20h

MoTA's configuration options are deep. Maybe too deep for beginners. But for someone who knows what they want, it's flexible.

#MoTA #TradingAgent #PortfolioOptimization #RiskManagement

12

101

40

19,798

Sometimes MoTA's agents disagree and that's actually when it's most useful. Forces you to weigh both arguments instead of following one signal.

#MoTA #TradingAgent #PortfolioOptimization #RiskManagement

67

30

10,151

Jun 13

MoTA update: week two. False signals are still a thing, same as any tool. But being able to trace back and see why the agent was wrong helps me learn.

#MoTA #TradingAgent #PortfolioOptimization #RiskManagement

44

8

29

10,656

📢 Most Viewed in #Forecasting

📖 Constructing Cybersecurity Stocks Portfolio Using AI

✍️ By Avishay Aiche, Zvi Winer and Gil Cohen

🔗 brnw.ch/21x3gWt

#AI #MachineLearning #Cybersecurity #Finance #PortfolioOptimization #QuantitativeFinance #StockMarket

12

Jun 9

🎓 PhD Opportunity in Mathematics 🇸🇪 | Örebro University

📌 Position: Doctoral Student in Mathematics

🏫 University: Örebro University

📍 Location: Örebro, Sweden 🇸🇪

🏢 Department: Mathematics and Statistics

👨🏫 Supervisor: Prof. Mårten Gulliksson

💰 Salary: SEK 32,300/month

📅 Deadline: August 17, 2026

⏳ Duration: 4 years ( 1 year with teaching duties)

🔬 About the Project

This PhD focuses on portfolio optimization and financial mathematics, inspired by classical models such as Markowitz (1952) and Modern Portfolio Theory.

The research tackles ill-posed problems in portfolio optimization, where small changes in data can lead to unstable investment strategies—especially when assets are highly correlated.

You will work on developing stable, efficient mathematical algorithms to improve robustness in financial decision-making models.

👥 Supervision Team

• Prof. Mårten Gulliksson (Principal Supervisor)

• Docent Magnus Ögren

• Docent Stepan Mazur

🎓 Programme Structure

• 240 ECTS (PhD degree)

• Combination of coursework independent research

• ~20% teaching responsibilities

• Total duration: up to 5 years

👤 Ideal Candidate

• Master’s degree in Mathematics or related field

• Strong background in mathematical modeling and analysis

• Interest in optimization, finance, or applied mathematics

• Background in economics is a plus

• English proficiency (Swedish is optional but beneficial)

🌟 Why Apply?

• Work on mathematically challenging and real-world relevant problems

• Gain expertise in financial mathematics and optimization

• Supportive academic environment with structured PhD training

• Opportunity to teach and develop academic skills

• Competitive salary and strong work-life balance in Sweden

🌍 Location Highlight – Örebro

A vibrant and student-friendly city in Sweden, Örebro offers a high quality of life, rich culture, and a welcoming international environment.

🔗 More Info & Apply:

phdscanner.com/opportunities…

#PhD #Mathematics #Optimization #FinancialMathematics #Sweden #ResearchOpportunity #AppliedMath #PortfolioOptimization #AcademicJobs

