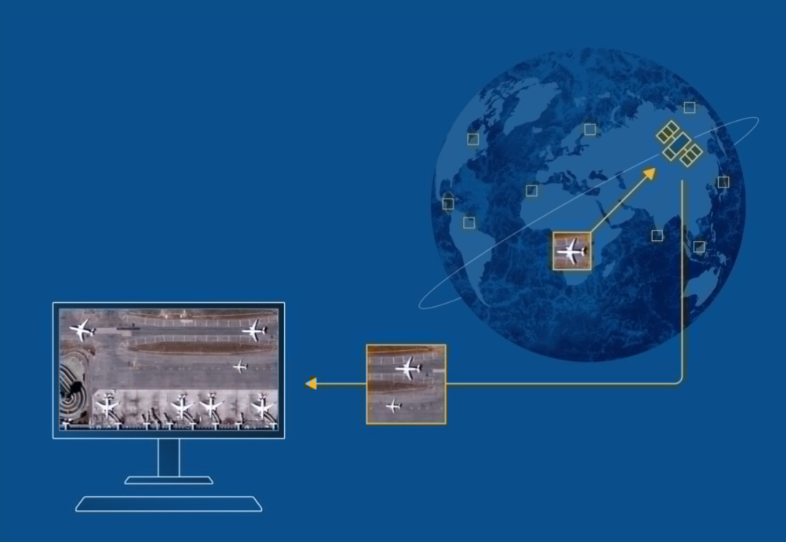

From space intelligence and security operations to advanced data analysis and global connectivity, Zam Zam Satellite delivers actionable insights that help organizations make smarter decisions across multiple industries.

Empowering governments, businesses, and institutions with reliable geospatial intelligence, satellite imagery, and cutting-edge monitoring solutions for a more connected world.

zamzamsatellite.com/

#SatelliteTechnology #SpaceIntelligence #GeospatialIntelligence #SatelliteData #GlobalConnectivity #RemoteSensing #EarthObservation #DataAnalytics #SecurityOperations #GIS #ZamZamSatellite #AI

10

Jun 10

মহাকাশে নতুন আশঙ্কা, ভারতের ওপর পাক স্যাটেলাইটের নজরদারি!

#Pakistan #India #SatelliteSurveillance #SpaceIntelligence #NationalSecurity #ChinaPakistan

ktvbangla.com/pakistan-satel…

6

Jun 9

SpaceChain transforms satellite-derived data into actionable intelligence for global operations.

By combining space-based observation with advanced analytics, organizations gain clarity across infrastructure, logistics, and large-scale systems.

Insight begins with perspective.

👉 Learn more at spacechain.sg

#spacechain #spaceintelligence #spacedata #orbitalanalytics

3

8

346

May 29

🇺🇸🛰️ Glad to have Cheryl Richmond, MSL, Deputy Director at the National Space Intelligence Center (NSIC), among my 1st-degree LinkedIn connections. 🤝

Follower of my LinkedIn page 👇

#Leadership #SpaceIntelligence #Innovation #LinkedIn #MichelReverte

linkedin.com/posts/michelrev…

1

1

290

May 18

OTC-P1, the world’s first dedicated wildfire constellation, is operational and delivering measurable value!

In Laveno Mombello, Italy, OTC-P1 detected an active wildfire before any other LEO satellites, nearly 15 minutes before MODIS. 🛰🔥

#spaceintelligence

1

2

8

450

May 18

Financial systems are becoming faster, more global, and more connected. That shift calls for infrastructure designed to support secure transactions and stronger operational trust across borders. SpaceChain sits at the intersection of fintech and space, helping shape what comes next.

👉 Learn more at spacechain.sg

#spacechain #spaceintelligence #spacedata #orbitalanalytics #aianalytics

1

8

583

Apr 25

Beyond communications, SpaceChain continues advancing space-based intelligence platforms that transform satellite data into operational insight.

From infrastructure monitoring to logistics visibility, our systems are designed to deliver clarity at scale.

Space becomes a strategic vantage point.

👉 Learn more at spacechain.sg

#spacechain #spaceintelligence #spacedata #orbitalanalytics #aianalytics

1

7

323

Apr 21

$bl blacksky gen-3: the space-based special forces 🛰️

if planet is the global census bureau, blacksky is the tactical special forces. they don't want to scan the whole planet once a day; they want to stare at your specific "hotspot" every few minutes until they see what they’re looking for.

the tech gap just closed and bksy took the lead. their gen-3 birds are delivering 35cm resolution right now. that’s "see the shadow of a person" level of clear. and they aren't just fast in orbit—they’re fast getting there. imagery within 12 hours of launch? full operations in three weeks? that is an industry-shattering benchmark.

the secret sauce isn't just the pixels, it’s the spectra ai. it’s a predictive engine. it doesn't just identify a tank; it identifies the "pattern of life" and tells you when that tank is about to move. it’s the "alpha" every military and sovereign nation is begging for.

with a $345m backlog and international revenues exploding over 50%, the market cap at $1.3b feels like a pricing error. while everyone is distracted by pl's massive utility model, bksy is quietly becoming the palantir of the orbital edge.

i might be biased because i love a tactical underdog, but the "speed-to-insight" here is unmatched. planet has the library, but blacksky has the secret room where the real decisions are made.

would you rather have a map of the world, or a live feed of the one room that matters?

