[LIVESTREAMED ON PUMP FUN - NEXT-GEN P2E BY CORPDEV]

spacexcolony.fun

I've seen countless "blockchain games" where you need to connect your wallet, complete random tasks, and waste hours doing things you don't enjoy just for a CHANCE to earn rewards.

That's kindergarten level.

Welcome to SpaceX Colony - a first-of-its-kind next-gen P2E that lives directly on the Solana blockchain.

The second you buy $COLONY, you start playing and earning $SPCX rewards directly to your wallet every 5 minutes, 24/7.

No sign-ups.

No wallet connections.

No random actions.

Your on-chain data is already enough.

Hold at least 1M $COLONY and your colony plot instantly appears on Mars.

Every holder owns a plot, develops it over time, improves in-game stats and receives rewards every 5 minutes.

Sell tokens?

Your colony gets downgraded.

Your stats decrease.

Your progress stops.

Read the thread below if you want more details.

17

4

27

2,662

Utsav retweeted

A day for sweets!

Do Your Own Deals

theindiaportfolio.com/

#TheIndiaPortfolio #corpdev #mergers #acquisitions #venturecapital #privateequity #directory #genAI #headless #agenticAI #elections

2

2

39

May 15

They gave me a choice between being retarded on social media and making millions of dollars on their corpdev team.

In hindsight, I may have chosen poorly 😂

1

3

75

May 13

Would love to see a playbook for CFOs supervising a corpdev/M&A/strategy team. From what I’ve seen, this can be a major learning curve for CFOs with traditional accounting backgrounds.

1

1

3

1,149

May 11

lol deposition video of Mike Wetter, the corpdev MSFT exec working with openAI, is interesting from a numbers perspective and the terms of the MSFT/OAI deal