271

May 25

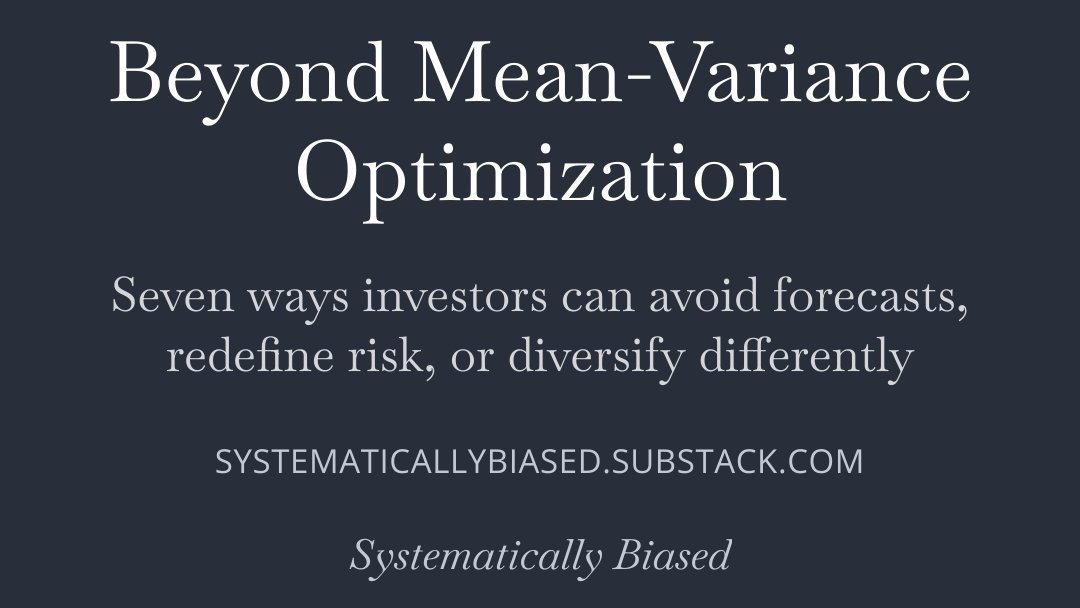

I recently discussed how mean-variance optimization (MVO) can go wrong. In the most recent post, I discuss some alternatives to MVO.

Post here 👇

open.substack.com/pub/system…

#QuantFinance #PortfolioOptimization #AssetAllocation #SystematicInvesting #Investing

2

2

15

797

May 3

🌅 GARCH Quant Academic Series|D. E. Shaw

📖 【Day 4/7】Portfolio Construction with Dynamic Risk Constraints

👤 Authors: D. E. Shaw Research (2003), Institutional Investment Research

📌 Summary

This paper explores portfolio construction under dynamic risk constraints. It proposes an adaptive portfolio optimization framework that dynamically adjusts risk budgets in response to real-time changes in market volatility and correlation structures. The study examines how to maximize returns while keeping overall risk under control, with strong emphasis on advanced risk measures such as Conditional Value-at-Risk (CVaR).

🏛️ Key Academic Contributions

• Proposed a CVaR-based portfolio optimization model that captures tail risk far more effectively than traditional variance approaches

• Designed dynamic risk budgeting mechanisms that adjust asset class exposures in real time according to prevailing market conditions

• Introduced a hybrid risk estimation approach combining multi-factor risk models with statistical factor models

📚 Why It’s Essential Reading

An advanced must-read for portfolio risk management.

The paper skillfully integrates academic risk theory with D.E. Shaw’s practical experience, offering profound insights into dynamic risk control in portfolio construction.

#DEShaw #PortfolioOptimization #CVaR #RiskManagement #DynamicRisk #QuantResearch #GARCHQuant

5

86

Apr 30

Portfolio Optimization: What Could Go Wrong?

Latest post here👇

systematicallybiased.substac…

#QuantFinance

#PortfolioOptimization

#AssetAllocation

#SystematicInvesting

#Investing

8

17,234

Thrilled to officially confirm the exciting first-stage alignment of our Horney Bull Market setup! 🚀📈 We are incredibly proud to unveil our meticulously crafted 5-stock weekly rebalancing portfolio strategy, a true game-changer for strategic wealth optimization. 🌟 Starting tomorrow, we can't wait to share a curated list of 5 high-potential stocks to elevate your watchlist! Whether you're leveraging this for your personal trading system or integrating it into a dynamic rebalancing workflow, this initiative is perfectly aligned with our shared mission of growth and success. Let's build the future of finance, together! 💼✨ #BullMarket #StrategicGrowth #PortfolioOptimization #InvestmentJourney

10

395

Feb 19

Hiring decisions are made faster than most people realise.

That’s why resumes and portfolios need to communicate value quickly, not through long descriptions, but through clear outcomes.

Optimisation helps remove guesswork for decision-makers, so trust can form faster.

If you want your resume and portfolio to reflect your real value in 2026, our Portfolio Optimisation Service is available on the Ariesphere service page.

selar.com/portfolios

#PortfolioStrategy #PortfolioOptimization #ProfessionalPortfolio #WorkShowcase #ProofOfWork

1

2

18

Feb 16

A lot of professionals assume their years of experience should carry weight on their own.

If they’ve done the work, it should be obvious.

But hiring decisions don’t happen that way anymore.

In 2026, people don’t have the time or patience to interpret long explanations. They look for proof. Clear signals. Tangible outcomes.

