Jun 11

メンバーシップでも扱ったASEとKYEC

テストの時代

大手パッケージング・テスト企業のASEとKYECは、MarvellとNVIDIAからの受注を確保したことで、構造的な成長に向けて準備が整っている。

「ファウンドリ2.0」時代の到来と、高度なパッケージングおよびテスト能力市場における需給の逼迫に伴い、主要なウェハファウンドリは余剰受注の放出を加速させており、世界のOSAT業界は急速な成長期を迎えている。

業界アナリストは、台湾の製造業の中で、ASE Technology Holding Co., Ltd.とその子会社であるSPIL、そして大手試験機器製造会社であるKing Yuan Electronicsが主要な受益者になると考えている。2026年5月の決算発表シーズンは、第2四半期の営業活動をさらに押し上げ、今年の四半期ごとの営業成長の傾向を確立すると予想される。

業界関係者は、AIおよび高性能コンピューティング(HPC)関連チップの需要急増が、世界の半導体産業の同時成長を牽引していると指摘している。IDCなどの調査会社は最近、2026年のOSAT生産額予測を上方修正し、年間成長率は16%に達すると予想しており、2025年からの力強い拡大の勢いが続くとしている。OSATは、ファウンドリ2.0市場の生産額の約25%を占めると予想されており、ウェハーファウンドリの59%に次ぐ割合となる。

ASEテクノロジーホールディングスは、2026年5月の連結売上高が前月比1.26%増、前年同月比28.57%増の630億3300万台湾ドルとなったと発表した。これは同社史上4番目に高い月間売上高であり、43ヶ月ぶりの高水準となる。2026年最初の5ヶ月間の累計売上高は2989億4300万台湾ドルに達し、2025年の同時期と比較して19.87%増加し、過去数年間の同時期の最高記 録を更新した。

中でも、AIやHPCアプリケーション関連のチップに対する旺盛な需要を背景に、ASEテクノロジーホールディングス(ATM)の中核事業は著しい成長を見せている。5月の連結売上高は421億6200万台湾ドルに達し、前月比4.1%増、前年同月比37.9%増となり、グループ全体の売上高の65%以上を占めた。

ASEテクノロジーホールディングスは以前、先進包装・検査(LEAP)事業の受注量が予想を上回ったと発表し、2026年の売上高目標を35億米ドル(1,000億台湾ドル以上)に修正した。これは、以前の予想である32億米ドルを約10%上回り、2025年の16億米ドルの2倍以上となる。

特筆すべきは、マーベルのCEOであるマット・マーフィー氏が基調講演を行った際、提携先の台湾企業であるASEテクノロジー・ホールディング社のCOO、ティエンユー・ウー氏がサプライズ登場したことだ。ウー氏は、両社は過去10年間、技術開発や製品戦略を共有しながら緊密に協力してきたと述べた。そして、ASEはまもなくマーベルへの出荷を開始する予定であり、生産能力の増強にも尽力していると語った。

さらに、GPU、CPU、ASICの需要が同時に増加し、台湾における新たな生産能力の継続的な拡大も相まって、キングユアンエレクトロニクスの5月の連結売上高は37億7,700万台湾ドルに達し、前月比0.91%増、前年同月比36.61%増となり、3ヶ月連続で過去最高を更新しました。1月から5月までの累計売上高は177億1,200万台湾ドルとなり、前年同期比37.71%増となりました。

ウェハーテスト(CP)および完成品テスト(FT)の受注に加え、AI関連アプリケーションチップの歩留まりに関する課題が大幅に増加している。キング・ユアン・エレクトロニクスは、バーンインテストおよびシステムレベルテスト(SLT)の需要増加からも恩恵を受けている。AI関連の収益は、2027年には総収益の3分の2を占めると予想されており、これは2024年比で40%の増加となる。

キング・ユアン・エレクトロニクスは、再び「1兆ドル晩餐会」に招待され、NVIDIAのCEOであるジェンセン・フアン氏をはじめとするサプライチェーンパートナー各社と並んで出席した。同社を代表して出席したゼネラルマネージャーのチャン・カオシュン氏は、クリーンルームの建設や試験装置の購入など、高度な試験能力への投資を継続的に拡大していくと述べた。同社は、2026年までに生産能力を拡大し、収益への貢献度を高めることを目指している。

ASEやKYECといった企業は、従来、特定の半導体顧客について公にコメントすることを控えてきた。しかし、主要な国際的な半導体メーカーが台湾のサプライチェーンの重要性を認識するにつれ、強力なパートナーシップを公に認め、アピールすることが一般的になってきている。

Hsin Chuan、Siliconware Precision Industries、Taiwan Star Technology、Chipbondなどの他の企業も、安定したパッケージングおよびテストの受注を抱えている。ロジックおよびメモリのパッケージングとテストに事業を拡大したPowertechやChipMOSのような企業でさえ、2026年には半導体パッケージングおよびテスト業界全体の好況を享受すると予想される。

4

4

93

18,251

Jun 11

ChipMOS $IMOS stock advanced ~12.4% to $61.95. Strong semiconductor packaging and testing demand guidance ahead of upcoming industrial rollouts triggered the double-digit session gains.

