While working-class families struggle with a brutal cost-of-living squeeze, elite MPs handed themselves a massive 5% pay rise this April, pushing their basic salary to £98,599. They always look after their own. #UKPolitics #WorkingClass

3

This can be answered only by our very own @_sabanaqvi @khanumarfa @RanaAyyub @asadowaisi.

It could be that English speaking Muslim women are exempt from Burqas, Hijab etc.

But women of workingclass background have to cover themselves up.

6

The people who keep hospitals, schools, and public services running deserve better than pay cuts in real terms. Workers are standing together and demanding fair wages. #StrikeAction #WorkingClass #FairWages #UnionStrong

2

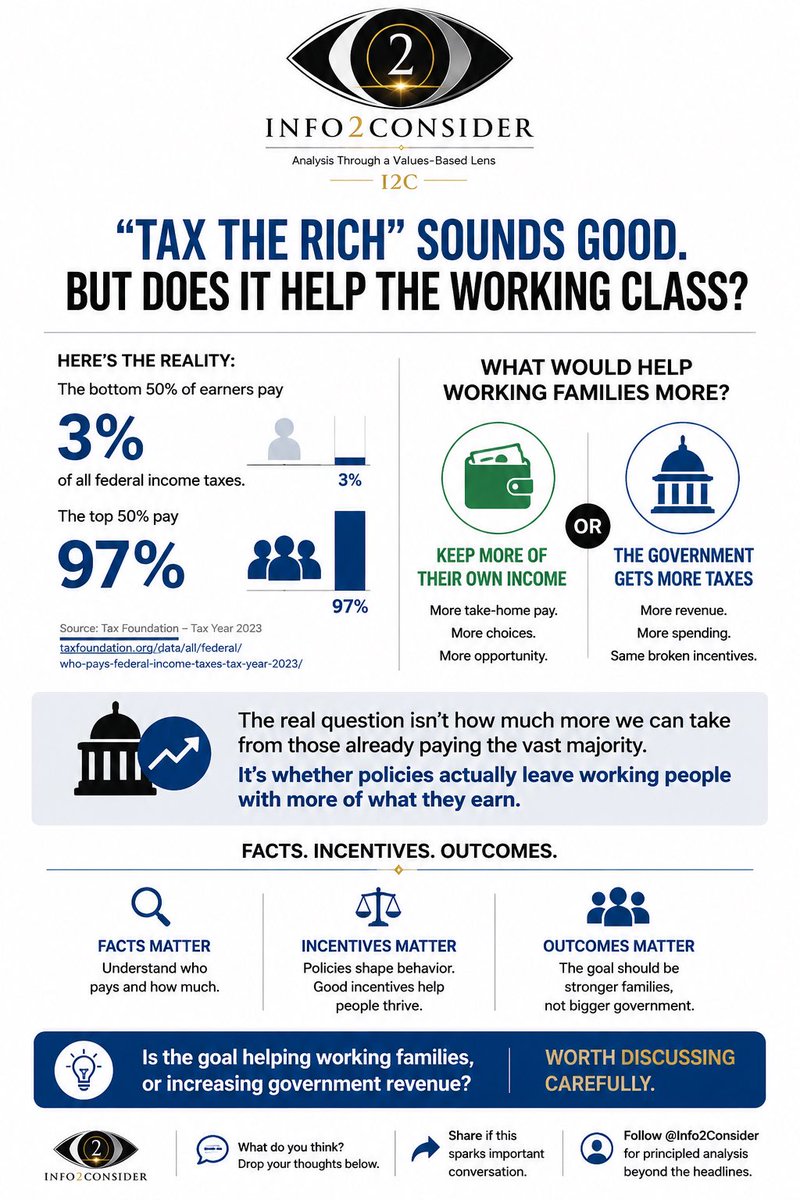

“Tax the Rich” sounds like a solution for working-class Americans.

But here’s a question:

If the bottom 50% of earners only pay about 3% of all federal income taxes, how does collecting even more taxes from higher earners improve the financial situation of those already paying little or no federal income tax?

Would working families benefit more from:

• Keeping more of their own income?

Or

• The government collecting more revenue from the people already paying roughly 97% of federal income taxes?

This is where the debate often shifts from helping the poor to expanding government revenue.

A serious discussion should ask not only who pays, but whether policies actually leave working people with more of what they earn.

Facts matter. Incentives matter. Outcomes matter.

What do you think? Is the goal helping working families, or increasing government revenue? Worth discussing carefully.

Source: Tax Foundation analysis of 2023 federal income tax data: taxfoundation.org/data/all/f…

#TaxPolicy #Taxes #Economics #WorkingClass #PublicPolicy #Info2Consider #CriticalThinking #FiscalPolicy

12

Such an important nuanced, thoughtful conversation - only the BBC does this. Please consider listening. What has happened to #workingclass #identity in Britain? @AdamRutherford explores the political fractures within #families and #communities.1/ bbc.co.uk/sounds/play/m002xn…

1

2

79

Lyari is often reduced to a story of crime, but its true legacy is defined by resilience, sports, and grassroots political participation.