This week is about understanding why experience alone isn’t enough anymore and how evidence changes how your work is received.

#PortfolioStrategy #PortfolioOptimization #ProfessionalPortfolio #WorkShowcase #ProofOfWork

3

16

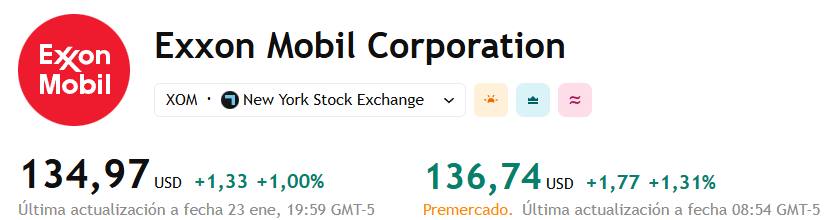

🛢️ Exxon Mobil Corp $XOM, through its XTO Energy unit, is exploring the sale of selected Eagle Ford shale assets in South Texas, opening a data room to gauge buyer interest. The package spans ~168,000 net acres, includes 1,000 wells, and is valued at over $1B, with both operated and royalty-generating non-operated interests.

The move aligns with Exxon’s portfolio optimization strategy as it prioritizes the Permian Basin, Guyana, and LNG, amid lower oil prices and rising concerns over global oversupply. ⚖️💰

#OilAndGas #PortfolioOptimization #EnergyMarkets

1

2

405

SABIC is optimizing its portfolio for long-term sustainable growth by divesting its European petrochemical business its engineering thermoplastics units in the Americas and Europe.