37

[DOW JONES NEWSWIRES] Table: ChipMOS Technologies May Rev NT$2.38B Vs NT$2.03B

$IMOS

28

Jun 9

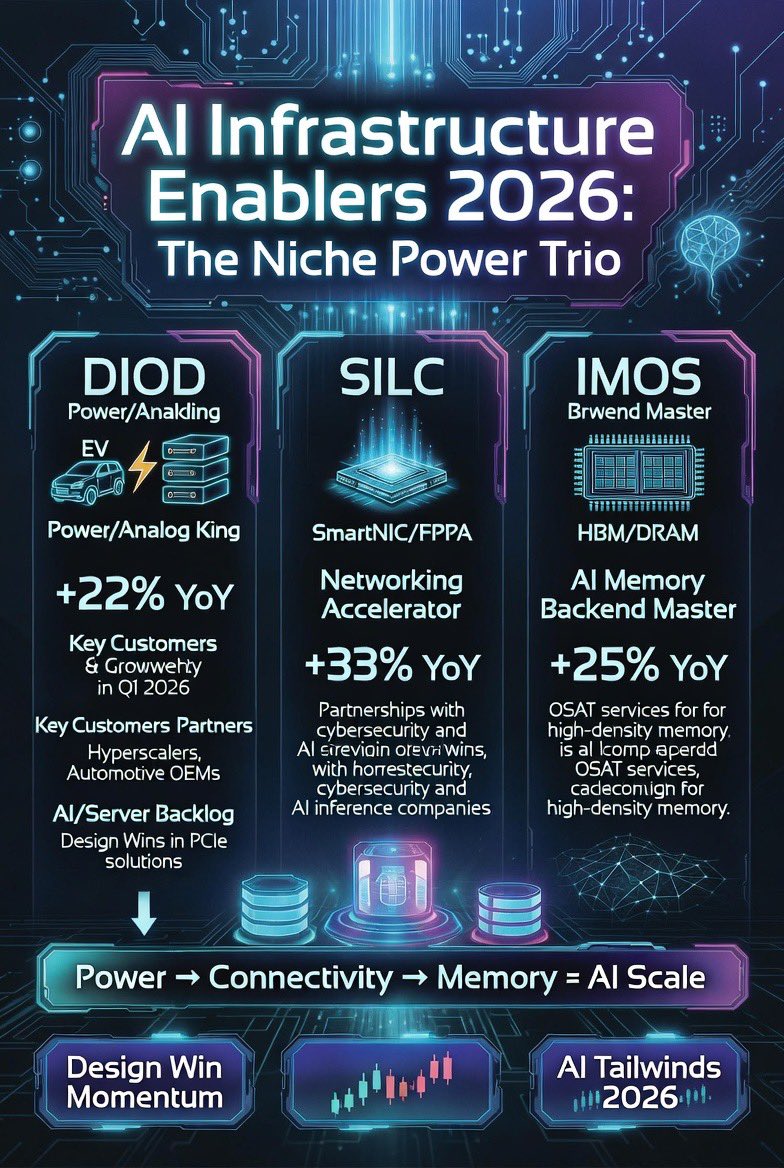

🌌 $SILC $DIOD $IMOS: The Quiet “Behind-the-Scenes” AI Enablers Most People Are Missing

While everyone talks about the big obvious names ($NVDA, $AMD, $AVGO, $TSM, etc.), there are smaller companies quietly solving the real bottlenecks that let AI clusters actually work at scale.

A sharp trader just highlighted three undervalued ones that most investors haven’t even heard of yet:

1. $DIOD (Diodes Incorporated) – ~$4.8B market cap

They make the power management parts that keep AI servers running efficiently (voltage regulators, MOSFETs, power ICs, switches, etc.).

• Q1 revenue: $405.5M ( 22% YoY) — 5th straight quarter of double-digit growth.

• Automotive and industrial revenue both up 30% .

• Management targeting $2B annual revenue by 2028.

Simple role: As AI racks get denser and hotter, you need better power delivery so the GPUs don’t melt or waste electricity. $DIOD supplies a lot of those critical “plumbing” parts.

2. $SILC (Silicom) – ~$248M market cap (tiny!)

They build high-performance networking hardware (SmartNICs, FPGA cards, switches) that moves data efficiently inside AI clusters.

• Q1 revenue: $19.1M ( 33% YoY)

• Q2 guidance: $20–21M (almost 40% growth)

Simple role: AI training and inference need massive amounts of data moving between thousands of GPUs at lightning speed with low latency. $SILC helps solve that “data traffic jam” inside the data center.

3. $IMOS (ChipMOS) – ~$2B market cap

They specialize in OSAT (Outsourced Semiconductor Assembly and Testing) — basically the final step that turns raw memory chips into ready-to-use products for AI servers.

• Q1 revenue: NT$6.94B ( 25.4% YoY), driven by memory demand.

Simple role: Every AI server needs huge amounts of advanced memory (DRAM/NAND). $IMOS tests and packages those memory chips so they actually work reliably.

Bottom Line (Super Simple)

These aren’t the sexy “front-page” AI names, but they’re the invisible infrastructure that makes the whole system scale:

• Power efficiency → $DIOD

• Data movement → $SILC

• Memory readiness → $IMOS

The trader calls them “undervalued enablers” solving real bottlenecks while the market is still obsessed with the obvious chip leaders.

Still small enough that most retail investors haven’t discovered them yet.

Not investment advice — always do your own research. Small/mid-cap stocks like these can be volatile and carry real execution risk.

Jun 9

$SILC $DIOD $IMOS

Three niche enablers of the AI ecosystem that most investors are completely overlooking.

$DIOD 4.8B mc

$SILC 248m mc

$IMOS 2B mc

Undervalued.

Everyone knows the obvious names like $NVDA, $AMD, $AVGO, $TSM, and $NBIS. But behind every AI cluster, data center, and server deployment are smaller companies solving critical bottlenecks around power efficiency, connectivity, and memory readiness.

If you haven’t heard of these yet, hit subscribe. Bookmark. 🔖

$DIOD

Diodes Incorporated is one of the more underappreciated semiconductor infrastructure companies in the market.

They don’t build the GPUs. They build many of the components that allow those systems to operate efficiently at scale.

The company supplies voltage regulators, MOSFETs, power management ICs, LED drivers, switches, protection devices, ReDrivers, timing solutions, and mixed-signal components used throughout AI servers, industrial systems, communications equipment, and automotive platforms.

As AI racks become denser and power consumption continues rising, efficient power delivery and signal integrity become increasingly important.

Q1 2026 revenue reached $405.5M, growing 22% YoY and marking the company’s fifth consecutive quarter of double-digit annual growth.

Automotive revenue grew 32% YoY while industrial revenue increased 31% YoY. AI infrastructure, industrial automation, and edge computing continue contributing to growth across multiple product categories.

Management is targeting roughly $2B in annual revenue by 2028.

The AI narrative often focuses on compute. $DIOD benefits from the power infrastructure required to support that compute.

$SILC

Silicom operates in one of the most important but least discussed areas of AI infrastructure: networking and data movement.

As AI clusters scale, moving data efficiently becomes just as important as processing it.

The company develops high-performance NICs, SmartNICs, FPGA acceleration cards, edge networking platforms, switches, and specialized hardware that enables encryption, security processing, packet inspection, and networking offload functions.

These solutions help reduce CPU overhead while improving throughput and latency inside modern data centers.

Silicom’s products help solve bottlenecks associated with AI training, inference, cloud infrastructure, cybersecurity workloads, SD-WAN deployments, and edge computing.

