Joined February 2023

- Tweets 47,483

- Following 139

- Followers 2,612

- Likes 83,967

2,007 Photos and videos

Pinned Tweet

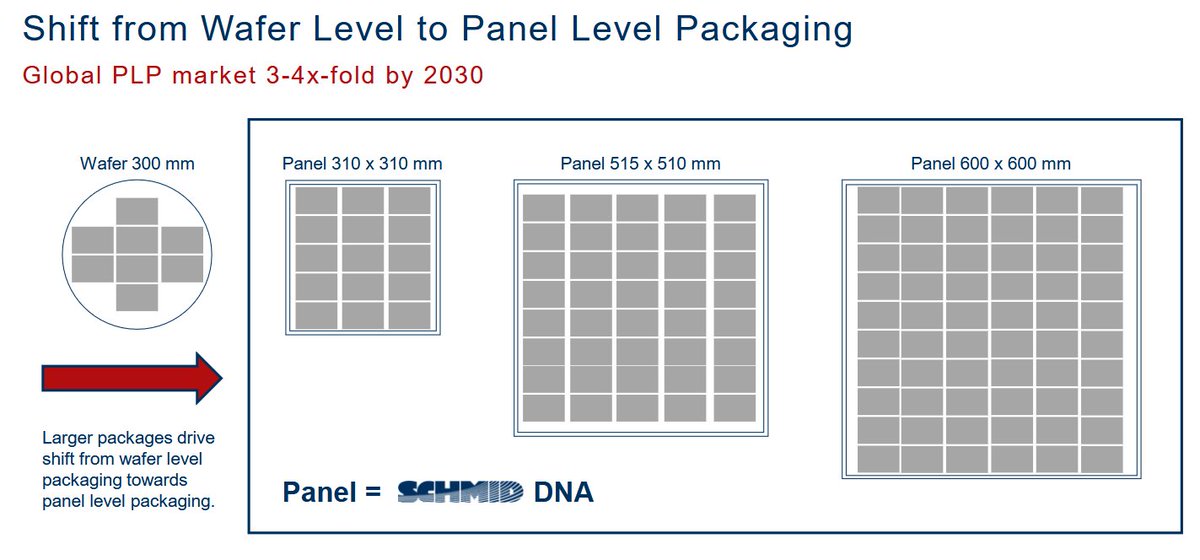

TSMC Preparing for Full-Scale Mass Production of "Panel-Level Packaging (PLP)" Semiconductors

TSMC is set to go head-to-head with Samsung Electronics using "panel-level packaging (PLP)," a next-generation semiconductor packaging technology. PLP can significantly improve the productivity of AI chip manufacturing, and with TSMC hurrying to ready mass production, a contest for leadership with Samsung Electronics—which entered the market first—looks inevitable.

According to industry sources on the 15th, TSMC is building out a materials, components, and equipment (MCE) supply chain to establish its PLP mass-production system. It is currently in discussions with domestic and overseas MCE companies on equipment investment. TSMC is reported to be planning to begin PLP mass production as early as next year, and this is read as a move in earnest toward that goal.

PLP is a technology in which a semiconductor wafer with circuitry already formed is cut into individual chips (dies) and then packaged on a rectangular panel to produce the finished product. It contrasts with "wafer-level packaging (WLP)," which is performed on a round wafer. When chips are packaged on a circular wafer, the edge regions cannot be completed into chips and must be discarded—meaning lower productivity. Running the process on a rectangular panel instead allows chips to be produced with no wasted area. Based on a standard 600×600 mm rectangular panel, roughly five to six times as many chips can be produced compared with the mainstream 300 mm (12-inch) wafer.

The company holding the upper hand in PLP technology is Samsung Electronics. After acquiring the PLP business from Samsung Electro-Mechanics in 2019, it has built up technical capability by applying PLP to mobile application processors (APs) and power management ICs (PMICs).

