and these agreements will allow MU to trade some near-term revenue for demand visibility and a smoother earnings profile. Consequently, we are raising EPS across C27/28/29E to $155/$167/$117 from $133/$122/$77 prior. Considering that investors typically reward stocks for durability and visibility, we see MU’s EPS remaining >$100 through C2029E as testament to the sort of lasting, structural change that should support a shift toward a broader semi multiple. Net, we lift our PT from $535 to $1,625, now based on ~15x NTM P/E versus prior SoTP on C2029E EPS of $117, one-year discounted, and reiterate Buy.

We now expect the DRAM industry to remain undersupplied until at least C2Q28 versus 4Q27 prior, and NAND undersupply to last until 4Q27 versus 3Q27 prior. An additional driver of upside versus our prior model stems from higher HBM ASP ($/GB) assumptions, something we highlighted already early in April, as MU/SK/Samsung intend to rebuild a premium for HBM pricing into C2027, leading us to now model MU HBM ASP up ~50% Y/Y versus 35% Y/Y prior on unchanged MU HBM bit shipment assumptions of 7.78B Gb for C2026 and 12.05B Gb for C2027. Into CQ3:26, our industry model now also considers the impact of LTAs, as primarily reflected in the magnitude of the quarterly DDR, up ~8% Q/Q, and NAND, up ~9% Q/Q, industry contract pricing increase. This implies Q/Q pricing growth now normalizing back toward the low SD% range after three consecutive quarters of pricing increases averaging >50%."

Analyst: Timothy Arcuri

32

134

865

331,017

I wasn’t planning to share this, but it’s such a high-quality explanation of CPO that I have to.

Just watch it. You’ll regret it if you don’t.