Q1 2026 revenue increased 33% YoY to $19.1M while management guided Q2 revenue to $20M-$21M, representing growth approaching 40% YoY.

The company continues reporting new SmartNIC, FPGA, cybersecurity, secure communications, and AI networking design wins that are beginning to ramp into production.

While much of the market focuses on compute acceleration, $SILC sits directly in the connectivity layer that allows those systems to scale.

$IMOS

ChipMOS occupies a different but equally important position within the semiconductor ecosystem.

The company specializes in outsourced semiconductor assembly and testing services, often referred to as OSAT.

Without OSAT providers, advanced semiconductors never reach end customers.

ChipMOS has developed a particularly strong position in high-density memory, including DRAM, NAND, and memory products increasingly tied to AI server deployments.

As AI demand continues driving memory requirements higher, the importance of assembly, testing, and packaging grows alongside it.

Q1 2026 revenue reached NT$6.94B, increasing 25.4% YoY.

Memory-related services remain the primary growth driver as AI server demand continues supporting advanced memory markets.

Every AI server requires massive amounts of memory. Every memory chip requires testing and packaging before deployment.

They’re enabling the broader ecosystem alongside names such as $GOOG, $AMZN, $INTC, $IREN, $NBIS, $AVGO, $AMD, and $TSM.

Sometimes the best opportunities aren’t the companies everyone is talking about.

They’re the companies quietly solving the bottlenecks.

1

2

723

Jun 9

$SILC $DIOD $IMOS

Three niche enablers of the AI ecosystem that most investors are completely overlooking.

$DIOD 4.8B mc

$SILC 248m mc

$IMOS 2B mc

Undervalued.

Everyone knows the obvious names like $NVDA, $AMD, $AVGO, $TSM, and $NBIS. But behind every AI cluster, data center, and server deployment are smaller companies solving critical bottlenecks around power efficiency, connectivity, and memory readiness.

If you haven’t heard of these yet, hit subscribe. Bookmark. 🔖

$DIOD

Diodes Incorporated is one of the more underappreciated semiconductor infrastructure companies in the market.

They don’t build the GPUs. They build many of the components that allow those systems to operate efficiently at scale.

The company supplies voltage regulators, MOSFETs, power management ICs, LED drivers, switches, protection devices, ReDrivers, timing solutions, and mixed-signal components used throughout AI servers, industrial systems, communications equipment, and automotive platforms.

As AI racks become denser and power consumption continues rising, efficient power delivery and signal integrity become increasingly important.

Q1 2026 revenue reached $405.5M, growing 22% YoY and marking the company’s fifth consecutive quarter of double-digit annual growth.

Automotive revenue grew 32% YoY while industrial revenue increased 31% YoY. AI infrastructure, industrial automation, and edge computing continue contributing to growth across multiple product categories.

Management is targeting roughly $2B in annual revenue by 2028.

The AI narrative often focuses on compute. $DIOD benefits from the power infrastructure required to support that compute.

$SILC

Silicom operates in one of the most important but least discussed areas of AI infrastructure: networking and data movement.

As AI clusters scale, moving data efficiently becomes just as important as processing it.

The company develops high-performance NICs, SmartNICs, FPGA acceleration cards, edge networking platforms, switches, and specialized hardware that enables encryption, security processing, packet inspection, and networking offload functions.

These solutions help reduce CPU overhead while improving throughput and latency inside modern data centers.

Silicom’s products help solve bottlenecks associated with AI training, inference, cloud infrastructure, cybersecurity workloads, SD-WAN deployments, and edge computing.

Q1 2026 revenue increased 33% YoY to $19.1M while management guided Q2 revenue to $20M-$21M, representing growth approaching 40% YoY.

The company continues reporting new SmartNIC, FPGA, cybersecurity, secure communications, and AI networking design wins that are beginning to ramp into production.

While much of the market focuses on compute acceleration, $SILC sits directly in the connectivity layer that allows those systems to scale.

$IMOS

ChipMOS occupies a different but equally important position within the semiconductor ecosystem.

The company specializes in outsourced semiconductor assembly and testing services, often referred to as OSAT.

Without OSAT providers, advanced semiconductors never reach end customers.

ChipMOS has developed a particularly strong position in high-density memory, including DRAM, NAND, and memory products increasingly tied to AI server deployments.

As AI demand continues driving memory requirements higher, the importance of assembly, testing, and packaging grows alongside it.

Q1 2026 revenue reached NT$6.94B, increasing 25.4% YoY.

Memory-related services remain the primary growth driver as AI server demand continues supporting advanced memory markets.

Every AI server requires massive amounts of memory. Every memory chip requires testing and packaging before deployment.

They’re enabling the broader ecosystem alongside names such as $GOOG, $AMZN, $INTC, $IREN, $NBIS, $AVGO, $AMD, and $TSM.

Sometimes the best opportunities aren’t the companies everyone is talking about.

They’re the companies quietly solving the bottlenecks.

42

10

51

5,286

May 27

🇹🇼 台湾の半導体エコシステム、かなり熱い。

売上・利益ともに50%超YoY成長してる企業がゴロゴロいる。WinbondとMacronixはかなり推してる。Adataも加えて、このサイクルでのメモリ専門リーダーだと思う。あとChipMOSはちょっと見落とされ気味だわ。

韓国のメモリ関連についてはSubstackで深掘り解説してるので、興味のある方はぜひチェックしてみてください!👇

substacktools.com/sharex/bSI…

3

2

28

3,332

May 24

TSMCの高雄、CPOの拠点

高雄のFeynman CPOクラスターは、世界のAIスーパーコンピューティング競争の最前線に立っている。改善すべき3つの主要分野。

高雄は、世界のAIスーパーコンピューティング競争の最前線に立っています。高度なプロセス技術、先進的なパッケージング技術、光電子技術から、AI分野、スーパーコンピューティング能力、国際協力に至るまで、高雄にはファインマン×CPO産業クラスターを構築するために必要なすべての条件が揃っています。

AIコンピューティングに対する世界的な需要が爆発的に高まる中、高雄は台湾の次世代テクノロジー拠点となるだけでなく、アジア初のファインマン×CPO実証都市、AI超高速コンピューティングと光通信の世界的な主要拠点、そして次世代AI技術の研究・検証センターとなる可能性を秘めています。これは、高雄が「伝統的な製造業都市」から「テクノロジー都市」へと変貌を遂げ、「AIスーパーコンピューティング都市」へと向かう中で、世界の技術競争において重要な地位を確立しつつあることを示しています。