Satya Nadella, who runs the $3 trillion market cap MSFT, has been sworn in

1

6

6,003

May 6

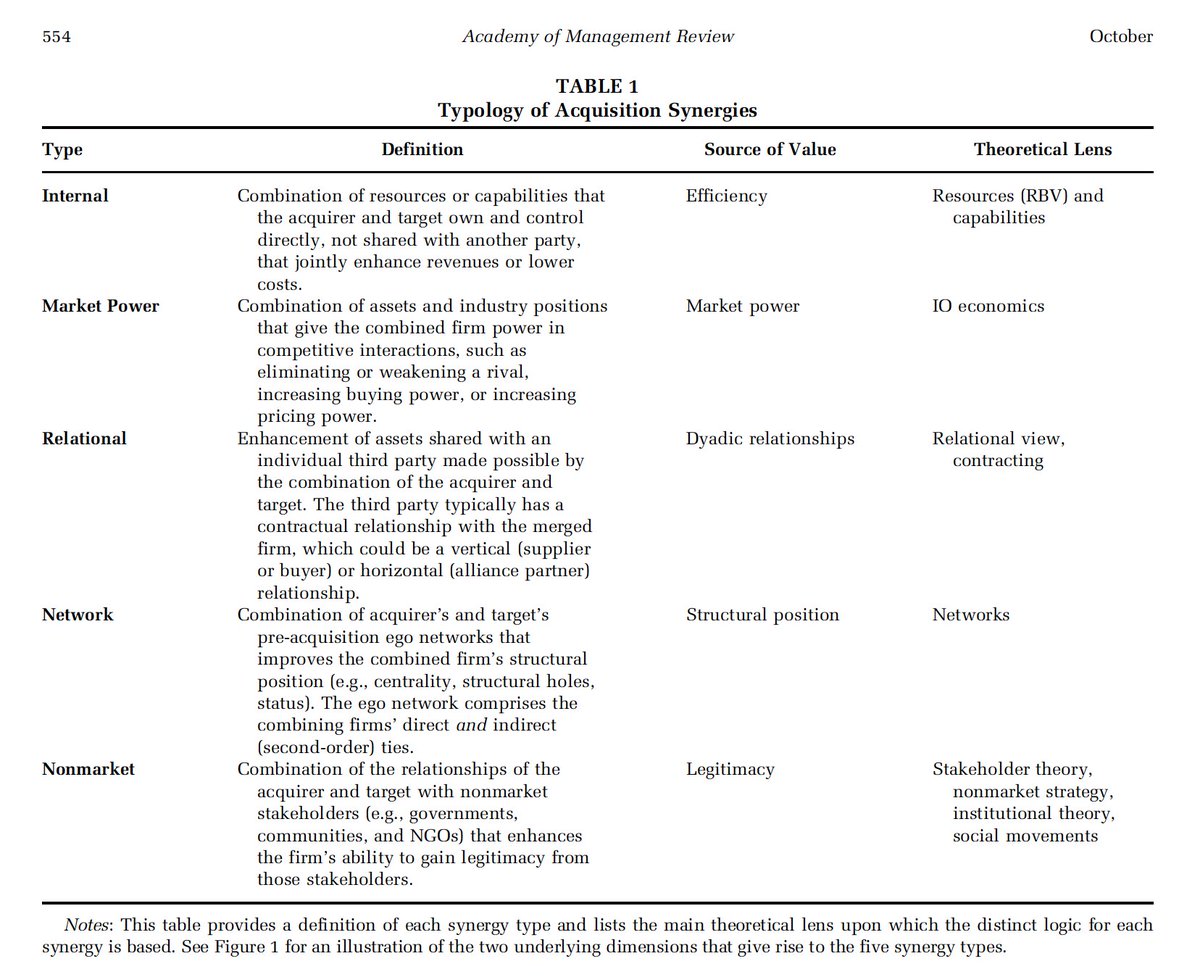

On the importance and categorization/valuation of synergies (long post):

Are synergies just a buzzword, or something important and meaningful for M&A and corporate development?

The answer is it's a bit of both. The term "synergies" had long been misused and abused and (oftentimes rightfully so) ridiculed.

At the end of the day, "synergies" are just a word, but in context, they are most useful as a conceptual device to think about mechanisms of value creation and capture in M&A and CorpDev, and if that's the intended use, they should be treated thoughtfully and methodically. But again, the word itself doesn't mean anything without elaborating specific "synergistic" mechanisms.

The key point is that synergies are important, because on the most basic level they elaborate value creation and capture when combining two businesses. For most transactions, the intent is to make 1 1 > 2. Synergies are value creation and capture mechanisms that explain how you intend to achieve that specific supra-additivity.

There are many different ways to think about specific types of synergies, but an important point first. What's often missing from many discussions of synergies is that value creation and capture are different. There is always value creation potential, and most assets have some intrinsic or potential value. But just because the value creation potential is there, does not mean that you would be able to create all of the value, or capture most of it. This should be reasonably intuitive. All owners and managers are not created equal and do not have the same capabilities and resources. You may project $ 100M in cost savings, but pragmatically you may only be able to achieve and capture $ 50M. You may value the firm currently trading at $100/share at $120/share because you project $20/share in some type of synergies, yet, even if the projection is correct, when there is a bidding contest, and you end up paying closer to $120/share, chances are that you are not capturing any value even if you succeed in achieving 100% of your projected value creation potential. This is where factors like your valuation, integration planning, specific capabilities become especially important.

Now, ahead to more specific types of synergies, how to think of them, and John Malone's career at TCI.