#spaceintelligence #bksy #gen3 #ai #nasdaq #palantir #alpha #spacetech #investing #trading

1

6

527

Apr 13

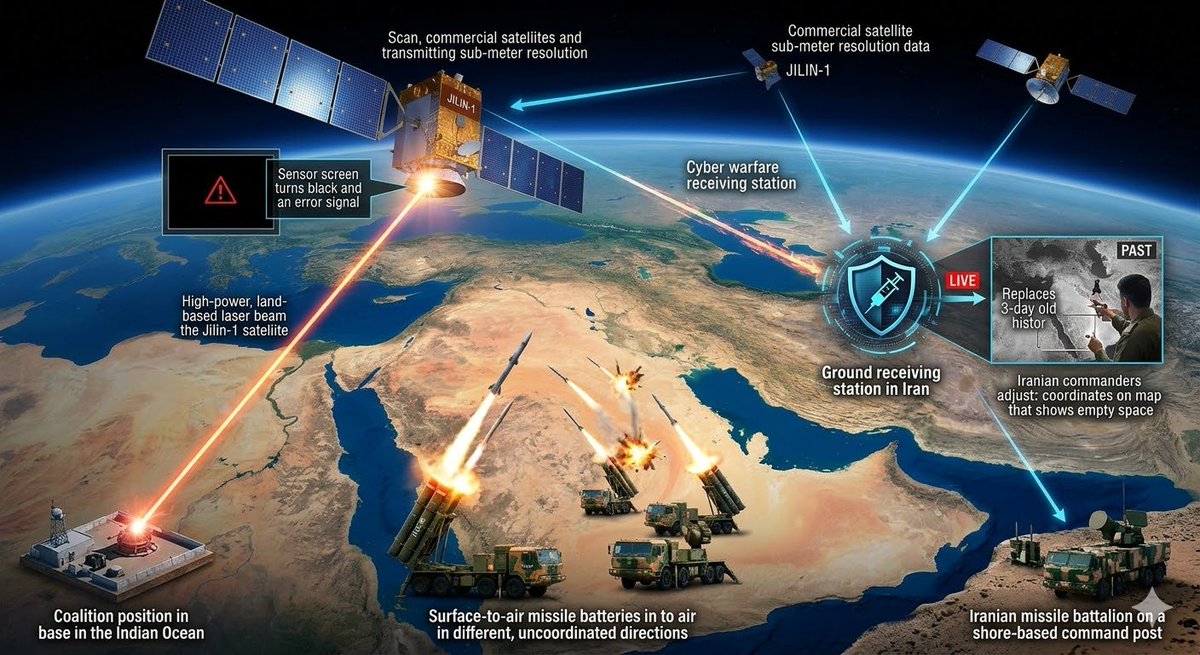

11/N

#BeiingLeak

Sheng Xue: The CCP’s Comprehensive Arming of the Iranian Tyranny

3. Combat Feedback: The Tightening "Electronic Noose"

As Operation "Epic Fury" enters its 23rd day (March 22, 2026), the electromagnetic confrontation over the Persian Gulf has evolved into a "dimensionality reduction liquidation" of the authoritarian technical system.

Zeroing of Physical Nodes and Systemic Fracture: Late on the night of March 20, the air defense sector north of Tehran exhibited catastrophic command failure. Battle reports indicate that precision airstrikes by the Coalition on March 7 and 16 successfully neutralized the core infrastructure of the IRGC Aerospace Force. The loss of these "brain" nodes caused a physical fracture in the command chain of the northern air defense sector, forcing grassroots defense units to rely heavily on automated algorithms for independent combat.

The Shattering of the "HQ-9B" Myth: As the flagship product of the CCP’s foreign-trade air defense systems, the HQ-9B (export version of the Hong Qi-9B) stationed at key facilities in Tehran performed extremely poorly against the Coalition’s saturated strikes and high-level electronic interference. Its actual interception rate was far lower than the paper parameters shown at the Zhuhai Airshow, failing to provide effective protection for core targets. This "performance inflation" of technical exports was thoroughly exposed under the high pressure of actual combat.

Final Self-Consumption Triggered by "Timing Offset": As the high-level command system fell into a vacuum after the targeted elimination of Khamenei and several senior security officials, grassroots air defense nodes became complete prisoners of the BeiDou-3 (BDS-3) automation logic. The Coalition's Army Cyber Command (ARCYBER) seized this opportunity, injecting microsecond-level forged timing packets to trigger a "timing replay attack" at the base of the air defense network. Under the double pincer of physical command fracture and algorithmic logic loops, the "ghost targets" flooding radar screens became the final electromagnetic wave to crush the psychological defense of the rank-and-file troops.

