Jun 12

Wednesday: how quants vs MFDs talk about risk.

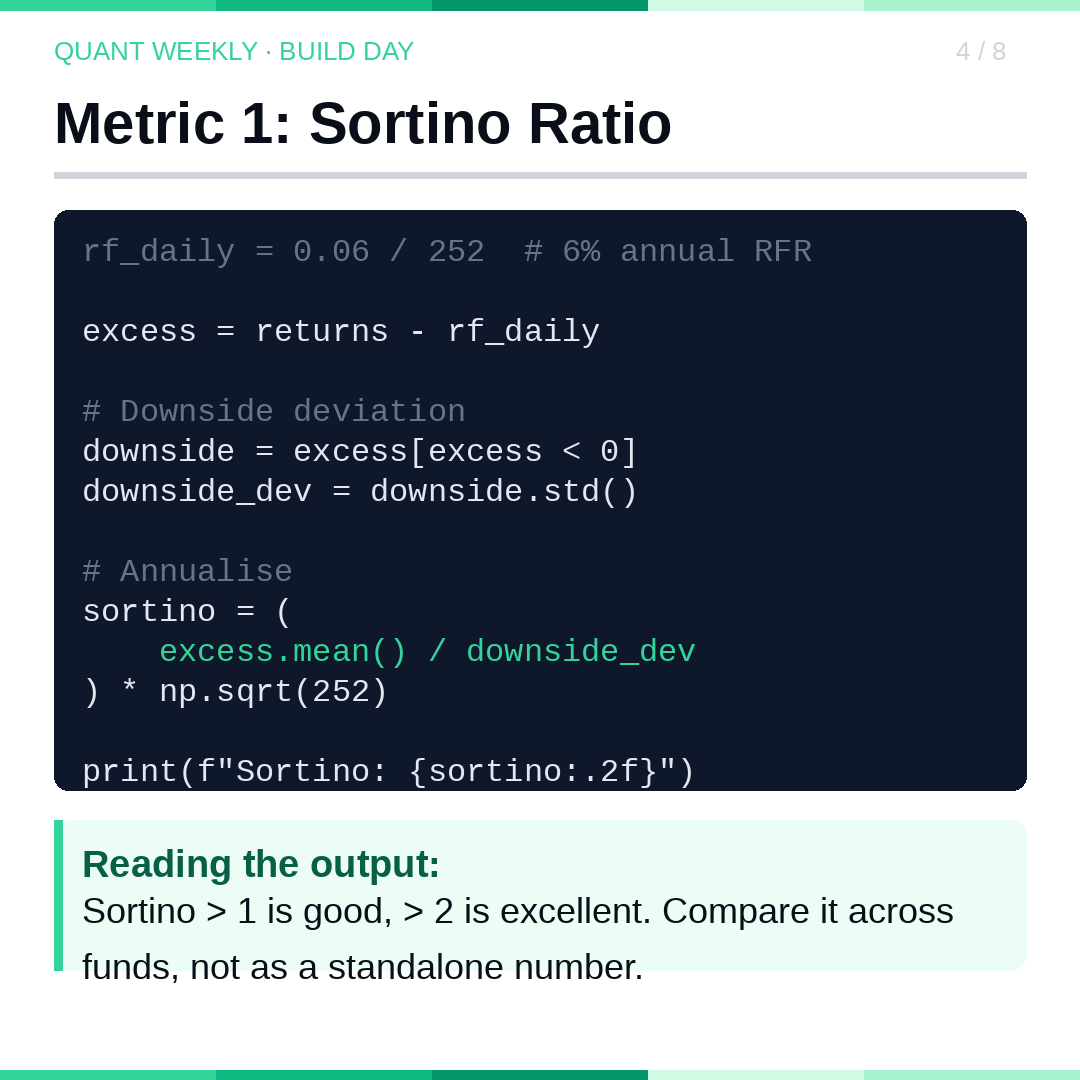

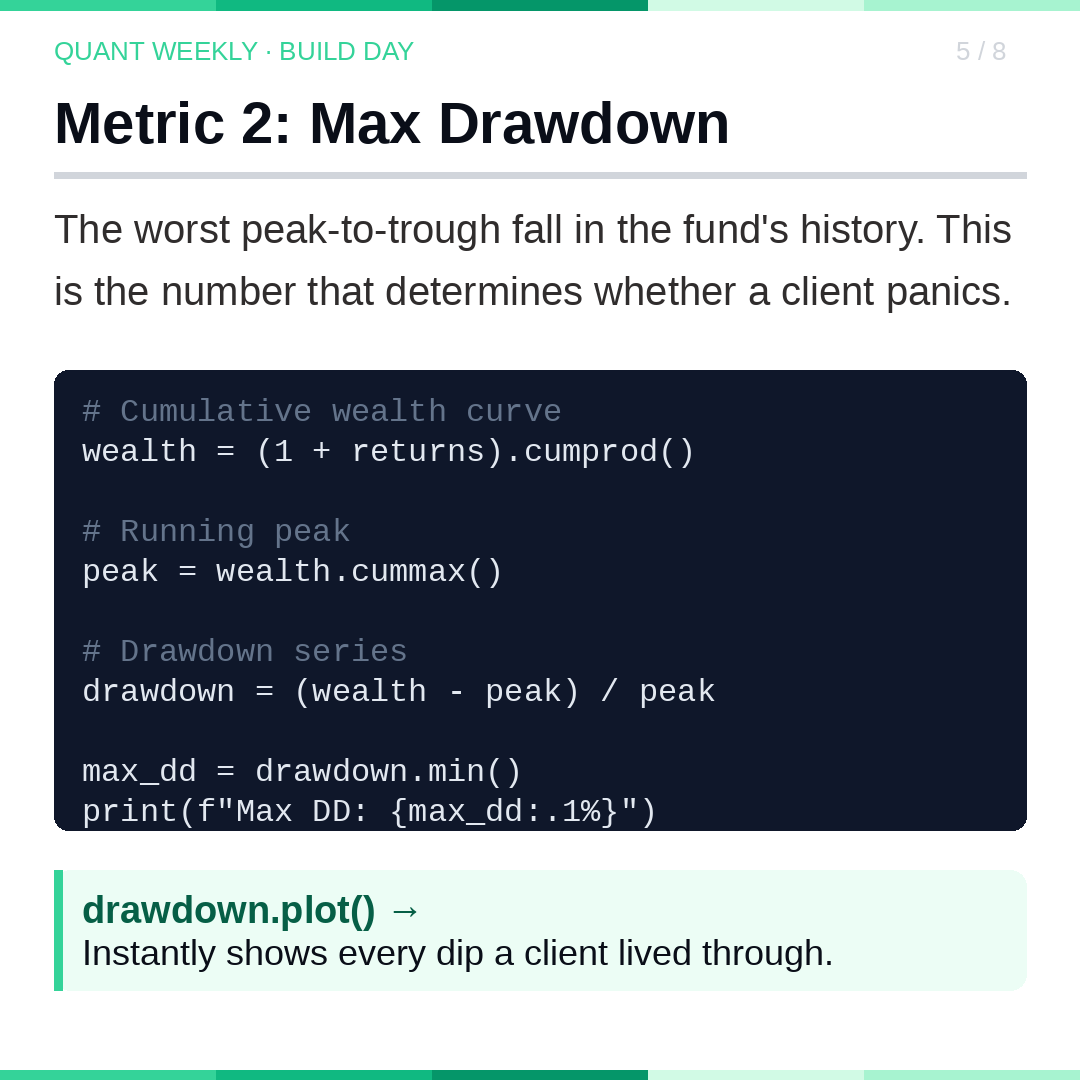