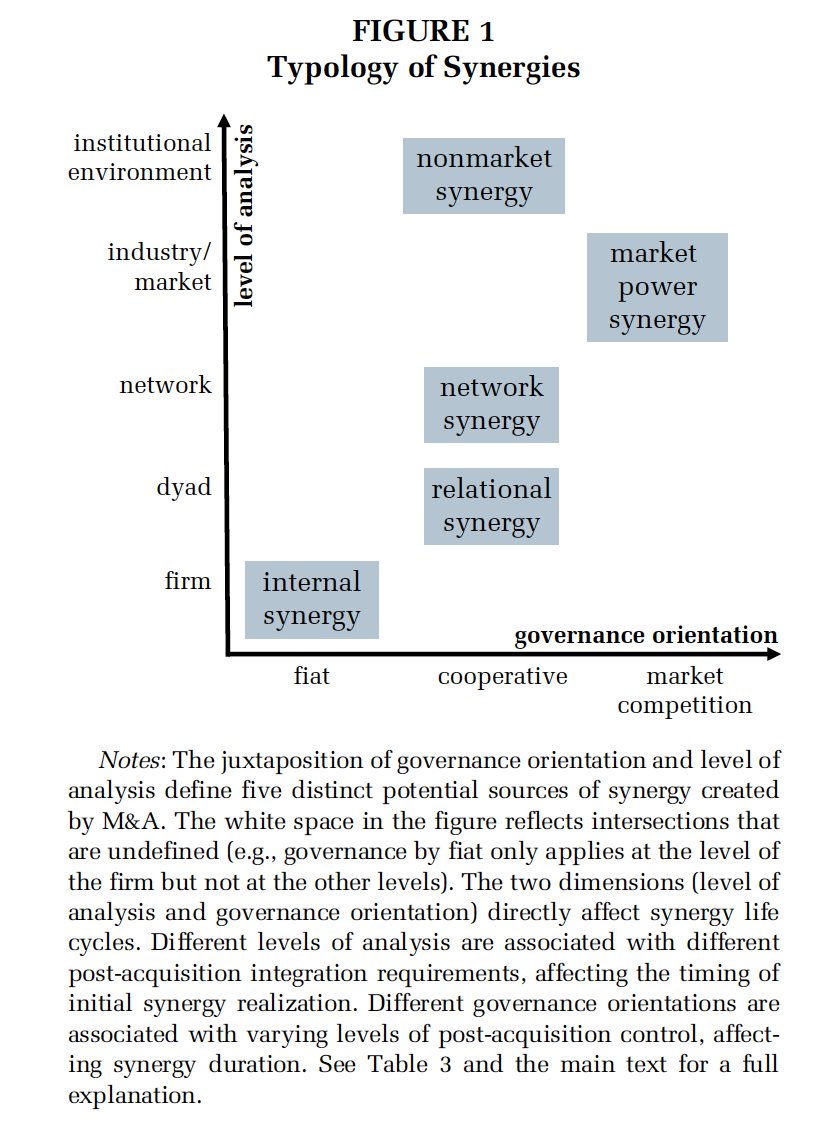

Most often, you hear about a couple of synergy categories - generally cost-based (bottom-line focused), revenue-based (topline-focused), and some type of financial/structural and other types of synergies. As the post cited below implies, you can also think about these in vertical/horizontal dimensions. More recently, researchers have been discussing additional categories of synergies, including network, relational, market power, stakeholder, and others. My brilliant colleagues Profs. Feldman and Hernandez have a wonderful paper discussing all of these (see tables below).

Malone's strategies provide a perfect context to discuss some of the categories and basics here:

1) Cost-based internal synergies: This is your bread and butter, workhorse synergies. Cost synergies could come from both economies of scale and scope and plain good competent ownership and management. Cost synergies are generally thought easier to achieve, with various studies estimating something like that on average, 50-80% of tthe predicted cost-based synergies are achieved. The key in understanding how realistic are these often comes down to evidence and experience - what's the evidence these are pragmatic and realistic, what are the assumptions and integration strategies necessary to achieve these? Perhaps just as, if not more importantly, does the acquirer have the experience in achieving these synergies?

Here Malone shines. As perhaps the best cable operator, especially in the 1970s-1990s, he created massive value at TCI by acquiring other cable operations and running them better. However, note that even here, he was extremely disciplined and cautious to make sure that the valuations did not subsume the value-creation potential, and refused to buy when the markets were frothy. Moreover, horizontal deals are where you are most likely to find and achieve cost-based savings, especially when you have the right capabilities and can focus on eliminating waste and redundancies.

2) Revenue-based internal synergies: These are often touted, rarely achieved. Generally, these require an increase in customers' willingness-to-pay, or some specific type of economies of scope. You should be very skeptical when large revenue synergies are projected, and all assumptions should be questioned. Studies ballpark that maybe 15-30% of these are ever achieved. Based on my own analysis of large public transactions, even execs are aware of the fickleness of revenue synergies and are less likely to use these as main motivations for deals today as opposed to 10-20 years ago.

Malone took full advantage of revenue-based synergies, but he did so in a counterintuitive way. In the vertical dimension, he relied primarily on contracting, partnerships, and minority investments. He secured access to valuable content not by integrating and acquiring majority control, but rather by securing access, investing in new content sources, and creating bundles that increased customer WTP. Again, this wasn't done through M&A, and these were not even conventional synergies as much as what we call "relational rents" - the equivalent of synergies that comes from partnerships and other similar arrangements with incomplete control.

3) Financial internal synergies: These are often even more ambiguous in 90% of the cases where they are mentioned, and they are often completely discounted by researchers, especially when the key mechanism is something like "risk management through diversification"

Yet in the case of Malone and TCI, I would argue that there were substantial synergies from his deals that fell into this bucket, and although there is some overlap with cost-based synergies, my interpretation is that there were siginificant financial and structural and tax-based synergies TCI realized because Malone was both the first to understand and create the financial and organizational structure that was optimal for cable businesses, and the best at managing the complex set of underlying mechanisms, from leverage to tax optimization, etc. Plugging acquired businesses into that structure allowed to create and capture more value.

