Joined September 2017

- Tweets 4,096

- Following 649

- Followers 595

- Likes 133,267

479 Photos and videos

Pinned Tweet

27 Oct 2023

"Dad, what was it like longing bonds into a global sovereign debt crisis?"

7

15

144

35,092

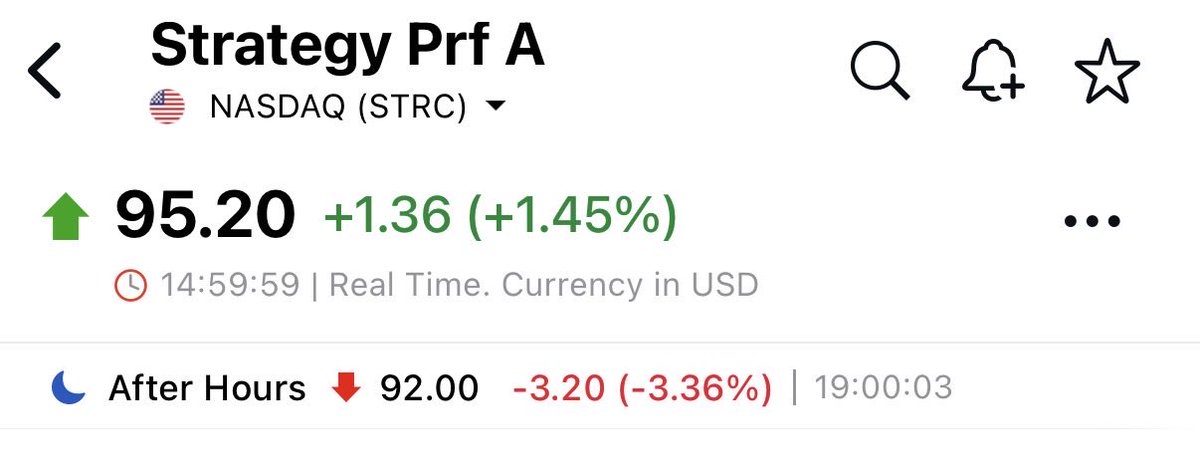

13h

$STRC investors looking around nervously "We'll get back to par right guys? No one is jumping ship right?"

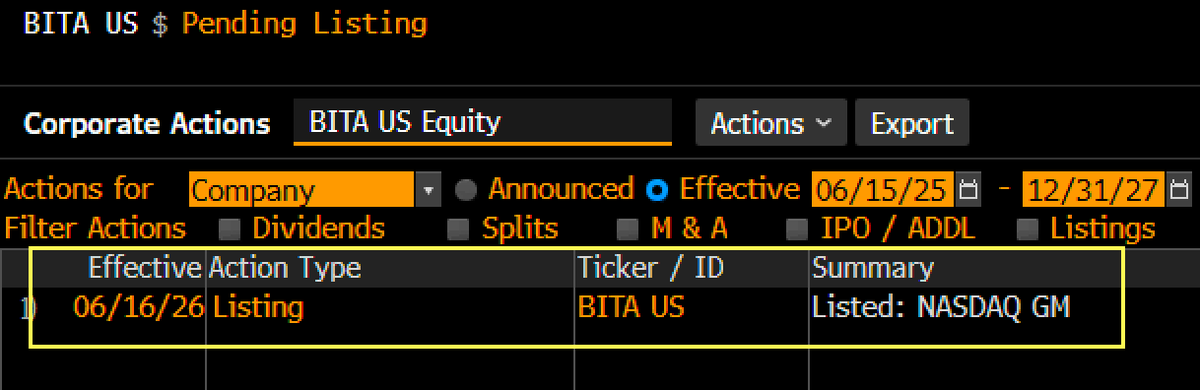

ALL SET: the iShares Bitcoin Premium Income ETF $BITA is launching TOMORROW (tue). Confirmed by Nasdaq. Also, the ETF will target 15-25% annual yield while trying to capture at least 70% of bitcoin's upside in process.