TSMC, by contrast, had been passive on PLP, given that it had secured its foundry competitive edge with conventional WLP. But the situation reversed as the AI chip market grew explosively—PLP can increase AI chip output and is also advantageous for realizing large-area AI chips. Accordingly, TSMC began pursuing the PLP business from 2024. It is expected to build and run a pilot production line this year and, following performance evaluation, enter large-scale production around next year. It is also reported to have already secured a global AI chip customer.

As TSMC accelerates toward PLP mass production, competition with Samsung Electronics is expected to intensify further. Samsung, too, plans to expand PLP application beyond its existing APs and PMICs to high-performance computing (HPC) chips such as AI semiconductors. Glass substrates, which are drawing attention as a substrate for AI chips, are also likely to be adopted in this PLP process—a point that suggests a leadership battle between Samsung Electronics and TSMC in the next-generation substrate market as well.

An industry official said, "Not only Samsung Electronics and TSMC, but also global outsourced semiconductor assembly and test (OSAT) companies have jumped into the PLP process market in large numbers," adding that "along with fierce competition, market growth is expected."

2

624

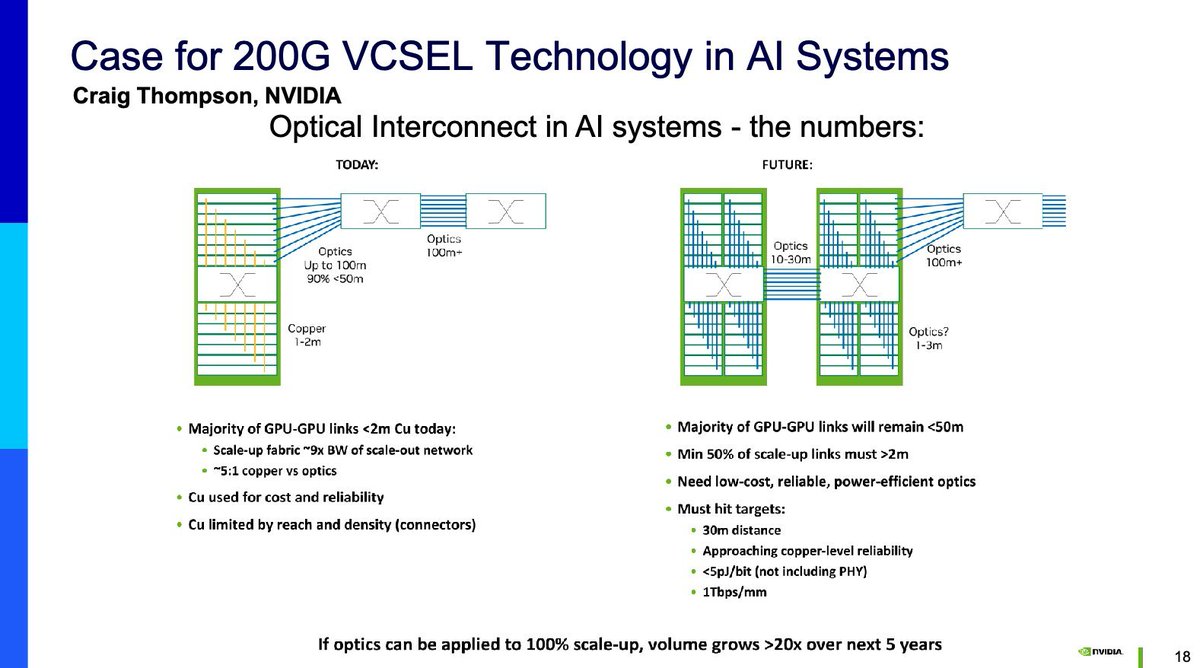

This is potential BIG NEWS in Photonics! 😱

200G VCSEL Lasers with mass volume production (potentially) starting in early 2027 👀🔥

"The 32x50G uVCSEL isn't trying to push a single lane to extreme speeds. It runs 32 lanes at 50G NRZ, a massively parallel approach that fits naturally into co-packaged optics and near-packaged optics architectures [...] for AI scale-up interconnect"

Would affect the medium-term Revenue profile of the Big Photonics companies (the InP oligopoly) $LITE $COHR $AAOI

PicoJool announced 200G VCSELs today. And it’s compelling.