By Mir Fahad Gabol

@Fahad_Gabol

Read: thefridaytimes.com/15-Jun-20…

#KarachiHistory #Lyari #Sociology #Sports #UrbanPakistan #Media #WorkingClass

2

1

43

ミーコ♪ retweeted

"Working class heroes! Proudly standing together for our rights."

@skinheadgirlstyle

#workingclass #bootsandbraces #skinheadstyle #punks #spiritof69

2

10

448

Why would you believe that #Farage & #ReformUK would put the welfare of the #Workingclass first? Why would you ignore the red flags? Why would you allow yourself to be duped by #Tories in a different coloured suit? The BIG question is, HOW FUCKING STUPID ARE YOU? #makerfield.

11

So @JackOsbourne is MAGA.

That's pretty pathetic.

@OzzyOsbourne is turning in his grave. A workingclass guy who sang WAR PIGS got a son on Trumps dick.

Sad.

14

A Billionaire Is Mad You Bought a $28 Lunch

Tim Dillon reacts to Kevin O'Leary telling Gen Z workers making $70k a year that spending $28 on lunch makes them financially stupid. 💀#TimDillon #KevinOLeary #WorkingClass #Comedy #TimDillonShow #PodcastClips #GenZ #Podcast #Wealth #Finance

22

You're insufferable. It's the biggest event in the world and he's making it so that the workingclass can enjoy it. New Yorkers love what Mamadani is doing. He's extremely popular.

16

105

youtu.be/HJZ2JXLGnz4?si=QCSw… via @YouTube

Fight For What Is Right* is a powerful anthem for Makerfield — for families, workers, communities, and everyone who believes the future can be better. This song is about hope, strength, local pride, and standing up for what matters: our children, our families, our towns, and our future. Makerfield has a proud history — coal mining, textile manufacturing, industrial strength, green spaces, and strong community spirit. Now it’s time to look forward. *Vote for Robert Kenyon — for the people of Makerfield.* *Not using this as a stepping stone.* *Fight for what is right. Vote Reform.* If you’ve never voted before, if you’ve been on the sidelines, if you feel forgotten or unheard — this song is for you. For our families. For our future. For Makerfield. Message: Vote Reform Party — Vote Robert Kenyon #Makerfield #RobertKenyon #ReformUK #VoteReform #NorthWestEngland #UKPolitics #BritishPolitics #VoteForChange #TimeForChange #GeneralElection #LocalElection #Vote2026 #ElectionSong #PoliticalSong #CampaignSong #ProtestSong #Anthem #WorkingClass #WorkingFamilies #FamilyFirst #ForOurChildren #ForOurFuture #CommunityFirst #LocalPeople #LocalPride #BritishWorkers #ForgottenPeople #FirstTimeVoters #NeverVotedBefore #SilentMajority #PeoplePower #StandTogether #WeRiseTogether #FightForWhatIsRight #BritainFirstNotParty #ProudPastBrightFuture #IndustrialHeritage #CommunitySpirit #LabourParty #ConservativeParty #LibDems #GreenParty #ReformParty #VoteRobertKenyon

22

On the anniversary of Che’s birth, remember: legacy isn’t something you wear. It’s something you understand, uphold, and fight for! #che #cheguevera #workingclass

5

"In other words, he has lost the faith of his most loyal supporters on the year’s most pressing issue." #Trump #WorkingClass

nytimes.com/2026/06/13/us/po…

24

The California Wealth Tax is Fraud: "Its proponents are so bad at analysis, it's really deception"

From Saturday's WSJ

The Deceptive Statistics Behind California’s Wealth Tax

You’ve heard the claim that billionaires pay a lower tax rate than workingclass Americans. It’s at the center of the case for California’s “Billionaire Tax” initiative, which would impose a 5% levy on the net worth of the ultra-wealthy. Almost every version of this claim traces back to economists Emmanuel Saez of UC Berkeley and Gabriel Zucman of the Paris School of Economics.

They teamed up with the SEIU United Healthcare Workers last year to place the measure on the California ballot. Mr. Saez worked with lawyers to draft “several rounds of wealth tax proposals,” and the original idea came from a 2021 policy brief he adapted from a co-authored book with Mr. Zucman.

The pair have released a flurry of working papers that aim to lend scholarly heft to the ballot measure. They tout it as a scientifically supported extension of dispassionate economic research on inequality and a purported fiscal crisis caused by insufficient taxation.

But the numbers don’t add up. For years the pair have relied on selective accounting methods and questionable assumptions to tilt the scales in favor of confiscatory wealth taxes.