今年のGTCカンファレンスで、ジェンセン・ファン氏は、AIの次の段階はもはや計算能力の追求だけではなく、高密度コンピューティング環境において大規模データ伝送、物理シミュレーション、システムレベルの統合を同時に実現できる能力が重要になると強調した。ファインマンアーキテクチャはAIと物理世界との緊密な連携を担い、CPOは従来の電子相互接続の帯域幅ボトルネックを打破する。この2つの組み合わせが、次世代AI超高速コンピューティングの基盤となるだろう。

これに対し、高雄市経済発展局の廖泰祥局長は、AI開発が次の段階に入ると、課題はもはや計算能力そのものではなく、高密度なコンピューティング環境において膨大な量のデータをリアルタイムで伝送・統合する方法にあると指摘した。高雄市の産業構造は、まさにこの転換点に合致している。

彼は、高雄はゼロから始めるのではなく、既存の強みを活かし、ファインマン×CPOの商業化に伴う高い需要を満たすための産業条件を備えていると強調した。

廖泰祥氏は、高雄市は現在、台湾で最も完成度の高いCPO(チップ製造装置)および光通信産業チェーンを形成しており、最大の量産能力を有していると述べた。その強みは、高度なチップ製造、高度なハイエンドパッケージングとテスト、システム統合、そして都市レベルの応用分野という4つである。

チップ製造の上流工程において、TSMCの高雄工場は2ナノメートル(N2)チップの量産とA16(1.6ナノメートル)世代のレイアウトを行い、次世代AIチップおよびCPOチップに必要な高度なプロセス基盤を提供する。FeynmanチップとCPOチップはプロセス安定性に極めて高い要求が課されるため、高雄工場はこれらの業務を担うのに最適な立地条件を備えている。

同氏によると、ASEは高雄にグローバルな事業運営と先進的なパッケージング拠点を有しており、そこには異種統合、光電子部品パッケージング、高周波・高速テスト能力など、CPOの量産に不可欠な要素がすべて備わっているという。

フォックスコンやウィストロンといったシステムレベルのメーカーは、高雄への投資を拡大し続けており、光相互接続機能を備えたAIコンピューティングチップをサーバーやデータセンターに迅速に導入できるようにしている。

廖泰祥氏は、高雄市にはアジア湾スマートテクノロジーパーク、高雄港スマートハーバー、スマート交通システム、5G AIoT都市レベル検証サイトなど、都市レベルの検証サイトも存在すると指摘した。これらは、Feynman × CPOが最も必要とする「実世界テスト環境」である。

廖泰祥氏は、「高雄は研究開発、量産、検証の統合能力を備えており、AI技術の研究開発、システム検証、産業実装を同時に支援できるアジアでも数少ない都市の一つである」と述べた。また、ファインマンアーキテクチャはAIと物理世界との深い統合を重視しており、スマート交通、スマート港湾、都市ガバナンス、産業シミュレーション、大規模リアルタイムコンピューティングなど、高雄のスマートシティの中核プロジェクトに特に適しているため、アジア湾をファインマンチップの最適な実証拠点とした。

同氏は、アジアベイは台湾で最も充実した5G AIoTデモンストレーション環境を備えており、新しいアーキテクチャチップをシステムに直接統合し、性能テストを行い、高速相互接続を検証し、都市レベルのAIモデルとしてトレーニングできると強調した。さらに、NVIDIAとFoxconnの共同事業である台北1スーパーコンピューティングセンターは、ファインマンアーキテクチャの初期テストに必要なコンピューティングリソースを提供し、高雄市が完全な「研究開発・コンピューティング能力・フィールド」連携を実現できるようにする。

廖泰祥氏は、高雄市政府が「現場主導型問題解決」モデルを採用しており、企業が研究所にとどまるのではなく、都市部で直接技術をテストできるようになっていると指摘した。そのため、「アジア湾は次世代AIアーキテクチャの重要な実証拠点となり、研究開発の検証から実用化へと移行していくだろう」と述べた。

同氏は、アジアベイスマートテクノロジーイノベーションパーク(アジアベイ2.0)が建設段階から実質的な運営段階に移行し、高雄市がAI、半導体、ハイエンドコンピューティングパワーを推進するための重要なプラットフォームになったと述べた。2025年までに、累積投資額は360億台湾ドルを超え、850億台湾ドルを超える生産額を生み出す。進出した企業は、AI、IC設計、スマート製造、スマート港湾、フィンテックなどの分野を網羅している。進出した企業には、フォックスコン、ペガトロン、IBM、シスコ、AMD、リンカービジョン、エランマイクロエレクトロニクス、新華科技などの国内外の有名メーカーが含まれる。中でも、IC設計企業は、高速データ伝送、AIコンピューティングアーキテクチャ、光電子統合、システムオンチップ(SoC)に重点を置いている。

廖泰祥氏は、アジアベイの役割は製造現場を置き換えることではなく、「研究開発の統合、システム検証、アプリケーション実装のための中間プラットフォームを構築すること」だと強調した。これにより、アジアベイは高雄の高度なプロセスと高度なパッケージングを補完する存在となり、重複するものではない。

AIコンピューティングに対する世界的な需要の爆発的な増加に直面し、ファインマンアーキテクチャは次世代AIスーパーコンピューティングの鍵と考えられている。廖泰祥氏は、高雄が新たなグローバルAIトラックに急いで参入する過程で、半導体、光電子工学、システム、AIの分野横断的な人材育成、高密度コンピューティングインフラストラクチャの構築、国際協力と標準化への参加による発言力の獲得という3つの重要な側面を強化する必要があると認めた。

このため、高雄市は国立中山大学と提携し、将来的に国際的な人材育成と研究開発拠点となるSPARK(シリコンフォトニクス・アリゾナ高雄センター)を推進している。同氏は、CPOとシリコンフォトニクスはまだ商業化の初期段階にあり、標準規格も確定していないため、高雄市が実証サイトを通じて経験を蓄積できれば、国際標準の策定において重要な地位を獲得できる可能性があると述べた。「高雄市は単なる製造拠点ではなく、新しいアーキテクチャを実際にテストし、新しいシステムを検証できる重要な場所なのです。」