The company is sampling quad 100G, quad 200G, and 32x50G NRZ uVCSELs next quarter, with high-volume ramp targeted for early 2027. The 200G parts clock in at 37GHz bandwidth, a meaningful threshold for 200G-per-lane operation.

Importantly, PicoJool is building on one of the largest existing optical manufacturing ecosystems. The company’s thesis is that GaAs VCSEL capacity scales far more easily than the InP laser supply chains that many investors have focused on.

PicoJool is building on GaAs with WIN Semiconductor, which has shipped over a billion VCSELs for 3D sensing applications. This decision to stay on GaAs instead of chasing indium phosphide or silicon photonics is important. GaAs VCSEL manufacturing capacity is vastly larger than merchant InP laser capacity.

I'm also interested in the "slow and wide" option.

The 32x50G uVCSEL isn't trying to push a single lane to extreme speeds. It runs 32 lanes at 50G NRZ, a massively parallel approach that fits naturally into co-packaged optics and near-packaged optics architectures. The cost target is to compete with copper which makes sense for AI scale-up interconnect, where you're wiring hundreds of GPUs inside a rack.

The founder has done this before, too.

Al Yuen shipped the first GbE VCSELs in 1996. At Alvesta, his first startup, he invented the active optical cable in 2001, the now-standard format where the E/O conversion lives inside the cable assembly rather than a separate pluggable module. Alvesta was acquired by Emcore in 2002. He went on to develop vertical oxidation techniques for high-volume VCSEL fabrication in 2016.

Roadmap goes to 3.2T. Worth watching!

44

26m

Great article about $AMPG , the 5G/AI-RAN play

Take into account it's missing a potential (big) supply deal for TELUS in Canada

1

5

585

RT @anasalhajji: Oil permabulls got smoked!

Here is a great advice form Will Rogers: “If you find yourself in a hole, stop digging.” https…