The first problem lies in how Messrs. Saez and Zucman measure taxable wealth. Under the U.S. system, taxes are generally assessed on income earned over the course of a year. Since 1920, federal tax law has followed the realization principle, meaning that income must actually be realized as earnings before it can be taxed. Messrs. Saez and Zucman instead propose taxing estimated changes in a person’s net worth—including unrealized capital gains that exist only on paper. If a billionaire’s stock portfolio rises in value, they want to tax the appreciation even if the assets are never sold.

Unrealized gains are notoriously volatile and speculative. They can disappear overnight with a market downturn. Federal courts have long viewed taxes on unrealized gains as constitutionally dubious, which is why Messrs. Saez and Zucman have shifted their efforts to the state level. California’s proposal is an attempt to circumvent the constitutional constraints that would doom a federal wealth tax.

Another problem is even more basic: The underlying wealth estimates are deeply unreliable. Because billionaire tax returns are private,

Messrs. Saez and Zucman rely heavily on outside estimates of billionaire wealth. One of their favorite

sources is the Forbes 400 list.

What they rarely acknowledge, though, is that the Forbes rankings were never designed to function as a tax database. The list has long suffered from what might be called the Donald Trump Problem. In the 1980s and ’90s, Mr. Trump repeatedly called Forbes reporters, at least once under a fake name, to lobby for higher estimates of his fortune.

But the problem extends far beyond Mr. Trump. The Forbes 400 carries enormous cachet, creating incentives for wealthy Americans to exaggerate rather than minimize their fortunes.

There is strong evidence that these estimates are systematically inflated. An analysis by Internal Revenue Service statisticians compared probate records for 376 deceased members of the Forbes 400 between 1982 and 2009 against the wealth Forbes attributed to them. On average, the net worth reported for tax purposes was only about half the amount estimated by Forbes.

Yet another problem concerns Messrs. Saez and Zucman’s headlinegrabbing claim that billionaires pay lower tax rates than ordinary workers. As part of their wealth-tax advocacy, the pair has repeatedly asserted that the ultrarich pay a combined federal, state, and local tax rate of only 23%, supposedly lower than the 24% working-class Americans pay.

Both figures are manipulated. In fact, Messrs. Saez and Zucman’s own earlier research told a very different story. In a 2018 paper published in the Quarterly Journal of Economics, their own data files showed that the top 0.001% pay an average combined tax rate of roughly 41%. So where did the new 23% figure come from?

The answer lies in an accounting gimmick involving the corporate income tax. For decades, mainstream economists have recognized that the burden of corporate taxation is shared among shareholders, employees and consumers. Corporate taxes can reduce wages, depress investment returns and raise prices.

Messrs. Saez and Zucman previously acknowledged this long-established understanding, including in their 2018 paper. When they shifted into wealth tax advocacy, however, they changed their approach and assigned the full burden of the corporate tax to shareholders alone. Because stock ownership is concentrated among the wealthy, and because the corporate rate is lower than top individual income-tax rates, this maneuver dramatically lowers the apparent tax rate paid by billionaires.

By changing the accounting assumptions, they transformed a 41% effective tax rate into a politically explosive 23% talking point. And as their latest academic study indicates, they built this dubious approach to corporate tax incidence into their claims about the California tax proposition.

At the same time, they artificially inflate the tax burden borne by lower-income Americans. The federal income tax is intentionally progressive, and one of its most important antipoverty mechanisms is the Earned Income Tax Credit. The EITC frequently reduces federal incometax liability for low-income workers to zero and in many cases provides net refunds.

Messrs. Saez and Zucman simply omit the EITC from their calculations. That creates the illusion that low-income Americans pay far more in taxes than they actually do. Harvard economist Jason Furman finds that the bottom 20% of Americans face an overall combined tax burden of approximately 11%—less than half the figure Messrs. Saez and Zucman claim.

The billionaire-tax movement depends heavily on stoking public outrage fueled by misleading statistics. Americans should be skeptical anytime activist academics present enormously complicated tax calculations as simple moral certainties.

By Phillip W. Magness

Mr. Magness holds a chair in political economy at the Independent Institute.

25

Such a beautiful family @JDVance, and a @POTUS administration for people with families, for the #WorkingClass...

...

I wish you to remain in History with this!

Happy Anniversary to our lovely Second Lady. 12 years and almost 4 kids later, and we're still going strong. Love you Usha!