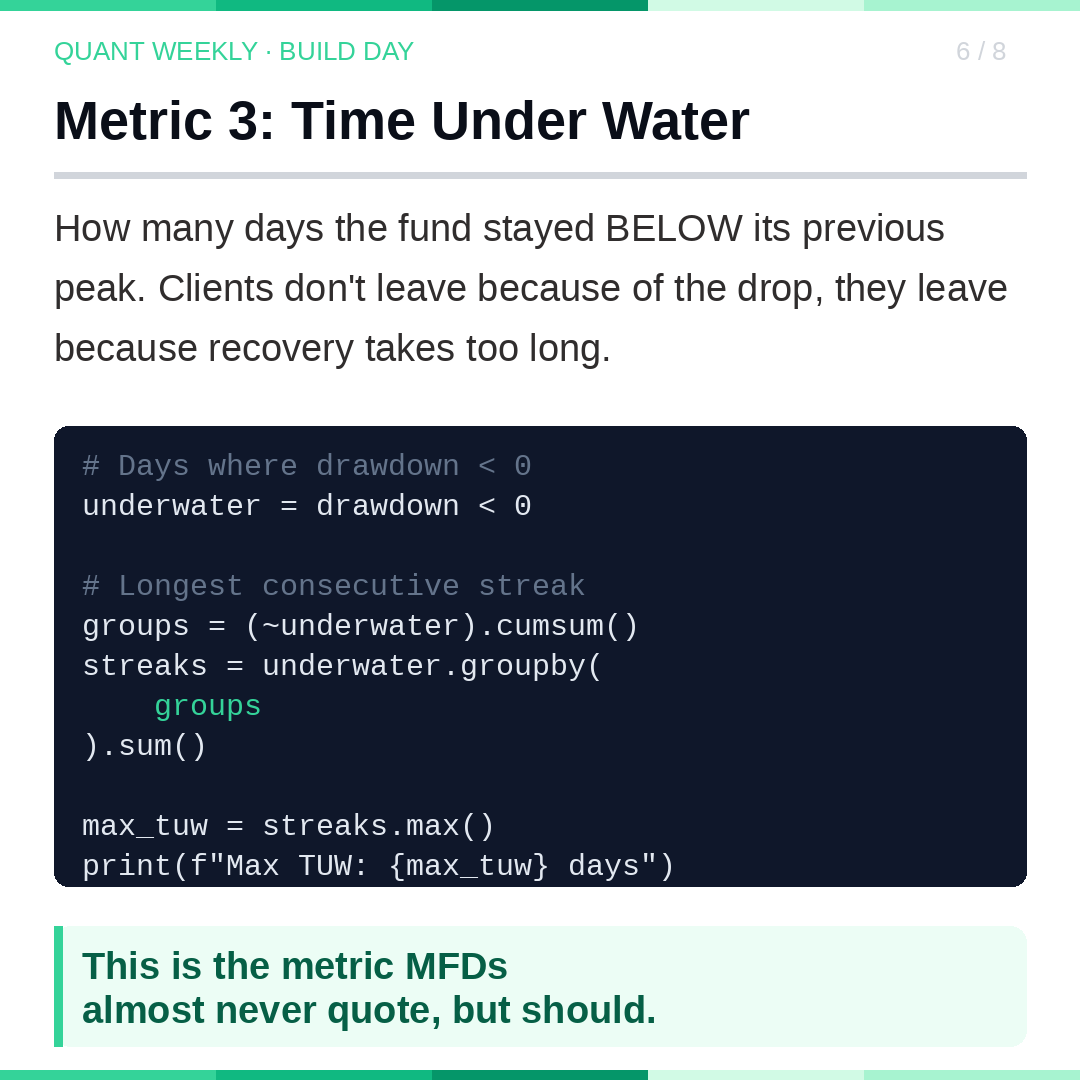

Today: How to actually CALCULATE it.

Sortino, Max Drawdown, Time Under Water, in under 30 lines of Python.