10

Alex A.C. retweeted

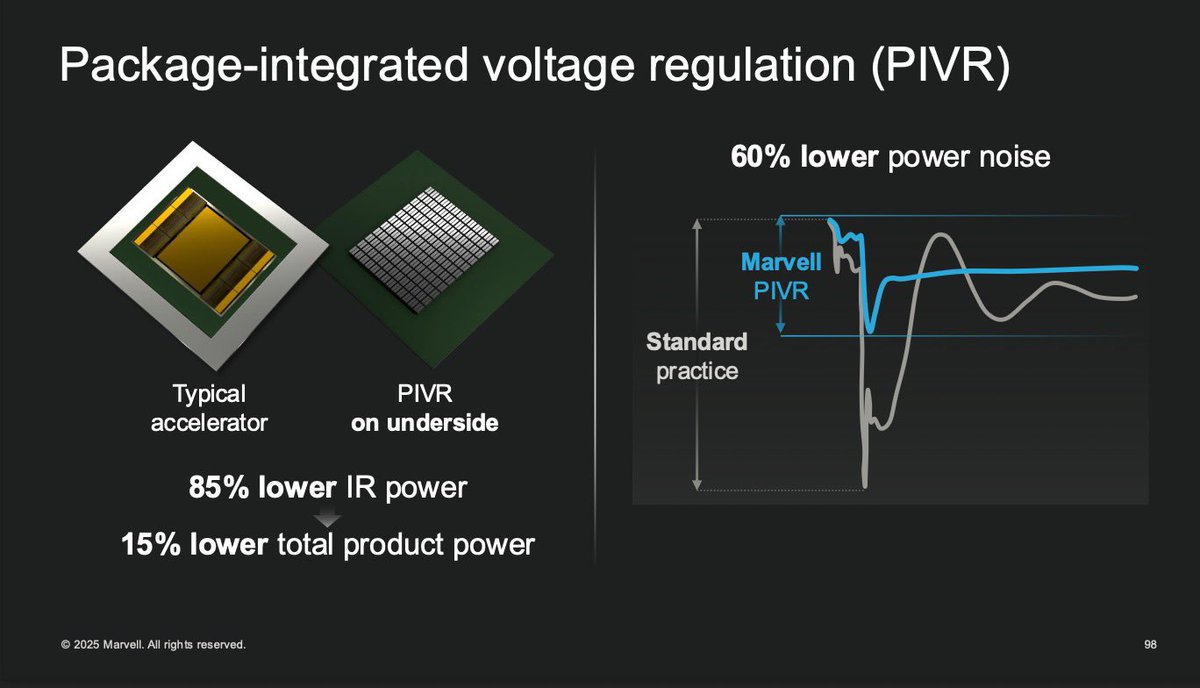

Marvell’s PIVR (Package-Integrated Voltage Regulator) technology combines high-performance PMICs, ultra-thin ferrite inductors, and precise power filtering control, achieving current densities of 3–4 A/mm²—significantly higher than the 1.5–2 A/mm² typical of traditional solutions—while supporting real-time voltage regulation to reduce overall power consumption by roughly 15%.

open.substack.com/pub/tspase…

2

5

32

1,808

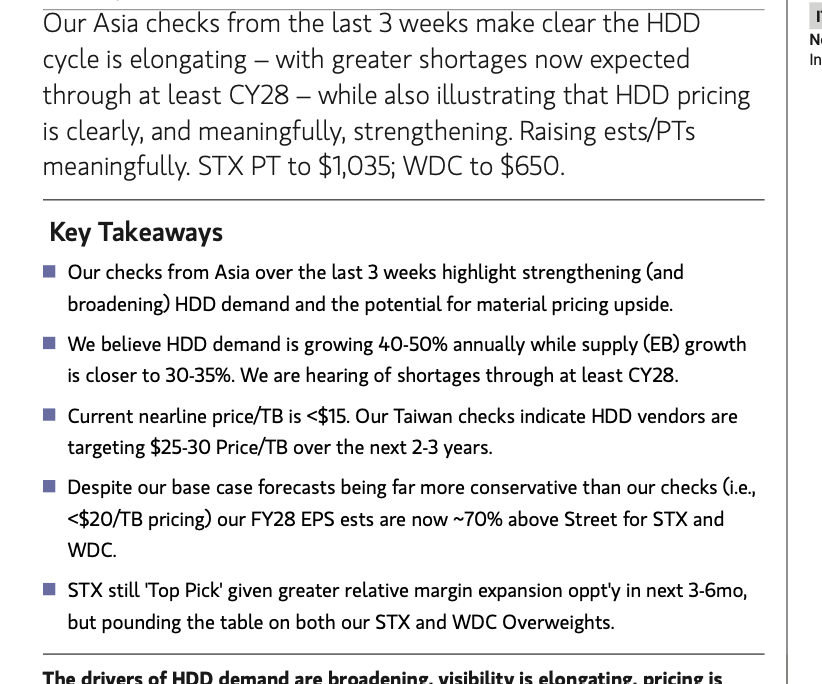

MS on storage. I actually think its much worse than many realize in terms of what agentic storage demand will cause. Detailed in our full report on agentic AI impact on storage.

thediligencestack.com/p/the-…

3

573

하이닉스 HR 분과 지속적으로 교류하며 미팅을 합니다. 로드맵을 들으니 전망이 밝아보였습니다.

누라두님께서 언급한 포인트도, HR을 통해 들었기에 중요한 트윗이라 생각하여 공유드립니다 :)

4

424

More WS investing firms join the club of PT $1600 for $MU Micron 🙌 Re-rate incoming? 🤞

10h

Aletheia on $MU:

"We forecast MU’s EPS to jump 8.5x in CY27E, followed by a further 1.8x expansion in CY28E. This implies roughly 15x cumulative EPS growth and $350–400bn of FCF generation in FY26-28E."