youtu.be/wiH6d4m9o4o?si=hwEO…

38

214

1,268

204,837

2(-)! retweeted

May 24

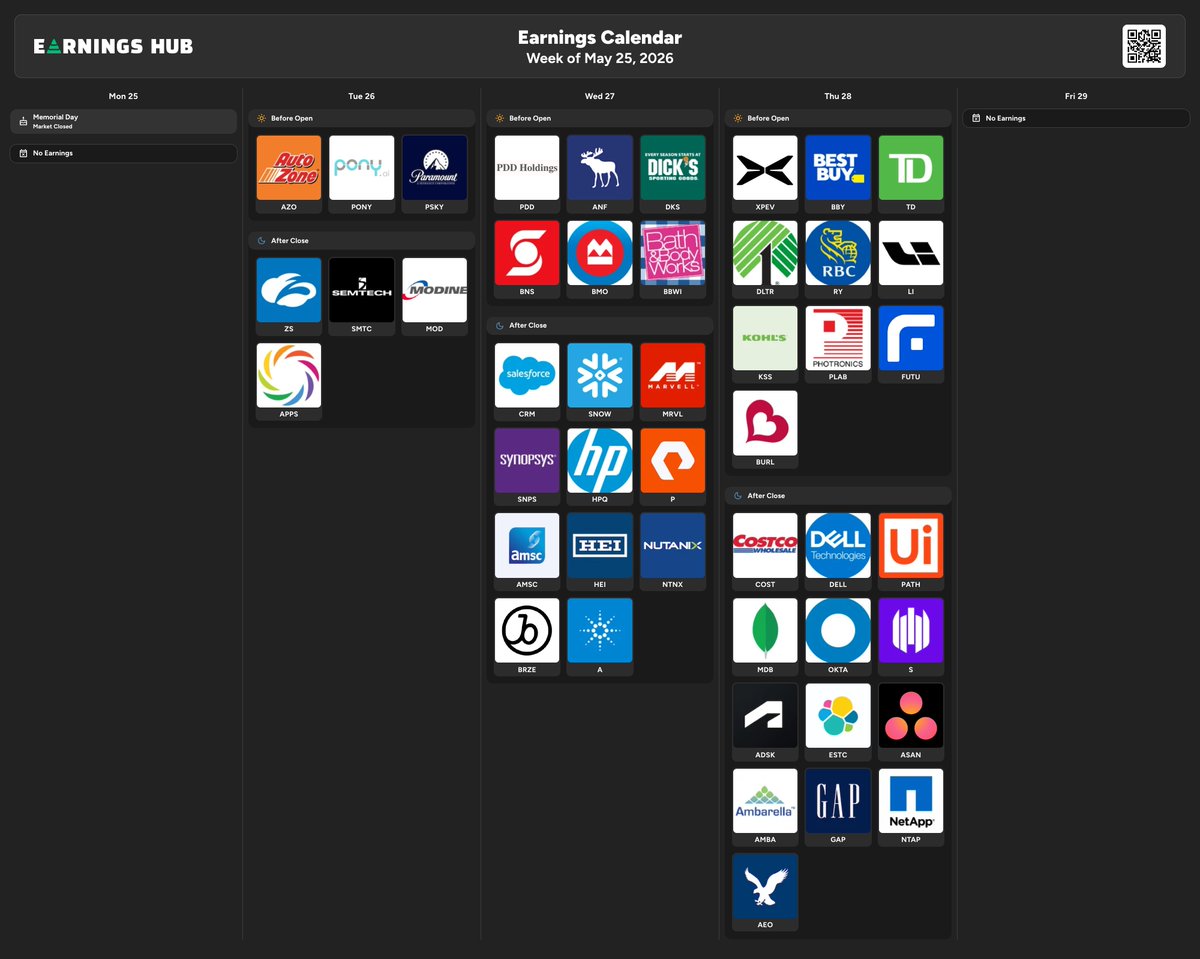

THE MASTER EARNINGS SEASON CALENDAR

Here are the most popular stocks that report earnings this week May 25th - May 29th

7

25

4,587

2(-)! retweeted

May 24

THE PHOTONICS LAYER OF THE AI BUILDOUT

Goldman Sachs says the AI optical networking market growing nearly 10x to $150B by 2028 as clusters scale into multi-rack systems like $NVDA Rubin Ultra NVL576.

The AI bottleneck is shifting to the fabric that lets hundreds of GPUs behave like one system driving a massive dollar content expansion across NVLink, co-packaged optics & optical interconnects:

• $AEHR burn-in & reliability test systems for photonics and AI hardware

• $AAOI data center optical transceivers with in-house laser manufacturing

• $LITE high-speed lasers & optical components for data center transceivers

• $VIAV optical testing & measurement tools used to validate high-speed networks

• $COHR lasers, photonic components & materials used across optical networking systems

• $MRVL optical DSPs, custom interconnect silicon & networking chips for AI infrastructure

• $CRDO retimers, DSPs & active electrical cables for rack-level signal integrity in AI clusters