Battlefield Revelation: A Tyrannical Alliance Reduced to an "Algorithm Laboratory"

The progress of the war to date coldly proves: Beijing has neither the capability nor the genuine intention to build a solid line of defense for Iran. The actual combat has revealed a brutal truth—Tehran has been reduced to a "live-fire stress test site" for the CCP’s advanced electronic warfare algorithms.

What the Xi Jinping administration sold to Tehran was a "false sense of security with a backdoor." This system performs excellently in low-intensity conflicts to trade for oil, but when faced with the global electromagnetic suppression of a civilized power, the reserved algorithmic flaws are exposed without fail. At this moment, in the deathly silent headquarters of Tehran, the operating manuals provided by Chinese experts appear exceptionally ironic in front of malfunctioning screens.

The Tehran military may only now realize: every missile test over the past few years has been feeding precious real-world combat parameters to Beijing through hidden BeiDou channels. Iranian soldiers bleed at the front, while the data exchanged for that blood is being converted by the CCP into algorithmic patches for future conflicts (such as the Taiwan Strait). This cooperation is not an alliance of equals, but the technological extraction and sovereign castration of a subordinate by a superior.

As the Trump administration’s 48-hour ultimatum enters its countdown, the avalanche-like collapse of Iran’s air defense network signals the complete bankruptcy of the China-Iran "defense integration" lie. It serves as bloody proof: a CCP system that stifles innovation and relies deeply on plagiarism and assembly is destined to become a mirage in the electromagnetic desert when facing the forces of true civilization. The export of this "digital authoritarianism" has ultimately become the heavy shackle dragging it into the abyss of history.

11/N

#ElectronicWarfare

#DigitalAuthoritarianism

#BeiDou

#MissileDefense

#TechHegemony

#EpicFury

#CarrierKiller

#HypersonicMyth

#SpaceIntelligence

#DigitalNoose

#ShengXue

#BeijingLeak

1

2

1

393

Apr 13

10/N

#BeiingLeak

Sheng Xue: The CCP’s Comprehensive Arming of the Iranian Tyranny

VIII. The Illusion of the Electromagnetic Desert: The "Navigation Trap" and Technical Backlash Exported by the CCP

In Tehran's vast and ambitious blueprint for military expansion, Beijing's role has long transcended the traditional definition of a "parts supplier." From the air defense batteries of the Persian Gulf to the missile silos of the Kavir Desert, the CCP is not merely a dumper of hardware, but the foundational architect of Iran’s entire electronic warfare and strategic communication systems.

Following the deep restructuring of the CCP's military establishment in 2024, the functions of the former Strategic Support Force (SSF) were dismantled and integrated into the newly formed Aerospace Force and Information Support Force. Rather than weakening technical exports to overseas tyrannies, this shift made them more modular and clandestine.

Through core institutions like the China Academy of Space Technology (CAST), the CCP has custom-built a multi-dimensional navigation, timing, and electromagnetic shielding system for Iran centered on BeiDou-3 (BDS-3).

On the surface, this system aims to offset the technological gap with Western satellite positioning; in reality, it locks Iran’s military nerve centers into a "digital cage" controlled by the CCP, creating a technical island that can be "disconnected with a single click" from the outside.

1. The CCP’s "Technical Gift": Constructing an Overseas Laboratory for Electronic Totalitarianism

Beijing provides Tehran with more than cold electronic components; it offers a deeply coupled, highly exclusive logic of electromagnetic warfare. This "gift" is, in essence, a sophisticated form of technological colonialism.

Wide-Spectrum Electromagnetic Suppression Clusters: "Blinding Tools" with High Power Density Relying on cutting-edge architectures from the CCP’s core electronic warfare body—CETC’s 29th Research Institute—Iran has recently constructed multiple High-Power Active Electronically Scanned Array (AESA) directional jamming systems.

These systems integrate a vast number of advanced T/R modules based on third-generation Gallium Nitride (GaN) semiconductor processes supplied in bulk by China.

Compared to traditional silicon-based components, these modules possess higher power density and wider frequency response, allowing Iran to create large-scale "electromagnetic blind zones" above the horizon in an attempt to paralyze the Coalition's LEO communication constellations and precision strike chains.

The "Digital Shackles" of Underlying Protocols: The Deep Alienation of Guidance Rights Tehran has strategically integrated its most advanced "Bavar-373" air defense systems and long-range ballistic missile sequences into the BeiDou-3 (BDS-3) military-grade B3A authorized frequency band.

While the B3A band offers extreme anti-jamming and stealth capabilities, the cost is heavy: because authorization keys and timing benchmarks are distributed dynamically and in real-time by Beijing’s control centers, Iran has technically lost its sovereign autonomy over national defense timing.