polymart.info/sabic-divests-…

#SABIC #PortfolioOptimization #Petrochemicals #EngineeringThermoplastics

2

54

6 Dec 2025

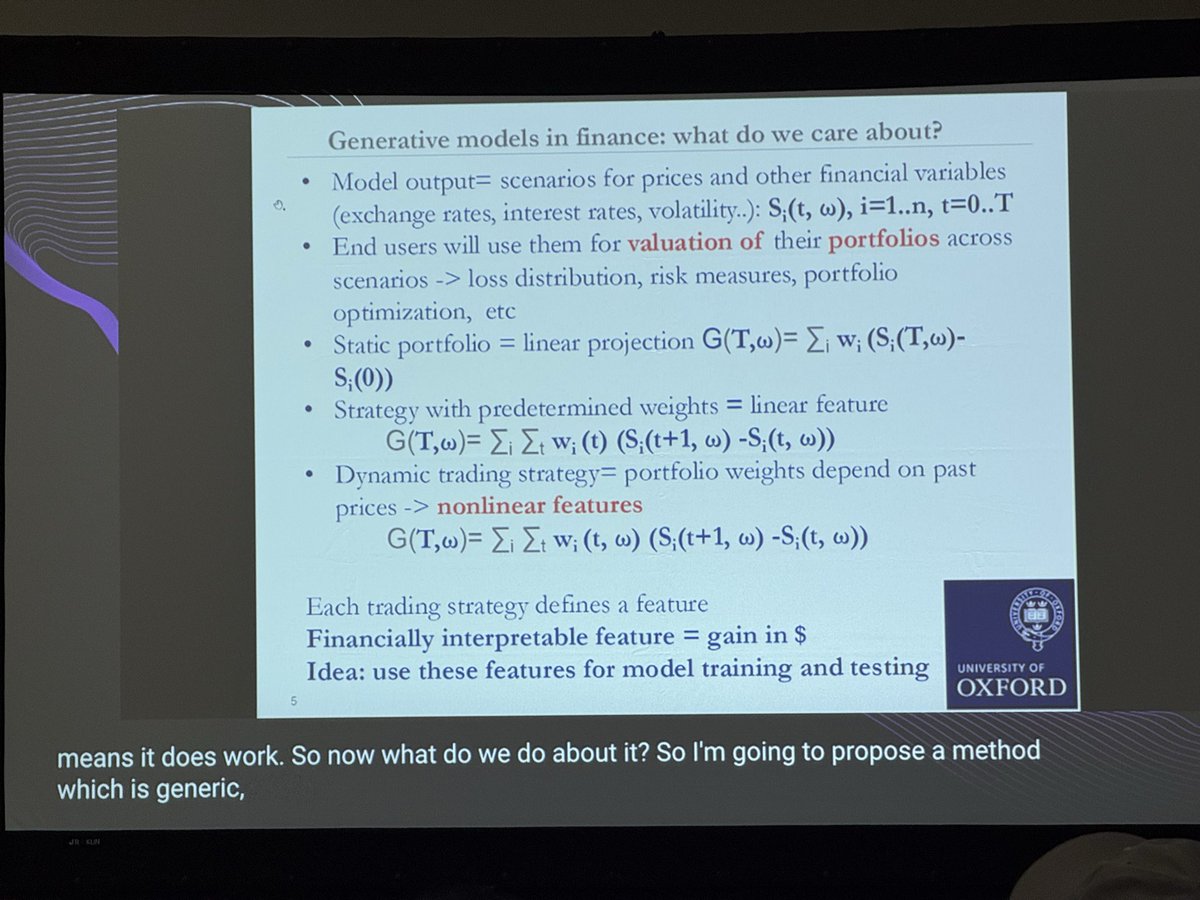

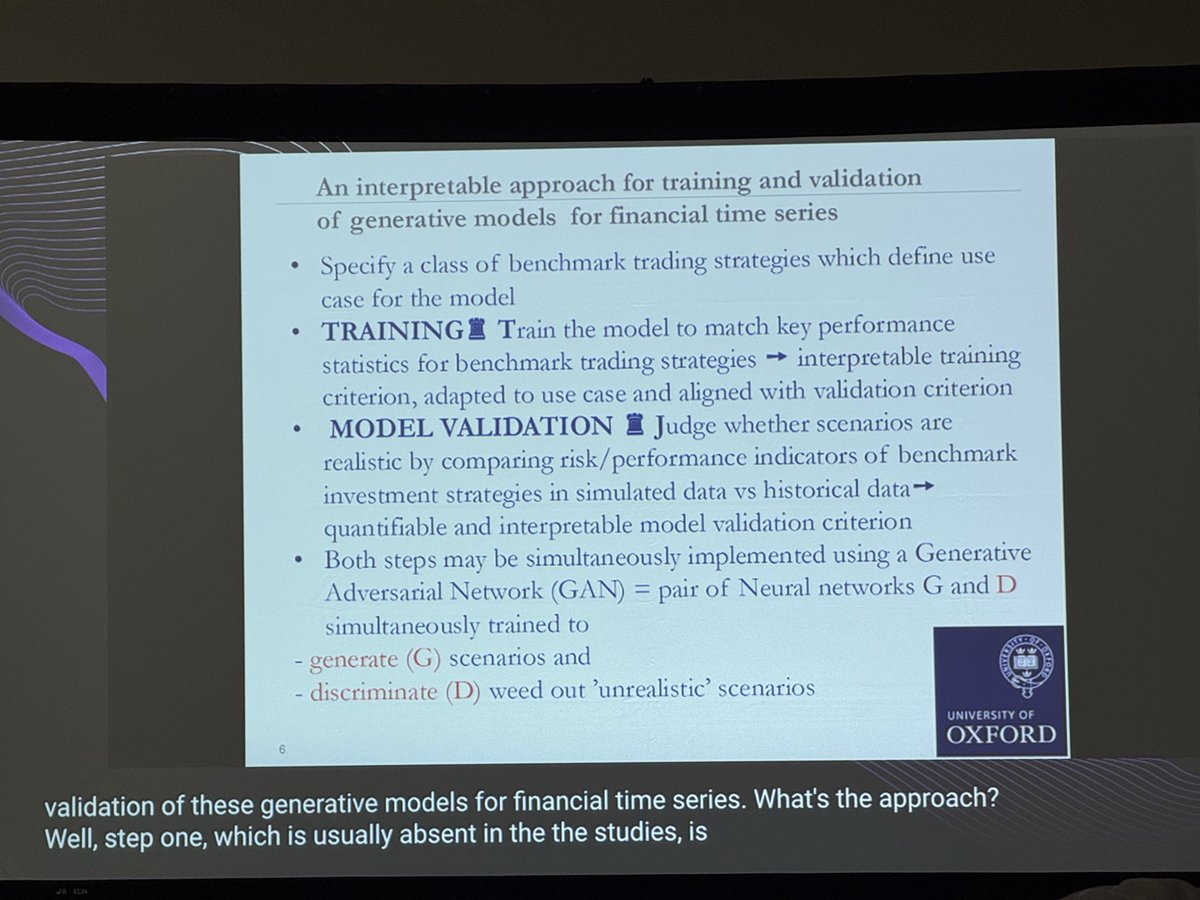

After a very interesting #NeurIPS2025 conference, it’s now time for the workshops. I’m attending the Generative AI in Finance workshop. #NeurIPS #Finance #Trading #PortfolioOptimization #ORMS