116

268

1,702

232,696

2(-)! retweeted

May 24

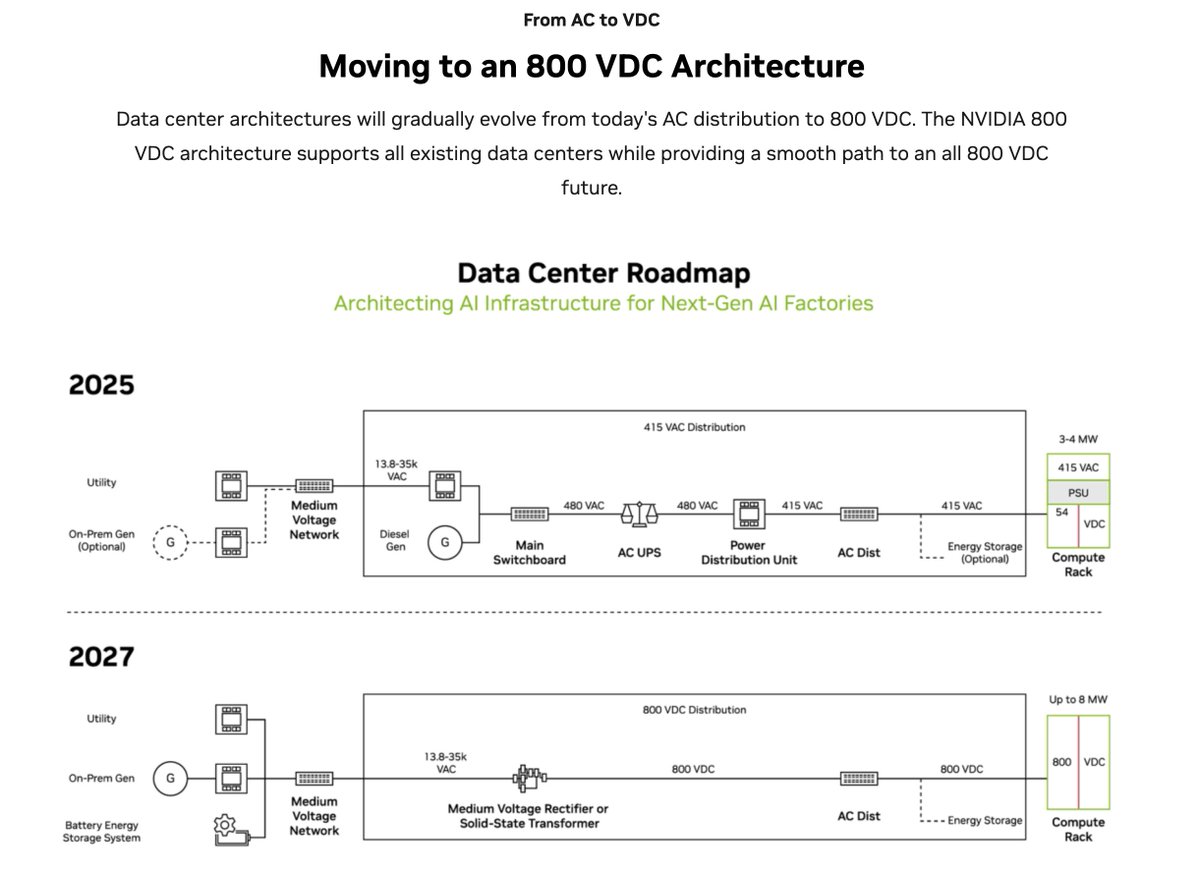

All right chat, crowdsourcing your #1 highest conviction (10x only) stock long for the Power Semi trade.

Especially given $NVDA pushing shift to 800 VDC.

Stuff like $NVTS or $WOLF, but high-beta, 10x potential only. Anywhere around the world.

What's your pick?

570

239

2,813

2,867,196

2(-)! retweeted

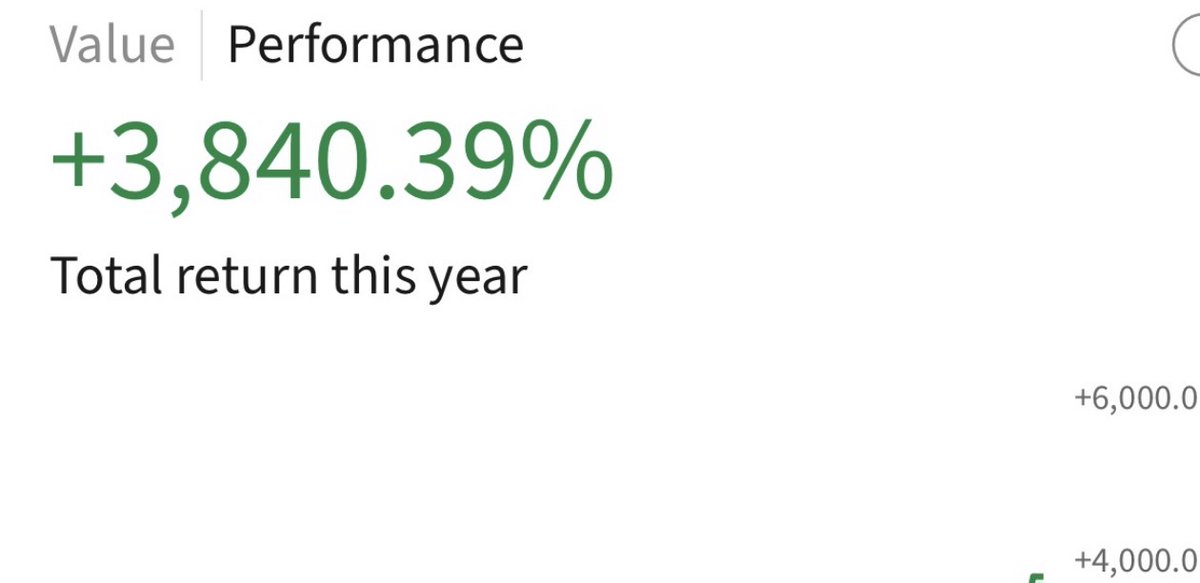

May 23

I don't post dollar amounts because they don't matter.

What matters is return %. Speaking of that...

YTD: 3840.39%.

I'm probably the only one in the world. Who called out multiple names that 10x'd in a short timeframe.

Do you remember these thesis anon?

1. $AXTI

2. $SIVE

3. $AAOI

4. $LITE

5. $IQE

6. $AEHR

7. $CRCL

8. $EWY

9. Unimicron

10. Nitto Boseki

11. $OSS

12. $GDRZF

13. $RPI

14. $SOI

15. $ALRIB

16. $SNDK

17. $SIMO

18. $VPG

19. $TSEM

20. $ARM

21. $MRVL

22. $INTC

23. $LPK

24. $NBIS

25. $MU

They're all up 100-1000% , because...