高雄市政府が投資誘致と関連産業導入に積極的に取り組んでいることに加え、経済部工業局(旧工業局)も国立中山大学工業開発センターと提携し、2009年に「南方IC設計研究開発インキュベーションセンター」を設立しました。国立中山大学工業開発センターの林健黄所長は、「南方IC設計研究開発インキュベーションセンター」は主に半導体、ICT、AIoT産業に焦点を当てていると述べました。現在までに、PixArt Imaging、AIoT、Compal Electronics、Elan Microelectronics、Motech Electronics、Genesys Logic、Vimo Technologies、M&V Technologyなど34社以上の企業が高雄に進出し、16億4000万台湾ドル以上の投資を誘致しています。

同氏は、2024年に経済部が国立中山大学産業発展センターと協力し、高雄アジア新湾区内の高雄ソフトウェアパークに「台湾南部チップ設計産業振興拠点」を設立したと述べた。この拠点は、国内外のIC設計関連企業を台湾南部に誘致し、半導体産業における国内外のリソースを結集することを目的としている。ツールとリソース、人材採用、賃貸インセンティブ、補助金制度、事業開発、技術リソースの6つの主要分野を網羅し、企業の成長と拡大に必要なサポートを提供する。これにより、入居企業の成長を効果的に加速し、支援する。開設以来、Yi Chuan Technology、ChipMOS Technologies、Hsin Hua Technologyなどの企業を台湾南部に誘致することに成功し、同地域のチップ設計能力を拡大している。

16

5

96

21,046

May 23

Interested in Macronix as a memory key player over there, do think Landmark is their Lumentum holdings (crazy multiples) and others that work closely with Nvidia like Foci.

Often overlooked are Baotek (Nittobo proxy), Microtek and ChipMOS $IMOS.

Sometimes they freeze trading in some particular stock and that's a bit annoying.

Mediatek got closed for 2 weeks if I'm not mistaken.

I have some new ones in my substack too.

2

1

4

1,130

May 16

$TRT

Up 49% yesterday

200M MC

A 100$ stock at 21$. I’m still bullish

Could be interesting asymmetric upside exposure to AI burn-in semiconductor reliability testing.

$TRT trading around ~3-4x sales vs. $AEHR historically trading at massive premiums during AI test ramps.

And we already know the testing tailwind is very real:

$TER AI exposure surpassed 70% of Q1 FY26 revenue

$AEHR reported ~$92M H2 bookings

Advantest operating profit 135% on HBM/HPC demand

ChipMOS Q1 FY26 revenue 25% on AI memory testing demand

Meanwhile $TRT quietly posted:

Q3 FY26 revenue 124% YoY

9M FY26 revenue 85% YoY

SBS segment 104% YoY

Stock up 685% 1Y

New 52W highs

AI GPU burn-in demand accelerating

But unlike pure-play equipment names, $TRT combines:

burn-in systems

reliability testing services

burn-in boards

manufacturing/distribution

Asia-based semiconductor backend ops

Heavy footprint across:

Malaysia

Singapore

Thailand

China

Exactly where semiconductor manufacturing AI packaging demand is scaling fastest rn.

Recent validation looks notable:

$5.3M burn-in board order tied to next-gen AI GPU platform

Additional $2.5M AI-related burn-in orders

$2.5M automotive IDM burn-in engagement

Strong speculation around potential $AMD adjacency through Malaysia ecosystem exposure

The order flow lines up w/ broader hyperscaler AI infrastructure burn-in expansion happening across the industry.

And the expansion is already starting:

New 104K sq ft Malaysia facility

Lease begins June 2026

Expansion funded partly through recent ~$10M raise

Capacity targeted directly at AI/HPC automotive demand

Financially:

~$15-20M cash

Low debt

~3.4x current ratio

~40% insider ownership

Limited dilution historically for a microcap expansion story

The bull thesis is pretty simple:

If AI GPU automotive testing demand keeps ramping, this becomes an operational leverage story fast.

Testing businesses carry high fixed costs.

If utilization ramps:

margins can inflect hard

revenue scales quickly

profitability expands disproportionately

Especially if these AI programs evolve into recurring high-volume engagements through FY27.

But the valuation gap vs. names like $AEHR exists for reasons too:

customer concentration risk

thinner margins (~16% gross margin recently)

less proprietary moat

more service-heavy mix

microcap volatility/liquidity risk

execution still needs proving

Still, catalysts matter. For $TRT:

Q4 FY26 earnings

AI order fulfillment

Margin expansion

Malaysia utilization ramp

Potential customer disclosure

Additional AI GPU burn-in wins

Any sell-side coverage initiation

Continued AI packaging/HBM/CoWoS demand acceleration

And broader sector tailwinds remain massive:

HBM4 ramp

CoWoS capacity expansion

Nvidia AI infrastructure scaling

AI power thermal complexity

Automotive semiconductor reliability demand

Higher burn-in requirements for advanced chips

Could be early innings if management executes.

High risk.

High volatility.

But potentially asymmetric if these AI relationships scale into multi-year testing programs.

Don’t miss the next $AEHR.