3

3

16

1,486

14h

ITT: A buncha trapped investors asking

"Wen back to $100" ...not looking good for them in the after hours pricing ☠️

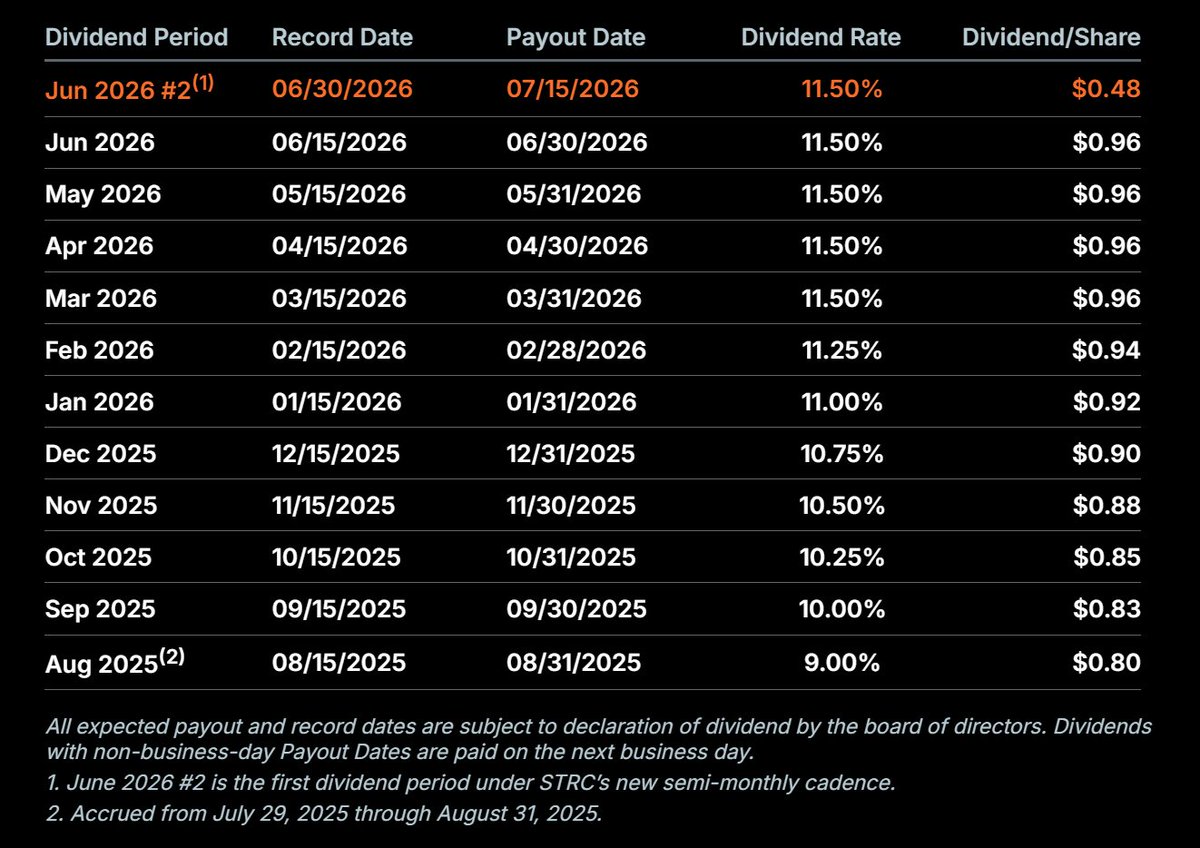

Semi-monthly dividends on $STRC start now. The first record date under the new cadence is June 30.