#FinTwit #QuantTwitter #WealthManagement #SystematicTrading $NIFTY #Risk #NASDAQ

1

1

63

Jun 10

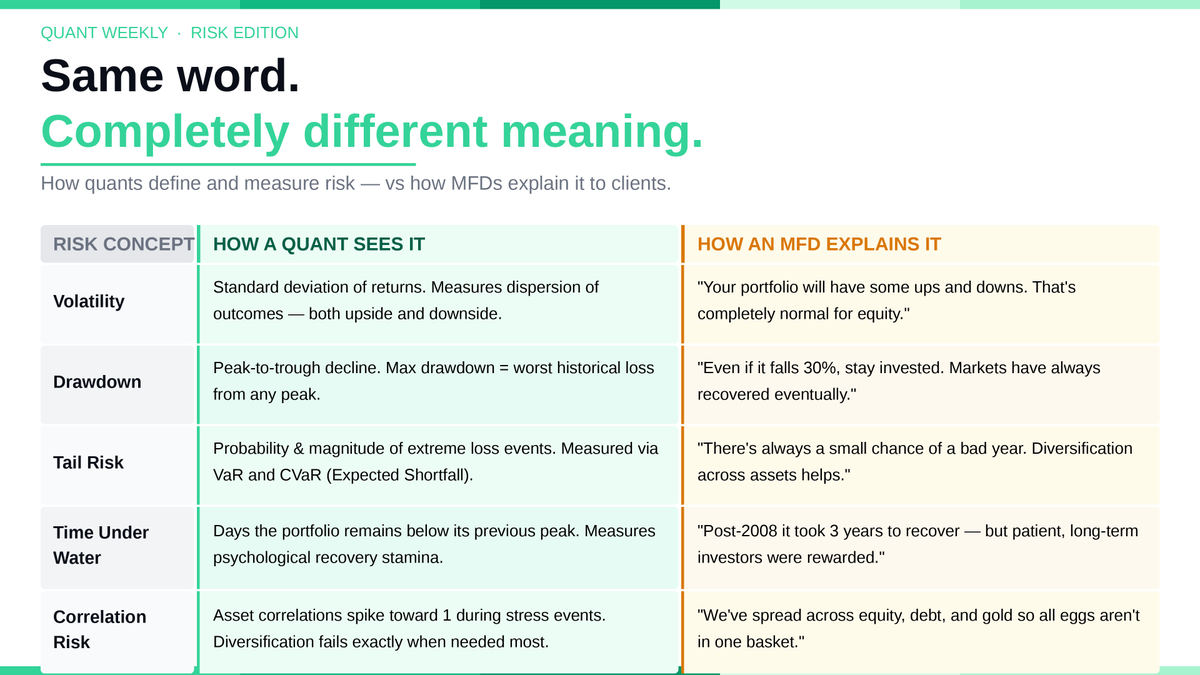

A client asks: "Is this fund risky?"

A quant and an MFD will give completely different answers.

Here's the translation table between them.