1

82

अब न्यूनतम वेतन नये मापदण्डों के आधार पर तय होगा

#minimumwage #determined #basedon #newcriteria #Under #newcode #workingclass #family #comprising #earningworker #spouse #twochildren #equivalent #threeadult #consumptionunits

shorturl.at/8Jv7e

1

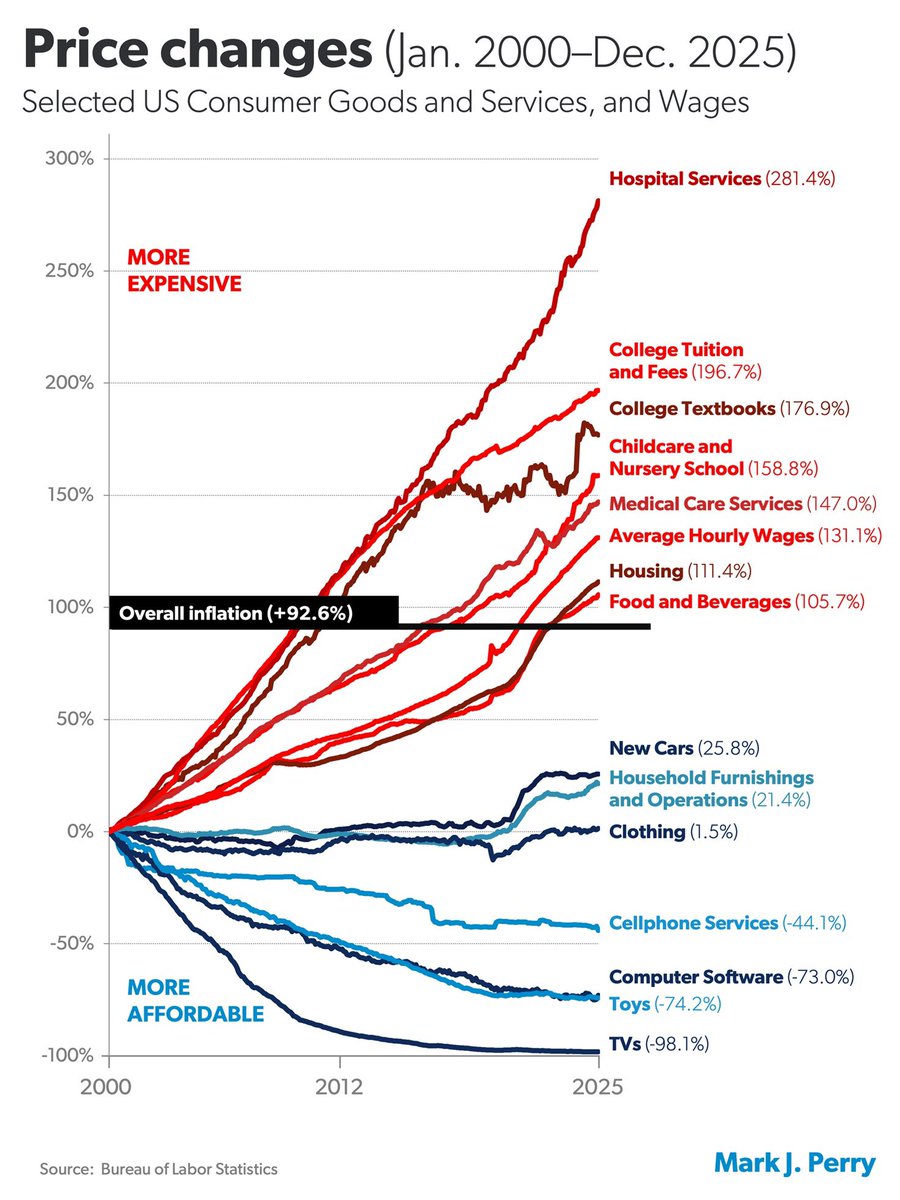

The middle class is getting crushed — and this chart says it all.

Hospital services are up 281.4%. College tuition and fees are up 196.7%. Childcare, medical care, housing, and food are all way ahead of wages. Average hourly wages rose 131.1%, but basic living costs have climbed even faster.

That is the real cost-of-living crisis.

It’s not just “inflation.” It’s a slow financial squeeze on working people, families, and anyone trying to build a life, save money, or get ahead. When essentials rise faster than paychecks, the middle class doesn’t just feel pressure — it gets drained.

Meanwhile, a few categories got cheaper, but that doesn’t matter much when the things people must pay for keep taking more of their income.

This is why so many people feel like they’re working harder just to stand still.

The question is simple: How are families supposed to keep up when the necessities keep outpacing wages year after year?

#CostOfLiving #Inflation #MiddleClass #Wages #HousingCrisis #HealthcareCosts #CollegeTuition #ChildcareCosts #FoodPrices #EconomicPressure #PersonalFinance #WealthGap #Money #Economy #FinancialFreedom #WorkingClass #LinkedInPost #Business #Entrepreneur #FamilyBudget #AmericanEconomy #Recession #InterestRates #SaveTheMiddleClass #IncomeInequality #LivingCosts #AffordableLiving #Debt #RealEstate #HealthCare

1

2

53