$COHR $MU $AMD $AAOI $GSIT $MRAM $LITE $TSM $CIEN

10

11

109

8,451

May 14

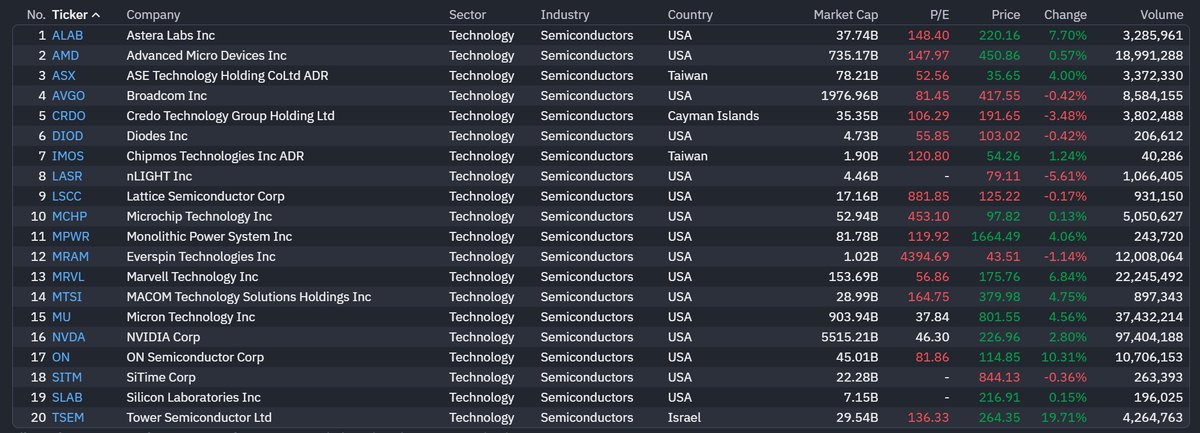

半導体で利益が伸びている銘柄だけをスクリーニング。

条件

①今年のEPS成長率 25%以上

② 来年のEPS成長率 25%以上

③ 直近四半期のEPS成長率 25%以上

「過去も、今も、未来も」利益が伸びている半導体銘柄だけを残した。

該当したのは、この20銘柄。

$ALAB Astera Labs

$AMD Advanced Micro Devices

$ASX ASE Technology

$AVGO Broadcom

$CRDO Credo Technology

$DIOD Diodes

$IMOS Chipmos Technologies

$LASR nLIGHT

$LSCC Lattice Semiconductor

$MCHP Microchip Technology

$MPWR Monolithic Power System

$MRAM Everspin Technologies

$MRVL Marvell Technology

$MTSI MACOM Technology

$MU Micron Technology

$NVDA NVIDIA

$ON ON Semiconductor

$SITM SiTime

$SLAB Silicon Laboratories

$TSEM Tower Semiconductor

注目ポイントをいくつか。

NVIDIAは当然入っている。

時価総額5.5兆ドル、AI半導体の王者は、利益成長でもまだフィルターを通過する。

面白いのはMicron。P/E 37.84はこのリストで最も割安水準。

メモリ需要×AI×HBMの恩恵を、まだ市場が十分に織り込みきっていない可能性がある。

TSEMは1日で 19.71%。

イスラエルの特殊プロセスファウンドリで、アナログ・RF・パワー半導体に強い。

AI以外の半導体需要回復の先行指標になり得る。

ON Semiconductor

も 10.31%。EV・産業用半導体の回復が効いている。

このスクリーニングで見えてくるのは、AI半導体だけじゃなく、アナログ・パワー・メモリ・パッケージングまで幅広く利益成長が起きているということ。

半導体=NVIDIAだけの時代は終わりつつあるね。

4

28

308

34,178

May 10

Earnings next week for across sectors like semis, space, and power.

Companies like $NBIS, $ASTS, and $PLUG all report. I think we’re all looking forward to hearing from $POET’s CFO too?

TLDR Summary:

Monday:

$ASTS: scheduled June SpaceX launches (addressing prior delays) fresh defense contracts incl. U.S. Missile Defense Agency SHIELD program recent partnership momentum w/ AT&T, Verizon & Vodafone. The only real negative has been launch execution risk from recent BlueBird 7 setback. Fresh delays / funding concerns could pressure valuation short term.

$HIMS: last quarter was huge ($2.35B rev = 59% YoY). Since then: launched Novo Nordisk branded GLP-1’s after legal settlement heavy institutional buying. Short interest still high at ~35%. Key signals are: subscriber growth past 2.5M, GLP-1 traction without margin erosion raise of the FY $2.7-2.9B rev guide.

$CRCL: riding momentum from Q4 - rev up 77% YoY ($770M) & solid EPS beat. Since then: new institutional payment platforms launched expanded African partnerships. Tailwinds from potential U.S. stablecoin legislation diversification into services. Valuation is way too high rn for me to consider, especially w/ risks in crypto sentiment / margin pressure.

$PLUG: Recent narrative has been mixed: services & hydrogen rev growth DOE loan progress are the positives. But high cash burn, capex needs seasonal Q1 weakness are the downsides. GM sustainability/expansion, backlog conversion (e.g. Canada wins), liquidity updates explicit confirmation of the 2026 path to positive EBITDA are all crucial.

Tuesday:

ChipMOS: shown strong momentum recently after weak 2025 - Customer demand visibility now extends past 2026: Q1 results tracking strong MRR, improving utilization/margins sustained AI tailwinds into the full year.

$SATL: recently signed $12M sovereign defense contract expanded defense/intel sales team. Still a small base but the AI Earth-observation thesis needs clear rev acceleration, backlog wins, Merlin constellation progress (Oct 2026 target), and cash discipline.

$CAMT: don’t think there’s many updates apart from recent Visual Layer acquisition to bolster inspection capabilities? As with most AI supply chain names, you’d want: strong backlog/orders, clear pipeline visibility.

Wednesday:

$NBIS: Eigen AI acquisition hyperscaler deployments ( $MSFT / $META) have enhanced the AI-infra narrative. To justify premium neocloud valuation: Q1 rev/ARR progress, capacity-ramp updates, Eigen integration traction. Hyperscaler execution backlog conversion would reinforce the 5x growth story.

$TSEM: Would be looking for healthy customer mix (RF/power/SiGe) AI comments. Fab-loading strength would confirm a durable cycle, but weakness would highlight foundry exposure. I personally trimmed ~50% of my holding over the last month to rotate elsewhere.

Thursday:

$POET: order cancellation by $MRVL was huge for them since rev is already tiny. So to offset that, they’d need to signal Malaysia production ramp confirmation any new hyperscaler wins. Visible revenue inflection backlog would validate the shift to commercialization. Personally don’t have patience for incompetent management (regret taking a position), so sold out of my position at break-even after that whole Marvell fiasco.

22

19

339

40,161

$IMOS - ChipMOS REPORTS 322 YoY INCREASE IN APRIL 2026 REVENUE

News & Disclaimer

ift.tt/T1sWS50

3

341

May 6

Happy for $IMOS which is getting finally some recognition.

ChipMOS TECHNOLOGIES INC. engages in the research and development, manufacture, and sale of integrated circuits, and related assembly and testing services in Taiwan, Japan, the People’s Republic of China, and internationally.

It operates through five segments: Testing; Assembly; Display Panel Driver Semiconductor Assembly and Testing; Bumping; and Others.

The company offers leadframe-based packages, such as the small outline package, thin small outline package, and quad flat package; and substrate-based packages, including FBGA, VFBGA, stacked chip-scale package, TFBGA, LGA, COG, and COF; and testing solutions comprising professional wafer and final testing, tester/tooling correlation, test program verification, engineering lot and pilot lot run arrangement, engineering support, device failure mode analysis, and automation system for simple digital logic, complex ASIC, high speed digital, memory, and mixed signal and display driver IC devices.