3

5

298

2 Dec 2025

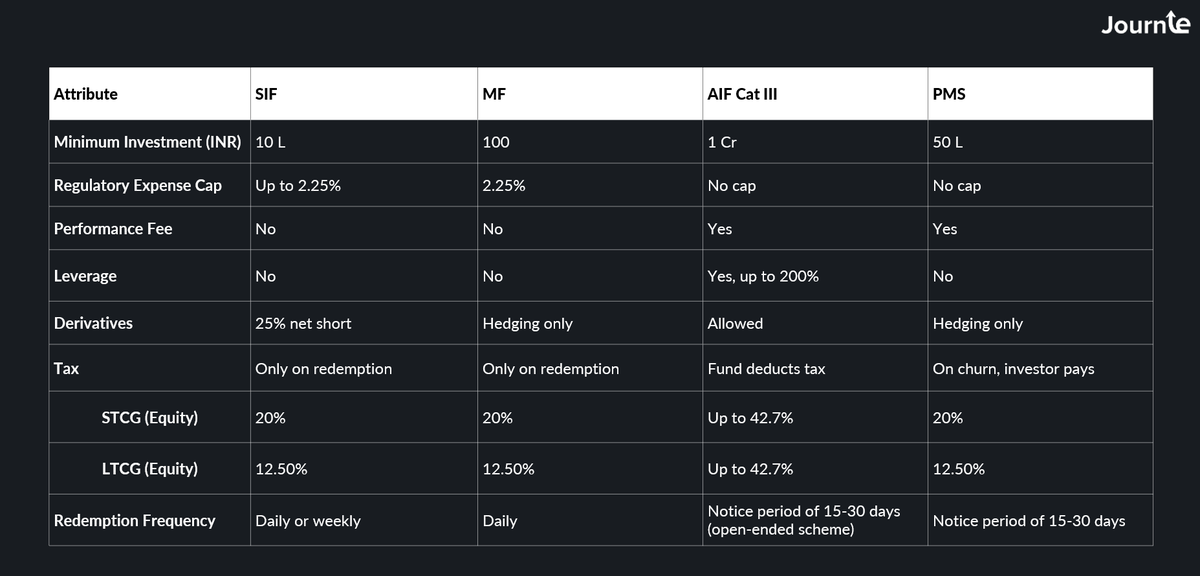

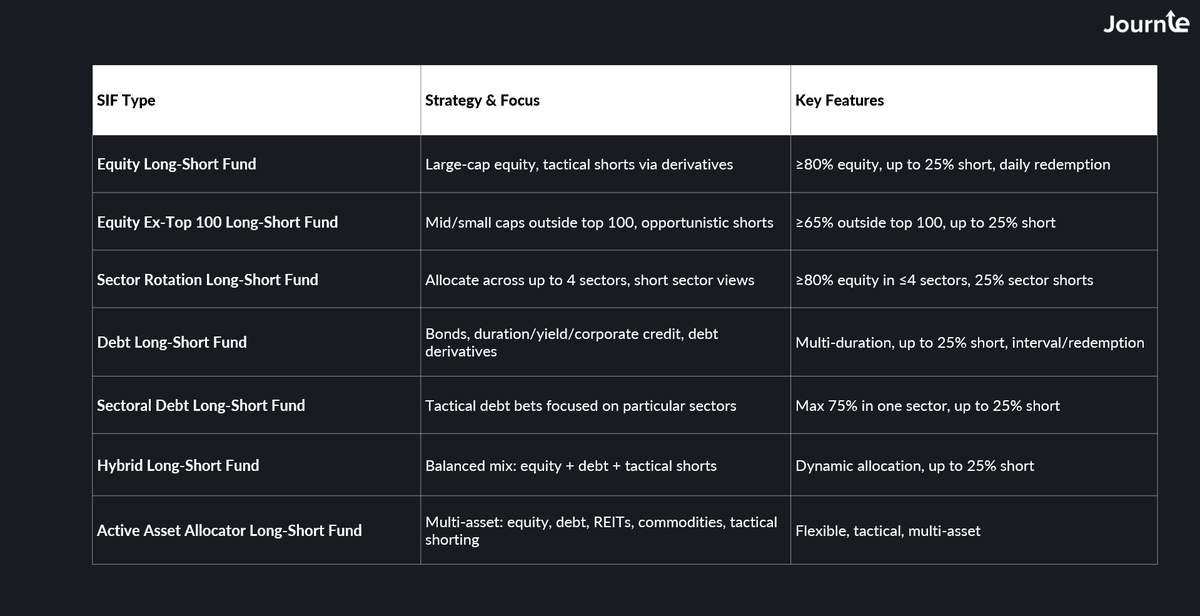

SIFs are the most underrated new category,

flexible regulated. A powerful combo

#MutualFunds #Investing #PortfolioOptimization #FinanceIndia #IndianStockMarket #SIF #PMS #AIF

3

87

1 Dec 2025

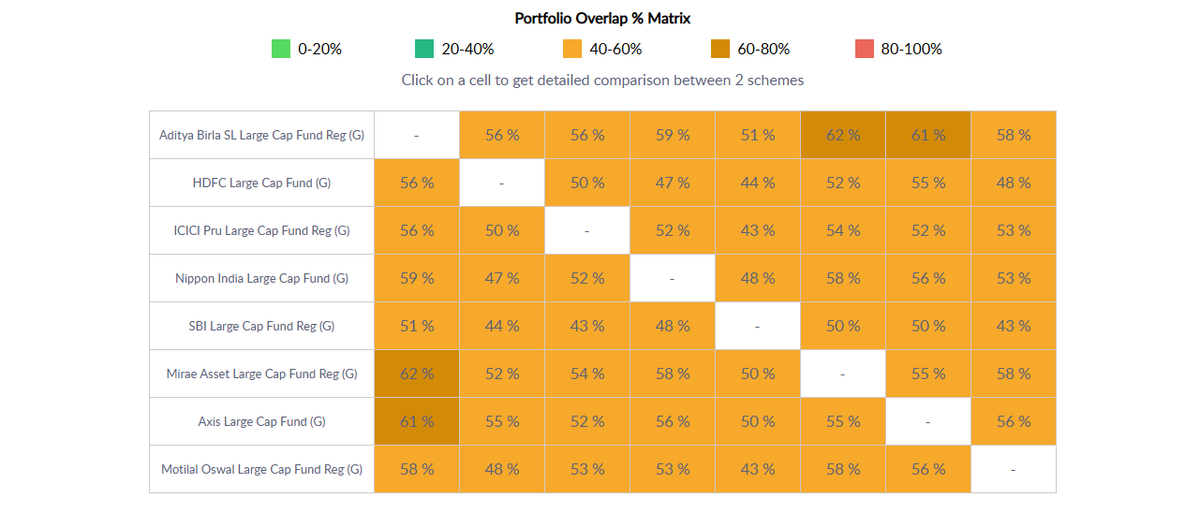

Most investors don’t need 15 mutual funds.

They need 4–6 high-quality ones with low overlap.

Here’s a portfolio-overlap comparison across leading large-cap funds. Owning 3 large-cap funds isn’t diversification—it’s the same portfolio in disguise.

#MutualFunds #Investing #PortfolioOptimization #FinanceIndia #IndianStockMarket #WealthBuilding #FinancialPlanning

3

70

17 Nov 2025

✨ 𝗧𝗵𝗿𝗶𝗹𝗹𝗲𝗱 𝘁𝗼 𝗦𝗵𝗮𝗿𝗲 𝗮 𝗠𝗶𝗹𝗲𝘀𝘁𝗼𝗻𝗲! ✨

We are delighted to announce that our research paper titled “AI-Driven Portfolio Optimization System for Dynamic Asset Allocation” has been officially accepted and approved for publication in the Advances in Consumer Research (ACR) Journal.