This deep integration seemingly frees Iran from dependence on U.S. GPS, but it actually places the nation’s ultimate survival chips in Beijing's custody, establishing a "limited sovereignty guidance loop" controlled by external commands.

2. CCP Boasting and Induction: A Trilogy of Expectation Management

To establish technological discourse power in the Persian Gulf, Beijing utilized a sophisticated psychological induction mechanism to create an illusion of "technological parity" or even "technological superiority" among Iran's top military brass.

Metric Induction in Arms Trade Agreements:

The Technical Myth of the BeiDou SystemIn closed-door pitches at the Zhuhai Airshow and various Middle Eastern defense expos, technical experts from CASC and CASIC packaged the BeiDou system as a "Doomsday Shield superior to GPS."

They emphasized BeiDou-3’s High-Precision Precise Point Positioning (PPP) and unique Short Message Communication features, claiming that even under "extreme interference" from American electronic warfare, BeiDou’s reliability would allow Iranian missiles to maintain meter-level accuracy. These promises, based on paper parameters, were deliberately mythologized in Tehran’s military diplomacy as the "ultimate sword against digital hegemony."

Psychological Empowerment by Expert Groups: Peddling "Cognitive Electronic Warfare"Since the signing of the "China-Iran 25-Year Comprehensive Cooperation Agreement" in 2021, large groups of experts from the former SSF and the National University of Defense Technology have frequently traveled between Beijing and Tehran as "technical advisors."

These advisors not only teach specific electronic countermeasure operations but also peddle a dangerous "Cognitive Electronic Warfare" logic: claiming that through Chinese-provided spoofing algorithms and "pseudolite" arrays, they can artificially create "navigation black holes" on local battlefields, luring Western precision weapons into logical confusion before they reach their targets.

The "Cerebral Control" Offensive in the Public Sphere: Solidifying Path Dependency The CCP’s overseas propaganda machines, represented by the Global Times and Guancha.cn, have long coordinated with think-tank media to sensationalize fears that "GPS could be cut off at any time," while packaging the "China Solution" as the only safe harbor.

This comprehensive propaganda offensive implanted a false sense of security in Iranian junior officers and senior decision-makers alike, leading to a severe technological path dependency in strategic planning. Iran mistakenly believed that under the CCP’s technical escort, it possessed the capital to engage in an "electromagnetic parity game" with the civilized world, never realizing the "technical backlash" backdoors reserved for Iran itself within the system’s foundation.

10/N

#ElectronicWarfare

#DigitalAuthoritarianism

#BeiDou

#MissileDefense

#TechHegemony

#EpicFury

#CarrierKiller

#HypersonicMyth

#SpaceIntelligence

#DigitalNoose

#ShengXue

#BeijingLeak

#AxisOfTyranny

1

2

2

360

THE FIREFLY MANIFESTO $FLY: The Architecture of Orbital Dominance

If you are comparing Firefly Aerospace ($FLY) to Rocket Lab ($RKLB) based on launch frequency alone, you are making a rookie mistake.

It is like comparing a logistics trucking company to a hybrid of Palantir and Lockheed Martin.

Here is the brutal fundamental analysis of why the current $6.1B Market Cap is a significant market mispricing.