"We now expect server DRAM ASP to jump a further 30% in C3Q26 (vs previous expectation of 10- 15%); this is likely to rise by another 10-15% in C4Q26 (same as previous expectation)"

"we now expect HBM ASP to double YoY in C2027"

"Our analysis shows that memory devices are becoming the most critical components in the AI hardware system as their combined content value are expected to cross over 70% in 2027 vs mid-40%s in 2025. For DRAM-intensive device such as Vera CPU, the SoCAAM alone contributes over 70% of BOM in 2H26; the full spec Vera CPU rack could reach a staggering $26M ASP per rack..."

1

1

6

1,093

Alex A.C. retweeted

$IQE & $TSEM enter a multi-year InP epiwafer supply agreement.

Do you understand how f*cking huge this is for IQE?

-> IQE is being designed into the pluggable wave next-gen modulator/OCS roadmap.

-> Confirms IQE as a qualified, non-Chinese InP epiwafer source.

-> Diversifies IQE's optical customer base beyond $LITE / $MTSI to foundry in $TSEM. So multiple Tier-1 optical anchors.

Quick fun fact: IQE sued Tower in 2022 for misappropriating trade secrets to obtain patents.

So this Tower agreement lets IQE keep optionality on RF SOI type engineered substrate/layer transfer applications without IP risk.

And converts a former enemy into a customer - always a massive bullish signal that a company's products are critical.

22

26

272

29,388

Jun 14

"The last thing any of us want is a world where every company across every sector is ceding value to a few models that eat everything they see. If all the value is accrued by only a few models, the political economy will simply not tolerate it [...] Let us not bring that dynamic into the AI era, with a small number of AI systems capturing all the economic returns, while entire industries find their knowledge commoditized right out from underneath them"