#FinTwit #QuantTwitter #WealthManagement

1

1

1

34

Jun 8

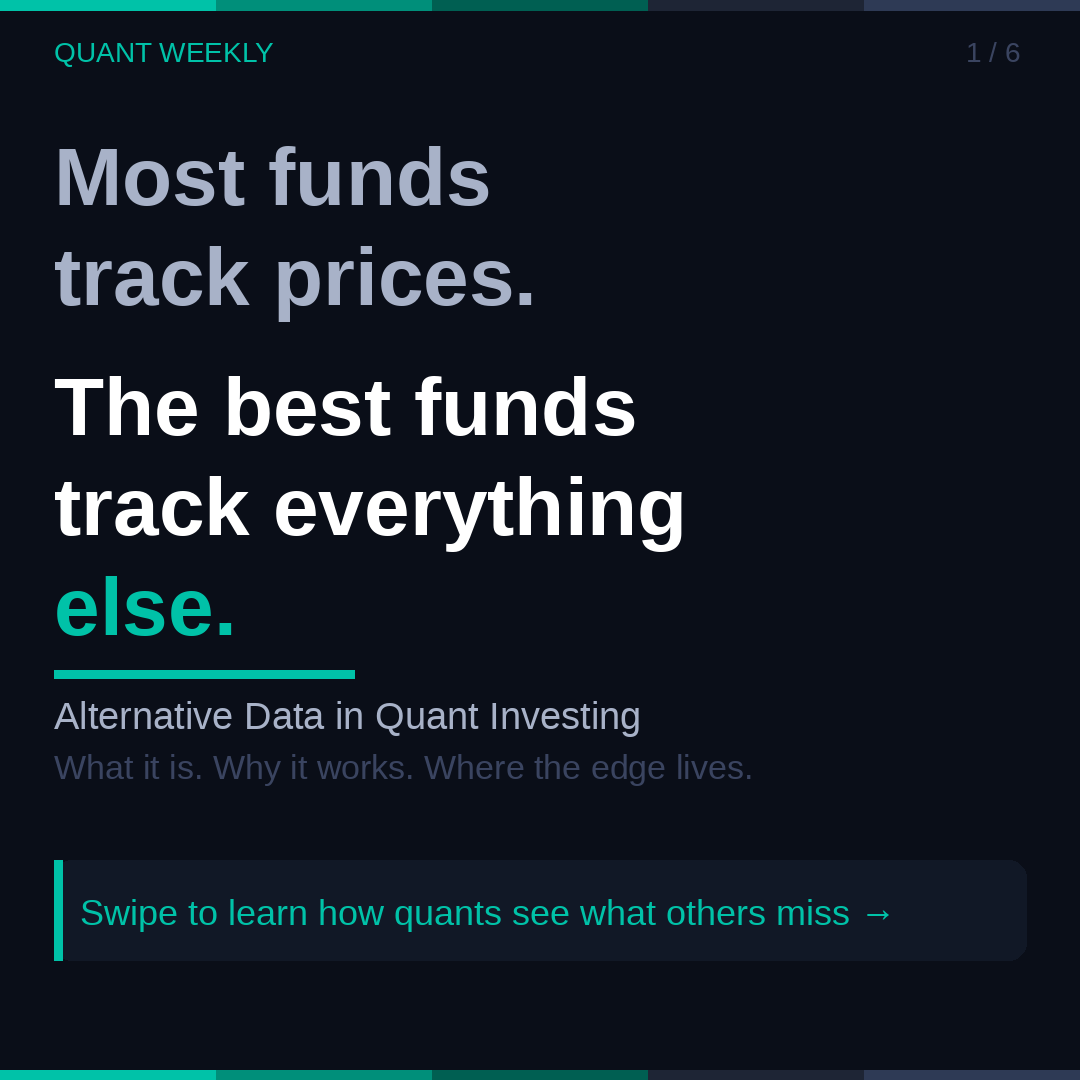

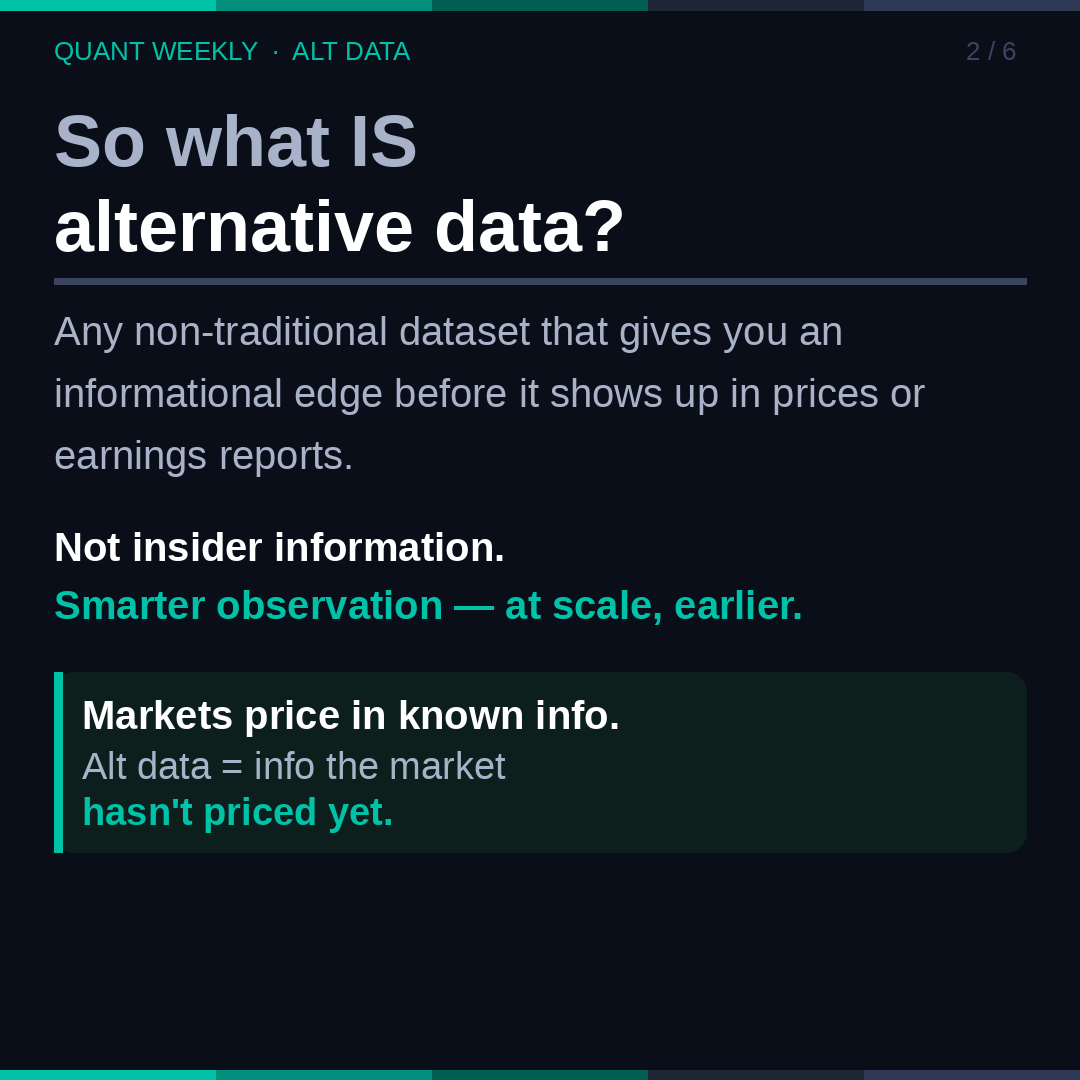

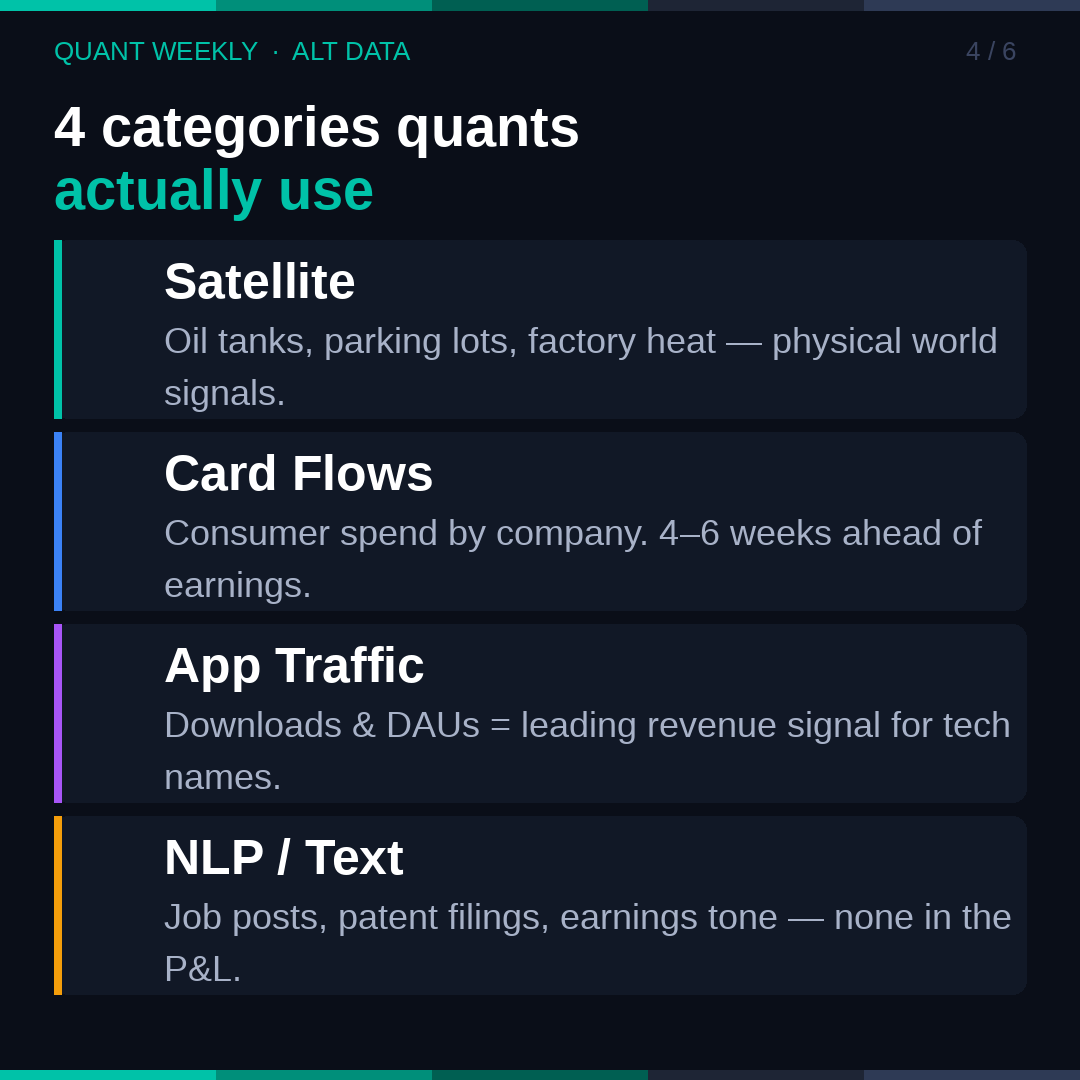

Most quant alpha today isn't coming from balance sheets or price charts.