1. I post a thesis.

2. People can see how the stock performs months later.

3. They turn out right (thesis validation) because they're up hundreds of percent hold their returns.

I really dislike the traditional X influencer who shows large dollar amounts or fancy watches/cars/private jets.

Then use that to get more by selling expensive subscriptions rather than through market returns.

So trying to set a new trend off pure information discovery/synthesis from free thesis posts and the results that follow in terms of return percentages.

TLDR: Market returns in terms of percentages matter the most to validate a thesis.

Not the dollar amount made.

May 23

Notice there's no dollar amount attributed

402

342

4,998

1,750,930

We’re partnering with @Samsung, @_GentleMonster_ and @WarbyParker on new intelligent eyewear.

Here's a sneak peek at two designs from this fall's upcoming collections.

#GoogleIO

288

950

8,855

1,536,245

2(-)! retweeted

May 19

Intel CEO Lip-Bu Tan sat down with CNBC’s Jim Cramer to talk about Apple; Intel 14A rivaling TSMC's top chip production technology; Shortages of CPUs and substrates; and the state of Intel's turnaround.

How to know when Intel signs Apple or other foundry customers:

Intel CEO Lip-Bu Tan: “Over time, the IP will be ready so we can serve some of these customers. I think the best indication, when you see I increase my capex, I’m putting money to buy equipment, that means I have real customers. That’s the discipline I have.”

Intel 14A manufacturing process and EMIB-T advanced packaging:

Intel CEO: “(A14) is 1.4nm, this is the most advanced. To be candid with you, in 2028 we will have risk production. 2029 will be volume production. It will be the same time as TSMC. So that is a major, major breakthrough, and I’m so excited.

And we already have multiple customers engaged with us, and we have 0.5 PDK available.”

Taking advantage of TSMC’s CoWoS shortage

Intel CEO: “Our technology is called EMIB-T, this is the next generation of advanced packaging. We really have the best technology and now we are making sure we can bring it into volume production with reliable yield so the customer can count on us.”

CEO: “You know, CoWoS…(TSMC) ran out of capacity, so in a way we’ve become in the unique position to support that and that’s something we are very excited (about).”

Shortages of CPUs and Substrates

CEO on the CPU shortage: “I’ll give you one example. I had one customer say Lip Bu, we gave you the forecast for this year, but we want to increase 3x, and I say I cannot do it overnight but give me a few quarters and I will catch up. So, I think this demand is not short term, it’s the next couple of years. It’s a great opportunity.”

CEO: “Right now, as I mentioned, CPU is in high demand. And that’s good for me. I cannot even ship enough to the customer. It used to be the CPU to GPU ratio for training was 1-to-8. And now, because of inference and agentic AI, and more agents you have to manage, and orchestration, and reinforced learning, CPU is actually better, so that becomes 1-to-4 and 1-to-1 and some people even talk about 4-to1, and so that’s a huge opportunity to me to drive the CPU....”

CEO on Substrates: “A couple of customers have prepaid for substrates, because the substrate supply chain is very tight – so I need to put up the money to secure this material…(and it shows) the commitment to me – so that’s very exciting.”

Intel’s Turnaround

CEO: “We used to have leadership in data center, and over the years we lost it…We made some big mistakes,” he said, adding he’s brought back some talent to refocus the product lines and that “Coral Rapids will have multi-threading, and will come out very strong.”

CEO: “When I took over, the 18A yield was not good, so I had to ask some of the ecosystem partners to help me look at the data, see how to improve. The best practice is to see 7% or 8% yield improvement per month, and now I’m seeing it.”

CEO: “The other part is supposed to be the yield performance, defect density, you know at the end of the year to see the target. Now I see that even before the end of the year – so that is very big encouragement for me and also that’s why Panther Lake can be shipped in volume now.

And now some customers knock on my door and say Lip Bu, now we hear you are making great progress, can you now open up to outside customers? So that is very exciting. It’s a lot of hard work, it’s a lot of teamwork, it’s a lot of talent I’ve brought on board.”

CEO: “In the past we made a lot of mistakes and now we correct the mistake and we’ve simplified the roadmap. By the way, from Day 1 I came on board as the CEO, I have all the engineers report to me so I have an understanding, hear from the customer, and know where are the mistakes.”