It also provides bumping services; intellectual property management and enabling technologies; and turnkey services, such as wafer bumping/RDL, wafer sort, assembly, final test, and drop shipment to display driver IC, memory IC, and logic mixed-signal IC.

The company serves fabless companies, integrated device manufacturers, and foundries.

4

3

23

6,008

ChipMOS @Mike10947310 pitch looks limit up two days in a row, insane.

1

2

1,719

May 4

$IMOS wants $100 in 2026

ChipMOS Invests NT$688.9 Million in New Semiconductor Manufacturing Equipment.

8

14

69

42,635

May 4

ChipMOS TECHNOLOGIES INC. $IMOS is a leading independent OSAT (outsourced semiconductor assembly and test) provider. It specializes in back-end semiconductor services—primarily assembly, testing, bumping, and turnkey solutions—for integrated circuits (ICs). The company focuses on high-density memory, mixed-signal/logic, and display panel driver semiconductors (DDIC, including LCD/OLED drivers). It was founded in 1997 and is headquartered in Hsinchu Science Park, Taiwan.

Products & ServicesChipMOS operates through five segments: Testing, Assembly, Display Panel Driver Semiconductor Assembly and Testing (LCDD/DDIC), Bumping, and Others. Key offerings include:Assembly/packaging: Leadframe-based packages (e.g., SOP, TSOP, QFP) and substrate-based packages (e.g., FBGA, VFBGA, stacked CSP, TFBGA, LGA, COG, COF). These support memory, mixed-signal, and display driver ICs used in consumer electronics, PCs, communications, office automation, automotive, drones, VR/AR, and data centers.

Testing: Wafer and final testing, plus engineering support (tester correlation, test program development, failure analysis, automation) for digital logic, ASIC, high-speed digital, memory, mixed-signal, and display driver devices.

Bumping: Wafer bumping/RDL (redistribution layer) services; ChipMOS holds a strong position in gold bumping for Taiwan-packaged LCD drivers (over 40% market share in that niche).

Turnkey services: Full end-to-end solutions from wafer bumping/sort/assembly/final test to drop shipment, tailored for DDIC, memory, and logic/mixed-signal ICs.

Other: Intellectual property management and enabling technologies.

Services are offered on a standalone or integrated turnkey basis, emphasizing vertically integrated supply-chain efficiency for short product lifecycles .Supply ChainAs a pure-play OSAT, ChipMOS sits in the downstream back-end of the semiconductor supply chain. It receives wafers from foundries (e.g., TSMC and others), performs bumping, wafer sort, assembly, and testing, then ships finished packaged/tested ICs directly to customers. It does not design or fabricate front-end wafers.Key inputs: Leadframes, organic substrates, chemicals, testing equipment, and packaging materials.

Facilities: All major operations are in Taiwan—testing in Hsinchu Science Park, packaging in Southern Taiwan Science Park, bumping in Chupei (Hsinchu). Recent capex includes NT$688.9 million in new equipment and an NT$880 million Tainan facility purchase to expand capacity amid AI/memory demand.

CustomersChipMOS serves fabless semiconductor companies, integrated device manufacturers (IDMs), and foundries globally. Specific customer names are not publicly disclosed (typical confidentiality in OSAT). Revenue is derived from end markets including consumer electronics, PCs, communications, office automation, automotive, and emerging areas like data centers/AI (memory), OLED/auto (DDIC stabilization). Taiwan accounts for the majority of revenue, followed by Japan, China, Singapore, and others.

Where They Operate & Best-Performing RegionsPrimary operations: Taiwan (HQ and all advanced facilities).

Geographic revenue: Majority from Taiwan; international sales in Japan, PRC (China), and elsewhere.

Best-performing regions/segments: Strongest recent momentum in memory (testing/assembly for high-value AI/data-center applications), which has driven utilization rates higher and offset softer DDIC demand. Taiwan remains the core hub; memory has fueled 20% YoY revenue growth in recent months. DDIC (display drivers) is a historical strength but has faced consumer weakness, with some stabilization in OLED/auto.

Competitors & ComparisonIMOS is a smaller/mid-tier OSAT player (ranked ~#10 globally by revenue in recent data, ~US$710M in 2024). Larger peers include:ASE Technology (ASX) — dominant leader (~45% share of top-10 OSAT).

Amkor (AMKR).

JCET (China-based, strong growth).

Others: Powertech, etc.

Strengths vs. peers: Specialized leadership in DDIC/gold bumping and growing memory/OSAT capabilities; agile turnkey services; strong Taiwan base for tech collaboration. Challenges: Smaller scale than ASE/Amkor (less diversification, pricing power); margins have been compressed industry-wide (gross margin ~11% TTM). OSAT sector overall saw modest ~3% growth in 2024 due to inventory corrections, but AI/memory tailwinds are now benefiting specialists like IMOS.

Sector PerformanceThe semiconductor OSAT sub-sector (part of broader Semiconductors & Semiconductor Equipment) is in a recovery/upcycle phase. AI/high-performance computing demand for memory is a major driver, offsetting earlier weakness in consumer/auto. Top-10 OSAT revenue grew modestly in 2024 but is accelerating in 2026 on AI memory. Broader semis remain strong (AI tailwinds), though OSAT faces cyclical risks, China competition, and capex intensity. IMOS has outperformed peers recently on memory exposure.

Bullish FactorsAI memory boom: Persistent demand/supply imbalance in high-value memory for data centers/AI workloads is driving strong revenue, utilization, and visibility.

Recent momentum: Q1 2026 revenue 25.4% YoY (NT$6.94B / US$216.4M); March 23.1% YoY. Memory segment leading; DDIC stabilizing.

Capacity expansion: Ongoing investments in equipment and facilities to capture growth.

2026 outlook: Analysts forecast ~21% revenue growth (to NT$28.99B); media reports of double-digit growth (company clarified to rely on official disclosures, but momentum supports it).

Valuation & dividend: Reasonable relative to growth in some views; 1.83% yield.