It's coming from parking lots. Shipping lanes. Credit card receipts.

A thread on Alternative Data, the quiet edge reshaping systematic investing.

#FinTwit #QuantTwitter #SystematicTrading $NIFTY #Risk

1

2

87

Apr 9

I find the quality of content on QuantTwitter disappointing. so in the next few weeks, I will be sharing novel stories about practitioners/legends, resources, anecdotes & many more

to kickstart this initiative I would like to share one of the most valuable websites for quant:

10

10

580

424,037

Apr 7

I encourage all my QuantTwitter followers who shit on academic finance to read Cochrane’s AFA address. Academic finance concerns itself with very different topics than industry. I think most confusion arises bc industry types tend to read easy papers from crappy journals and not the more advanced stuff happening on the frontier, which is concerned with entirely different things than industry. static1.squarespace.com/stat…

6

4

138

14,597

@fordoglunk @elletwocache could yall signal boost please? I’m joining #quantTwitter and want to become an influencer

1

3

126

Mar 9

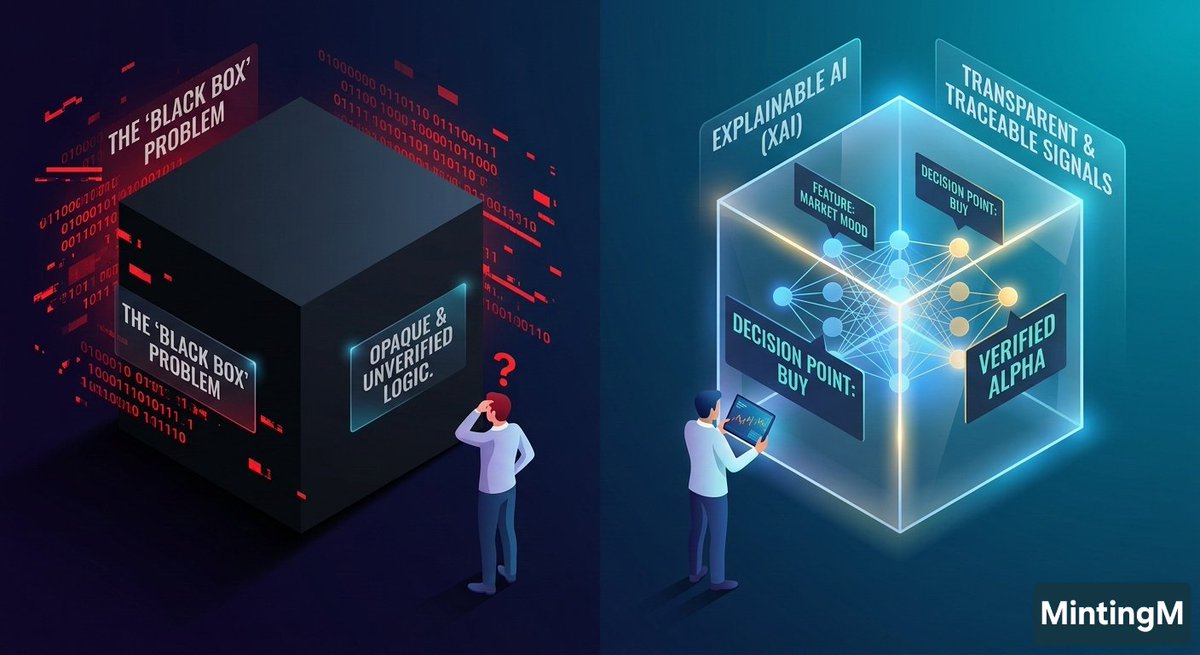

Would you trust an algorithm with your capital if it couldn’t explain why it made a trade?

The biggest risk in modern quant trading is the "Black Box" Problem.

Here is why....

#QuantTwitter #MachineLearning #DataScience #Trading #MintingM

1

1

2

31

30 Nov 2025

🚀 Today, I’m excited to officially launch DataSetIQ — a platform built to transform how analysts, economists, and finance teams work with public macro & financial data.

For years, access to high-quality dataset intelligence has been locked behind expensive ($30k–$50k/yr) terminals and fragmented data portals.

So I built something new.

DataSetIQ is now LIVE — a unified AI-powered intelligence layer for:

Searching millions of economic & financial datasets

Instantly generating structured AI briefs

Identifying trends, cycles, risks, and anomalies

Tracking dataset updates in real time

Comparing global indicators in seconds

Researching with a modern, clean workflow

It’s fast, affordable, and built from the ground up to support both individual analysts and full research teams.

You can explore it here: DataSetIQ.com

Huge thank you to everyone who supported this journey.

I’m excited for what comes next.

#Fintwit #Macroeconomics #QuantTwitter #AltData #DataScience

1

3

78

17 Oct 2025

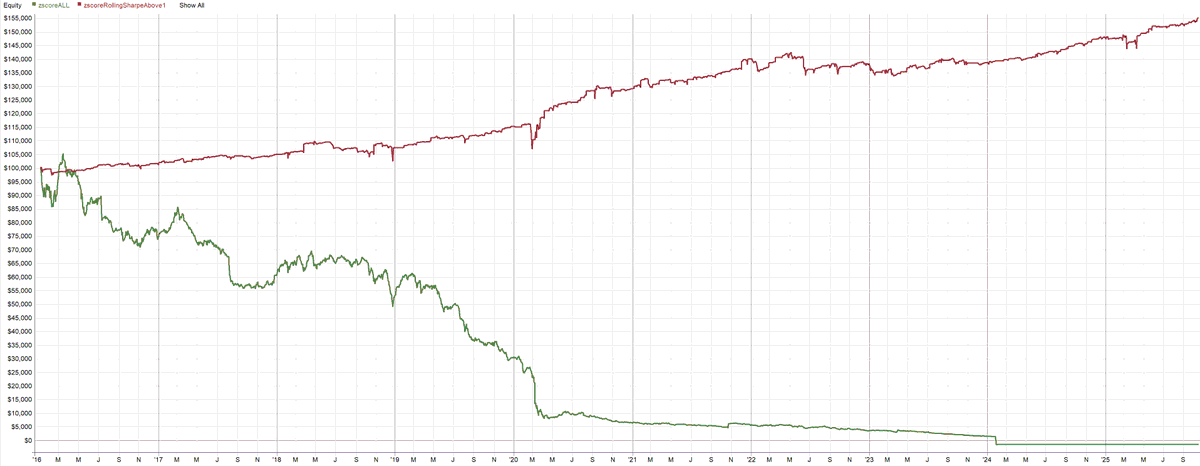

Do strategies work better if you only trade the names that historically like that strategy?