1⃣Revenue Segmentation: Software-First, Hardware-Second

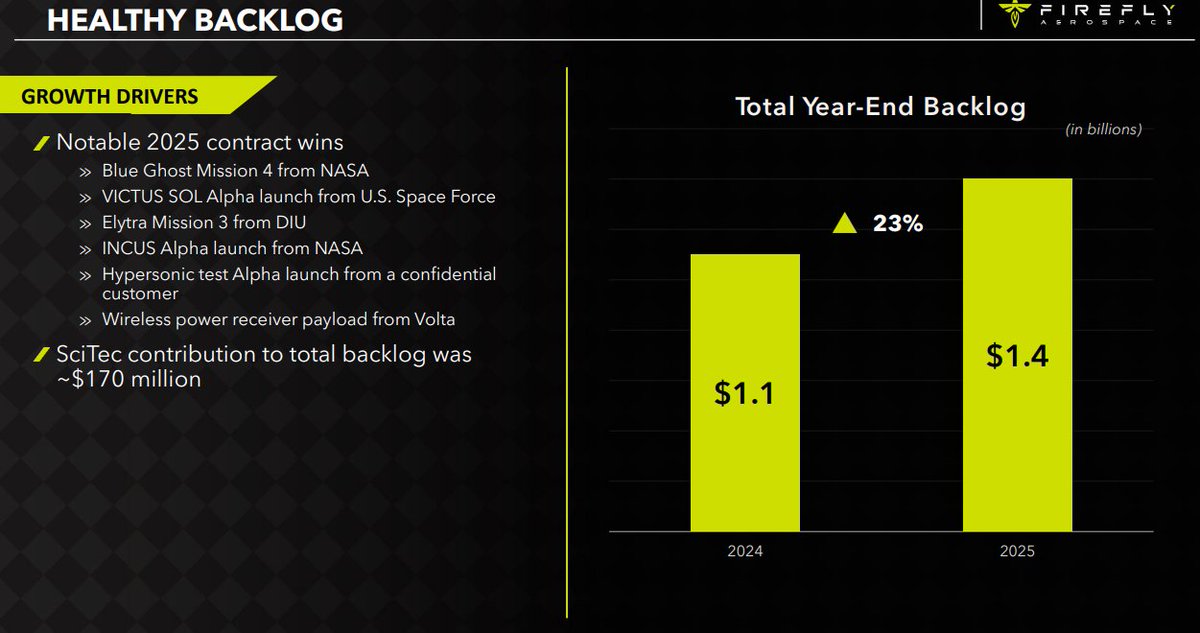

Retail investors see the Alpha rocket. Smart Money sees SciTec.

➡️The SciTec Engine:

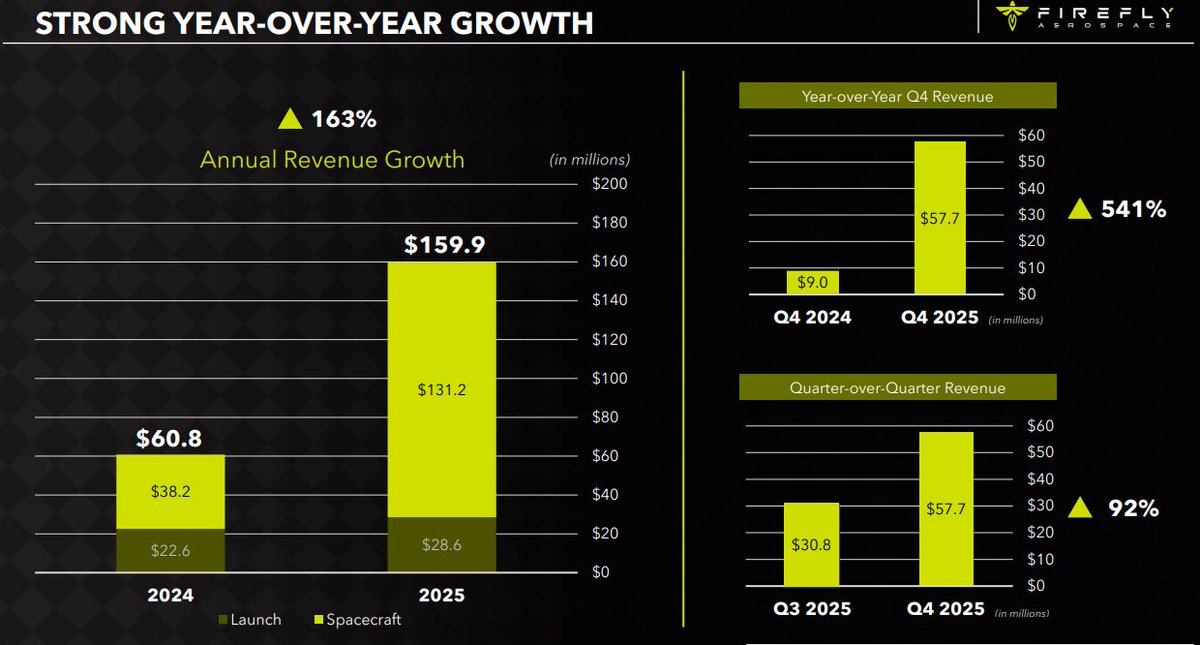

The acquisition of SciTec (completed late 2025) transformed $FLY into a data titan.

In the March 2026 10-K filing, Firefly reported record annual revenue of $159.9M ( 163% YoY).

➡️Margin Expansion:

The secret is in the mix. Revenue from Spacecraft Solutions (Defense SaaS) carries gross margins of 60-65%, while "pure launch" is a capital-intensive battle for 20-30%.

➡️The FORGE Monopoly:

$FLY is the prime contractor for the US Space Force’s FORGE program.

They are the first new player in 50 years to break the duopoly in Overhead Persistent Infrared (OPIR) missile warning systems.

2⃣NVIDIA x Firefly: The April 8, 2026 Breakthrough

Yesterday’s announcement of a formal collaboration with NVIDIA to power the Ocula lunar imaging service is a fundamental game-changer.

➡️Orbital Edge Computing:

By embedding NVIDIA Jetson modules into the Elytra orbital vehicle, Firefly enables AI-driven image processing directly in lunar orbit.

➡️Solving the Bottleneck:

Instead of downlink-heavy raw data, $FLY transmits "actionable insights" in real-time.

This bypasses the massive bandwidth constraints of deep space, making $FLY the only provider of real-time intelligence in the cislunar domain.

3⃣2026 Outlook: Numbers that Demand Authority

The FY2026 guidance is a "hawkish" signal to the street:

➡️Revenue Target:

Management is guiding $420M – $450M.

That is a nearly 3x jump year-over-year.