Cramer: “They didn’t report to the previous CEO?”

CEO: “No. And in a way, they had too many silos, too many people reporting…So I decided, the best thing is to really understand where the problem is, so I can focus on the engineering, how to redesign, simplify the product and then get the real killer products out.”

Cramer asks about China, Taiwan and the importance of US manufacturing:

CEO: “I was very glad for President Trump understanding the strategic importance for the United States to have (chip manufacturing supply chain) and their support is so valuable to me – it’s so critical for the country to have the technology, R&D development, manufacturing in the United States. That’s why I came back in, as a U.S. citizen – as a calling – to do that.”

CEO: “From time to time I update President Trump and also (Sec.) Howard Lutnick and they are big supporters of me and we are delighted to have their support.”

Going forward:

CEO: “I recruited some key talent…and now, by the end of June, I will have my team, what I consider my team, so that we can work on the next 5-years, 10-years, how to become a different company. I call it the New Intel, work at the speed of light, work as a team to progress forward.”

$INTC $TSM #Samsung $UMC $GFS #semiconductors

cnbc.com/video/2026/05/18/in…

15

93

477

220,833

2(-)! retweeted

May 17

UPDATED SOFTWARE COMP SHEET

Rule of 40 breakdown:

• Best-in-class (60% ) | $PLTR, $APP

• Elite (50-59%) | $NOW, $CRWD, $PANW

• Great (40-49%) | $SNOW, $DDOG, $ZS, $ADBE, $CRM, $NET, $RBRK, $TEAM

• Good (30-39%) | $MNDY, $HUBS, $MDB, $FIG, $PATH, $ZETA

May 7

$DDOG delivered one of the strongest software quarters in a while with NRR reaccelerating to 121% and reminding the market that software isn't dead.

Agentic AI is making infrastructure more complex since companies juggle multiple models, multi-cloud workloads, GPU fleets, token costs and production reliability.

That creates a massive monitoring problem and Datadog monetizes that complexity.

76

171

1,108

919,583

2(-)! retweeted

May 17

MY 3 FAVORITE WAYS TO PLAY THE CPU BOTTLENECK

Jensen Huang keeps saying the next era of computing will be built around “AI factories” but every agentic workload creates a massive amount of CPU-bound work around the GPU.

The best way to think about this is the GPU will still continue being the engine but CPU will now become the traffic controller. If AI agents are going to run inside enterprises all day across millions of workflows then the CPU layer becomes a much more important part of the AI infrastructure stack.

1. $AMD | AMD

AMD is the cleanest way to play the agentic AI CPU bottleneck through EPYC where they just posted record Q1 data center revenue of $5.8B ( 57% YoY) and biggest gem was AMD capturing ~46% of server CPU revenue despite only 27% unit share (AMD is winning higher-value server CPU dollars that AI infrastructure actually needs).

CEO Lisa Su also raised the server CPU TAM forecast to $120B by 2030, guided Q2 server CPU revenue to grow more than 70% YoY and layered on the $META 6GW Instinct deal which also makes Meta one of the first customers for next-gen Venice and Verano EPYC processors. Intel's Diamond Rapids was also delayed to mid-2027 which means AMD has effectively zero competitive response during the steepest part of the agentic AI buildout.

2. $ARM | Arm

Arm is the most interesting of the three because the story is no longer just “Arm collects royalties” since they're now becoming a direct silicon supplier through the Arm AGI CPU which it says can deliver more than 2x performance per rack versus x86 platforms while reducing AI data center capex by up to $10B per gigawatt.

Arm said customer demand for the AGI CPU has already reached more than $2B across FY27 and FY28 which now gives Arm two ways to win from the same bottleneck: royalties on custom hyperscaler CPUs and direct sales into AI infrastructure.

3. $INTC | Intel

Intel is the most controversial of the three because the market still treats it like a permanent AI-cycle loser but agentic AI could lift every credible x86 supplier and Intel now has two ways to capitalize on it: product and foundry.

On the product side, AI-driven businesses now account for 60% of total revenue and are growing 40% YoY while Xeon 6 was selected as the host CPU for $NVDA DGX Rubin NVL8 systems giving Intel a role inside the next generation of Nvidia AI deployment.

On the foundry side, Intel agreed to manufacture chips designed by $AAPL while Nvidia's $5B investment and commitments from Musk-linked companies validate Intel's manufacturing roadmap at the exact moment AI infrastructure needs more advanced domestic chip capacity.

83

112

851

187,015