I was skeptical. I kept hearing this from Perry J. Kaufman and in my bubble (Max Martone). So I tested it.

Setup (simple swing mean‑reversion):

• If z‑score < ‑1 → go long next bar open

• Exit when Close > Open (first green day) or after 5 bars (whichever comes first)

Ranking idea:

I ran this on each stock and tracked a running Sharpe (up to the day before the signal to avoid look‑ahead). That running Sharpe became the ranking metric.

Final test (S&P 500, historical constituents):

• Same entry/exit rules

• Red line: trade only stocks whose running Sharpe > 1 for this strategy; pick the top 10 each day

• Green line: trade the whole index, simply sorting by z‑score (deeper oversold first)

Result (see chart):

Filtering the universe to stocks that historically respond to mean reversion produced a near‑Sharpe ≈ 1 after costs.

Trading everything by z‑score alone? The equity curve bleeds out—effectively bankrupt.

Takeaways:

• Universe selection is not a footnote; it’s an edge.

• Signals are name‑dependent—some stocks are mean‑reverters, others are momentum‑driven.

• Rank by behavioral fit (rolling, out‑of‑sample stats), not just by signal intensity.

• This is a rich vein for further testing: different lookbacks, decay, re‑ranking cadence, position caps, and risk parity.

If this kind of evidence‑first research helps, follow for more systematic tests and automation ideas. 📈