1

44

Rob retweeted

Americans realizing they spent $75 billion fighting Iran, then another $300 billion rebuilding Iran, just to reopen the Strait of Hormuz that was already open before the war started

1,203

9,499

58,635

1,447,603

Rob retweeted

Jun 14

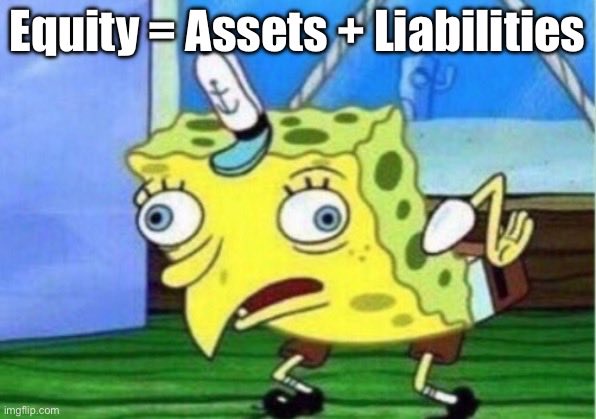

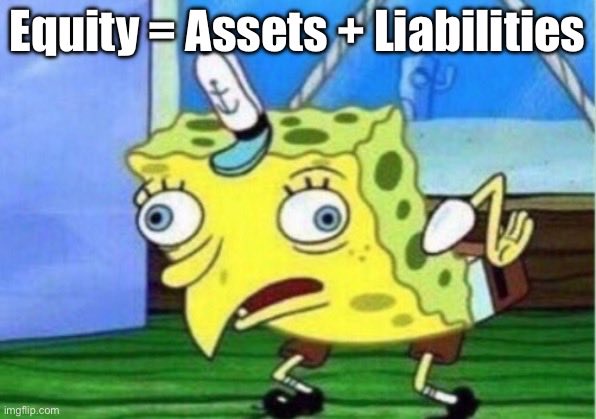

Their own marketing "ev mNAV" slop breaks the most fundamental rule of finance 101:

The shareholders’ equity number is a company’s total assets minus its total liabilities.

Equity = Assets - Liabilities

Therefore, they've somehow hoodwinked their investors to believe that:

Equity = Assets Liabilities

It is the most public facepalm of epic proportions regarding basic finance I've ever witnessed lmao.

4

1

11

425

Rob retweeted

Jun 14

This is nearly as absurd as community adjusted EBITDA

Jun 14

BPS measures Bitcoin per common share before senior claims. CEBE BPS measures Bitcoin per common share after senior claims. CEBE is the conservative risk metric. BPS is the common equity growth metric. BTC Yield measures BPS execution.

13

1

94

22,733

The ~0.81x market cap to net BTC holdings (after debt & preferred) is the more relevant multiple for common shareholder accretion/dilution.

It directly compares issuance price to common equity’s NAV claim. Below 1x, selling common to buy BTC at par dilutes existing holders’ NAV per share.

mNAV at 1.20x (EV/BTC) captures the levered enterprise view but isn’t the precise test for common equity issuance.

1

1

1

308

Rob retweeted

Fascinating watching a viral meme decay. Before Saylor blew up the balance sheet you could explain this promote in two words: "Bitcoin vacuum"

Jun 14

BPS measures Bitcoin per common share before senior claims. CEBE BPS measures Bitcoin per common share after senior claims. CEBE is the conservative risk metric. BPS is the common equity growth metric. BTC Yield measures BPS execution.

1

1

4

930

Rob retweeted

Jun 14

Absolutely mind boggling that @Strategy is still levering up. They're selling $MSTR shares that are worth 80 cents on the dollar to buy $1 dollar bills. Relative to its BTC holdings after accounting for debt and preferred equity liabilities, MSTR common trades at ~0.8x NAV. This behaviors tells me the market's message needs to get louder for it to be understood.

