Seems interesting to consider from comms perspective. Imagine alternative scenario: Since the acquisition is very small compared to current project market cap, it could've been framed as "acquring adjacent property allows us to maintain focus". There can be too much optionality.

1

Markets are drifting because investors are waiting on the new operating language from the Fed.

Kevin Warsh’s first Federal Reserve meeting as chair is not just another rate event.

It is a credibility test.

The market already understands the headline setup:

Inflation is still above target.

Rates remain restrictive.

Geopolitical risk is still alive.

Growth assets remain valuation-sensitive.

Bond investors are moving more neutral.

The real question is not simply whether the Federal Open Market Committee cuts, holds, or hikes.

The real question is how Warsh frames the path forward.

If the Fed sounds too loose, inflation risk gets repriced.

If the Fed sounds too tight, growth risk gets repriced.

If the Fed sounds unclear, volatility gets repriced.

That is why this meeting matters.

My read:

This is not the market panicking.

This is the market waiting for policy clarity before committing more capital to crowded trades.

For portfolios, the playbook stays disciplined:

Preserve liquidity.

Avoid overleveraged names.

Do not chase pre-Fed price action.

Watch Treasury yields.

Watch small caps.

Watch semiconductors.

Watch crypto beta.

Watch the dollar.

The important signal is not one trading day.

It is whether the Fed gives markets confidence that inflation, rates, liquidity, and growth are being managed with discipline.

Until then, cash is not dead money.

Cash is optionality.

Read to allocate capital. Not to consume noise.

Source:

finance.yahoo.com/markets/li…

EDUCATIONAL MARKET COMMENTARY ONLY!❗ NOT A RECOMMENDATION TO BUY, SELL, OR HOLD!❗

#StockMarket #Investing #FederalReserve #MarketStructure #RiskManagement

3

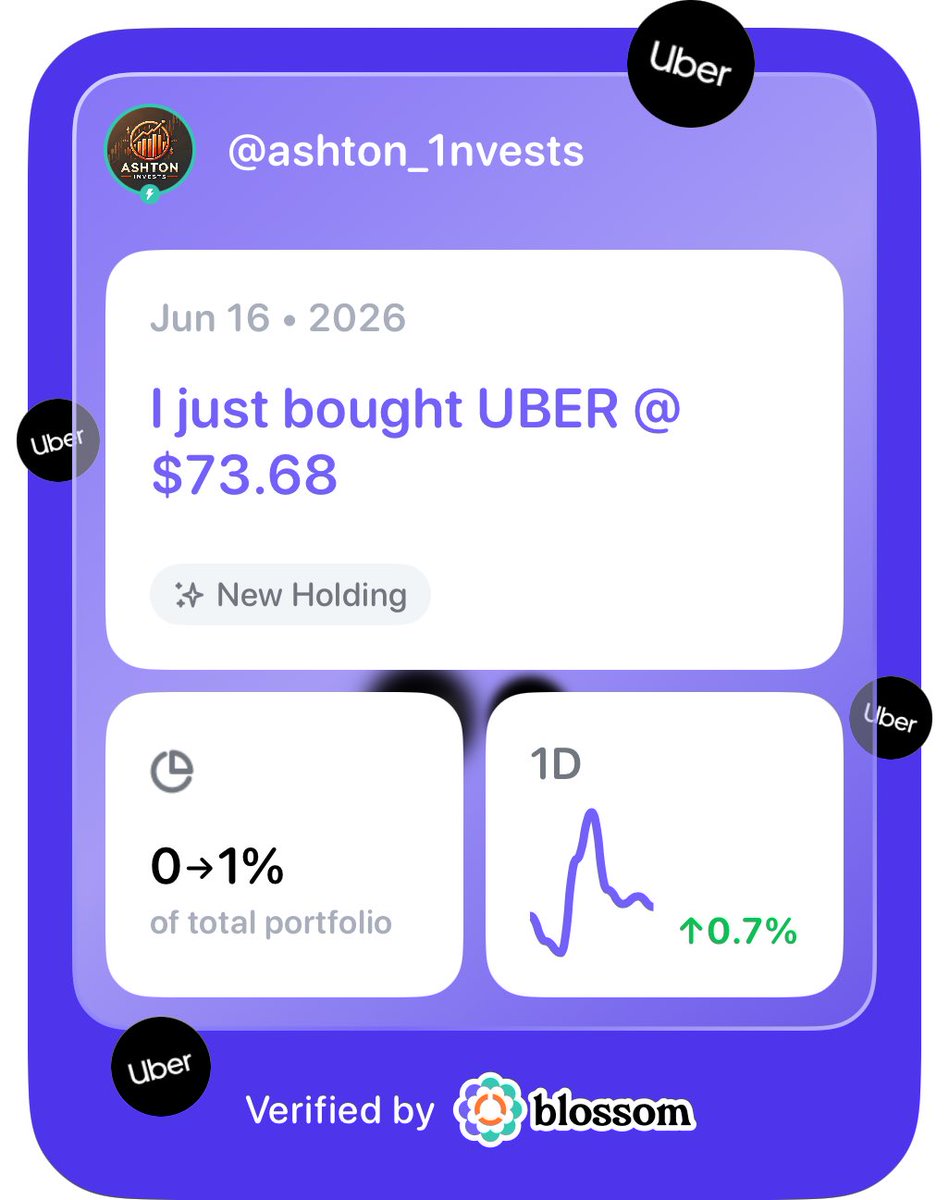

I finally started my $UBER position today.

I was done waiting.

I’ve been watching this one for a while, and I’m starting to think the market still does not fully understand what Uber is becoming.

Mobility. Delivery. Ads. Subscriptions. Autonomous optionality.

This is not just a ride-sharing company anymore.

Position is still small, but I’m officially in.

4

5

122

Exactly $SPCX at $2.5T with ~$18.7B 2025 revenue (and a $4.9B net loss) vs $MSFT’s ~$280-300B rev and $120B profits. No fundamental basis for overtaking yet… just massive future optionality premium on Starlink/Starship/AI bets priced at 130x sales.

Microsoft is the proven compounder printing cash today. SpaceX is the moonshot lottery ticket. One’s a business, the other’s a vision with rockets attached. I’ll ride the data, not the hopium 😂

34

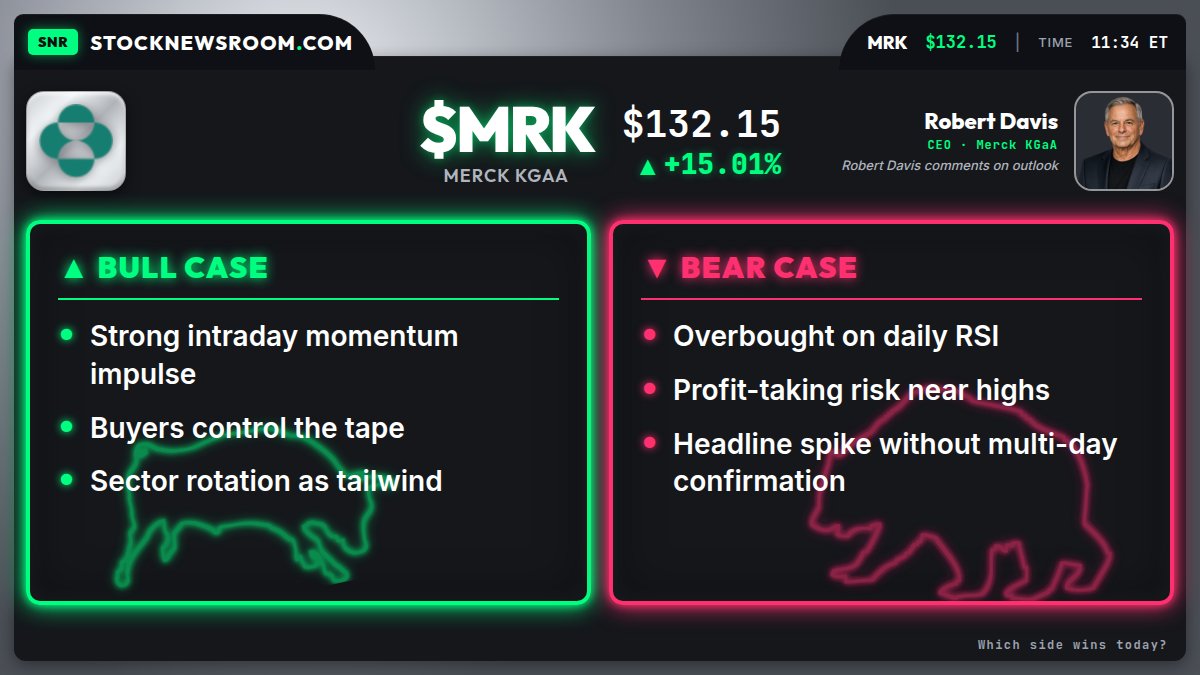

$MRK Merck KGaA reads like a 2013-style rerate: sleepy dividend name, then one AI deal and suddenly everyone discovers the pipeline. The market loves optionality until the first data check. Then it gets honest.

stocknewsroom.com/merck-prot… 2/2

The "fundamentally flawed" critique often reveals more about the critic's mental model than the company itself.