#QuantTwitter #SystematicTrading #MeanReversion #SP500

5

2

75

5,995

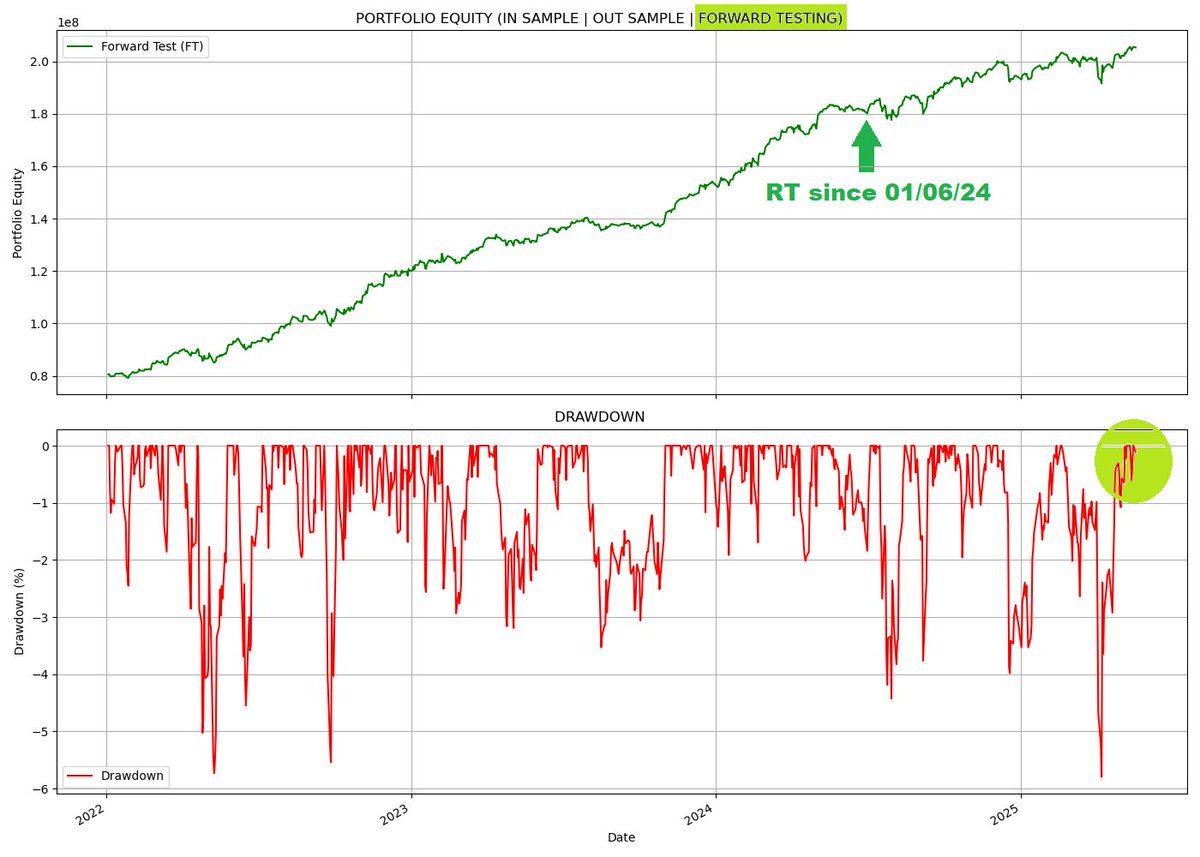

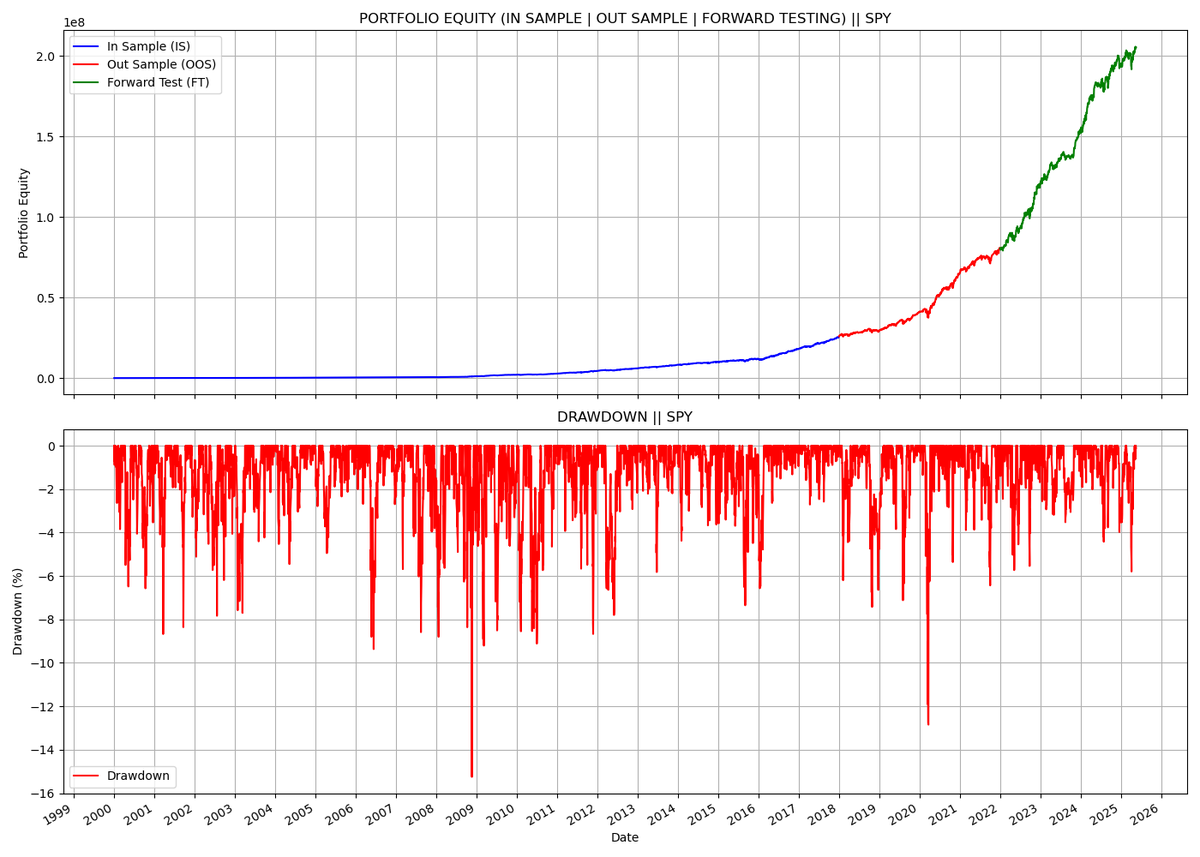

21 Sep 2025

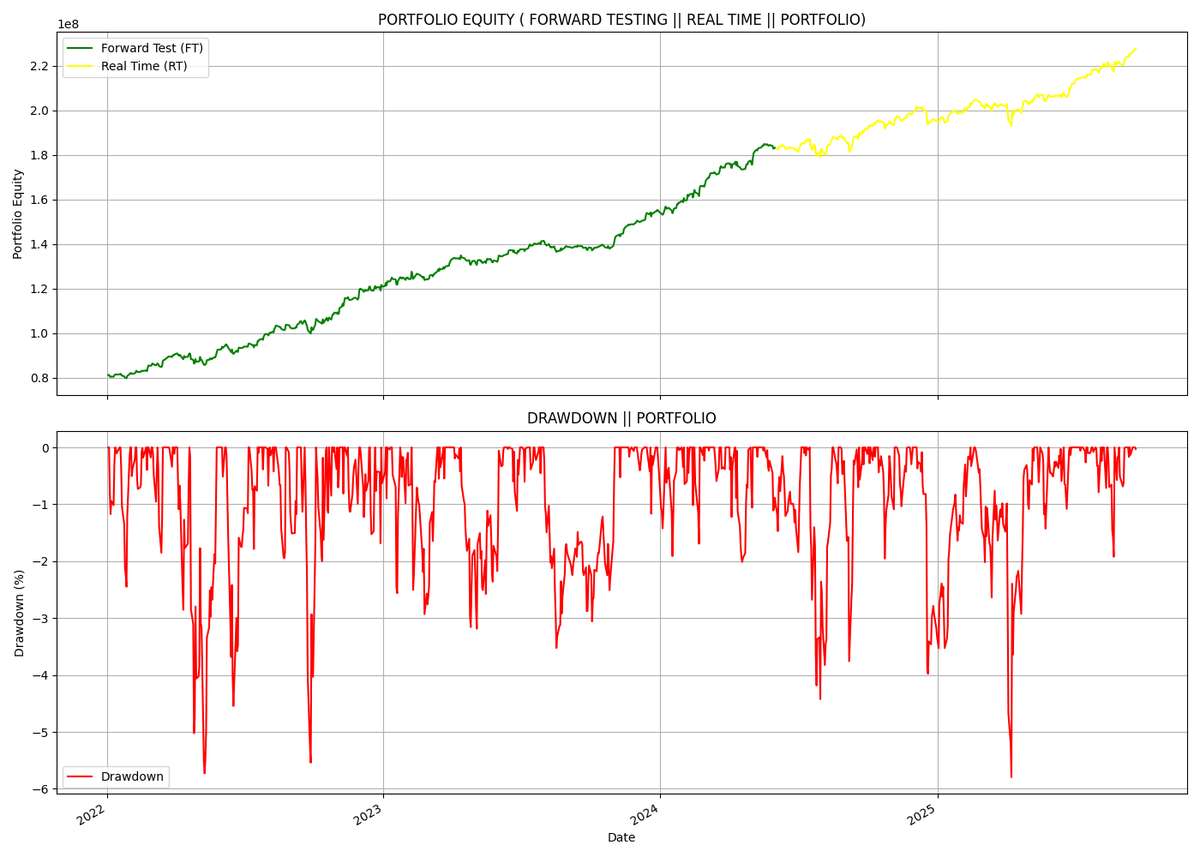

🚀 New All-Time Equity High! 📈

Linear Regression – LONG (PACK 1) keeps pressing higher in forward real-time.

From May’s peak… another 4 months of relentless grind up.

🧠 Stats snapshot:

• Annual Return: 35.0%

• Winners: 65.9%

• Max DD: -13.2%

• % Positive Months: ~80%

Packs 2 & 3 also available.

⚠️ Only 1 slot left — then closed.

👀 Next project? The SHORT pack.