Earnings Expectations & Last PerformanceExpectations (TWD): Q2 2026 revenue ~7.19B ( 25% YoY); Q3 ~7.56B ( 23%); full-year 2026 ~28.99B ( 21% YoY). 2027 more conservative/flat at

Last earnings (Q4 2025, reported Feb 2026): Strong rebound—revenue NT$6.52B ( 20.8% YoY), net profit before tax 126%, attributable profit 116%, EPS beat estimates. Full-year 2025 revenue NT$23.93B but net income down YoY (FX/margin pressures earlier in year). Q1 2026 continued the surge.

Financial Breakdown (TWD, in thousands unless noted; TTM/FY2025 ended Dec 2025)Revenue: 23,932,900 (up modestly from prior years; accelerating in 2026).

Gross Profit: 2,538,930 (~10.6% margin; compressed vs. historical due to mix/costs).

Operating Income: 1,142,693.

Net Income (attributable): ~495–551M (profit margin ~2.07%; down sharply YoY in 2025 from FX but rebounding quarterly).

Diluted EPS: ~15.40 TWD (TTM; ADR USD equivalents much lower due to share structure/FX, e.g., recent quarterly ~US$0.46).

Other: Cash ~14.98B; Debt/Equity 68%; ROE ~2.02%; ROA ~1.57%. Free cash flow pressured by capex. Employees ~5,800–5,900.

Margins are lower than peak years (e.g., FY2022 net ~3.44B) due to product mix, costs, and FX, but memory-driven volume/ASP improvements are helping.Stock Price Outlook (Next 12–18 Months)IMOS ADR closed recently around US$45–46 (after a massive ~168% 1-year run and 50% YTD; 52-week range ~15–51). Momentum is bullish on AI memory, with analysts (limited coverage) seeing potential upside (some targets in the $45–60 range in various models). Continued 20% revenue growth and margin recovery could support further gains, especially if memory demand holds and capacity ramps.Risks: High valuation (TTM P/E ~93x), geopolitical/Taiwan-China tensions, DDIC cyclicality, competition, capex/FX volatility, and macro slowdown. Near-term catalysts include Q1 2026 earnings (expected mid-May) and ongoing monthly revenue strength.Overall, bullish bias if AI tailwinds persist—potential 20–40% upside in a strong scenario, but volatile and not without downside risks.

OSAT (Outsourced Semiconductor Assembly and Test) is the back-end segment of the semiconductor supply chain. It involves packaging (assembly), testing, bumping, and related services for integrated circuits after front-end wafer fabrication. OSAT providers handle everything from wafer dicing and die attachment to final testing and shipping of packaged chips, enabling specialization for fabless companies, IDMs, and foundries.Current Market Size and Growth OutlookThe global OSAT market is experiencing solid growth amid the broader semiconductor upcycle, driven primarily by AI but supported by other end-markets.2025 estimates: Around US$45–47 billion, with ~11–12% YoY growth in some reports (inventory rebuilding and early AI

2026 projections: Revenue expected to rise ~12.8% YoY to roughly US$50–52 billion (Digitimes), with other forecasts showing 8–9% CAGR through 2030–2035, potentially reaching US$60–77 billion by 2031 or higher in optimistic scenarios.

Longer-term: CAGRs of 7–9% commonly cited through the early 2030s, with advanced packaging as the key accelerator.

Growth is uneven—advanced packaging (2.5D/3D, chiplets, SiP, fan-out) is outpacing traditional packaging, while testing services are seeing strong demand for AI/HPC validation.

Key Industry Trends (2025–2026 )AI and Advanced Packaging Boom

AI/HPC (especially high-bandwidth memory/HBM, chiplet architectures, and heterogeneous integration) is the dominant driver. OSATs are investing heavily in LEAP (leading-edge advanced packaging) capabilities. Utilization rates for advanced lines are near 90% , with price increases of 5–20% (up to 30% for memory packaging) due to tight capacity.

AI-related revenues are ramping strongly in 2026, offsetting softer areas.

Memory Strength Offsetting Consumer/Traditional Weakness

High-value memory for data centers/AI is fueling revenue (e.g., strong memory testing/assembly). This contrasts with cyclical softness in consumer electronics and earlier DDIC (display driver IC) challenges, though DDIC is stabilizing with some automotive/OLED recovery. Rising costs (materials, labor, energy) are prompting OSAT price hikes, which may flow through to customers.

Geographic and Geopolitical Shifts

Asia-Pacific (Taiwan, China, South Korea) dominates (~80–90% of capacity). Taiwan leads in technology/quality; China is gaining share rapidly. Five Chinese firms were in the global top 10 by revenue in 2025 (e.g., JCET, Tongfu, Huatian), holding ~33% of top-10 share vs. Taiwan's similar portion.

Diversification is accelerating due to geopolitics—new capacity in the US, Europe, and elsewhere (policy-driven "friendshoring"), though talent and ecosystem challenges persist.

Capacity Expansion and Capex Surge

Major players are ramping capex for equipment, new fabs, and advanced packaging (especially for AI and automotive). This includes overseas builds for resilience. However, this increases fixed costs amid cyclical risks.

Cost Pressures and Pricing Power

Rising foundry/OSAT costs, precious metals, and tight capacity (especially for certain packages like COF/COG) are leading to surcharges. This supports better margins but risks downstream pushback.

Technological Evolution Shift to chiplets and hybrid bonding.

Greater integration of testing with AI/ML for efficiency.

Sustainability focus (energy use, geographic diversification).

Automotive electrification and 5G/IoT demanding higher reliability packaging.

Competitive LandscapeThe market is somewhat concentrated but competitive:Leaders: ASE Technology (dominant #1), Amkor, JCET (China's largest).

Others: Powertech, ChipMOS (strong in memory/DDIC niches), Tongfu, etc.

Taiwan still holds technological edge; China is closing the gap on volume/share.

Risks and ChallengesCyclicality and inventory swings.

Geopolitical tensions (Taiwan Strait, US-China trade).

Talent shortages in advanced packaging.

Potential overcapacity if AI demand slows.

Rising input costs and energy prices in Asia.

Overall, the OSAT industry is in a strong upswing phase in 2026, powered by the AI supercycle and advanced packaging demand. It's more resilient than in past cycles due to structural AI tailwinds, but remains sensitive to macro slowdowns, memory pricing, and geopolitics. Traditional volume packaging faces more pressure, while high-end services enjoy pricing power and growth. This bodes well for specialists with AI/memory exposure.

1

3

760

May 3

ChipMOS!

2

1

10

3,305