4

609

Alex A.C. retweeted

Jun 14

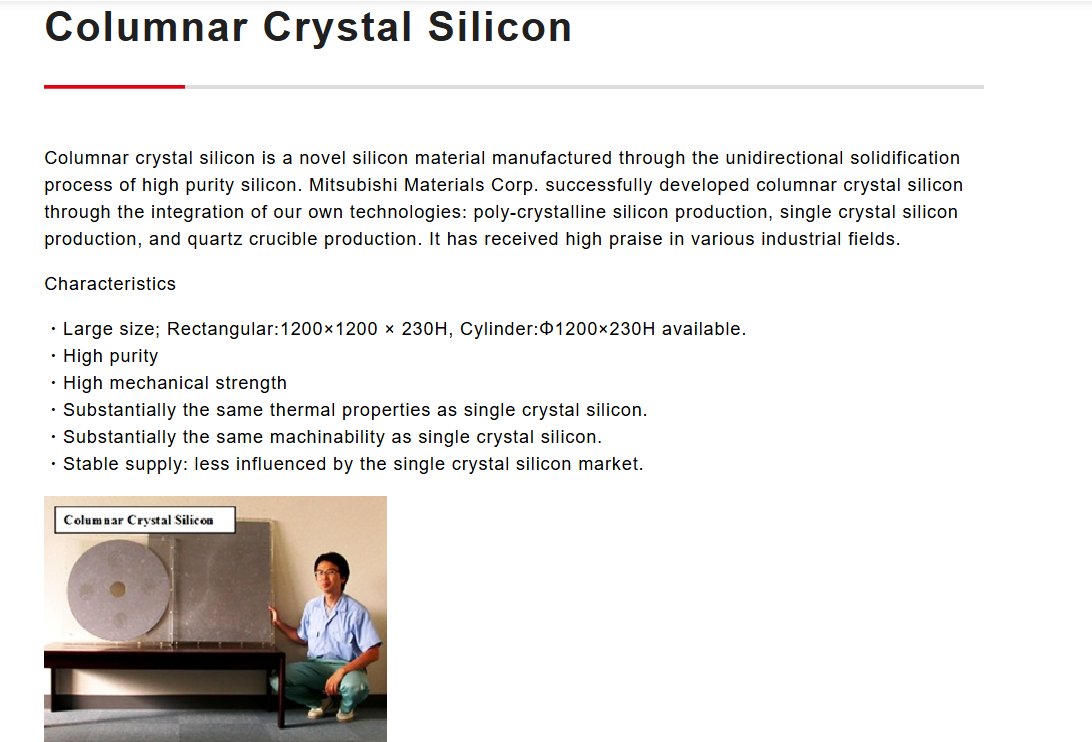

Jokes aside

Square silicon substrates for packaging do exist

Mitsubishi Materials has produced 510mm x 510mm square silicon panel substrates in 2024

Now, these are not made by using the Czochralski process, which creates a super-high-purity monocrystalline silicon boule

Mitsubishi's columnar silicon is made by casting high-purity silicon and directionally solidifying it, and it is polycrystalline with grain boundaries

These are not suitable for transistor production because they are not that pure (7N vs 11N), but they can absolutely be used as substrates for advanced packaging

Jun 14

Stacy has created a new process for creating cuboidal silicon ingots called the Rasgon process

It's a huge upgrade over the traditional Czochralski (CZ) process

6

14

190

40,823

The shift brought about by HBM:

- From 1957 to 2020, DRAM cost per Gb declined by roughly one order of magnitude every five years, making it one of the clearest examples of Moore’s Law in cost terms.

- However, demand for AI infrastructure and the emergence of HBM have directly overturned the cost-reduction pattern that had persisted for decades.

35

107

847

191,416

Jun 14

Little ones can grow much faster than the big ones and to find MUCH more opportunities

Take the advantage anons 👌

Jun 14

Warren Buffett: "If I do something brilliant — don't count on it — with $5 billion, it's 1% of [Berkshire Hathaway's] net worth. And 1% doesn't do much. So I have to think about big things — and they are limited."

"I made money in an entirely different way when I was working with, originally, $9,800 ... Everything I did could double our net worth. There were thousands of possibilities — and I wanted to know every one of them."

(Charlie Rose || 2022)

284

Alex A.C. retweeted

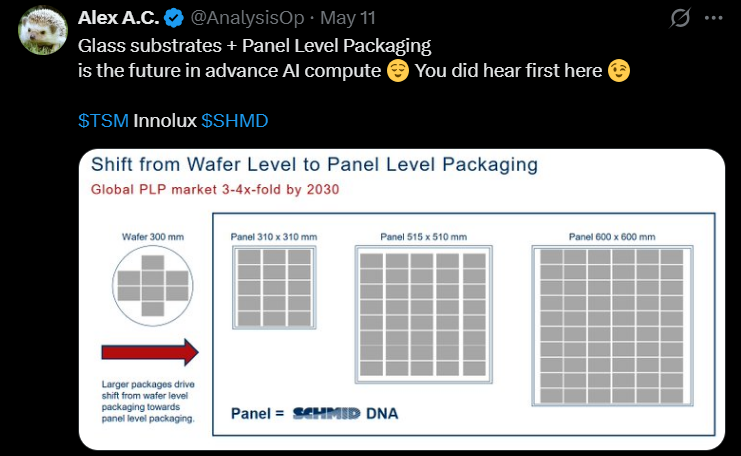

May 11

Glass substrates Panel Level Packaging

is the future in advance AI compute 😌 You did hear first here 😉

$TSM Innolux $SHMD

May 11

Rumor: TSMC will partner with Innolux on FOPLP (Fan-out Panel-Level-Packaging) advanced packaging for AI chips, media report. TSMC will work with Innolux at its Longtan plant, aiming to use FOPLP on future AI and HPC chips. Innolux is already said to be working with SpaceX on FOPLP, and its annual report says monthly FOPLP output has already 10x’ed to 40 million units, at high yield. Capacity is full. $TSM #Innolux $3481TW $2303TW #semiconductors #semiconductor #FOPLP

money.udn.com/money/story/56…

6

22

103

22,293

Jun 14

For the 🐔🐔🐤 bros that are afraid of allocating money in names that require knowledge and to follow the story continuously; you can between 50% - x2 in the next few years with the Big Tech/Big Semis stocks

Jun 14

There is no stock market bubble.