If you thought LONG was smooth, wait until both are combined. 🔥

📊 See it yourself 👉

🔗 ko-fi.com/s/256a86b7b8

#QuantTwitter #TradingEdge #AlgoTrading #EquityHigh

19 May 2025

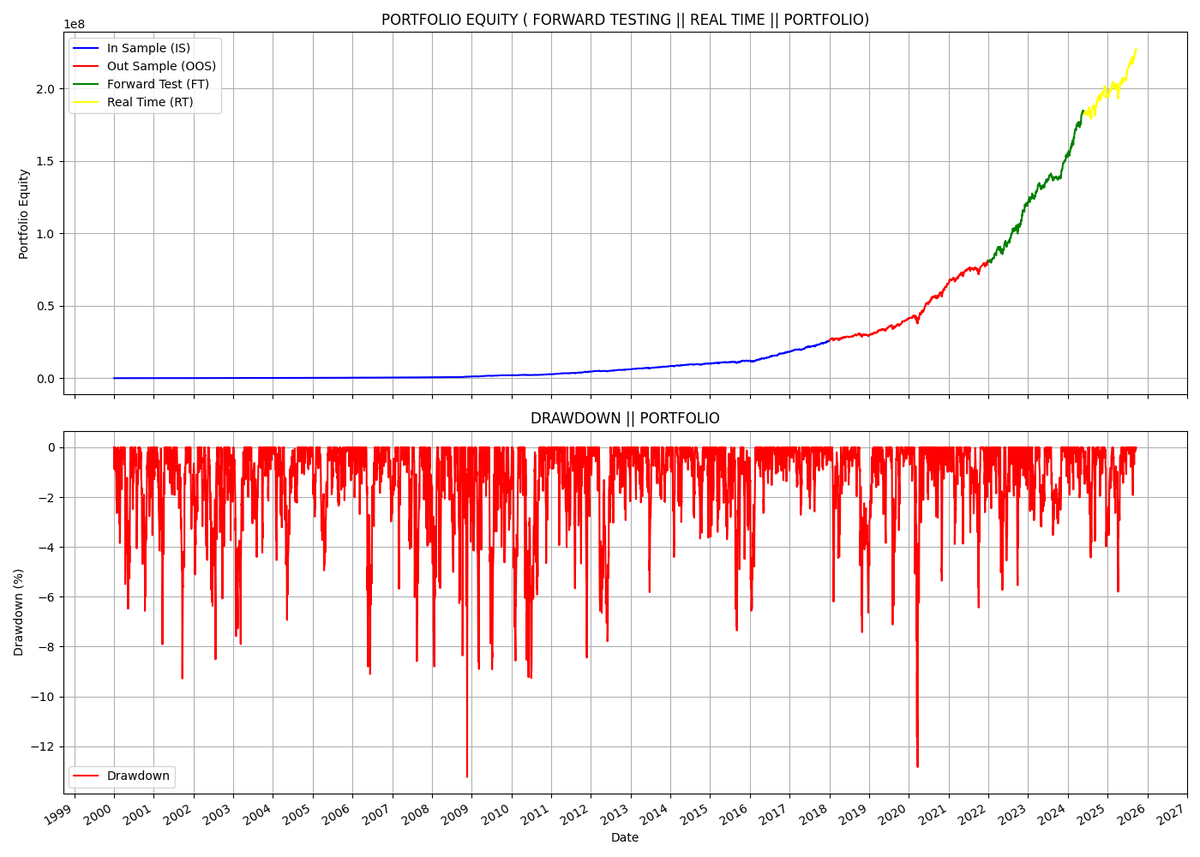

🚀 New Equity High Alert! 📈

Linear Regression – LONG (PACK 1) just hit a fresh all-time high in forward testing real-time!

🧠 Packs 2 & 3 also available — more edges, same consistency.

⚠️ Only 3 slots left — last chance to grab this research project!

👀 New project in the making...

This time, we’re going SHORT. 📉

If you liked the LONG edge, wait until you see what happens when you combine both.

Stay tuned. 🔥

📊 See it yourself 👉

🔗 ko-fi.com/s/256a86b7b8

#QuantTwitter #TradingEdge #Backtest #AlgoTrading #EquityHigh

1

7

2,378

19 Jul 2025

Poll time!

Do you prefer backtest results as a thread or an article?

👇 Drop your backtest ideas in the replies — I’ll pick a few to run next!

#NQ #Backtest #TradingStats #QuantTwitter

45%

Article

55%

Thread

99 votes • Final results

6

1

7

3,525

16 Jun 2025

🧵 How I Trade $TSLA Using Dealer Flow, Gamma Traps, and Real Risk Zones

This isn’t about trendlines.

It’s about who’s forced to move size — and when.

Here’s how I catch $TSLA trades before the breakout 👇

#TSLA #optionsflow #QuantTwitter

1

1

7

225

19 May 2025

🚀 New Equity High Alert! 📈

Linear Regression – LONG (PACK 1) just hit a fresh all-time high in forward testing real-time!

🧠 Packs 2 & 3 also available — more edges, same consistency.

⚠️ Only 3 slots left — last chance to grab this research project!

👀 New project in the making...

This time, we’re going SHORT. 📉

If you liked the LONG edge, wait until you see what happens when you combine both.

Stay tuned. 🔥

📊 See it yourself 👉

🔗 ko-fi.com/s/256a86b7b8

#QuantTwitter #TradingEdge #Backtest #AlgoTrading #EquityHigh

1

6

5,125

22 Sep 2024

Connors' RSI(2) strategy flips the script: buy pullbacks, not breakouts, sell oversold bounces, not support breaks. 📉 This mean-reversion model helps traders capitalize on short-term market moves. Python lets you easily tweak the system. Check out the GitHub code for your own fine-tuning and backtesting! 🔧📊

#RSI #MeanReversion #AlgoTrading #PythonFinance #QuantTwitter

github.com/russs123/RSI/blob…

6

288

5 Nov 2020

Join our Department & the @UNC Tar Heel community! We are hiring a Teaching Assistant Professor to teach statistics and research methods! Preferred start date is January 2021. #AcademicTwitter #QuantTwitter #StatsTwitter unc.peopleadmin.com/postings…

4

2

9 Oct 2019

On my way to my first #SMEP Annual Meeting in Baltimore. Looking very much forward meeting everyone!

#TeamMethods #QuantTwitter

@EDMSatUMD #smep19

2

11

9 Oct 2019

We’re so excited to host methodologists from all over for the #SMEP Annual Meeting in Baltimore this week.

Welcome to Charm City! 🥳🍾

#TeamMethods #QuantTwitter

9

7 Sep 2019

He’s got it out for QuantTwitter... poor guy needs to learn some python

2

3

26 Aug 2019

Welcome back, @UMDCollegeofEd!

We’re looking forward to another great year full of beautiful, beautiful statistics.

#teamMethods #quantTwitter

3