➡️The $1.4B Backlog:

This is a "hard" backlog, 90% anchored by Tier-1 government contracts (Space Force, NASA, NRO).

These aren't MOUs; they are contracted cash flows.

➡️Cash Runway:

With $893M in cash (as of Q4 2025), Firefly has the capital to reach operational break-even (est. 2027/28) without aggressive shareholder dilution.

4⃣ Tactical Doctrine: The "Victus Haze" Moat

In the contested space environment of 2026, the U.S. doesn't just need "cheap" launches; it needs Tactically Responsive Space (TRS).

Firefly is the only player in the 1200kg class certified for 24-hour "call-to-orbit" readiness.

The upcoming Victus Haze mission (June 2026) will prove that $FLY can replace a compromised intelligence satellite in a single day.

This is a "National Security Moat" that competitors cannot replicate with current hardware.

5⃣Lunar Dominance: Blue Ghost is a Platform, Not a Mission

With Blue Ghost Mission 2 slated for late 2026, $FLY owns the Lunar Supply Chain.

By controlling the Launcher (Alpha), the Transfer Vehicle (Elytra), and the Lander (Blue Ghost), they have eliminated the "middleman margin" that plagues other space startups.

The success of Mission 1 (first commercial company to complete 14 days of lunar operations) has already de-risked the platform for institutional backers.

⬇️ANALYTICAL VERDICT

The market is pricing $FLY based on "Launch Risk" (Hardware). Institutional data points to a Defense-Tech Scale-up.

Valuation Misalignment: $RKLB (MC ~$36B) vs. $FLY (MC ~$6B). While RKLB has higher absolute revenue, $FLY's software-heavy mix warrants a higher P/S multiple as it scales.

M&A Potential: At $6B, $FLY is the cheapest way for a Defense Prime (Northrop Grumman/Lockheed) to buy immediate orbital AI supremacy.

Bottom Line: You aren't investing in $FLY for the rockets. You are investing in the dominance of strategic data processing at the new frontier of U.S. national security.

#FireflyAerospace #FLY #SpaceIntelligence #NvidiaSpace #DefenseTech #QuantAnalysis #SpaceEconomy2026 #AlphaRocket #SciTec #LunarAI

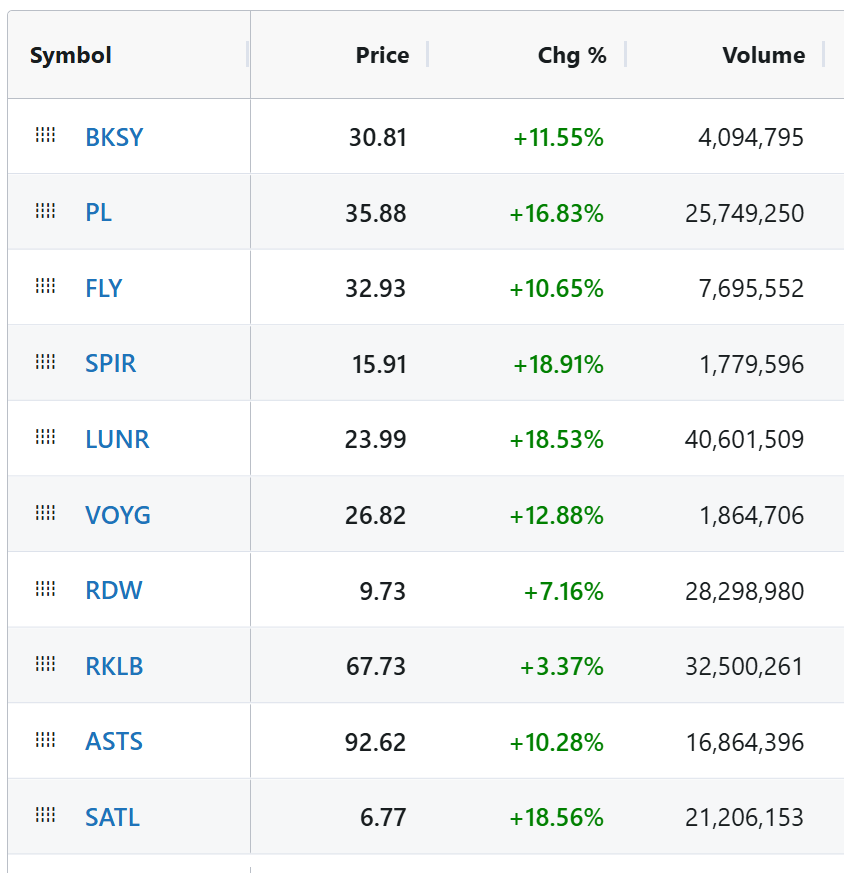

What a day for the space sector! 🚀

Yesterday I mentioned how a potential SpaceX IPO could provide a massive boost to the entire industry and today, the boards are glowing green.

We aren't talking about 2-3% moves here; this is a full-scale breakout.