Large Cap Fwd P/E's (2027/28) & Analysis:

$NVDA: 22.9x -> 16.1x

$GOOGL: 24.8x -> 20.6x

$MSFT: 20.2x -> 16.8x

$AMZN: 24.2x -> 17.9x

$META: 15.7x -> 13.8x

$AVGO: 19.7x -> 16.2x

Analysis:

$NVDA: 16.1x (2028) on >40% growth is the market pricing a sharp deceleration. But Vera Rubin in full priduction ramping in H2. Feel like the market is pricing in ASIC share erosion heading into 2028, but then you've got CPO coming soon.

$GOOGL: The most priced to perfection on this list on cloud backlog Search re-acceleration. But you've got things like TPUs, OCS Jupiter fabric as a structural cost edge. Gemini too.

$MSFT: Stupid cheap. Maia live in DCs for Copilot/foundry inference. Targeting ~50% of AI compute on own silicon by 2028. Rights to OAI's chip designs.

$AMZN: Tough company to model margin trajectory on tbh. AWS acceleration retail/advertising operating leverage make the earnings base the most optionality-driven & hardest to pin. And Trainium shipping, anchored by Anthropic. Plus at what point do robotics/automation start to ramp?

$META: Very cheap due to a "trust discount" on their AI capex, not an earnings problem. If the capex visibly converts to revenue/margin, you get both EPS upside multiple re-rating.

$AVGO: Steep de-rating after their earnings report last week mainly because of ASIC ramp. On CPO, there's arguments to be made that Broadcom wins over Nvidia longer-term.

Personally, I'll be buying Nvidia, Microsoft, Meta and Broadcom a little more heavily through Q3-Q4.

I highly doubt we'll see such compressed valuations in quality tech names for a very long time.

Caveat: 2028 PE's are via my own EPS modelling.

3

823

Alex A.C. retweeted

Jun 14

Simple, the Trump admin cannot roll out new restrictions/export controls targeting China because the Chinese can/will retaliate

We are not in the H100 era, where the supply chain was largely concentrated in Taiwan/Korea/Japan

Becuz of shortages, Nvidia & hyperscalers have been forced to qualify Chinese suppliers, especially in the PCB supply chain and electrical components like transformers

China had a chokehold on optics (optical fibers and transceivers) from the beginning, and this is just getting amplified as optical content in DCs is increasing

Coherent CEO went to China with the Trump delegation, asking for InP for lasers

I want u guys to study the optical fiber preform supply chain, and who are the largest suppliers

Btw, Chinese exposure is also spreading to other parts of the AI supply chain

High end MLCCs use Dysprosium Oxide and China supplies most of it to Japanese producers

Tungsten ban from China is causing the prices of WF6 gases to shoot up

If PTFE is finalized for M9/M10 CCL, then Shengyi and Chinese PTFE suppliers will have a huge chokehold over Nvidia

Google is in talks with Envicool for the supply of cooling components

If diamond-copper composites are adopted as heat spreaders for GPUs, then China will establish a chokehold there as well, since most of the synthetic diamonds are produced there and China is at the cutting edge of this tech

I haven't even talked about the use cases of gallium, germanium, tellurium, antimony, bismuth, fluorine, terbium, yttrium, ferrite cores in the AI supply chain, and how China has a chokehold there

The Trump admin is constrained in a lot of ways and can't unilaterally export control stuff

Jun 13

I share concerns about China’s access to advanced AI models, but if the admin feels so strongly about this, I have a series of questions it should answer:

- Why did it loosen export controls to allow AI chip sales to China, which allow China to build its own Mythos?