Many highly educated investors are trained in environments that reward clean, linear thinking:

Better inputs → better outputs

Better fundamentals → better company

Cleaner model → cleaner conclusion

Messy company → reject

This works in exams, consulting decks, academic papers, and textbook finance.

But fortunately or unfortunately markets do not work that way.

Market returns are not normally distributed. They are closer to power law systems.

A small handful of outcomes drive the majority of long term returns. The difference between a decent portfolio and a legendary one often comes down to whether you owned one or two extreme winners.

This is why the old line "If you’re so smart, why aren't you rich?" stings.

Intelligence, effort, and analytical talent may be roughly normally distributed.

Wealth and investment success are not.

They are skewed by timing, positioning, leverage, cumulative advantage, and sequences of events that compound in ways no clean model can fully capture.

That is why "fundamentally flawed" is often an incomplete stopping point.

The real question is not:

"Is the company flawed?"

Of course many high conviction ideas are flawed.

Small revenue base.

Execution risk.

Dilution risk.

Unproven manufacturing.

Pipeline uncertainty.

Customer-conversion risk.

The better question is:

Are the flaws fatal, or are they bridgeable?

Most flawed companies remain flawed. Some are landmines.

But a few flawed companies become massive outliers precisely because the market overweights today's mess and underweights the possibility of a transformed future state.

This is not an argument for abandoning rigor or blindly buying story stocks.

It is an argument for the right kind of rigor in a power law environment.

Instead of demanding perfection, the real work is underwriting asymmetric optionality:

1. Can the company cross from current mess to larger scale?

2. Are the bottlenecks real, and are they solvable?

3. Are the people capable of crossing the chasm?

4. Is the market mispricing the probability of a positive tail outcome?

That is the difference between gambling on hope and deliberately positioning in messy branches with outlier potential.

Perfection is rare.

Obvious perfection is usually expensive.

The edge is not in saying "this is flawed."

The edge is in knowing which flaws are fatal, which flaws are bridgeable, and which bridgeable flaws the market has mistaken for fatal ones.

Jun 13

$SIVE is the GameStop of 2026, and Serenity is its Wallstreetbets.

$SIVE is not a strong company. Its technology lacks meaningful differentiation. Execution has been consistently weak. Manufacturing capabilities remain mediocre at best.

The much-touted $700M pipeline is largely meaningless. Garbage in, garbage out. Having reviewed numerous startups and established players over the years, I have seen pipelines that generate little to no revenue time and again. It is straightforward to inflate these figures: one introductory meeting with a junior contact, an entry in Salesforce, and an inflated LTV projection, sufficient to impress investors who chase headline numbers.

More importantly, when companies like $SIVE command such rapid valuation growth, it confirms we are in a substantial bubble. If you wish to gamble, that is your choice. This is a free market. One can always visit a casino and play roulette. Your capital, your risk.

$SOXX sits at all-time highs. With multiple semiconductor cycles behind me, I have observed this pattern repeatedly. Debates about “this time is different” can continue indefinitely. My advice remains straightforward: exercise caution. Avoid investing in weak companies. There are no hidden gems. $POET, $SIVE, $LWLG, $AEVA, and similar names are fundamentally flawed.

12

$GRR.AX

( GRANGE RESOURCES LIMITED) is a rare ugly stock opportunity that could reward patient and long-term driven investors.

Grange Resources Limited (ASX: GRR) is Australia’s oldest continuous magnetite iron ore producer, operating the Savage River integrated mine and pellet plant in Tasmania for over 55 years. At a price of A$0.16 per share, the company trades at a deep discount to its net-tangible asset value of A$0.93 per share. Its balance sheet is loaded with A$284 million in cash and liquid investments against a market capitalization of only A$185–231 million. The implied deeply negative enterprise value of approximately A$95 million looks interesting.

The market is essentially paying you to own the underlying operating business, the Port Latta pellet plant, the world-class Southdown Magnetite Project optionality, and the rights to over 1.2 billion tonnes of mineral resources.

#Australia #ironore #tasmania #contrarian #netnet

open.substack.com/pub/melifi……

12

Haha exactly

Gotta follow Lindy ancestral wisdom re:cultural and social capital to maximize optionality

So that you may eventually get the equivalent of “F you” capital & set your own trends

like Kings and their dress whose courts copy, eventually becoming the people’s norm

20m

A 15 handle with OPEX Friday and MU next week means convexity is cheap right as the catalyst path gets busy. That's the setup to own optionality, not sell it.