90

31

357

136,734

Rob retweeted

Jun 14

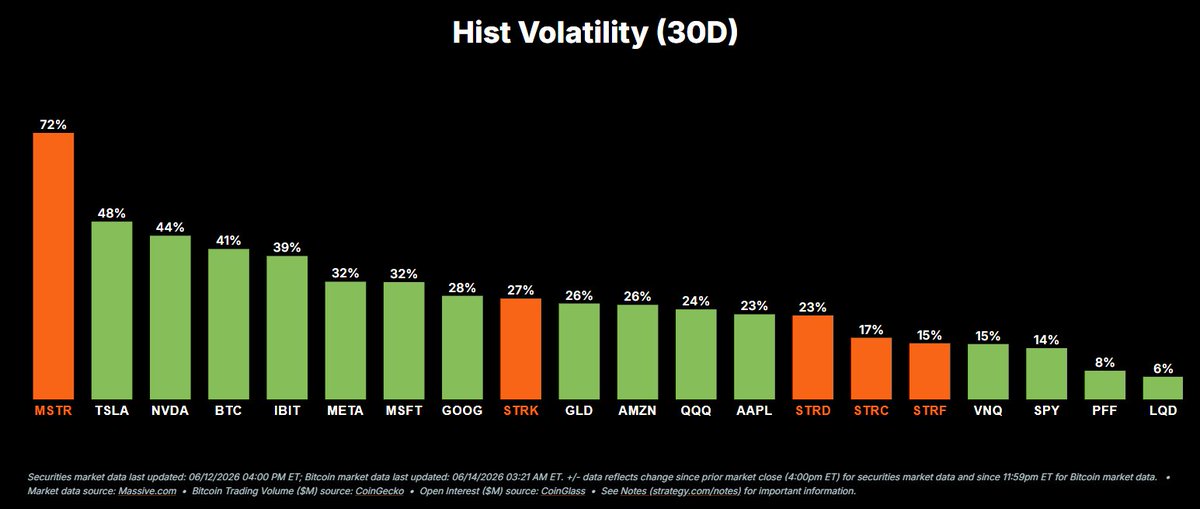

$STRC has never traded this low into an ex-dividend date (tomorrow). Highly unlikely a 25 bps dividend rate increase fixes this next month, and maybe not even 50 bps at this pace. Meanwhile the hubris has not been dented. Pain can only end when the orange dot tweets do.

Jun 1

“Steady”…not sure the market agrees but let’s see. For the month of June it appears Strategy will be prioritizing MSTR owners over STRC owners.

24

9

122

16,351

I'm genuinely concerned about Strategy's position right now.

Trading at 84% of its Bitcoin value, every option available to them makes things worse:

- Issue stock → dilutes BTC per share

- Issue more prefs → adds to a $10.7B cash obligation

- Sell Bitcoin → panic the market & drive price lower

- Suspend dividends → retail holders flee

There is no clean exit.

231

25

367

61,305

Jun 14

Things are so bad they have to push a residual liquidation value metric now that the leveraged Bitcoin exposure stuff no longer works lmao

Jun 14

BPS measures Bitcoin per common share before senior claims. CEBE BPS measures Bitcoin per common share after senior claims. CEBE is the conservative risk metric. BPS is the common equity growth metric. BTC Yield measures BPS execution.

1

69

Rob retweeted

Jun 13

If you just give us a few percent more of your money, we could finally fix the worsening education, homelessness and crime caused by our own terrible policies…

Please bro… just a few percent more.

One last tax. I swear bro. Then I’m done.

107

695

5,441

62,451

Rob retweeted

Jun 11

“I said to YOU to never sell your Bitcoin. I never said that THE COMPANY wouldn’t sell its Bitcoin.”

Jesus Christ.

1,158

772

10,784

2,409,336

Jun 11

-Anchor Protocol (Terra): 19.5% - 20% APY (Algorithmic stablecoin collapse)

-Celsius Network: Up to 18% APY (Rehypothecated balance sheet black hole)

-Pillow Fund: Up to 14% APY (Automated management unwind)

-Vauld, Hodlnaut, & Zipmex: Up to 12% - 14% APY (Contagion dominoes)

-Voyager Digital: Up to 12% APY (Unsecured credit defaults)

-BlockFi: Up to 9.25% APY (Shadow banking liquidity crunch)

-Gemini Earn / Genesis: Up to 7.4% APY (Institutional loan desk freeze)

Same candy, different cycle.