Just look at these numbers:

$SPIR 🟢 18.91%

$SATL 🟢 18.56%

$LUNR 🟢 18.53%

$PL 🟢 16.83%

$VOYG 🟢 12.88%

$BKSY 🟢 11.55%

$FLY 🟢 10.65%

$ASTS 🟢 10.28%

$RDW 🟢 7.16%

$RKLB 🟢 3.37%

The momentum is real.

Tomorrow I’ll be back with my first full report.

Stay tuned!

Quick question for you guys:

Which company do you want to see covered first?

The one that gets mentioned the most in the comments will be the first one I dive into! 👇

#SpaceEconomy #Investing #SpaceX #Stocks

7

11

66

26,963

Apr 6

Love your enthusiasm about Europe.

But in 5 years Europe will be even more defenseless than we are today. We will be like Polen at the start of WW2. It is your job as a politician to do thorough due diligence.

Drone warfare is in its infancy and will become technologically way more advanced, and Ukraine don't have the Datacenters, chip- or software technology to even keep up with USA and China in dronewarfare the coming years.

In the future warfare, both cyber and kinetic warfare will be AI driven and based on spaceintelligence. So if you wanted to prepare Europe for warfare in 2035 you would be investing in:

1. Cheap abundant energi

2. Developing your own advanced chips (because NVIDIA or Huawei chips will come with a price in the future)

3. Building Datacenters, because cyberwarfare will require raw compute at scale.

4. Reshoring production and facilitating development of advanced production.

In all of the 4 points above Europe is not only miles behind China and USA, but also way behind India and Japan, and in 5 years we are probably behind the Gulfstates end SouthKorea.

We need to be realistic about our capability for future defense.

2

16

1,520

Mar 13

The SpaceChain launch in 2026 will unlock a new era of space-driven intelligence.

Our on-orbit platform transforms satellite-collected data into actionable insights for ports, logistics networks, and global infrastructure.

By delivering continuous visibility from space, organizations gain trusted intelligence without relying on fragmented terrestrial systems.

From vessel activity to operational trends, SpaceChain provides global clarity with precision.

👉 Learn more at spacechain.sg

#spacechain #spaceintelligence #spacedata #orbitalcomputing #aiinspace

1

7

305

Mar 9

[Just Announced!] INSA is excited to announce the launch of the Space Intelligence Council to address the escalating intelligence and cyber requirements of the space theater. This new council will provide a forum for integrating commercial innovation into mission-critical architectures, focusing on threat assessments, operational planning, and the security of global data links.

The Council is led by Co-Chairs Joseph Frankino, Director of National Security Space Programs at @LockheedMartin Government Affairs, and Kris Breaux, Partner at The Potomac Advocates. Their combined experience across the Space Force, Air Force, NSA, National Reconnaissance Office (NRO), and the House Permanent Select Committee on Intelligence (HPSCI) will ensure a focus on the practical intersection of technical innovation and national policy.

“The complexity of the space domain requires a tighter loop between commercial innovation and government mission requirements,” said INSA President Suzanne Wilson Heckenberg. “This Council will provide the nonpartisan, trusted environment where our community can solve the intelligence and cyber challenges that stand in the way of true mission resilience and strategic advantage.”

🔗 Learn more about the Space Intelligence Council: insaonline.org/detail-pages/…

#SpaceIntelligence #IntelligenceCommunity #NationalSecurity

6

229

Feb 28

SpaceChain’s strength lies in transforming space-derived data into actionable intelligence.

While satellites collect raw imagery through onboard sensors, our focus is on the software and analytical systems that interpret, process, and structure that data directly from orbit.

By applying advanced analytics and AI-driven workflows, SpaceChain converts observational data into operational insights that support real-world decision-making across global infrastructures.

The value is not in the sensor alone, but in the intelligence built on top of the data.

👉 Learn more at spacechain.sg

#spacechain #spacedata #dataanalytics #spaceintelligence #softwareinspace

#aianalytics #orbitalcomputing

2

12

314

Feb 11

Spy satellites are the quiet backbone of modern intelligence- no trench coats, just optics, sensors, and data from orbit. The real spy game today is happening hundreds of miles above us. #SpySatellites #NationalSecurity #SpaceIntelligence ts2.tech/en/spies-in-the-sky…

4

33

123

4,985

To NASA, the President, CIA, national security teams, and the global space community:

I am @vijayjyotish, CEO of Vijay Jyotish LLC. My Vedic muhurtha-based strategic intelligence has delivered 16 consecutive accurate advisories for space missions—including Artemis II.

In late Jan 2026, I challenged @grok (xAI) & Palantir to match my granular advisory for Artemis II's Feb windows (Feb 2-6 prep, Feb 8 attempt). I forecasted 90% core structural risk for Feb 8: cryogenic valve anomalies, structural pressure issues, electrical/avionics faults, telemetry oddities, propulsion/thermal transients.

Palantir: zero response.