1

11

Technically not yet. We get the confirmation in July/August, but pictures coming out of Marion indicate that it is likely the case. I also use other major data points to infer that the scale up likely works - like the major deals signed with Mitsubishi Materials and POSCO. Both of which came with major investments, JV optionality, signed offtake, and both under the approval of the US government.

1

9

the vexing problem of fertility rates: it's all about time and optionality, what I call neverboredom. a quick thread

1

15

The stock trades at 0.7x book, arguably not yet reflecting the optionality of the North of Scotland land bank and infrastructure housing contracts. The key question is whether the new strategy takes longer to generate material revs than the market expects.

1

62

35m

Today, the obvious trade wasn't chasing weakness but it was shorting the strength at the right time.

The setups were there for the taking, but honestly, if you missed them then preserving your capital matters way more than chasing a quick win a risky entry. Mediocre positions are often the first ones worth trimming or rebalancing when caution is warranted. And the market often closes them for you if you don't but only if you allow it to manage risk for you!

You can't take advantage of an edge if you blow up your account chasing everything late. Keep your chips safe for another day and especially rainy days. And if you have the resources, invest in intelligence. Be early to opportunities and retain the freedom to act or.. not act

That's optionality. That's what money is for..

11

122

If thats true its insane

Pure optionality for $META , same ad infrastructure,

If even 10% of those users monetise at X rates, it's a potentially meaningful revenue line

2

1

77

I think they have a lot more optionality long term than Netflix

They’re expecting at least 20% operating margins in the next 3-4 years as they continue to scale, flex pricing, and their advertisement revamp is complete. Ad revenue growth is sitting around 3% right now and back end of 2026 they’re expecting to reaccelerate and get to 10% long term.

They’ve also had significant FX headwinds recently (8% revenue YoY but 14% constant currency)

1

1

23

6/ Kicker: the market still prices IONQ mostly on the compute fruit. Which means the other fruits are largely unpriced optionality. The strongest bull case isn't "they control the substrate" — it's "you're getting the adjacencies close to free while everyone argues about qubit counts."

1

89

One of the most underrated advantages of scale is optionality.

The strongest companies don't just have more capital they have more ways to deploy it strategically.

280

5/ The trade-off is honest: you give up the undiluted torque a pure-play has on the compute jackpot, in exchange for diversified, illegible optionality. Concentrated legible high-torque vs diversified hedged hard-to-value.

1

10

Space Exploration Technologies Corp. is trading 8.6% up at $209.04 following its planned $60 billion all-stock acquisition of AI startup Anysphere (Cursor).

• The deal positions the company deeper into AI-native developer tools and software, with traders pricing in significant long-term growth optionality.

• The move extends a sharp post-IPO rally for the stock, which has climbed from $160.95 on June 12.

• Investors are reacting positively to the anticipated AI synergies and the strategic deal structure.

$SPCX

9

Adam Block retweeted

Jun 12

$META

near monopoly at 17 PE

40% operating margins

20% revenue growth

w/ AI optionality

and this incentive structure

👇

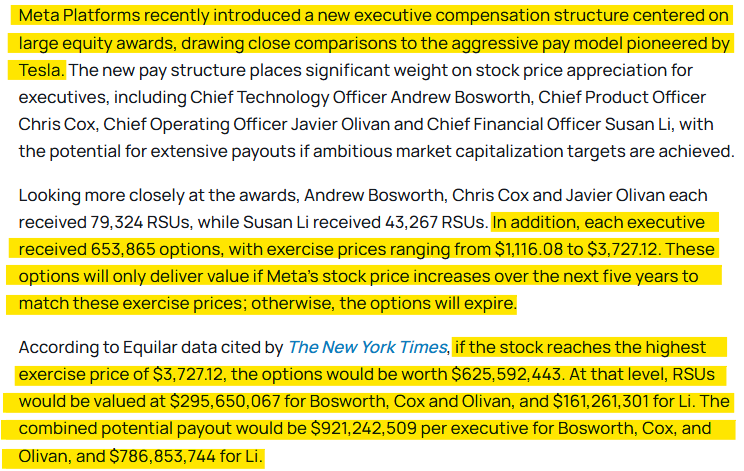

Jun 12

$META friendly reminder than the recent executive compensation structure changes are only reached if the stock price hits between $1,116 to $3,727 over the next 5 years

3

1

21

5,998