- Why is it not enforcing existing export controls that would prevent China from smuggling AI chips from Southeast Asia and other countries?

- Why is it not enforcing existing export controls that would prohibit Chinese companies from training advanced AI models on remotely accessed AI chips? Or imposing tighter controls on remote access?

- Why has it still not closed a loophole it created that allows Chinese front companies outside China from making AI chips at TSMC or Samsung?

- Why has it not tightened controls on China’s access to semiconductor manufacturing equipment (which have not been updated in over 18 months - the longest the US has ever gone without updating them)?

- Why has it not imposed equivalent controls on all advanced AI models being served to China/Chinese companies?

- Why did it restrict access to all countries and foreign nationals accessing Mythos/Fable, not just China?

If the admin was serious about addressing the challenges posed by China in AI, it would be using export controls to address all of these questions and build a comprehensive strategy to prevent China from building or obtaining advanced models. But over the last 1.5 years, it has loosened or ignored controls on China, and only opened new loopholes in controls it inherited. If the admin truly has deep concerns about China’s access to advanced models, it has to act accordingly. It isn’t.

41

113

957

192,511

Alex A.C. retweeted

Jensen Huang giving a masterclass on why open-source AI matters, and why, by extension, the $NBIS token factory thesis gets more important as AI moves into cyber defense against Mythos-class models:

“The answer to that, as it turns out, is not another Mythos. The way you defend against a super force is not with another super force. It’s with an abundance of cheap force.

And so the best answer for Mythos is actually open source.

Open source so that we have swarms of white blood cells. We have swarms of white blood cells, and these white blood cells are trained to detect and alert us of threats.

And the moment that it detects threats, it figures out where the threat is coming from and closes the door.

And so you can’t count on the fact that your AI is better than their AI, but you can count on the fact that you got more AI than they got. That you can count on.

And so the number of defenders we can have, so long as they’re open source, because open source is cheap, open source models are very good now.

And we can run all of these open source models trained on defending ourselves, and that’s the swarm, the dome if you will - the cybersecurity dome.

And so that’s the answer.”

Open source isn't just good for developers, it's one of America's strongest tools for AI security.

More models means more defenders and more front doors protected.

Earlier this week at the @MilkenInstitute Global Conference, Jensen sat down with @beckyquick to explain why 👇

1

7

40

6,873

Alex A.C. retweeted

Jun 13

Anthropic Deputy CISO Jason Clinton: "And so when I think about what a nightmare scenario now looks like, it's we have this evidence of assault typhoons, type actors using agents to run their attacks, we can now see if you can combine that agentic attack with nation-state level vulnerability finding, as we're seeing from models like Mythos and models in that class, that's where I think it's just as I'm thinking through the next few years, it's just an incredible daunting challenge for security leaders to figure out how am I going to defend myself from that because that call in the middle of the night could be literally one of the most sophisticated things you've ever seen."

Jun 13

Anthropic Deputy CISO Jason Clinton earlier this week:

"I suspect that we have ~7 to 10 months before open weights models have this capability. And when that happens, we will have the roughest, most difficult time in our careers that we've had as cybersecurity folks. That will happen for approximately I would guess 18 months."

1

4

21

9,486

Jun 14

"A backup option where an enterprise controls the [AI] model layer is a must now" 👀

Zephyr is answering a fren a question about AI demand.

What I see is Zephyr is getting independently to the same place where $NBIS Nebius is going to start working soon: the new concept of "partner ecosystem" with the enterprises 🔥

Jun 13

BRUH

I'm talking about trust

Why are u inserting AI demand in it??

AI demand will obviously grow (including demand/token processing for closed-source models), but a backup option where an enterprise controls the model layer is a must now

1

443