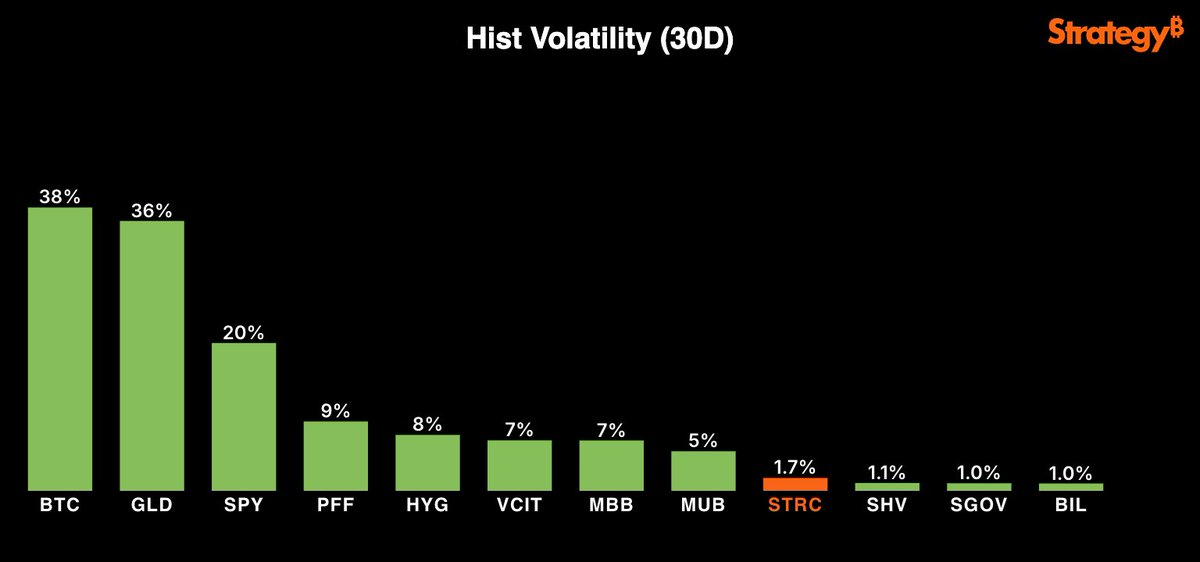

Surely, it will turn out differently this time with $STRC offering 11.5%, right?

In the words of the great @HodlMagoo:

"Don't be a retard."

(@comic is excluded)

2

2

6

298

Jun 12

✅

I saw all the Saylor cult followers posting as if $STRC was some genius revolutionary piece of financial engineering from Saylor. It is not.

Wall Street has already run a very similar playbook with Auction Rate Preferred Securities (ARPS).

They are very similar:

1) Perpetual capital for the issuer.

2) Variable yield for investors.

3) A security expected to stay near par.

4) If demand weakens, just raise the yield.

For years, they worked well, and then they got absolutely smoked in 2008.

And just like $MSTR and $STRC, the issuers of the ARPS mostly survived. The assets mostly survived. The investors are who got hurt the most.

Why? Because the buyer base disappeared overnight.

ARPS proved that a higher yield doesn't guarantee a $100 price. Once holders of it start asking "Who is buying this from me?" instead of "What's the yield?", the market will implode far far below par. It is not as if there is any collateral pledged that would create a floor on price in this scenario.

$STRC pumpers always point to liquidation preference, seniority, and even Strategy's Bitcoin as protection. Those things don't create liquidity. They don't guarantee a $100 market price.

The lesson $STRC holders are going to learn is the same lesson ARPS holders learned. That they are absorbing the risk of a liquidity vaccum.

1

2

48

Rob retweeted

Jun 11

"I promise not to sell the Bitcoin."

- Michael Saylor

That might be actual fraud right there.

60

97

916

94,641