Stepping back from internally-focused synergies, we can now look externally.

4 and 5) Relational and network synergies: We already touched on a great example of creating value through relational synergies in #2 above. Network synergies are similar, where combining two relational networks results in a stronger overall network. These figured somewhat in Malone's career but not as much, yet the strength of scale becomes important for the next type:

6) Market-power synergies: These are synergies from the ability to compete better, dictate higher prices, etc. There is still some debate here as to how often these exist and when they're achieved, but there are certainly some industrial contexts where market power is a critical consideration.

Market power (real or perceived) can be both a challenge and an opportunity. Once Malone and TCI achieved scale and prominence in the cable industry, he certainly wielded more market power, and was not afraid to use it in some contexts - e.g. negotiating with cable channels or municipalities. Yet, market power is not always easy to fully wield. Especially in the modern business context, there is a careful balance here since the regulators and politicians were always watching closely and threatening to interfere for decades, which brings me to the final set of interesting synergies here:

7) Non-market synergies: These are the synergies, also related to #4-6 above, that are related to being better able to manage external stakeholders that can range from unions to politicians to customers and so on.

Much like in other categories and examples above, Malone carefully managed the multiplex webs of stakeholder relationships, from becoming a de-facto industry leader who often shepherded and rallied and protected his industry competitors through the tough times, to someone who dedicated great resources to developing the ecosystem, to someone who hated the politics but still went to Washington every time he was called, to educating the investors and analysts as to why his stubborn approach to refusing to make profits and instead reinvesting and leveraging were optimal in the cable industry. My interpretation is that he intuitively managed a complex, multi-dimensional portfolio of both direct and indirect assets, options, etc. As silly as it is, he really was pretty good at playing 4D chess here.

So, in conclusion: there are many types of distinct but often related synergies and synergistic mechanisms that may allow you to create and then capture value from M&A and other corporate development activities. All have their challenges and opportunities, and each should be considered thoughtfully, carefully, and in context: what are the assumptions, what needs to happen? Some synergies we encounter are more common and conventional (cost and revenue), yet others, even while sounding ambiguous or exotic, may still help create and capture very real value. Synergies are also not limited to majority ownership, and relational rents provide an equivalent of synergies from partnerships and other hybrid arrangements. Moreover, there are occasionally opportunities for creative and innovative structures that may help increase value creation in one context, or help alleviate risks and uncertainties in others.

TL;DR on the very basics: Be thoughtful and structured when approaching synergies, and remember that 90% of the time, this is all that matters:

-Make sure that target price is lower than the sum of the target standalone value and pragmatic valuation of synergies

-Cost-based synergies tend to be more achievable especially if you have the right evidence, experience, assumptions (but could still be challenging)

-Revenue-based synergies are generally more pie-in-the-sky, get very skeptical when you see those mentioned, and be ready to run from deals that rely primarily on revenue-based improvements

-Most other synergies are likely not that important in most cases, especially if the base case isn't built on solid ground, and are more likely to be important on a higher level of managing the corporate portfolio and external relationships and stakeholders

May 6

John Malone series #3

Importance and Limitations of Synergies

Key Point: Realistic and calculable synergies (cost, tax, revenue) drive the value of acquisitions, but “soft” or intangible synergies should be treated skeptically.

Quote:

“Horizontal synergies… usually they're quite calculable… when you get more into things like: it'll help the brand or… intangibles… those are much harder…”

1

1

15

3,622

LOL HL has no purpose, their Rob Brown their corpdev guy is probably itching to do a deal.

2

199

Mar 17

Do you guys keep a keg of Red Bull in the office for your CorpDev team? How is this pace of acquisitions even possible?

Big fan of what you're building btw.

4

509

Mar 17

I think when you are speaking to a corpdev normie it’s now easier to say OpenClaw than it is to say modular agent harness 🤷🏻♂️

2

191

saw it, have not gotten any comms or answers from the @binance team about it.

my only xp with the @binance corpdev team has been them randomly demanding things from us with no notice, no consideration.

not sure whats behind their analysis, but the xp has not been positive one so far. maybe they think its 2017 still and CEXes are still the only game in town. they sure are acting like a rent-seeking intermedaiary.

2

2

520

Mar 10

meta's corpdev team doesnt even tell you why they're acquiring things, they just look at you like this

Mar 10

BREAKING: META acquires Moltbook, a social network built for AI agents.

15

1,348