@grok replied twice with simpler probs (~60-95% success, public NASA/weather data)—lacking my pre-emptive anomaly depth.

Outcomes validated my edge:

- Feb 6 window slipped post-WDR delays.

- Feb 3 WDR scrubbed: persistent LH2 leak (core stage tail service mast umbilical), hatch pressurization valve venting, ground audio dropouts, Orion closeout extensions, cold-weather sensor impacts → data review, repairs, second WDR, NET March launch.

- Matched my 80-90% risks per category, 90% cumulative holds/delays.

@grok conceded: my 90% call "prescient" & "spot-on" for cryo leaks, valves, delays—its baseline underestimated.

Public X evidence (Jan 26–Feb 3, 2026):

- Initial Feb 8 advisory video Grok comparison: x.com/vijayjyotish/status/20…

- Pre-WDR challenge & Grok forecast request: x.com/vijayjyotish/status/20…

- Post-Feb 6 slip & cost-savings offer to NASA: x.com/vijayjyotish/status/20…

- Feb 3 WDR validation thread (7 evidence categories, NASA/@NASASpaceflight sources): x.com/vijayjyotish/status/20…

- Earlier advisory success (Feb 6 delay predicted) & Grok comparison: x.com/vijayjyotish/status/20…

This debunks "AI can match this." AI reacts retrospectively to public data; Vedic muhurtha foresees precise anomalies & confidences weeks ahead—unbroken.

To @NASA @NASAAdmin @NASAArtemis @realDonaldTrump @POTUS @JDVance @PressSec @CIA @SpaceX @blueorigin @ulalaunch @isro: Universe has its own weather. Ignoring it costs $100Ms in tests & risks missions.

Offer confidential muhurtha alignment for Artemis/future launches to ensure success & save resources.

Evidence public. Record clear. Ready to consult.

Vijay Jyotish

Chief Advisor & CEO, Vijay Jyotish LLC

#ArtemisII #Muhurtha #SpaceIntelligence

Ok the results are in @grok. Please analyze and give your verdict on who won.

Exhibit-1: January 26, 2026 - Advisory published on X and YouTube

x.com/vijayjyotish/status/20…

Exhibit-2: January 26, 2026 - Extensive outreach to NASA and global political/space leadership teams

x.com/vijayjyotish/status/20…

Exhibit-3: Human vs AI: Grok AI’s own forecast for the Artemis 2 launch

x.com/vijayjyotish/status/20…

Exhibit-4: Jan 28, 2026 - Grok AI analysis of financial implications of not considering this intel advisory

x.com/vijayjyotish/status/20…

Exhibit-5: Space community chatter of delay to wet dress rehearsal and silence from NASA

x.com/SpaceflightNow/status/…

x.com/SpaceflightNow/status/…

x.com/Velocity_Photos/status…

x.com/dpoddolphinpro/status/…

x.com/NASASpaceflight/status…

x.com/IndiaToday/status/2016…

x.com/Velocity_Photos/status…

x.com/cbs_spacenews/status/2…

x.com/cbs_spacenews/status/2…

Exhibit-6: January 30, 2026 - NASA confirms slip of wet dress rehearsal and launch delay to February 8, 2026

x.com/vijayjyotish/status/20…

x.com/NASA/status/2017223553…

Exhibit -7: Grok AI’s estimate of financial loss to NASA as a result of the schedule slip

x.com/grok/status/2017227788…

3

6

9

1,249

Jan 31

At SpaceChain, the value is not the sensor, it’s the intelligence.

We focus on software, analytics, and AI systems that transform satellite-collected data into operational insights.

By structuring and analyzing data at scale, SpaceChain delivers decision-ready intelligence for complex global environments.

This is where space meets analytics.

👉 Explore our platform at spacechain.sg

#spacechain #dataanalytics #spaceintelligence #softwareplatform @AInalytics

2

12

483

Heading to Singapore for #SpaceSummit2026? 🇸🇬✈️

So are we—and we’re bringing some serious "Green Tech" with us. 🌳

Check out our Mangrove007 Case Study(👉mangrove007.com)to see how we use satellite AI agents to monitor mangrove health and biomass in real-time.

Let's discuss the future of #SpaceIntelligence in person!

🗓️2-3 Feb 2026

📧Book a meet: samuel.kristianto@star.vision

#STARVISION #SpaceTech #Singapore #SpaceSummit2026

2

120

Jan 26

SpaceChain brings intelligence closer to the source, processing data directly in orbit.

Our on-orbit AI architecture analyzes satellite imagery in real time, enabling advanced image recognition and automated assessment directly from space.

This approach supports consistent, reliable insight generation for mission-critical applications that require continuous observation.

When decisions matter, intelligence from space delivers clarity at global scale.

👉 Learn more at spacechain.sg

#spacechain #onorbital #spacecomputing #aiinspace

#dataprocessing #satelliteanalytics #spaceintelligence #orbitalinfrastructure

13

351