🔗 Published article: acr-journal.com/article/ai-d…

This work is a collaborative effort with an esteemed team of co-authors — Dr. Bosky Ashokkumar Suratwala, Dr. Amitabha Maheshwari, Dr. Hardik Brahmbhatt, Dr. K T Vigneswara Rao, and Dr. Naresh Guduru — and we are grateful for the opportunity to contribute to the growing conversation at the intersection of artificial intelligence, wealth management, and dynamic asset allocation.

The review process was rigorous, insightful, and immensely rewarding. With a strong plagiarism check result and all revisions successfully incorporated, this acceptance validates our commitment to producing high-quality, actionable research.

💡 As someone deeply passionate about the evolving role of AI in wealth management, this publication strengthens our resolve to explore how human-AI collaboration can shape the future of investment strategies.

A heartfelt thank you to the Editorial Board at ACR Journal for this recognition and to our co-authors for their expertise and collaboration.

Looking forward to contributing more to research and innovation in this space!

#Research #ArtificialIntelligence #WealthManagement #AcademicPublication #PortfolioOptimization #DynamicAssetAllocation #FinancialInnovation #AIinFinance #ACRJournal

2

52

25 Oct 2025

🚀 What if your investment portfolio could be optimized using quantum computers—for free? 🤯💸

IBM and Vanguard are exploring quantum algorithms to tackle one of finance’s toughest challenges: building the perfect portfolio under real-world constraints. And now, thanks to platforms like IBM Qiskit and Global Data Quantum, even individual investors can experiment with quantum-powered tools—no PhD required! 🧠⚛️

Would you trust a quantum computer to manage your money? 🤔📈

#QuantumComputing #PortfolioOptimization #IBMQuantum #FinTech #InvestSmart #AIinFinance #Qiskit #FreeTools #QuantumFinance #TechForInvestors

1

4

52

26 Sep 2025

Sharpe ratio pitfalls: Ignores fat tails, so pair it with Sortino for downside focus. Optimal portfolios? Mean-variance works until kurtosis bites. Tweak with CVaR constraints for crash-proof alpha. Edge refined. #PortfolioOptimization

1

3

102

9 Sep 2025

📊⚡ Dynamic Portfolio Optimization: Leveraging Analytics for Q4 Capital Markets Strategies 🚀✅

Opening:

Q4 is the most critical quarter in capital markets. Liquidity shifts, regulatory deadlines, and portfolio rebalancing converge into volatility storms. Static allocation is no longer enough. Dynamic, analytics-driven portfolio optimization has become the competitive edge.

Sections:

1️⃣ Advanced Analytics in Q4 – ML-driven return forecasting, factor-based optimization, alternative data integration.

2️⃣ Real-Time Adjustment Strategies – Intraday VaR, tactical rebalancing, liquidity-sensitive adjustments.

3️⃣ Case Studies –

Asset manager outperforming peers by 4% through predictive models.

Hedge fund cutting liquidity mismatches by 35% with treasury-OMS integration.

Pension fund improving Sharpe ratios by 20% with dynamic correlations.

4️⃣ Optimization Checklist – Monitoring, liquidity integration, compliance automation, scenario testing.

5️⃣ Expert Insights – CIOs, quants, and regulators weighing in.

6️⃣ Future Outlook – AI quantum optimization, blockchain-based tokenized portfolios, personalized robo-optimization.

Closing Thought:

Static allocation is a relic. Q4 winners will be those who run living portfolios — predictive, adaptive, and optimized in real time.

📩 Full newsletter: linkedin.com/pulse/dynamic-p…

💬 What’s YOUR Q4 edge — AI, analytics, or execution speed?

#PortfolioOptimization #CapitalMarkets #Analytics #RiskManagement #Q4Strategy #MDMarketInsights #BusinessAnalysis #CapitalMarkets #FinancialServices #TradeFloor #FinanceIndustry #InvestmentAnalysis #DataAnalytics #RiskManagement #TradingStrategies #MarketResearch #FinancialData #InvestmentManagement #AssetManagement #Fintech #RegulatoryCompliance #PortfolioManagement #Derivatives #MarketAnalysis #FinancialTechnology #TradingTools #QuantitativeAnalysis #InvestmentStrategy #BusinessIntelligence #FinancialInnovation #EconomicAnalysis #TradingSystems #DataScience #HedgeFunds #PrivateEquity #RiskAnalysis

1

2

27